Advanced Financial Accounting Assignment Report - HA3011, T1 2019

VerifiedAdded on 2022/10/31

|14

|3413

|494

Report

AI Summary

This report examines advanced financial accounting concepts, measurement issues, and qualitative characteristics within the framework of the IASB's conceptual framework. It begins with an introduction to the framework's emphasis on measurement basis for financial reporting, focusing on relevance and reliability. The report then delves into accounting concepts like business entity, going concern, money measurement, accrual, matching, and realization, illustrating their application through the analysis of Charter Hall Long WALE REIT's annual report. The second part discusses measurement issues, particularly the shift from historical cost to fair value, and the challenges associated with market volatility and subjectivity. It explores the mixed model approach, using the selected company's financial statements as an example. The final section analyzes the significance of relevance and faithful representation, two key qualitative principles of the conceptual framework, again with reference to examples from the company's annual report. The report highlights the importance of these principles in ensuring the quality of financial reporting for various stakeholders and concludes with a summary of the key findings and analysis.

1

HA3011

Advanced Financial Accounting

HA3011

Advanced Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Contents

Introduction......................................................................................................................................3

Part 1: Description on accounting concepts and application of same by the selected company.....3

Part 2: Discussion of Measurement Issues in Accounting in reference to Conceptual Framework

and by Using Examples from Selected Company...........................................................................6

Part 3: Analysis of Significance of Relevance and Faithful Representation Qualitative Principles

of Conceptual Framework with Reference to Examples from selected company...........................9

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

Contents

Introduction......................................................................................................................................3

Part 1: Description on accounting concepts and application of same by the selected company.....3

Part 2: Discussion of Measurement Issues in Accounting in reference to Conceptual Framework

and by Using Examples from Selected Company...........................................................................6

Part 3: Analysis of Significance of Relevance and Faithful Representation Qualitative Principles

of Conceptual Framework with Reference to Examples from selected company...........................9

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

3

Introduction

The conceptual framework is being developed by the IASB for enhancing the quality of

financial reports and ensuring that it is able to meet the varying interests of end-users in an

effective manner. As such, the framework has emphasized on using the measurement basis for

reporting the value of assets and liabilities that is able to improve the qualitative characteristics

of relevancy and reliability of financial reporting. The impact on relevance and reliability that are

the two fundamental qualitative characteristics of financial reporting provided by conceptual

framework must be considered before the selection of a measurement basis for valuing the assets

and liabilities. In this context, the report has examined the accounting concepts, measurement

issues and qualitative criteria of conceptual framework by analysis of the annual report of a

selected ASX listed entity of CHTR H LWR FP Units Stapled Securities.

Part 1: Description on accounting concepts and application of same by the selected

company

Accounting concepts is most important concepts that act as the basic assumptions,

accounting principles and rules while performing the recording of business transactions and

drafting the financial statements of the company. The complete accounting process is based on

the accounting concepts and it is also mandatory for the business entities to follow the

accounting concepts. All the major accounting concepts have been discussed below and their

practical applications by Charter Hall Long WALE REIT have also been provided.

Business Entity Concept

The main objective of including this accounting concept is to make the business process

separate from the individual (Owner) so that it helps to perform proper accounting and allow

entity to have separate name, identity and presence. In simple words, this accounting concept

provides that business entity and business owners are two distinct persons and have distinct

identities. For example, if there is contract made with business entity than it implies that such

contract is binding on entity not on the business owner (Damodaran, 2011).

Introduction

The conceptual framework is being developed by the IASB for enhancing the quality of

financial reports and ensuring that it is able to meet the varying interests of end-users in an

effective manner. As such, the framework has emphasized on using the measurement basis for

reporting the value of assets and liabilities that is able to improve the qualitative characteristics

of relevancy and reliability of financial reporting. The impact on relevance and reliability that are

the two fundamental qualitative characteristics of financial reporting provided by conceptual

framework must be considered before the selection of a measurement basis for valuing the assets

and liabilities. In this context, the report has examined the accounting concepts, measurement

issues and qualitative criteria of conceptual framework by analysis of the annual report of a

selected ASX listed entity of CHTR H LWR FP Units Stapled Securities.

Part 1: Description on accounting concepts and application of same by the selected

company

Accounting concepts is most important concepts that act as the basic assumptions,

accounting principles and rules while performing the recording of business transactions and

drafting the financial statements of the company. The complete accounting process is based on

the accounting concepts and it is also mandatory for the business entities to follow the

accounting concepts. All the major accounting concepts have been discussed below and their

practical applications by Charter Hall Long WALE REIT have also been provided.

Business Entity Concept

The main objective of including this accounting concept is to make the business process

separate from the individual (Owner) so that it helps to perform proper accounting and allow

entity to have separate name, identity and presence. In simple words, this accounting concept

provides that business entity and business owners are two distinct persons and have distinct

identities. For example, if there is contract made with business entity than it implies that such

contract is binding on entity not on the business owner (Damodaran, 2011).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

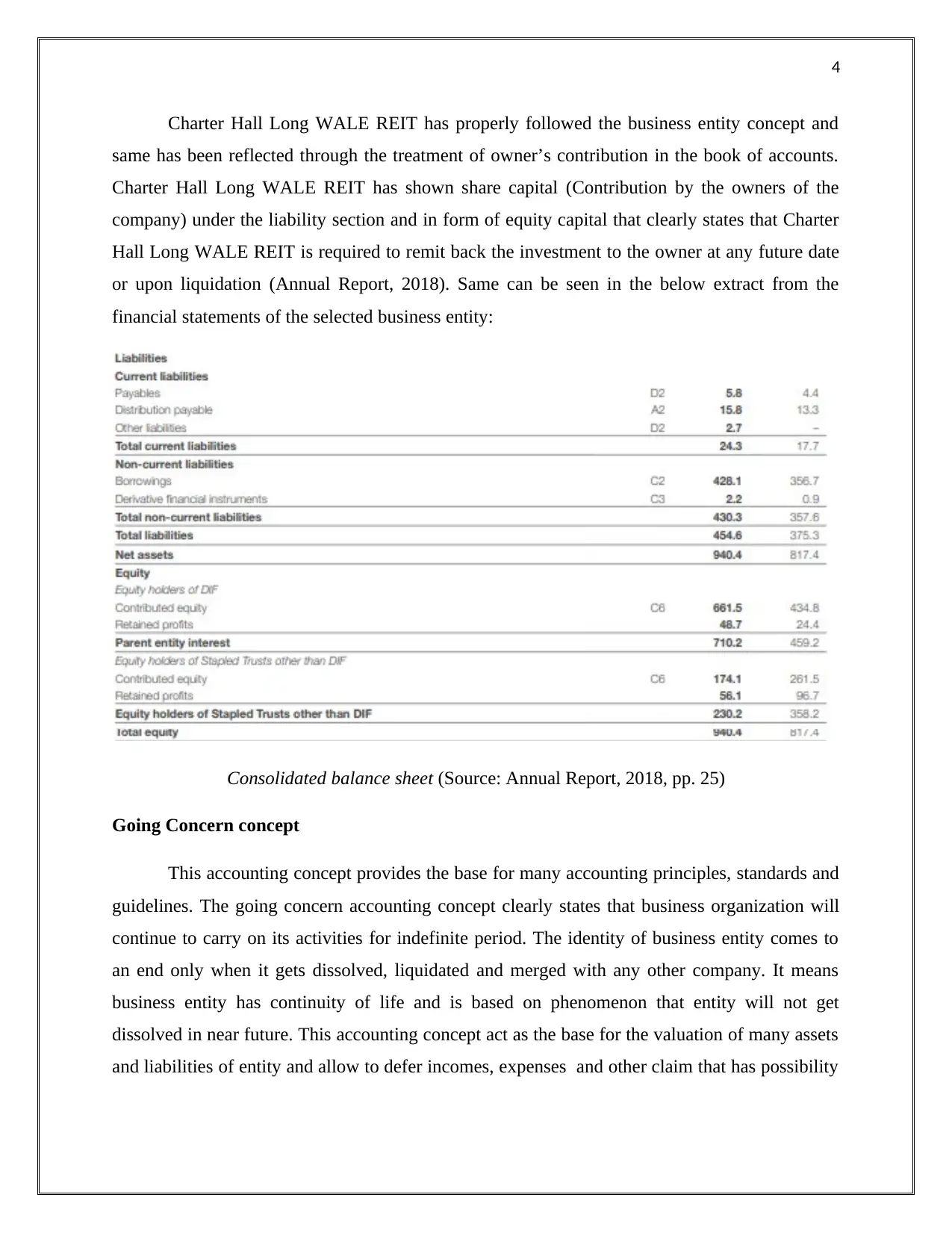

Charter Hall Long WALE REIT has properly followed the business entity concept and

same has been reflected through the treatment of owner’s contribution in the book of accounts.

Charter Hall Long WALE REIT has shown share capital (Contribution by the owners of the

company) under the liability section and in form of equity capital that clearly states that Charter

Hall Long WALE REIT is required to remit back the investment to the owner at any future date

or upon liquidation (Annual Report, 2018). Same can be seen in the below extract from the

financial statements of the selected business entity:

Consolidated balance sheet (Source: Annual Report, 2018, pp. 25)

Going Concern concept

This accounting concept provides the base for many accounting principles, standards and

guidelines. The going concern accounting concept clearly states that business organization will

continue to carry on its activities for indefinite period. The identity of business entity comes to

an end only when it gets dissolved, liquidated and merged with any other company. It means

business entity has continuity of life and is based on phenomenon that entity will not get

dissolved in near future. This accounting concept act as the base for the valuation of many assets

and liabilities of entity and allow to defer incomes, expenses and other claim that has possibility

Charter Hall Long WALE REIT has properly followed the business entity concept and

same has been reflected through the treatment of owner’s contribution in the book of accounts.

Charter Hall Long WALE REIT has shown share capital (Contribution by the owners of the

company) under the liability section and in form of equity capital that clearly states that Charter

Hall Long WALE REIT is required to remit back the investment to the owner at any future date

or upon liquidation (Annual Report, 2018). Same can be seen in the below extract from the

financial statements of the selected business entity:

Consolidated balance sheet (Source: Annual Report, 2018, pp. 25)

Going Concern concept

This accounting concept provides the base for many accounting principles, standards and

guidelines. The going concern accounting concept clearly states that business organization will

continue to carry on its activities for indefinite period. The identity of business entity comes to

an end only when it gets dissolved, liquidated and merged with any other company. It means

business entity has continuity of life and is based on phenomenon that entity will not get

dissolved in near future. This accounting concept act as the base for the valuation of many assets

and liabilities of entity and allow to defer incomes, expenses and other claim that has possibility

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

that it will arise but they cannot be recognised as to maintain the economic interest of the

company and business owner as well (Brigham and Michael, 2013).

The application of going concern by Charter Hall Long WALE REIT can be seen in

many accounting transactions such as depreciation on assets, treatment of prepaid and

outstanding expenses and many others. In case this accounting is not available than it will all the

expenses made on fixed assets will be treated as expenses and will be claimed in same year of

purchase. It will adversely impact the financial position of the company and there will great

threat on the existence of company in future (Annual Report, 2018).

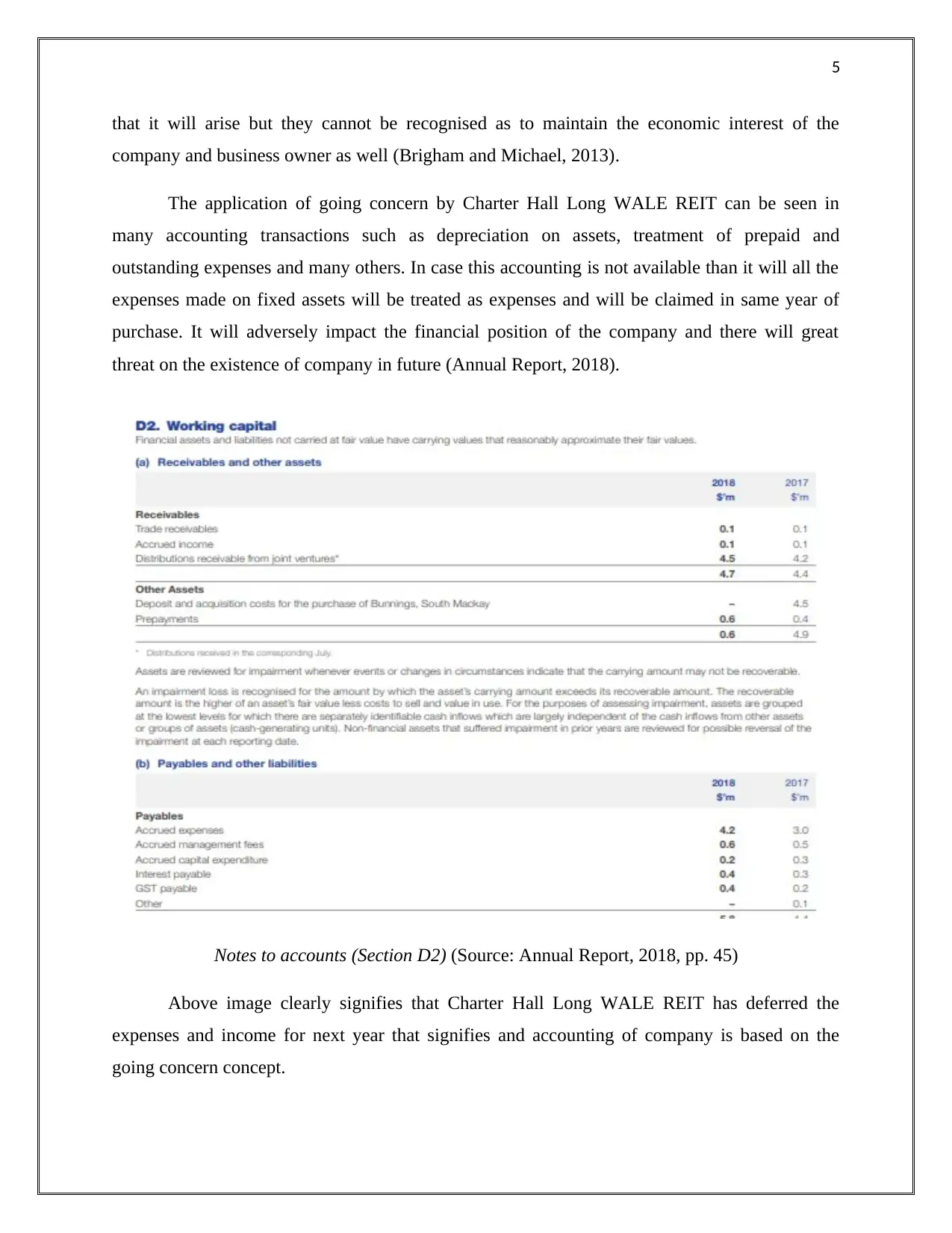

Notes to accounts (Section D2) (Source: Annual Report, 2018, pp. 45)

Above image clearly signifies that Charter Hall Long WALE REIT has deferred the

expenses and income for next year that signifies and accounting of company is based on the

going concern concept.

that it will arise but they cannot be recognised as to maintain the economic interest of the

company and business owner as well (Brigham and Michael, 2013).

The application of going concern by Charter Hall Long WALE REIT can be seen in

many accounting transactions such as depreciation on assets, treatment of prepaid and

outstanding expenses and many others. In case this accounting is not available than it will all the

expenses made on fixed assets will be treated as expenses and will be claimed in same year of

purchase. It will adversely impact the financial position of the company and there will great

threat on the existence of company in future (Annual Report, 2018).

Notes to accounts (Section D2) (Source: Annual Report, 2018, pp. 45)

Above image clearly signifies that Charter Hall Long WALE REIT has deferred the

expenses and income for next year that signifies and accounting of company is based on the

going concern concept.

6

Money measurement concept

This accounting concept provides that all the accounting business transactions must be

expressed in terms of money and should be reflected in terms of currency of country (Davies and

Crawford, 2011).

Charter Hall Long WALE REIT has reported all its business transactions in terms of

money and represented them in financial statements as AUD $ Millions. It means company is

following the money measurement concept properly (Annual Report, 2018).

Accrual Concept

This accounting concept is very important and it is mandatory for all the business entities.

Accrual accounting concept is very important as it helps to treat the income and expenses in

accounting period to which it relates. It means revenue are being recognised when there is

reasonable assurance that money will be receivable and expenses are recognized when they

become payable. So it can be said that cash payment for expenses and cash received for revenue

has no relation to account for the income and expenses for the relevant period. Accrual concept

gives rise to assets and liabilities with regards to income and expenses such as outstanding

expenses, prepaid expense, unearned income and accrued revenue (Wolk, Dodd and Rozycki,

2016).

Charter Hall Long WALE REIT has based its accounting on accrual basis and shown all

the outstanding expenses, accrued incomes, and prepaid expenses separately in balance sheet

(Annual Report, 2018).

Matching Concept

Matching accounting concept provides that all the incomes and expenses incurred to earn

the particular revenue must be taken to same accounting period to which such revenue is being

recognized. This accounting concept is framed to support the accrual accounting concept and

also to take expenses and revenue of one period at one place (Moles and Kidwekk, 2011).

Realization Concept

Money measurement concept

This accounting concept provides that all the accounting business transactions must be

expressed in terms of money and should be reflected in terms of currency of country (Davies and

Crawford, 2011).

Charter Hall Long WALE REIT has reported all its business transactions in terms of

money and represented them in financial statements as AUD $ Millions. It means company is

following the money measurement concept properly (Annual Report, 2018).

Accrual Concept

This accounting concept is very important and it is mandatory for all the business entities.

Accrual accounting concept is very important as it helps to treat the income and expenses in

accounting period to which it relates. It means revenue are being recognised when there is

reasonable assurance that money will be receivable and expenses are recognized when they

become payable. So it can be said that cash payment for expenses and cash received for revenue

has no relation to account for the income and expenses for the relevant period. Accrual concept

gives rise to assets and liabilities with regards to income and expenses such as outstanding

expenses, prepaid expense, unearned income and accrued revenue (Wolk, Dodd and Rozycki,

2016).

Charter Hall Long WALE REIT has based its accounting on accrual basis and shown all

the outstanding expenses, accrued incomes, and prepaid expenses separately in balance sheet

(Annual Report, 2018).

Matching Concept

Matching accounting concept provides that all the incomes and expenses incurred to earn

the particular revenue must be taken to same accounting period to which such revenue is being

recognized. This accounting concept is framed to support the accrual accounting concept and

also to take expenses and revenue of one period at one place (Moles and Kidwekk, 2011).

Realization Concept

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

This accounting concept is framed to support many of the accounting standards and all

the accrual basis of accounting. According to this accounting concept revenue should be

recognised by the business entity when there is reasonable assurance that economic benefit will

flow to the company in near future and realization of revenue provide a legal right to the entity to

receive the money (Wahlen, Baginski and Bradshaw, 2017).

All the revenue recognised in the income statement of Charter Hall Long WALE REIT

has reasonable assurance that economic benefits will flow to company in near future or they have

been already been received (Annual Report, 2018).

Part 2: Discussion of Measurement Issues in Accounting in reference to Conceptual

Framework and by Using Examples from Selected Company

There has been the use of single method of measurement, that is, historical cost for

measuring the value of assets and liabilities of an entity. However, there has been a gradual shift

from using traditional basis of measurement that is historical costing towards the use of fair

value method of measurement accounting. This has been largely due to limitations associated

with historical cost of not able to depict the actual value of financial items of income statement

such as profit and expenses. This is because the value is based on past evaluations and does not

reflect the value as per the current market conditions and therefore not very relevant. This is

leading to cause widespread adoption of fair value model of accounting measurement which

reflects the value of financial items as per the current market prices (IFRS, 2017).

Thus, it is able to overcome the limitations associated with historical method of

accounting by recognizing the financial items at their current price and thus able to depict the

actual value. However, the major issue that is faced by businesses towards the use of fair value

approach of measurement is that it is not able to provide reliable outcomes under the conditions

of market volatility. Also, there is lot of subjectivity associated with the use of this method as the

value is obtained on the basis of manager’s judgments and estimations that can have an impact

on the reliability of the financial outcomes obtained (International Accounting Standards Board,

2016). Therefore, the standard-setters are presently facing the issue of determining an accurate

model of measurement that is able to reflect both reliable and relevant value as per the qualitative

objective of financial reporting provided by the conceptual framework. This has resulted in

This accounting concept is framed to support many of the accounting standards and all

the accrual basis of accounting. According to this accounting concept revenue should be

recognised by the business entity when there is reasonable assurance that economic benefit will

flow to the company in near future and realization of revenue provide a legal right to the entity to

receive the money (Wahlen, Baginski and Bradshaw, 2017).

All the revenue recognised in the income statement of Charter Hall Long WALE REIT

has reasonable assurance that economic benefits will flow to company in near future or they have

been already been received (Annual Report, 2018).

Part 2: Discussion of Measurement Issues in Accounting in reference to Conceptual

Framework and by Using Examples from Selected Company

There has been the use of single method of measurement, that is, historical cost for

measuring the value of assets and liabilities of an entity. However, there has been a gradual shift

from using traditional basis of measurement that is historical costing towards the use of fair

value method of measurement accounting. This has been largely due to limitations associated

with historical cost of not able to depict the actual value of financial items of income statement

such as profit and expenses. This is because the value is based on past evaluations and does not

reflect the value as per the current market conditions and therefore not very relevant. This is

leading to cause widespread adoption of fair value model of accounting measurement which

reflects the value of financial items as per the current market prices (IFRS, 2017).

Thus, it is able to overcome the limitations associated with historical method of

accounting by recognizing the financial items at their current price and thus able to depict the

actual value. However, the major issue that is faced by businesses towards the use of fair value

approach of measurement is that it is not able to provide reliable outcomes under the conditions

of market volatility. Also, there is lot of subjectivity associated with the use of this method as the

value is obtained on the basis of manager’s judgments and estimations that can have an impact

on the reliability of the financial outcomes obtained (International Accounting Standards Board,

2016). Therefore, the standard-setters are presently facing the issue of determining an accurate

model of measurement that is able to reflect both reliable and relevant value as per the qualitative

objective of financial reporting provided by the conceptual framework. This has resulted in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

developing a mixed model of accounting provided by accounting standard-setters to be used by

businesses for overcoming the issue of measurement in accounting.

The mixed model of valuation has regarded that a reporting entity need to adopt the use

of both historical cost and fair valuation approach to recognize the value of the financial items

whose value cannot be accurately determined due to absence of an active market. As such, the

business entities are reporting the value of their fixed assets on cost basis due to absence of their

active market (Kythreotis, 2014). Also, it would be able to provide a reliable value of fixed

assets that is not possible to provide by the use of fair valuation approach as it involves a lot of

subjectivity which can make the value of fixed assets non-reliable and thus negatively impacting

the interests of investors. On the other hand, the fair valuation approach of measurement is used

for measuring the value of financial items having the presence of an active market such as

financial assets and liabilities. The use of this approach make the value of financial items of

income statement more relevant and supporting the future investment decisions of investors by

providing an estimate of future cash flows of an entity. However, the acceptance of this approach

by the preparers of financial reports has lead to the problem of providing inconsistent and non-

comparable financial information (ICAEW, 2016).

This is because different business entities tend to adopt the use of different methods of

measurement for reporting the value of their financial items on the basis of nature of their

operations and the type of industry. This generally results in making the financial information

obtained with the use of mixed model of valuation to be largely inconsistent and not trustworthy

for to be used in economic decision-making. The issue of measurement in financial reporting can

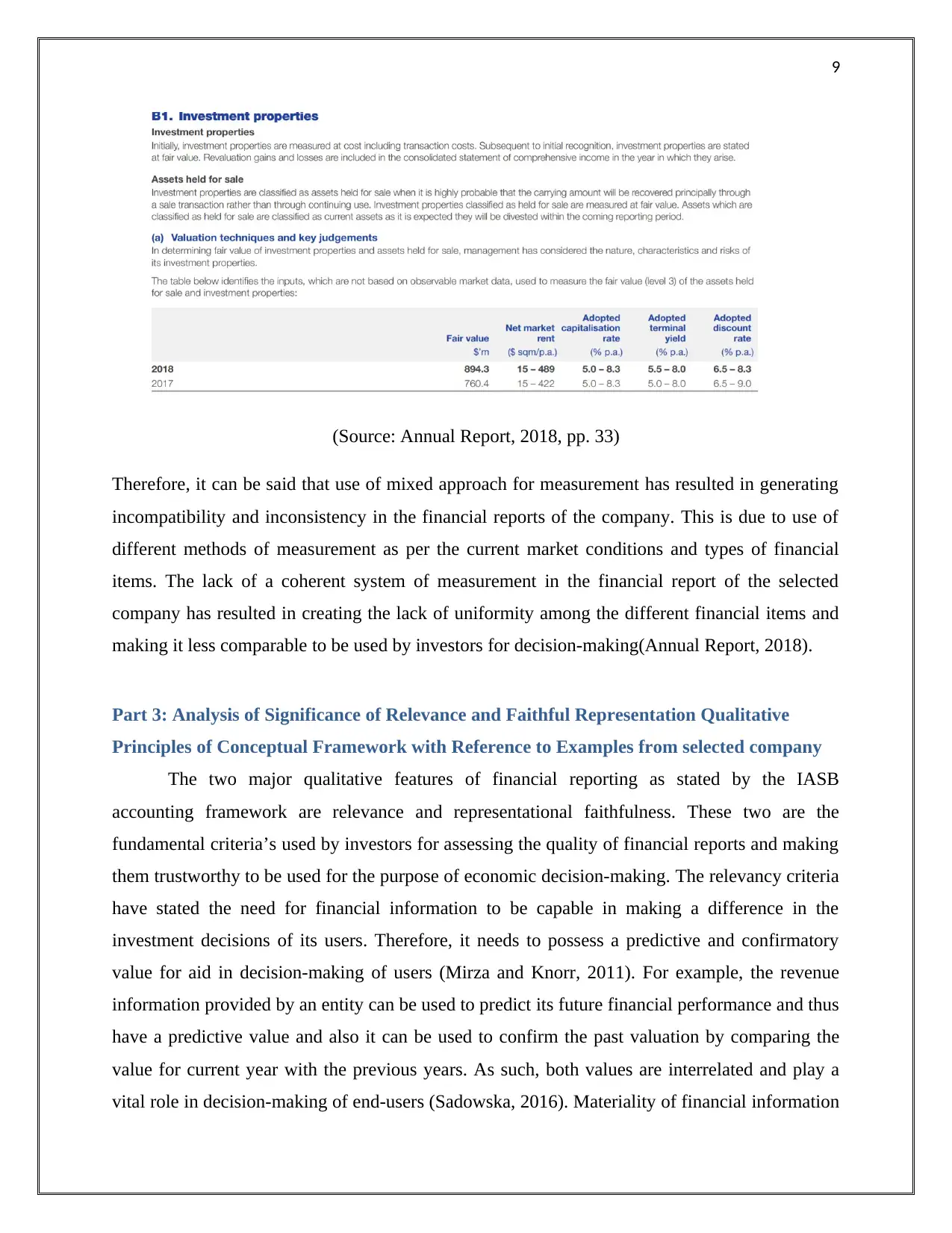

be demonstrated through the examples from the annual report of CHTR H LWR FP Units

Stapled Securities. The company has adopted the use of nixed model of measurement for

recognition and measuring the value of its different financial items. The consolidated financial

statements have been developed with the use of historical cost basis while derivatives, financial

assets, assets held for sale and investment properties have been recognized at fair value. The key

judgments and estimates have been used in determination of the fair value of different financial

items as depicted below:

developing a mixed model of accounting provided by accounting standard-setters to be used by

businesses for overcoming the issue of measurement in accounting.

The mixed model of valuation has regarded that a reporting entity need to adopt the use

of both historical cost and fair valuation approach to recognize the value of the financial items

whose value cannot be accurately determined due to absence of an active market. As such, the

business entities are reporting the value of their fixed assets on cost basis due to absence of their

active market (Kythreotis, 2014). Also, it would be able to provide a reliable value of fixed

assets that is not possible to provide by the use of fair valuation approach as it involves a lot of

subjectivity which can make the value of fixed assets non-reliable and thus negatively impacting

the interests of investors. On the other hand, the fair valuation approach of measurement is used

for measuring the value of financial items having the presence of an active market such as

financial assets and liabilities. The use of this approach make the value of financial items of

income statement more relevant and supporting the future investment decisions of investors by

providing an estimate of future cash flows of an entity. However, the acceptance of this approach

by the preparers of financial reports has lead to the problem of providing inconsistent and non-

comparable financial information (ICAEW, 2016).

This is because different business entities tend to adopt the use of different methods of

measurement for reporting the value of their financial items on the basis of nature of their

operations and the type of industry. This generally results in making the financial information

obtained with the use of mixed model of valuation to be largely inconsistent and not trustworthy

for to be used in economic decision-making. The issue of measurement in financial reporting can

be demonstrated through the examples from the annual report of CHTR H LWR FP Units

Stapled Securities. The company has adopted the use of nixed model of measurement for

recognition and measuring the value of its different financial items. The consolidated financial

statements have been developed with the use of historical cost basis while derivatives, financial

assets, assets held for sale and investment properties have been recognized at fair value. The key

judgments and estimates have been used in determination of the fair value of different financial

items as depicted below:

9

(Source: Annual Report, 2018, pp. 33)

Therefore, it can be said that use of mixed approach for measurement has resulted in generating

incompatibility and inconsistency in the financial reports of the company. This is due to use of

different methods of measurement as per the current market conditions and types of financial

items. The lack of a coherent system of measurement in the financial report of the selected

company has resulted in creating the lack of uniformity among the different financial items and

making it less comparable to be used by investors for decision-making(Annual Report, 2018).

Part 3: Analysis of Significance of Relevance and Faithful Representation Qualitative

Principles of Conceptual Framework with Reference to Examples from selected company

The two major qualitative features of financial reporting as stated by the IASB

accounting framework are relevance and representational faithfulness. These two are the

fundamental criteria’s used by investors for assessing the quality of financial reports and making

them trustworthy to be used for the purpose of economic decision-making. The relevancy criteria

have stated the need for financial information to be capable in making a difference in the

investment decisions of its users. Therefore, it needs to possess a predictive and confirmatory

value for aid in decision-making of users (Mirza and Knorr, 2011). For example, the revenue

information provided by an entity can be used to predict its future financial performance and thus

have a predictive value and also it can be used to confirm the past valuation by comparing the

value for current year with the previous years. As such, both values are interrelated and play a

vital role in decision-making of end-users (Sadowska, 2016). Materiality of financial information

(Source: Annual Report, 2018, pp. 33)

Therefore, it can be said that use of mixed approach for measurement has resulted in generating

incompatibility and inconsistency in the financial reports of the company. This is due to use of

different methods of measurement as per the current market conditions and types of financial

items. The lack of a coherent system of measurement in the financial report of the selected

company has resulted in creating the lack of uniformity among the different financial items and

making it less comparable to be used by investors for decision-making(Annual Report, 2018).

Part 3: Analysis of Significance of Relevance and Faithful Representation Qualitative

Principles of Conceptual Framework with Reference to Examples from selected company

The two major qualitative features of financial reporting as stated by the IASB

accounting framework are relevance and representational faithfulness. These two are the

fundamental criteria’s used by investors for assessing the quality of financial reports and making

them trustworthy to be used for the purpose of economic decision-making. The relevancy criteria

have stated the need for financial information to be capable in making a difference in the

investment decisions of its users. Therefore, it needs to possess a predictive and confirmatory

value for aid in decision-making of users (Mirza and Knorr, 2011). For example, the revenue

information provided by an entity can be used to predict its future financial performance and thus

have a predictive value and also it can be used to confirm the past valuation by comparing the

value for current year with the previous years. As such, both values are interrelated and play a

vital role in decision-making of end-users (Sadowska, 2016). Materiality of financial information

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

is also closely related to its relevance which means that it should be materialistic correct to

enhance correct decision-making. On the other hand, representational faithfulness is another

major criterion that governs the quality of financial reports. It has stated that a financial depiction

should be complete, neutral and also free from any type of error. This means that financial

information should provide explanation of the facts and figures related with a financial item and

also should not favor any particular group of users. There should be not the presence of any error

in describing an accounting phenomenon and should be accurate in all aspects (Needles, Powers

and Crosson, 2013).

The business entities as per these qualitative criteria need to make their financial

information both relevant and providing faithful depiction. However, a major issue that is faced

by them in this aspect is that high reliability any significantly reduces the relevance of financial

statements whereas higher relevancy might have an effect on faithful presentation of

information. This is because higher relevancy means the use of fair valuation approach which is

helpful in making an estimate of the future cash flows of an entity. This results in making use of

subjective estimates and assumptions which can result in occurrence of error and significantly

reducing the faithful presentation of information (Horton and Serafeim, 2010).

On the other hand, making financial information more reliable, complete and error-free

requires the use of measurement method such as historical basis that provides an accurate value

of financial items without the use of any type of estimates and assumptions. However, it will

result in negatively impacting the relevancy criteria of financial reporting by making as it would

not able to predict the future earning potential of a company (Riedl, 2010). The same can be

depicted by the use of examples from the annual report of the selected company. The company

has emphasized on achieving a balance between the two characteristics of financial reporting of

the information. It ahs provided relevant financial information through development and

presentation of income statement which includes depiction of values of revenue and expenses

that helps in making forecast about the future growth prospects as depicted below:

is also closely related to its relevance which means that it should be materialistic correct to

enhance correct decision-making. On the other hand, representational faithfulness is another

major criterion that governs the quality of financial reports. It has stated that a financial depiction

should be complete, neutral and also free from any type of error. This means that financial

information should provide explanation of the facts and figures related with a financial item and

also should not favor any particular group of users. There should be not the presence of any error

in describing an accounting phenomenon and should be accurate in all aspects (Needles, Powers

and Crosson, 2013).

The business entities as per these qualitative criteria need to make their financial

information both relevant and providing faithful depiction. However, a major issue that is faced

by them in this aspect is that high reliability any significantly reduces the relevance of financial

statements whereas higher relevancy might have an effect on faithful presentation of

information. This is because higher relevancy means the use of fair valuation approach which is

helpful in making an estimate of the future cash flows of an entity. This results in making use of

subjective estimates and assumptions which can result in occurrence of error and significantly

reducing the faithful presentation of information (Horton and Serafeim, 2010).

On the other hand, making financial information more reliable, complete and error-free

requires the use of measurement method such as historical basis that provides an accurate value

of financial items without the use of any type of estimates and assumptions. However, it will

result in negatively impacting the relevancy criteria of financial reporting by making as it would

not able to predict the future earning potential of a company (Riedl, 2010). The same can be

depicted by the use of examples from the annual report of the selected company. The company

has emphasized on achieving a balance between the two characteristics of financial reporting of

the information. It ahs provided relevant financial information through development and

presentation of income statement which includes depiction of values of revenue and expenses

that helps in making forecast about the future growth prospects as depicted below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

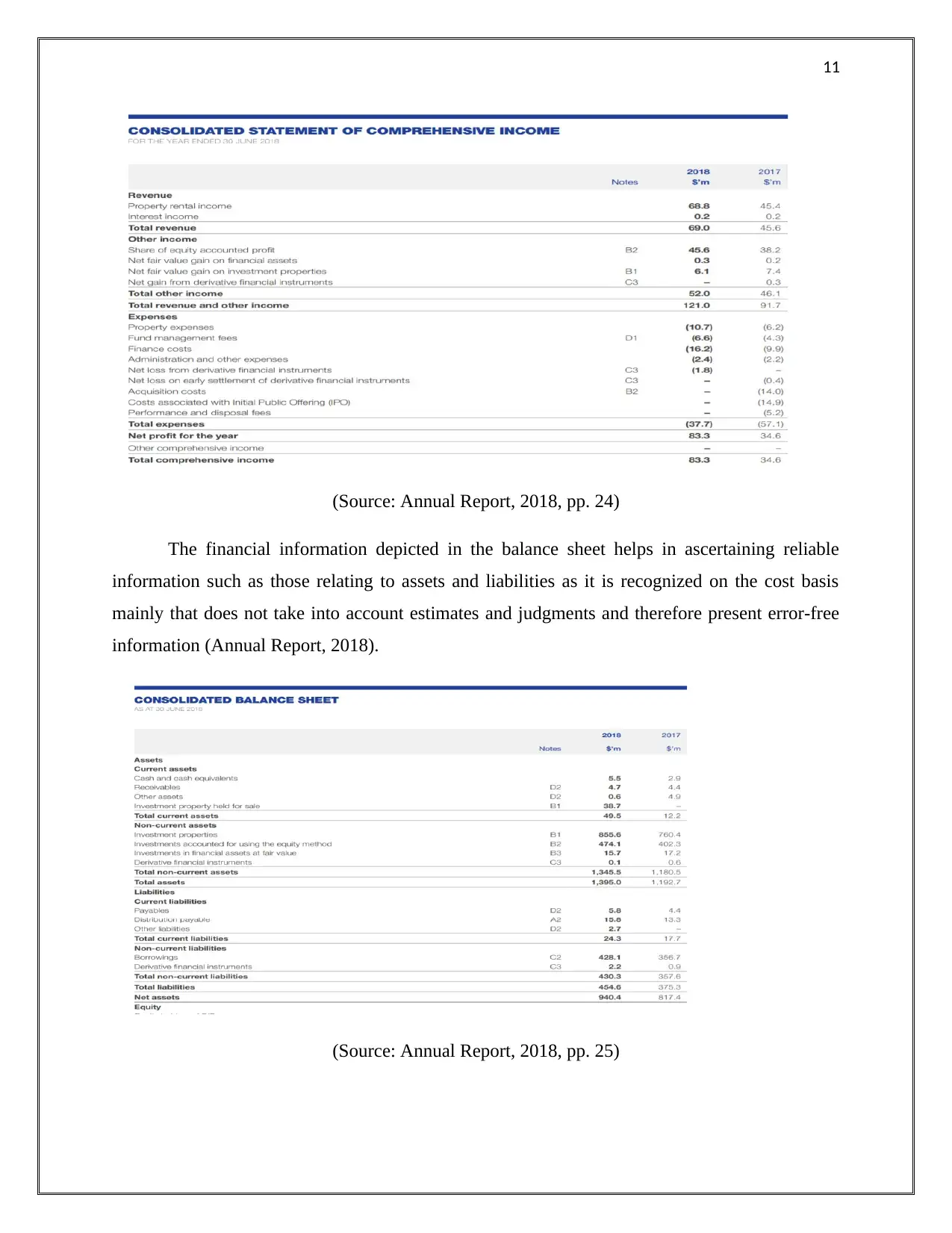

(Source: Annual Report, 2018, pp. 24)

The financial information depicted in the balance sheet helps in ascertaining reliable

information such as those relating to assets and liabilities as it is recognized on the cost basis

mainly that does not take into account estimates and judgments and therefore present error-free

information (Annual Report, 2018).

(Source: Annual Report, 2018, pp. 25)

(Source: Annual Report, 2018, pp. 24)

The financial information depicted in the balance sheet helps in ascertaining reliable

information such as those relating to assets and liabilities as it is recognized on the cost basis

mainly that does not take into account estimates and judgments and therefore present error-free

information (Annual Report, 2018).

(Source: Annual Report, 2018, pp. 25)

12

Conclusion

It can be said on the basis of overall discussion held that accounting concepts need to be

applied by business entities for reporting their financial information in a fair manner. Also, the

businesses are currently facing the issue of using a coherent system of measurement and

achieving a balance between the qualitative characteristics of conceptual framework. The

businesses such as CHTR H LWR FP Units Stapled Securities are adopting the use of mixed

model of measurement for resolving the issue of measurement. Also, they are trying to attain

congruence between the two characteristics of financial reporting by making the financial statists

in a format so that it depicts both reliable and faithful information.

Conclusion

It can be said on the basis of overall discussion held that accounting concepts need to be

applied by business entities for reporting their financial information in a fair manner. Also, the

businesses are currently facing the issue of using a coherent system of measurement and

achieving a balance between the qualitative characteristics of conceptual framework. The

businesses such as CHTR H LWR FP Units Stapled Securities are adopting the use of mixed

model of measurement for resolving the issue of measurement. Also, they are trying to attain

congruence between the two characteristics of financial reporting by making the financial statists

in a format so that it depicts both reliable and faithful information.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.