Advanced Financial Accounting: AASB 16 and Company Analysis Report

VerifiedAdded on 2022/10/18

|10

|3038

|17

Report

AI Summary

This report analyzes advanced financial accounting principles, focusing on the application of accounting concepts and the impact of AASB 16 (Leases) on a selected company, Xero Limited, listed on the ASX. The report details the accounting concepts used, including historical cost convention and the application of NZ GAAP and IFRS. It explores the changes introduced by AASB 16, replacing NZ IAS 17, and their implications on financial reporting, specifically the shift from operating to finance lease accounting. The report also summarizes the key disclosures made by the company regarding its accounting for leases, including the transition to AASB 16. The analysis includes the effects on the company's financial statements, the impact on key metrics like EBITDA, and the importance of proactive management of potential financial reporting anomalies and bank covenants. The report also highlights the critical accounting estimates and the company's approach to deferred taxes, providing a comprehensive overview of the company's financial reporting practices.

ADVANCED FINANCIAL ACCOUNTING 1

ADVANCED

FINANCIAL

ACCOUNTING

ADVANCED

FINANCIAL

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED FINANCIAL ACCOUNTING 2

Contents

Introduction:...............................................................................................................................3

Accounting concepts used:.........................................................................................................3

Changes in AASB 116:..............................................................................................................5

Key disclosures:.........................................................................................................................6

Conclusion:................................................................................................................................7

References..................................................................................................................................8

Contents

Introduction:...............................................................................................................................3

Accounting concepts used:.........................................................................................................3

Changes in AASB 116:..............................................................................................................5

Key disclosures:.........................................................................................................................6

Conclusion:................................................................................................................................7

References..................................................................................................................................8

ADVANCED FINANCIAL ACCOUNTING 3

Introduction:

The company chosen for review is Xero Limited which is the company registered under the

New Zealand companies Act 1993 and is also listed on the ASX. The company follows the

FMC reporting under Part 7 of the financial Markets Conduct Act 2013. The final accounts of

the company along with that of its subsidiaries have been prepared in accordance with the

provisions of the Part 7 of the financial Markets Conduct Act 2013 along with the different

listing rules laid down by ASX. This report aims at discussing the various accounting

concepts that have been followed when preparing the final accounts and also, throws light o

the requirements of the new leasing accounting standard.

Accounting concepts used:

The company has prepared its final accounts for the year ended March 31, 2018.

The following are the accounting concepts that were used:

In terms of basis for accounting, the final accounts of the company have bene prepared using

the provisions and the principals of generally accepted Accounting Practices in New Zealand.

The group is the profit entity for the purposes of complying with the provisions of NZ

GAAP. The consolidated final accounts of the company have been prepared under the

provisions and in the light of the International Financial Reporting Standards along with such

other accounting standards of the country and the authoritative notices that are applicable on

all of the companies. The final accounts have been prepared using the historical cost

convention of the group. The functional currency being used by the company is the New

Zealand $. In respect of the changes in the policies of accounting for the company and the

disclosures, the policies in respect of accounting and the disclosures are very much the same

as were followed during the previous year. But there is some of the information and the fact

that have to be reclassified in order to bring them with the current period amounts.

There are some of the standards and the interpretations that are not effective on the group but

are relevant to the group. These include the following:

NZ IFRS 9: this is the standard on accounting which relates with the financial instruments.

This standard replaces NZ IAS 139 which deals with the financial instruments, recognition

and measurement and the addressing of the classification, measurement and the recognition

of the assets and the liabilities of the company. This new standard on accounting is effective

from January 31, 2019. This standard on accounting is the one which introduces the expected

Introduction:

The company chosen for review is Xero Limited which is the company registered under the

New Zealand companies Act 1993 and is also listed on the ASX. The company follows the

FMC reporting under Part 7 of the financial Markets Conduct Act 2013. The final accounts of

the company along with that of its subsidiaries have been prepared in accordance with the

provisions of the Part 7 of the financial Markets Conduct Act 2013 along with the different

listing rules laid down by ASX. This report aims at discussing the various accounting

concepts that have been followed when preparing the final accounts and also, throws light o

the requirements of the new leasing accounting standard.

Accounting concepts used:

The company has prepared its final accounts for the year ended March 31, 2018.

The following are the accounting concepts that were used:

In terms of basis for accounting, the final accounts of the company have bene prepared using

the provisions and the principals of generally accepted Accounting Practices in New Zealand.

The group is the profit entity for the purposes of complying with the provisions of NZ

GAAP. The consolidated final accounts of the company have been prepared under the

provisions and in the light of the International Financial Reporting Standards along with such

other accounting standards of the country and the authoritative notices that are applicable on

all of the companies. The final accounts have been prepared using the historical cost

convention of the group. The functional currency being used by the company is the New

Zealand $. In respect of the changes in the policies of accounting for the company and the

disclosures, the policies in respect of accounting and the disclosures are very much the same

as were followed during the previous year. But there is some of the information and the fact

that have to be reclassified in order to bring them with the current period amounts.

There are some of the standards and the interpretations that are not effective on the group but

are relevant to the group. These include the following:

NZ IFRS 9: this is the standard on accounting which relates with the financial instruments.

This standard replaces NZ IAS 139 which deals with the financial instruments, recognition

and measurement and the addressing of the classification, measurement and the recognition

of the assets and the liabilities of the company. This new standard on accounting is effective

from January 31, 2019. This standard on accounting is the one which introduces the expected

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ADVANCED FINANCIAL ACCOUNTING 4

credit loss model which means that there is no requirement of any trigger before the company

recognises any amount of impairment loss in the final accounts. The company would be

required to assess the loss on impairment on the trade receivables at the time, revenue is

recognised. The management of the company has assessed the impact of the NZ IFRS 9 on

the measurement of the expected losses of impairment. This would lead to an increase in the

amount of the provision for the doubtful debts.. but then this assessment does not have any

material impact over the final accounts. The sun total of this amount would be adjusted in the

statement of retained earnings.

The company indulges in the hedging operations. The company has to align its business and

accounting relationships with the risk management objectives and the strategies of the

company. This includes the qualitative and an increased forward looking approach when it

comes to the assessment of the effectiveness of hedging. This hedging relationship would

continue in the future too.

NZ IFRS 15 which deals south the revenues from the contracts from the customers. This is

the accounting standards which deals with the recognition of revenue for the company. Many

amount of money incurred or spent by the company towards obtaining the contracts from the

customers is required to be capitalised and shall be expensed on so systematic basis. Such of

the costs would include the costs of commission etc.

This standard goes in for the recognising of the amount of revenue as being distinct perform

obligations but this could change the timing and the classification of the revenue recognition.

The management had successfully performed the initial assessment of the impact of NZ IFRS

15 and this does not expect the recognition and the measurement of the revenue that could

change under the new accounting standard. The majority of the customers of the company on

monthly terms which means that the maximum amount of the costs are connected with the

customer contracts. The offerings of the company mainly comprise of the provision of the

cloud software along with its ancillary support services. These are the services that are

determined on the basis of the contractual terms and that usually are of a term of 1 month.

This means that there is an identification of the distinct performance obligation hat has no

impact over the timing of the revenue recognition for the company. The effect of these

incremental costs is the obtaining of the contract of nay revenue which could be deferred

which results from the contracts that are of a greater term which extends to more than a

month and is not expected to be material.

credit loss model which means that there is no requirement of any trigger before the company

recognises any amount of impairment loss in the final accounts. The company would be

required to assess the loss on impairment on the trade receivables at the time, revenue is

recognised. The management of the company has assessed the impact of the NZ IFRS 9 on

the measurement of the expected losses of impairment. This would lead to an increase in the

amount of the provision for the doubtful debts.. but then this assessment does not have any

material impact over the final accounts. The sun total of this amount would be adjusted in the

statement of retained earnings.

The company indulges in the hedging operations. The company has to align its business and

accounting relationships with the risk management objectives and the strategies of the

company. This includes the qualitative and an increased forward looking approach when it

comes to the assessment of the effectiveness of hedging. This hedging relationship would

continue in the future too.

NZ IFRS 15 which deals south the revenues from the contracts from the customers. This is

the accounting standards which deals with the recognition of revenue for the company. Many

amount of money incurred or spent by the company towards obtaining the contracts from the

customers is required to be capitalised and shall be expensed on so systematic basis. Such of

the costs would include the costs of commission etc.

This standard goes in for the recognising of the amount of revenue as being distinct perform

obligations but this could change the timing and the classification of the revenue recognition.

The management had successfully performed the initial assessment of the impact of NZ IFRS

15 and this does not expect the recognition and the measurement of the revenue that could

change under the new accounting standard. The majority of the customers of the company on

monthly terms which means that the maximum amount of the costs are connected with the

customer contracts. The offerings of the company mainly comprise of the provision of the

cloud software along with its ancillary support services. These are the services that are

determined on the basis of the contractual terms and that usually are of a term of 1 month.

This means that there is an identification of the distinct performance obligation hat has no

impact over the timing of the revenue recognition for the company. The effect of these

incremental costs is the obtaining of the contract of nay revenue which could be deferred

which results from the contracts that are of a greater term which extends to more than a

month and is not expected to be material.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED FINANCIAL ACCOUNTING 5

In respect of NZ IFRS 16 which deals with leases, this standard goes on to replace NZ IAS

17 which deals with the leases and the changes in the way in which the company accounts are

used for the operating leases. The new standard on accounting requires the reporting of the

liability of lease and the right of use as at the initiation of the future lease payments that

would affect all of the leasing contracts. These are the expenses that were recorded in

connection with the operating leases and this would move the operating leases from being

reported as the operating expenses to the depreciation and the finance expense. This is the

standard of accounting which is applicable on the company from the year ending March 31,

2020 but an early adoption of the same is allowed. The company intends to adopt the

provisions of this standard for the year ended March 31, 2019.

With regard to the critical accounting estimates, the company uses its past experience,

judgments, along with the various assumptions for the purposes of assessing the true impact

of the future events on the company. All of these judgments, estimates and the assumptions

are considered to be reasonable which are based upon the most current set of the scenarios

which are available to the group. These actual results may be very different from the

judgments, estimates and the assumptions that have been made.

In respect of deferred taxes, the company recognises the amounts of the deferred taxes in

relation with the taxation losses only to the extent the same applies to the deferred taxation

liabilities of the company. The group recognises these assets and the liabilities in respect of

the additional amounts of the losses on the temporary differences that are given in time of the

uncertainty of the timing of the probability along with the requirement for the purposes of

continuity of the ownership of the company ("Annual report 2018", 2019).

Changes in AASB 116:

The old standard on accounting entailed the recording the obligation of the company to

record the future payments under the arrangement of operating lease but the same was never

included in the statement of financial position or in the final accounts. This recording of the

expenses was never to be made in the final account even when there was an outflow of cash

for the company ("AASB 16 Leases: 2019 accounting changes - Accru", 2019). This was a

cause of concern for the various stakeholders since it did not give the accurate reflection of

the true financial facts of the company.

The changes came into effect from January 1, 2019. This resulted in the inclusion of the

liability for lease and the right to use an asset as the date of the balance sheet. In the other

In respect of NZ IFRS 16 which deals with leases, this standard goes on to replace NZ IAS

17 which deals with the leases and the changes in the way in which the company accounts are

used for the operating leases. The new standard on accounting requires the reporting of the

liability of lease and the right of use as at the initiation of the future lease payments that

would affect all of the leasing contracts. These are the expenses that were recorded in

connection with the operating leases and this would move the operating leases from being

reported as the operating expenses to the depreciation and the finance expense. This is the

standard of accounting which is applicable on the company from the year ending March 31,

2020 but an early adoption of the same is allowed. The company intends to adopt the

provisions of this standard for the year ended March 31, 2019.

With regard to the critical accounting estimates, the company uses its past experience,

judgments, along with the various assumptions for the purposes of assessing the true impact

of the future events on the company. All of these judgments, estimates and the assumptions

are considered to be reasonable which are based upon the most current set of the scenarios

which are available to the group. These actual results may be very different from the

judgments, estimates and the assumptions that have been made.

In respect of deferred taxes, the company recognises the amounts of the deferred taxes in

relation with the taxation losses only to the extent the same applies to the deferred taxation

liabilities of the company. The group recognises these assets and the liabilities in respect of

the additional amounts of the losses on the temporary differences that are given in time of the

uncertainty of the timing of the probability along with the requirement for the purposes of

continuity of the ownership of the company ("Annual report 2018", 2019).

Changes in AASB 116:

The old standard on accounting entailed the recording the obligation of the company to

record the future payments under the arrangement of operating lease but the same was never

included in the statement of financial position or in the final accounts. This recording of the

expenses was never to be made in the final account even when there was an outflow of cash

for the company ("AASB 16 Leases: 2019 accounting changes - Accru", 2019). This was a

cause of concern for the various stakeholders since it did not give the accurate reflection of

the true financial facts of the company.

The changes came into effect from January 1, 2019. This resulted in the inclusion of the

liability for lease and the right to use an asset as the date of the balance sheet. In the other

ADVANCED FINANCIAL ACCOUNTING 6

words, the amounts that the company incurred towards the use of the leased asset would not

be reported in the final accounts. The AASB 16 which is the new standard on accounting

went on to give a more accurate picture of the financial facts of the company which indicated

the true amount of the assets, liabilities and which would also provide the correct final picture

of the company and would show the downside of this information as well. The changes that

accrues to the company world would help in increasing the level of the commercial and the

risk of financial reporting, keeping in mind the complexity and the issues that are hidden

which may arise when this new accounting standard is implemented ("AASB 16: Leases",

2019).

The new accounting standard would go on to change the profile of the expense. Under the old

method, the expense was constant over the period of years but this accounting standard goes

on to show and indicate lesser amount of an expense with the increase in the years. This will

further go on to increase the metric such as the EBITDA ("AASB 16 - Lease Accounting",

2019). Instead of moving the operating rental amount of the expenses, there would now be

the movement of the expenses below the EBITDA which would be beyond the range of some

of the issues associated with them. Also, there would be a possible financial reporting

anomalies that would show the issues connected with the amount of the working capital with

the current liability about the funding of the non-current asset. There could be some of the

effects on the bank convents that could lead to the breach in case, the company is not

conscious about the proactive when it comes to approaching its customers.

Another impact of this is the fact that more and more companies would go on to qualify the

large proprietary companies and would include the various rights of the use of the assets in

the final accounts which would lead to an increase in the total amount of the assets and this

would require the filing of the final accounts ("New Leasing Standard (AASB 16) Brings

Significant Impacts | HLB Mann Judd", 2019).

The changes that would take place due to the new standard on accounting is something that

would comply with the rules and the requirements of Australian Accounting standards.

The non-reporting companies are the ones that are not duty bound to prepare their final

accounts as per the relevant standards on accounting and these are the changes that have an

impact over the stakeholders such as the banks that would put in place the conditions with

regard to the application of these set of standards.

words, the amounts that the company incurred towards the use of the leased asset would not

be reported in the final accounts. The AASB 16 which is the new standard on accounting

went on to give a more accurate picture of the financial facts of the company which indicated

the true amount of the assets, liabilities and which would also provide the correct final picture

of the company and would show the downside of this information as well. The changes that

accrues to the company world would help in increasing the level of the commercial and the

risk of financial reporting, keeping in mind the complexity and the issues that are hidden

which may arise when this new accounting standard is implemented ("AASB 16: Leases",

2019).

The new accounting standard would go on to change the profile of the expense. Under the old

method, the expense was constant over the period of years but this accounting standard goes

on to show and indicate lesser amount of an expense with the increase in the years. This will

further go on to increase the metric such as the EBITDA ("AASB 16 - Lease Accounting",

2019). Instead of moving the operating rental amount of the expenses, there would now be

the movement of the expenses below the EBITDA which would be beyond the range of some

of the issues associated with them. Also, there would be a possible financial reporting

anomalies that would show the issues connected with the amount of the working capital with

the current liability about the funding of the non-current asset. There could be some of the

effects on the bank convents that could lead to the breach in case, the company is not

conscious about the proactive when it comes to approaching its customers.

Another impact of this is the fact that more and more companies would go on to qualify the

large proprietary companies and would include the various rights of the use of the assets in

the final accounts which would lead to an increase in the total amount of the assets and this

would require the filing of the final accounts ("New Leasing Standard (AASB 16) Brings

Significant Impacts | HLB Mann Judd", 2019).

The changes that would take place due to the new standard on accounting is something that

would comply with the rules and the requirements of Australian Accounting standards.

The non-reporting companies are the ones that are not duty bound to prepare their final

accounts as per the relevant standards on accounting and these are the changes that have an

impact over the stakeholders such as the banks that would put in place the conditions with

regard to the application of these set of standards.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ADVANCED FINANCIAL ACCOUNTING 7

Keeping in mind the changes that have bene introduced, it is imperative for each company to

dedicate the resources of the company so that it could adopt these changes in the most

efficient manner ("IFRS 16", 2019). This would go on to include to factor an immense

amount of time for the consulting with the audit team and other such stakeholders.

In respect of the annual accounts for the year 2018-19, each company should detail out the

impact of these new standards on accounting which are not yet effective. Considering these

changes from the new accounting standard, the company is required to provide the estimates

for the expected impacts of these new standards on accounting.

The new AASB 16 would see the assets, excluding the smaller assets and the ones that have a

12 month rental agreement, to be reported in the final accounts by the way of recording the

right of use of the assets and the liability of lease. The initial entry on transition is to record

the right of use for the assets and the liability of the same amount, which is the amount of the

cash flows that are unpaid and that are connected with the lease discounted at the proper rate

of discount ("Changes to Accounting Standards - AASB 16 Leases | Davidsons Accountants

and Business Consultants", 2019). The right of use of these assets is the expense which is

amortised over the period of the agreement of lease and this is the amount of the lease

liability which is incurred with an effective interest and is reduced by the amount of the lease

payments until the amount reaches to 0.

These are few of the changes that affect the key financial ratios such as gearing, current ratios

and the earnings before taxes. The benchmarks would be desired to be adjusted with the key

performance indicators, especially when these have been set by the external parties such as

the banks connected with the borrowings, regulators connected with funding.

Key disclosures:

In respect of NZ IFRS 16 which deals with leases, this standard goes on to replace NZ IAS

17 which deals with the leases and the changes in the way in which the company accounts are

used for the operating leases. The new standard on accounting requires the reporting of the

liability of lease and the right of use as at the initiation of the future lease payments that

would affect all of the leasing contracts. These are the expenses that were recorded in

connection with the operating leases and this would move the operating leases from being

reported as the operating expenses to the depreciation and the finance expense. This is the

standard of accounting which is applicable on the company from the year ending March 31,

Keeping in mind the changes that have bene introduced, it is imperative for each company to

dedicate the resources of the company so that it could adopt these changes in the most

efficient manner ("IFRS 16", 2019). This would go on to include to factor an immense

amount of time for the consulting with the audit team and other such stakeholders.

In respect of the annual accounts for the year 2018-19, each company should detail out the

impact of these new standards on accounting which are not yet effective. Considering these

changes from the new accounting standard, the company is required to provide the estimates

for the expected impacts of these new standards on accounting.

The new AASB 16 would see the assets, excluding the smaller assets and the ones that have a

12 month rental agreement, to be reported in the final accounts by the way of recording the

right of use of the assets and the liability of lease. The initial entry on transition is to record

the right of use for the assets and the liability of the same amount, which is the amount of the

cash flows that are unpaid and that are connected with the lease discounted at the proper rate

of discount ("Changes to Accounting Standards - AASB 16 Leases | Davidsons Accountants

and Business Consultants", 2019). The right of use of these assets is the expense which is

amortised over the period of the agreement of lease and this is the amount of the lease

liability which is incurred with an effective interest and is reduced by the amount of the lease

payments until the amount reaches to 0.

These are few of the changes that affect the key financial ratios such as gearing, current ratios

and the earnings before taxes. The benchmarks would be desired to be adjusted with the key

performance indicators, especially when these have been set by the external parties such as

the banks connected with the borrowings, regulators connected with funding.

Key disclosures:

In respect of NZ IFRS 16 which deals with leases, this standard goes on to replace NZ IAS

17 which deals with the leases and the changes in the way in which the company accounts are

used for the operating leases. The new standard on accounting requires the reporting of the

liability of lease and the right of use as at the initiation of the future lease payments that

would affect all of the leasing contracts. These are the expenses that were recorded in

connection with the operating leases and this would move the operating leases from being

reported as the operating expenses to the depreciation and the finance expense. This is the

standard of accounting which is applicable on the company from the year ending March 31,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED FINANCIAL ACCOUNTING 8

2020 but an early adoption of the same is allowed. The company intends to adopt the

provisions of this standard for the year ended March 31, 2019. The management did assess

the initial assessment based on the leases. For year ending March 31, 2018, the new standard

would have led to an operating lease expense of $10.8 million with a depreciation expense of

$0.9 million and $2.2 million increase in the finance expense. The entire impact shall be

around $0.4 million increase in the net losses before taxes. And the impact of it on the final

accounts would be $46.4 million and the increase in the liabilities of $52.4 million. These

estimates would have been materially different had the new accounting standard were

adopted.

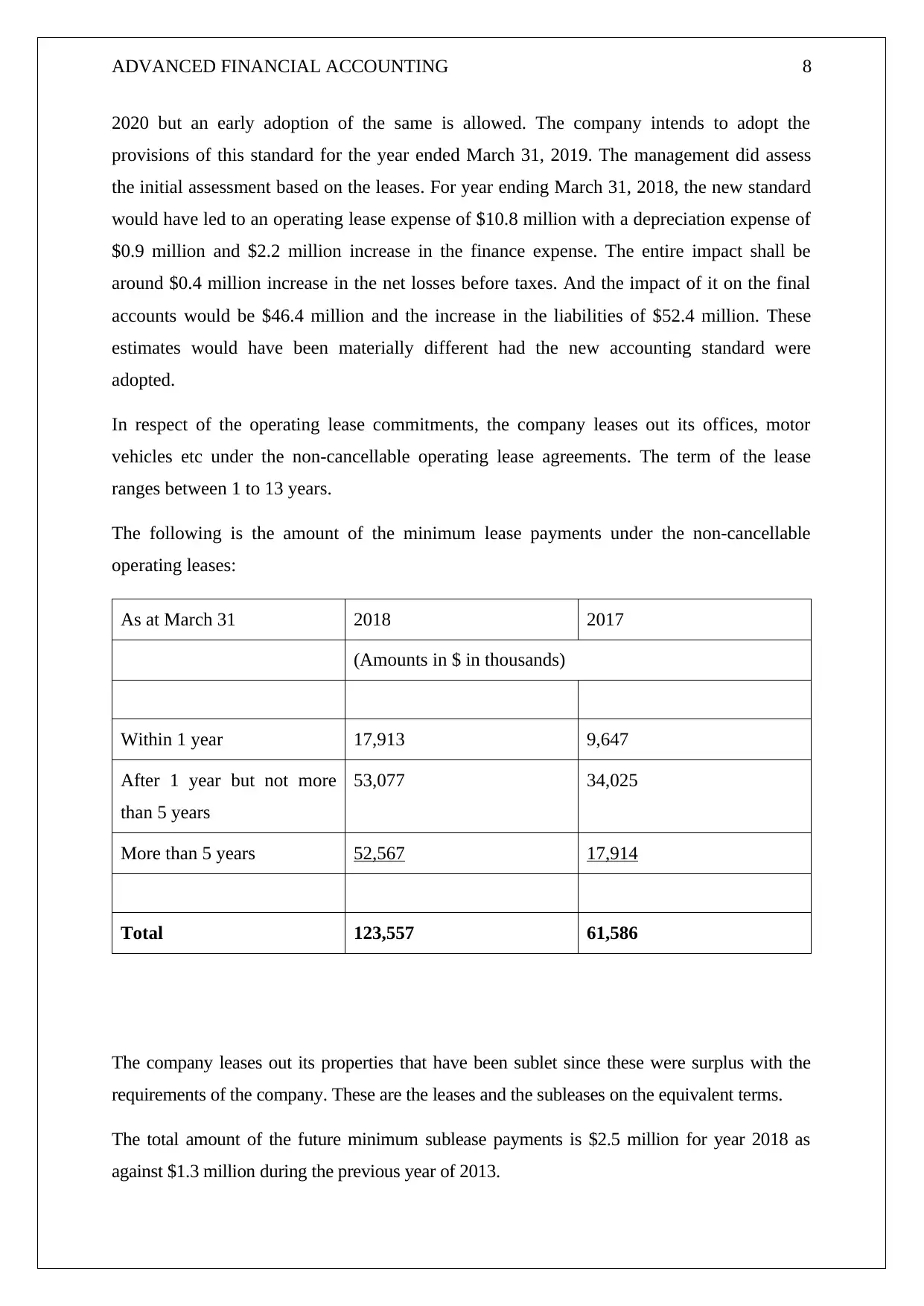

In respect of the operating lease commitments, the company leases out its offices, motor

vehicles etc under the non-cancellable operating lease agreements. The term of the lease

ranges between 1 to 13 years.

The following is the amount of the minimum lease payments under the non-cancellable

operating leases:

As at March 31 2018 2017

(Amounts in $ in thousands)

Within 1 year 17,913 9,647

After 1 year but not more

than 5 years

53,077 34,025

More than 5 years 52,567 17,914

Total 123,557 61,586

The company leases out its properties that have been sublet since these were surplus with the

requirements of the company. These are the leases and the subleases on the equivalent terms.

The total amount of the future minimum sublease payments is $2.5 million for year 2018 as

against $1.3 million during the previous year of 2013.

2020 but an early adoption of the same is allowed. The company intends to adopt the

provisions of this standard for the year ended March 31, 2019. The management did assess

the initial assessment based on the leases. For year ending March 31, 2018, the new standard

would have led to an operating lease expense of $10.8 million with a depreciation expense of

$0.9 million and $2.2 million increase in the finance expense. The entire impact shall be

around $0.4 million increase in the net losses before taxes. And the impact of it on the final

accounts would be $46.4 million and the increase in the liabilities of $52.4 million. These

estimates would have been materially different had the new accounting standard were

adopted.

In respect of the operating lease commitments, the company leases out its offices, motor

vehicles etc under the non-cancellable operating lease agreements. The term of the lease

ranges between 1 to 13 years.

The following is the amount of the minimum lease payments under the non-cancellable

operating leases:

As at March 31 2018 2017

(Amounts in $ in thousands)

Within 1 year 17,913 9,647

After 1 year but not more

than 5 years

53,077 34,025

More than 5 years 52,567 17,914

Total 123,557 61,586

The company leases out its properties that have been sublet since these were surplus with the

requirements of the company. These are the leases and the subleases on the equivalent terms.

The total amount of the future minimum sublease payments is $2.5 million for year 2018 as

against $1.3 million during the previous year of 2013.

ADVANCED FINANCIAL ACCOUNTING 9

Conclusion:

The new accounting standard goes in for the classification for leases in the most

appropriate way. It has the ability of reporting the operational leases in the

footnotes of the final accounts. The reason for the stated change for reporting

the changes in the notes to final accounts is that the final accounts could be

misleading about the true nature of the amount of the liabilities of the company.

In response to it, the IASB released the IFRS 16 and the AASB soon followed

up with the AASB 16. The new standard on accounting has plucked all of the

loopholes since now, it requires to disclose all of the operating leases as the

finance lease ("AASB 16 - Lease Accounting", 2019).

Conclusion:

The new accounting standard goes in for the classification for leases in the most

appropriate way. It has the ability of reporting the operational leases in the

footnotes of the final accounts. The reason for the stated change for reporting

the changes in the notes to final accounts is that the final accounts could be

misleading about the true nature of the amount of the liabilities of the company.

In response to it, the IASB released the IFRS 16 and the AASB soon followed

up with the AASB 16. The new standard on accounting has plucked all of the

loopholes since now, it requires to disclose all of the operating leases as the

finance lease ("AASB 16 - Lease Accounting", 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ADVANCED FINANCIAL ACCOUNTING 10

References:

AASB 16 - Lease Accounting. (2019). Retrieved 21 September 2019, from

https://leaseaccounting.com/aasb-16/

AASB 16 - Lease Accounting. (2019). Retrieved 21 September 2019, from

https://leaseaccounting.com/aasb-16/

AASB 16 Leases: 2019 accounting changes - Accru. (2019). Retrieved 21 September 2019,

from https://www.accru.com/2019/08/aasb-16-leases-2019-accounting-changes/

AASB 16: Leases. (2019). Retrieved 21 September 2019, from

https://home.kpmg/au/en/home/insights/2017/04/aasb-16-leases-standard.html

Annual report 2018. (2019). Retrieved 21 September 2019, from

https://www.xero.com/content/dam/xero/pdf/About%20Us/xero-annual-report-2018.pdf

Changes to Accounting Standards - AASB 16 Leases | Davidsons Accountants and Business

Consultants. (2019). Retrieved 21 September 2019, from

https://www.davidsons.com.au/news/2019/03/06/changes-to-accounting-standards-aasb-

16-leases/

IFRS 16. (2019). Retrieved 21 September 2019, from

https://www.bdo.com.au/en-au/services/audit-assurance/ifrs-advisory-services/ifrs-16

New Leasing Standard (AASB 16) Brings Significant Impacts | HLB Mann Judd. (2019).

Retrieved 21 September 2019, from https://www.hlb.com.au/new-leasing-standard-aasb-

16-brings-significant-impacts/

References:

AASB 16 - Lease Accounting. (2019). Retrieved 21 September 2019, from

https://leaseaccounting.com/aasb-16/

AASB 16 - Lease Accounting. (2019). Retrieved 21 September 2019, from

https://leaseaccounting.com/aasb-16/

AASB 16 Leases: 2019 accounting changes - Accru. (2019). Retrieved 21 September 2019,

from https://www.accru.com/2019/08/aasb-16-leases-2019-accounting-changes/

AASB 16: Leases. (2019). Retrieved 21 September 2019, from

https://home.kpmg/au/en/home/insights/2017/04/aasb-16-leases-standard.html

Annual report 2018. (2019). Retrieved 21 September 2019, from

https://www.xero.com/content/dam/xero/pdf/About%20Us/xero-annual-report-2018.pdf

Changes to Accounting Standards - AASB 16 Leases | Davidsons Accountants and Business

Consultants. (2019). Retrieved 21 September 2019, from

https://www.davidsons.com.au/news/2019/03/06/changes-to-accounting-standards-aasb-

16-leases/

IFRS 16. (2019). Retrieved 21 September 2019, from

https://www.bdo.com.au/en-au/services/audit-assurance/ifrs-advisory-services/ifrs-16

New Leasing Standard (AASB 16) Brings Significant Impacts | HLB Mann Judd. (2019).

Retrieved 21 September 2019, from https://www.hlb.com.au/new-leasing-standard-aasb-

16-brings-significant-impacts/

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.