Advanced Financial Accounting Assignment: Solution and Analysis, 2018

VerifiedAdded on 2023/03/23

|18

|2229

|61

Homework Assignment

AI Summary

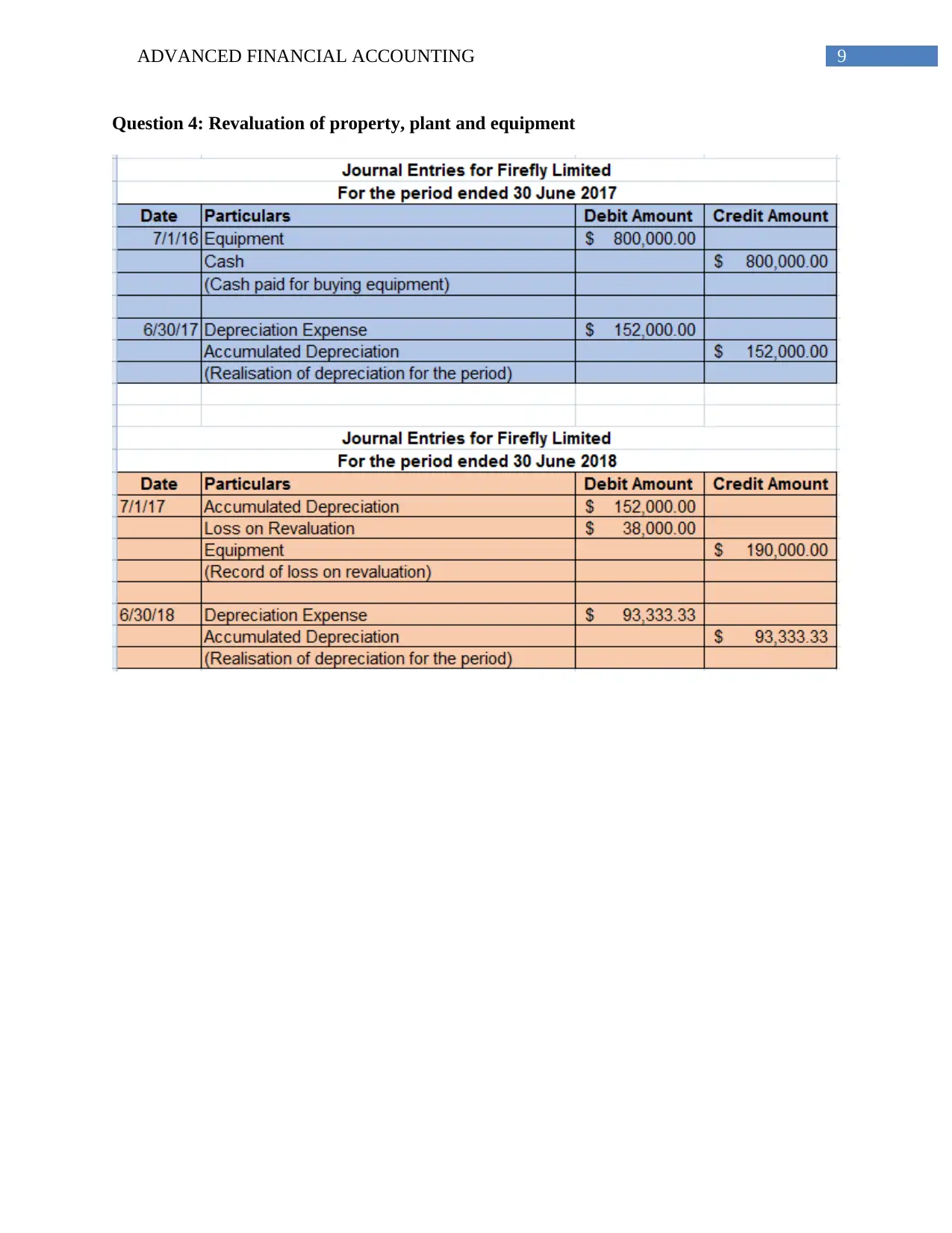

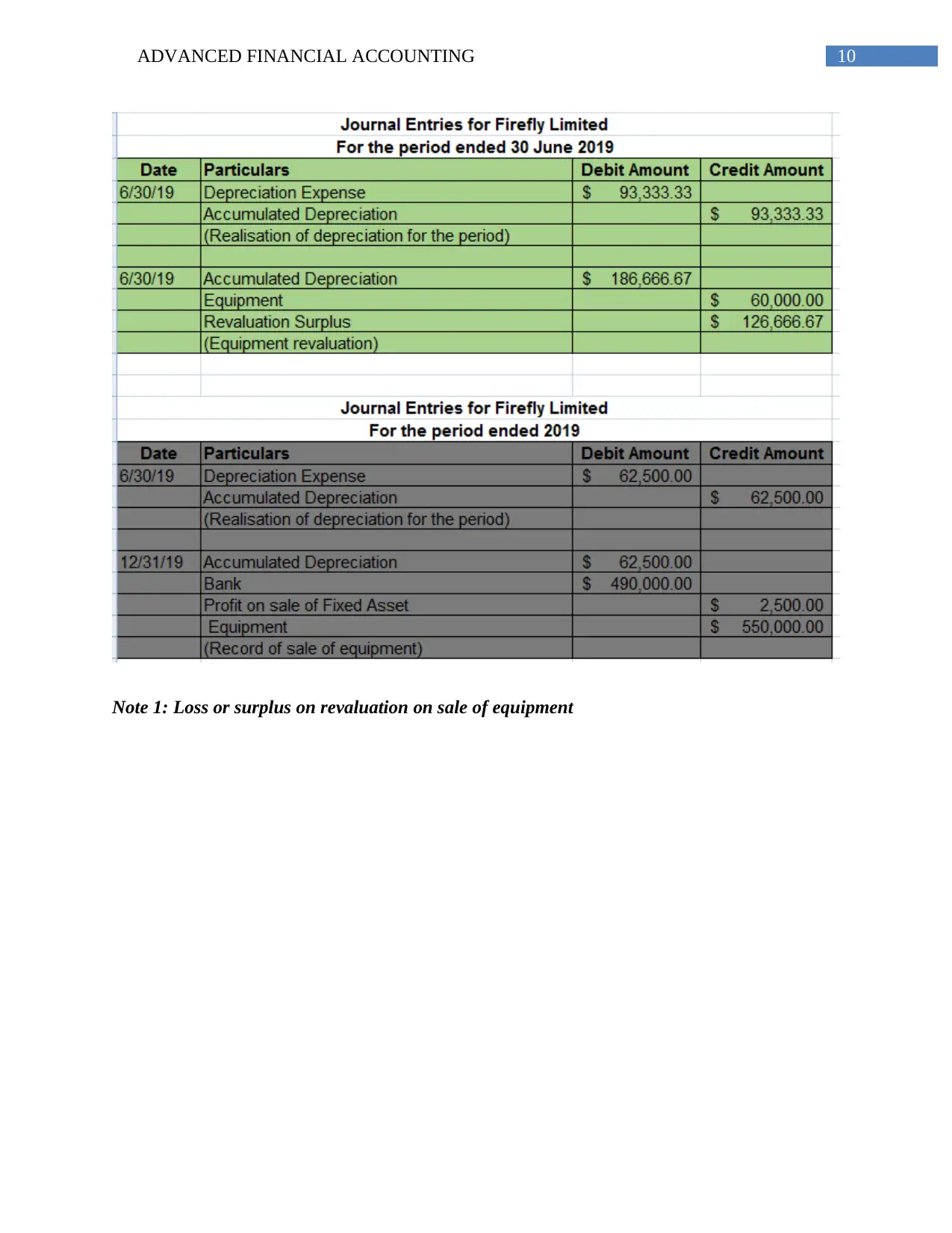

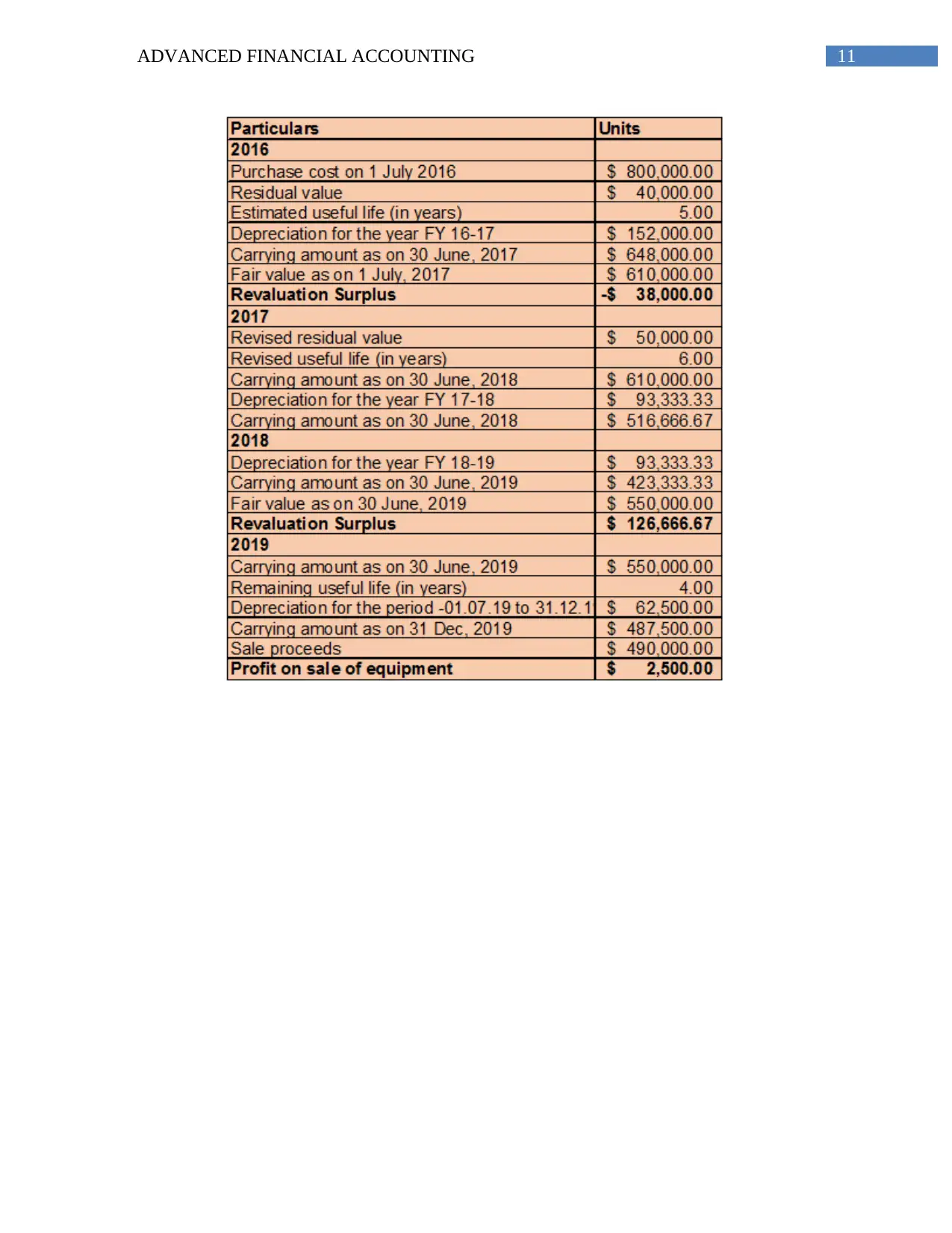

This document provides a comprehensive solution to an Advanced Financial Accounting assignment. The assignment covers five key questions, including financial statement disclosures, accounting for share capital, accounting for income tax (including deferred tax calculations), revaluation of property, plant, and equipment, and impairment of assets. The solution includes detailed explanations, journal entries, and calculations, referencing relevant Australian Accounting Standards (AASB) such as AASB 108, AASB 110, and AASB 136. The financial statement disclosures section analyzes scenarios involving warranty provisions, bad debts, changes in tax rates, and error corrections. The share capital section includes notes on allotment amounts and refunds. The income tax section provides worksheets for deferred tax calculations. The revaluation and impairment sections detail the accounting treatment for asset valuation changes and impairment losses, including the allocation of impairment losses to goodwill and other assets. The document is a valuable resource for students studying advanced financial accounting, offering a practical application of accounting principles.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.