Detailed Solution: Advanced Financial Accounting Assignment (ACC204)

VerifiedAdded on 2023/06/10

|9

|1344

|354

Homework Assignment

AI Summary

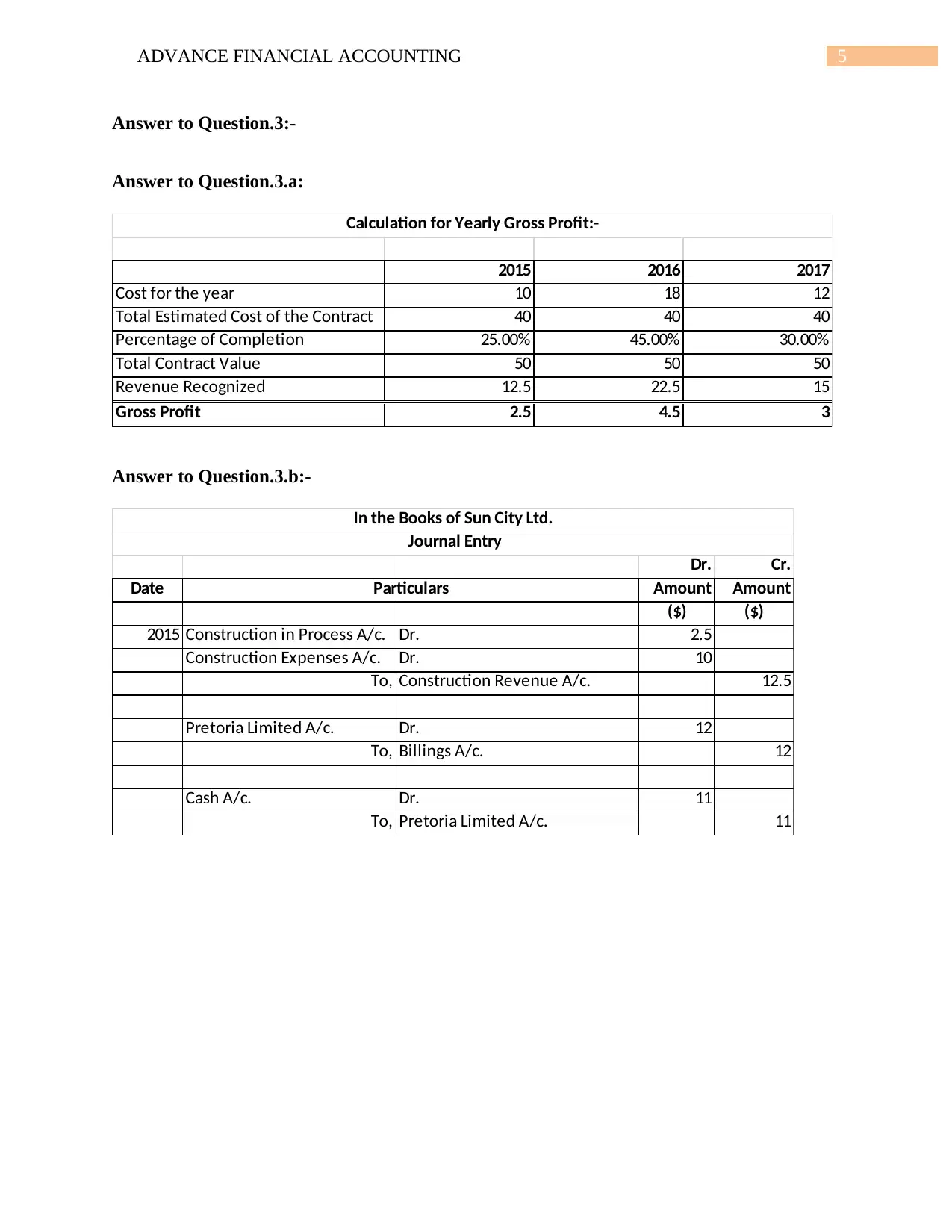

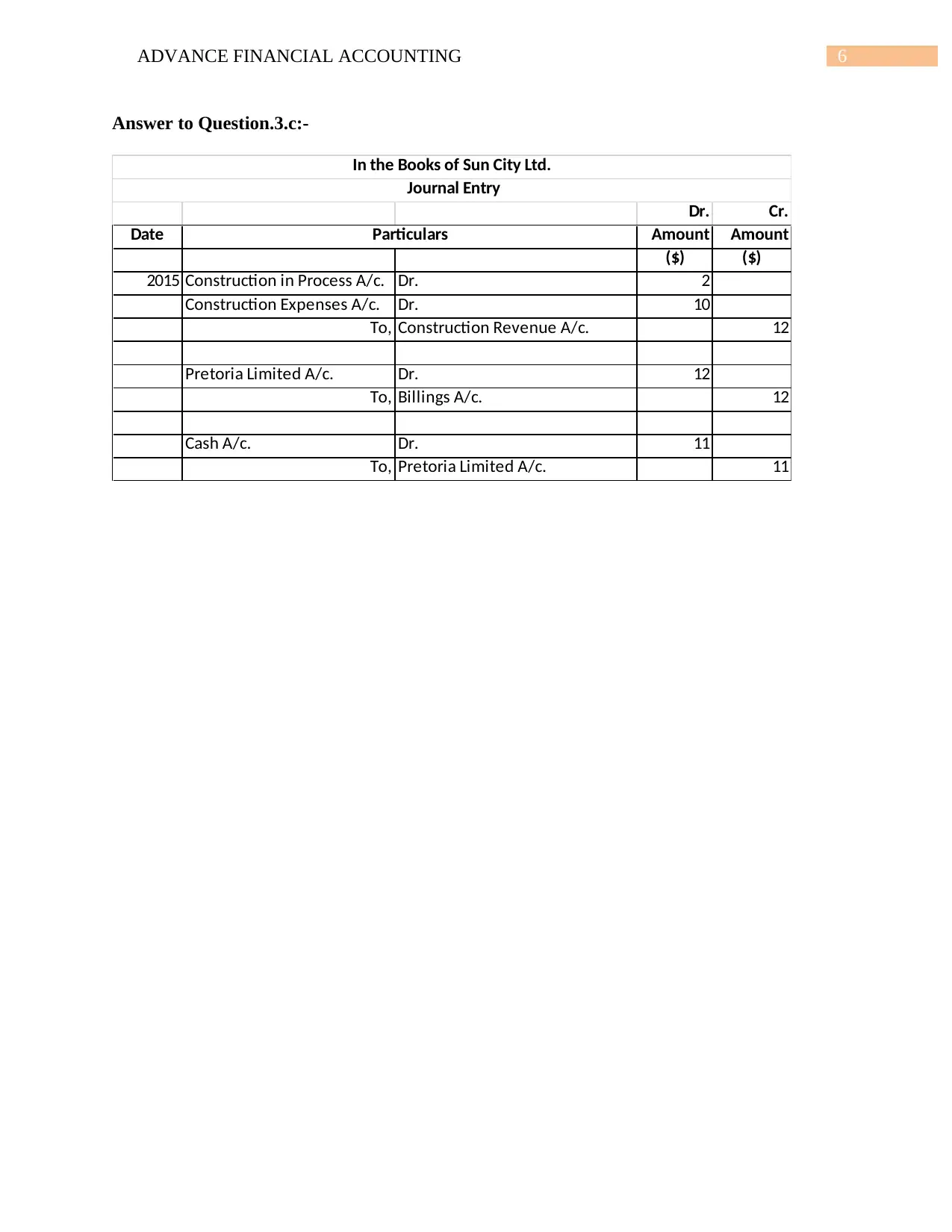

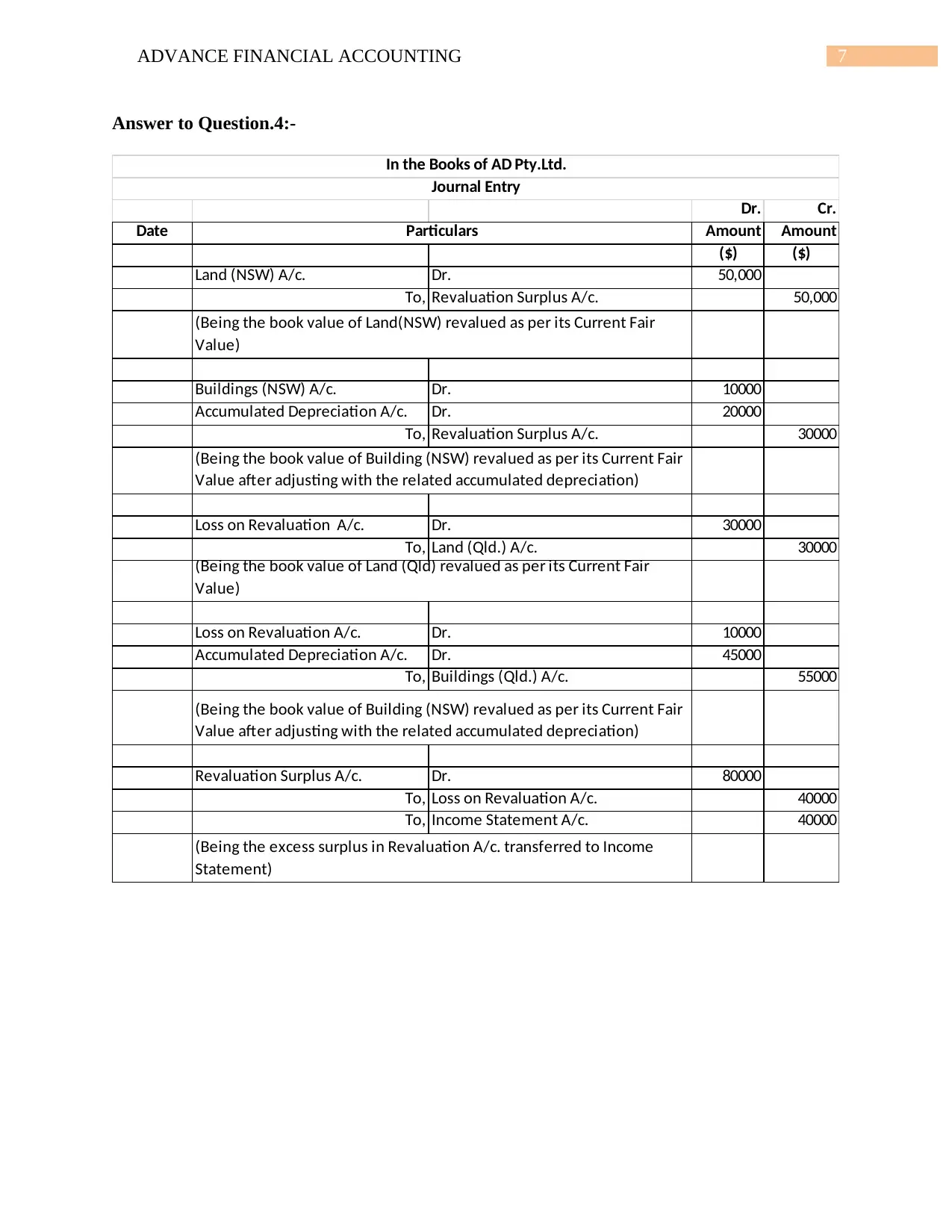

This document presents a comprehensive solution to an Advanced Financial Accounting (ACC204) assignment. The assignment covers several key areas of financial accounting, including the revaluation of assets, accounting for debentures, and construction accounting. The solution includes detailed journal entries, calculations, and explanations for each question. The first question addresses asset revaluation, providing journal entries to record changes in the fair value of land and buildings. The second question focuses on debentures, calculating the fair value, and preparing relevant journal entries for issuance and interest payments. The third question delves into construction accounting, calculating gross profit and preparing journal entries for revenue recognition. The fourth question mirrors the first, reinforcing understanding of asset revaluation. The document includes a bibliography with relevant sources, showcasing the student's research and understanding of the subject matter. This assignment provides a thorough examination of accounting principles and practices, offering valuable insights for students studying financial accounting.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.