AASB Standards and Accounting Policies: An Advanced Financial Report

VerifiedAdded on 2023/06/06

|10

|1684

|368

Report

AI Summary

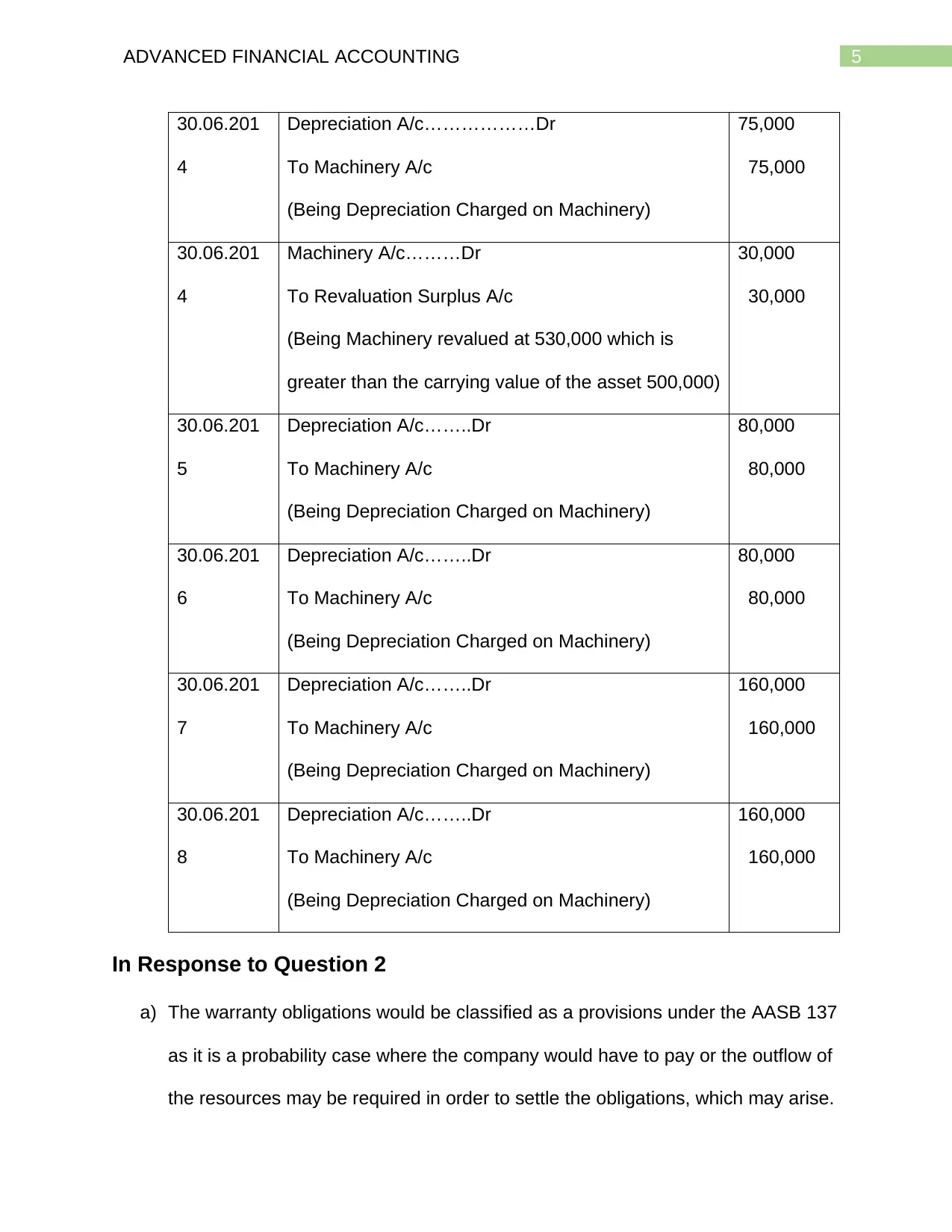

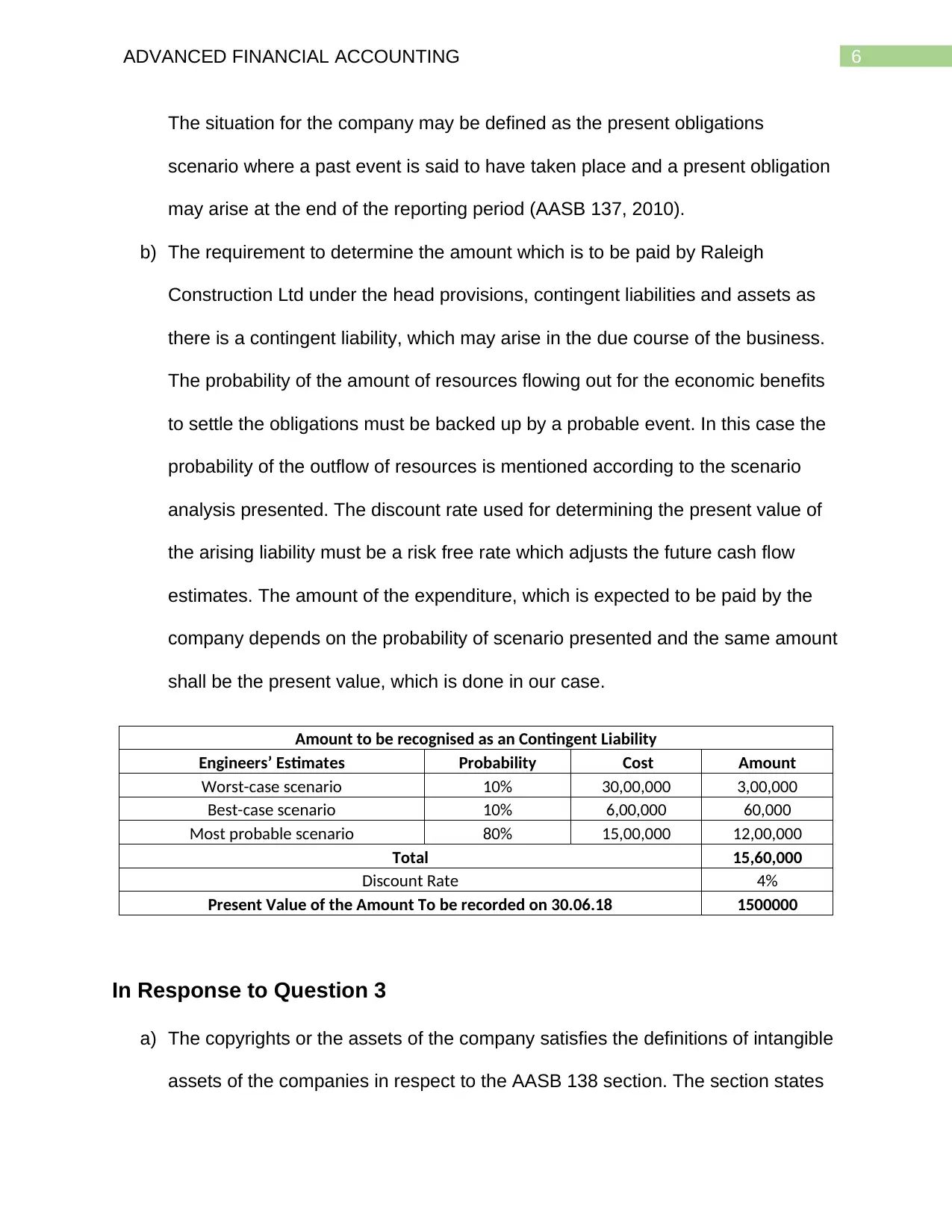

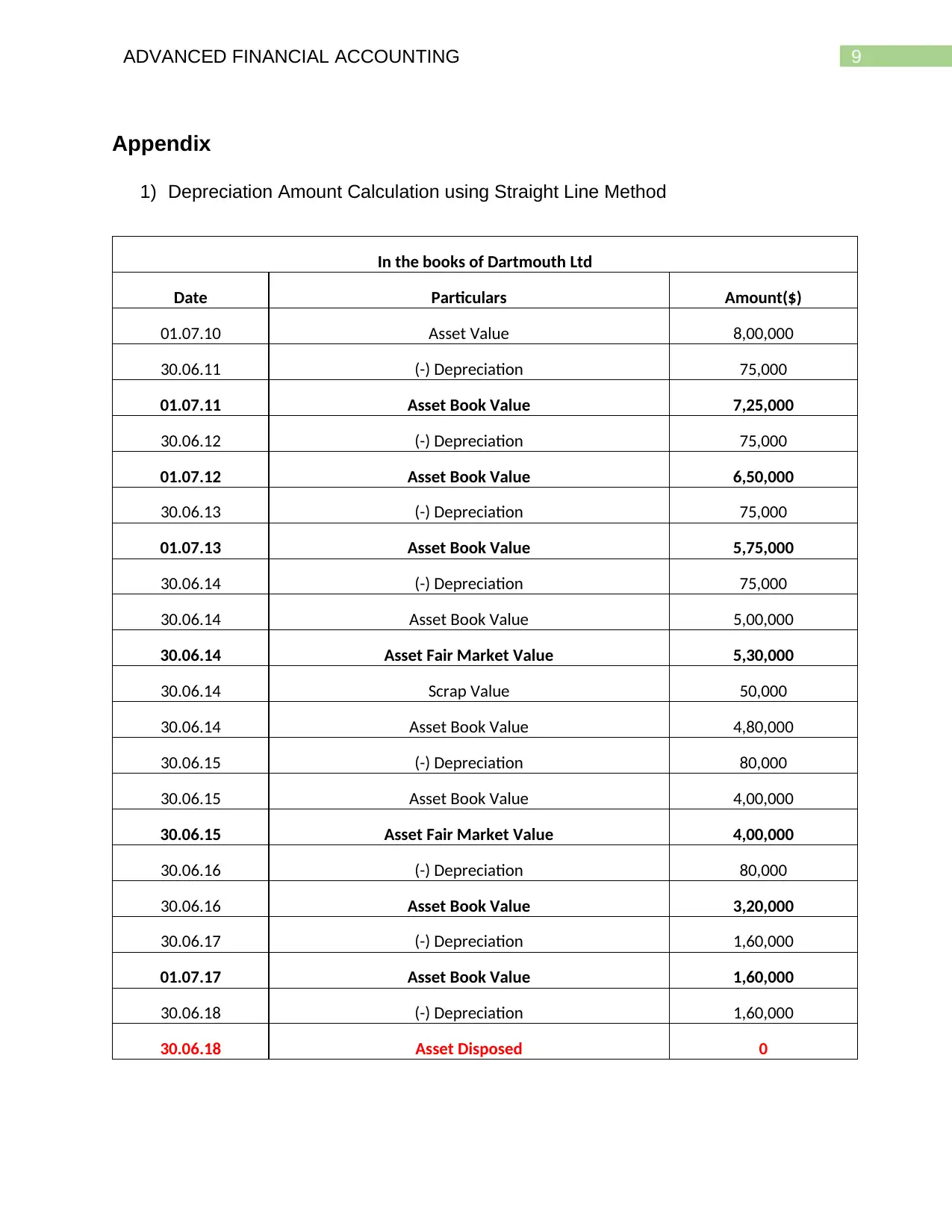

This report provides a comprehensive analysis of accounting policies and their changes within a company, focusing on the application of various Australian Accounting Standards Board (AASB) standards such as AASB 108, AASB 116, AASB 137, and AASB 138. It delves into accounting techniques and methods, illustrating their application through examples related to asset revaluation, depreciation, warranty obligations, and intangible assets like copyrights. The report includes detailed journal entries, calculations for depreciation using the straight-line method, and an evaluation of contingent liabilities, offering a practical understanding of advanced financial accounting principles and their implementation in real-world scenarios. The document provides detailed insights into handling changes in accounting estimates, determining warranty obligations, and managing intangible assets, making it a valuable resource for understanding complex accounting procedures.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.