Consolidated Financial Statements: Advance Financial Accounting

VerifiedAdded on 2023/04/21

|7

|755

|116

Homework Assignment

AI Summary

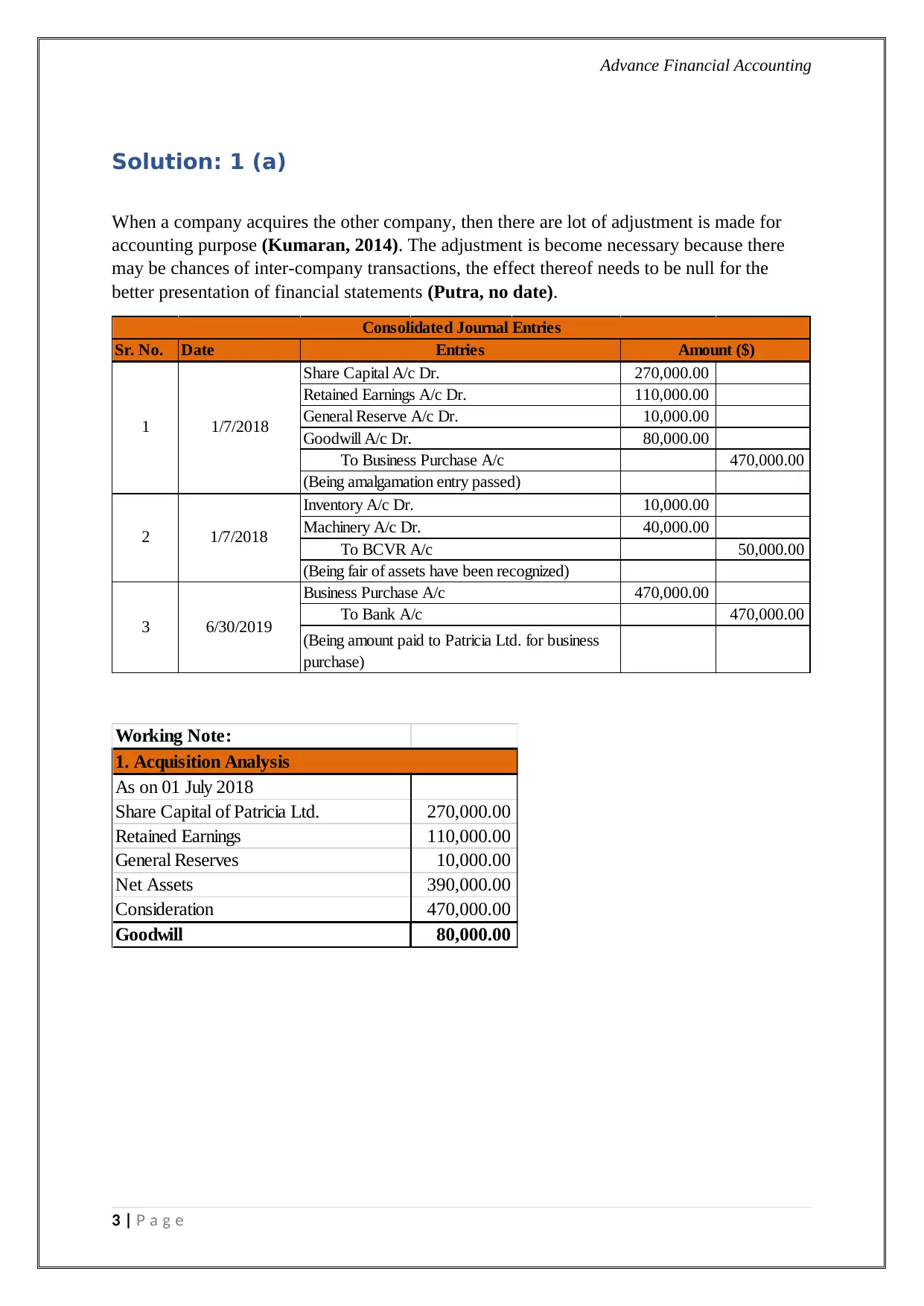

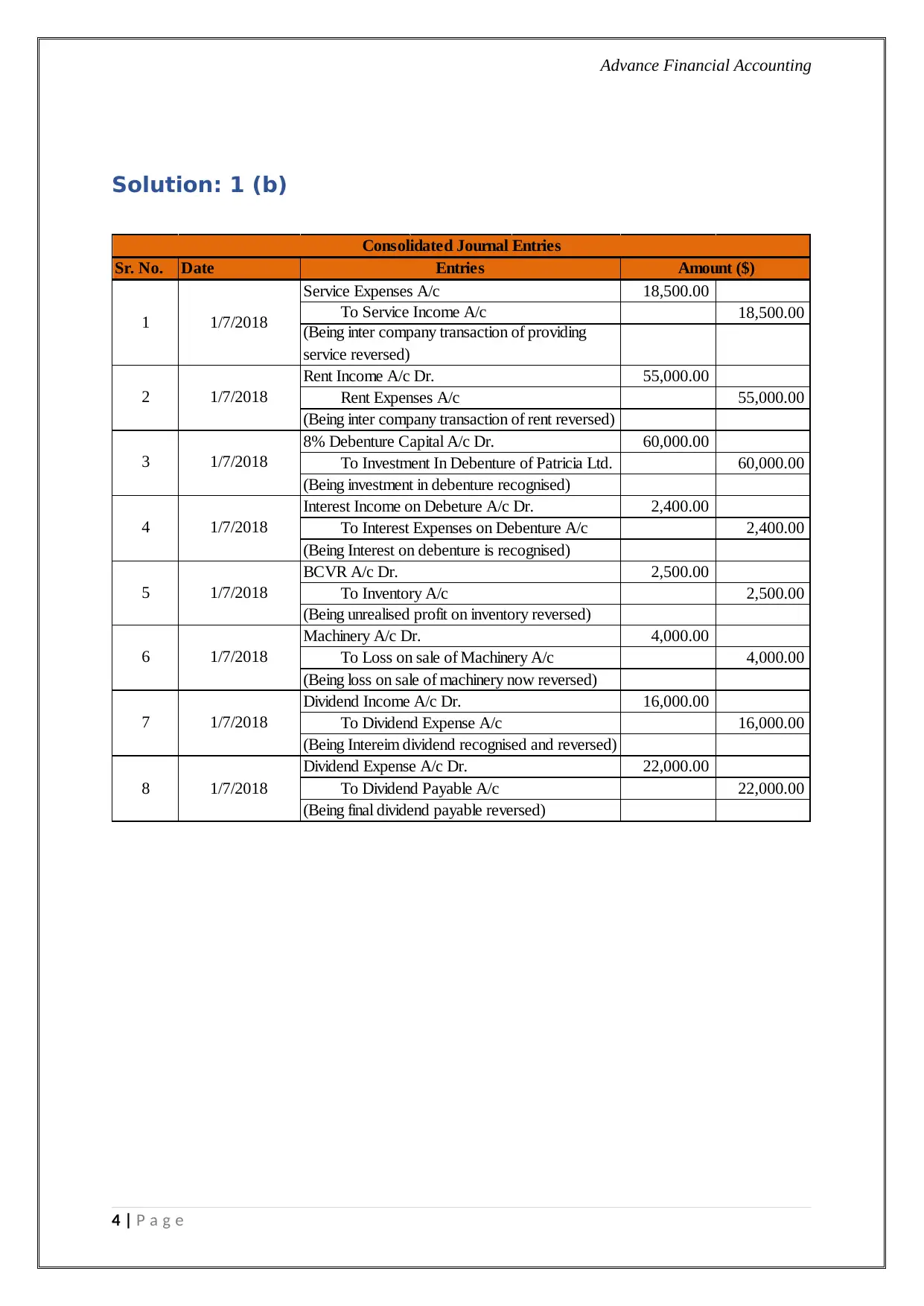

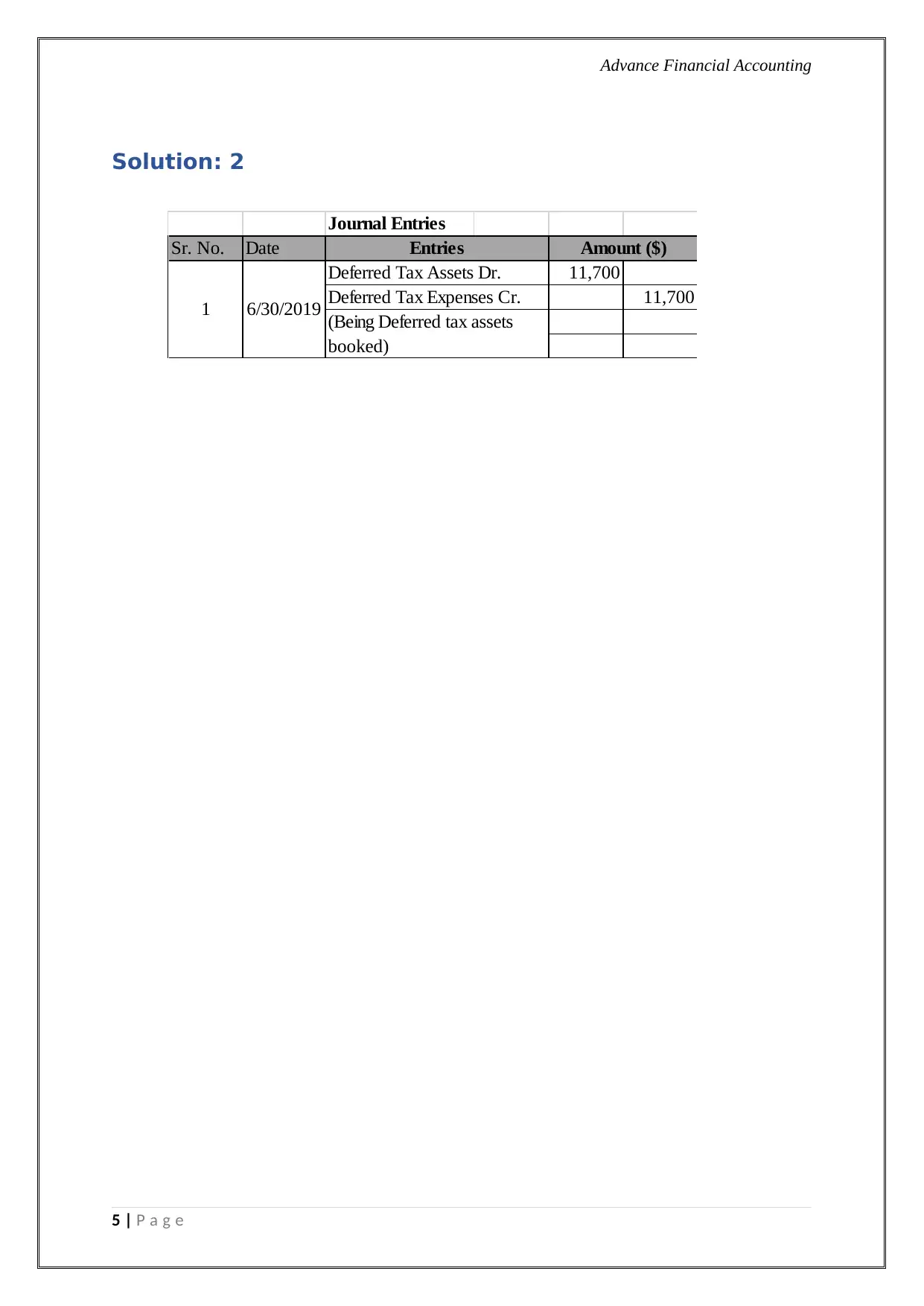

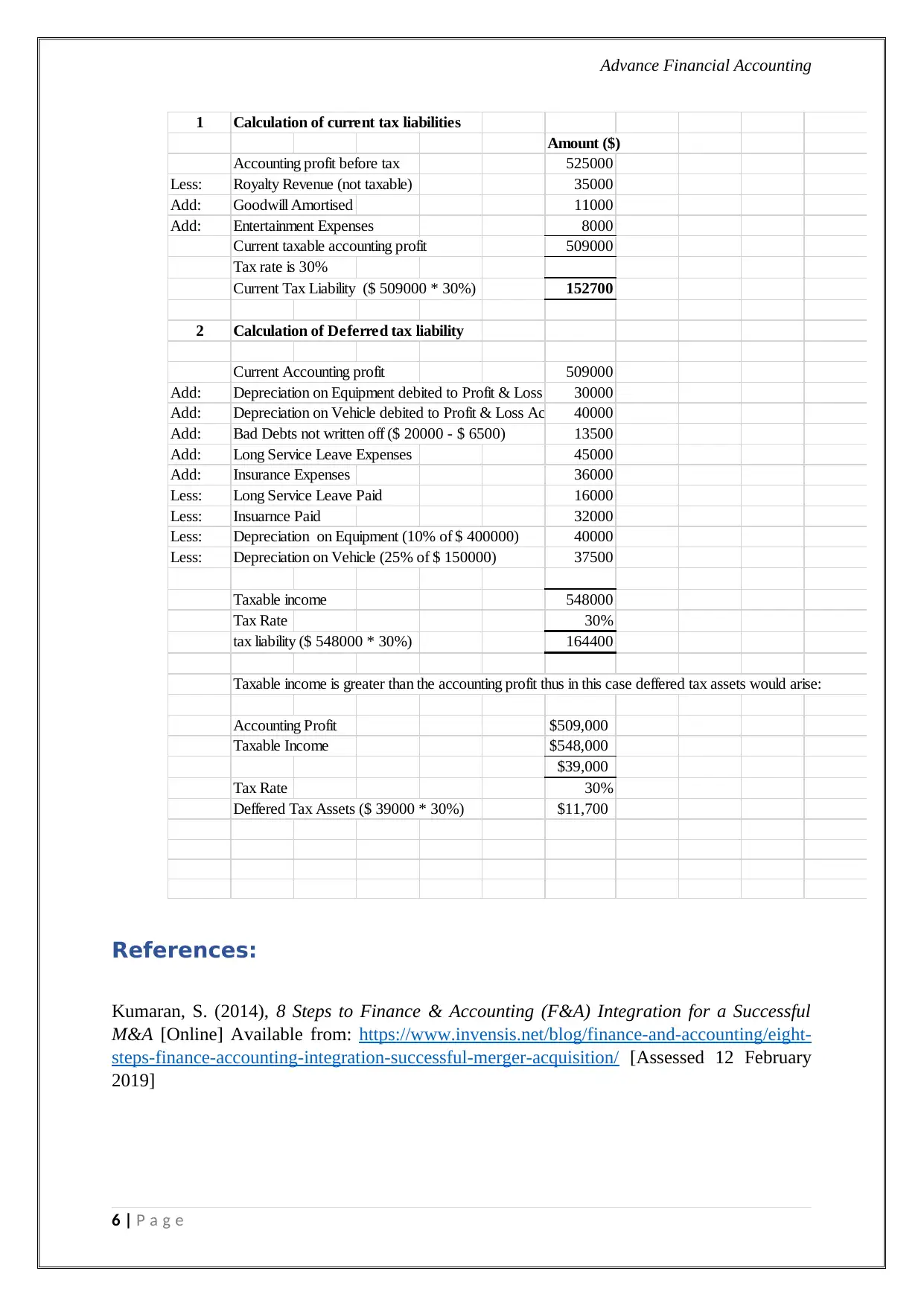

This document presents a solution to an advanced financial accounting assignment involving the consolidation of Jenny Ltd. and Patricia Ltd. following Jenny Ltd.'s acquisition of Patricia Ltd.'s shares. The solution includes consolidated journal entries for the amalgamation, fair value adjustments of assets, and the elimination of inter-company transactions such as services, rent, debentures, inventory sales, machinery sales, and dividends. It also addresses the calculation of current and deferred tax liabilities, considering items like royalty revenue, goodwill amortization, entertainment expenses, depreciation, bad debts, and long service leave. The analysis incorporates acquisition details, share capital, retained earnings, general reserves, and goodwill calculations to provide a comprehensive financial consolidation.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.