Holmes Institute HA3011: Advanced Financial Accounting Assignment

VerifiedAdded on 2022/11/13

|10

|3173

|325

Homework Assignment

AI Summary

This assignment solution explores advanced financial accounting principles and their application within the context of Bingo Industries Limited. It delves into key accounting concepts such as going concern, consistency, and accrual accounting, explaining their significance in financial reporting. The document outlines various accounting concepts including revenue recognition, conservatism, cost, economic entity, matching principle, materiality, reliability, and time period concepts. It then examines the conceptual framework and the issue of measurement, specifically addressing the adoption of AASB 9 for financial instruments and its impact. The assignment provides insights into revenue recognition, net finance costs, and trade receivables, along with a discussion on the measurement and recognition of these items. The solution adheres to Australian accounting standards and includes examples to illustrate the practical application of accounting concepts.

Advanced Financial Accounting

T12019

T12019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Structure...................................................................................................................... 2

Introduction.................................................................................................................. 2

Description of Accounting Concepts.............................................................................2

Conceptual Framework and the issue of measurement...............................................4

Fundamental Qualitative Characteristics – Understanding of relevance and

Representational Faithfulness...................................................................................... 6

Conclusion.................................................................................................................... 7

References................................................................................................................... 8

1

Structure...................................................................................................................... 2

Introduction.................................................................................................................. 2

Description of Accounting Concepts.............................................................................2

Conceptual Framework and the issue of measurement...............................................4

Fundamental Qualitative Characteristics – Understanding of relevance and

Representational Faithfulness...................................................................................... 6

Conclusion.................................................................................................................... 7

References................................................................................................................... 8

1

Structure

This assignment covers the accounting concepts or accounting principles used by management of

Bingo industries limited in preparation of its financial statement. Accounting concepts and

methods used by the company are explained in detail in the later part of this assignment with

suitable examples wherever required. Importance of financial reporting framework in preparation

and presentation of financial statement is explained to the users and stakeholders with relevant

and required information. Various assumptions and estimates are used by the company in

preparation of financial statement by giving proper explanation of basis of such assumptions and

estimates made. Conclusion is made on the basis of company’s usage of concepts or methods of

accounting in preparation of its books of accounts following regulatory framework of accounting.

Introduction

Books of accounts of company are made as per generally accepted accounting principles

(GAAP). Management (Board of directors) are accountable for the preparation of its financial

statements that gives fair view and complied with Australian accounting standards and

Corporation Act, 2011. Its books of accounts are prepared on the basis of accrual concept of

accounting and that method is followed on the regular basis by the company (Alexander, 2016).

Majorly three concepts of accounting like accrual concept, going concern and consistency are

followed regularly by bingo industries ltd. as per reporting framework. Bingo industries ltd

prepares its annual report to ensure that the desired expectations of stakeholders are met.

Generally stakeholders are of two types first is Internal stakeholders and second is External

stakeholders. Internal stakeholders are internally connected with the operations of the company

whereas external stakeholders are not internally connected or they are not involved in the

operations of the company. Internal stakeholders includes managers, employees, board of

directors, investors in the contrary external stakeholders includes financial institution such as

banks, government agencies, customers, suppliers. After the audit gets completed annual report of

the company is circulated to the various stakeholders to inform them regarding the company’s

operations (Bizfluent, 2017).

Description of Accounting

Concepts

There are mainly three concepts of accounting which is mandatory for the company to follow such

concepts and apply those concepts of accounting in the preparation of its books of accounts.

Those concepts are going concern, consistency and accrual. Disclosure of such accounting

concepts are not required in the financial statement of the company if they are regularly applied

by the company but disclosure is must in financial statement of the company if such accounting

concepts are not regularly applied or there is some deviation in accounting concepts adopted by

company (Bumgarner & Vasarhelyi, 2018).

Going concern accounting concept presumes that company will carry on its operations or

business for very long period i.e. an foreseeable future, in other way it can be said that entity will

not be forced to cease its business unless there is no possible option other than its liquidation

where company can’t continue its operations. Thus, in preparation of financial statement it is

assumed that entity has followed the going concern concept and if there is any risk of continuity

2

This assignment covers the accounting concepts or accounting principles used by management of

Bingo industries limited in preparation of its financial statement. Accounting concepts and

methods used by the company are explained in detail in the later part of this assignment with

suitable examples wherever required. Importance of financial reporting framework in preparation

and presentation of financial statement is explained to the users and stakeholders with relevant

and required information. Various assumptions and estimates are used by the company in

preparation of financial statement by giving proper explanation of basis of such assumptions and

estimates made. Conclusion is made on the basis of company’s usage of concepts or methods of

accounting in preparation of its books of accounts following regulatory framework of accounting.

Introduction

Books of accounts of company are made as per generally accepted accounting principles

(GAAP). Management (Board of directors) are accountable for the preparation of its financial

statements that gives fair view and complied with Australian accounting standards and

Corporation Act, 2011. Its books of accounts are prepared on the basis of accrual concept of

accounting and that method is followed on the regular basis by the company (Alexander, 2016).

Majorly three concepts of accounting like accrual concept, going concern and consistency are

followed regularly by bingo industries ltd. as per reporting framework. Bingo industries ltd

prepares its annual report to ensure that the desired expectations of stakeholders are met.

Generally stakeholders are of two types first is Internal stakeholders and second is External

stakeholders. Internal stakeholders are internally connected with the operations of the company

whereas external stakeholders are not internally connected or they are not involved in the

operations of the company. Internal stakeholders includes managers, employees, board of

directors, investors in the contrary external stakeholders includes financial institution such as

banks, government agencies, customers, suppliers. After the audit gets completed annual report of

the company is circulated to the various stakeholders to inform them regarding the company’s

operations (Bizfluent, 2017).

Description of Accounting

Concepts

There are mainly three concepts of accounting which is mandatory for the company to follow such

concepts and apply those concepts of accounting in the preparation of its books of accounts.

Those concepts are going concern, consistency and accrual. Disclosure of such accounting

concepts are not required in the financial statement of the company if they are regularly applied

by the company but disclosure is must in financial statement of the company if such accounting

concepts are not regularly applied or there is some deviation in accounting concepts adopted by

company (Bumgarner & Vasarhelyi, 2018).

Going concern accounting concept presumes that company will carry on its operations or

business for very long period i.e. an foreseeable future, in other way it can be said that entity will

not be forced to cease its business unless there is no possible option other than its liquidation

where company can’t continue its operations. Thus, in preparation of financial statement it is

assumed that entity has followed the going concern concept and if there is any risk of continuity

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of business then it proper disclosure is essential in the financial statement. It is the accountability

of management to assess whether the entity will run its operations for a very long time following

going concern requirement (Defond & Lennox, 2017). In Bingo Ltd., there is no question on

going concern however, there could be some conditions or events arising in future which may

cause Bingo ltd to rethink on its going concern assumption.

Consistency concept of accounting is based on the idea that accounting method once adopted by

an entity shall be followed or applied in future also consistently. However, method of accounting

could be changed on occurrence of any of the three events like: a.) Accounting method could be

changed or altered if it is required by law or regulation b.) Method of accounting could be

changed due to change in accounting standards c.) Accounting principle or method of accounting

could be changed for better presentation of financial report. In case of Bingo Ltd. this concept of

accounting is regularly followed (Vieira, et al., 2017).

Accrual concepts of accounting is one of the most important accounting concept which explains

that all revenues/income should be recorded in the books as and when the income/revenue is

earned and not at the time when they are actually received in cash in the same way in case of

expenses, expenses should be recorded in books as and when they are incurred not when the

expenses are actually paid. Accrual as an expense which is recognized in the current period for

which bill from vendor is not received or as an income when billing is not made to debtors. Thus,

another affect of accruals in the profit &loss can be either assets or liabilities in the balance sheet.

Accrual concept of accounting is regularly followed by the company Bingo Ltd. thus it doesn’t

disclose this while preparing its financial report (Mubako & O'Donnell, 2018).

Besides three accounting concepts explained above there are other various accounting concepts

also which are equally important for the company to adopt and follow such accounting concepts.

Other accounting concepts are Revenue recognition, Conservatism, Cost, Economic entity

concept, Matching principle, Materiality, Reliability, Time period concept. These are explained

below with example wherever required:

Revenue recognition concept explains that revenue should be recognized in the company’s

books if it is certain that revenues will be realized and earned. Revenues are considered to be

earned only when goods are transferred to the party along with the risk and rewards also gets

transferred or services are rendered without considering the fact that when cash is actually

received by the entity. AASB 15 deals with revenue from contracts (Kachelmeier, et al., 2018).

AASB 15 is based on the principle that company shall recognise revenue related to the transfer of

goods or services only when control of the goods or services gets transfeered to the customer.

Group has reviewed few samples of sales contracts to analyze if there is any potential impact

from application of AASB15.

Conservatism concept says that all expenses and liabilities relating to company shall be

recognized in the books of accounts as early as possible, but income and assets shall be recorded

only if there is certainity or surety that such income or revenue will be received. This concept of

accounting is based on the idea that all the losses should be recognized first. Conservatism

concept is strictly follwed by Bingo ltd (Fukukawa & Mock, 2011).

Reliabilty Concept of accounting is based on the idea that only those transactions to be

recognized in the books of company which can be proved easily. Example, bill from the vendor

3

of management to assess whether the entity will run its operations for a very long time following

going concern requirement (Defond & Lennox, 2017). In Bingo Ltd., there is no question on

going concern however, there could be some conditions or events arising in future which may

cause Bingo ltd to rethink on its going concern assumption.

Consistency concept of accounting is based on the idea that accounting method once adopted by

an entity shall be followed or applied in future also consistently. However, method of accounting

could be changed on occurrence of any of the three events like: a.) Accounting method could be

changed or altered if it is required by law or regulation b.) Method of accounting could be

changed due to change in accounting standards c.) Accounting principle or method of accounting

could be changed for better presentation of financial report. In case of Bingo Ltd. this concept of

accounting is regularly followed (Vieira, et al., 2017).

Accrual concepts of accounting is one of the most important accounting concept which explains

that all revenues/income should be recorded in the books as and when the income/revenue is

earned and not at the time when they are actually received in cash in the same way in case of

expenses, expenses should be recorded in books as and when they are incurred not when the

expenses are actually paid. Accrual as an expense which is recognized in the current period for

which bill from vendor is not received or as an income when billing is not made to debtors. Thus,

another affect of accruals in the profit &loss can be either assets or liabilities in the balance sheet.

Accrual concept of accounting is regularly followed by the company Bingo Ltd. thus it doesn’t

disclose this while preparing its financial report (Mubako & O'Donnell, 2018).

Besides three accounting concepts explained above there are other various accounting concepts

also which are equally important for the company to adopt and follow such accounting concepts.

Other accounting concepts are Revenue recognition, Conservatism, Cost, Economic entity

concept, Matching principle, Materiality, Reliability, Time period concept. These are explained

below with example wherever required:

Revenue recognition concept explains that revenue should be recognized in the company’s

books if it is certain that revenues will be realized and earned. Revenues are considered to be

earned only when goods are transferred to the party along with the risk and rewards also gets

transferred or services are rendered without considering the fact that when cash is actually

received by the entity. AASB 15 deals with revenue from contracts (Kachelmeier, et al., 2018).

AASB 15 is based on the principle that company shall recognise revenue related to the transfer of

goods or services only when control of the goods or services gets transfeered to the customer.

Group has reviewed few samples of sales contracts to analyze if there is any potential impact

from application of AASB15.

Conservatism concept says that all expenses and liabilities relating to company shall be

recognized in the books of accounts as early as possible, but income and assets shall be recorded

only if there is certainity or surety that such income or revenue will be received. This concept of

accounting is based on the idea that all the losses should be recognized first. Conservatism

concept is strictly follwed by Bingo ltd (Fukukawa & Mock, 2011).

Reliabilty Concept of accounting is based on the idea that only those transactions to be

recognized in the books of company which can be proved easily. Example, bill from the vendor

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

can be considered as a proof that expenses are recognized. Reliabilty concept is very much helpful

for the auditors which helps an auditor to gather some evidences.

Cost Method of accounting explains that assets and liabilites must be recorded on cost not on fair

value or market value. However, in contast to that there are few accounting standards which

requires assets and liabilities to be recorded at fair values. Bingo Ltd. consistently applies this

principle of accounting except in case where accounting standard are required to be follwed then

assets and liabilities are recorded at fair value instead of cost (Kew & Stredwick, 2017).

Full disclosure principle is based on the concept that company shall cover all the relevant and

important information while preparation of financial report as it helps the readers of financial

statements such as investors, financial institutions, vendors etc. gets the clear picture and

understanding of the financial report. Full disclosure is made by Bingo Ltd along with Financial

statement by correctly following the full disclosure concept.

Matching Principle explains that when revenue is recognized in the books of accounts all

expenses related to such revenue or income shall also be recognized at the same point time.

Example when income from sale of goods is recorded, at the same time stock is charged to cost of

goods sold. Those entity uses matching concept who is using accrual concept of accountin instead

following cash method. Entity who follows cash method for the accounting purpose they don’t

follow matching concept. Bingo Ltd uses accrual method for the purpose of accounting thus it

also comply with the matching principle of accounting (Jefferson, 2017).

Monetary unit concept is based on the concept that company shall recognize only that

transactions which can be presented in the form of value or sume unit of currency. For example ,

purchase of fixed assets can be easily recorded or recognized in the books of company since it is

in the form of unit of currency, opposite to that value of controls in the entity can’t be recorded in

the books because that is not in the form of value of currency.

Time period concept says that entity shall show oearations results within a prescribed time line.

This concept is based on the idea that while showing figures of current period in the financial

statement, corresponding figures of previous period should also be shown as comparison to

current period as it helps a lot for making trend analisys. It shows that the company is very

efficient and follow the strict deadlines (Linden & Freeman, 2017).

Conceptual Framework and the

issue of measurement

Financial statements of Bingo Limited has been prepared in accordance with the Corporation Act,

2001, Interpretations and accounting standards and in compliance with relevant laws and

regulations. Financial statements includes Consolidated financial statement of the group. Bingo ltd

is a profit entity for the purpose of preparation of consolidated financial statement. Basis of

consolidated financial statement is historical cost . All figures in the financial statement are in

Australian dollars.Items of financial statement is correctly measured in accordance with

Australian accounting standards.

Measurement of Financial Instruments :Earlier AASB 139 was used for recognition and

measurement of financial instruments for group’s consolidated financial instrument. Now AASB

4

for the auditors which helps an auditor to gather some evidences.

Cost Method of accounting explains that assets and liabilites must be recorded on cost not on fair

value or market value. However, in contast to that there are few accounting standards which

requires assets and liabilities to be recorded at fair values. Bingo Ltd. consistently applies this

principle of accounting except in case where accounting standard are required to be follwed then

assets and liabilities are recorded at fair value instead of cost (Kew & Stredwick, 2017).

Full disclosure principle is based on the concept that company shall cover all the relevant and

important information while preparation of financial report as it helps the readers of financial

statements such as investors, financial institutions, vendors etc. gets the clear picture and

understanding of the financial report. Full disclosure is made by Bingo Ltd along with Financial

statement by correctly following the full disclosure concept.

Matching Principle explains that when revenue is recognized in the books of accounts all

expenses related to such revenue or income shall also be recognized at the same point time.

Example when income from sale of goods is recorded, at the same time stock is charged to cost of

goods sold. Those entity uses matching concept who is using accrual concept of accountin instead

following cash method. Entity who follows cash method for the accounting purpose they don’t

follow matching concept. Bingo Ltd uses accrual method for the purpose of accounting thus it

also comply with the matching principle of accounting (Jefferson, 2017).

Monetary unit concept is based on the concept that company shall recognize only that

transactions which can be presented in the form of value or sume unit of currency. For example ,

purchase of fixed assets can be easily recorded or recognized in the books of company since it is

in the form of unit of currency, opposite to that value of controls in the entity can’t be recorded in

the books because that is not in the form of value of currency.

Time period concept says that entity shall show oearations results within a prescribed time line.

This concept is based on the idea that while showing figures of current period in the financial

statement, corresponding figures of previous period should also be shown as comparison to

current period as it helps a lot for making trend analisys. It shows that the company is very

efficient and follow the strict deadlines (Linden & Freeman, 2017).

Conceptual Framework and the

issue of measurement

Financial statements of Bingo Limited has been prepared in accordance with the Corporation Act,

2001, Interpretations and accounting standards and in compliance with relevant laws and

regulations. Financial statements includes Consolidated financial statement of the group. Bingo ltd

is a profit entity for the purpose of preparation of consolidated financial statement. Basis of

consolidated financial statement is historical cost . All figures in the financial statement are in

Australian dollars.Items of financial statement is correctly measured in accordance with

Australian accounting standards.

Measurement of Financial Instruments :Earlier AASB 139 was used for recognition and

measurement of financial instruments for group’s consolidated financial instrument. Now AASB

4

139 is replaced by AASB 9 which covers a new measurement and classification approach for

financial assets (Lavassani & Movahedi, 2017). There are three categories for classification of

financial assets : a.) Amortized cost measurement b.)Fair value through OCI c.)Fair value through

P &L. Earlier as per AASB 139 there was different classification category for financial assets.

Following impacts can be expected from the group on adoption of AASB 9:

a.) No significant impact on measuremant and classification of its financial instruments.

b.) It was decided that impairment losses including trade receivables are measured using

expected credit loss model rather than incurred credit losses.

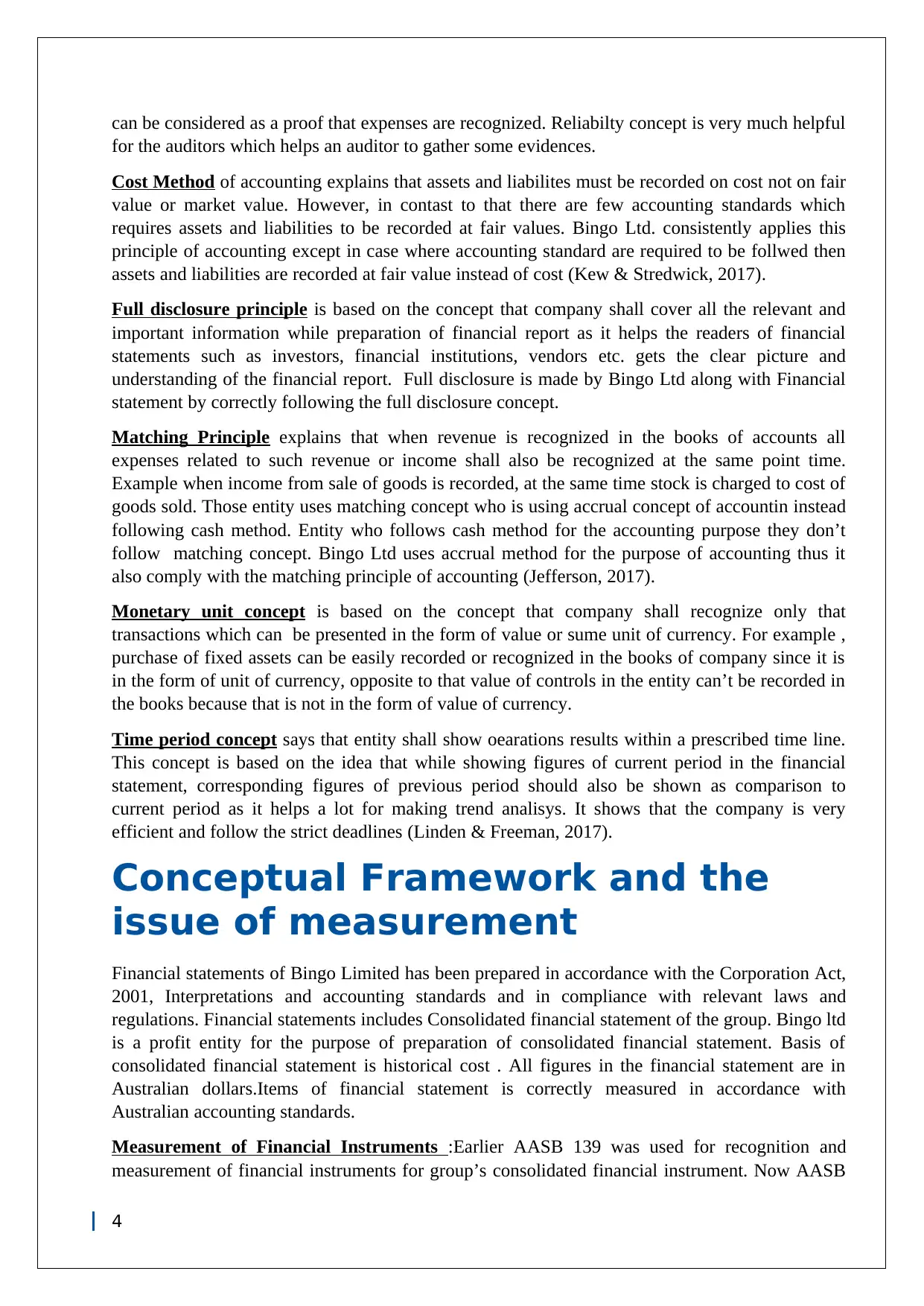

Revenue recognition and measurement : Measurement of revenue is made at fair value of the

consideration whether received or receivabl. If there are any returns from the customers, rebates

or other similar allowances then it is reduced from the revenue of the group. Revenues are

recognized by Bingo Ltd. when the bins are taken from the customers and waste is received at the

various recycling centres. In case of bins which are manufactured, revenue arising from sale of

manufactured bins is recognized in the books only when the significant risk and reward of goods

is passed on to the buyer (Meroño-Cerdán, et al., 2017).

Table showing measurement and recognition of revenue and other income:

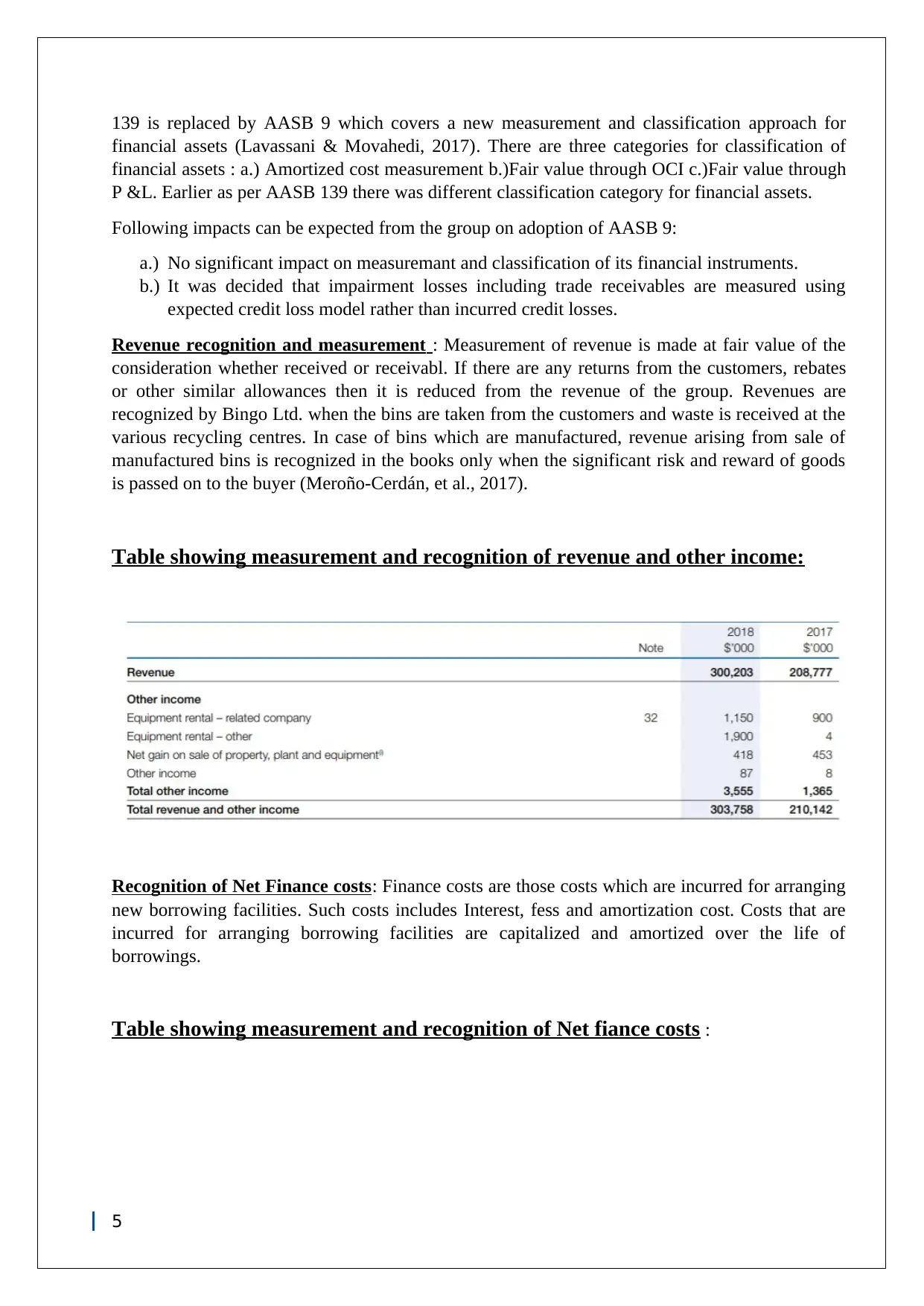

Recognition of Net Finance costs: Finance costs are those costs which are incurred for arranging

new borrowing facilities. Such costs includes Interest, fess and amortization cost. Costs that are

incurred for arranging borrowing facilities are capitalized and amortized over the life of

borrowings.

Table showing measurement and recognition of Net fiance costs :

5

financial assets (Lavassani & Movahedi, 2017). There are three categories for classification of

financial assets : a.) Amortized cost measurement b.)Fair value through OCI c.)Fair value through

P &L. Earlier as per AASB 139 there was different classification category for financial assets.

Following impacts can be expected from the group on adoption of AASB 9:

a.) No significant impact on measuremant and classification of its financial instruments.

b.) It was decided that impairment losses including trade receivables are measured using

expected credit loss model rather than incurred credit losses.

Revenue recognition and measurement : Measurement of revenue is made at fair value of the

consideration whether received or receivabl. If there are any returns from the customers, rebates

or other similar allowances then it is reduced from the revenue of the group. Revenues are

recognized by Bingo Ltd. when the bins are taken from the customers and waste is received at the

various recycling centres. In case of bins which are manufactured, revenue arising from sale of

manufactured bins is recognized in the books only when the significant risk and reward of goods

is passed on to the buyer (Meroño-Cerdán, et al., 2017).

Table showing measurement and recognition of revenue and other income:

Recognition of Net Finance costs: Finance costs are those costs which are incurred for arranging

new borrowing facilities. Such costs includes Interest, fess and amortization cost. Costs that are

incurred for arranging borrowing facilities are capitalized and amortized over the life of

borrowings.

Table showing measurement and recognition of Net fiance costs :

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

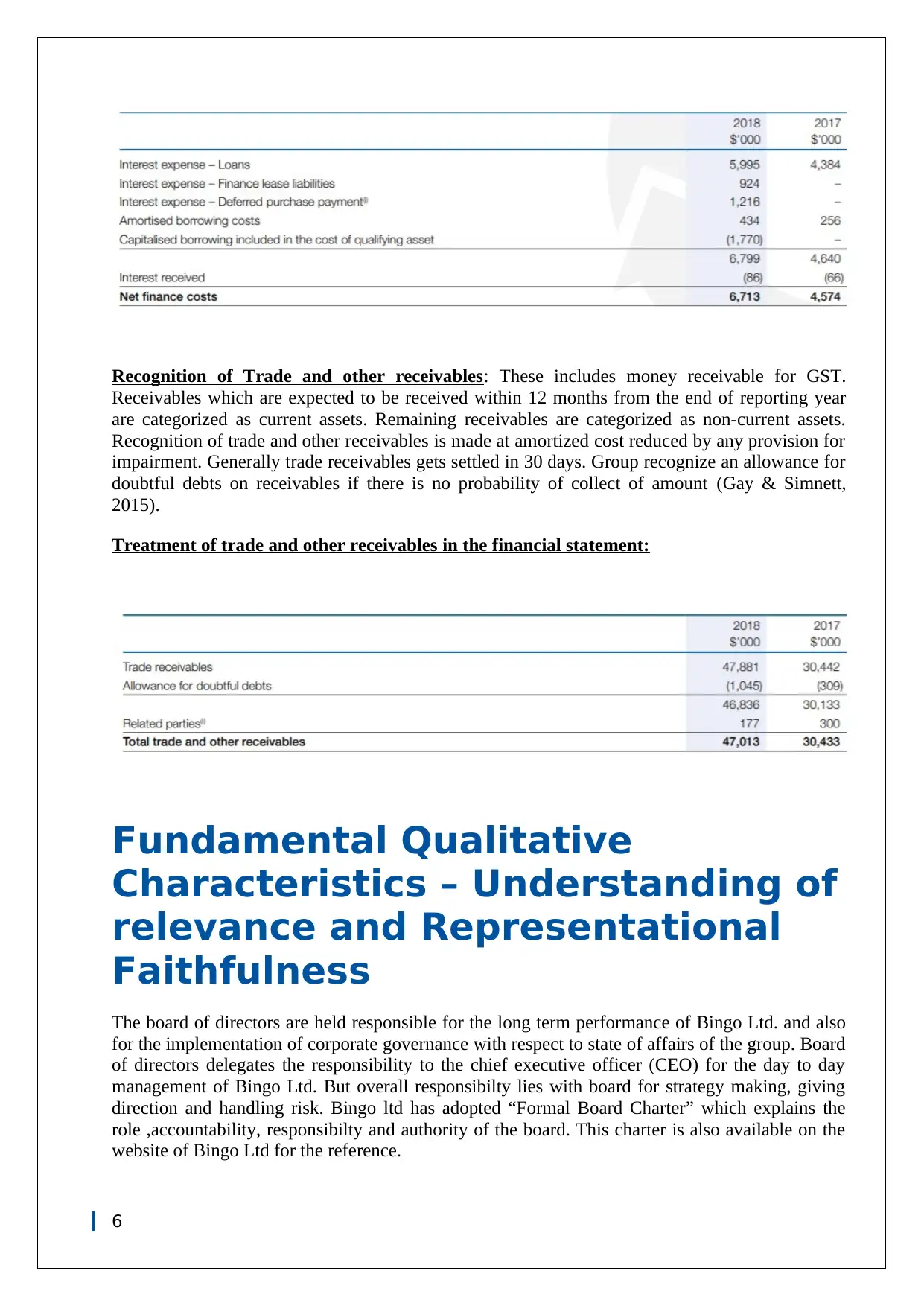

Recognition of Trade and other receivables: These includes money receivable for GST.

Receivables which are expected to be received within 12 months from the end of reporting year

are categorized as current assets. Remaining receivables are categorized as non-current assets.

Recognition of trade and other receivables is made at amortized cost reduced by any provision for

impairment. Generally trade receivables gets settled in 30 days. Group recognize an allowance for

doubtful debts on receivables if there is no probability of collect of amount (Gay & Simnett,

2015).

Treatment of trade and other receivables in the financial statement:

Fundamental Qualitative

Characteristics – Understanding of

relevance and Representational

Faithfulness

The board of directors are held responsible for the long term performance of Bingo Ltd. and also

for the implementation of corporate governance with respect to state of affairs of the group. Board

of directors delegates the responsibility to the chief executive officer (CEO) for the day to day

management of Bingo Ltd. But overall responsibilty lies with board for strategy making, giving

direction and handling risk. Bingo ltd has adopted “Formal Board Charter” which explains the

role ,accountability, responsibilty and authority of the board. This charter is also available on the

website of Bingo Ltd for the reference.

6

Receivables which are expected to be received within 12 months from the end of reporting year

are categorized as current assets. Remaining receivables are categorized as non-current assets.

Recognition of trade and other receivables is made at amortized cost reduced by any provision for

impairment. Generally trade receivables gets settled in 30 days. Group recognize an allowance for

doubtful debts on receivables if there is no probability of collect of amount (Gay & Simnett,

2015).

Treatment of trade and other receivables in the financial statement:

Fundamental Qualitative

Characteristics – Understanding of

relevance and Representational

Faithfulness

The board of directors are held responsible for the long term performance of Bingo Ltd. and also

for the implementation of corporate governance with respect to state of affairs of the group. Board

of directors delegates the responsibility to the chief executive officer (CEO) for the day to day

management of Bingo Ltd. But overall responsibilty lies with board for strategy making, giving

direction and handling risk. Bingo ltd has adopted “Formal Board Charter” which explains the

role ,accountability, responsibilty and authority of the board. This charter is also available on the

website of Bingo Ltd for the reference.

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial information of the company is very much important to various stakeholder such as

shareholders who are the owners of the company who on the basis of relevance of financial

position of the company considers for investment (Sonu, et al., 2017).

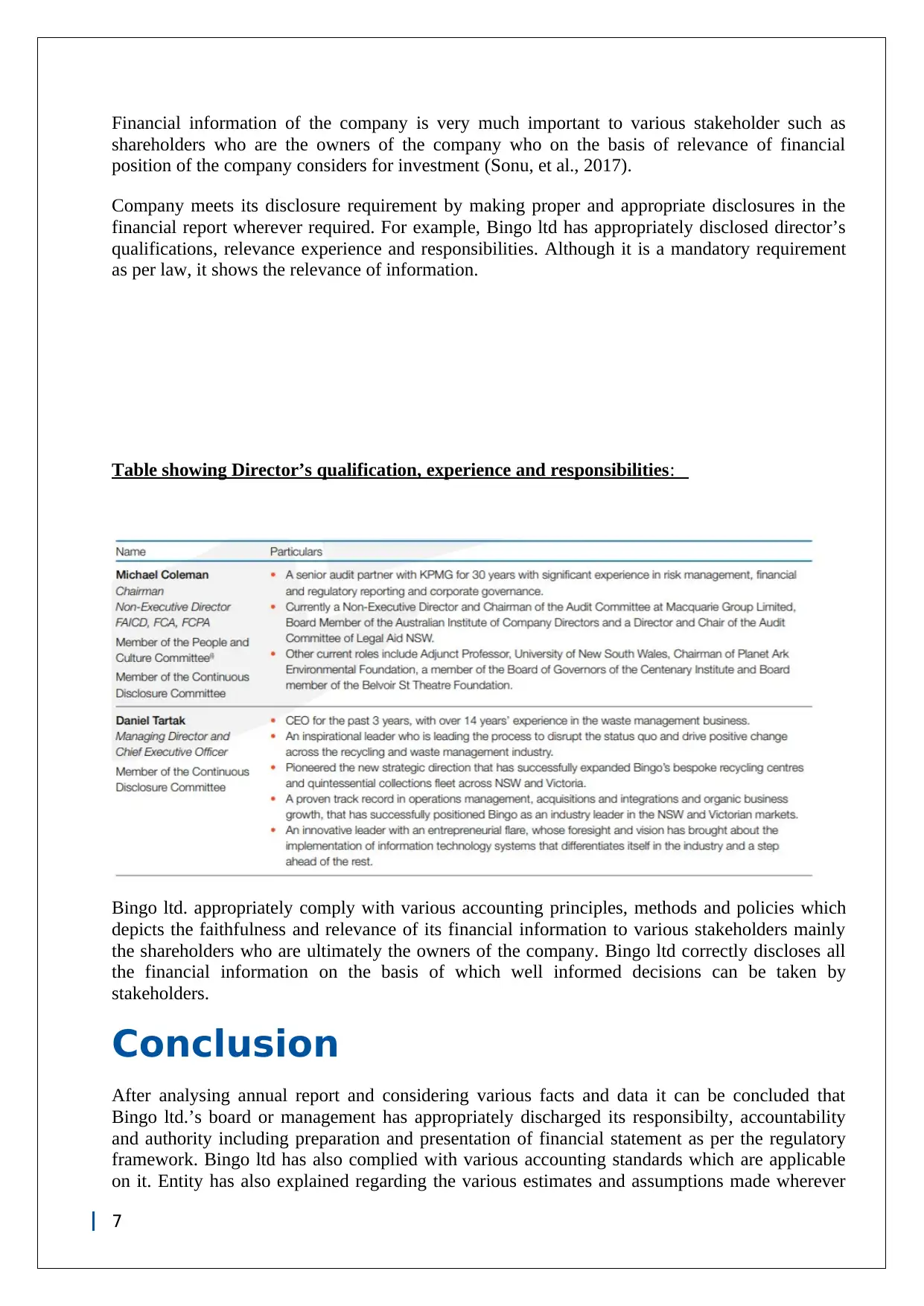

Company meets its disclosure requirement by making proper and appropriate disclosures in the

financial report wherever required. For example, Bingo ltd has appropriately disclosed director’s

qualifications, relevance experience and responsibilities. Although it is a mandatory requirement

as per law, it shows the relevance of information.

Table showing Director’s qualification, experience and responsibilities:

Bingo ltd. appropriately comply with various accounting principles, methods and policies which

depicts the faithfulness and relevance of its financial information to various stakeholders mainly

the shareholders who are ultimately the owners of the company. Bingo ltd correctly discloses all

the financial information on the basis of which well informed decisions can be taken by

stakeholders.

Conclusion

After analysing annual report and considering various facts and data it can be concluded that

Bingo ltd.’s board or management has appropriately discharged its responsibilty, accountability

and authority including preparation and presentation of financial statement as per the regulatory

framework. Bingo ltd has also complied with various accounting standards which are applicable

on it. Entity has also explained regarding the various estimates and assumptions made wherever

7

shareholders who are the owners of the company who on the basis of relevance of financial

position of the company considers for investment (Sonu, et al., 2017).

Company meets its disclosure requirement by making proper and appropriate disclosures in the

financial report wherever required. For example, Bingo ltd has appropriately disclosed director’s

qualifications, relevance experience and responsibilities. Although it is a mandatory requirement

as per law, it shows the relevance of information.

Table showing Director’s qualification, experience and responsibilities:

Bingo ltd. appropriately comply with various accounting principles, methods and policies which

depicts the faithfulness and relevance of its financial information to various stakeholders mainly

the shareholders who are ultimately the owners of the company. Bingo ltd correctly discloses all

the financial information on the basis of which well informed decisions can be taken by

stakeholders.

Conclusion

After analysing annual report and considering various facts and data it can be concluded that

Bingo ltd.’s board or management has appropriately discharged its responsibilty, accountability

and authority including preparation and presentation of financial statement as per the regulatory

framework. Bingo ltd has also complied with various accounting standards which are applicable

on it. Entity has also explained regarding the various estimates and assumptions made wherever

7

required with proper justification of the assumption made. Deloitte has successfully completed the

audit of financial report of Bingo industries limited and its subsidiaries by forming an unqualified

opinion on state of affairs of the company. Auditor has also appropriately disclosed the basis of

opinion formed.

References

Alexander, F., 2016. The Changing Face of Accountability. The Journal of Higher Education, 71(4), pp.

411-431.

Bizfluent, 2017. Advantages & Disadvantages of Internal Control. [Online]

Available at: https://bizfluent.com/info-8064250-advantages-disadvantages-internal-control.html

Bumgarner, N. & Vasarhelyi, M., 2018. Continuous auditing—a new view.. Continuous Auditing: Theory

and Application, 20(1), pp. 7-51.

Defond, M. & Lennox, C., 2017. Do PCAOB Inspections Improve the Quality of Internal Control Audits?.

Journal of Accounting Research, 55(3), pp. 591-627.

Fukukawa, H. & Mock, T., 2011. Audit risk assessments using belief versus probability. Auditing: A

Journal of Practice & Theory, 30(1), pp. 75-99.

Gay, G. & Simnett, R., 2015. Auditing and assurance services in Australia. s.l.:McGraw-Hill Education

Australia.

Jefferson, M., 2017. Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland.

Technological Forecasting and Social Change, pp. 353-354.

Kachelmeier, S., Schmidt, J. & Valentine, K., 2018. The disclaimer effect of disclosing critical audit

matters in the auditor’s report. SSRN, 2(1), pp. 1-39.

Kew, J. & Stredwick, J., 2017. Business Environment: Managing in a Strategic Context. 2nd ed. London:

Chartered Institute of Personnel and Development.

Lavassani, K. & Movahedi, B., 2017. Applications Driven Information Systems: Beyond Networks toward

Business Ecosystems. International Journal of Innovation in the Digital Economy.

Linden, B. & Freeman, R., 2017. Profit and Other Values: Thick Evaluation in Decision Making. Business

Ethics Quarterly, 27(3), pp. 353-379.

Meroño-Cerdán, A., Lopez-Nicolas, C. & Molina-Castillo, F., 2017. Risk aversion, innovation and

performance in family firms. Economics of Innovation and new technology, pp. 1-15.

8

audit of financial report of Bingo industries limited and its subsidiaries by forming an unqualified

opinion on state of affairs of the company. Auditor has also appropriately disclosed the basis of

opinion formed.

References

Alexander, F., 2016. The Changing Face of Accountability. The Journal of Higher Education, 71(4), pp.

411-431.

Bizfluent, 2017. Advantages & Disadvantages of Internal Control. [Online]

Available at: https://bizfluent.com/info-8064250-advantages-disadvantages-internal-control.html

Bumgarner, N. & Vasarhelyi, M., 2018. Continuous auditing—a new view.. Continuous Auditing: Theory

and Application, 20(1), pp. 7-51.

Defond, M. & Lennox, C., 2017. Do PCAOB Inspections Improve the Quality of Internal Control Audits?.

Journal of Accounting Research, 55(3), pp. 591-627.

Fukukawa, H. & Mock, T., 2011. Audit risk assessments using belief versus probability. Auditing: A

Journal of Practice & Theory, 30(1), pp. 75-99.

Gay, G. & Simnett, R., 2015. Auditing and assurance services in Australia. s.l.:McGraw-Hill Education

Australia.

Jefferson, M., 2017. Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland.

Technological Forecasting and Social Change, pp. 353-354.

Kachelmeier, S., Schmidt, J. & Valentine, K., 2018. The disclaimer effect of disclosing critical audit

matters in the auditor’s report. SSRN, 2(1), pp. 1-39.

Kew, J. & Stredwick, J., 2017. Business Environment: Managing in a Strategic Context. 2nd ed. London:

Chartered Institute of Personnel and Development.

Lavassani, K. & Movahedi, B., 2017. Applications Driven Information Systems: Beyond Networks toward

Business Ecosystems. International Journal of Innovation in the Digital Economy.

Linden, B. & Freeman, R., 2017. Profit and Other Values: Thick Evaluation in Decision Making. Business

Ethics Quarterly, 27(3), pp. 353-379.

Meroño-Cerdán, A., Lopez-Nicolas, C. & Molina-Castillo, F., 2017. Risk aversion, innovation and

performance in family firms. Economics of Innovation and new technology, pp. 1-15.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Mubako, G. & O'Donnell, E., 2018. Effect of fraud risk assessments on auditor skepticism: Unintended

consequences on evidence evaluation. International Journal of Auditing, 22(1), pp. 55-64.

Sonu, C., Ahn, H. & Choi, A., 2017. Audit fee pressure and audit risk: evidence from the financial crisis of

2008. Asia-Pacific Journal of Accounting & Economics , 24(1-2), pp. 127-144.

Vieira, R., O’Dwyer, B. & Schneider, R., 2017. Aligning Strategy and Performance Management Systems.

SAGE Journals, 30(1), pp. 23-48.

9

consequences on evidence evaluation. International Journal of Auditing, 22(1), pp. 55-64.

Sonu, C., Ahn, H. & Choi, A., 2017. Audit fee pressure and audit risk: evidence from the financial crisis of

2008. Asia-Pacific Journal of Accounting & Economics , 24(1-2), pp. 127-144.

Vieira, R., O’Dwyer, B. & Schneider, R., 2017. Aligning Strategy and Performance Management Systems.

SAGE Journals, 30(1), pp. 23-48.

9

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.