Holmes Institute HA3011: Advanced Financial Accounting Report Analysis

VerifiedAdded on 2023/03/23

|16

|3343

|59

Report

AI Summary

This report examines the application of accounting concepts and the conceptual framework within Super Cheap Auto, a subsidiary of Super Retail Group. It analyzes the company's adherence to key accounting principles such as the business entity, money measurement, and going concern concepts. The report also explores the mixed measurement model adopted by the company, which integrates historical cost and fair value methods for asset and liability valuation. Furthermore, it discusses the importance of relevance and representational faithfulness in financial statements, referencing the selected company's practices. The report is structured into three parts: an overview of accounting concepts used by Super Retail Group, an analysis of measurement issues using examples from Super Cheap Auto, and an examination of the relevance and representational faithfulness of financial statements. The report concludes by highlighting the significance of the conceptual framework in developing high-quality financial reports and its impact on accounting practices.

Advance Financial Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

This report has been developed for the purpose of examining the accounting concepts and

the conceptual accounting framework principles adoption within an ASX listed entity, that is,

Super Cheap Auto. It has been identified on the basis of the report that the company integrates

the use of going concern, money measurement and going concern concept for development of

financial reports. Also, it has adopted a mixed model of accounting that integrates the use of

historical and fair value method for accounting of its assets and liabilities.

2

This report has been developed for the purpose of examining the accounting concepts and

the conceptual accounting framework principles adoption within an ASX listed entity, that is,

Super Cheap Auto. It has been identified on the basis of the report that the company integrates

the use of going concern, money measurement and going concern concept for development of

financial reports. Also, it has adopted a mixed model of accounting that integrates the use of

historical and fair value method for accounting of its assets and liabilities.

2

Contents

Introduction.................................................................................................................................................4

Part 1: Description of accounting concepts used by Super Retail Group to prepare the annual report......4

Part 2: Issue of Measurement in Accounting with Example from Allocated Company................................9

Part 3: Examination of Relevance and Representational Faithfulness of Financial Statements with the use

of Allocated Company...............................................................................................................................12

Conclusion.................................................................................................................................................14

References.................................................................................................................................................15

3

Introduction.................................................................................................................................................4

Part 1: Description of accounting concepts used by Super Retail Group to prepare the annual report......4

Part 2: Issue of Measurement in Accounting with Example from Allocated Company................................9

Part 3: Examination of Relevance and Representational Faithfulness of Financial Statements with the use

of Allocated Company...............................................................................................................................12

Conclusion.................................................................................................................................................14

References.................................................................................................................................................15

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

The present report has been developed for analyzing and examining the importance of

conceptual framework of accounting for development of high quality financial reports. The

usefulness of relevance and faithful representation of financial information provided by the

conceptual framework has been discussed within the report in context of a selected ASX listed

company. The issue associated with measurement approach used for accounting of assets and

liabilities has also been discussed within the report by citing example from the selected

company. The company selected for analysis purpose is Super Cheap Auto, a subsidiary of Super

Retail Group Limited, an Australian based company that is involved in operating a portfolio of

retail brands across Australia. Super cheap auto subsidiary of the Group is a recognized

automotive retailing company of Australia that is involved in production of auto spares parts and

accessories.

Part 1: Description of accounting concepts used by Super Retail Group to

prepare the annual report

There are different accounting policies and treatments that can be followed to account for

the same financial items. So it becomes necessary to bring some uniformity and consistency in

accounting for the user’s sake so that books of accounts maintained by companies globally can

become comparable. Taking a note to the matter of maintain uniformity and making books of

accounts comparable, international accounting bodies laid down some principles and guidelines

which are to be followed while preparing the accounts of the company. These principles and

guidelines are classified as accounting concepts and conventions. Some of the accounting

concepts are discussed in below points which have been followed by Super Retail Group in its

financial reporting process (Needles, Powers and Crosson, 2013).

Business Entity Concept: Business entity concept assumes the corporate and its owners two

separate entity. Company maintains its corporate veil between owners and company.Which

shows that every single transaction will be done by the company and for the company and not for

any personal gain of the owners and managers. Super Retail Group has shown owner’s capital or

4

The present report has been developed for analyzing and examining the importance of

conceptual framework of accounting for development of high quality financial reports. The

usefulness of relevance and faithful representation of financial information provided by the

conceptual framework has been discussed within the report in context of a selected ASX listed

company. The issue associated with measurement approach used for accounting of assets and

liabilities has also been discussed within the report by citing example from the selected

company. The company selected for analysis purpose is Super Cheap Auto, a subsidiary of Super

Retail Group Limited, an Australian based company that is involved in operating a portfolio of

retail brands across Australia. Super cheap auto subsidiary of the Group is a recognized

automotive retailing company of Australia that is involved in production of auto spares parts and

accessories.

Part 1: Description of accounting concepts used by Super Retail Group to

prepare the annual report

There are different accounting policies and treatments that can be followed to account for

the same financial items. So it becomes necessary to bring some uniformity and consistency in

accounting for the user’s sake so that books of accounts maintained by companies globally can

become comparable. Taking a note to the matter of maintain uniformity and making books of

accounts comparable, international accounting bodies laid down some principles and guidelines

which are to be followed while preparing the accounts of the company. These principles and

guidelines are classified as accounting concepts and conventions. Some of the accounting

concepts are discussed in below points which have been followed by Super Retail Group in its

financial reporting process (Needles, Powers and Crosson, 2013).

Business Entity Concept: Business entity concept assumes the corporate and its owners two

separate entity. Company maintains its corporate veil between owners and company.Which

shows that every single transaction will be done by the company and for the company and not for

any personal gain of the owners and managers. Super Retail Group has shown owner’s capital or

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

share capital under heading equity and liability not as the asset of the company which shows that

it has followed the business entity concept (Mirza and Knorr, 2011).

Money Measurement Concept: As per this concept, entities should record only those

transactions which are in monetary terms and that should also recorded in home currency. Let’s

say a company formed in USA will record its all transactions in US Dollar only and not in any

other currency. On looking at annual report of Super Retail Group all the transactions are

recorded in Australian Dollar and no transaction is recorded as non-monetary. The purpose of

this accounting concept is to help the accountants to know what transactions have to be recorded

and what not to record (Needles, Powers and Crosson, 2013).

Going Concern Concept: This concept provides that entity will continue to run its business for

foreseeable future until there is no plan to shut down the company in near future. This concept is

one of the most important concepts as it makes them determine the method of valuation of

entity’s assets and liabilities. For an example any machinery recorded in the books will be

depreciated over its useful life and not shown as an expense on its purchase. Super Retail Group

has followed the going concern concept as it has deferred many expenses in the form of assets

and liabilities in the balance sheet (Wolk, Dodd and Rozycki, 2016).

5

it has followed the business entity concept (Mirza and Knorr, 2011).

Money Measurement Concept: As per this concept, entities should record only those

transactions which are in monetary terms and that should also recorded in home currency. Let’s

say a company formed in USA will record its all transactions in US Dollar only and not in any

other currency. On looking at annual report of Super Retail Group all the transactions are

recorded in Australian Dollar and no transaction is recorded as non-monetary. The purpose of

this accounting concept is to help the accountants to know what transactions have to be recorded

and what not to record (Needles, Powers and Crosson, 2013).

Going Concern Concept: This concept provides that entity will continue to run its business for

foreseeable future until there is no plan to shut down the company in near future. This concept is

one of the most important concepts as it makes them determine the method of valuation of

entity’s assets and liabilities. For an example any machinery recorded in the books will be

depreciated over its useful life and not shown as an expense on its purchase. Super Retail Group

has followed the going concern concept as it has deferred many expenses in the form of assets

and liabilities in the balance sheet (Wolk, Dodd and Rozycki, 2016).

5

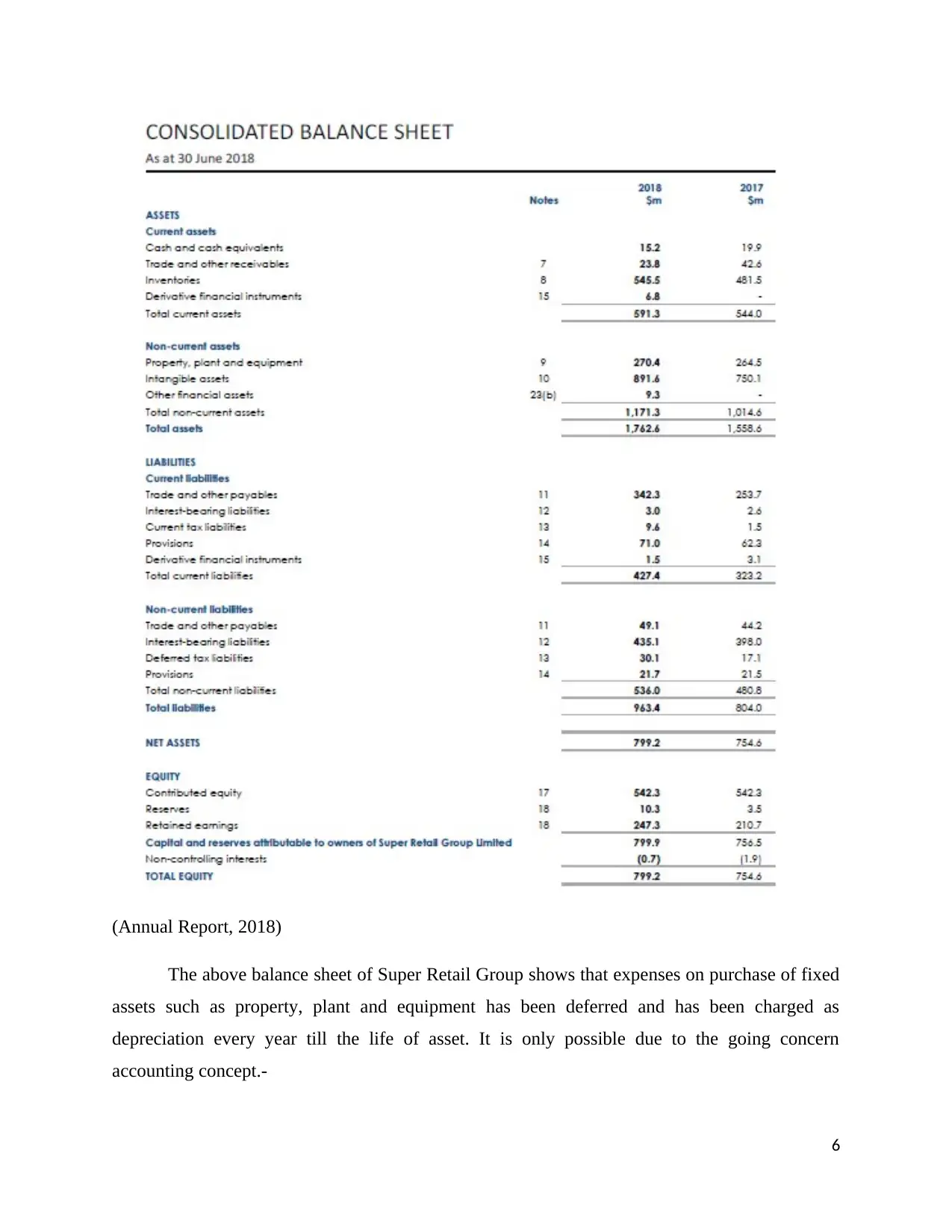

(Annual Report, 2018)

The above balance sheet of Super Retail Group shows that expenses on purchase of fixed

assets such as property, plant and equipment has been deferred and has been charged as

depreciation every year till the life of asset. It is only possible due to the going concern

accounting concept.-

6

The above balance sheet of Super Retail Group shows that expenses on purchase of fixed

assets such as property, plant and equipment has been deferred and has been charged as

depreciation every year till the life of asset. It is only possible due to the going concern

accounting concept.-

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

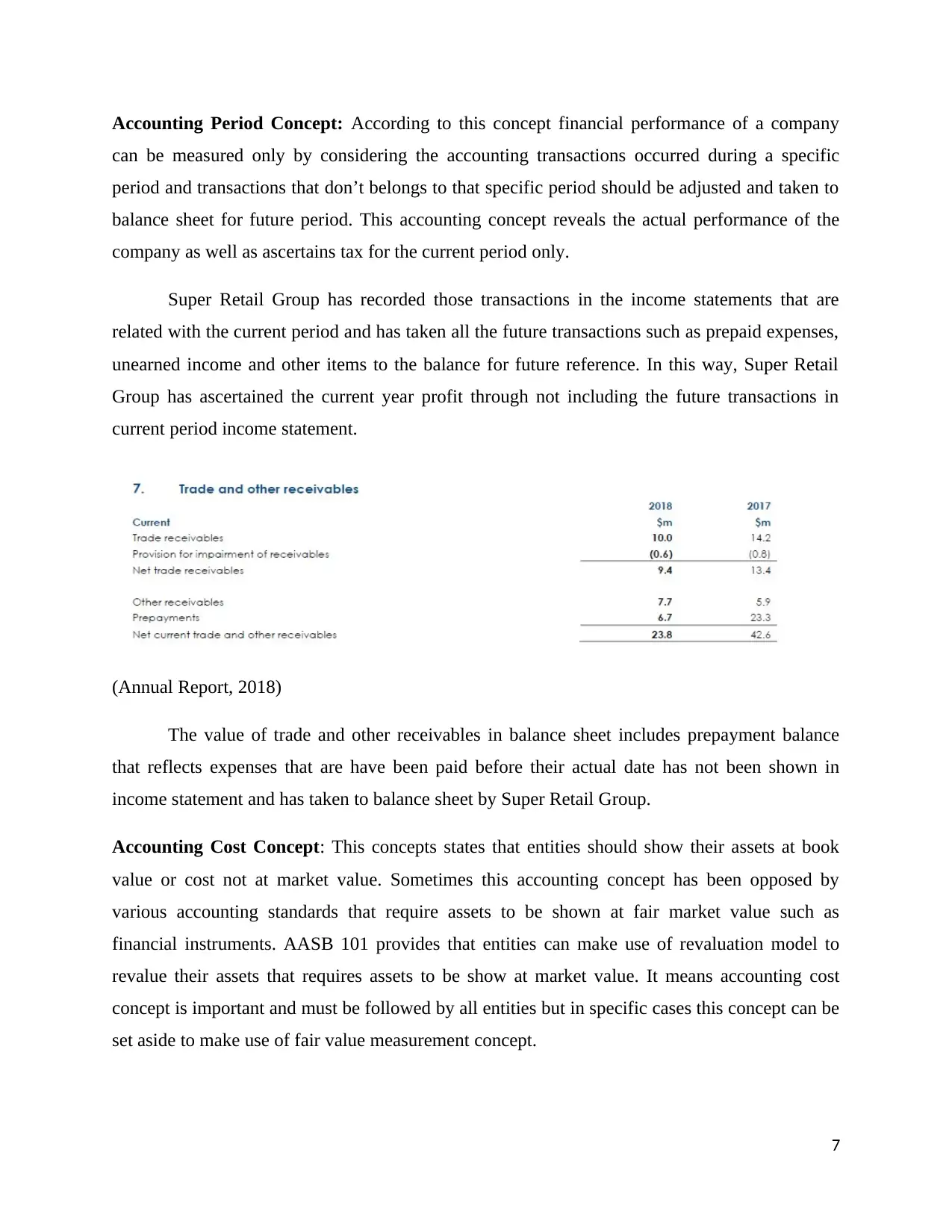

Accounting Period Concept: According to this concept financial performance of a company

can be measured only by considering the accounting transactions occurred during a specific

period and transactions that don’t belongs to that specific period should be adjusted and taken to

balance sheet for future period. This accounting concept reveals the actual performance of the

company as well as ascertains tax for the current period only.

Super Retail Group has recorded those transactions in the income statements that are

related with the current period and has taken all the future transactions such as prepaid expenses,

unearned income and other items to the balance for future reference. In this way, Super Retail

Group has ascertained the current year profit through not including the future transactions in

current period income statement.

(Annual Report, 2018)

The value of trade and other receivables in balance sheet includes prepayment balance

that reflects expenses that are have been paid before their actual date has not been shown in

income statement and has taken to balance sheet by Super Retail Group.

Accounting Cost Concept: This concepts states that entities should show their assets at book

value or cost not at market value. Sometimes this accounting concept has been opposed by

various accounting standards that require assets to be shown at fair market value such as

financial instruments. AASB 101 provides that entities can make use of revaluation model to

revalue their assets that requires assets to be show at market value. It means accounting cost

concept is important and must be followed by all entities but in specific cases this concept can be

set aside to make use of fair value measurement concept.

7

can be measured only by considering the accounting transactions occurred during a specific

period and transactions that don’t belongs to that specific period should be adjusted and taken to

balance sheet for future period. This accounting concept reveals the actual performance of the

company as well as ascertains tax for the current period only.

Super Retail Group has recorded those transactions in the income statements that are

related with the current period and has taken all the future transactions such as prepaid expenses,

unearned income and other items to the balance for future reference. In this way, Super Retail

Group has ascertained the current year profit through not including the future transactions in

current period income statement.

(Annual Report, 2018)

The value of trade and other receivables in balance sheet includes prepayment balance

that reflects expenses that are have been paid before their actual date has not been shown in

income statement and has taken to balance sheet by Super Retail Group.

Accounting Cost Concept: This concepts states that entities should show their assets at book

value or cost not at market value. Sometimes this accounting concept has been opposed by

various accounting standards that require assets to be shown at fair market value such as

financial instruments. AASB 101 provides that entities can make use of revaluation model to

revalue their assets that requires assets to be show at market value. It means accounting cost

concept is important and must be followed by all entities but in specific cases this concept can be

set aside to make use of fair value measurement concept.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

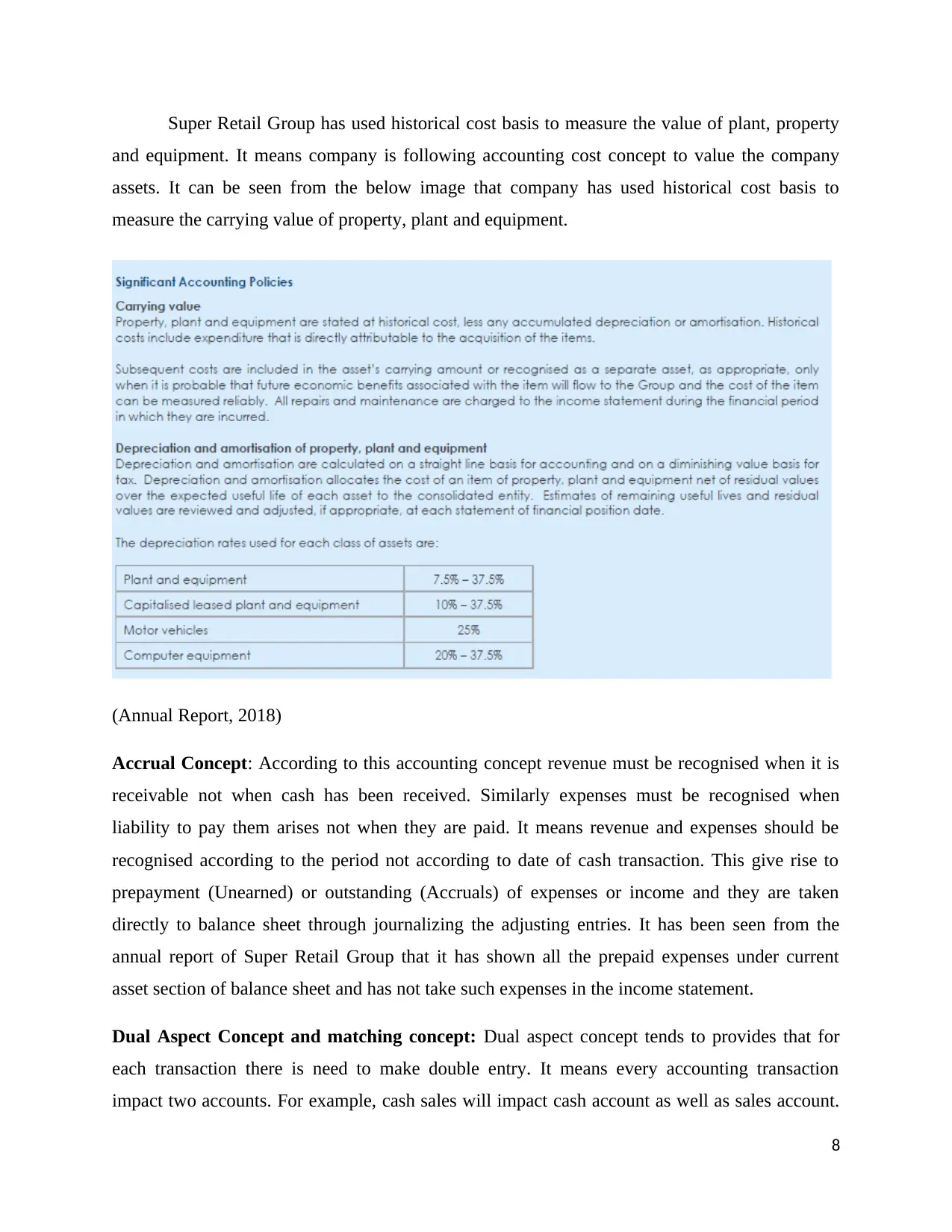

Super Retail Group has used historical cost basis to measure the value of plant, property

and equipment. It means company is following accounting cost concept to value the company

assets. It can be seen from the below image that company has used historical cost basis to

measure the carrying value of property, plant and equipment.

(Annual Report, 2018)

Accrual Concept: According to this accounting concept revenue must be recognised when it is

receivable not when cash has been received. Similarly expenses must be recognised when

liability to pay them arises not when they are paid. It means revenue and expenses should be

recognised according to the period not according to date of cash transaction. This give rise to

prepayment (Unearned) or outstanding (Accruals) of expenses or income and they are taken

directly to balance sheet through journalizing the adjusting entries. It has been seen from the

annual report of Super Retail Group that it has shown all the prepaid expenses under current

asset section of balance sheet and has not take such expenses in the income statement.

Dual Aspect Concept and matching concept: Dual aspect concept tends to provides that for

each transaction there is need to make double entry. It means every accounting transaction

impact two accounts. For example, cash sales will impact cash account as well as sales account.

8

and equipment. It means company is following accounting cost concept to value the company

assets. It can be seen from the below image that company has used historical cost basis to

measure the carrying value of property, plant and equipment.

(Annual Report, 2018)

Accrual Concept: According to this accounting concept revenue must be recognised when it is

receivable not when cash has been received. Similarly expenses must be recognised when

liability to pay them arises not when they are paid. It means revenue and expenses should be

recognised according to the period not according to date of cash transaction. This give rise to

prepayment (Unearned) or outstanding (Accruals) of expenses or income and they are taken

directly to balance sheet through journalizing the adjusting entries. It has been seen from the

annual report of Super Retail Group that it has shown all the prepaid expenses under current

asset section of balance sheet and has not take such expenses in the income statement.

Dual Aspect Concept and matching concept: Dual aspect concept tends to provides that for

each transaction there is need to make double entry. It means every accounting transaction

impact two accounts. For example, cash sales will impact cash account as well as sales account.

8

Matching concept provides income and expenses of same period must be recorded at one place

to calculate the actual profit. For example, if any revenue is earned from sale any product than

cost incurred to produce that product should also be taken in the same period not in future period

(Wahlen, Baginski and Bradshaw, 2017).

Part 2: Issue of Measurement in Accounting with Example from Allocated

Company

The conceptual framework of accounting has mainly provided the use of historical cost

and fair value measurement basis to be used in development of financial reports. The

determination of measuring an asset or liability is linked to the stated objectives of developing

the financial reports as provided by the conceptual accounting framework. Therefore, the

preparers selected an adequate measurement approach on the basis of characteristics of assets

and liabilities for meeting the decision-usefulness perspective of developing financial reports.

The preparers of the financial reports tend to value some of the assets and liabilities at historical

cost while some are measured at the fair value for ensuring that end-users are provided with

relevant and reliable information as per the qualitative principles of conceptual framework

(Conceptual framework- Measurements and elements of financial statements, 2013).

The mixed measurement model of accounting is generally used by the developers at the

time of valuation of assets and liabilities. This means that there does not imply a single universal

measurement model for classification of assets and liabilities. This model of accounting provides

flexibility for the developers in valuing the assets and liabilities. This can be stated from the

example that preparers of financial statements tend to select fair value for measurement when

there exist a fair value for an asset (Filipova, 2016). The absence of active market of an asset the

prepared tend to select historical cost method of accounting. However, the use of this model of

accounting in determining the value of assets and liabilities can result in negatively impacting the

decision-usefulness perspective of the financial information. This is because it tends to generate

inconsistency in the financial reporting system as certain financial items are measured with the

use of historical cost while some are measured on the basis of fair value (International

Accounting Standards Board, 2016).

9

to calculate the actual profit. For example, if any revenue is earned from sale any product than

cost incurred to produce that product should also be taken in the same period not in future period

(Wahlen, Baginski and Bradshaw, 2017).

Part 2: Issue of Measurement in Accounting with Example from Allocated

Company

The conceptual framework of accounting has mainly provided the use of historical cost

and fair value measurement basis to be used in development of financial reports. The

determination of measuring an asset or liability is linked to the stated objectives of developing

the financial reports as provided by the conceptual accounting framework. Therefore, the

preparers selected an adequate measurement approach on the basis of characteristics of assets

and liabilities for meeting the decision-usefulness perspective of developing financial reports.

The preparers of the financial reports tend to value some of the assets and liabilities at historical

cost while some are measured at the fair value for ensuring that end-users are provided with

relevant and reliable information as per the qualitative principles of conceptual framework

(Conceptual framework- Measurements and elements of financial statements, 2013).

The mixed measurement model of accounting is generally used by the developers at the

time of valuation of assets and liabilities. This means that there does not imply a single universal

measurement model for classification of assets and liabilities. This model of accounting provides

flexibility for the developers in valuing the assets and liabilities. This can be stated from the

example that preparers of financial statements tend to select fair value for measurement when

there exist a fair value for an asset (Filipova, 2016). The absence of active market of an asset the

prepared tend to select historical cost method of accounting. However, the use of this model of

accounting in determining the value of assets and liabilities can result in negatively impacting the

decision-usefulness perspective of the financial information. This is because it tends to generate

inconsistency in the financial reporting system as certain financial items are measured with the

use of historical cost while some are measured on the basis of fair value (International

Accounting Standards Board, 2016).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The inconsistency generated within the financial reports has a large negative impact on

the comparability of the financial reports. This negatively impacts the interests of the investors as

they are not able to undertake comparison of the financial performance of an entity with that of

others. The objective of measurement as stated by the conceptual accounting framework is to

faithfully present the most relevant information about the economic resources possessed by an

entity. As such, the selection of an adequate method of measurement depends on the perceived

costs and benefits associated with the use of this method. Therefore, preparers at the time of

selecting a measurement approach should ensure that the benefits realized from it exceeds the

costs attained to the potential investors, lenders and other users of the reporting entity. This will

provide a rational basis for selection of a measurement approach and ensuring that quality

financial information is provided to the end-users (Hopwood, 2013).

The main issue of measurement that is present within a reported entity is due to use of

different method for measuring the value of financial assets and liabilities. The company selected

Super Cheap Auto recognizes the fair value of financial assets and liabilities by the using the

appropriate recognition and measurement criteria for disclosure purposes. The derivates are also

recognized at fair value and other items of income statements such as gains and losses are valued

at carrying amount. The management has also ensured that it has adopted the adequate use of

valuation techniques at the time of determination of fair value of the assets and liabilities. Super

Retail Group (Super Cheap Auto) has recognized its property, plant and equipment at historical

cost basis. It means some parts of assets have been recognized at cost basis and some at fair

value that helps to clarify that nature of assets play an important role in selection of appropriate

measurement basis by the preparers of annual report(Annual Report: Super retail Group, 2018).

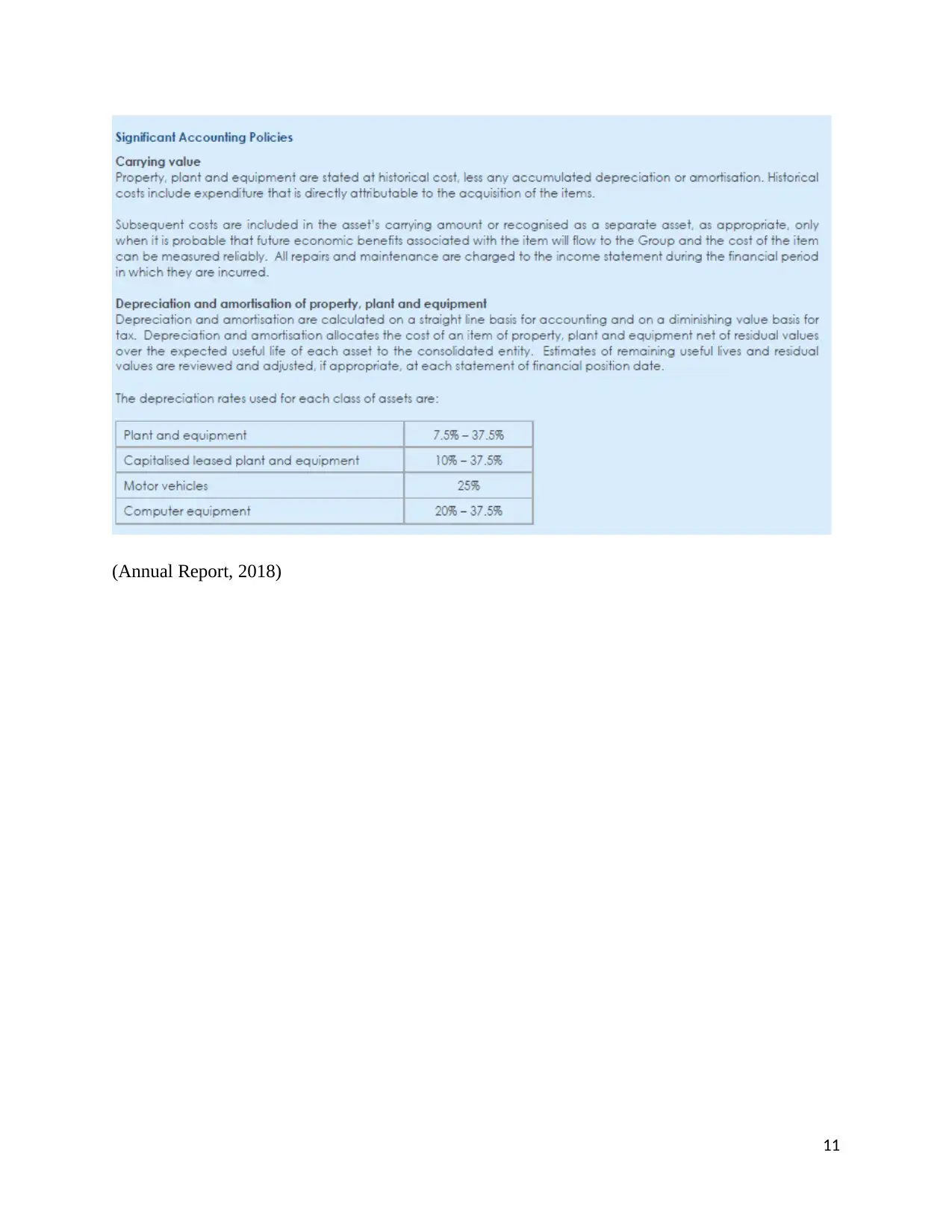

Below are some screenshot from the annual report that clarifies that different

measurement basis has been used by Super Retail Group (Super Cheap Auto):

10

the comparability of the financial reports. This negatively impacts the interests of the investors as

they are not able to undertake comparison of the financial performance of an entity with that of

others. The objective of measurement as stated by the conceptual accounting framework is to

faithfully present the most relevant information about the economic resources possessed by an

entity. As such, the selection of an adequate method of measurement depends on the perceived

costs and benefits associated with the use of this method. Therefore, preparers at the time of

selecting a measurement approach should ensure that the benefits realized from it exceeds the

costs attained to the potential investors, lenders and other users of the reporting entity. This will

provide a rational basis for selection of a measurement approach and ensuring that quality

financial information is provided to the end-users (Hopwood, 2013).

The main issue of measurement that is present within a reported entity is due to use of

different method for measuring the value of financial assets and liabilities. The company selected

Super Cheap Auto recognizes the fair value of financial assets and liabilities by the using the

appropriate recognition and measurement criteria for disclosure purposes. The derivates are also

recognized at fair value and other items of income statements such as gains and losses are valued

at carrying amount. The management has also ensured that it has adopted the adequate use of

valuation techniques at the time of determination of fair value of the assets and liabilities. Super

Retail Group (Super Cheap Auto) has recognized its property, plant and equipment at historical

cost basis. It means some parts of assets have been recognized at cost basis and some at fair

value that helps to clarify that nature of assets play an important role in selection of appropriate

measurement basis by the preparers of annual report(Annual Report: Super retail Group, 2018).

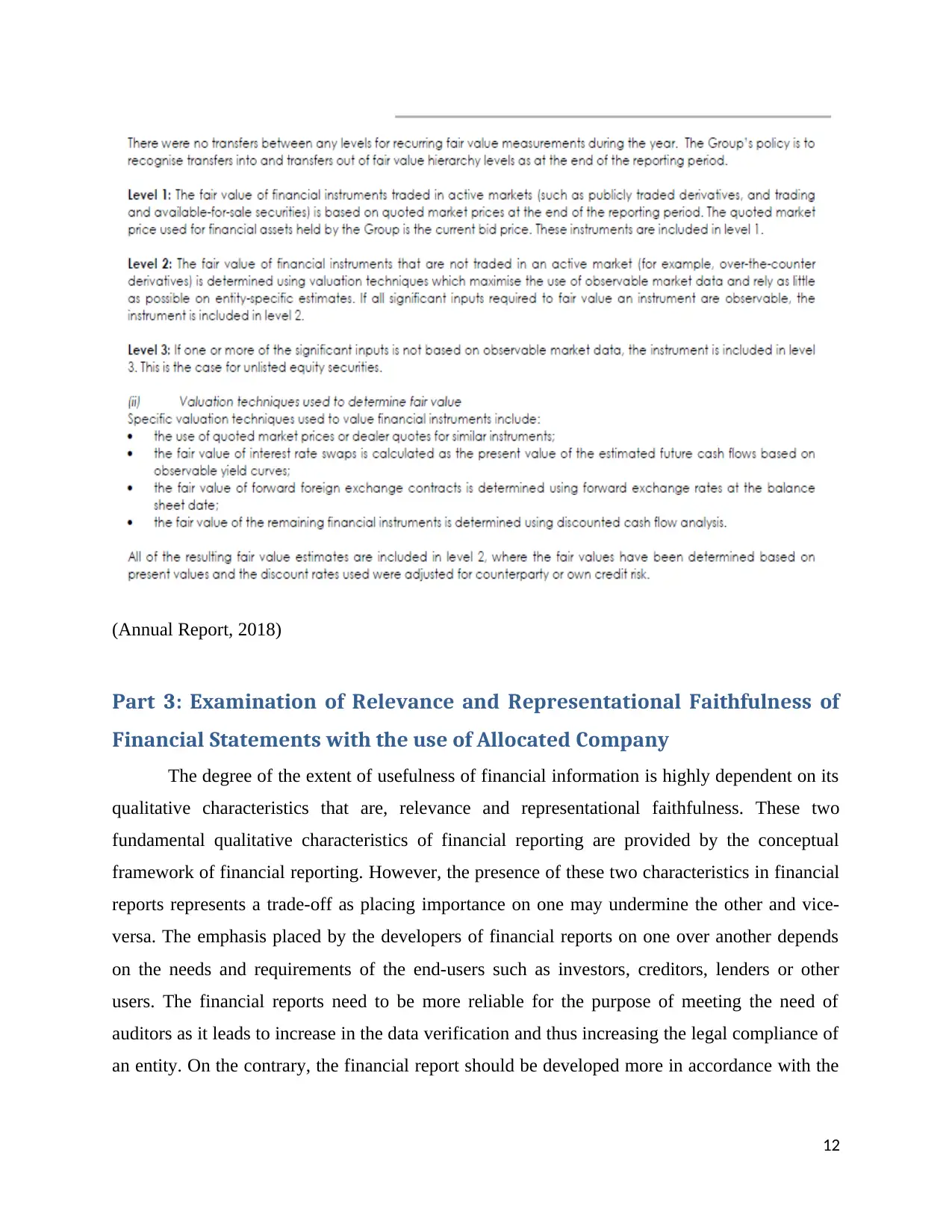

Below are some screenshot from the annual report that clarifies that different

measurement basis has been used by Super Retail Group (Super Cheap Auto):

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Annual Report, 2018)

11

11

(Annual Report, 2018)

Part 3: Examination of Relevance and Representational Faithfulness of

Financial Statements with the use of Allocated Company

The degree of the extent of usefulness of financial information is highly dependent on its

qualitative characteristics that are, relevance and representational faithfulness. These two

fundamental qualitative characteristics of financial reporting are provided by the conceptual

framework of financial reporting. However, the presence of these two characteristics in financial

reports represents a trade-off as placing importance on one may undermine the other and vice-

versa. The emphasis placed by the developers of financial reports on one over another depends

on the needs and requirements of the end-users such as investors, creditors, lenders or other

users. The financial reports need to be more reliable for the purpose of meeting the need of

auditors as it leads to increase in the data verification and thus increasing the legal compliance of

an entity. On the contrary, the financial report should be developed more in accordance with the

12

Part 3: Examination of Relevance and Representational Faithfulness of

Financial Statements with the use of Allocated Company

The degree of the extent of usefulness of financial information is highly dependent on its

qualitative characteristics that are, relevance and representational faithfulness. These two

fundamental qualitative characteristics of financial reporting are provided by the conceptual

framework of financial reporting. However, the presence of these two characteristics in financial

reports represents a trade-off as placing importance on one may undermine the other and vice-

versa. The emphasis placed by the developers of financial reports on one over another depends

on the needs and requirements of the end-users such as investors, creditors, lenders or other

users. The financial reports need to be more reliable for the purpose of meeting the need of

auditors as it leads to increase in the data verification and thus increasing the legal compliance of

an entity. On the contrary, the financial report should be developed more in accordance with the

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.