Holmes Institute T1 2019: Advanced Financial Accounting Report

VerifiedAdded on 2023/04/04

|13

|2239

|369

Report

AI Summary

This report provides a comprehensive overview of advanced financial accounting, commencing with an introduction to fundamental accounting concepts, principles, and terminologies. It explores the conceptual framework, emphasizing its role in establishing accounting standards and resolving disputes. The report then analyzes National Storage REIT, examining its accounting practices, conceptual framework, and adherence to Australian Accounting Standards. Key concepts such as matching, conservatism, materiality, and the going concern principle are discussed in detail. Furthermore, the report delves into the company's financial reporting, highlighting its compliance with the Corporations Act Cth 2001 and the Australian International Financial Reporting Standards. It also examines the fundamental qualitative characteristics of financial reporting data, including relevance and faithful representation. The report concludes by emphasizing the importance of a sound conceptual framework for developing reliable accounting standards and enhancing the understanding of financial statements.

Running head: REPORT 0

ADVANCED FINANCIAL ACCOUNTING

MAY 28, 2019

STUDENT DETAILS:

ADVANCED FINANCIAL ACCOUNTING

MAY 28, 2019

STUDENT DETAILS:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 1

Contents

Introduction................................................................................................................................2

Company overview....................................................................................................................2

Description of accounting concepts...........................................................................................2

Conceptual framework and issue of measurement.....................................................................3

Fundamental Qualitative Characteristics...................................................................................4

Conclusion..................................................................................................................................5

References..................................................................................................................................6

Contents

Introduction................................................................................................................................2

Company overview....................................................................................................................2

Description of accounting concepts...........................................................................................2

Conceptual framework and issue of measurement.....................................................................3

Fundamental Qualitative Characteristics...................................................................................4

Conclusion..................................................................................................................................5

References..................................................................................................................................6

REPORT 2

Introduction

The explanation of the accounting basics address certain fundamental concepts of accounting,

accounting principles, as well as the accounting terminologies. The accounting

concept means the fundamental rules, principles, and assumptions that work as a base of

recording the transactions related to business and making accounts. This concept assumes

that, for accounting, a business entity, and the owners are 2 distinct independent companies.

The conceptual framework of company may describe as a scheme of concepts and aims that

lead to a production of the reliable and constant set of the laws, rules, and regulations. The

agreed conceptual framework is very useful for setting the standards of accounting. The

conceptual framework of company is also useful in resolving the accounting issue (Schulze,

et. al, 2016). It also state the fundamental principles to be used. The major reason for

establishing the conceptual framework is that it provides basis for solving significant dispute,

and framework for describing the standards. In the following report the accounting concepts

followed by National Storage REIT, is discussed, and assessed. The report also state

corporation’s conceptual framework, issues of measurement, and fundamental qualitative

characteristics.

Company overview

National Storage REIT is real rstate investment trust. It is the administrated within and

incorporated the operators and owners of the Australian self-storage centres. This corporation

has about 105 self-storage centres in the administration as well as operations, rendering the

solution related to the storage to above thirty-five thousands clients in New Zealand and

Australia.

Introduction

The explanation of the accounting basics address certain fundamental concepts of accounting,

accounting principles, as well as the accounting terminologies. The accounting

concept means the fundamental rules, principles, and assumptions that work as a base of

recording the transactions related to business and making accounts. This concept assumes

that, for accounting, a business entity, and the owners are 2 distinct independent companies.

The conceptual framework of company may describe as a scheme of concepts and aims that

lead to a production of the reliable and constant set of the laws, rules, and regulations. The

agreed conceptual framework is very useful for setting the standards of accounting. The

conceptual framework of company is also useful in resolving the accounting issue (Schulze,

et. al, 2016). It also state the fundamental principles to be used. The major reason for

establishing the conceptual framework is that it provides basis for solving significant dispute,

and framework for describing the standards. In the following report the accounting concepts

followed by National Storage REIT, is discussed, and assessed. The report also state

corporation’s conceptual framework, issues of measurement, and fundamental qualitative

characteristics.

Company overview

National Storage REIT is real rstate investment trust. It is the administrated within and

incorporated the operators and owners of the Australian self-storage centres. This corporation

has about 105 self-storage centres in the administration as well as operations, rendering the

solution related to the storage to above thirty-five thousands clients in New Zealand and

Australia.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT 3

Additionally, this company administers about 59,200 units for storage through above 542,000

square meters of net settable extent in New Zealand and Australia. National Storage Property

Trust (NSPT) owns about sixty self-storage centres. There are sixteen self-storage centres,

which are functioned as long-run leasehold centres. On the other hand, there are twenty six

thousand self-storage centres, which are administrated for the South Cross Storage Group and

over three third-people administrated the centres. The self-storage centres of corporations are

placed at the Gold Coast, Christchurch, Brisbane, North Queensland, Perth, Sunshine Coast,

Geelong, Canberra, Sydney, Hobart, Melbourne, Hamilton, Wellington, and Darwin

(Bloomberg, 2018).

Description of accounting concepts

There are various theoretical issues. It is required that one should understand the accounting

concepts to establish the entity foundation of how the accounting does work. The

fundamental accounting concepts are below:

1. The concept of matching - the expenditures related to revenues must be identified in

the similar time, where the revenues were identified. From conducting this, there are

no deferrals of expenditure identification in subsequent reporting period, with the

intention of someone viewing, the financial statements of company may be

guaranteed that all the features of the transactions have noted at the similar period.

2. The conservatism concept- Revenues are only identified while there are the proper

certainty that this would be realized, where the expenditures are identified earlier,

whenever there are the reasonable possibilities that they would be earned. The

conservatism concept inclines the outcome in conventional financial statement

(Kelley and Knowles, 2016).

Additionally, this company administers about 59,200 units for storage through above 542,000

square meters of net settable extent in New Zealand and Australia. National Storage Property

Trust (NSPT) owns about sixty self-storage centres. There are sixteen self-storage centres,

which are functioned as long-run leasehold centres. On the other hand, there are twenty six

thousand self-storage centres, which are administrated for the South Cross Storage Group and

over three third-people administrated the centres. The self-storage centres of corporations are

placed at the Gold Coast, Christchurch, Brisbane, North Queensland, Perth, Sunshine Coast,

Geelong, Canberra, Sydney, Hobart, Melbourne, Hamilton, Wellington, and Darwin

(Bloomberg, 2018).

Description of accounting concepts

There are various theoretical issues. It is required that one should understand the accounting

concepts to establish the entity foundation of how the accounting does work. The

fundamental accounting concepts are below:

1. The concept of matching - the expenditures related to revenues must be identified in

the similar time, where the revenues were identified. From conducting this, there are

no deferrals of expenditure identification in subsequent reporting period, with the

intention of someone viewing, the financial statements of company may be

guaranteed that all the features of the transactions have noted at the similar period.

2. The conservatism concept- Revenues are only identified while there are the proper

certainty that this would be realized, where the expenditures are identified earlier,

whenever there are the reasonable possibilities that they would be earned. The

conservatism concept inclines the outcome in conventional financial statement

(Kelley and Knowles, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 4

3. The materiality concept- as per this accounting concept, the transactions must be

recorded while not conducting so may change the decision taken by readers of the

financial statement of corporation. It tends to effect in comparatively smaller-size

dealings being recorded, so as to the financial statements broadly show results related

to economic outcomes, statement of cash flow related to business and financial

condition (Kršeková and Pakšiová, 2015).

4. The Economic entity concept – business transaction is to be retained isolated from the

owner’s transaction. Through making this, there are no intermixing of own

transactions and the transactions related to business in the financial statements of

corporation (Gummer and Mandinach, 2015).

5. The concept of consistency- at the time when the business selects to utilise the

particular accounting method, this must continue utilising this over the go-forward

base. Through conducting this, the financial statements of company made in the

various periods may be consistently compared (Schnipper, et. al, 2015).

6. The going concern concept- The financial statements of entity are made according to

assumption that businesses would remain in the operations in the upcoming time

(Christensen, Nikolaev and Wittenberg‐Moerman, 2016). As according to the going

concern assumption, the expenses recognition as well as the revenue recognition can

be deferred to the upcoming time, while the corporation is still running. Or else, all

the expenditure recognition in particular will be accelerated in the present time.

7. Accruals concept- according to accruals concept, the revenues are recognized at the

time while they earned. In the addition of this, this concept state that the expenditures

are recognized at the time while asset is consumed. In this way, the accruals concept

addresses that the business may can identify the revenues based on the cash accepted

3. The materiality concept- as per this accounting concept, the transactions must be

recorded while not conducting so may change the decision taken by readers of the

financial statement of corporation. It tends to effect in comparatively smaller-size

dealings being recorded, so as to the financial statements broadly show results related

to economic outcomes, statement of cash flow related to business and financial

condition (Kršeková and Pakšiová, 2015).

4. The Economic entity concept – business transaction is to be retained isolated from the

owner’s transaction. Through making this, there are no intermixing of own

transactions and the transactions related to business in the financial statements of

corporation (Gummer and Mandinach, 2015).

5. The concept of consistency- at the time when the business selects to utilise the

particular accounting method, this must continue utilising this over the go-forward

base. Through conducting this, the financial statements of company made in the

various periods may be consistently compared (Schnipper, et. al, 2015).

6. The going concern concept- The financial statements of entity are made according to

assumption that businesses would remain in the operations in the upcoming time

(Christensen, Nikolaev and Wittenberg‐Moerman, 2016). As according to the going

concern assumption, the expenses recognition as well as the revenue recognition can

be deferred to the upcoming time, while the corporation is still running. Or else, all

the expenditure recognition in particular will be accelerated in the present time.

7. Accruals concept- according to accruals concept, the revenues are recognized at the

time while they earned. In the addition of this, this concept state that the expenditures

are recognized at the time while asset is consumed. In this way, the accruals concept

addresses that the business may can identify the revenues based on the cash accepted

REPORT 5

from the customer or while the cash is paid to workers as well as dealers. In this way,

the auditors would only confirm the financial statements of the company that have

been made as according to the accruals concept (Geisker, and Tallis, 2018).

By analysis of company’s annual report, this is clear that the financial reports have been

made and presented as per the basis of going concern and consistency. The directors of the

corporation believed that the group would continue to make the operating cash flow to fulfil

all the obligations related to payment in an ordinary course of business (Henderson, et. al,

2015). Further, NSR diminishes the probable influences of fluctuating the financial condition

by looking for maintaining the conservative as well as strong balance sheet and the financial

condition. In this way, the estimates as well as assumptions are depended on the existing

constraints while the consolidated financial statements of company were made. The key

assumptions regarding an upcoming period and relevant major sources of the approximation

uncertainty at a reporting date, which have important risks of resulting the material

adjustments to a carrying amount of liabilities as well as assets in upcoming financial year.

In the addition of this, the company, in preparing the financial reports, incorporates the GRI

Reporting Principles. According to the GRI Principle ‘Materiality’, the financial impacts,

environmental impacts as well as social impacts were evaluated and ranked in relation to

risks to the stakeholders and company itself. The company also follows the GRI Principle

‘Stakeholder Inclusiveness’. As per this, a review of shareholders and connected engagement

through the reporting year was made, but not particularly for composing of the report.

Furthermore, according to the GRI Principle ‘Sustainability Context’, social impacts,

environmental impacts, and financial impacts of the National Storage operation was

recognised and measured. Moreover, the GRI Principle ‘Completeness’ states the GRI and

other matters involved in the report are those, which have been recognised as material to

National Storage and the shareholders in the Financial Year 2018 (Díaz, et. al, 2015).

from the customer or while the cash is paid to workers as well as dealers. In this way,

the auditors would only confirm the financial statements of the company that have

been made as according to the accruals concept (Geisker, and Tallis, 2018).

By analysis of company’s annual report, this is clear that the financial reports have been

made and presented as per the basis of going concern and consistency. The directors of the

corporation believed that the group would continue to make the operating cash flow to fulfil

all the obligations related to payment in an ordinary course of business (Henderson, et. al,

2015). Further, NSR diminishes the probable influences of fluctuating the financial condition

by looking for maintaining the conservative as well as strong balance sheet and the financial

condition. In this way, the estimates as well as assumptions are depended on the existing

constraints while the consolidated financial statements of company were made. The key

assumptions regarding an upcoming period and relevant major sources of the approximation

uncertainty at a reporting date, which have important risks of resulting the material

adjustments to a carrying amount of liabilities as well as assets in upcoming financial year.

In the addition of this, the company, in preparing the financial reports, incorporates the GRI

Reporting Principles. According to the GRI Principle ‘Materiality’, the financial impacts,

environmental impacts as well as social impacts were evaluated and ranked in relation to

risks to the stakeholders and company itself. The company also follows the GRI Principle

‘Stakeholder Inclusiveness’. As per this, a review of shareholders and connected engagement

through the reporting year was made, but not particularly for composing of the report.

Furthermore, according to the GRI Principle ‘Sustainability Context’, social impacts,

environmental impacts, and financial impacts of the National Storage operation was

recognised and measured. Moreover, the GRI Principle ‘Completeness’ states the GRI and

other matters involved in the report are those, which have been recognised as material to

National Storage and the shareholders in the Financial Year 2018 (Díaz, et. al, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT 6

Conceptual framework and issue of measurement

The major purpose to develop conceptual framework is that it delivers a framework for

setting standards of accounting, and a base for resolving accounting related dispute. A

conceptual framework of the company also provides fundamental principles that do not

require repeating again regarding accounting standards. A framework to present as well as

prepare the financial statements of the organisation as changed involves the conceptual

framework for financial reporting as provided through the IASB. Conceptual framework’s

provisions of measurement cover the general purpose financial reporting, purpose of financial

reporting, the fundamental qualitative characteristics in relation to accounting information,

corporation’s financial statements measurements, as well as fundamental elements related to

the financial statements of corporation.

According to annual report of National Storage REIT, this is analysed that financial report of

this company has prepared as well as presented according to requirements of Corporation Act

Cth 2001, and commanding announcement of he AASB, and Accounting standards of

Australia. A company made the financial report according to the Australian International

Financial Reporting Standard delivered by International Accounting Standards Board and

Accounting Standards of Australia standards (Annual Report 2018). Additionally, directors

of National Storage REIT made resolution that financial statements of organisation are made

as well as presented as per Corporation Act Cth 2001. In order to make sure the compliance

with the Corporations Act 2001 as well as constitution, the accountable entity has in place the

compliance planning that sets measures this will implement in managing NSPT (Panteli and

Mancarella, 2015).

Conceptual framework and issue of measurement

The major purpose to develop conceptual framework is that it delivers a framework for

setting standards of accounting, and a base for resolving accounting related dispute. A

conceptual framework of the company also provides fundamental principles that do not

require repeating again regarding accounting standards. A framework to present as well as

prepare the financial statements of the organisation as changed involves the conceptual

framework for financial reporting as provided through the IASB. Conceptual framework’s

provisions of measurement cover the general purpose financial reporting, purpose of financial

reporting, the fundamental qualitative characteristics in relation to accounting information,

corporation’s financial statements measurements, as well as fundamental elements related to

the financial statements of corporation.

According to annual report of National Storage REIT, this is analysed that financial report of

this company has prepared as well as presented according to requirements of Corporation Act

Cth 2001, and commanding announcement of he AASB, and Accounting standards of

Australia. A company made the financial report according to the Australian International

Financial Reporting Standard delivered by International Accounting Standards Board and

Accounting Standards of Australia standards (Annual Report 2018). Additionally, directors

of National Storage REIT made resolution that financial statements of organisation are made

as well as presented as per Corporation Act Cth 2001. In order to make sure the compliance

with the Corporations Act 2001 as well as constitution, the accountable entity has in place the

compliance planning that sets measures this will implement in managing NSPT (Panteli and

Mancarella, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 7

The financial statements of organisation show true and fair view of performances of

organisation along with financial position of organisation. The corporation’s financial

statements comply with Corporations Regulations 2001 as well as accounting. National

Storage REIT adopts the significant accounting policies to create the basis from the asset’s

value, income and expenses, value of liability and equity’s value. In the addition, the

company is independent of a group according with the requirements related to the auditor’s

independence as per the Corporations Act 2001, as well as ethical provisions of APES 110

Code of Ethics of Accounting Professional and Ethical Standards Board for Skilled

Accountant, which are associated with financial auditor’s report in Australia. Company has

also complete the other ethical duties according to the code (Lewandowski, 2016).

Fundamental Qualitative Characteristics

The financial reporting data’s fundamental qualitative characteristics of include the relevance

and faithful representation. According to the fundamental qualitative characteristics of

financial reporting data, this is essential that information must be relevant towards a

requirement of user, which is subject of concern while the data influence financial decisions

taken by users. It can include the reporting specific data, or the data whose mistake and

misstatement can affect the user’s financial decisions (Bridgett, et. al, 2015).

Further, the faithful representation is also considered as other significant fundamental

qualitative characteristic. Faithful representation means to the concept stating that financial

statement of the organisation should be generated in the way to precisely show the condition

of business. With the help of corporation’s annual report, it is clear that the financial

statements of organisation render the proper as well as faithful representation. National

Storage REIT faithfully states the transactions and different events, reflects fundamental

The financial statements of organisation show true and fair view of performances of

organisation along with financial position of organisation. The corporation’s financial

statements comply with Corporations Regulations 2001 as well as accounting. National

Storage REIT adopts the significant accounting policies to create the basis from the asset’s

value, income and expenses, value of liability and equity’s value. In the addition, the

company is independent of a group according with the requirements related to the auditor’s

independence as per the Corporations Act 2001, as well as ethical provisions of APES 110

Code of Ethics of Accounting Professional and Ethical Standards Board for Skilled

Accountant, which are associated with financial auditor’s report in Australia. Company has

also complete the other ethical duties according to the code (Lewandowski, 2016).

Fundamental Qualitative Characteristics

The financial reporting data’s fundamental qualitative characteristics of include the relevance

and faithful representation. According to the fundamental qualitative characteristics of

financial reporting data, this is essential that information must be relevant towards a

requirement of user, which is subject of concern while the data influence financial decisions

taken by users. It can include the reporting specific data, or the data whose mistake and

misstatement can affect the user’s financial decisions (Bridgett, et. al, 2015).

Further, the faithful representation is also considered as other significant fundamental

qualitative characteristic. Faithful representation means to the concept stating that financial

statement of the organisation should be generated in the way to precisely show the condition

of business. With the help of corporation’s annual report, it is clear that the financial

statements of organisation render the proper as well as faithful representation. National

Storage REIT faithfully states the transactions and different events, reflects fundamental

REPORT 8

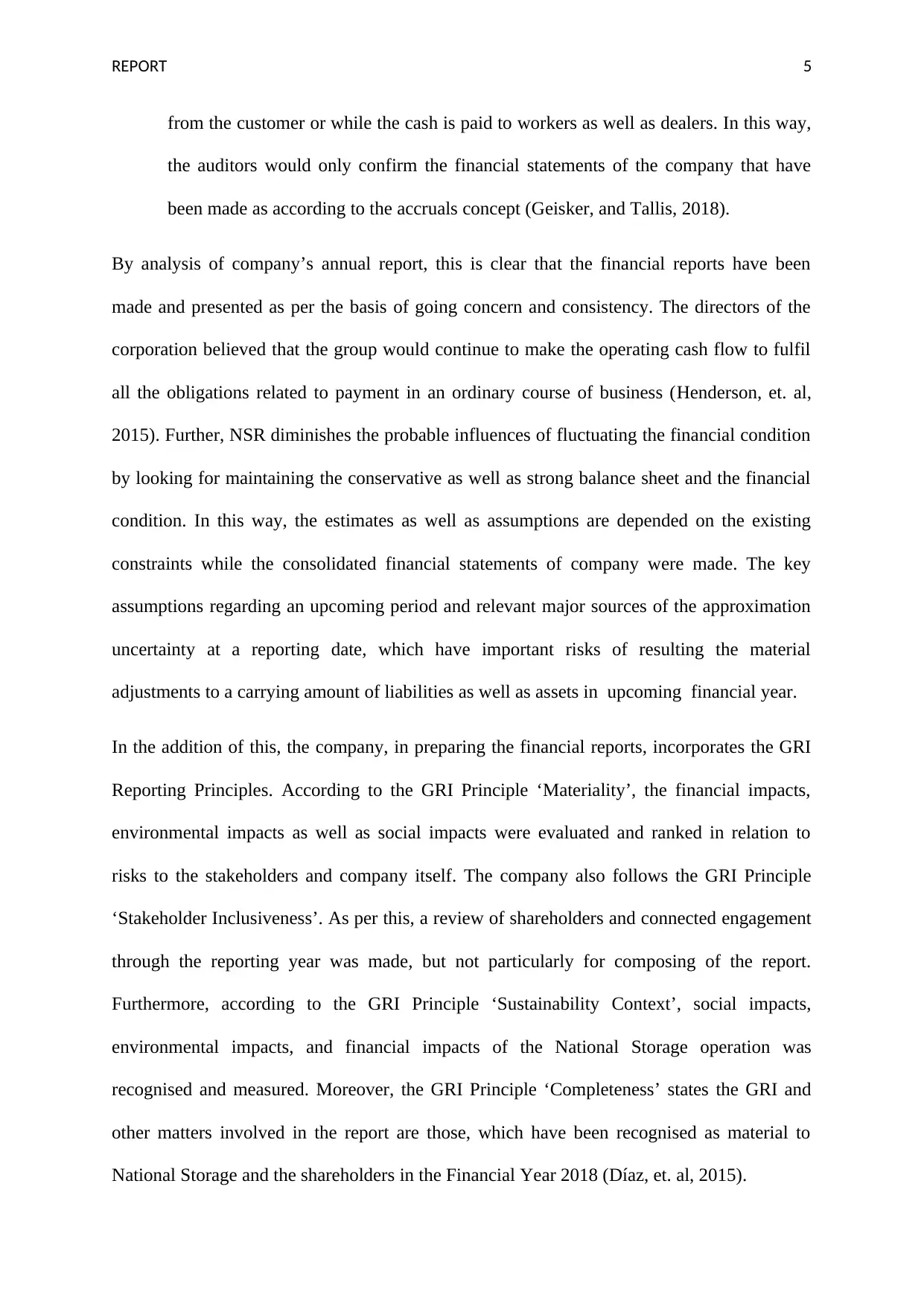

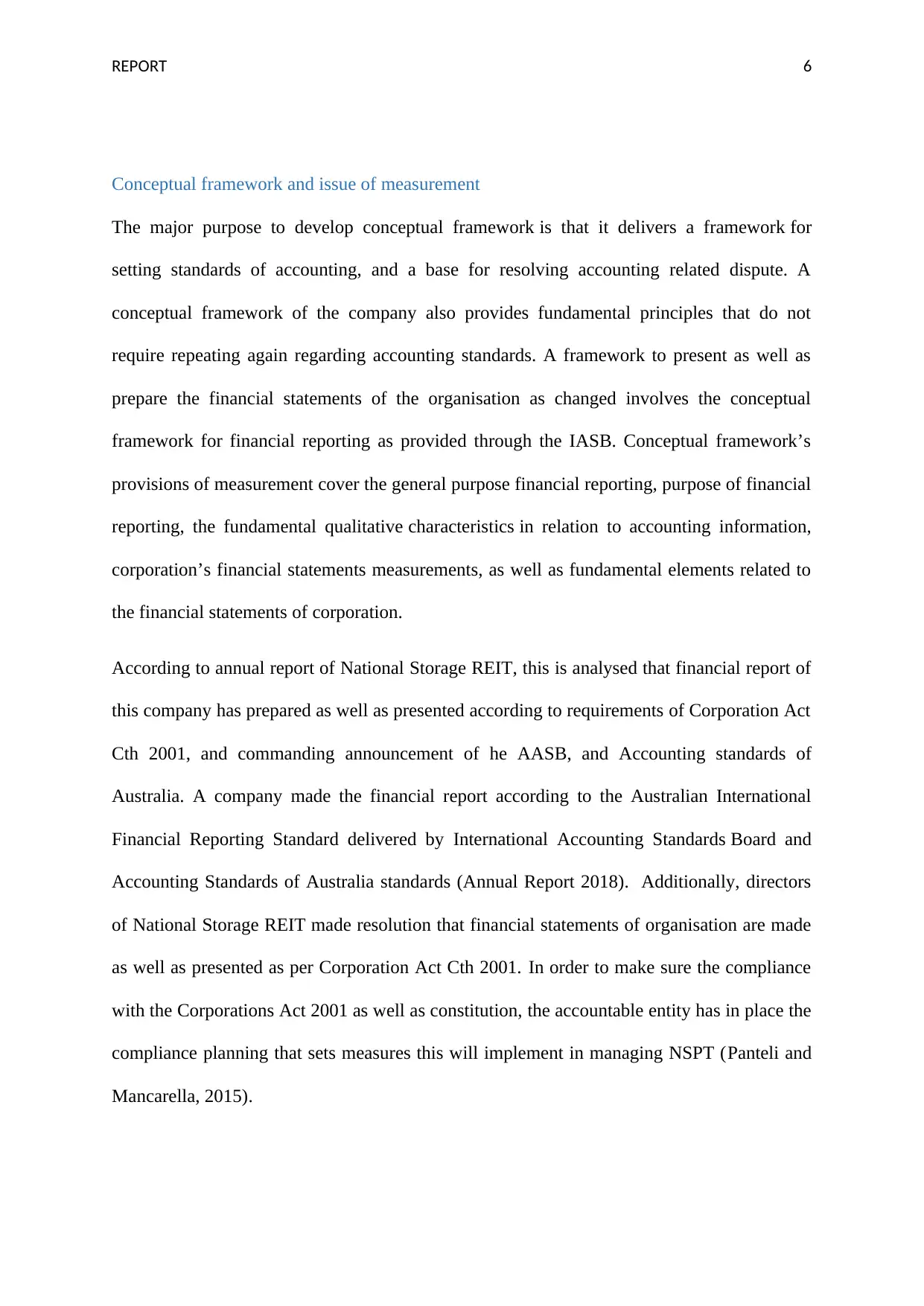

matters related to the event, prudently states estimates, as well as uncertainties through the

relevant disclosures. For the instance, an organisation has complied with faithful presentation

characteristics regarding the revenues -

Conclusion

According to the above discussion, it can say that non-appearance of conceptual framework

may result into making of accounting system based on rules, whose major purpose is that

treatments of the transactions related to accounting must be dispensed with inclusive

particular requirements, laws, as well as rules. In this way, rule based accounting system is

more contracted as well as uncompromising; however has financial statement’s attraction

matters related to the event, prudently states estimates, as well as uncertainties through the

relevant disclosures. For the instance, an organisation has complied with faithful presentation

characteristics regarding the revenues -

Conclusion

According to the above discussion, it can say that non-appearance of conceptual framework

may result into making of accounting system based on rules, whose major purpose is that

treatments of the transactions related to accounting must be dispensed with inclusive

particular requirements, laws, as well as rules. In this way, rule based accounting system is

more contracted as well as uncompromising; however has financial statement’s attraction

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT 9

being equivalent and constant (Sampaio and González, 2017). The sound conceptual

framework is capable to issue helpful and reliable standards. Additionally, deprived of the

present set of standards, this is not possible to solve the new issues that develop. The

conceptual framework also enhances the financial statements reader's knowledge of and self-

assurance in financial reporting and creates this simpler to make comparison between the

different financial statements of the corporation.

being equivalent and constant (Sampaio and González, 2017). The sound conceptual

framework is capable to issue helpful and reliable standards. Additionally, deprived of the

present set of standards, this is not possible to solve the new issues that develop. The

conceptual framework also enhances the financial statements reader's knowledge of and self-

assurance in financial reporting and creates this simpler to make comparison between the

different financial statements of the corporation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 10

References

Annual Report (2018). National Storage REIT. Available at:

https://www.nationalstorageinvest.com.au/wp-content/uploads/sites/5/2018/09/3.-FY18-

Annual-Report.pdf. Access on 28/05/2018

Bloomberg (2018). National Storage REIT. Available at:

https://www.bloomberg.com/profile/company/NSR:AU Access on 28/05/2019

Bridgett, D.J., Burt, N.M., Edwards, E.S. and Deater-Deckard, K. (2015) Intergenerational

transmission of self-regulation: A multidisciplinary review and integrative conceptual

framework. Psychological bulletin, 141(3), p.602.

Christensen, H.B., Nikolaev, V.V. and Wittenberg‐Moerman, R. (2016) Accounting

information in financial contracting: The incomplete contract theory perspective. Journal of

accounting research, 54(2), pp.397-435.

Díaz, S., Demissew, S., Carabias, J., Joly, C., Lonsdale, M., Ash, N., Larigauderie, A.,

Adhikari, J.R., Arico, S., Báldi, A. and Bartuska, A. (2015) The IPBES Conceptual

Framework—connecting nature and people. Current Opinion in Environmental

Sustainability, 14, pp.1-16.

Geisker, J. and Tallis, J. (2018) Litigation funding in Australia: A year of review and

change?. LSJ: Law Society of NSW Journal, (46), p.81.

Gummer, E. and Mandinach, E. (2015) Building a Conceptual Framework for Data

Literacy. Teachers College Record, 117(4), p.n4.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B. (2015) Issues in financial

accounting. Pearson Higher Education AU.

References

Annual Report (2018). National Storage REIT. Available at:

https://www.nationalstorageinvest.com.au/wp-content/uploads/sites/5/2018/09/3.-FY18-

Annual-Report.pdf. Access on 28/05/2018

Bloomberg (2018). National Storage REIT. Available at:

https://www.bloomberg.com/profile/company/NSR:AU Access on 28/05/2019

Bridgett, D.J., Burt, N.M., Edwards, E.S. and Deater-Deckard, K. (2015) Intergenerational

transmission of self-regulation: A multidisciplinary review and integrative conceptual

framework. Psychological bulletin, 141(3), p.602.

Christensen, H.B., Nikolaev, V.V. and Wittenberg‐Moerman, R. (2016) Accounting

information in financial contracting: The incomplete contract theory perspective. Journal of

accounting research, 54(2), pp.397-435.

Díaz, S., Demissew, S., Carabias, J., Joly, C., Lonsdale, M., Ash, N., Larigauderie, A.,

Adhikari, J.R., Arico, S., Báldi, A. and Bartuska, A. (2015) The IPBES Conceptual

Framework—connecting nature and people. Current Opinion in Environmental

Sustainability, 14, pp.1-16.

Geisker, J. and Tallis, J. (2018) Litigation funding in Australia: A year of review and

change?. LSJ: Law Society of NSW Journal, (46), p.81.

Gummer, E. and Mandinach, E. (2015) Building a Conceptual Framework for Data

Literacy. Teachers College Record, 117(4), p.n4.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B. (2015) Issues in financial

accounting. Pearson Higher Education AU.

REPORT 11

Kelley, T.R. and Knowles, J.G. (2016) A conceptual framework for integrated STEM

education. International Journal of STEM Education, 3(1), p.11.

Kršeková, M. and Pakšiová, R. (2015) Financial reporting on information about the financial

position and financial performance in the financial statements of the public sector. Finance

and risk 2015, 14(1), pp.136-145.

Lewandowski, M. (2016) Designing the business models for circular economy—Towards the

conceptual framework. Sustainability, 8(1), p.43.

Panteli, M. and Mancarella, P. (2015) The grid: Stronger bigger smarter?: Presenting a

conceptual framework of power system resilience. IEEE Power Energy Mag, 13(3), pp.58-

66.

Sampaio, P.G.V. and González, M.O.A. (2017) Photovoltaic solar energy: Conceptual

framework. Renewable and Sustainable Energy Reviews, 74, pp.590-601.

Schnipper, L.E., Davidson, N.E., Wollins, D.S., Tyne, C., Blayney, D.W., Blum, D., Dicker,

A.P., Ganz, P.A., Hoverman, J.R., Langdon, R. and Lyman, G.H. (2015) American Society of

Clinical Oncology statement: a conceptual framework to assess the value of cancer treatment

options. Journal of Clinical Oncology, 33(23), p.2563.

Schulze, M., Nehler, H., Ottosson, M. and Thollander, P. (2016) Energy management in

industry–a systematic review of previous findings and an integrative conceptual

framework. Journal of Cleaner Production, 112, pp.3692-3708.

Kelley, T.R. and Knowles, J.G. (2016) A conceptual framework for integrated STEM

education. International Journal of STEM Education, 3(1), p.11.

Kršeková, M. and Pakšiová, R. (2015) Financial reporting on information about the financial

position and financial performance in the financial statements of the public sector. Finance

and risk 2015, 14(1), pp.136-145.

Lewandowski, M. (2016) Designing the business models for circular economy—Towards the

conceptual framework. Sustainability, 8(1), p.43.

Panteli, M. and Mancarella, P. (2015) The grid: Stronger bigger smarter?: Presenting a

conceptual framework of power system resilience. IEEE Power Energy Mag, 13(3), pp.58-

66.

Sampaio, P.G.V. and González, M.O.A. (2017) Photovoltaic solar energy: Conceptual

framework. Renewable and Sustainable Energy Reviews, 74, pp.590-601.

Schnipper, L.E., Davidson, N.E., Wollins, D.S., Tyne, C., Blayney, D.W., Blum, D., Dicker,

A.P., Ganz, P.A., Hoverman, J.R., Langdon, R. and Lyman, G.H. (2015) American Society of

Clinical Oncology statement: a conceptual framework to assess the value of cancer treatment

options. Journal of Clinical Oncology, 33(23), p.2563.

Schulze, M., Nehler, H., Ottosson, M. and Thollander, P. (2016) Energy management in

industry–a systematic review of previous findings and an integrative conceptual

framework. Journal of Cleaner Production, 112, pp.3692-3708.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.