Report: Advanced Financial Accounting Analysis, T1 2019, Holmes

VerifiedAdded on 2023/03/30

|14

|3005

|488

Report

AI Summary

This report provides a detailed analysis of advanced financial accounting principles, policies, and conceptual frameworks. It uses Domain Holdings Australia as a case study to illustrate the application of various accounting concepts, including accrual, full disclosure, matching, conservatism, business entity, and materiality. The report examines the company's compliance with the Corporation Act 2001 and Australian Accounting Standards Board (AASB) standards, focusing on issues related to intangible assets, financial instruments, and impairment. It also explores the conceptual framework, its qualitative characteristics, and its influence on accounting practice. The analysis covers the measurement of assets and liabilities, the recognition of revenue and expenses, and the company's approach to risk management, providing insights into how accounting standards are applied in practice and identifying areas of non-compliance. The report concludes with an overview of the issues identified and the importance of a strong conceptual framework for ensuring consistent and reliable financial reporting.

ADVANCED FINANCIAL

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction...........................................................................................................................................3

Domain Holding Australia......................................................................................................................3

Descriptions of Accounting Concepts....................................................................................................4

Conceptual framework and the Issue of Measurement........................................................................7

Conclusion...........................................................................................................................................12

References...........................................................................................................................................13

Introduction...........................................................................................................................................3

Domain Holding Australia......................................................................................................................3

Descriptions of Accounting Concepts....................................................................................................4

Conceptual framework and the Issue of Measurement........................................................................7

Conclusion...........................................................................................................................................12

References...........................................................................................................................................13

Introduction

This report brings out a discussion on accosting procedures, policies, rules, and conceptual

framework. The company complies with the Corporation Act, 2001 that includes against the

liabilities that are incurred in respective capacities while defending to the proceedings against

them. There are several policies, rules, amendments prohibits the details of liability, and the

premium paid. The company chosen for the analysis for the AASBs is the Domain Holdings

Australia. In this concept, the evaluation is based on handling every transaction and other

events for the accounts (Hoyle, Schaefer, and Doupnik, 2015). Further, a debate over the

issues identified in regards to each accounting concepts and measurement for the intangible

assets and measuring the assets in order to handle the assets and liabilities. The report

evaluates and monitors on the basis of quantitative features relevant to information given in

the annual reports when taking into consideration the calculation of liabilities and assets.

Several issues have been found as per the non-compliance of standards and policies so that it

could fulfil to foresee the demand of AASB for financial instruments that has not be

regulated yet. Conceptual framework will provide a standard to monitor the consistency of

the main principles considered in the conceptual framework (Hoyle, Schaefer, and Doupnik,

2015).

Domain Holding Australia

Domain Holding Australia is a leading Australian real estate technological and media level

company Service Company. The main purpose of the company is to inform and connect

people with the help of property lifecycle. The main assets of the company include

accessibility of digital facility to the large audience, social and print that are further driven by

listed strengths and other rich engagements. The source of Domain`s ecosystem for revenues

are residential, commercial, print, transactions, media, developers and agent services. In

This report brings out a discussion on accosting procedures, policies, rules, and conceptual

framework. The company complies with the Corporation Act, 2001 that includes against the

liabilities that are incurred in respective capacities while defending to the proceedings against

them. There are several policies, rules, amendments prohibits the details of liability, and the

premium paid. The company chosen for the analysis for the AASBs is the Domain Holdings

Australia. In this concept, the evaluation is based on handling every transaction and other

events for the accounts (Hoyle, Schaefer, and Doupnik, 2015). Further, a debate over the

issues identified in regards to each accounting concepts and measurement for the intangible

assets and measuring the assets in order to handle the assets and liabilities. The report

evaluates and monitors on the basis of quantitative features relevant to information given in

the annual reports when taking into consideration the calculation of liabilities and assets.

Several issues have been found as per the non-compliance of standards and policies so that it

could fulfil to foresee the demand of AASB for financial instruments that has not be

regulated yet. Conceptual framework will provide a standard to monitor the consistency of

the main principles considered in the conceptual framework (Hoyle, Schaefer, and Doupnik,

2015).

Domain Holding Australia

Domain Holding Australia is a leading Australian real estate technological and media level

company Service Company. The main purpose of the company is to inform and connect

people with the help of property lifecycle. The main assets of the company include

accessibility of digital facility to the large audience, social and print that are further driven by

listed strengths and other rich engagements. The source of Domain`s ecosystem for revenues

are residential, commercial, print, transactions, media, developers and agent services. In

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

regards to foresee the growth, it is seen that company delivers a revenue growth of 11.5

percent until $357.3. This is the reflection of the strong performance of the digital sector. The

earnings before interest and tax has increased by 12.5 percent to 115.7 million dollars.

Descriptions of Accounting Concepts

Accrual concept- it is necessary to know that financial statements are prepared under the

concept of accrual concept that necessitates that income and expense are further recognised in

the fixed fiscal period that is related to cash related transaction. One of the main exception

related accrual basis is the cash flow statement where the main purpose is related to cash flow

effect of the transaction.

Domain measures revenue as per the accrual basis with the substance of the relevant

agreements. The amount that has been disclosed as revenues are rebates, commissions and

discounts that are to be recognised while considering the reliable measurement. Revenue has

been identified on the basis of accruals as per the substance of the related agreements. As

soon as the cash is received in regards to income in advance where the cash is received but

the service is deferred to be performed. Income in advance will be considered as the goods in

advance.

Full disclosure concept- this accounting concept describes that there should be relevant

information that will be disclosed in the statements. This will help a number of the external

users will depend on financial statements to give information to the investors to invest. In

regards to this, any contingent liability will be transferred under the recognition of fair value

in the acquisition date.

When the company acquires an organisation that assesse financial assets and the liabilities

expected for the classification and the designation as per the economic conditions and

percent until $357.3. This is the reflection of the strong performance of the digital sector. The

earnings before interest and tax has increased by 12.5 percent to 115.7 million dollars.

Descriptions of Accounting Concepts

Accrual concept- it is necessary to know that financial statements are prepared under the

concept of accrual concept that necessitates that income and expense are further recognised in

the fixed fiscal period that is related to cash related transaction. One of the main exception

related accrual basis is the cash flow statement where the main purpose is related to cash flow

effect of the transaction.

Domain measures revenue as per the accrual basis with the substance of the relevant

agreements. The amount that has been disclosed as revenues are rebates, commissions and

discounts that are to be recognised while considering the reliable measurement. Revenue has

been identified on the basis of accruals as per the substance of the related agreements. As

soon as the cash is received in regards to income in advance where the cash is received but

the service is deferred to be performed. Income in advance will be considered as the goods in

advance.

Full disclosure concept- this accounting concept describes that there should be relevant

information that will be disclosed in the statements. This will help a number of the external

users will depend on financial statements to give information to the investors to invest. In

regards to this, any contingent liability will be transferred under the recognition of fair value

in the acquisition date.

When the company acquires an organisation that assesse financial assets and the liabilities

expected for the classification and the designation as per the economic conditions and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

contractual terms. The group`s accounting policies and operating conditions on the

acquisition date.

Matching concept- This concept cross checks each of the transaction especially. It is related

to cause and effect relationship in regards to the specific expenses and revenues and record

them at the same time. As there is no relationship while charging the cost to each of the

expense at once. It is one of the crucial concept that mandates the total effect of each

transaction has to recorded in the same reporting and accounting period.

While measuring the fair value of the assets, it is seen that the company follows appropriate

policy for trade receivable as they are identified on the fair value and they are subsequently

evaluated on the amortised costs that is at the original invoice that is less than the allowance

for the uncollectable amount. Collection of trade receivables is analysed on the basis of

ongoing concept. Further, provisions for the PDD (provisions for doubtful debts) is identified

as when there is an objective proof that the group will not be able to collect those debts.

Conservatism- This concept provides careful insight in accounting procedure. It says that

profit will not be included until it is not realised. Losses that are not realised but it will be

included in occurrence in the financial reports of the company. Another instance and

application of this concept is that recording of the asset will always be recorded at historical

cost rather than market price. Although, it will realised at the market price but it will be

recorded at whichever is low.

The company considers and identifies accounting standards that prioritises provisions as a

legal, constructive duty and obligation that are obliged to sacrifice benefit in terms of

economic that are required to reliable estimation that can be based on the payment of duty.

These provisions are not further recognised while evaluating operating losses.

acquisition date.

Matching concept- This concept cross checks each of the transaction especially. It is related

to cause and effect relationship in regards to the specific expenses and revenues and record

them at the same time. As there is no relationship while charging the cost to each of the

expense at once. It is one of the crucial concept that mandates the total effect of each

transaction has to recorded in the same reporting and accounting period.

While measuring the fair value of the assets, it is seen that the company follows appropriate

policy for trade receivable as they are identified on the fair value and they are subsequently

evaluated on the amortised costs that is at the original invoice that is less than the allowance

for the uncollectable amount. Collection of trade receivables is analysed on the basis of

ongoing concept. Further, provisions for the PDD (provisions for doubtful debts) is identified

as when there is an objective proof that the group will not be able to collect those debts.

Conservatism- This concept provides careful insight in accounting procedure. It says that

profit will not be included until it is not realised. Losses that are not realised but it will be

included in occurrence in the financial reports of the company. Another instance and

application of this concept is that recording of the asset will always be recorded at historical

cost rather than market price. Although, it will realised at the market price but it will be

recorded at whichever is low.

The company considers and identifies accounting standards that prioritises provisions as a

legal, constructive duty and obligation that are obliged to sacrifice benefit in terms of

economic that are required to reliable estimation that can be based on the payment of duty.

These provisions are not further recognised while evaluating operating losses.

Provisions that are measured on the basis of the present value of the management`s

estimation of best expenditure which is required to settlement with the present duty at the

fiscal date by using the discounted cash flow. Accomplishment with such risk-free corporate

and government bond rate that is relative to expected life of provision that are factored into

cash flows where time value of money is provisioned and material by using the current pre-

tax rate that directly specifies to the liability. With the increase in the provision with the

passage of time will be recognised as finance cost. With the provisions are not recognisable

within the liability until dividend is declared after determining the publicly recommendation

either on or before the reporting date (Schulze, Nehler, Ottosson, and Thollander, 2016).

Business entity concept- This concept is on the basis of accounting purposes where

organisation and the owners are two separate entities. This concept helps in ascertaining the

revenue of the organisation as expenses, profits have recorded, and personal expenses are not

considered. This concept also ensures that organisation will continue to operate its business

operations in a definite period. This concept helps the organisation assists to formulate

financial statements. For example- this concept decides the depreciation on fixed asset

(Schulze, Nehler, Ottosson, and Thollander, 2016).

AASB 3 combination allows the measurement per the time after the business combination in

a way provide acquirer a proper time to get the information in regards to find and evaluate the

various components of combination of business on the acquisition date.

Materiality concept- This concept states that all the material facts should be the part of

accounting process. Some of the immaterial facts is that insignificant information would left

out. It is important to know materiality will depend on the nature, significance, and the value

to the external stakeholders. Material information is significant, as it will affect the

investment decision of the person (Schulze, Nehler, Ottosson, and Thollander, 2016).

estimation of best expenditure which is required to settlement with the present duty at the

fiscal date by using the discounted cash flow. Accomplishment with such risk-free corporate

and government bond rate that is relative to expected life of provision that are factored into

cash flows where time value of money is provisioned and material by using the current pre-

tax rate that directly specifies to the liability. With the increase in the provision with the

passage of time will be recognised as finance cost. With the provisions are not recognisable

within the liability until dividend is declared after determining the publicly recommendation

either on or before the reporting date (Schulze, Nehler, Ottosson, and Thollander, 2016).

Business entity concept- This concept is on the basis of accounting purposes where

organisation and the owners are two separate entities. This concept helps in ascertaining the

revenue of the organisation as expenses, profits have recorded, and personal expenses are not

considered. This concept also ensures that organisation will continue to operate its business

operations in a definite period. This concept helps the organisation assists to formulate

financial statements. For example- this concept decides the depreciation on fixed asset

(Schulze, Nehler, Ottosson, and Thollander, 2016).

AASB 3 combination allows the measurement per the time after the business combination in

a way provide acquirer a proper time to get the information in regards to find and evaluate the

various components of combination of business on the acquisition date.

Materiality concept- This concept states that all the material facts should be the part of

accounting process. Some of the immaterial facts is that insignificant information would left

out. It is important to know materiality will depend on the nature, significance, and the value

to the external stakeholders. Material information is significant, as it will affect the

investment decision of the person (Schulze, Nehler, Ottosson, and Thollander, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

On the basis of preliminary analysis, the effect on the group for new requirement, it is seen

that recognition is based on expected credit loss that is not anticipated to have material effect

on balance sheet and income statement.

Conceptual framework and the Issue of Measurement

On the basis of preparation, it is seen that there are several new accounting standards that

have been issued but not applied yet. Inclusive of those effective reporting period, the

company has not applied AASB 9 for the financial instruments for June 2019. AASB 9 has

led to replacement of AASB 139 for the financial instruments. It is seen that recognition,

clarification, impairment, hedging accounting and the measurement of the financial

accounting. Moreover, the company does not expect any material impact on balance sheet

and equity by applying the measurement and classification of the AASB 9 (Schulze, Nehler,

Ottosson, and Thollander, 2016).

The company accounts for the liquidity risk as the company is not able to m meet its

obligation and other financial commitments as the AASB9 for the financial instruments. At

this time, the company does not have any appropriate credit risk exposures related to the

group of the individual customers and the financial institution (Schulze, Nehler, Ottosson,

and Thollander, 2016). In order to treat such risk, it is seen that company`s financial assets

are considered and impaired when there is an objective proof where the group is not able to

collect all the relevant amount due as per the original trading and other receivable terms and

conditions. Certain trading terms and counter parties. The company trading terms are not

related to the requirement of the customers in order provide collateral security for the

financial assets (Walton, 2016).

that recognition is based on expected credit loss that is not anticipated to have material effect

on balance sheet and income statement.

Conceptual framework and the Issue of Measurement

On the basis of preparation, it is seen that there are several new accounting standards that

have been issued but not applied yet. Inclusive of those effective reporting period, the

company has not applied AASB 9 for the financial instruments for June 2019. AASB 9 has

led to replacement of AASB 139 for the financial instruments. It is seen that recognition,

clarification, impairment, hedging accounting and the measurement of the financial

accounting. Moreover, the company does not expect any material impact on balance sheet

and equity by applying the measurement and classification of the AASB 9 (Schulze, Nehler,

Ottosson, and Thollander, 2016).

The company accounts for the liquidity risk as the company is not able to m meet its

obligation and other financial commitments as the AASB9 for the financial instruments. At

this time, the company does not have any appropriate credit risk exposures related to the

group of the individual customers and the financial institution (Schulze, Nehler, Ottosson,

and Thollander, 2016). In order to treat such risk, it is seen that company`s financial assets

are considered and impaired when there is an objective proof where the group is not able to

collect all the relevant amount due as per the original trading and other receivable terms and

conditions. Certain trading terms and counter parties. The company trading terms are not

related to the requirement of the customers in order provide collateral security for the

financial assets (Walton, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

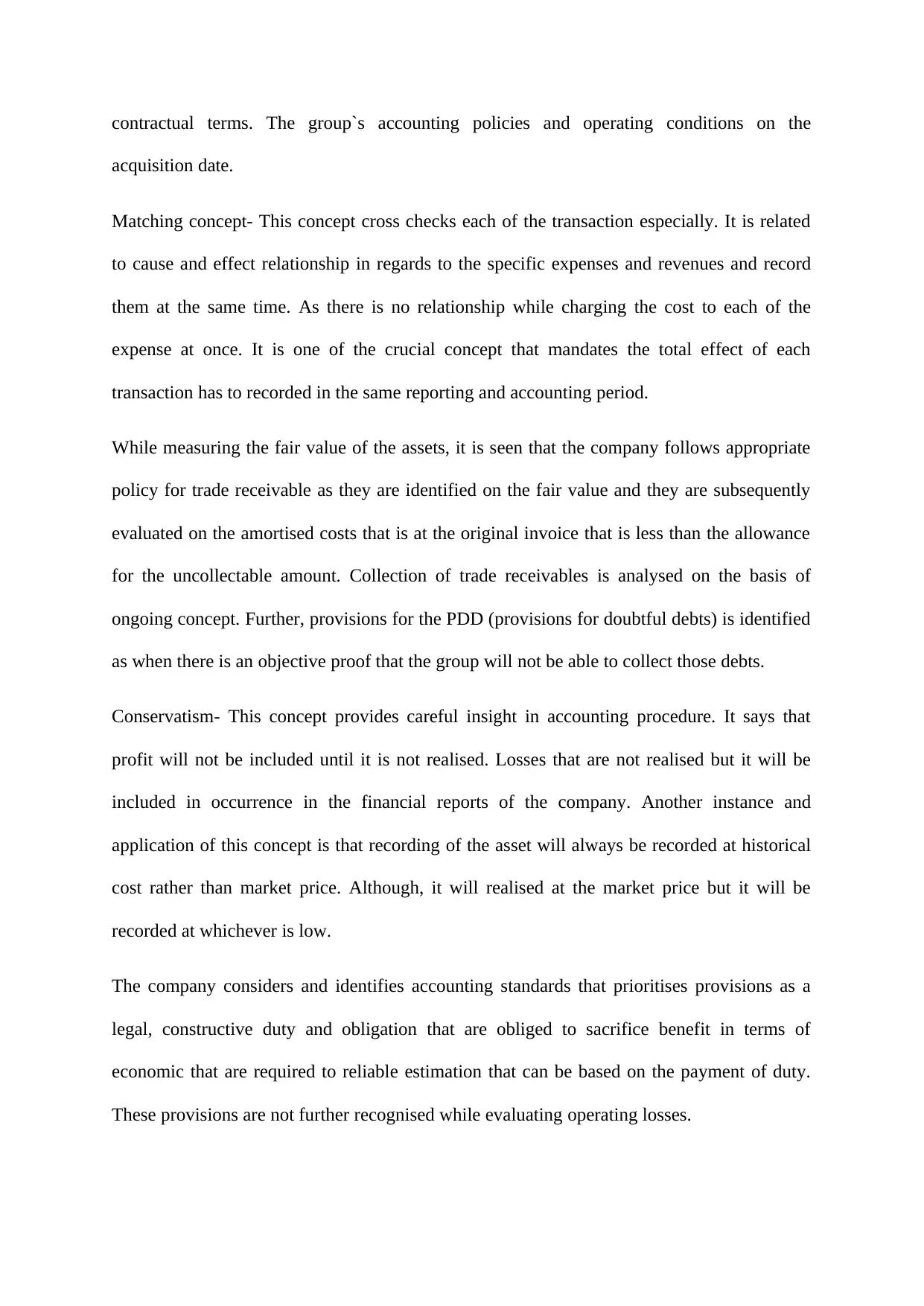

(Source: Domain Holdings Australia Limited, 2018)

While considering accounting policies for the intangible assets, it is seen that the company`s

brand name operate with the limited conditions and further it is expected that it will continue

to accomplish to compliment new initiatives. The issue related to the intangible assets is that

there is not appropriate foreseeable limit to the period and it also has indefinite useful live as

the assets are expected to generate net cash flows in the group. The assets are not even

amortised but are tested as per impairment annually. Trademarks are assessed on the basis of

definite life that are further amortised on the basis of straight line method.

The main purpose of the conceptual framework is to assist international accounting standard

board (IASB) in the development of IFRS and also while reviewing the existing IFRS. This

framework helps the management while preparing the financial statements to comply with the

accounting policies for the transactions and other events, which are not covered in the

existi8ng accounting standards.

Fundamental Qualitative Characteristics

While considering accounting policies for the intangible assets, it is seen that the company`s

brand name operate with the limited conditions and further it is expected that it will continue

to accomplish to compliment new initiatives. The issue related to the intangible assets is that

there is not appropriate foreseeable limit to the period and it also has indefinite useful live as

the assets are expected to generate net cash flows in the group. The assets are not even

amortised but are tested as per impairment annually. Trademarks are assessed on the basis of

definite life that are further amortised on the basis of straight line method.

The main purpose of the conceptual framework is to assist international accounting standard

board (IASB) in the development of IFRS and also while reviewing the existing IFRS. This

framework helps the management while preparing the financial statements to comply with the

accounting policies for the transactions and other events, which are not covered in the

existi8ng accounting standards.

Fundamental Qualitative Characteristics

Understanding of Relevance- This characteristic reveals that information should be readily

understanding to the people who can use financial statements. This illustrates that the data

should be represented clearly with all the additional data given in the footnotes or the

supporting notes as needed to clarify each of the transaction (Eldridge et al., 2016).

The group describes that when identifying the operating segment on the basis of internal

reports (Giner, Hellman, Jorissen, Quagli, and Taleb, 2016). When reporting regarding the

segment of transaction and digital services, the company connects to the services that is

relevant to the segment for the different property lifecycle stages, commercial utilities

connections, residential, insurance, home loans and trade services (Domain Holdings

Australia Limited, 2017).

Impairment as per the annual reports is estimated as $11.9 million with the goodwill of nearly

$ 4.7 million, other assets as 0.7 million dollars and the equity accountable investment as

$12.3 million were finally recognised with the following-

Decisions to exit in order to certain the business in the period.

Destruction of value of the investment with the decline in the value of market where they

operate.

These crucial changes will lead to re-assessment of the carrying amount of the related assets

in order to ensure the carrying valuation, which does not exceed the recoverable value of

assets (Domain Holdings Australia Limited, 2017). It is visible that recoverable account will

be determined to less than as compared to the carrying value (impairment charge) that has

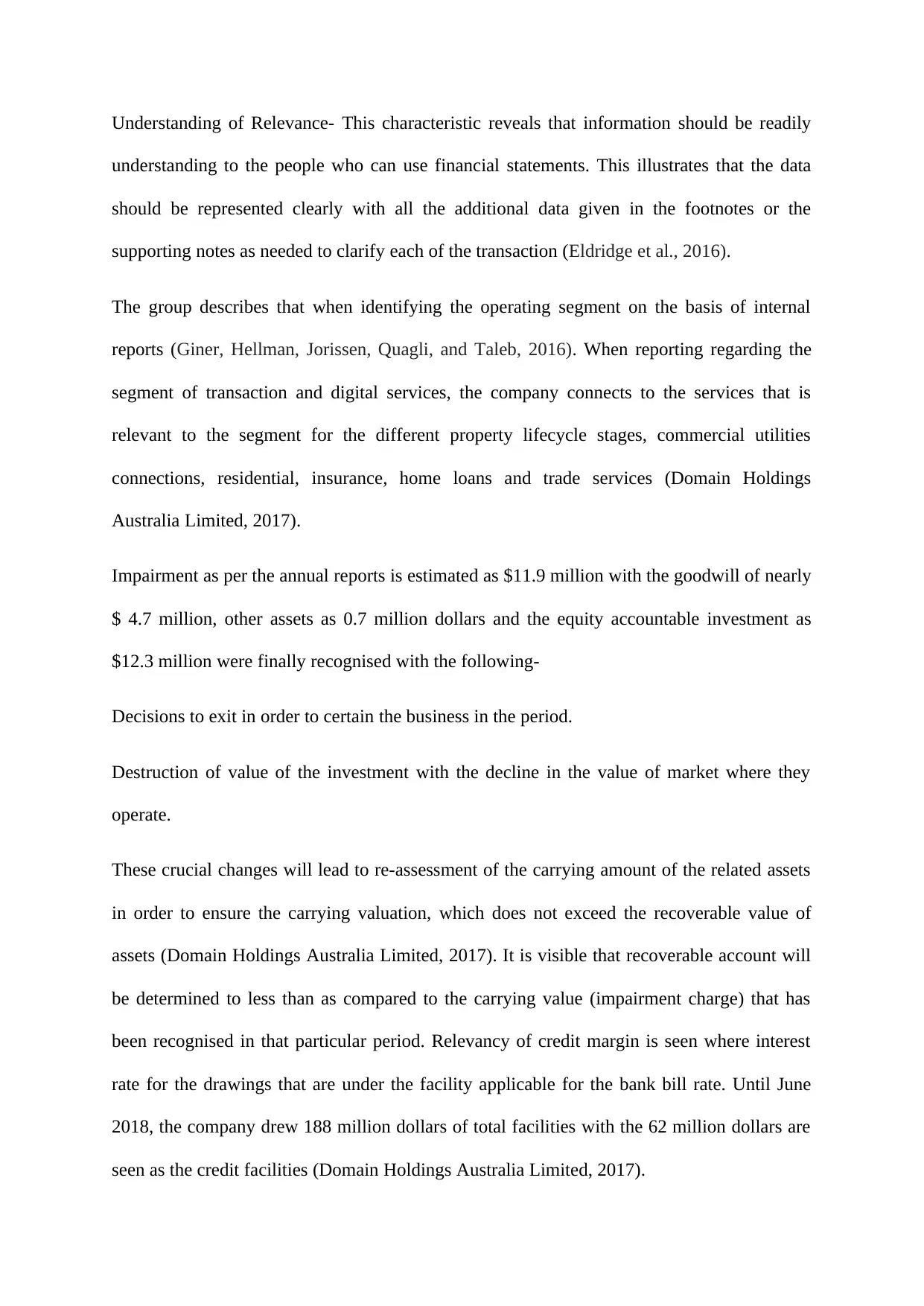

been recognised in that particular period. Relevancy of credit margin is seen where interest

rate for the drawings that are under the facility applicable for the bank bill rate. Until June

2018, the company drew 188 million dollars of total facilities with the 62 million dollars are

seen as the credit facilities (Domain Holdings Australia Limited, 2017).

understanding to the people who can use financial statements. This illustrates that the data

should be represented clearly with all the additional data given in the footnotes or the

supporting notes as needed to clarify each of the transaction (Eldridge et al., 2016).

The group describes that when identifying the operating segment on the basis of internal

reports (Giner, Hellman, Jorissen, Quagli, and Taleb, 2016). When reporting regarding the

segment of transaction and digital services, the company connects to the services that is

relevant to the segment for the different property lifecycle stages, commercial utilities

connections, residential, insurance, home loans and trade services (Domain Holdings

Australia Limited, 2017).

Impairment as per the annual reports is estimated as $11.9 million with the goodwill of nearly

$ 4.7 million, other assets as 0.7 million dollars and the equity accountable investment as

$12.3 million were finally recognised with the following-

Decisions to exit in order to certain the business in the period.

Destruction of value of the investment with the decline in the value of market where they

operate.

These crucial changes will lead to re-assessment of the carrying amount of the related assets

in order to ensure the carrying valuation, which does not exceed the recoverable value of

assets (Domain Holdings Australia Limited, 2017). It is visible that recoverable account will

be determined to less than as compared to the carrying value (impairment charge) that has

been recognised in that particular period. Relevancy of credit margin is seen where interest

rate for the drawings that are under the facility applicable for the bank bill rate. Until June

2018, the company drew 188 million dollars of total facilities with the 62 million dollars are

seen as the credit facilities (Domain Holdings Australia Limited, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Source: Domain Holdings Australia Limited, 2018)

(Source: Domain Holdings Australia Limited, 2018)

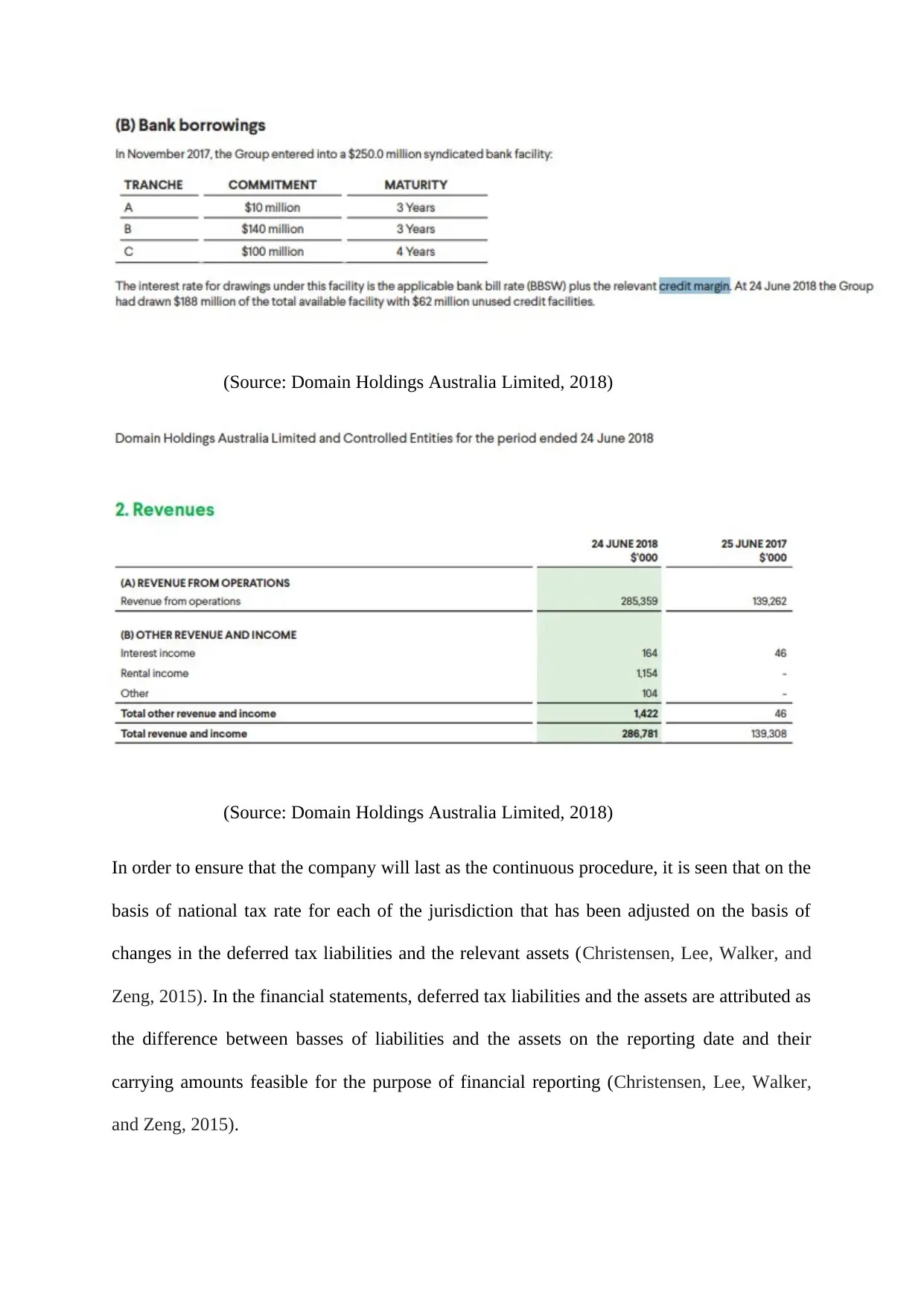

In order to ensure that the company will last as the continuous procedure, it is seen that on the

basis of national tax rate for each of the jurisdiction that has been adjusted on the basis of

changes in the deferred tax liabilities and the relevant assets (Christensen, Lee, Walker, and

Zeng, 2015). In the financial statements, deferred tax liabilities and the assets are attributed as

the difference between basses of liabilities and the assets on the reporting date and their

carrying amounts feasible for the purpose of financial reporting (Christensen, Lee, Walker,

and Zeng, 2015).

(Source: Domain Holdings Australia Limited, 2018)

In order to ensure that the company will last as the continuous procedure, it is seen that on the

basis of national tax rate for each of the jurisdiction that has been adjusted on the basis of

changes in the deferred tax liabilities and the relevant assets (Christensen, Lee, Walker, and

Zeng, 2015). In the financial statements, deferred tax liabilities and the assets are attributed as

the difference between basses of liabilities and the assets on the reporting date and their

carrying amounts feasible for the purpose of financial reporting (Christensen, Lee, Walker,

and Zeng, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Representational Faithfulness- From the concept of conceptual framework, it is seen that

information should be quite relevant to the needs of the users. The information will affect the

economic decision of the users (Carneiro, Rodrigues, and Craig, 2017). The representation

should be based on materiality and it should be bias free, error free and parted from

misleading. This will include relevant information and the information where omission

misstatement will influence the investment decision (Kim, and Zhang, 2016).

The company has undertaken fair value measurement of the financial liabilities that has been

reported on the accounting date. In relation to the Accounting policy, it is seen that a

subsequent initial recognition for the fair value (Li, 2015). The company has been reporting

fair transaction cost incurrence and liabilities bearing interest are further measured at the

amortised cost. Any type of difference incurred between the proceeds and the redemption of

the amount recognized in the net of the transaction costs and the redemption amount relatable

to recognised income statement in the period of borrowing by using the effective interest type

(Christensen, Lee, Walker, and Zeng, 2015).

As of Corporation Act, 2001, it is seen that domain acquires legacy of assets and liabilities

from the relevant entities complied within the consolidated group “Fairfax” as the

consolidated group with the consideration of $1279 million dollars. The process of

acquisition of assets have been treated as the corporation combination with the recognition of

the fair values of the assets on the acquiring date (Simone, 2016). It is seen that the revenue

evaluation has been examined under the accounting standards where it is quite probable that

economic benefits will transfer to the whole group and it is reliably measured without

thinking when the payment has been received. It is seen that the company measures revenue

has measured fair value of the consideration once received by taking into account the

contractual defined concepts by excluding the duty and the taxes (Simone, 2016).

information should be quite relevant to the needs of the users. The information will affect the

economic decision of the users (Carneiro, Rodrigues, and Craig, 2017). The representation

should be based on materiality and it should be bias free, error free and parted from

misleading. This will include relevant information and the information where omission

misstatement will influence the investment decision (Kim, and Zhang, 2016).

The company has undertaken fair value measurement of the financial liabilities that has been

reported on the accounting date. In relation to the Accounting policy, it is seen that a

subsequent initial recognition for the fair value (Li, 2015). The company has been reporting

fair transaction cost incurrence and liabilities bearing interest are further measured at the

amortised cost. Any type of difference incurred between the proceeds and the redemption of

the amount recognized in the net of the transaction costs and the redemption amount relatable

to recognised income statement in the period of borrowing by using the effective interest type

(Christensen, Lee, Walker, and Zeng, 2015).

As of Corporation Act, 2001, it is seen that domain acquires legacy of assets and liabilities

from the relevant entities complied within the consolidated group “Fairfax” as the

consolidated group with the consideration of $1279 million dollars. The process of

acquisition of assets have been treated as the corporation combination with the recognition of

the fair values of the assets on the acquiring date (Simone, 2016). It is seen that the revenue

evaluation has been examined under the accounting standards where it is quite probable that

economic benefits will transfer to the whole group and it is reliably measured without

thinking when the payment has been received. It is seen that the company measures revenue

has measured fair value of the consideration once received by taking into account the

contractual defined concepts by excluding the duty and the taxes (Simone, 2016).

Conclusion

From the above discussion, it can be concluded that Domain Holdings Group account as per

the Corporation Act, 2001. As per the Auditor`s report, the company have complied with all

the necessary accounting standards. It has been noticed that Domain holding limited has

prepared its annual reports in regards to compliance of the AASB (Australian Accounting

standard Board). The operations of the organised group, which are arranged as per the

recording in base, group with the usage of consistent accounting procedures and accounting

policies. The purpose of the study is to identify and comply with the accounting information

and its relation to data in the light of three main level of analysis such as measurement,

recognition, and its relation to the conceptual framework. Recently, the company has

recognised and identified AASB 9 and 15 so that it can conduct proper accounting for

financial instruments and its related treatment of the revenues received from the customers in

the name of contract.

From the above discussion, it can be concluded that Domain Holdings Group account as per

the Corporation Act, 2001. As per the Auditor`s report, the company have complied with all

the necessary accounting standards. It has been noticed that Domain holding limited has

prepared its annual reports in regards to compliance of the AASB (Australian Accounting

standard Board). The operations of the organised group, which are arranged as per the

recording in base, group with the usage of consistent accounting procedures and accounting

policies. The purpose of the study is to identify and comply with the accounting information

and its relation to data in the light of three main level of analysis such as measurement,

recognition, and its relation to the conceptual framework. Recently, the company has

recognised and identified AASB 9 and 15 so that it can conduct proper accounting for

financial instruments and its related treatment of the revenues received from the customers in

the name of contract.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.