HA3011 Advanced Financial Accounting: Analysis of Financial Reports

VerifiedAdded on 2023/04/04

|12

|2454

|142

Report

AI Summary

This assignment analyzes the financial accounting practices of the New Hope Foundation Group, an Australian Stock Exchange (ASX) listed company, focusing on the application of accounting concepts and the conceptual framework in preparing and presenting financial reports. The report identifies key accounting concepts such as materiality, going concern, accrual, periodicity, consistency, and business entity concepts, demonstrating their integration within the company's financial reporting. It examines the company's adherence to the Generally Accepted Accounting Principles (GAAP), the measurement issues, and the qualitative characteristics of relevance and representational faithfulness. The report assesses how the company complies with the accounting standards and provides a conclusion on the overall application of accounting concepts and their relevance in financial reporting.

2019

HA3011

aDVANCED financial accounting

HA3011

aDVANCED financial accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Abstract

This assignment primarily aims at identifying and analysing the accounting concepts which are used

in preparing and presenting financial reports by an Australian Stock Exchange (ASX) Listed company

“New Hope Foundation Group”.

In addition, the conceptual framework involved in making of accounting policies has been shown.

The financial reports by the company has been studied in details and a brief note has been given

regarding the framework of reporting which has been used in financial reports.

The fundamental qualitative characteristics has been studied in the historical financial reports of this

company. The same has been studied to understand its relevance and representational faithfulness

in the financial matters reported by the company in its annual report of 2018.

A conclusion has been drawn on the overall assignment regarding the concepts used and shown

while preparing and presenting this annual report and the relevance of accounting concepts and its

framework in preparation and presentation of financial reports of a company.

1 | P a g e

This assignment primarily aims at identifying and analysing the accounting concepts which are used

in preparing and presenting financial reports by an Australian Stock Exchange (ASX) Listed company

“New Hope Foundation Group”.

In addition, the conceptual framework involved in making of accounting policies has been shown.

The financial reports by the company has been studied in details and a brief note has been given

regarding the framework of reporting which has been used in financial reports.

The fundamental qualitative characteristics has been studied in the historical financial reports of this

company. The same has been studied to understand its relevance and representational faithfulness

in the financial matters reported by the company in its annual report of 2018.

A conclusion has been drawn on the overall assignment regarding the concepts used and shown

while preparing and presenting this annual report and the relevance of accounting concepts and its

framework in preparation and presentation of financial reports of a company.

1 | P a g e

Contents

Abstract.................................................................................................................................................1

Introduction...........................................................................................................................................3

Accounting Concepts and Its Utilisation in Financial Reporting.............................................................3

Conceptual Framework and the issue of measurement........................................................................7

Fundamental Qualitative Characteristics – Understanding of relevance and representational

faithfulness............................................................................................................................................8

Conclusion.............................................................................................................................................9

References...........................................................................................................................................10

2 | P a g e

Abstract.................................................................................................................................................1

Introduction...........................................................................................................................................3

Accounting Concepts and Its Utilisation in Financial Reporting.............................................................3

Conceptual Framework and the issue of measurement........................................................................7

Fundamental Qualitative Characteristics – Understanding of relevance and representational

faithfulness............................................................................................................................................8

Conclusion.............................................................................................................................................9

References...........................................................................................................................................10

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

The accounting concepts are integrated in the company’s financial reports which have been

identified by considering its annual report for 2018. The key significant accounting concepts

considered by this company while presentation of financial reports are the fundamental accounting

concepts such as materiality concept, going concern concept, accrual concept, and other concepts of

accounting such as periodicity concept, consistency, accrual and even business entity concept.

The company has taken into account the consideration, the reporting principles along with the

concepts of accounting. The qualitative characteristics observed in this historical financial report of

the company is the completeness and the relevant disclosures have been made in accordance with

the standards on accounting that applies for this company (Almasi, et al., 2018).

These financial reports of the company are prepared based on the financial reporting framework

where it contains a set of rules and regulations aligning with principles of accounting and accounting

concepts, thereby providing a basis for reporting any kind of financial transactions within the

company. From time to time, based on relevance and requirements as per the regulatory

requirement revises the company keeps on revising the way of presentation.

The company has a well set corporate governance framework to look into affairs of company and

reporting standards and that the internal controls are operating effectively within the company. This

is an added advantage for a company to comply with accounting requirement of regulatory body

(Andiola, et al., 2018).

Accounting Concepts and Its Utilisation in Financial Reporting

The accounting concepts used by company mentioned above includes going concern concept,

accrual, and consistency, some of which has been briefly described in below points

Business Entity Concept

This company has transactions dealing with related parties. As per existing accounting

policies of company and its financial framework for reporting, these are shown separately in

historical financial reports and appropriate disclosure are made in accordance with

Corporations Act 2001.

As per Business entity concept, a company is different from its owner. In nonprofessional

terms the accounting of business is separate for the company and the business of the owner

is separate for himself (Belton, 2017).

Further, this concept tells that recording a transaction of owner in accounts of the company

should be accounted as an outsider and third party to the company; owner should be

treated as shareholders in the books of the company.

3 | P a g e

The accounting concepts are integrated in the company’s financial reports which have been

identified by considering its annual report for 2018. The key significant accounting concepts

considered by this company while presentation of financial reports are the fundamental accounting

concepts such as materiality concept, going concern concept, accrual concept, and other concepts of

accounting such as periodicity concept, consistency, accrual and even business entity concept.

The company has taken into account the consideration, the reporting principles along with the

concepts of accounting. The qualitative characteristics observed in this historical financial report of

the company is the completeness and the relevant disclosures have been made in accordance with

the standards on accounting that applies for this company (Almasi, et al., 2018).

These financial reports of the company are prepared based on the financial reporting framework

where it contains a set of rules and regulations aligning with principles of accounting and accounting

concepts, thereby providing a basis for reporting any kind of financial transactions within the

company. From time to time, based on relevance and requirements as per the regulatory

requirement revises the company keeps on revising the way of presentation.

The company has a well set corporate governance framework to look into affairs of company and

reporting standards and that the internal controls are operating effectively within the company. This

is an added advantage for a company to comply with accounting requirement of regulatory body

(Andiola, et al., 2018).

Accounting Concepts and Its Utilisation in Financial Reporting

The accounting concepts used by company mentioned above includes going concern concept,

accrual, and consistency, some of which has been briefly described in below points

Business Entity Concept

This company has transactions dealing with related parties. As per existing accounting

policies of company and its financial framework for reporting, these are shown separately in

historical financial reports and appropriate disclosure are made in accordance with

Corporations Act 2001.

As per Business entity concept, a company is different from its owner. In nonprofessional

terms the accounting of business is separate for the company and the business of the owner

is separate for himself (Belton, 2017).

Further, this concept tells that recording a transaction of owner in accounts of the company

should be accounted as an outsider and third party to the company; owner should be

treated as shareholders in the books of the company.

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This concept is followed by company as its integrated into the reporting of financial reports.

Furthermore it has been analysed that all related party transactions disclosed by company

relates to shareholders or directors of company which tells clearly the importance of

integrating business entity concept in field of accounting for reporting of financial

statements by the company.

Matching Concept

This concept is also integrated into financial reports of company. As per this all the cost

which have been incurred by the company for earning the revenue during the given period

should be shown in the books of acocunts (Hepp, 2018).

The matching concept eliminates the concept of omission of accounting elements by posting

dual aspect of accounting instead of only one aspect of accounting. It tells that a transaction

reported needs to match with transaction happening in the actual course of business.

Dual Aspect Concept

This concept tells about the importance of accounting a transaction in both the aspects of a

transaction based on golden rules of accounting, which tells about accounting for personal

accounts like natural persons, artificial persons, and Representative personal accounts.

While analysing the historical financial reports of this company it understood that basics of

preparation of accounts and financial reports have been well maintained by company and

accounting has been done considering the dual aspects of a transaction such as the debit

aspect and credit aspect involved in a transaction (Dichev, 2017).

Periodicity Concept

This concept shows importance of consistency in reporting of financial reports of

company for the defined period, which include monthly reporting, quarterly reporting,

yearly reporting and sometimes few companies even follow half-yearly reporting based on

requirement of stake-holders at large.

Also based on regulatory requirements such as for calculation of tax, the reports are

prepared periodically and maintained for consistency in preparing and presenting financial

reports in a well manner over different period (Loftus, et al., 2018). This also helps in making

the financial statements comparable over the period.

The other accounting concepts followed by company include fundamental accounting concepts such

as accrual, consistency and going concern.

Accrual means a financial statement should contain the transactions made not only on cash basis but

on credit basis as well.

Consistency means the transactions has to be recorded in accordance with accounting policies

followed by company and there should be no deviation in following such accounting policies. In case

the deviation arises, it would lead to inconsistent financial reporting leading to non-standardised

accounting reports.

4 | P a g e

Furthermore it has been analysed that all related party transactions disclosed by company

relates to shareholders or directors of company which tells clearly the importance of

integrating business entity concept in field of accounting for reporting of financial

statements by the company.

Matching Concept

This concept is also integrated into financial reports of company. As per this all the cost

which have been incurred by the company for earning the revenue during the given period

should be shown in the books of acocunts (Hepp, 2018).

The matching concept eliminates the concept of omission of accounting elements by posting

dual aspect of accounting instead of only one aspect of accounting. It tells that a transaction

reported needs to match with transaction happening in the actual course of business.

Dual Aspect Concept

This concept tells about the importance of accounting a transaction in both the aspects of a

transaction based on golden rules of accounting, which tells about accounting for personal

accounts like natural persons, artificial persons, and Representative personal accounts.

While analysing the historical financial reports of this company it understood that basics of

preparation of accounts and financial reports have been well maintained by company and

accounting has been done considering the dual aspects of a transaction such as the debit

aspect and credit aspect involved in a transaction (Dichev, 2017).

Periodicity Concept

This concept shows importance of consistency in reporting of financial reports of

company for the defined period, which include monthly reporting, quarterly reporting,

yearly reporting and sometimes few companies even follow half-yearly reporting based on

requirement of stake-holders at large.

Also based on regulatory requirements such as for calculation of tax, the reports are

prepared periodically and maintained for consistency in preparing and presenting financial

reports in a well manner over different period (Loftus, et al., 2018). This also helps in making

the financial statements comparable over the period.

The other accounting concepts followed by company include fundamental accounting concepts such

as accrual, consistency and going concern.

Accrual means a financial statement should contain the transactions made not only on cash basis but

on credit basis as well.

Consistency means the transactions has to be recorded in accordance with accounting policies

followed by company and there should be no deviation in following such accounting policies. In case

the deviation arises, it would lead to inconsistent financial reporting leading to non-standardised

accounting reports.

4 | P a g e

Based on observation, it is clear the given company has maintained consistency in maintaining the

same accounting policies over period.

Accounting of financial reports needs a change based on nature of business as per accounting

concepts that shows the way to account for a transaction in financial reports of an entity (Smith,

2015).

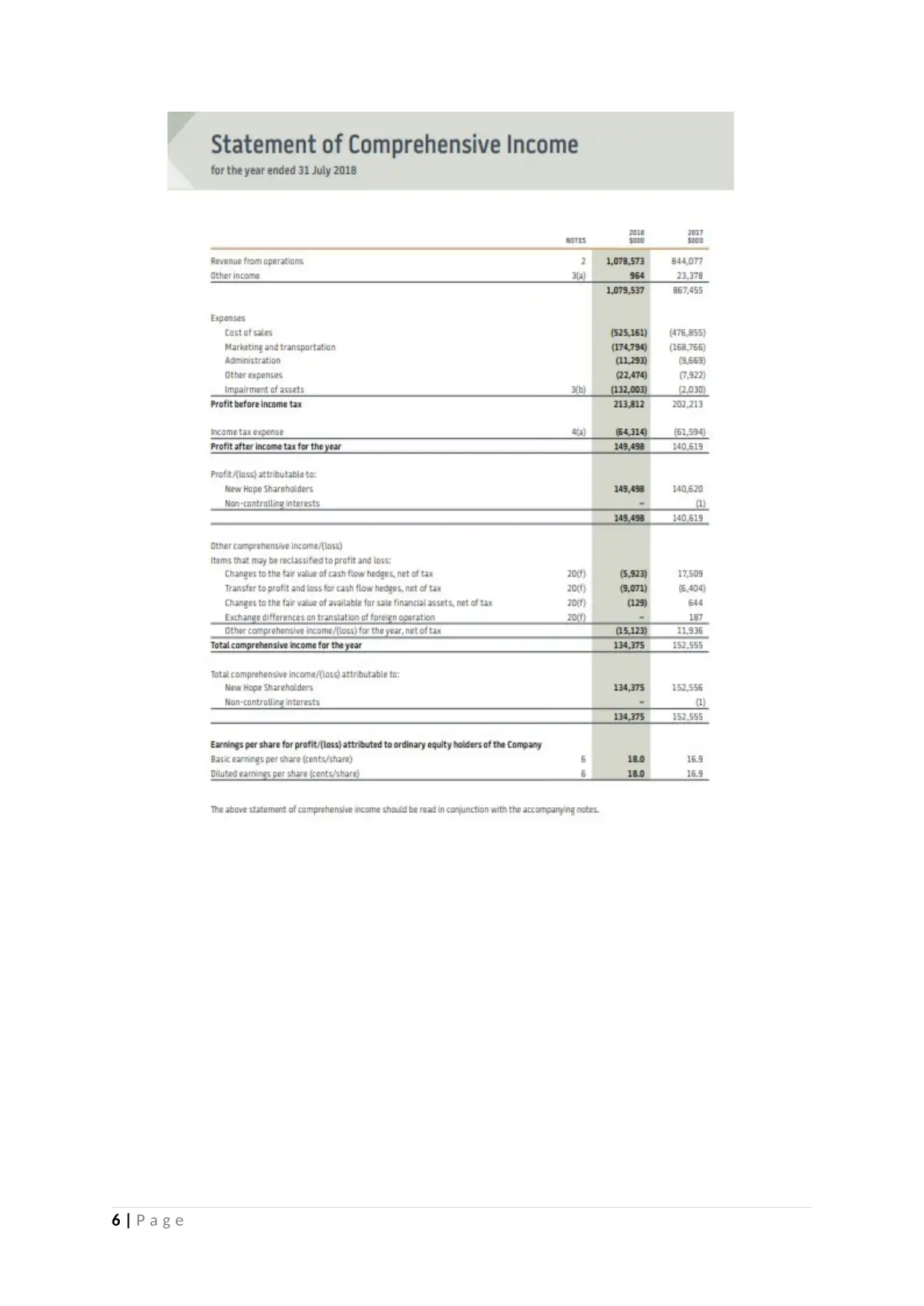

The accounting concepts followed by company can be seen in the screenshot from the annual report

of the company where above mentioned accounting concepts are followed on consistent basis by

entity based on past analysis.

Other accounting concepts such as materiality has also been followed by entity while reporting in its

financial reports and disclosed in notes to accounts accordingly.

5 | P a g e

same accounting policies over period.

Accounting of financial reports needs a change based on nature of business as per accounting

concepts that shows the way to account for a transaction in financial reports of an entity (Smith,

2015).

The accounting concepts followed by company can be seen in the screenshot from the annual report

of the company where above mentioned accounting concepts are followed on consistent basis by

entity based on past analysis.

Other accounting concepts such as materiality has also been followed by entity while reporting in its

financial reports and disclosed in notes to accounts accordingly.

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

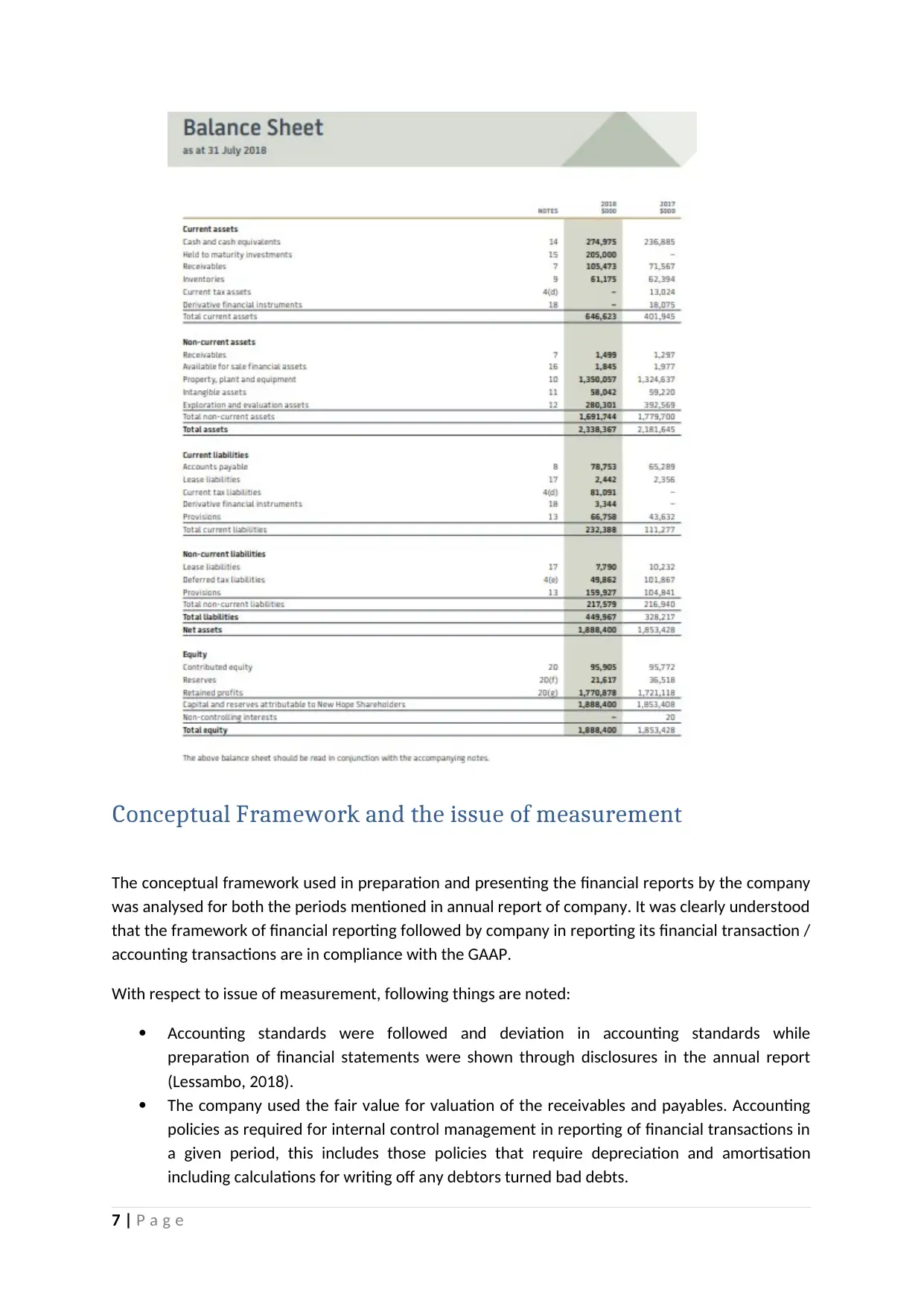

Conceptual Framework and the issue of measurement

The conceptual framework used in preparation and presenting the financial reports by the company

was analysed for both the periods mentioned in annual report of company. It was clearly understood

that the framework of financial reporting followed by company in reporting its financial transaction /

accounting transactions are in compliance with the GAAP.

With respect to issue of measurement, following things are noted:

Accounting standards were followed and deviation in accounting standards while

preparation of financial statements were shown through disclosures in the annual report

(Lessambo, 2018).

The company used the fair value for valuation of the receivables and payables. Accounting

policies as required for internal control management in reporting of financial transactions in

a given period, this includes those policies that require depreciation and amortisation

including calculations for writing off any debtors turned bad debts.

7 | P a g e

The conceptual framework used in preparation and presenting the financial reports by the company

was analysed for both the periods mentioned in annual report of company. It was clearly understood

that the framework of financial reporting followed by company in reporting its financial transaction /

accounting transactions are in compliance with the GAAP.

With respect to issue of measurement, following things are noted:

Accounting standards were followed and deviation in accounting standards while

preparation of financial statements were shown through disclosures in the annual report

(Lessambo, 2018).

The company used the fair value for valuation of the receivables and payables. Accounting

policies as required for internal control management in reporting of financial transactions in

a given period, this includes those policies that require depreciation and amortisation

including calculations for writing off any debtors turned bad debts.

7 | P a g e

Further, the logic involved in making provisions and accounting entries was based on the

historical experience of the company.

The company recognised revenue in the books on fair value basis of the consideration

received or receivable. IT was recognised only when the significant risks and rewards have

been transferred to the buyer and when the amount was certain and its collectability was

also certain, which is as per the accounting standard.

Company follows accrual based accounting system and proof for every transactions.

The company has valued the fixed assets based on historical cost less impairment less

depreciation and the intangible costs at historical cost less impairment less amortization.

All the financial assets and liabilities have been valued and measured as per the fair value in

line with the accounting standards.

Further the various accounting estimates made by company and the consistency concept

followed by entity to achieve consistency in reporting of financial transactions in an

accounting period (ICAEW, 2011).

Every company which is reporting in the financial transactions is required to have a set of rules and

procedures for accounting and needs to consider well-disciplined measurement concepts in order to

make the financials useful for the decision makers.

The framework in preparation and presenting financial reports and for measurement are

appropriately and accurately used in financial reports of the entity and further changes are not

required in its financial reporting framework as mentioned in above points (Kangarluie & Aalizadeh,

2017).

Fundamental Qualitative Characteristics – Understanding of

relevance and representational faithfulness

The qualitative characteristics of company include the reporting standards followed by company, the

nature of financial reporting framework available in this company and the accounting concepts

followed by company through integrating them in financial reports in an accounting period.

As per the fundamental analysis made on the annual report of entity, it is clear that there is no

deviation in application of applicable accounting standards as issued by the regulatory bodies as

mentioned.

The audit report of company observed to clear the assumptions of these financial reports

maintained by the company in accordance with applicable standards on accounting and various

ethical standards required by regulatory requirements (Trieu, 2017).

The framework in preparation and presenting financial reports available in the company is adequate

for accounting transactions accurately in financial reports of entity and further changes are not

required in its financial reporting framework as mentioned in above points, which tells the

consistency in compliance is more in this company proving the quality in delivering a relevant and

representational faithfulness.

8 | P a g e

historical experience of the company.

The company recognised revenue in the books on fair value basis of the consideration

received or receivable. IT was recognised only when the significant risks and rewards have

been transferred to the buyer and when the amount was certain and its collectability was

also certain, which is as per the accounting standard.

Company follows accrual based accounting system and proof for every transactions.

The company has valued the fixed assets based on historical cost less impairment less

depreciation and the intangible costs at historical cost less impairment less amortization.

All the financial assets and liabilities have been valued and measured as per the fair value in

line with the accounting standards.

Further the various accounting estimates made by company and the consistency concept

followed by entity to achieve consistency in reporting of financial transactions in an

accounting period (ICAEW, 2011).

Every company which is reporting in the financial transactions is required to have a set of rules and

procedures for accounting and needs to consider well-disciplined measurement concepts in order to

make the financials useful for the decision makers.

The framework in preparation and presenting financial reports and for measurement are

appropriately and accurately used in financial reports of the entity and further changes are not

required in its financial reporting framework as mentioned in above points (Kangarluie & Aalizadeh,

2017).

Fundamental Qualitative Characteristics – Understanding of

relevance and representational faithfulness

The qualitative characteristics of company include the reporting standards followed by company, the

nature of financial reporting framework available in this company and the accounting concepts

followed by company through integrating them in financial reports in an accounting period.

As per the fundamental analysis made on the annual report of entity, it is clear that there is no

deviation in application of applicable accounting standards as issued by the regulatory bodies as

mentioned.

The audit report of company observed to clear the assumptions of these financial reports

maintained by the company in accordance with applicable standards on accounting and various

ethical standards required by regulatory requirements (Trieu, 2017).

The framework in preparation and presenting financial reports available in the company is adequate

for accounting transactions accurately in financial reports of entity and further changes are not

required in its financial reporting framework as mentioned in above points, which tells the

consistency in compliance is more in this company proving the quality in delivering a relevant and

representational faithfulness.

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The accounting concepts followed by company is visible in provided screenshot of this company,

where above mentioned accounting concepts are followed on consistent basis by entity based on

past analysis (Vieira, et al., 2017).

This shows the qualitative characteristic of company as due to relevance in integrating accounting

concepts in accordance with applicable financial reporting framework for entity along with various

standards on accounting as mentioned above in previous paragraph.

Accounting policies as required for internal control management in reporting of financial

transactions in a given period are followed by company with consistency and proper applicable form

of disclosures were made by company in its historical financial reports that considered for this

assignment (Heminway, 2017).

This company’s financial reporting framework includes those policies that require depreciation and

amortisation including calculations for writing off any debtors turned bad debts which are known as

accounting estimates as on analysis of financial reports of company, It is clear that company follows

all the accounting estimates mentioned above and in the financial reporting framework in consistent

basis.

Further, the logic involved in making provisions and accounting entries considered are accurate and

show a fair judgement taken by those charged with governance on preparation and presentation of

historical financial statements of the entity that includes various provisions and reserves made in

historical financial reports of entity (Kew & Stredwick, 2017).

Based on the above points, it is clear that this company maintains proper books of accounts and

historical financial reports of the company depict a true and fair view of affairs of reporting of

financial transactions by the entity as a whole.

This conclusion on quality of financial reports of an entity is also based on the adherence to

standards on accounting as stated in director’s responsibility report and independent auditor report

of entity showing that the company follows all applicable standards on accounting and ethical

standards that prescribed (Farmer, 2018).

Conclusion

From the above stated facts in this assignment, it is clear that the assignment has been made

focusing on the accounting concepts used by entity and ways of preparation and presentation of

financial reports made in accordance with standards on accounting.

Various qualitative and quantitative characteristics of entity discussed in detail with relevant

examples related to conclusion drawn on its quality and nature of reporting of financial reports.

It further aimed at providing insights of company’s available framework for reporting of financial

reports and integration of various accounting policies available in entity for reporting and relevant

framework rules of entity observed for consistency.

9 | P a g e

where above mentioned accounting concepts are followed on consistent basis by entity based on

past analysis (Vieira, et al., 2017).

This shows the qualitative characteristic of company as due to relevance in integrating accounting

concepts in accordance with applicable financial reporting framework for entity along with various

standards on accounting as mentioned above in previous paragraph.

Accounting policies as required for internal control management in reporting of financial

transactions in a given period are followed by company with consistency and proper applicable form

of disclosures were made by company in its historical financial reports that considered for this

assignment (Heminway, 2017).

This company’s financial reporting framework includes those policies that require depreciation and

amortisation including calculations for writing off any debtors turned bad debts which are known as

accounting estimates as on analysis of financial reports of company, It is clear that company follows

all the accounting estimates mentioned above and in the financial reporting framework in consistent

basis.

Further, the logic involved in making provisions and accounting entries considered are accurate and

show a fair judgement taken by those charged with governance on preparation and presentation of

historical financial statements of the entity that includes various provisions and reserves made in

historical financial reports of entity (Kew & Stredwick, 2017).

Based on the above points, it is clear that this company maintains proper books of accounts and

historical financial reports of the company depict a true and fair view of affairs of reporting of

financial transactions by the entity as a whole.

This conclusion on quality of financial reports of an entity is also based on the adherence to

standards on accounting as stated in director’s responsibility report and independent auditor report

of entity showing that the company follows all applicable standards on accounting and ethical

standards that prescribed (Farmer, 2018).

Conclusion

From the above stated facts in this assignment, it is clear that the assignment has been made

focusing on the accounting concepts used by entity and ways of preparation and presentation of

financial reports made in accordance with standards on accounting.

Various qualitative and quantitative characteristics of entity discussed in detail with relevant

examples related to conclusion drawn on its quality and nature of reporting of financial reports.

It further aimed at providing insights of company’s available framework for reporting of financial

reports and integration of various accounting policies available in entity for reporting and relevant

framework rules of entity observed for consistency.

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The report also highlighted the fact as to whether they followed concepts on consistent basis or not.

On an average, this assignment contains almost all accounting concepts integrated in reporting

system procedures by management of entity along with various qualitative and quantitative

characteristics of entity in a clear manner for a person to get to trust the company’s financial

reports.

References

Almasi, P., Dagher, J. & Prato, C., 2018. Regulatory Cycles: A Political Economy Model. Working

Paper, 1(1), pp. 25-30.

Andiola, L., Lambert, T. & Lynch, E., 2018. Sprandel, Inc.: Electronic Workpapers, Audit

Documentation, and Closing Review Notes in the Audit of Accounts Receivable. Issues in Accounting

Education, 33(2), pp. 43-55.

Belton, P., 2017. Competitive Strategy: Creating and Sustaining Superior Performance. London:

Macat International ltd.

Dichev, I., 2017. On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), pp. 617-632.

Farmer, Y., 2018. Ethical Decision Making and Reputation Management in Public Relations. Journal

of Media Ethics, 33(1), pp. 1-12.

Heminway, J., 2017. Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN, pp. 1-35.

Hepp, J., 2018. ASC 606: Challenges in understanding and applying revenue recognition. Journal of

Accounting Education, 42(1), pp. 49-51.

ICAEW, 2011. Measurement of Financial Reporting. Financial Reporting Faculty, pp. 6-22.

Kangarluie, S. & Aalizadeh, A., 2017. 'The expectation gap in auditing. Accounting, 3(1), pp. 19-22.

Kew, J. & Stredwick, J., 2017. Business Environment: Managing in a Strategic Context. 2nd ed.

London: Chartered Institute of Personnel and Development.

Lessambo, F., 2018. Audit Risks: Identification and Procedures. Auditing, Assurance Services, and

Forensics, 3(1), pp. 183-202.

Loftus, J. et al., 2018. Financial reporting. 2 ed. Australia: John Wiley & Sons Australia, Ltd.

Smith, G. S., 2015. The Accountant Stereotype: Positive or Negative?. The Research Gate, 10(3), pp.

1-3.

Trieu, V., 2017. Getting value from Business Intelligence systems: A review and research agenda.

Decision Support Systems, 93(1), pp. 111-124.

10 | P a g e

On an average, this assignment contains almost all accounting concepts integrated in reporting

system procedures by management of entity along with various qualitative and quantitative

characteristics of entity in a clear manner for a person to get to trust the company’s financial

reports.

References

Almasi, P., Dagher, J. & Prato, C., 2018. Regulatory Cycles: A Political Economy Model. Working

Paper, 1(1), pp. 25-30.

Andiola, L., Lambert, T. & Lynch, E., 2018. Sprandel, Inc.: Electronic Workpapers, Audit

Documentation, and Closing Review Notes in the Audit of Accounts Receivable. Issues in Accounting

Education, 33(2), pp. 43-55.

Belton, P., 2017. Competitive Strategy: Creating and Sustaining Superior Performance. London:

Macat International ltd.

Dichev, I., 2017. On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), pp. 617-632.

Farmer, Y., 2018. Ethical Decision Making and Reputation Management in Public Relations. Journal

of Media Ethics, 33(1), pp. 1-12.

Heminway, J., 2017. Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN, pp. 1-35.

Hepp, J., 2018. ASC 606: Challenges in understanding and applying revenue recognition. Journal of

Accounting Education, 42(1), pp. 49-51.

ICAEW, 2011. Measurement of Financial Reporting. Financial Reporting Faculty, pp. 6-22.

Kangarluie, S. & Aalizadeh, A., 2017. 'The expectation gap in auditing. Accounting, 3(1), pp. 19-22.

Kew, J. & Stredwick, J., 2017. Business Environment: Managing in a Strategic Context. 2nd ed.

London: Chartered Institute of Personnel and Development.

Lessambo, F., 2018. Audit Risks: Identification and Procedures. Auditing, Assurance Services, and

Forensics, 3(1), pp. 183-202.

Loftus, J. et al., 2018. Financial reporting. 2 ed. Australia: John Wiley & Sons Australia, Ltd.

Smith, G. S., 2015. The Accountant Stereotype: Positive or Negative?. The Research Gate, 10(3), pp.

1-3.

Trieu, V., 2017. Getting value from Business Intelligence systems: A review and research agenda.

Decision Support Systems, 93(1), pp. 111-124.

10 | P a g e

Vieira, R., O’Dwyer, B. & Schneider, R., 2017. Aligning Strategy and Performance Management

Systems. SAGE Journals, 30(1), pp. 23-48.

11 | P a g e

Systems. SAGE Journals, 30(1), pp. 23-48.

11 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.