Advanced Financial Accounting Assignment Report: HA3011 Analysis

VerifiedAdded on 2022/12/02

|12

|3878

|243

Report

AI Summary

This report provides a comprehensive analysis of advanced financial accounting, focusing on key concepts and their practical applications. It begins by discussing the nature and benefits of the conceptual framework for financial reporting, emphasizing its role in establishing credibility and guiding accounting practices. The report then delves into AASB accounting standards, highlighting their importance in presenting an organization's financial position, and explores the theoretical constructs of contemporary financial accounting, including assets, liabilities, equity, and income. A significant portion of the report is dedicated to analyzing Property, Plant, and Equipment (PPE), referencing the Sigma Healthcare Ltd. annual report to illustrate accounting practices. The report also examines the Australian accounting regulatory environment, the accounting treatment of assets and liabilities, and the calculation of journalized transactions for non-current assets, including revaluations and impairments. Finally, the report concludes with an overview of accounting for leases from both the lessees' and lessors' perspectives. The report aims to provide a detailed understanding of advanced financial accounting principles, their application, and their significance in financial reporting.

HA3011 : - ADVANCED

FINANCIAL ACCOUNTING

FINANCIAL ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1. Discussing the nature and benefits of conceptual framework for financial reporting.............1

2. AASB Accounting Standards and their application.................................................................3

3. Theoretical construct of contemporary financial accounting...................................................3

4. Discussing and analysing Property, Plant and Equipment of the company.............................4

5. Australian accounting regulatory environment and conceptual framework............................6

6. How to account for assets and liabilities..................................................................................7

7. Calculation of journalised transactions of non-current assets..................................................7

8. Lessees and lessors accounting................................................................................................8

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1. Discussing the nature and benefits of conceptual framework for financial reporting.............1

2. AASB Accounting Standards and their application.................................................................3

3. Theoretical construct of contemporary financial accounting...................................................3

4. Discussing and analysing Property, Plant and Equipment of the company.............................4

5. Australian accounting regulatory environment and conceptual framework............................6

6. How to account for assets and liabilities..................................................................................7

7. Calculation of journalised transactions of non-current assets..................................................7

8. Lessees and lessors accounting................................................................................................8

CONCLUSION................................................................................................................................8

REFERENCES..............................................................................................................................10

INTRODUCTION

Advance financial accounting is known as the design which helps the organization by

providing the skills which are applicable internationally in their practices. It contains financial

reporting and business skills which is then applied by the business in their professional

environment. Advance financial accounting is important for the members of accounting

professions as they are responsible for providing financial reports. In this project Sigma

healthcare is used as the organization for understanding its financial reports with the help of

advance financial accounting. The organization is the leading whole-seller and distributor to

pharmacy business products. In this project different type of theoretical models of accounting are

understood. This project shows the application of financial reporting on specific issues of AASB

accounting standards. This project also discusses the theoretical construction of contemporary

financial accounting. In this project the need of development for conceptual accounting and the

discussion of it frame work is done. It helps in understanding Australian accounting regulatory

environment. With the help of this project the ability for calculation of journalized transaction is

done.

MAIN BODY

1. Discussing the nature and benefits of conceptual framework for financial reporting

Conceptual Framework (CF) is a particular body which is interconnected with objectives

and fundamentals followed by organization. The purpose behind this is to incline credibility of

financial reporting. It establishes the standards that encourages firms to cope up with structural

of financial accounting. From the analysis of Sigma Healthcare (SH) it can be analyzed that firm

positively implement it operational practices to cooperate with conceptual framework. It gives

focus on presenting is accounting and financial information in most systematic pattern in order to

compliance with this particular framework. Sigma Healthcare directors not only understand this

concept but apply these policies for attaining development

From the evaluating of accounting report of 2020-2021 it can be evaluated that particular

organization comply with appropriate accounting standards to provide clear and fair view of

financial condition & performance of company. Sigma Healthcare concentrate on financial

factors through getting guidance from experts so that appropriate risk and operational

management according to standard can be maintained (Flower and Ebbers, 2018).

1

Advance financial accounting is known as the design which helps the organization by

providing the skills which are applicable internationally in their practices. It contains financial

reporting and business skills which is then applied by the business in their professional

environment. Advance financial accounting is important for the members of accounting

professions as they are responsible for providing financial reports. In this project Sigma

healthcare is used as the organization for understanding its financial reports with the help of

advance financial accounting. The organization is the leading whole-seller and distributor to

pharmacy business products. In this project different type of theoretical models of accounting are

understood. This project shows the application of financial reporting on specific issues of AASB

accounting standards. This project also discusses the theoretical construction of contemporary

financial accounting. In this project the need of development for conceptual accounting and the

discussion of it frame work is done. It helps in understanding Australian accounting regulatory

environment. With the help of this project the ability for calculation of journalized transaction is

done.

MAIN BODY

1. Discussing the nature and benefits of conceptual framework for financial reporting

Conceptual Framework (CF) is a particular body which is interconnected with objectives

and fundamentals followed by organization. The purpose behind this is to incline credibility of

financial reporting. It establishes the standards that encourages firms to cope up with structural

of financial accounting. From the analysis of Sigma Healthcare (SH) it can be analyzed that firm

positively implement it operational practices to cooperate with conceptual framework. It gives

focus on presenting is accounting and financial information in most systematic pattern in order to

compliance with this particular framework. Sigma Healthcare directors not only understand this

concept but apply these policies for attaining development

From the evaluating of accounting report of 2020-2021 it can be evaluated that particular

organization comply with appropriate accounting standards to provide clear and fair view of

financial condition & performance of company. Sigma Healthcare concentrate on financial

factors through getting guidance from experts so that appropriate risk and operational

management according to standard can be maintained (Flower and Ebbers, 2018).

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In the present scenario the specified organization has given focus on adopting all the new

accounting standards as per the conceptual framework for adhering fair practices. It largely

focuses on Australian Accounting Standard Board (AASB). For Instance- In the company’s

financial statements, insurance contracts, etc. Sigma HealthCare gives importance to AASB for

formulating its financial statement so that users can get the understanding for taking economic

and monetary decisions. By giving emphasis on company’s financials statements it can be

interpreted that specified enterprise its concentrates on qualitative features such as reliability,

relevancy, comparability, timeliness, etc. From this it can be identified that firm has shown its

net profitability, ROI, COGS, current liability & assets, equity, retained earnings so that

stakeholders can take accurate decisions.

Conceptual framework execution provides various type of benefits to organization which

enable it to derive positive goodwill in the industry. Following FASB’s CF helps SH to get

positive outcome that provides opportunity to measure, resolve, etc accounting disputes in

standard manner. For example- Sigma Healthcare has not made any changes in accounting

policies for measuring and disclosure of its financial statements so that company can cope with

accounting principle and validate its actions for proofing concept of going concern. It has as well

provided the financial information in understanding manner for making judgments of

performance of organization. This comprises sales & revenue. Segment information, expenses,

taxation, subsequent event, dividends, earning per share, etc. It aids firm to get credibility,

trustworthiness among stakeholders, etc.

Financial reporting is exerted by company in ethical manner so that it can meet the

elements like objectivity, fundamental principles, qualitative features, etc Sigma Healthcare

ensures that its cooperate with ASX while maintaining the balance with conceptual framework.

It records and publish all of its financial data according to IFRS, IASB and AASB. In addition to

this, it can eb identified from the all regulatory requirements relevant to its reporting process is

appropriately implemented (Coetsee, 2021). For essence- deferred tax is presented in balance

sheet by making difference between carrying value of assets and liabilities in order to accomplish

the reporting and taxation purpose. This provides consistency and useful standards so that on

going concern can perform effectively so that it's objectives can be accomplished. It provides

ease to compare different companies financial statements so that investors can rely on these

information for making appropriate decisions. Reporting according to prevailing standards as

2

accounting standards as per the conceptual framework for adhering fair practices. It largely

focuses on Australian Accounting Standard Board (AASB). For Instance- In the company’s

financial statements, insurance contracts, etc. Sigma HealthCare gives importance to AASB for

formulating its financial statement so that users can get the understanding for taking economic

and monetary decisions. By giving emphasis on company’s financials statements it can be

interpreted that specified enterprise its concentrates on qualitative features such as reliability,

relevancy, comparability, timeliness, etc. From this it can be identified that firm has shown its

net profitability, ROI, COGS, current liability & assets, equity, retained earnings so that

stakeholders can take accurate decisions.

Conceptual framework execution provides various type of benefits to organization which

enable it to derive positive goodwill in the industry. Following FASB’s CF helps SH to get

positive outcome that provides opportunity to measure, resolve, etc accounting disputes in

standard manner. For example- Sigma Healthcare has not made any changes in accounting

policies for measuring and disclosure of its financial statements so that company can cope with

accounting principle and validate its actions for proofing concept of going concern. It has as well

provided the financial information in understanding manner for making judgments of

performance of organization. This comprises sales & revenue. Segment information, expenses,

taxation, subsequent event, dividends, earning per share, etc. It aids firm to get credibility,

trustworthiness among stakeholders, etc.

Financial reporting is exerted by company in ethical manner so that it can meet the

elements like objectivity, fundamental principles, qualitative features, etc Sigma Healthcare

ensures that its cooperate with ASX while maintaining the balance with conceptual framework.

It records and publish all of its financial data according to IFRS, IASB and AASB. In addition to

this, it can eb identified from the all regulatory requirements relevant to its reporting process is

appropriately implemented (Coetsee, 2021). For essence- deferred tax is presented in balance

sheet by making difference between carrying value of assets and liabilities in order to accomplish

the reporting and taxation purpose. This provides consistency and useful standards so that on

going concern can perform effectively so that it's objectives can be accomplished. It provides

ease to compare different companies financial statements so that investors can rely on these

information for making appropriate decisions. Reporting according to prevailing standards as

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

well aid firm to avoid unnecessary legal obligations. The performance of SH is measured by

independent bodies in turn trustworthiness can be maintained among shareholders and continual

growth can be obtained

2. AASB Accounting Standards and their application

The main purpose of the accounting standards is to showcase the financial position of the

organisation in this case which is the Sigma healthcare ltd. The company should properly

maintain its accounting standards as it helps the investors, owner, creditors, analysts, employees

to know the financial conditions of the company. AASB is the Australian Accounting Standards

Board which is an Australian government agency which is responsible for the development and

issuing of the accounting standards which comply with the Australian company law. The main

vision of this government body is to be recognised as a global centre, producing high quality of

financial accounting standards (Daú and et.al., 2019).

The main objective of the AASB is to develop and commence good quality financial

accounting standards for all the sectors of the economy of Australia. The agency also pursues to

contribute to the global financial accounting standards. To apply the global accounting standards

with that of the Australian accounting standards for the native companies. Transaction are one of

the most crucial parts of accounting and to produce standards which are treated like transactions

is one of the AASB. The AASB ultimately focuses to influence the International Financial

Reporting Standards. The basic purpose of these government bodies is to find loopholes in the

existing standards and act upon it by making new standards. To promote the global and

consistent application of these accounting standards is the goals of the AASB.

3. Theoretical construct of contemporary financial accounting

The AASB has given out to some financial elements that make the backbone of every

financial statement.

Assets: An asset is a commercial resource which a company possess by either creating it

or acquiring it in the past. The Assets is a potential economic entity which can be used as

to create a benefit of all kinds. The company Sigma health care Ltd also possess some

assets which can be beneficial for the company. Some examples of an asset are land,

building, machinery and even cash (Herath and Alsulmi, 2017).

Liability: A liability is occurred when a party is liable to pay or return the sum or even

an object to the other party. A liability can be said as an obligation which forms an

3

independent bodies in turn trustworthiness can be maintained among shareholders and continual

growth can be obtained

2. AASB Accounting Standards and their application

The main purpose of the accounting standards is to showcase the financial position of the

organisation in this case which is the Sigma healthcare ltd. The company should properly

maintain its accounting standards as it helps the investors, owner, creditors, analysts, employees

to know the financial conditions of the company. AASB is the Australian Accounting Standards

Board which is an Australian government agency which is responsible for the development and

issuing of the accounting standards which comply with the Australian company law. The main

vision of this government body is to be recognised as a global centre, producing high quality of

financial accounting standards (Daú and et.al., 2019).

The main objective of the AASB is to develop and commence good quality financial

accounting standards for all the sectors of the economy of Australia. The agency also pursues to

contribute to the global financial accounting standards. To apply the global accounting standards

with that of the Australian accounting standards for the native companies. Transaction are one of

the most crucial parts of accounting and to produce standards which are treated like transactions

is one of the AASB. The AASB ultimately focuses to influence the International Financial

Reporting Standards. The basic purpose of these government bodies is to find loopholes in the

existing standards and act upon it by making new standards. To promote the global and

consistent application of these accounting standards is the goals of the AASB.

3. Theoretical construct of contemporary financial accounting

The AASB has given out to some financial elements that make the backbone of every

financial statement.

Assets: An asset is a commercial resource which a company possess by either creating it

or acquiring it in the past. The Assets is a potential economic entity which can be used as

to create a benefit of all kinds. The company Sigma health care Ltd also possess some

assets which can be beneficial for the company. Some examples of an asset are land,

building, machinery and even cash (Herath and Alsulmi, 2017).

Liability: A liability is occurred when a party is liable to pay or return the sum or even

an object to the other party. A liability can be said as an obligation which forms an

3

economic resource and that entity may or may not be transferred to another entity for

some activities in the past. The company Sigma healthcare ltd also has some liabilities

which can be in form of equities, loans or outstanding.

Equity: Equity is the leftover which is residual in nature and is gathered by deducting the

liabilities from the assets of an entity. These equities can be used as an asset creation of

another stature and can be even profitable for the company.

Income: Income can be referred as the rise of assets and the deduction of the liabilities of

a company such as Sigma healthcare ltd which may further lead to the increase in the

equity of the particular company. Income is not for the ones who hold the equities in the

company (Eyenubo, Mohammed and Ali, 2017).

4. Discussing and analysing Property, Plant and Equipment of the company

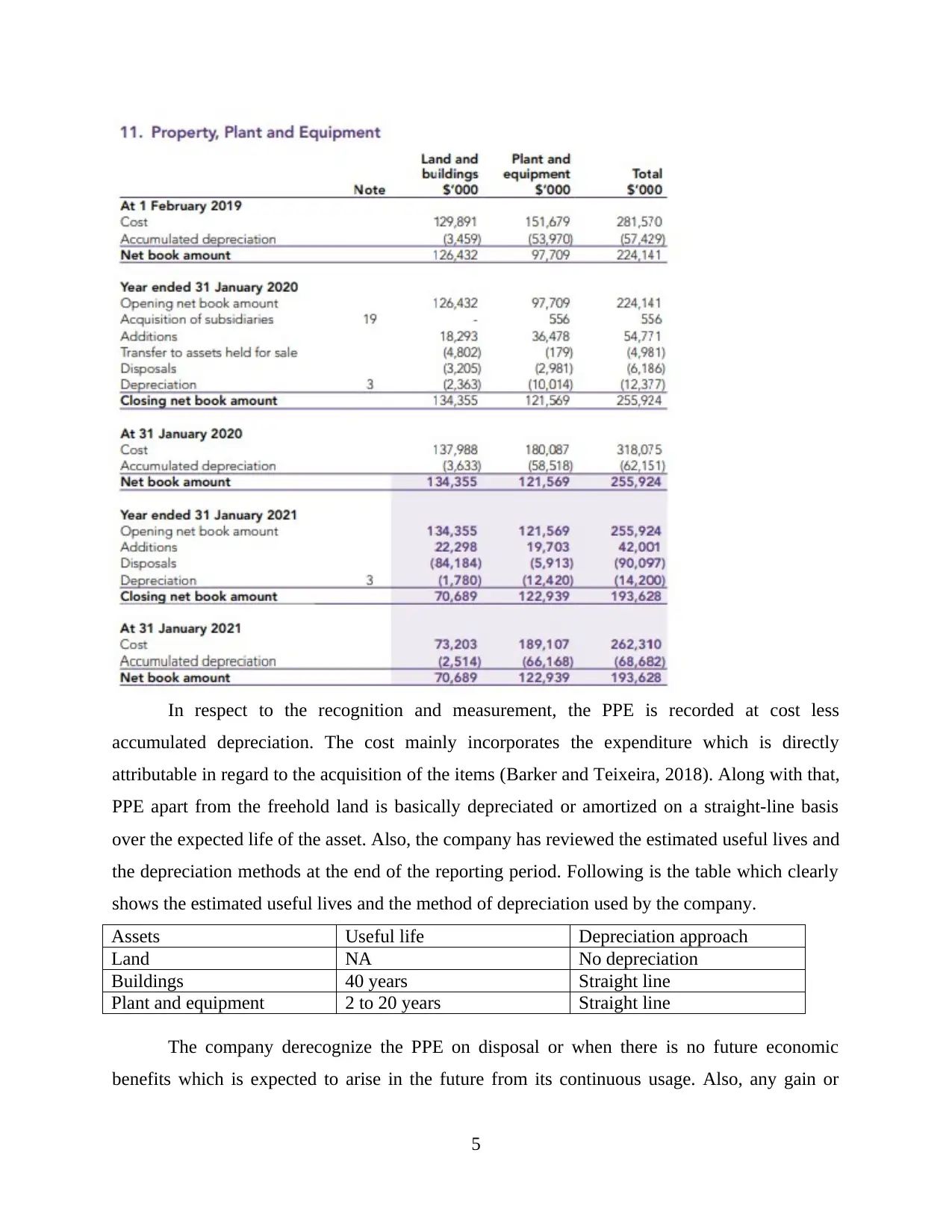

On looking at the annual report of the company Sigma Healthcare ltd, in respect to the

Property, Plant and Equipment, at February 1, 2019, the net book value of the assets was in total

224,141 which incorporates land and building amount to net value of 126,432 and plant and

equipment amounting to 97,709. In the past year, the company acquired new entities as its

subsidies which resulted into increase in plant and equipment and in addition to this, the

company has even purchased new land and building of 18293 and plant and equipment of 36478

(Annual Report 2020/21. 2021). This resulted into increase in the net book amount of the PPE to

255,924. By the end of January 2021, the net book value of the assets declined which was due to

the heavy disposal of the assets and reduction in purchase. It is also important to note that it also

involves the capital work in progress which is included in the PPE at 31 January 2021 amounting

to $27437000 which is an increase in comparison to the previous year of $15740000. This is

mainly belonging to the construction of the plant and equipment for the Truganina distribution

centre in Victoria.

4

some activities in the past. The company Sigma healthcare ltd also has some liabilities

which can be in form of equities, loans or outstanding.

Equity: Equity is the leftover which is residual in nature and is gathered by deducting the

liabilities from the assets of an entity. These equities can be used as an asset creation of

another stature and can be even profitable for the company.

Income: Income can be referred as the rise of assets and the deduction of the liabilities of

a company such as Sigma healthcare ltd which may further lead to the increase in the

equity of the particular company. Income is not for the ones who hold the equities in the

company (Eyenubo, Mohammed and Ali, 2017).

4. Discussing and analysing Property, Plant and Equipment of the company

On looking at the annual report of the company Sigma Healthcare ltd, in respect to the

Property, Plant and Equipment, at February 1, 2019, the net book value of the assets was in total

224,141 which incorporates land and building amount to net value of 126,432 and plant and

equipment amounting to 97,709. In the past year, the company acquired new entities as its

subsidies which resulted into increase in plant and equipment and in addition to this, the

company has even purchased new land and building of 18293 and plant and equipment of 36478

(Annual Report 2020/21. 2021). This resulted into increase in the net book amount of the PPE to

255,924. By the end of January 2021, the net book value of the assets declined which was due to

the heavy disposal of the assets and reduction in purchase. It is also important to note that it also

involves the capital work in progress which is included in the PPE at 31 January 2021 amounting

to $27437000 which is an increase in comparison to the previous year of $15740000. This is

mainly belonging to the construction of the plant and equipment for the Truganina distribution

centre in Victoria.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In respect to the recognition and measurement, the PPE is recorded at cost less

accumulated depreciation. The cost mainly incorporates the expenditure which is directly

attributable in regard to the acquisition of the items (Barker and Teixeira, 2018). Along with that,

PPE apart from the freehold land is basically depreciated or amortized on a straight-line basis

over the expected life of the asset. Also, the company has reviewed the estimated useful lives and

the depreciation methods at the end of the reporting period. Following is the table which clearly

shows the estimated useful lives and the method of depreciation used by the company.

Assets Useful life Depreciation approach

Land NA No depreciation

Buildings 40 years Straight line

Plant and equipment 2 to 20 years Straight line

The company derecognize the PPE on disposal or when there is no future economic

benefits which is expected to arise in the future from its continuous usage. Also, any gain or

5

accumulated depreciation. The cost mainly incorporates the expenditure which is directly

attributable in regard to the acquisition of the items (Barker and Teixeira, 2018). Along with that,

PPE apart from the freehold land is basically depreciated or amortized on a straight-line basis

over the expected life of the asset. Also, the company has reviewed the estimated useful lives and

the depreciation methods at the end of the reporting period. Following is the table which clearly

shows the estimated useful lives and the method of depreciation used by the company.

Assets Useful life Depreciation approach

Land NA No depreciation

Buildings 40 years Straight line

Plant and equipment 2 to 20 years Straight line

The company derecognize the PPE on disposal or when there is no future economic

benefits which is expected to arise in the future from its continuous usage. Also, any gain or

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

benefit which arises from such derecognition is included in the P&L statement in the period

when it was derecognized. Along with this, the PPE is also tested for the impairment as and

when the events or changes in the situations takes place which conveys that the carrying amount

might not be recovered. Sigma Healthcare ltd has also recognized the impairment loss for the

amount by which the carrying amount exceeds its recoverable amount (Sellhorn and Stier, 2019).

In order to assess the impairment, the company has grouped the assets at the lowest level for

which they are separately identifiable cash flows which is mainly not dependent upon the cash

flows through other assets or groups. In the previous year, the organization, was committed to

selling the sites of its dormant Belmont and Newcastle distribution centers in which the assets

belonged to these sites were categorized as the held for sale. It was measured at the carrying

amount. In the month of July 2020, both the sites were sold at a gain which was recognized

under the heading comprehensive income in the consolidated income statement under the

heading “Other revenue”.

The non-current assets of the company are classified as the held for sale under the

situation when their carrying amount will be recovered mainly by the way of sale transaction

instead of continuing the use and a sale is taken to be high probably (Raхimova, 2020). It is

measured at probably lower of its carrying amount and the fair value reduced by the costs of

disposal except for the assets like the deferred tax assets along with the assets which is generated

from the employees benefits and the financial assets as these are specially exempted from this

requirement. The only measurement issue which is being identified from the analysis of the

annual report of the company is that it depreciates all its assets on straight line basis only,

therefore, it should again consider this whether it is providing right basis for measuring assets.

5. Australian accounting regulatory environment and conceptual framework

The two major sources of the Australian accounting regulatory environment are The

Corporation Act 2001 and the Australian Accounting Standards (AASB). The corporation Act

states that the companies should prepare all the financial reports. The preparation is necessary for

all the disclosing entities which are listed on the securities exchange, large proprietary

companies, public companies and also the registered schemes. The proprietary companies are

thoese companies which may or may not offer shares for the sale in public. It is generally

consisted of known shareholders and the company could classify their status as small or large

with not more than 50 non-employee shareholders(Barth and et.al.,2017). It does not discloses

6

when it was derecognized. Along with this, the PPE is also tested for the impairment as and

when the events or changes in the situations takes place which conveys that the carrying amount

might not be recovered. Sigma Healthcare ltd has also recognized the impairment loss for the

amount by which the carrying amount exceeds its recoverable amount (Sellhorn and Stier, 2019).

In order to assess the impairment, the company has grouped the assets at the lowest level for

which they are separately identifiable cash flows which is mainly not dependent upon the cash

flows through other assets or groups. In the previous year, the organization, was committed to

selling the sites of its dormant Belmont and Newcastle distribution centers in which the assets

belonged to these sites were categorized as the held for sale. It was measured at the carrying

amount. In the month of July 2020, both the sites were sold at a gain which was recognized

under the heading comprehensive income in the consolidated income statement under the

heading “Other revenue”.

The non-current assets of the company are classified as the held for sale under the

situation when their carrying amount will be recovered mainly by the way of sale transaction

instead of continuing the use and a sale is taken to be high probably (Raхimova, 2020). It is

measured at probably lower of its carrying amount and the fair value reduced by the costs of

disposal except for the assets like the deferred tax assets along with the assets which is generated

from the employees benefits and the financial assets as these are specially exempted from this

requirement. The only measurement issue which is being identified from the analysis of the

annual report of the company is that it depreciates all its assets on straight line basis only,

therefore, it should again consider this whether it is providing right basis for measuring assets.

5. Australian accounting regulatory environment and conceptual framework

The two major sources of the Australian accounting regulatory environment are The

Corporation Act 2001 and the Australian Accounting Standards (AASB). The corporation Act

states that the companies should prepare all the financial reports. The preparation is necessary for

all the disclosing entities which are listed on the securities exchange, large proprietary

companies, public companies and also the registered schemes. The proprietary companies are

thoese companies which may or may not offer shares for the sale in public. It is generally

consisted of known shareholders and the company could classify their status as small or large

with not more than 50 non-employee shareholders(Barth and et.al.,2017). It does not discloses

6

the securities as it needs the permission of the shareholders. There are a limited number of shares

which offer the shareholders with more protection.

The conceptual framework is a intelligible system of correlated goals and essentials that

are likely to lead to the standards. It is the attempt to provide a better thorough and structured

theory of accounting which can prescribe and practise. While implementing the accounting

standards into rela life situations, it is needed that these standards are relevant and making proper

sense, this is provided by the conceptual framework. The main objectives of the conceptual

framework is to assist the accounting standards consistently, to assist the users to interpret

statement and also to assist the auditors which will be forming opinion on compliance.

6. How to account for assets and liabilities

Assets are considered as the economic benefits obtained as a result of the entities past

transactions. Assets are classified in two parts intangible and tangible assets. Assets can be

further sub categorised in two parts which are current assets and non current assets. Non current

assets are the assets for which the company cannot realise the whole value during the current

accounting year. These assests can also include those ones which do not possess much or any

value such as intangible assets. The non current assets are capitalised rather than being expensed.

This means that the non current asset’s cost is stretched over the time duration of the assets life

rather than accounting it in the same year in which the company bought it. Investments are

considered as the non-current assets only if they are not expected to yield profit over a period of

1 year.

A company’s liabilities are the debts and the dues are represented on the liabilities side of the

balance sheet. The liabilities are totally the opposite of assets. Liabilities are detracted from the

company’s total value, the liabilities of the companies are to be paid over time. The types of

liability may vary such as expenses, loans, unearned revenues or legal obligations. There are two

types of liabilities which are current liabilities and long term liabilities.

7. Calculation of journalised transactions of non-current assets

Impairment testing is a process which is used to review the value of assets which are

present in the balance sheet. For the impairment of non-current assets, it is important for the

organization to provide useful and meaningful information about its which will eventually help

the financial reports to the organization itself in being confident while taking decisions. In the

impairment of non-current asset, as per the AASB 136 the following are selected, goodwill and

7

which offer the shareholders with more protection.

The conceptual framework is a intelligible system of correlated goals and essentials that

are likely to lead to the standards. It is the attempt to provide a better thorough and structured

theory of accounting which can prescribe and practise. While implementing the accounting

standards into rela life situations, it is needed that these standards are relevant and making proper

sense, this is provided by the conceptual framework. The main objectives of the conceptual

framework is to assist the accounting standards consistently, to assist the users to interpret

statement and also to assist the auditors which will be forming opinion on compliance.

6. How to account for assets and liabilities

Assets are considered as the economic benefits obtained as a result of the entities past

transactions. Assets are classified in two parts intangible and tangible assets. Assets can be

further sub categorised in two parts which are current assets and non current assets. Non current

assets are the assets for which the company cannot realise the whole value during the current

accounting year. These assests can also include those ones which do not possess much or any

value such as intangible assets. The non current assets are capitalised rather than being expensed.

This means that the non current asset’s cost is stretched over the time duration of the assets life

rather than accounting it in the same year in which the company bought it. Investments are

considered as the non-current assets only if they are not expected to yield profit over a period of

1 year.

A company’s liabilities are the debts and the dues are represented on the liabilities side of the

balance sheet. The liabilities are totally the opposite of assets. Liabilities are detracted from the

company’s total value, the liabilities of the companies are to be paid over time. The types of

liability may vary such as expenses, loans, unearned revenues or legal obligations. There are two

types of liabilities which are current liabilities and long term liabilities.

7. Calculation of journalised transactions of non-current assets

Impairment testing is a process which is used to review the value of assets which are

present in the balance sheet. For the impairment of non-current assets, it is important for the

organization to provide useful and meaningful information about its which will eventually help

the financial reports to the organization itself in being confident while taking decisions. In the

impairment of non-current asset, as per the AASB 136 the following are selected, goodwill and

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

identifiable intangible assets. The impairment of such assets are done by collecting the

information about the recoverable amount of the organization's asset. Lower recoverable value of

the asset needs a higher value less cost for their disposal. For revaluation of the non-current asset

the journalized transaction is carried at the revalued amount (Sampaio and González, 2017). It is

the calculation of the revaluation less subsequent accumulated deprecation and the losses inured

in the impairment (BDO Australia ,2018).

8. Lessees and lessors accounting

According to the IFRS 16 the lessors have to follow the following treatments for their

lease accounting, It can be classified as the finance lease only is the risk and rewards is owned by

the entity of the leased asset. In any other case the situation will be known as the operating lease.

The lessor who does the lease transfer transfers all the risks and rewards of the leased property to

the lessee in the situation of finance lease whereas in the operating lease the risks and rewards

are not completely transferred (Aziz, Md Husin and Hussin, 2017).

For the accounting of lessees the AASB standards are applicable which helps it in

implementation of changes which are needed for complete understanding of their requirements

and impacts on the balance sheet of the lessee. It also requires the preparation of income

statement and cash flow statements. This guides the lessee for the assistance in order to

understand the required accounting transactions needed for the new standard. With the help of

the lessees accounting can be done.

CONCLUSION

With the help of this project is has been understood that Sigma healthcare should

properly maintain its accounts with the help of all the accounting standards and financial reports

which are discussed in the project. This project helped in understanding the theoretical model of

accounting. It also shows how to understand the accounting of assets and its liabilities. In this

project the AASB accounting standards are understood for the financial accounting of Sigma

healthcare. This project helps in understanding the accounting regulatory environment of this

organization and also its conceptual framework. This project helps in understanding the account

of the assets and liabilities of this company and its focus is over the non current asset. In this

project the theories of contemporary financial accounting is also understood. The aim of this

project has also been to understand the ability of calculation to the journalized transactions for

impairments and revaluation of the non current assets.

8

information about the recoverable amount of the organization's asset. Lower recoverable value of

the asset needs a higher value less cost for their disposal. For revaluation of the non-current asset

the journalized transaction is carried at the revalued amount (Sampaio and González, 2017). It is

the calculation of the revaluation less subsequent accumulated deprecation and the losses inured

in the impairment (BDO Australia ,2018).

8. Lessees and lessors accounting

According to the IFRS 16 the lessors have to follow the following treatments for their

lease accounting, It can be classified as the finance lease only is the risk and rewards is owned by

the entity of the leased asset. In any other case the situation will be known as the operating lease.

The lessor who does the lease transfer transfers all the risks and rewards of the leased property to

the lessee in the situation of finance lease whereas in the operating lease the risks and rewards

are not completely transferred (Aziz, Md Husin and Hussin, 2017).

For the accounting of lessees the AASB standards are applicable which helps it in

implementation of changes which are needed for complete understanding of their requirements

and impacts on the balance sheet of the lessee. It also requires the preparation of income

statement and cash flow statements. This guides the lessee for the assistance in order to

understand the required accounting transactions needed for the new standard. With the help of

the lessees accounting can be done.

CONCLUSION

With the help of this project is has been understood that Sigma healthcare should

properly maintain its accounts with the help of all the accounting standards and financial reports

which are discussed in the project. This project helped in understanding the theoretical model of

accounting. It also shows how to understand the accounting of assets and its liabilities. In this

project the AASB accounting standards are understood for the financial accounting of Sigma

healthcare. This project helps in understanding the accounting regulatory environment of this

organization and also its conceptual framework. This project helps in understanding the account

of the assets and liabilities of this company and its focus is over the non current asset. In this

project the theories of contemporary financial accounting is also understood. The aim of this

project has also been to understand the ability of calculation to the journalized transactions for

impairments and revaluation of the non current assets.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

9

REFERENCES

Books and Journals

Abang’a, A.O.G., 2017. Determinants of quality of financial reporting among semi-autonomous

government agencies in Kenya (Doctoral dissertation, Strathmore University).

Aziz, S., Md Husin, M. and Hussin, N., 2017. Conceptual framework of factors determining

intentions towards the adoption of family takaful-An extension of decomposed theory of

planned behaviour. International Journal of Organizational Leadership. 6. pp.385-399.

Barker, R. and Teixeira, A., 2018. Gaps in the IFRS conceptual framework. Accounting in

Europe. 15(2). pp.153-166.

Barth, J., and et.al.,2017. Informational urbanism. A conceptual framework of smart cities.

Camfferman, K. and Zeff, S.A., 2018. The challenge of setting standards for a worldwide

constituency: Research implications from the IASB’s early history. European Accounting

Review. 27(2). pp.289-312.

Coetsee, D., 2021. The underlying concepts of the definition of a liability in financial reporting:

A doctrinal research perspective. South African Journal of Accounting Research, 35(1),

pp.20-41.

Daú, G., and et.al., 2019. The healthcare sustainable supply chain 4.0: The circular economy

transition conceptual framework with the corporate social responsibility

mirror. Sustainability. 11(12). p.3259.

Eyenubo, S.A., Mohammed, M. and Ali, M., 2017. Audit committee effectiveness of financial

reporting quality in listed companies in Nigeria stock exchange. International Journal of

Academic Research in Business and Social Sciences. 7(6). pp.487-505.

Flower, J. and Ebbers, G., 2018. Global financial reporting. Macmillan International Higher

Education.

Herath, S.K. and Alsulmi, F.H., 2017. International financial reporting standards (IFRS): The

benefits, obstacles, and opportunities for implementation in Saudi Arabia. International

Journal of Social Science and Business. 2(1). pp.1-18.

Raхimova, G. M., 2020. PROBLEMS OF ACCOUNTING AND AUDIT OF FIXED

ASSETS. Theoretical & Applied Science. (5). pp.726-729.

Sampaio, P.G.V. and González, M.O.A., 2017. Photovoltaic solar energy: Conceptual

framework. Renewable and Sustainable Energy Reviews. 74. pp.590-601.

Sellhorn, T. and Stier, C., 2019. Fair value measurement for long-lived operating assets:

Research evidence. European Accounting Review. 28(3). pp.573-603.

Zadeh, F.N., Salehi, M. and Shabestari, H., 2018. The relationship between corporate governance

mechanisms and internet financial reporting in Iran. Corporate Governance: The

International Journal of Business in Society.

Online

BDO Australia ,2018. IFRS 16.[Online] Available trough:

<https://www.bdo.com.au/en-au/accounting-news/accounting-news-october-2018/ifrs-16>

Annual Report 2020/21. 2021. [Online]. Available Through:<

https://investorcentre.sigmahealthcare.com.au/static-files/5faa2ef7-bdf6-418d-8784-

46c751d3563a >.

10

Books and Journals

Abang’a, A.O.G., 2017. Determinants of quality of financial reporting among semi-autonomous

government agencies in Kenya (Doctoral dissertation, Strathmore University).

Aziz, S., Md Husin, M. and Hussin, N., 2017. Conceptual framework of factors determining

intentions towards the adoption of family takaful-An extension of decomposed theory of

planned behaviour. International Journal of Organizational Leadership. 6. pp.385-399.

Barker, R. and Teixeira, A., 2018. Gaps in the IFRS conceptual framework. Accounting in

Europe. 15(2). pp.153-166.

Barth, J., and et.al.,2017. Informational urbanism. A conceptual framework of smart cities.

Camfferman, K. and Zeff, S.A., 2018. The challenge of setting standards for a worldwide

constituency: Research implications from the IASB’s early history. European Accounting

Review. 27(2). pp.289-312.

Coetsee, D., 2021. The underlying concepts of the definition of a liability in financial reporting:

A doctrinal research perspective. South African Journal of Accounting Research, 35(1),

pp.20-41.

Daú, G., and et.al., 2019. The healthcare sustainable supply chain 4.0: The circular economy

transition conceptual framework with the corporate social responsibility

mirror. Sustainability. 11(12). p.3259.

Eyenubo, S.A., Mohammed, M. and Ali, M., 2017. Audit committee effectiveness of financial

reporting quality in listed companies in Nigeria stock exchange. International Journal of

Academic Research in Business and Social Sciences. 7(6). pp.487-505.

Flower, J. and Ebbers, G., 2018. Global financial reporting. Macmillan International Higher

Education.

Herath, S.K. and Alsulmi, F.H., 2017. International financial reporting standards (IFRS): The

benefits, obstacles, and opportunities for implementation in Saudi Arabia. International

Journal of Social Science and Business. 2(1). pp.1-18.

Raхimova, G. M., 2020. PROBLEMS OF ACCOUNTING AND AUDIT OF FIXED

ASSETS. Theoretical & Applied Science. (5). pp.726-729.

Sampaio, P.G.V. and González, M.O.A., 2017. Photovoltaic solar energy: Conceptual

framework. Renewable and Sustainable Energy Reviews. 74. pp.590-601.

Sellhorn, T. and Stier, C., 2019. Fair value measurement for long-lived operating assets:

Research evidence. European Accounting Review. 28(3). pp.573-603.

Zadeh, F.N., Salehi, M. and Shabestari, H., 2018. The relationship between corporate governance

mechanisms and internet financial reporting in Iran. Corporate Governance: The

International Journal of Business in Society.

Online

BDO Australia ,2018. IFRS 16.[Online] Available trough:

<https://www.bdo.com.au/en-au/accounting-news/accounting-news-october-2018/ifrs-16>

Annual Report 2020/21. 2021. [Online]. Available Through:<

https://investorcentre.sigmahealthcare.com.au/static-files/5faa2ef7-bdf6-418d-8784-

46c751d3563a >.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.