Advanced Financial Accounting Report: Chorus Limited Analysis, HA3011

VerifiedAdded on 2022/08/24

|12

|2515

|28

Report

AI Summary

This report provides a comprehensive analysis of advanced financial accounting principles, focusing on the application of AASB accounting standards and IFRS. The report examines the financial statements of Chorus Limited, a telecommunications company, evaluating its reporting entity, and the fundamental qualitative characteristics of relevance and faithful representation. It delves into the company's overview, including its infrastructure and services, and assesses its adherence to accounting standards within the Australian accounting framework. The analysis includes discussions on the concept of reporting entity, the importance of consolidated financial statements, and the application of qualitative characteristics in financial reporting. The report also covers the company's adoption of new accounting standards and provides insights into its financial performance, including revenue, expenses, and key audit matters. The conclusion emphasizes the significance of IFRS in ensuring a transparent view of a company's financial position and the relevance of the annual report for stakeholders. The report also suggests areas for improvement, such as providing more detailed explanations of assets, liabilities, and accounting standards.

Running head: ADVANCED FINANCIAL ACCOUNTING

Advanced Financial Accounting

Name of the Student

Name of the University

Author Note

Advanced Financial Accounting

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ADVANCED FINANCIAL ACCOUNTING

Table of Contents

Introduction................................................................................................................................2

Discussion..................................................................................................................................2

Company’s Overview.............................................................................................................2

Reporting Entity.....................................................................................................................3

Fundamental Qualitative Characteristics...............................................................................5

Relevance and Faithful Representation..............................................................................6

Conclusion..................................................................................................................................8

References................................................................................................................................10

Table of Contents

Introduction................................................................................................................................2

Discussion..................................................................................................................................2

Company’s Overview.............................................................................................................2

Reporting Entity.....................................................................................................................3

Fundamental Qualitative Characteristics...............................................................................5

Relevance and Faithful Representation..............................................................................6

Conclusion..................................................................................................................................8

References................................................................................................................................10

2ADVANCED FINANCIAL ACCOUNTING

Introduction

Financial reports have the most significant position for both the internal and external

stakeholders, as it displays as a company’s scorecard. Thus, the financial reports must

disclose effective information with certain limitation so that it does not reveal any misleading

information. IFRSs provide a set of rules in terms with financial report worldwide.

Australian Accounting Board provided a framework of accounting that consist of regulations

and disclosures that an organization has to follow while maintaining financial reports1. The

aim of preparing this report is to develop an understanding of the theoretical model of

accounting and the need for an accounting framework within an annual report on an entity.

The company chosen within this report is Chorus Limited Foreign Exempt NZX (CNU),

which is engaged in the telecommunications industry. The discussion will demonstrate a

thorough understanding of AASB accounting standards and its related framework as well as

IFRS that is essential for preparing an annual report. It includes the concept of reporting

entity and fundamental qualitative characteristics like relevance and faithfulness. Further, the

discussion will go through the recent annual report of Chorus Limited to analyze the extent of

maintaining the accounting standards of Australian accounting. At last, the report will reflect

the vital need of accounting in the reporting of an entity for an effective outcome for the

stakeholders.

Discussion

Company’s Overview

Chorus Limited is considered as largest telecommunications Infrastructure Company

in New Zealand2. It is listed on the NZX stock exchange and comes within the list of NZX 50

1 Howieson, Bryan. "The phoenix rises: The Australian accounting standards board and IFRS

adoption." Journal of International Accounting Research 16.2 (2017): 127-154.

2 Company.chorus.co.nz, "Who We Are | Corporate Website", Company.Chorus.Co.Nz (Webpage, 2020)

<https://company.chorus.co.nz/who-we-are>

Introduction

Financial reports have the most significant position for both the internal and external

stakeholders, as it displays as a company’s scorecard. Thus, the financial reports must

disclose effective information with certain limitation so that it does not reveal any misleading

information. IFRSs provide a set of rules in terms with financial report worldwide.

Australian Accounting Board provided a framework of accounting that consist of regulations

and disclosures that an organization has to follow while maintaining financial reports1. The

aim of preparing this report is to develop an understanding of the theoretical model of

accounting and the need for an accounting framework within an annual report on an entity.

The company chosen within this report is Chorus Limited Foreign Exempt NZX (CNU),

which is engaged in the telecommunications industry. The discussion will demonstrate a

thorough understanding of AASB accounting standards and its related framework as well as

IFRS that is essential for preparing an annual report. It includes the concept of reporting

entity and fundamental qualitative characteristics like relevance and faithfulness. Further, the

discussion will go through the recent annual report of Chorus Limited to analyze the extent of

maintaining the accounting standards of Australian accounting. At last, the report will reflect

the vital need of accounting in the reporting of an entity for an effective outcome for the

stakeholders.

Discussion

Company’s Overview

Chorus Limited is considered as largest telecommunications Infrastructure Company

in New Zealand2. It is listed on the NZX stock exchange and comes within the list of NZX 50

1 Howieson, Bryan. "The phoenix rises: The Australian accounting standards board and IFRS

adoption." Journal of International Accounting Research 16.2 (2017): 127-154.

2 Company.chorus.co.nz, "Who We Are | Corporate Website", Company.Chorus.Co.Nz (Webpage, 2020)

<https://company.chorus.co.nz/who-we-are>

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ADVANCED FINANCIAL ACCOUNTING

Index. Its infrastructure consists of local telephone exchanges, copper, cabinets and fibre

cables. CNU works within such products and services that are named as Fibre, Basic and

Enhanced Copper, Field Services, Value Added Network, and Infrastructure Services.

Reporting Entity

Paragraphs 3.10 of the AASB Conceptual Framework of Accounting defines the

reporting entity as an entity, which is required, or have selected to prepare financial reports. It

is not necessary to be a legal entity. An entity can be sole or a part of an entity or can be a

combination of more than one entity3. To explain a clear concept about the reporting entity

SAC 1 defines the following terms, which is discussed below, which puts a benchmark for

the financial reporting’s minimum required quality for an entity.

General-purpose of Financial Reporting- It means that a financial statement intends to

meet the user’s requirement who is not able to command the reports, thereby satisfying their

informational needs.

Control- The entity’s capacity to govern the decision making whether it is directly or

indirectly, in context with the fiscal and operating policies of a different entity so that to

allow that entity to perform and achieve the objectives of the controlling entity4.

Entity- It refers to any legal, administrative, or any organizational structure or a

person with the capability to organize scarce resources so that to achieve objectives.

Economic entity- it refers to a group of entities that are comprised of controlling

entity and one or more than one controlled entities performing together to attain the objective

that is constant with those of the controlling activity.

3 Aasb.gov.au, Aasb.Gov.Au (Webpage, 2020)

<https://www.aasb.gov.au/admin/file/content105/c9/Conceptual_Framework_05-19.pdf>

4 Aasb.gov.au, Aasb.Gov.Au (Webpage, 2020) “https://www.aasb.gov.au/admin/file/content”102/c3/SAC1_8-

90_2001V.pdf

Index. Its infrastructure consists of local telephone exchanges, copper, cabinets and fibre

cables. CNU works within such products and services that are named as Fibre, Basic and

Enhanced Copper, Field Services, Value Added Network, and Infrastructure Services.

Reporting Entity

Paragraphs 3.10 of the AASB Conceptual Framework of Accounting defines the

reporting entity as an entity, which is required, or have selected to prepare financial reports. It

is not necessary to be a legal entity. An entity can be sole or a part of an entity or can be a

combination of more than one entity3. To explain a clear concept about the reporting entity

SAC 1 defines the following terms, which is discussed below, which puts a benchmark for

the financial reporting’s minimum required quality for an entity.

General-purpose of Financial Reporting- It means that a financial statement intends to

meet the user’s requirement who is not able to command the reports, thereby satisfying their

informational needs.

Control- The entity’s capacity to govern the decision making whether it is directly or

indirectly, in context with the fiscal and operating policies of a different entity so that to

allow that entity to perform and achieve the objectives of the controlling entity4.

Entity- It refers to any legal, administrative, or any organizational structure or a

person with the capability to organize scarce resources so that to achieve objectives.

Economic entity- it refers to a group of entities that are comprised of controlling

entity and one or more than one controlled entities performing together to attain the objective

that is constant with those of the controlling activity.

3 Aasb.gov.au, Aasb.Gov.Au (Webpage, 2020)

<https://www.aasb.gov.au/admin/file/content105/c9/Conceptual_Framework_05-19.pdf>

4 Aasb.gov.au, Aasb.Gov.Au (Webpage, 2020) “https://www.aasb.gov.au/admin/file/content”102/c3/SAC1_8-

90_2001V.pdf

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ADVANCED FINANCIAL ACCOUNTING

According to Paragraph 13 of the concept of entity, reporting states that its acceptance

is nor dependent on public or private sectors, business or non-business profits or legal or

other. Therefore, the Reporting entity consists of all the entities included economic entities as

a concern to which it can be expected that the users are dependent on such reports for making

their economic decisions. The concept of reporting entity is about fulfilling the necessities of

the users and evaluating the decision related to resource allocation, which has been clearly

mentioned in Paragraph 15 of the entity concept. The general propose of financial reporting

as per SAC 1, Paragraph 8 of reporting entity concept refers to those financial reports which

have been prepared so that to meet the objectives.

Chorus Limited is also a Reporting entity as it has chosen to maintain financial reports

for the user. Chorus Limited has adopted GAAP in New Zealand and Part 7 of the Financial

Markets Conduct Act 2013 for preparing its financial report, which is equivalent to the

guidelines of NZ International Financial Reporting Standards (IFRS). IFRS consists of a set

of rules that determine to reveal a consistent, transparent, and comparable financial statement

across the world5. The chosen accounting standards is considered appropriate for the profit-

oriented companies and with IFRSs.

Paragraph 3.15 reveals the components included in the financial reports. According to

Paragraph 3.11 of the AASB conceptual framework of reporting, there is a situation when a

single or parent entity has control of its other subsidiary entity. In that case, the reporting

entity has to prepare financial reports, which is called as consolidated financial statements6.

As Chorus Limited has two wholly-owned subsidiaries CNZL and CLTL, so the

Consolidated Financial report of the Chorus Limited as a single reporting entity provides

information about all their assets, liabilities, income, expenses and equity with clear notes.

5 Ifrs.org, "IFRS", Ifrs.Org (Webpage, 2020) <https://www.ifrs.org/about-us/who-we-are/>

6 Company.chorus.co.nz, Company.Chorus.Co.Nz (Webpage, 2020) <https://company.chorus.co.nz/file-

download/download/public/2019>

According to Paragraph 13 of the concept of entity, reporting states that its acceptance

is nor dependent on public or private sectors, business or non-business profits or legal or

other. Therefore, the Reporting entity consists of all the entities included economic entities as

a concern to which it can be expected that the users are dependent on such reports for making

their economic decisions. The concept of reporting entity is about fulfilling the necessities of

the users and evaluating the decision related to resource allocation, which has been clearly

mentioned in Paragraph 15 of the entity concept. The general propose of financial reporting

as per SAC 1, Paragraph 8 of reporting entity concept refers to those financial reports which

have been prepared so that to meet the objectives.

Chorus Limited is also a Reporting entity as it has chosen to maintain financial reports

for the user. Chorus Limited has adopted GAAP in New Zealand and Part 7 of the Financial

Markets Conduct Act 2013 for preparing its financial report, which is equivalent to the

guidelines of NZ International Financial Reporting Standards (IFRS). IFRS consists of a set

of rules that determine to reveal a consistent, transparent, and comparable financial statement

across the world5. The chosen accounting standards is considered appropriate for the profit-

oriented companies and with IFRSs.

Paragraph 3.15 reveals the components included in the financial reports. According to

Paragraph 3.11 of the AASB conceptual framework of reporting, there is a situation when a

single or parent entity has control of its other subsidiary entity. In that case, the reporting

entity has to prepare financial reports, which is called as consolidated financial statements6.

As Chorus Limited has two wholly-owned subsidiaries CNZL and CLTL, so the

Consolidated Financial report of the Chorus Limited as a single reporting entity provides

information about all their assets, liabilities, income, expenses and equity with clear notes.

5 Ifrs.org, "IFRS", Ifrs.Org (Webpage, 2020) <https://www.ifrs.org/about-us/who-we-are/>

6 Company.chorus.co.nz, Company.Chorus.Co.Nz (Webpage, 2020) <https://company.chorus.co.nz/file-

download/download/public/2019>

5ADVANCED FINANCIAL ACCOUNTING

The company provides different parameters of asset valuation, depreciation, allocation of

costs amongst fibre and other services, crown financing and unrecovered losses7.

Consolidated financial reports are maintained to provide discrete data about the assets,

liabilities, income, expense and equity of all its subsidiaries.

Fundamental Qualitative Characteristics

The qualitative characteristics of financial data are to identify the kinds of data, which

can be more useful for its existing and potential investors and lenders so that to make

decisions about the reporting entity based on the data provided within the financial reports.

Financial reports of a company provide information about the economic resources of

reporting8. Some financial reports possibly do not reveal explanatory material that is related

to the expectation of the management and their strategies or any other types of information

that reflects the forward-looking information of the company.

According to Paragraph 2.4 of the AASB conceptual framework of accounting, the

financial information within the annual report is to be represented faithfully and must be

relevance. The financial data represented in the financial reports can be enhanced if it is

timely and can be comparable, verifiable and understandable9. It means that the financial

report is to be prepared by the company in such a way that it gives a clear understanding to

the users about its similarities and differences between the entities. The information must be

confirmed with reliable resources and materialistic information timely represented amongst

the users. The understandability of the report means to prepare the reports in such a manner

that is prepared, classified, and represented to the users in a clear and concise manner.

7 Houqe, Muhammad Nurul, Reza M. Monem, and Tony van Zijl. "The economic consequences of IFRS

adoption: Evidence from New Zealand." Journal of International Accounting, Auditing and Taxation 27 (2016):

40-48.

8 Herath, S.K. and Albarqi, N., 2017. Financial reporting quality: A literature review. Int. J. Bus. Manag.

Commer, 2(2), pp.1-14.

9 Bisogno, M., Santis, S. and Tommasetti, A., 2015. Public-Sector consolidated financial statements: An

analysis of the comment letters on IPSASB’s exposure draft no. 49. International Journal of Public

Administration, 38(4), pp.311-324.

The company provides different parameters of asset valuation, depreciation, allocation of

costs amongst fibre and other services, crown financing and unrecovered losses7.

Consolidated financial reports are maintained to provide discrete data about the assets,

liabilities, income, expense and equity of all its subsidiaries.

Fundamental Qualitative Characteristics

The qualitative characteristics of financial data are to identify the kinds of data, which

can be more useful for its existing and potential investors and lenders so that to make

decisions about the reporting entity based on the data provided within the financial reports.

Financial reports of a company provide information about the economic resources of

reporting8. Some financial reports possibly do not reveal explanatory material that is related

to the expectation of the management and their strategies or any other types of information

that reflects the forward-looking information of the company.

According to Paragraph 2.4 of the AASB conceptual framework of accounting, the

financial information within the annual report is to be represented faithfully and must be

relevance. The financial data represented in the financial reports can be enhanced if it is

timely and can be comparable, verifiable and understandable9. It means that the financial

report is to be prepared by the company in such a way that it gives a clear understanding to

the users about its similarities and differences between the entities. The information must be

confirmed with reliable resources and materialistic information timely represented amongst

the users. The understandability of the report means to prepare the reports in such a manner

that is prepared, classified, and represented to the users in a clear and concise manner.

7 Houqe, Muhammad Nurul, Reza M. Monem, and Tony van Zijl. "The economic consequences of IFRS

adoption: Evidence from New Zealand." Journal of International Accounting, Auditing and Taxation 27 (2016):

40-48.

8 Herath, S.K. and Albarqi, N., 2017. Financial reporting quality: A literature review. Int. J. Bus. Manag.

Commer, 2(2), pp.1-14.

9 Bisogno, M., Santis, S. and Tommasetti, A., 2015. Public-Sector consolidated financial statements: An

analysis of the comment letters on IPSASB’s exposure draft no. 49. International Journal of Public

Administration, 38(4), pp.311-324.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ADVANCED FINANCIAL ACCOUNTING

Relevance and Faithful Representation

Fundamental qualitative characteristics are the qualities that are essential for the

financial reports, or else the whole purpose of the preparation of the financial reports would

be defeated10. According to AASB para 2.5, the fundamental qualitative characteristics are

considered to relevance and faithful representation.

Relevance means that the entire material information that can be helpful for the users

for their economic decision making should be disclosed in the financial report irrespective of

the fact whether it is used or not. As per para 2.6 of AASB, relevant financial data is

proficient in creating an alteration in the decision making made by the users.

Faithful representation means that is contained within the financial report should be

complete and unbiased. It must be free from material misstatement, so that gives a true and

fair view of the company11. As per the AASB conceptual framework, financial reports

demonstrate its fiscal phenomena in words and numbers. To represent a pure, faithful

representation, the information provided within the report has to be complete, error free, and

neutral.

Chorus Limited has summarized its measurement basis that is relevant to understand

the financial reports and is provided throughout the notes. The measurement basis is adopted

as historical cost while preparing the reports. The accounting standards adopted by the

company and computed data have also revealed in the reports to remove any ambiguity.

Chorus is lessee and lessor of specific network assets within the lease agreement. Chorus

adopts NZ IFRS 16 Lease within its report that allows a single discount rate to a portfolio

lease with parallel features. The company has adopted three new accounting standards NZ

10 Bisogno, M., Santis, S. and Tommasetti, A., 2015. Public-Sector consolidated financial statements: An

analysis of the comment letters on IPSASB’s exposure draft no. 49. International Journal of Public

Administration, 38(4), pp.311-324.

11Andon, P., Baxter, J. and Chua, W.F., 2015. Accounting for stakeholders and making accounting

useful. Journal of Management Studies, 52(7), pp.986-1002.

Relevance and Faithful Representation

Fundamental qualitative characteristics are the qualities that are essential for the

financial reports, or else the whole purpose of the preparation of the financial reports would

be defeated10. According to AASB para 2.5, the fundamental qualitative characteristics are

considered to relevance and faithful representation.

Relevance means that the entire material information that can be helpful for the users

for their economic decision making should be disclosed in the financial report irrespective of

the fact whether it is used or not. As per para 2.6 of AASB, relevant financial data is

proficient in creating an alteration in the decision making made by the users.

Faithful representation means that is contained within the financial report should be

complete and unbiased. It must be free from material misstatement, so that gives a true and

fair view of the company11. As per the AASB conceptual framework, financial reports

demonstrate its fiscal phenomena in words and numbers. To represent a pure, faithful

representation, the information provided within the report has to be complete, error free, and

neutral.

Chorus Limited has summarized its measurement basis that is relevant to understand

the financial reports and is provided throughout the notes. The measurement basis is adopted

as historical cost while preparing the reports. The accounting standards adopted by the

company and computed data have also revealed in the reports to remove any ambiguity.

Chorus is lessee and lessor of specific network assets within the lease agreement. Chorus

adopts NZ IFRS 16 Lease within its report that allows a single discount rate to a portfolio

lease with parallel features. The company has adopted three new accounting standards NZ

10 Bisogno, M., Santis, S. and Tommasetti, A., 2015. Public-Sector consolidated financial statements: An

analysis of the comment letters on IPSASB’s exposure draft no. 49. International Journal of Public

Administration, 38(4), pp.311-324.

11Andon, P., Baxter, J. and Chua, W.F., 2015. Accounting for stakeholders and making accounting

useful. Journal of Management Studies, 52(7), pp.986-1002.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ADVANCED FINANCIAL ACCOUNTING

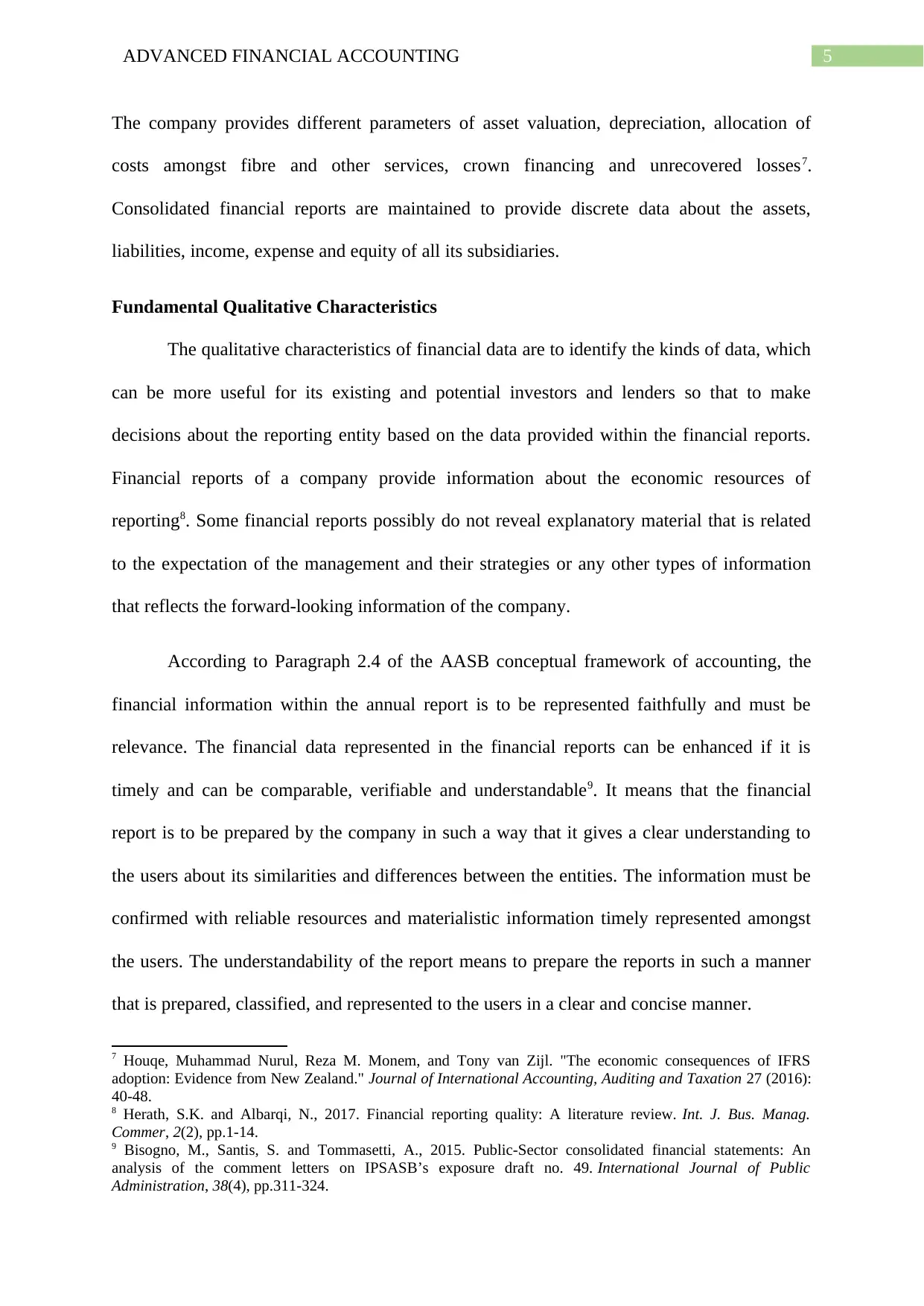

IFRS 9 financial instruments, 15 revenue from a contract with customers and 16 leases12. The

company has clearly described its lease valuation under the notes. The net lease payable of

the company is $254 million, in which $8M is current whose computation is shown below.

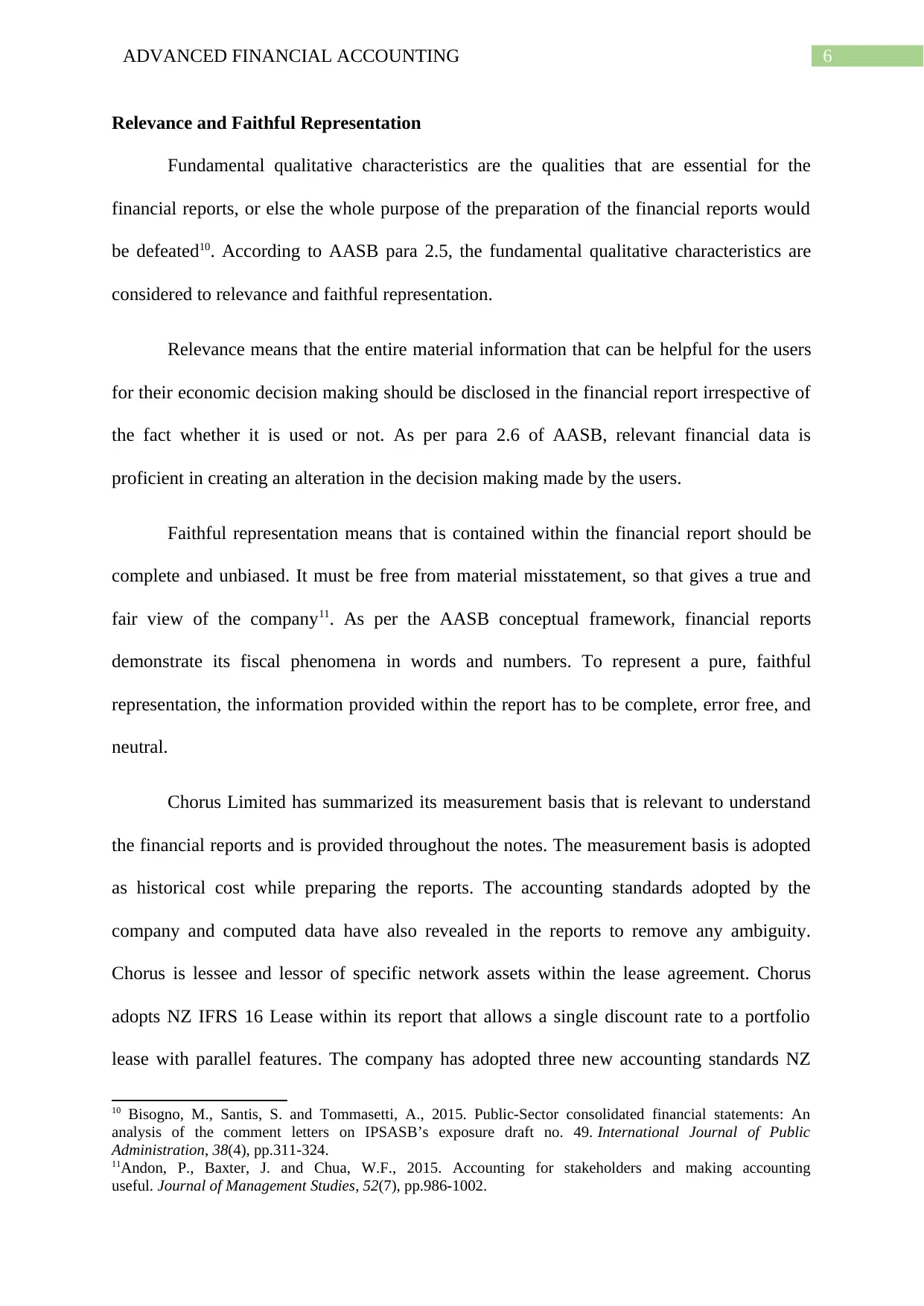

Chorus Limited has made estimation and assumptions for the future that may affect

the amount of assets and liabilities and the amount of revenue and expenses during the year.

The company has separately revealed the figures of copper and fibre that is useful for the

users in understanding and evaluating the data. The EBITDA for the year 2019 is revealed at

$636 million, which shows downfall from the previous year that is from $653M. The

company’s income statement has disclosed the figures, as shown below.

12 Richards, Glenn, and Chris van Staden. "The readability impact of international financial reporting

standards." Pacific Accounting Review (2015).

IFRS 9 financial instruments, 15 revenue from a contract with customers and 16 leases12. The

company has clearly described its lease valuation under the notes. The net lease payable of

the company is $254 million, in which $8M is current whose computation is shown below.

Chorus Limited has made estimation and assumptions for the future that may affect

the amount of assets and liabilities and the amount of revenue and expenses during the year.

The company has separately revealed the figures of copper and fibre that is useful for the

users in understanding and evaluating the data. The EBITDA for the year 2019 is revealed at

$636 million, which shows downfall from the previous year that is from $653M. The

company’s income statement has disclosed the figures, as shown below.

12 Richards, Glenn, and Chris van Staden. "The readability impact of international financial reporting

standards." Pacific Accounting Review (2015).

8ADVANCED FINANCIAL ACCOUNTING

Chorus Limited has shown its operating revenue in the year 2019 decreased from the

previous year. The company has revealed in their financial report that the growth of fiber

broadband mostly offsets the reduction in the copper connections. In addition to this, its tight

control over cost has decreased its operating expenses for the year 2019. The company has

issued a $500M bond in December 2018, whose average rate of interest presently is 5.75%.

The Chorus has slowed to conduct an independent audit for its financial statement for

representing a faithful and relevant reporting of its financial statement for the year 2019. The

application of the audit was influenced by materiality so that to evaluate the effect of

misstatement13. It helps to remove any misguidance to the users from any misstatement either

due to fraud or due to error14. The materiality for the company is chosen for the consolidated

financial report at $5.9 million. The audit has revealed its key audit matter in its report, which

highlighted the matter that could be relevant for the users.

Conclusion

The information disclosed within the company’s annual report is about the business's

current financial position and gives a detailed description of the ongoing operations of the

company. The application of IFRS plays an essential role in a fair and transparent view of the

financial report of the company. The users of the company find it relevant for making and

effective financial decision. The annual report of Chorus Limited gives users relevant

information about its liabilities and assets and demonstrates a clear picture to the users. The

audit report displays that the company has given authentic information to the users and key

audit matters have been highlighted. However, the company can provide their explanations

for all the assets and liabilities within their report for a better understanding of the users.

Further, the company can provide detail about all the accounting standards used within the

13 Douglas, Regan. "Quantitative materiality disclosure and the impact on investor decision making and

perceptions of audit quality." (2017).

14 Li, Hong, David Hay, and David Lau. "Assessing the impact of the new auditor’s report." Pacific Accounting

Review (2019).

Chorus Limited has shown its operating revenue in the year 2019 decreased from the

previous year. The company has revealed in their financial report that the growth of fiber

broadband mostly offsets the reduction in the copper connections. In addition to this, its tight

control over cost has decreased its operating expenses for the year 2019. The company has

issued a $500M bond in December 2018, whose average rate of interest presently is 5.75%.

The Chorus has slowed to conduct an independent audit for its financial statement for

representing a faithful and relevant reporting of its financial statement for the year 2019. The

application of the audit was influenced by materiality so that to evaluate the effect of

misstatement13. It helps to remove any misguidance to the users from any misstatement either

due to fraud or due to error14. The materiality for the company is chosen for the consolidated

financial report at $5.9 million. The audit has revealed its key audit matter in its report, which

highlighted the matter that could be relevant for the users.

Conclusion

The information disclosed within the company’s annual report is about the business's

current financial position and gives a detailed description of the ongoing operations of the

company. The application of IFRS plays an essential role in a fair and transparent view of the

financial report of the company. The users of the company find it relevant for making and

effective financial decision. The annual report of Chorus Limited gives users relevant

information about its liabilities and assets and demonstrates a clear picture to the users. The

audit report displays that the company has given authentic information to the users and key

audit matters have been highlighted. However, the company can provide their explanations

for all the assets and liabilities within their report for a better understanding of the users.

Further, the company can provide detail about all the accounting standards used within the

13 Douglas, Regan. "Quantitative materiality disclosure and the impact on investor decision making and

perceptions of audit quality." (2017).

14 Li, Hong, David Hay, and David Lau. "Assessing the impact of the new auditor’s report." Pacific Accounting

Review (2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ADVANCED FINANCIAL ACCOUNTING

report and can add some other accounting standards to reflect better and transparent

reporting.

report and can add some other accounting standards to reflect better and transparent

reporting.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ADVANCED FINANCIAL ACCOUNTING

References

Aasb.gov.au, Aasb.Gov.Au (Webpage, 2020)

<https://www.aasb.gov.au/admin/file/content105/c9/Conceptual_Framework_05-19.pdf>

Aasb.gov.au, Aasb.Gov.Au (Webpage, 2020)

<https://www.aasb.gov.au/admin/file/content102/c3/SAC1_8-90_2001V.pdf>

Andon, P., Baxter, J. and Chua, W.F., 2015. Accounting for stakeholders and making

accounting useful. Journal of Management Studies, 52(7), pp.986-1002.

Bisogno, M., Santis, S. and Tommasetti, A., 2015. Public-Sector consolidated financial

statements: An analysis of the comment letters on IPSASB’s exposure draft no.

49. International Journal of Public Administration, 38(4), pp.311-324.

Bisogno, M., Santis, S. and Tommasetti, A., 2015. Public-Sector consolidated financial

statements: An analysis of the comment letters on IPSASB’s exposure draft no.

49. International Journal of Public Administration, 38(4), pp.311-324.

Douglas, Regan. "Quantitative materiality disclosure and the impact on investor decision

making and perceptions of audit quality." (2017).

Eyisi, A.S. and Okpe, I.I., 2014. The impact of cash flow ratio on corporate

performance. Research Journal of Finance and Accounting, 5(6).

Herath, S.K. and Albarqi, N., 2017. Financial reporting quality: A literature review. Int. J.

Bus. Manag. Commer, 2(2), pp.1-14.

Houqe, Muhammad Nurul, Reza M. Monem, and Tony van Zijl. "The economic

consequences of IFRS adoption: Evidence from New Zealand." Journal of International

Accounting, Auditing and Taxation 27 (2016): 40-48.

References

Aasb.gov.au, Aasb.Gov.Au (Webpage, 2020)

<https://www.aasb.gov.au/admin/file/content105/c9/Conceptual_Framework_05-19.pdf>

Aasb.gov.au, Aasb.Gov.Au (Webpage, 2020)

<https://www.aasb.gov.au/admin/file/content102/c3/SAC1_8-90_2001V.pdf>

Andon, P., Baxter, J. and Chua, W.F., 2015. Accounting for stakeholders and making

accounting useful. Journal of Management Studies, 52(7), pp.986-1002.

Bisogno, M., Santis, S. and Tommasetti, A., 2015. Public-Sector consolidated financial

statements: An analysis of the comment letters on IPSASB’s exposure draft no.

49. International Journal of Public Administration, 38(4), pp.311-324.

Bisogno, M., Santis, S. and Tommasetti, A., 2015. Public-Sector consolidated financial

statements: An analysis of the comment letters on IPSASB’s exposure draft no.

49. International Journal of Public Administration, 38(4), pp.311-324.

Douglas, Regan. "Quantitative materiality disclosure and the impact on investor decision

making and perceptions of audit quality." (2017).

Eyisi, A.S. and Okpe, I.I., 2014. The impact of cash flow ratio on corporate

performance. Research Journal of Finance and Accounting, 5(6).

Herath, S.K. and Albarqi, N., 2017. Financial reporting quality: A literature review. Int. J.

Bus. Manag. Commer, 2(2), pp.1-14.

Houqe, Muhammad Nurul, Reza M. Monem, and Tony van Zijl. "The economic

consequences of IFRS adoption: Evidence from New Zealand." Journal of International

Accounting, Auditing and Taxation 27 (2016): 40-48.

11ADVANCED FINANCIAL ACCOUNTING

Howieson, Bryan. "The phoenix rises: The Australian accounting standards board and IFRS

adoption." Journal of International Accounting Research 16.2 (2017): 127-154.

Ifrs.org, "IFRS", Ifrs.Org (Webpage, 2020) <https://www.ifrs.org/about-us/who-we-are/>

Laing, G. and Perrin, R.W., 2014. Deconstructing an accounting paradigm shift: AASB 116

non-current asset measurement models. International Journal of Critical Accounting, 6(5/6),

pp.509-519.

Li, Hong, David Hay, and David Lau. "Assessing the impact of the new auditor’s

report." Pacific Accounting Review (2019).

Richards, Glenn, and Chris van Staden. "The readability impact of international financial

reporting standards." Pacific Accounting Review (2015).

Yu, Gwen, and Aida Sijamic Wahid. "Accounting standards and international portfolio

holdings." The Accounting Review 89.5 (2014): 1895-1930.

Howieson, Bryan. "The phoenix rises: The Australian accounting standards board and IFRS

adoption." Journal of International Accounting Research 16.2 (2017): 127-154.

Ifrs.org, "IFRS", Ifrs.Org (Webpage, 2020) <https://www.ifrs.org/about-us/who-we-are/>

Laing, G. and Perrin, R.W., 2014. Deconstructing an accounting paradigm shift: AASB 116

non-current asset measurement models. International Journal of Critical Accounting, 6(5/6),

pp.509-519.

Li, Hong, David Hay, and David Lau. "Assessing the impact of the new auditor’s

report." Pacific Accounting Review (2019).

Richards, Glenn, and Chris van Staden. "The readability impact of international financial

reporting standards." Pacific Accounting Review (2015).

Yu, Gwen, and Aida Sijamic Wahid. "Accounting standards and international portfolio

holdings." The Accounting Review 89.5 (2014): 1895-1930.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.