Advanced Financial Accounting Assignment - University Name

VerifiedAdded on 2023/04/26

|8

|1306

|369

Homework Assignment

AI Summary

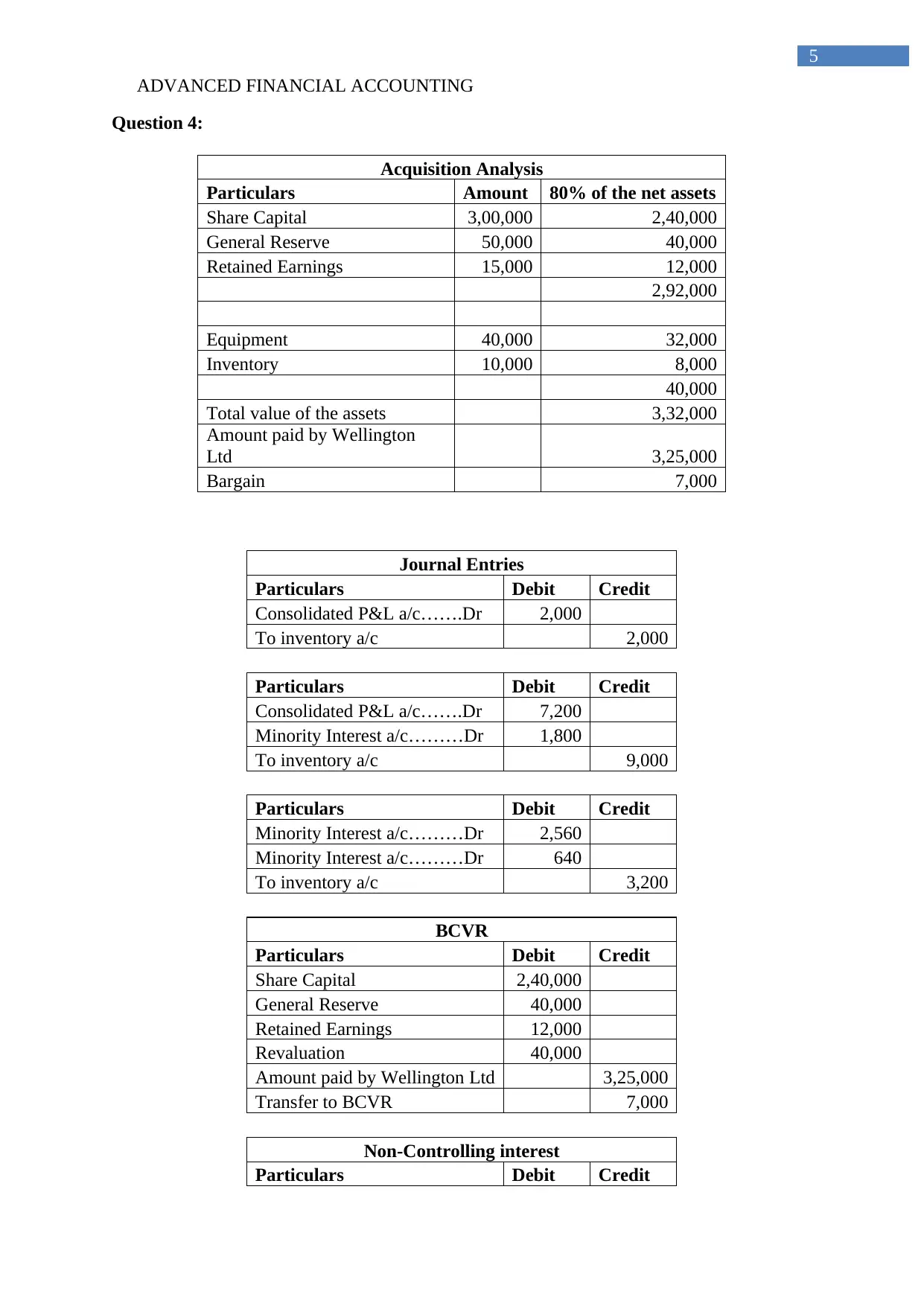

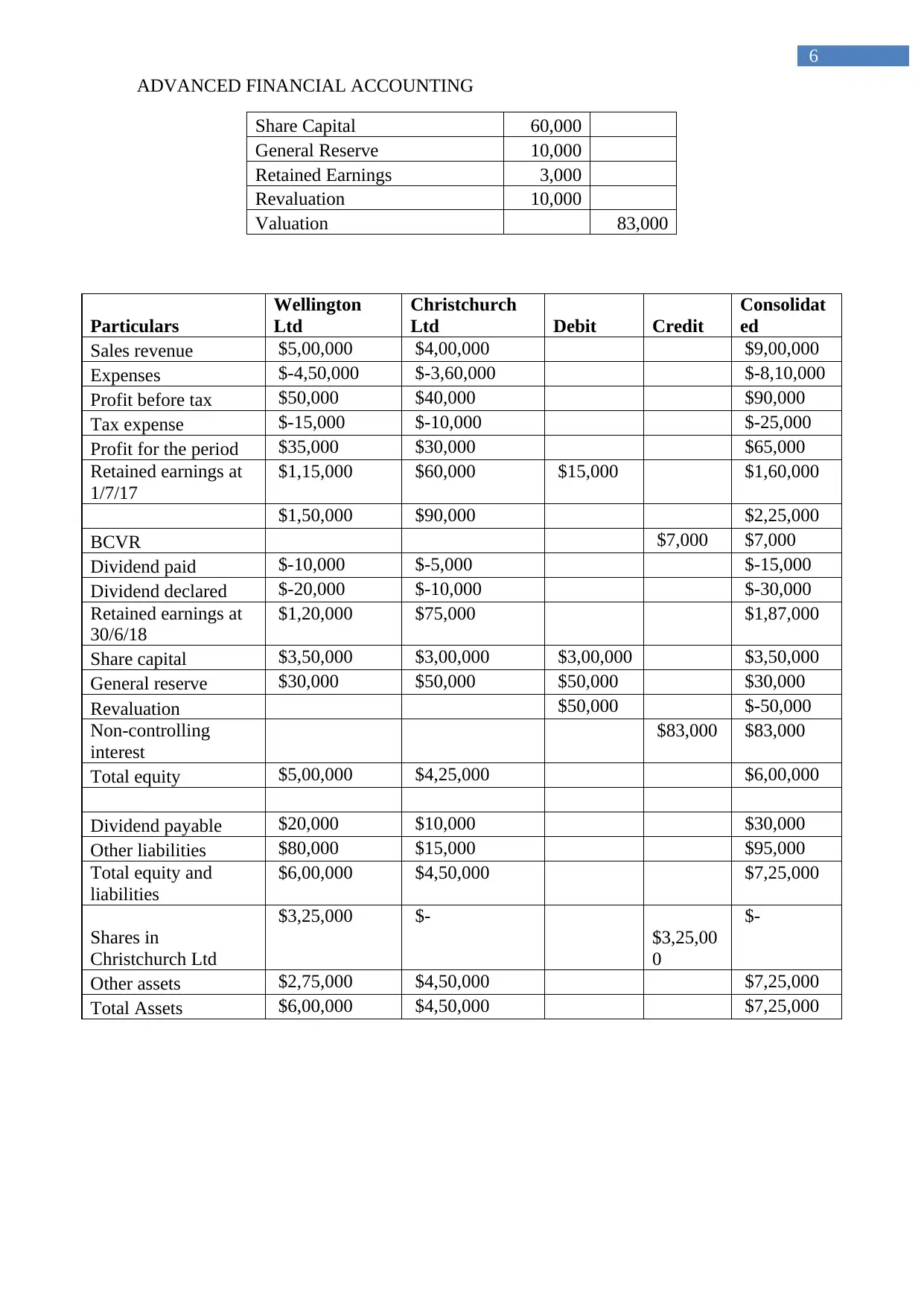

This document provides a comprehensive solution to an advanced financial accounting assignment. The solution addresses several key areas, including the calculation of current tax and the preparation of the tax journal entry, with detailed explanations of the steps involved. It also analyzes a call option contract, categorizing it as a derivative financial instrument and outlining the accounting treatment from both the buyer's and seller's perspectives, including journal entries. Furthermore, the document includes journal entries for various transactions, such as purchases and land acquisition, and provides a detailed analysis of consolidated financial statements, covering the acquisition of a subsidiary, calculation of goodwill, and preparation of consolidated profit and loss statements and balance sheets. The assignment covers topics such as derivative instruments, journal entries, and consolidated financial statements.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.