Financial Accounting Assignment: Comprehensive Solutions and Analysis

VerifiedAdded on 2022/12/27

|11

|1485

|70

Homework Assignment

AI Summary

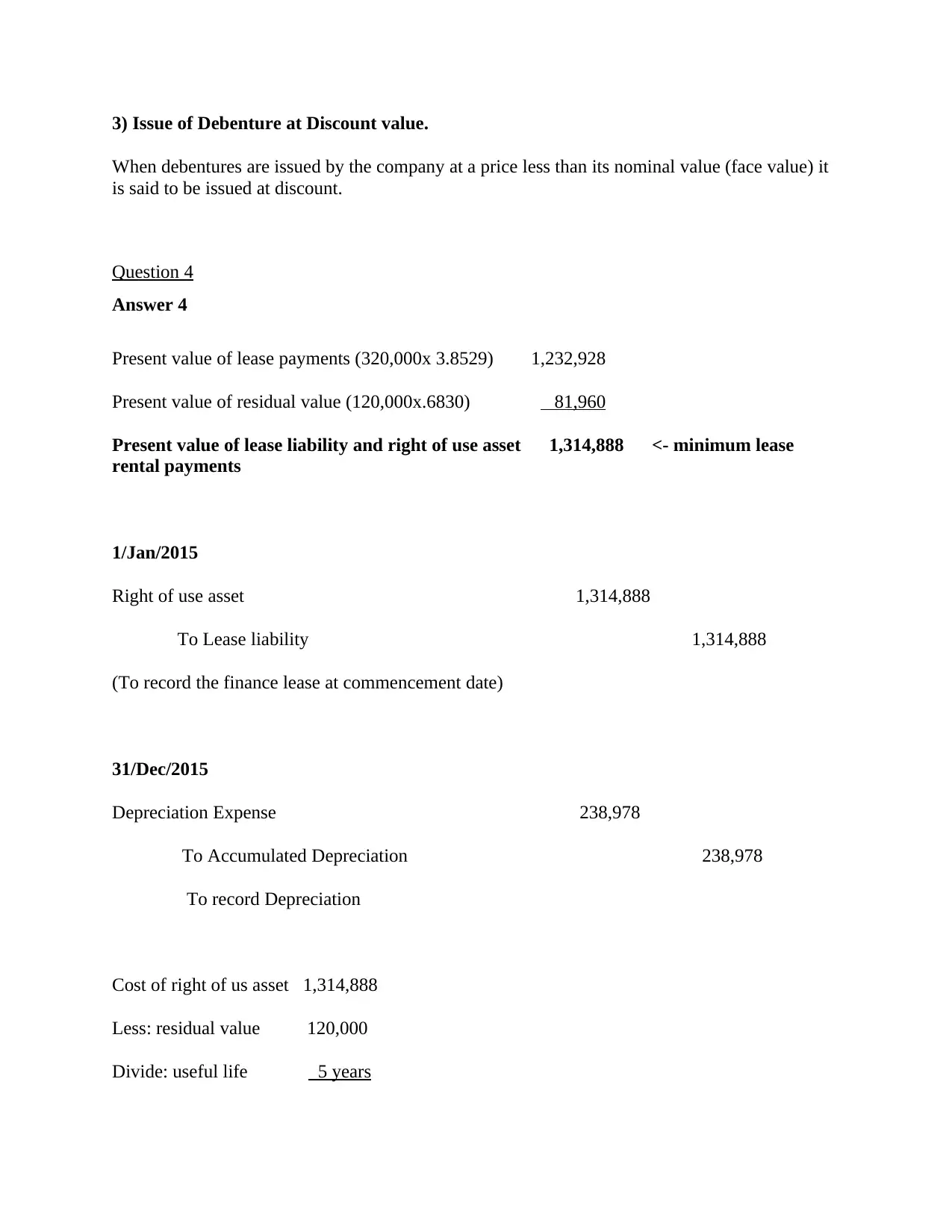

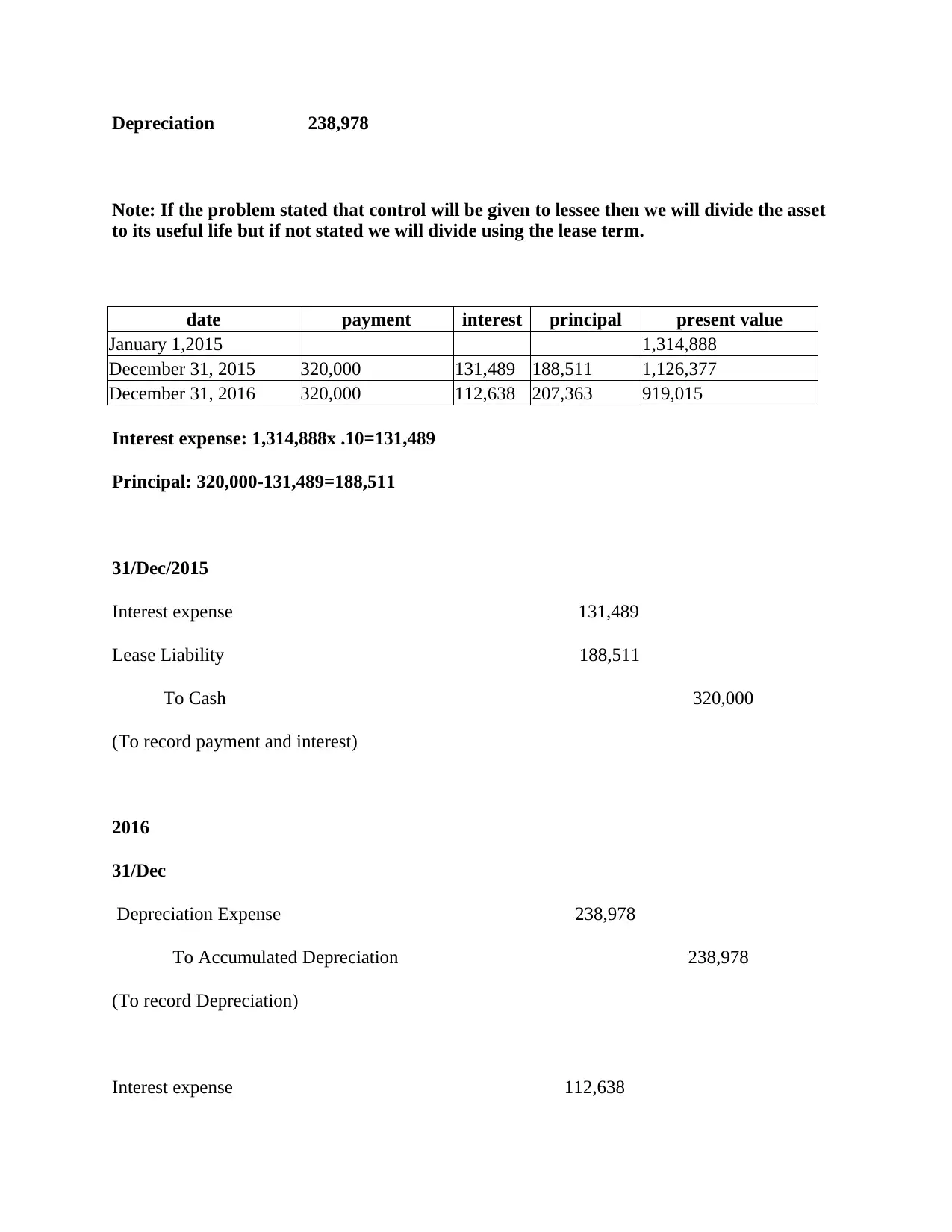

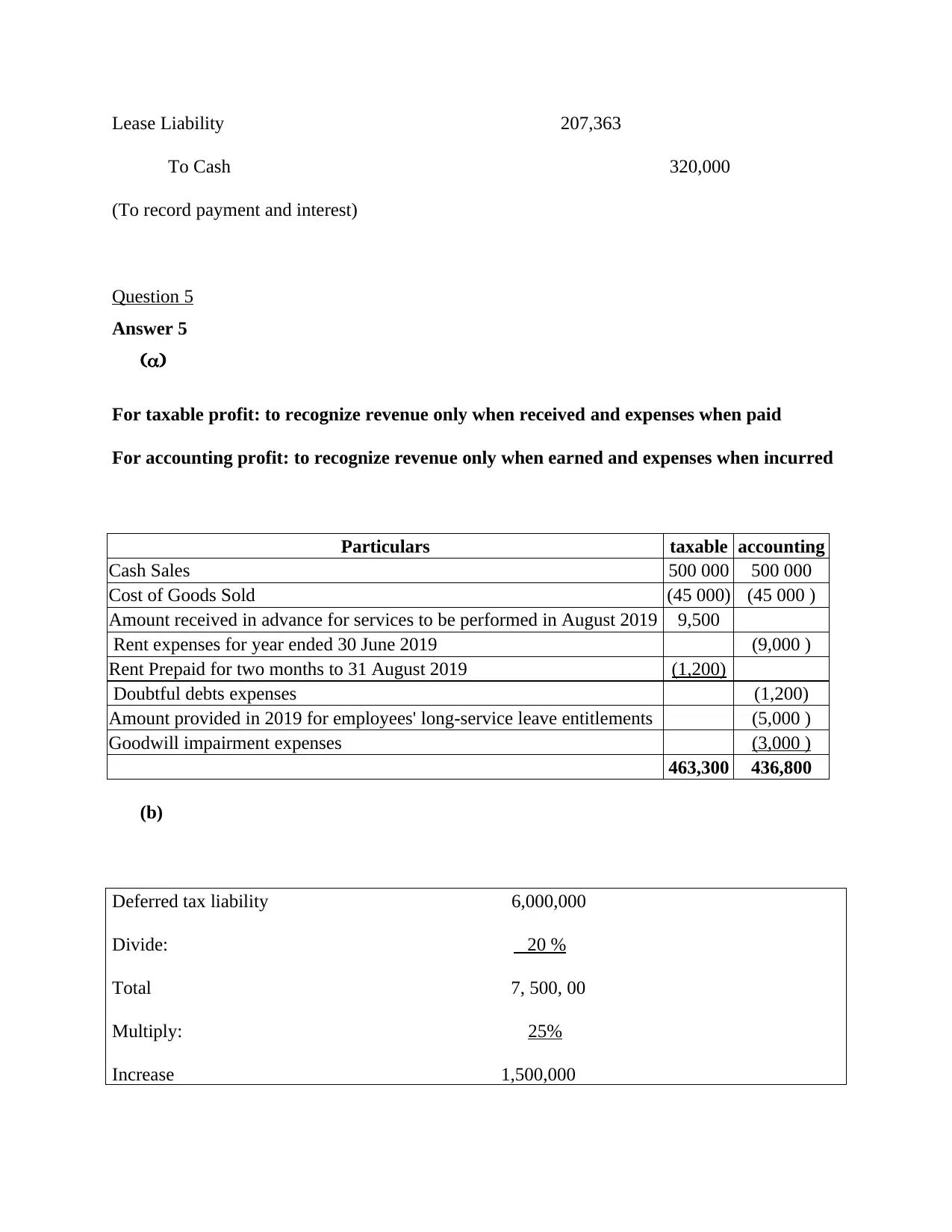

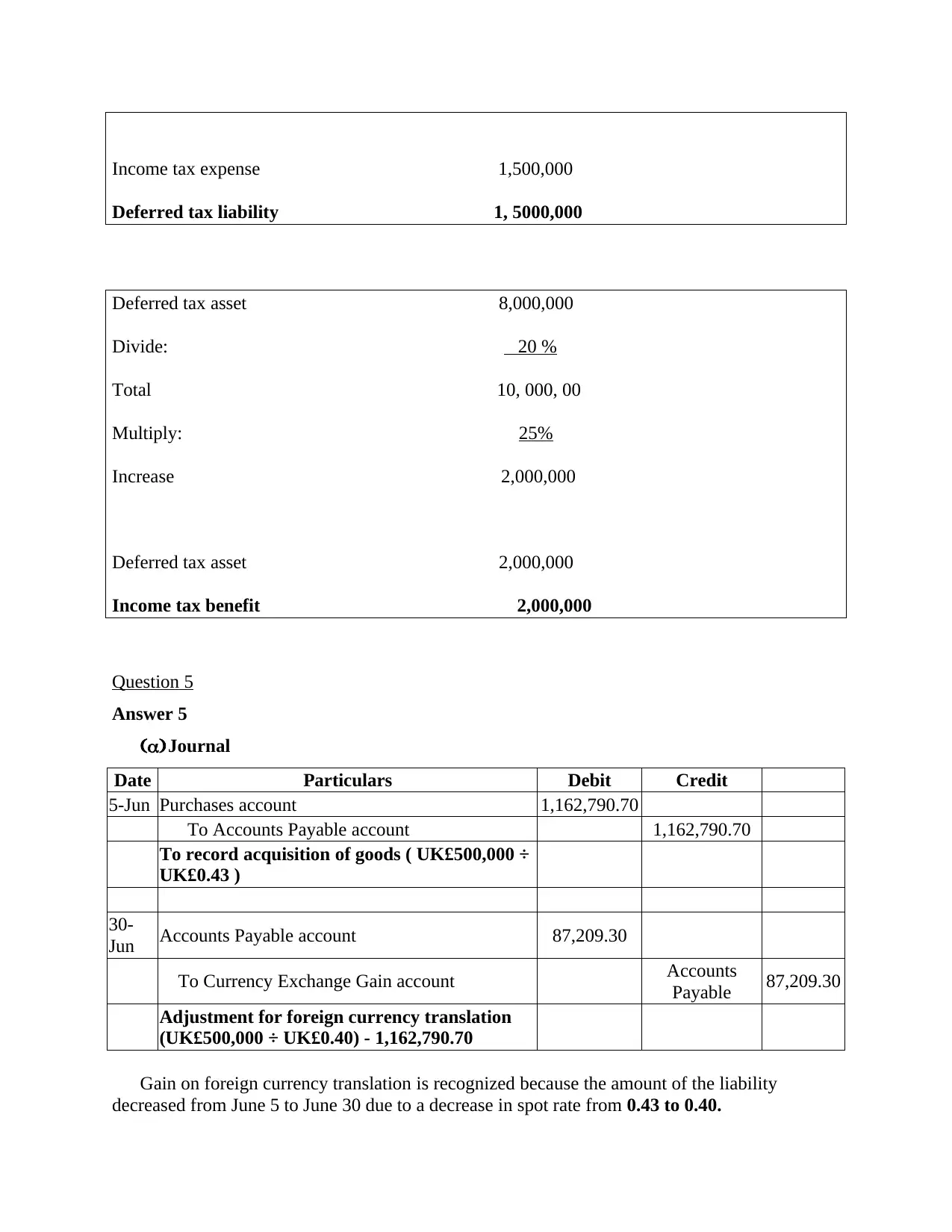

This document provides a comprehensive set of solutions for an advanced financial accounting assignment. The solutions cover a range of topics, including asset acquisition, journal entries for revaluation losses, debenture accounting (issuance, interest, and redemption), lease accounting (present value calculations, journal entries for both lessee and lessor), deferred tax calculations, and foreign currency translation. Each question is answered with detailed step-by-step explanations, including journal entries, calculations, and relevant accounting principles. The document also includes a list of references to support the solutions provided. This resource is valuable for students studying financial accounting, providing a clear understanding of complex accounting concepts and practical application through detailed examples and explanations.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.