Advanced Financial Accounting Report: Impairment and Leasing Standards

VerifiedAdded on 2020/05/28

|12

|2497

|80

Report

AI Summary

This report delves into advanced financial accounting, focusing on impairment testing and leasing standards within the context of Sai Global Limited's financial statements. Part A examines impairment testing of various assets, including goodwill, intangible assets, and trade receivables, detailing the two-step impairment process, the company's impairment expenditures, and the estimation of value-in-use. It also explores the subjectivity inherent in applying IAS 36 and the determination of fair value under IFRS 113. Part B shifts to the impact of new accounting standards on leasing, highlighting the historical treatment of operating leases, the lack of comparability, and the potential economic and commercial impacts of these changes. The report emphasizes the significance of these accounting changes for investors and financial statement users, and how the new standards aim to improve decision-making related to leasing versus purchasing assets. The report concludes with a list of relevant references to support the analysis.

Running head: ADVANCED FINANCIAL ACCOUNTING

Advanced Financial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Advanced Financial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ADVANCED FINANCIAL ACCOUNTING

Table of Contents

Part A:..............................................................................................................................................2

Part (i):.........................................................................................................................................2

Part (ii):........................................................................................................................................2

Part (iii):.......................................................................................................................................3

Part (iv):.......................................................................................................................................4

Part (v):........................................................................................................................................4

Part (vi):.......................................................................................................................................5

Part (vii):......................................................................................................................................5

Part (viii):.....................................................................................................................................5

Part B:..............................................................................................................................................6

Part (i):.........................................................................................................................................6

Part (ii):........................................................................................................................................7

Part (iii):.......................................................................................................................................7

Part (iv):.......................................................................................................................................8

Part (v):........................................................................................................................................8

References:......................................................................................................................................9

Table of Contents

Part A:..............................................................................................................................................2

Part (i):.........................................................................................................................................2

Part (ii):........................................................................................................................................2

Part (iii):.......................................................................................................................................3

Part (iv):.......................................................................................................................................4

Part (v):........................................................................................................................................4

Part (vi):.......................................................................................................................................5

Part (vii):......................................................................................................................................5

Part (viii):.....................................................................................................................................5

Part B:..............................................................................................................................................6

Part (i):.........................................................................................................................................6

Part (ii):........................................................................................................................................7

Part (iii):.......................................................................................................................................7

Part (iv):.......................................................................................................................................8

Part (v):........................................................................................................................................8

References:......................................................................................................................................9

2ADVANCED FINANCIAL ACCOUNTING

Part A:

Part (i):

As per the financial statements report of Sai Global limited for the year 2015,

impairment testing for several asset classes was carried out. Several intangible assets with

goodwill are not amortized and they are further tested for annual impairment. In case frequency

is more than once annually because of differences within situations or events it indicates that

assets might are impaired and are mentioned within the annual report at less cost with

accumulated impairment loss (Amel-Zadeh et al. 2016). Some different assets like the trade

receivables along with property, plant and equipment with inventory are taken into impairment

testing while there is an indication that the assets carrying amount might not be recoverable.

Part (ii):

Sai Global limited carries out a two-step process in impairment testing. The first step is to

align by the fair value of reporting unit within its carrying value that includes the goodwill. In

case the operating unit’s carrying value is higher in contrast to the fair value, the second step

associated with impairment testing must be conducted for ensuring the amount of impairment

loss in case it takes place (Carlin, Finch and Manh Tran 2014). The second step explains the

impaired fair value of reporting unit along with the carrying amount associated with the unit. In

case the implied fair value is lesser in comparison to the carrying amount, certain charge of

impairment is realized within the amount related to that excess. Such realized loss cannot be

more than the asset’s carrying amount.

Part A:

Part (i):

As per the financial statements report of Sai Global limited for the year 2015,

impairment testing for several asset classes was carried out. Several intangible assets with

goodwill are not amortized and they are further tested for annual impairment. In case frequency

is more than once annually because of differences within situations or events it indicates that

assets might are impaired and are mentioned within the annual report at less cost with

accumulated impairment loss (Amel-Zadeh et al. 2016). Some different assets like the trade

receivables along with property, plant and equipment with inventory are taken into impairment

testing while there is an indication that the assets carrying amount might not be recoverable.

Part (ii):

Sai Global limited carries out a two-step process in impairment testing. The first step is to

align by the fair value of reporting unit within its carrying value that includes the goodwill. In

case the operating unit’s carrying value is higher in contrast to the fair value, the second step

associated with impairment testing must be conducted for ensuring the amount of impairment

loss in case it takes place (Carlin, Finch and Manh Tran 2014). The second step explains the

impaired fair value of reporting unit along with the carrying amount associated with the unit. In

case the implied fair value is lesser in comparison to the carrying amount, certain charge of

impairment is realized within the amount related to that excess. Such realized loss cannot be

more than the asset’s carrying amount.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ADVANCED FINANCIAL ACCOUNTING

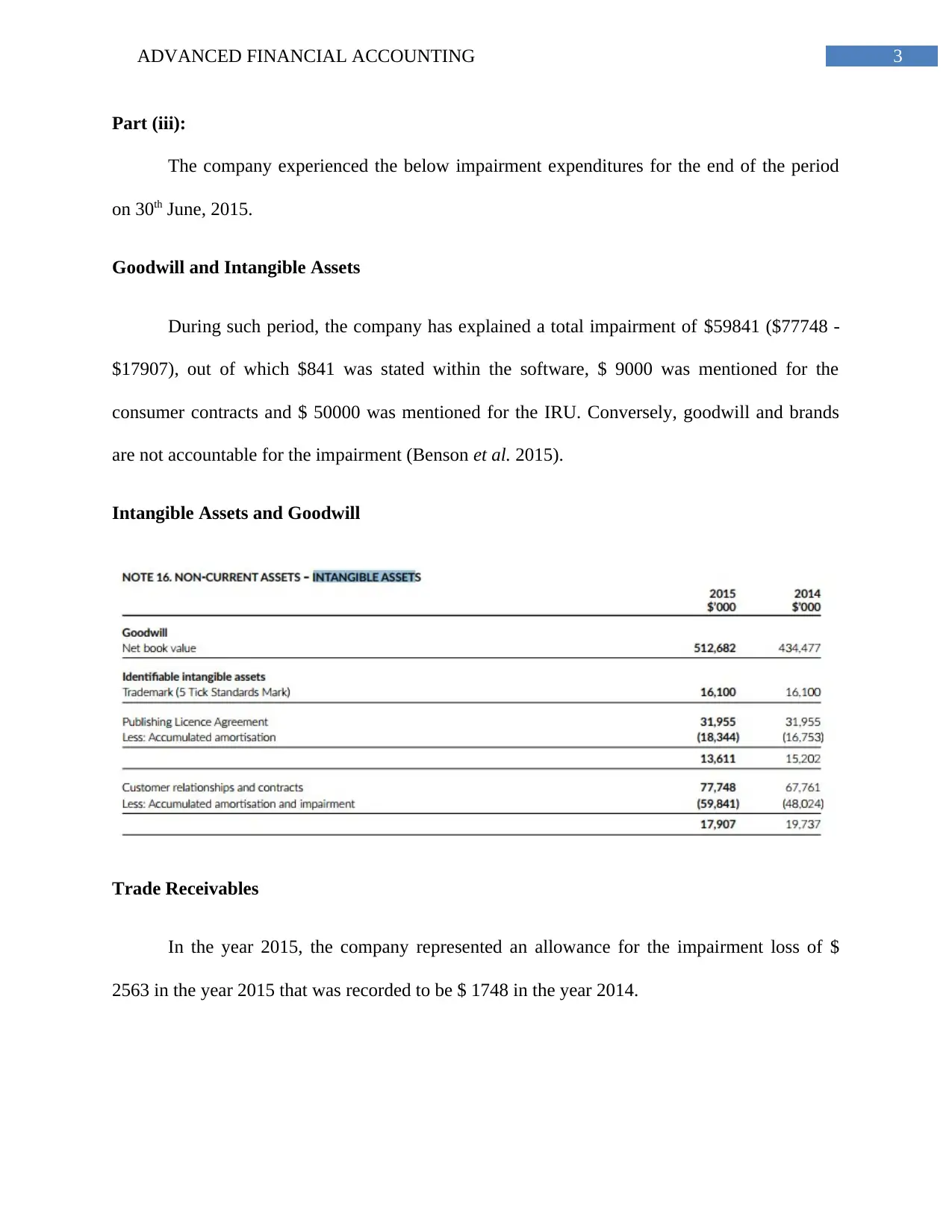

Part (iii):

The company experienced the below impairment expenditures for the end of the period

on 30th June, 2015.

Goodwill and Intangible Assets

During such period, the company has explained a total impairment of $59841 ($77748 -

$17907), out of which $841 was stated within the software, $ 9000 was mentioned for the

consumer contracts and $ 50000 was mentioned for the IRU. Conversely, goodwill and brands

are not accountable for the impairment (Benson et al. 2015).

Intangible Assets and Goodwill

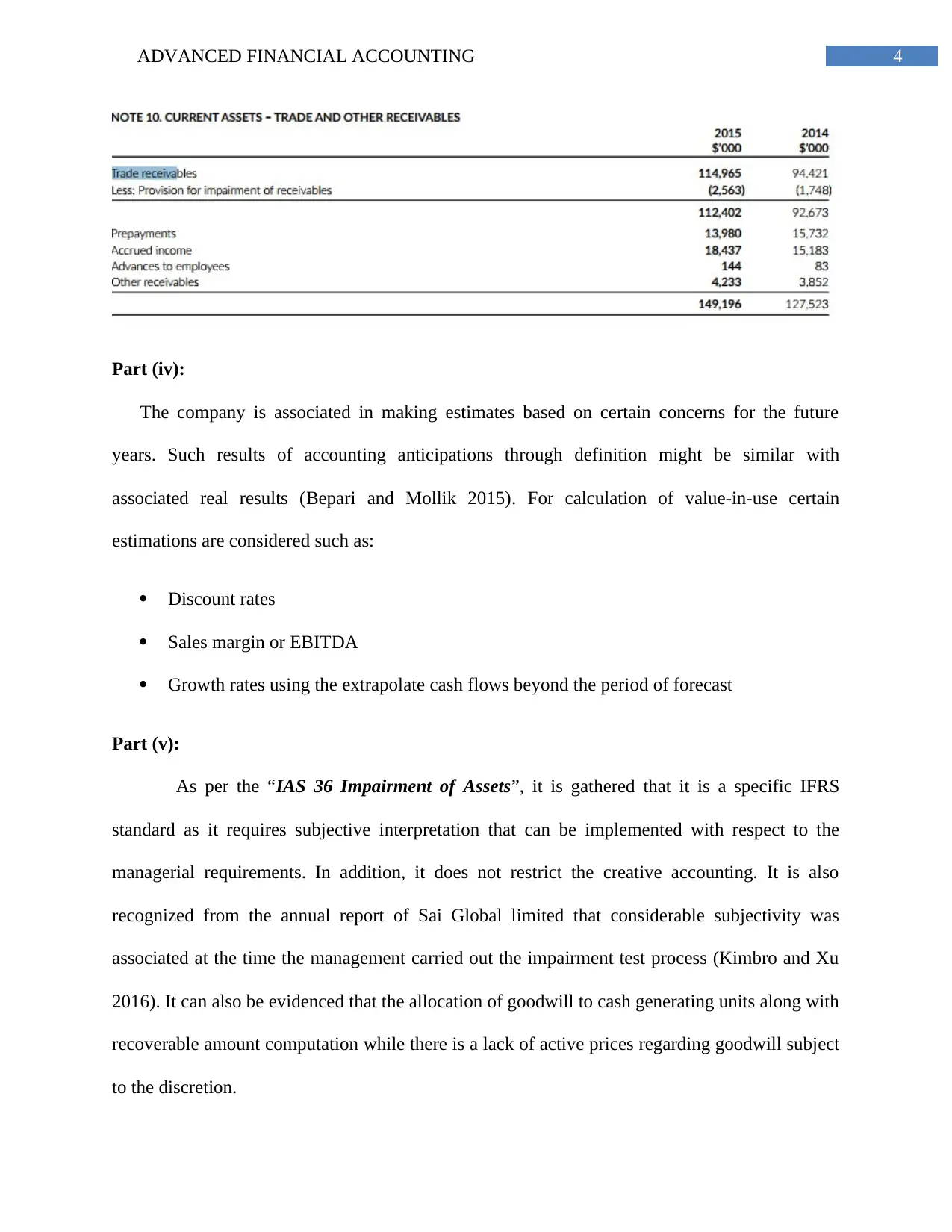

Trade Receivables

In the year 2015, the company represented an allowance for the impairment loss of $

2563 in the year 2015 that was recorded to be $ 1748 in the year 2014.

Part (iii):

The company experienced the below impairment expenditures for the end of the period

on 30th June, 2015.

Goodwill and Intangible Assets

During such period, the company has explained a total impairment of $59841 ($77748 -

$17907), out of which $841 was stated within the software, $ 9000 was mentioned for the

consumer contracts and $ 50000 was mentioned for the IRU. Conversely, goodwill and brands

are not accountable for the impairment (Benson et al. 2015).

Intangible Assets and Goodwill

Trade Receivables

In the year 2015, the company represented an allowance for the impairment loss of $

2563 in the year 2015 that was recorded to be $ 1748 in the year 2014.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ADVANCED FINANCIAL ACCOUNTING

Part (iv):

The company is associated in making estimates based on certain concerns for the future

years. Such results of accounting anticipations through definition might be similar with

associated real results (Bepari and Mollik 2015). For calculation of value-in-use certain

estimations are considered such as:

Discount rates

Sales margin or EBITDA

Growth rates using the extrapolate cash flows beyond the period of forecast

Part (v):

As per the “IAS 36 Impairment of Assets”, it is gathered that it is a specific IFRS

standard as it requires subjective interpretation that can be implemented with respect to the

managerial requirements. In addition, it does not restrict the creative accounting. It is also

recognized from the annual report of Sai Global limited that considerable subjectivity was

associated at the time the management carried out the impairment test process (Kimbro and Xu

2016). It can also be evidenced that the allocation of goodwill to cash generating units along with

recoverable amount computation while there is a lack of active prices regarding goodwill subject

to the discretion.

Part (iv):

The company is associated in making estimates based on certain concerns for the future

years. Such results of accounting anticipations through definition might be similar with

associated real results (Bepari and Mollik 2015). For calculation of value-in-use certain

estimations are considered such as:

Discount rates

Sales margin or EBITDA

Growth rates using the extrapolate cash flows beyond the period of forecast

Part (v):

As per the “IAS 36 Impairment of Assets”, it is gathered that it is a specific IFRS

standard as it requires subjective interpretation that can be implemented with respect to the

managerial requirements. In addition, it does not restrict the creative accounting. It is also

recognized from the annual report of Sai Global limited that considerable subjectivity was

associated at the time the management carried out the impairment test process (Kimbro and Xu

2016). It can also be evidenced that the allocation of goodwill to cash generating units along with

recoverable amount computation while there is a lack of active prices regarding goodwill subject

to the discretion.

5ADVANCED FINANCIAL ACCOUNTING

Part (vi):

After critical analysis, it is gathered that the complex or confessing aspect of impairment

is associated with the impairment indication. Even though such indications just focus on the

internal as well as external signs concerning the assets impairment, the frequency of conducting

such test for goodwill along with intangible assets just focus on the management’s discretion

(Bond, Govendir and Wells 2016). For this reason, there is a chance that the management might

carry out test opportunistically in case there is a difference in value.

Part (vii):

It is elucidated that, impairment loss can be observed as certain variance within an asset’s

recoverable amount along with an assets carrying amount. The recoverable asset is higher than

the fair asset value subtracted from the value-in-use and disposal cost (Dye, Glover and Sunder

2014). Fair value is estimated by the asset within the active market or the sales agreement within

which the asset trading is conducted or accessibility of important information in disclosing

amount at which the company can sell its assets. In contrast, the value-in-use is deemed as

present value related with future cash inflows that are anticipated to be gathered from cost of

goods unit or asset as per IAS 36 (Khokan Bepari, Rahman and Taher Mollik 2014).

Part (viii):

In alignment with the IFRS 113 standard, ascertainment of fair value is conducted through

below points:

Sales agreement

Asset value within active market within the asset trading is conducted

Part (vi):

After critical analysis, it is gathered that the complex or confessing aspect of impairment

is associated with the impairment indication. Even though such indications just focus on the

internal as well as external signs concerning the assets impairment, the frequency of conducting

such test for goodwill along with intangible assets just focus on the management’s discretion

(Bond, Govendir and Wells 2016). For this reason, there is a chance that the management might

carry out test opportunistically in case there is a difference in value.

Part (vii):

It is elucidated that, impairment loss can be observed as certain variance within an asset’s

recoverable amount along with an assets carrying amount. The recoverable asset is higher than

the fair asset value subtracted from the value-in-use and disposal cost (Dye, Glover and Sunder

2014). Fair value is estimated by the asset within the active market or the sales agreement within

which the asset trading is conducted or accessibility of important information in disclosing

amount at which the company can sell its assets. In contrast, the value-in-use is deemed as

present value related with future cash inflows that are anticipated to be gathered from cost of

goods unit or asset as per IAS 36 (Khokan Bepari, Rahman and Taher Mollik 2014).

Part (viii):

In alignment with the IFRS 113 standard, ascertainment of fair value is conducted through

below points:

Sales agreement

Asset value within active market within the asset trading is conducted

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ADVANCED FINANCIAL ACCOUNTING

Existence of quality information for revealing the amount at which the company might

sell its assets

For this reason, the fair value can be elucidated as selling price that is considered on the parts

of both the seller and buyer through anticipating that the parties have conducted a free

transaction. Numerous investments are deemed to have a fair value that is estimated on the

behalf of the market within which trading of security is done (Gimbar, Hansen and Ozlanski

2016). In addition, fair value indicates the asset along with the liabilities value of a company

while the annual report of the subsidiary company remains consolidated with a parent company.

For example, of the shares of a company is trading within an exchange, the players within the

market offers a bid through asking price of that share. In this condition, the investors might

consider selling shares to the leader in the market at a bid price at the time of acquiring the

shares from the market player within the ask price. Therefore it can be inferred that exchange can

serve as the most trusted ascertaining technique regarding shares fair value estimation (Jorissen

et al. 2014).

Part B:

Part (i):

More than 50% of the companies employing IFRS or US GAAP are greatly impacted

because of certain changes within accounting. As per the present status, the companies within

IFRS or US GAAP have leased assets along with societies that amount to around $3.3 million,

out of which more than 85% is not disclosed within the financial position statement as they are

treated as part of operating leases (Mora and Walker 2015). For compensating the same, the

investors are deemed to contain certain projections that are incomparable, inconsistent as well as

Existence of quality information for revealing the amount at which the company might

sell its assets

For this reason, the fair value can be elucidated as selling price that is considered on the parts

of both the seller and buyer through anticipating that the parties have conducted a free

transaction. Numerous investments are deemed to have a fair value that is estimated on the

behalf of the market within which trading of security is done (Gimbar, Hansen and Ozlanski

2016). In addition, fair value indicates the asset along with the liabilities value of a company

while the annual report of the subsidiary company remains consolidated with a parent company.

For example, of the shares of a company is trading within an exchange, the players within the

market offers a bid through asking price of that share. In this condition, the investors might

consider selling shares to the leader in the market at a bid price at the time of acquiring the

shares from the market player within the ask price. Therefore it can be inferred that exchange can

serve as the most trusted ascertaining technique regarding shares fair value estimation (Jorissen

et al. 2014).

Part B:

Part (i):

More than 50% of the companies employing IFRS or US GAAP are greatly impacted

because of certain changes within accounting. As per the present status, the companies within

IFRS or US GAAP have leased assets along with societies that amount to around $3.3 million,

out of which more than 85% is not disclosed within the financial position statement as they are

treated as part of operating leases (Mora and Walker 2015). For compensating the same, the

investors are deemed to contain certain projections that are incomparable, inconsistent as well as

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ADVANCED FINANCIAL ACCOUNTING

inadequate. Therefore, it is evidenced that the previous standard of accounting failed in

explaining the economic actuality.

Part (ii):

In consideration to previous accounting standards, a lot of companies are reported to be

85% of their leases that realizes the amount within the operating leases and it did not signify the

ones mentioned within the company’s financial position statement. Even if the operating leases

are not recorded within the financial position statement there has been certain generation of

actual liabilities (Pacter 2014). While at the time of financial crisis there are certain retail

companies that turned out to be bankrupt as they failed to adjust the updated economic reality in

a better manner. In addition, the company had considerable amount of commitments in

accordance with long term operating leases and their financial position statement is observed to

be lean drastically.

Part (iii):

The previous accounting system is accordance with the lease might result in lack of

comparability. The industry in which the company operates accounts for a great amount of leases

in the operating leases. Along with that the record is not prepared under the financial position

statement of the company (Wen and Moehrle 2015). For this reason, as the company is involved

in leasing all its products that is not identical to its competitors acquiring all its products.

Conversely, the financial obligations of the two types of companies are not that identical. This

also indicates that there is a lack of level playing field within the company. With emergence of a

new standard, all such leases might be responsible for reforming the assets along with lessees

that might record them in the liability form. For this reason, it is anticipated that such type of

issue might get resolved.

inadequate. Therefore, it is evidenced that the previous standard of accounting failed in

explaining the economic actuality.

Part (ii):

In consideration to previous accounting standards, a lot of companies are reported to be

85% of their leases that realizes the amount within the operating leases and it did not signify the

ones mentioned within the company’s financial position statement. Even if the operating leases

are not recorded within the financial position statement there has been certain generation of

actual liabilities (Pacter 2014). While at the time of financial crisis there are certain retail

companies that turned out to be bankrupt as they failed to adjust the updated economic reality in

a better manner. In addition, the company had considerable amount of commitments in

accordance with long term operating leases and their financial position statement is observed to

be lean drastically.

Part (iii):

The previous accounting system is accordance with the lease might result in lack of

comparability. The industry in which the company operates accounts for a great amount of leases

in the operating leases. Along with that the record is not prepared under the financial position

statement of the company (Wen and Moehrle 2015). For this reason, as the company is involved

in leasing all its products that is not identical to its competitors acquiring all its products.

Conversely, the financial obligations of the two types of companies are not that identical. This

also indicates that there is a lack of level playing field within the company. With emergence of a

new standard, all such leases might be responsible for reforming the assets along with lessees

that might record them in the liability form. For this reason, it is anticipated that such type of

issue might get resolved.

8ADVANCED FINANCIAL ACCOUNTING

Part (iv):

Certain changes within accounting standard are likely to have an impact on more than

half of listed organizations and they are deemed to be famous in the companies. The major cause

behind this is that such changes might result in controversies and might lead to warning impacts

in consideration to negative economic situations and expenses associated with the variations

within the system. In addition these alterations might have increased commercial impacts (Yao,

Percy and Hu 2015).

Part (v):

In consideration to new standard of accounting, it is gathered that most of the companies

are treating operating leases as an aspect of off-balance sheet aspects. For this reason, the

investors along with financial statement users do not attain an efficient insight of the company’s

financial situation (Sai Global limited. 2018). This restricts the company in contrasting leasing

assets with the purchasing assets of the company. Moreover, this new standard is anticipated to

update IFRS 16 and this is estimated that it might greatly outweigh the expenses that might result

in highly informed decisions associated with investment. Ii can also be indicated that the lease

against the decisions regarding purchases in a better manner on the behalf of the management.

Part (iv):

Certain changes within accounting standard are likely to have an impact on more than

half of listed organizations and they are deemed to be famous in the companies. The major cause

behind this is that such changes might result in controversies and might lead to warning impacts

in consideration to negative economic situations and expenses associated with the variations

within the system. In addition these alterations might have increased commercial impacts (Yao,

Percy and Hu 2015).

Part (v):

In consideration to new standard of accounting, it is gathered that most of the companies

are treating operating leases as an aspect of off-balance sheet aspects. For this reason, the

investors along with financial statement users do not attain an efficient insight of the company’s

financial situation (Sai Global limited. 2018). This restricts the company in contrasting leasing

assets with the purchasing assets of the company. Moreover, this new standard is anticipated to

update IFRS 16 and this is estimated that it might greatly outweigh the expenses that might result

in highly informed decisions associated with investment. Ii can also be indicated that the lease

against the decisions regarding purchases in a better manner on the behalf of the management.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ADVANCED FINANCIAL ACCOUNTING

References:

Amel-Zadeh, A., Faasse, J., Li, K. and Meeks, G., 2016. Stewardship and Value Relevance in

Accounting for the Depletion of Purchased Goodwill.

Benson, K., Clarkson, P.M., Smith, T. and Tutticci, I., 2015. A review of accounting research in

the Asia Pacific region. Australian Journal of Management, 40(1), pp.36-88.

Bepari, M.K. and Mollik, A.T., 2015. Effect of audit quality and accounting and finance

backgrounds of audit committee members on firms’ compliance with IFRS for goodwill

impairment testing. Journal of Applied Accounting Research, 16(2), pp.196-220.

Bond, D., Govendir, B. and Wells, P., 2016. An evaluation of asset impairments by Australian

firms and whether they were impacted by AASB 136. Accounting & Finance, 56(1), pp.259-288.

Dye, R.A., Glover, J.C. and Sunder, S., 2014. Financial engineering and the arms race between

accounting standard setters and preparers. Accounting Horizons, 29(2), pp.265-295.

Gimbar, C., Hansen, B. and Ozlanski, M.E., 2016. The effects of critical audit matter paragraphs

and accounting standard precision on auditor liability. The Accounting Review, 91(6), pp.1629-

1646.

Jorissen, A., Lybaert, N., Orens, R. and Van Der Tas, L., 2014. Constituents’ Participation in the

IASC/IASB’s due Process of International Accounting Standard Setting: A Longitudinal

Analysis. In Accounting and Regulation (pp. 79-110). Springer New York.

Jorissen, A., Lybaert, N., Orens, R. and Van Der Tas, L., 2014. Corporate participation in the due

process of international accounting standard setting: An analysis of antecedents.

References:

Amel-Zadeh, A., Faasse, J., Li, K. and Meeks, G., 2016. Stewardship and Value Relevance in

Accounting for the Depletion of Purchased Goodwill.

Benson, K., Clarkson, P.M., Smith, T. and Tutticci, I., 2015. A review of accounting research in

the Asia Pacific region. Australian Journal of Management, 40(1), pp.36-88.

Bepari, M.K. and Mollik, A.T., 2015. Effect of audit quality and accounting and finance

backgrounds of audit committee members on firms’ compliance with IFRS for goodwill

impairment testing. Journal of Applied Accounting Research, 16(2), pp.196-220.

Bond, D., Govendir, B. and Wells, P., 2016. An evaluation of asset impairments by Australian

firms and whether they were impacted by AASB 136. Accounting & Finance, 56(1), pp.259-288.

Dye, R.A., Glover, J.C. and Sunder, S., 2014. Financial engineering and the arms race between

accounting standard setters and preparers. Accounting Horizons, 29(2), pp.265-295.

Gimbar, C., Hansen, B. and Ozlanski, M.E., 2016. The effects of critical audit matter paragraphs

and accounting standard precision on auditor liability. The Accounting Review, 91(6), pp.1629-

1646.

Jorissen, A., Lybaert, N., Orens, R. and Van Der Tas, L., 2014. Constituents’ Participation in the

IASC/IASB’s due Process of International Accounting Standard Setting: A Longitudinal

Analysis. In Accounting and Regulation (pp. 79-110). Springer New York.

Jorissen, A., Lybaert, N., Orens, R. and Van Der Tas, L., 2014. Corporate participation in the due

process of international accounting standard setting: An analysis of antecedents.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ADVANCED FINANCIAL ACCOUNTING

Khokan Bepari, M., F. Rahman, S. and Taher Mollik, A., 2014. Firms' compliance with the

disclosure requirements of IFRS for goodwill impairment testing: Effect of the global financial

crisis and other firm characteristics. Journal of Accounting & Organizational Change, 10(1),

pp.116-149.

Kimbro, M.B. and Xu, D., 2016. The accounting treatment of goodwill, idiosyncratic risk, and

market pricing. Journal of Accounting, Auditing & Finance, 31(3), pp.365-387.

M Carlin, T., Finch, N. and Manh Tran, D., 2014. IFRS compliance in the year of the pig: Hong

Kong impairment testing. Journal of Economics and Development, 16(1), p.23.

Mora, A. and Walker, M., 2015. The implications of research on accounting conservatism for

accounting standard setting. Accounting and Business Research, 45(5), pp.620-650.

Pacter, P., 2014. Global accounting standards-from vision to reality. The CPA Journal, 84(1),

p.6.

Sai Global limited., 2018. [online] Available at: http:// Sai Global

limited.au/investor-centre/reports-presentations-and-resources/annual-reports/ [Accessed 9 Jan.

2018].

Wen, H.J. and Moehrle, S.R., 2015. Accounting for goodwill: A literature review and analysis.

Yao, D.F.T., Percy, M. and Hu, F., 2015. Fair value accounting for non-current assets and audit

fees: Evidence from Australian companies. Journal of Contemporary Accounting &

Economics, 11(1), pp.31-45.

Khokan Bepari, M., F. Rahman, S. and Taher Mollik, A., 2014. Firms' compliance with the

disclosure requirements of IFRS for goodwill impairment testing: Effect of the global financial

crisis and other firm characteristics. Journal of Accounting & Organizational Change, 10(1),

pp.116-149.

Kimbro, M.B. and Xu, D., 2016. The accounting treatment of goodwill, idiosyncratic risk, and

market pricing. Journal of Accounting, Auditing & Finance, 31(3), pp.365-387.

M Carlin, T., Finch, N. and Manh Tran, D., 2014. IFRS compliance in the year of the pig: Hong

Kong impairment testing. Journal of Economics and Development, 16(1), p.23.

Mora, A. and Walker, M., 2015. The implications of research on accounting conservatism for

accounting standard setting. Accounting and Business Research, 45(5), pp.620-650.

Pacter, P., 2014. Global accounting standards-from vision to reality. The CPA Journal, 84(1),

p.6.

Sai Global limited., 2018. [online] Available at: http:// Sai Global

limited.au/investor-centre/reports-presentations-and-resources/annual-reports/ [Accessed 9 Jan.

2018].

Wen, H.J. and Moehrle, S.R., 2015. Accounting for goodwill: A literature review and analysis.

Yao, D.F.T., Percy, M. and Hu, F., 2015. Fair value accounting for non-current assets and audit

fees: Evidence from Australian companies. Journal of Contemporary Accounting &

Economics, 11(1), pp.31-45.

11ADVANCED FINANCIAL ACCOUNTING

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.