Advanced Financial Accounting Report: Framework and Reporting

VerifiedAdded on 2022/10/19

|16

|3859

|116

Report

AI Summary

This report provides a detailed analysis of financial accounting, focusing on the conceptual framework for financial reporting and the application of integrated and sustainability reporting. It examines the history and concerns surrounding the IASB's conceptual framework, including issues raised by the AASB and academics. The report analyzes Caltex Australia's 2018 annual report, highlighting the application of the conceptual framework, including the recognition principles, measurement bases, and qualitative characteristics. Furthermore, the report compares and contrasts the Global Reporting Initiative (GRI) and the International Integrated Reporting Council (IIRC), explores the limitations of conventional accounting, and discusses the application of theories to explain the content of sustainability and integrated reports. It includes an examination of elements within the Nedbank Limited 2017 report and aspects of the Banks of Queensland's (BOQ) 2018 sustainability report, concluding with a comparison of the two reports.

Financial Accounting 1

Advanced Financial Accounting by Student Name

Student Number

Class & Course Code

Trimester Number

Professor

University

The City & State

Date

Advanced Financial Accounting by Student Name

Student Number

Class & Course Code

Trimester Number

Professor

University

The City & State

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Accounting 2

Executive Summary

Business entities are guided by conceptual frameworks when preparing their financial reports and

statements. Likewise, the changing trends in financial reporting have seen the stakeholders

changing their focus on the items to be included in financial reports. Companies are now

focussing on creating value by forming a positive relationship with their stakeholders. The

increasing need to include non-financial performance in the financial statements have led to the

creation of sustainability reporting as well as integrated reporting. This report exams the two

important components of accounting, that is, the conceptual framework and integrated and

sustainability reporting. Key elements of the two pillars of accounting have been exhausted. The

findings show that although the Australian Accounting Standards Board (AASB) fully support

the IASB's conceptual framework, several issues need to be addressed as listed in the paper.

Likewise, the application of integrated and sustainability reporting at the expense of conventional

financial reporting is slowly gaining momentum.

Executive Summary

Business entities are guided by conceptual frameworks when preparing their financial reports and

statements. Likewise, the changing trends in financial reporting have seen the stakeholders

changing their focus on the items to be included in financial reports. Companies are now

focussing on creating value by forming a positive relationship with their stakeholders. The

increasing need to include non-financial performance in the financial statements have led to the

creation of sustainability reporting as well as integrated reporting. This report exams the two

important components of accounting, that is, the conceptual framework and integrated and

sustainability reporting. Key elements of the two pillars of accounting have been exhausted. The

findings show that although the Australian Accounting Standards Board (AASB) fully support

the IASB's conceptual framework, several issues need to be addressed as listed in the paper.

Likewise, the application of integrated and sustainability reporting at the expense of conventional

financial reporting is slowly gaining momentum.

Financial Accounting 3

Introduction

The report examines the application of the conceptual framework for financial reporting as well

as integral/ sustainability reporting by the Australian and South African firms. The paper is

divided into two parts. Part A examines the development, issues surrounding, and application of

the conceptual framework. This part is further divided into several sections. The introductory

section examines the history of IASB’s conceptual framework. The second and third sections

discuss the concerns raised by the AASB and academicians in relations to the application of the

conceptual framework for, respectively. The last section examines elements of the conceptual

framework and how Caltex Australia applied the conceptual framework in its 2018 annual report.

Part B examines the issues surrounding integrated reporting and sustainability reporting. This

part is further divided into five sections. Section one compares and contrasts the Global

Reporting Initiative (GRI) sustainability reporting, and the International Integrated Reporting

Council (IIRC) integrated reporting. Section two examines the limitation of conventional

accounting to support sustainability or integrated reporting. Section three discusses the

application of theories to explain the contents of sustainability and integrated reports. Section

four examines the elements of an integrated report contained in the Nedbank Limited 2017 report.

Section five discusses the aspects of Banks of Queensland's (BOQ) 2018 sustainability report.

The last part compares the reports by Nedbank and BOQ.

PART A

a) The history of the Conceptual Framework for Financial Reporting

The conceptual framework for financial reporting addresses the conceptual and theoretical issues

that influence financial reporting. The framework seeks to provide a consistent and coherent

Introduction

The report examines the application of the conceptual framework for financial reporting as well

as integral/ sustainability reporting by the Australian and South African firms. The paper is

divided into two parts. Part A examines the development, issues surrounding, and application of

the conceptual framework. This part is further divided into several sections. The introductory

section examines the history of IASB’s conceptual framework. The second and third sections

discuss the concerns raised by the AASB and academicians in relations to the application of the

conceptual framework for, respectively. The last section examines elements of the conceptual

framework and how Caltex Australia applied the conceptual framework in its 2018 annual report.

Part B examines the issues surrounding integrated reporting and sustainability reporting. This

part is further divided into five sections. Section one compares and contrasts the Global

Reporting Initiative (GRI) sustainability reporting, and the International Integrated Reporting

Council (IIRC) integrated reporting. Section two examines the limitation of conventional

accounting to support sustainability or integrated reporting. Section three discusses the

application of theories to explain the contents of sustainability and integrated reports. Section

four examines the elements of an integrated report contained in the Nedbank Limited 2017 report.

Section five discusses the aspects of Banks of Queensland's (BOQ) 2018 sustainability report.

The last part compares the reports by Nedbank and BOQ.

PART A

a) The history of the Conceptual Framework for Financial Reporting

The conceptual framework for financial reporting addresses the conceptual and theoretical issues

that influence financial reporting. The framework seeks to provide a consistent and coherent

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Accounting 4

foundation for developing accounting principles and standards. The development of a conceptual

framework for financial reporting began at different dates in the US, the UK, and globally. The

globally recognised conceptual frameworks for financial reporting were developed by the

International Accounting Standards Board (IASB) (IASB, 2018).

The FASB was established in 1973 in the U.S. to replace the Accounting Principles Board

(APB). FASB began the process of developing its conceptual framework in 1973. The board

released its eight frameworks between 1978 and 2010. The conceptual framework for conceptual

reporting no. 8 was approved and released in 2010 to replace the SFAC nos. 1 and 2

(International Accounting Standards Board, 2018).

The UK's Accounting Standards Board initiated the process of developing its conceptual

framework for financial reporting in 1991. However, the collection of views and recommendation

began in the 1940s. The final concept was released in 2010. Likewise, IASB approved the IFRS'

conceptual frameworks in 2010. The concept has undergone several revisions since then. In 2013,

the revisions of the concept began. Comment period ran between 2013 and 2015 before the board

incorporated the amendments of IFRS 3 in the concept in 2018 (IASB, 2018).

b) The Australian accounting profession’s concerns regarding the Conceptual Framework

The AASB and other accounting professions raised several concerns with the IASB's conceptual

frameworks. The board believes that the IASB's conceptual framework exposure draft cannot be

considered to be up to date, complete and clear to form the basis of developing accounting

standards. The board noted that some sections of the exposure draft laid the foundation for

developing concepts in the future instead of addressing the current accounting issues (Delloite,

2018).

foundation for developing accounting principles and standards. The development of a conceptual

framework for financial reporting began at different dates in the US, the UK, and globally. The

globally recognised conceptual frameworks for financial reporting were developed by the

International Accounting Standards Board (IASB) (IASB, 2018).

The FASB was established in 1973 in the U.S. to replace the Accounting Principles Board

(APB). FASB began the process of developing its conceptual framework in 1973. The board

released its eight frameworks between 1978 and 2010. The conceptual framework for conceptual

reporting no. 8 was approved and released in 2010 to replace the SFAC nos. 1 and 2

(International Accounting Standards Board, 2018).

The UK's Accounting Standards Board initiated the process of developing its conceptual

framework for financial reporting in 1991. However, the collection of views and recommendation

began in the 1940s. The final concept was released in 2010. Likewise, IASB approved the IFRS'

conceptual frameworks in 2010. The concept has undergone several revisions since then. In 2013,

the revisions of the concept began. Comment period ran between 2013 and 2015 before the board

incorporated the amendments of IFRS 3 in the concept in 2018 (IASB, 2018).

b) The Australian accounting profession’s concerns regarding the Conceptual Framework

The AASB and other accounting professions raised several concerns with the IASB's conceptual

frameworks. The board believes that the IASB's conceptual framework exposure draft cannot be

considered to be up to date, complete and clear to form the basis of developing accounting

standards. The board noted that some sections of the exposure draft laid the foundation for

developing concepts in the future instead of addressing the current accounting issues (Delloite,

2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Accounting 5

The board believed that the conceptual framework could not be relied upon to effectively address

the ever-changing needs of financial reporting at its current start. For example, the conceptual

framework failed to provide a clear distinction in the definitions of profit and loss statement and

the other comprehensive income (OCI). The board proposed that it was essential to give a clarity

between the two accounting statements. A clear definition of the two statements would help

preparers of financial reports to different items that need to appear in either of them (IASB,

2018).

c) The academics’ concerns about the quality of the Conceptual Framework

Australia has adopted the IASB's conceptual framework. Amid numerous benefits, the

framework has received criticism from the Australian accounting professions. First, the process

of developing a conceptual framework has been linked to the process of developing the

constitutions, which is subject to political interference. In other words, the conceptual framework

is a product of a political process where contributors sought to advance their self-interests.

Second, the conceptual framework loses its objectivity when addressing measurement issues

which attract a high level of disagreement. Based on this point, the framework has been criticised

for its failure to address difficult accounting/ financial issues (IASB, 2018).

Third, the conceptual framework focuses more on the financial (economic) performance of

business entities. For instance, the conceptual framework ignores the environmental and social

performance of an entity if the reports. Ignoring the non-financial corporate performance make

the conceptual framework less objective (IASB, 2018).

d) The application of the conceptual framework by Caltex Australia (ASX: CTX).

This section is discussed based on Caltex Australia’s 2018 annual report.

The board believed that the conceptual framework could not be relied upon to effectively address

the ever-changing needs of financial reporting at its current start. For example, the conceptual

framework failed to provide a clear distinction in the definitions of profit and loss statement and

the other comprehensive income (OCI). The board proposed that it was essential to give a clarity

between the two accounting statements. A clear definition of the two statements would help

preparers of financial reports to different items that need to appear in either of them (IASB,

2018).

c) The academics’ concerns about the quality of the Conceptual Framework

Australia has adopted the IASB's conceptual framework. Amid numerous benefits, the

framework has received criticism from the Australian accounting professions. First, the process

of developing a conceptual framework has been linked to the process of developing the

constitutions, which is subject to political interference. In other words, the conceptual framework

is a product of a political process where contributors sought to advance their self-interests.

Second, the conceptual framework loses its objectivity when addressing measurement issues

which attract a high level of disagreement. Based on this point, the framework has been criticised

for its failure to address difficult accounting/ financial issues (IASB, 2018).

Third, the conceptual framework focuses more on the financial (economic) performance of

business entities. For instance, the conceptual framework ignores the environmental and social

performance of an entity if the reports. Ignoring the non-financial corporate performance make

the conceptual framework less objective (IASB, 2018).

d) The application of the conceptual framework by Caltex Australia (ASX: CTX).

This section is discussed based on Caltex Australia’s 2018 annual report.

Financial Accounting 6

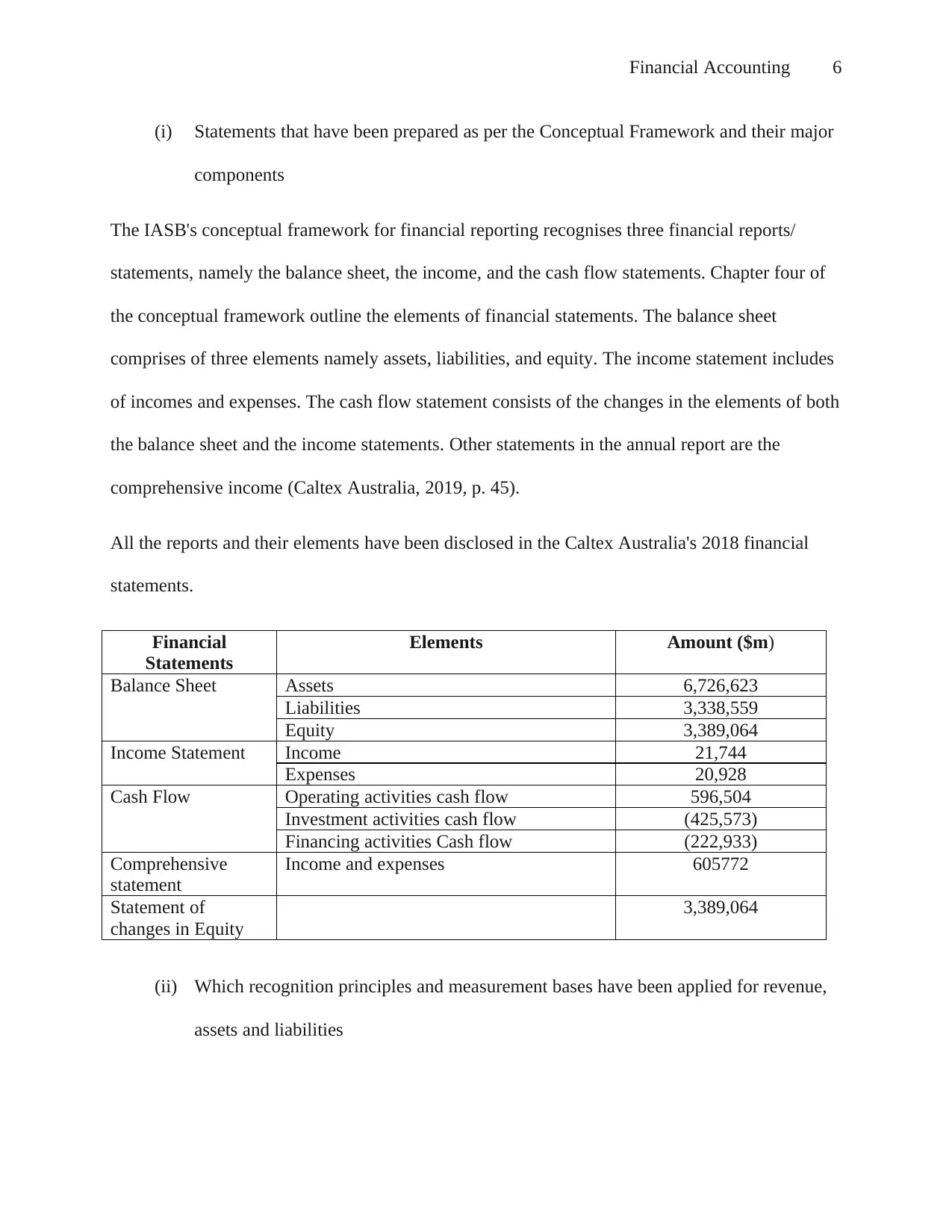

(i) Statements that have been prepared as per the Conceptual Framework and their major

components

The IASB's conceptual framework for financial reporting recognises three financial reports/

statements, namely the balance sheet, the income, and the cash flow statements. Chapter four of

the conceptual framework outline the elements of financial statements. The balance sheet

comprises of three elements namely assets, liabilities, and equity. The income statement includes

of incomes and expenses. The cash flow statement consists of the changes in the elements of both

the balance sheet and the income statements. Other statements in the annual report are the

comprehensive income (Caltex Australia, 2019, p. 45).

All the reports and their elements have been disclosed in the Caltex Australia's 2018 financial

statements.

Financial

Statements

Elements Amount ($m)

Balance Sheet Assets 6,726,623

Liabilities 3,338,559

Equity 3,389,064

Income Statement Income 21,744

Expenses 20,928

Cash Flow Operating activities cash flow 596,504

Investment activities cash flow (425,573)

Financing activities Cash flow (222,933)

Comprehensive

statement

Income and expenses 605772

Statement of

changes in Equity

3,389,064

(ii) Which recognition principles and measurement bases have been applied for revenue,

assets and liabilities

(i) Statements that have been prepared as per the Conceptual Framework and their major

components

The IASB's conceptual framework for financial reporting recognises three financial reports/

statements, namely the balance sheet, the income, and the cash flow statements. Chapter four of

the conceptual framework outline the elements of financial statements. The balance sheet

comprises of three elements namely assets, liabilities, and equity. The income statement includes

of incomes and expenses. The cash flow statement consists of the changes in the elements of both

the balance sheet and the income statements. Other statements in the annual report are the

comprehensive income (Caltex Australia, 2019, p. 45).

All the reports and their elements have been disclosed in the Caltex Australia's 2018 financial

statements.

Financial

Statements

Elements Amount ($m)

Balance Sheet Assets 6,726,623

Liabilities 3,338,559

Equity 3,389,064

Income Statement Income 21,744

Expenses 20,928

Cash Flow Operating activities cash flow 596,504

Investment activities cash flow (425,573)

Financing activities Cash flow (222,933)

Comprehensive

statement

Income and expenses 605772

Statement of

changes in Equity

3,389,064

(ii) Which recognition principles and measurement bases have been applied for revenue,

assets and liabilities

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Accounting 7

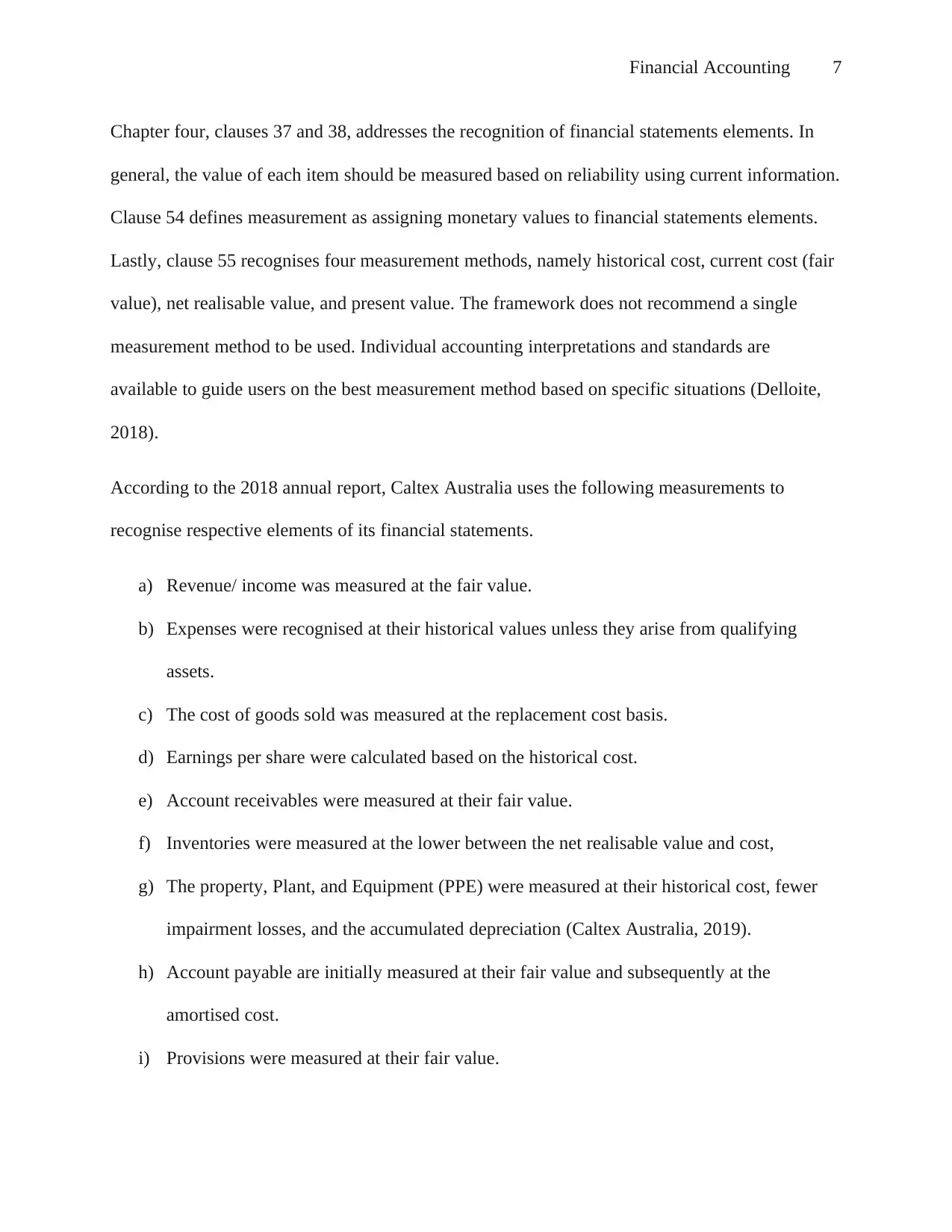

Chapter four, clauses 37 and 38, addresses the recognition of financial statements elements. In

general, the value of each item should be measured based on reliability using current information.

Clause 54 defines measurement as assigning monetary values to financial statements elements.

Lastly, clause 55 recognises four measurement methods, namely historical cost, current cost (fair

value), net realisable value, and present value. The framework does not recommend a single

measurement method to be used. Individual accounting interpretations and standards are

available to guide users on the best measurement method based on specific situations (Delloite,

2018).

According to the 2018 annual report, Caltex Australia uses the following measurements to

recognise respective elements of its financial statements.

a) Revenue/ income was measured at the fair value.

b) Expenses were recognised at their historical values unless they arise from qualifying

assets.

c) The cost of goods sold was measured at the replacement cost basis.

d) Earnings per share were calculated based on the historical cost.

e) Account receivables were measured at their fair value.

f) Inventories were measured at the lower between the net realisable value and cost,

g) The property, Plant, and Equipment (PPE) were measured at their historical cost, fewer

impairment losses, and the accumulated depreciation (Caltex Australia, 2019).

h) Account payable are initially measured at their fair value and subsequently at the

amortised cost.

i) Provisions were measured at their fair value.

Chapter four, clauses 37 and 38, addresses the recognition of financial statements elements. In

general, the value of each item should be measured based on reliability using current information.

Clause 54 defines measurement as assigning monetary values to financial statements elements.

Lastly, clause 55 recognises four measurement methods, namely historical cost, current cost (fair

value), net realisable value, and present value. The framework does not recommend a single

measurement method to be used. Individual accounting interpretations and standards are

available to guide users on the best measurement method based on specific situations (Delloite,

2018).

According to the 2018 annual report, Caltex Australia uses the following measurements to

recognise respective elements of its financial statements.

a) Revenue/ income was measured at the fair value.

b) Expenses were recognised at their historical values unless they arise from qualifying

assets.

c) The cost of goods sold was measured at the replacement cost basis.

d) Earnings per share were calculated based on the historical cost.

e) Account receivables were measured at their fair value.

f) Inventories were measured at the lower between the net realisable value and cost,

g) The property, Plant, and Equipment (PPE) were measured at their historical cost, fewer

impairment losses, and the accumulated depreciation (Caltex Australia, 2019).

h) Account payable are initially measured at their fair value and subsequently at the

amortised cost.

i) Provisions were measured at their fair value.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Accounting 8

j) Interest-bearing liabilities were initially measured at their fair value and subsequently at

their amortised cost.

k) The share capital was measured at its fair value.

(iii) What qualitative characteristics of information exhibit in Caltex’s financial reports

According to the IASB's conceptual framework, relevance and faithful representation are key

qualitative characteristics of financial information. An entity's stakeholder entrusts auditors to

establish whether financial information disclosures relevant, true, and faithful representation of

an entity (Caltex Australia, 2019, p. 39).

Caltex Australia's financial reports were audited by KMPG. According to the audited report, the

information gave the true and fair view of Caltex Australia's financial position. Moreover, the

company had complied with the requirements of the Corporations Regulations 2001 and

Australian Accounting Standards. Lastly, the company had complied with International Financial

Reporting Standards (IFRS), which stipulates that financial information should relevant and

demonstrate the faithful representation of financial position (Caltex Australia, 2019, p. 40);

(Epstein, 2018, p. 163).

PART B

a) Comparison of Sustainability Reporting Guidelines and International Integrated Reporting

Framework

Companies and their executives are investing more time and resources to promote sustainable

practices. Both the Global Reporting Initiative (GRI) and the International Integrated Reporting

Council (IIRC) seek to encourage globally accepted sustainable financial reporting. GRI has been

j) Interest-bearing liabilities were initially measured at their fair value and subsequently at

their amortised cost.

k) The share capital was measured at its fair value.

(iii) What qualitative characteristics of information exhibit in Caltex’s financial reports

According to the IASB's conceptual framework, relevance and faithful representation are key

qualitative characteristics of financial information. An entity's stakeholder entrusts auditors to

establish whether financial information disclosures relevant, true, and faithful representation of

an entity (Caltex Australia, 2019, p. 39).

Caltex Australia's financial reports were audited by KMPG. According to the audited report, the

information gave the true and fair view of Caltex Australia's financial position. Moreover, the

company had complied with the requirements of the Corporations Regulations 2001 and

Australian Accounting Standards. Lastly, the company had complied with International Financial

Reporting Standards (IFRS), which stipulates that financial information should relevant and

demonstrate the faithful representation of financial position (Caltex Australia, 2019, p. 40);

(Epstein, 2018, p. 163).

PART B

a) Comparison of Sustainability Reporting Guidelines and International Integrated Reporting

Framework

Companies and their executives are investing more time and resources to promote sustainable

practices. Both the Global Reporting Initiative (GRI) and the International Integrated Reporting

Council (IIRC) seek to encourage globally accepted sustainable financial reporting. GRI has been

Financial Accounting 9

pushing organisations to adopt sustainable reporting. The organisation aims to develop a

sustainability reporting where business entities include the economic, social, governance, and

environmental performance in their annual reports. GRI believes that adoption of sustainability

reporting standards will push business entities to contribute more to an effective and efficient

global economy (Deegan, 2012, p. 771).

Likewise, the International Integrated Reporting Council (IIRC) push for an integrated format for

a globally accepted framework for accounting. The integrated format incorporates financial,

social, governance, and environmental information. Therefore, GRI pushes for sustainability

financial reporting, while IIRC supports an integrated format of financial reporting (Camilleri,

2018).

IIRC and GRI work together regularly because of their shared missions and objectives. Through

the strategic partnership, the two organisations seek to promote the inclusion of non-financial

corporate performance indicators in financial reporting. They aim to enhance comparability, the

consistency as a way of fostering sustainable corporate practices. IIRC has a broader objective

because it incorporates sustainability reporting in its integrated format for reporting (Deloitte,

2018).

b) Rigour of the conventional accounting, based upon the Conceptual Framework for

contents of sustainability as well as integrated reports

Conventional (traditional) accounting method focuses on the financial aspect of corporate

performance. Traditionally stakeholders were more interested in the financial performance.

Considering the current environmental, social, and governance issues, stakeholders seek financial

reports that are inclusive of the financial and non-financial aspects of performance. The

pushing organisations to adopt sustainable reporting. The organisation aims to develop a

sustainability reporting where business entities include the economic, social, governance, and

environmental performance in their annual reports. GRI believes that adoption of sustainability

reporting standards will push business entities to contribute more to an effective and efficient

global economy (Deegan, 2012, p. 771).

Likewise, the International Integrated Reporting Council (IIRC) push for an integrated format for

a globally accepted framework for accounting. The integrated format incorporates financial,

social, governance, and environmental information. Therefore, GRI pushes for sustainability

financial reporting, while IIRC supports an integrated format of financial reporting (Camilleri,

2018).

IIRC and GRI work together regularly because of their shared missions and objectives. Through

the strategic partnership, the two organisations seek to promote the inclusion of non-financial

corporate performance indicators in financial reporting. They aim to enhance comparability, the

consistency as a way of fostering sustainable corporate practices. IIRC has a broader objective

because it incorporates sustainability reporting in its integrated format for reporting (Deloitte,

2018).

b) Rigour of the conventional accounting, based upon the Conceptual Framework for

contents of sustainability as well as integrated reports

Conventional (traditional) accounting method focuses on the financial aspect of corporate

performance. Traditionally stakeholders were more interested in the financial performance.

Considering the current environmental, social, and governance issues, stakeholders seek financial

reports that are inclusive of the financial and non-financial aspects of performance. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Accounting 10

conventional accounting method cannot support sustainability and integrated accounting

reporting approaches (Brockett, 2012, p. 81]).

Likewise, the conceptual framework for financial reporting is guided by the qualitative

characteristics of relevance and faithful representation. Today companies are acknowledging the

impact their parties bring to the society and the environment. Subsequently, the corporates invest

significant resources and time to protect society and the environment by promoting sustainable

practices. In most cases, such decisions have a significant influence on corporate governance and

image. However, the impact of non-financial investments cannot be captured in the financial

reports because of the limitation of conventional accounting method. Therefore, it's time to adopt

sustainability and integrated financial reporting methods (Villiers, 2017, p. 112).

c) Applicability (usefulness or limitations) of the theories to explain contents of

sustainability as well as integrated reports

Two theories can be used to describe the applicability of the materials of sustainability and

integrated reporting. The stewardship theory is based on organisational behaviour that drives

intrinsic values and doing best to the society. The theory stipulates that higher value is created

through cooperation and not defection. The stewards (managers) maximise shareholders' wealth

by satisfying the needs of other stakeholder groups. Previously, financial reports lacked social

and environmental elements. Organisations focussed more on maximising wealth and avoiding

expenses which failed to present an accurate and fair position of entities. Therefore, the adoption

of sustainability and integrated reporting will improve an accurate and fair presentation of

business entities (Loftus, 2015, p. 500).

conventional accounting method cannot support sustainability and integrated accounting

reporting approaches (Brockett, 2012, p. 81]).

Likewise, the conceptual framework for financial reporting is guided by the qualitative

characteristics of relevance and faithful representation. Today companies are acknowledging the

impact their parties bring to the society and the environment. Subsequently, the corporates invest

significant resources and time to protect society and the environment by promoting sustainable

practices. In most cases, such decisions have a significant influence on corporate governance and

image. However, the impact of non-financial investments cannot be captured in the financial

reports because of the limitation of conventional accounting method. Therefore, it's time to adopt

sustainability and integrated financial reporting methods (Villiers, 2017, p. 112).

c) Applicability (usefulness or limitations) of the theories to explain contents of

sustainability as well as integrated reports

Two theories can be used to describe the applicability of the materials of sustainability and

integrated reporting. The stewardship theory is based on organisational behaviour that drives

intrinsic values and doing best to the society. The theory stipulates that higher value is created

through cooperation and not defection. The stewards (managers) maximise shareholders' wealth

by satisfying the needs of other stakeholder groups. Previously, financial reports lacked social

and environmental elements. Organisations focussed more on maximising wealth and avoiding

expenses which failed to present an accurate and fair position of entities. Therefore, the adoption

of sustainability and integrated reporting will improve an accurate and fair presentation of

business entities (Loftus, 2015, p. 500).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Accounting 11

The institutional theory clarifies how organisations address social and environmental issues.

According to the theory, firms should positively impact stakeholders. Key stakeholders under the

stakeholder theory are the government, NGOs, the industry, and society. Therefore, firms should

voluntary engage in CSR initiatives which should be presented in the financial reports (Deegan,

2012, p. 213).

d) Integrated Report

i) Components (criteria) of an integrated report

The table below presents the key components of an integrated report

Components Explanation

1 External environment

and organizational

overview

Describes the primary activities of the firm as well as the

environment which the firm operates.

2 Governance Governance describes a company’s governance structure. The

structure shows the company’s ability to supports value creation in

the short, medium and long run.

3 Stakeholder

relationships

The element identifies the stakeholders of a firm and the nature of

their relationship with the company

4 Capital Discusses the necessary resources required to implement CSR

initiatives and create value.

5 Business model Describes the firm’s business model, which includes elements

such as input, activities, outputs, and outcomes.

6 Performance Explains the achievements of the company in line with its strategic

objectives.

7 Internal controls,

risks and

opportunities

This component of an integrated report describes the opportunities

and risks associated with value creation. It also discusses the

internal control mechanisms to counter such risks.

ii) Elements of the integrated report in the Nedbank Group Limited

The IIRC framework prepared Nedbank's 2017 integrated report. The report focused on provides

the stakeholders with a clear picture of the company's creation of sustainable value. The

integrated report comprises of critical components such as capitals, financial elements,

The institutional theory clarifies how organisations address social and environmental issues.

According to the theory, firms should positively impact stakeholders. Key stakeholders under the

stakeholder theory are the government, NGOs, the industry, and society. Therefore, firms should

voluntary engage in CSR initiatives which should be presented in the financial reports (Deegan,

2012, p. 213).

d) Integrated Report

i) Components (criteria) of an integrated report

The table below presents the key components of an integrated report

Components Explanation

1 External environment

and organizational

overview

Describes the primary activities of the firm as well as the

environment which the firm operates.

2 Governance Governance describes a company’s governance structure. The

structure shows the company’s ability to supports value creation in

the short, medium and long run.

3 Stakeholder

relationships

The element identifies the stakeholders of a firm and the nature of

their relationship with the company

4 Capital Discusses the necessary resources required to implement CSR

initiatives and create value.

5 Business model Describes the firm’s business model, which includes elements

such as input, activities, outputs, and outcomes.

6 Performance Explains the achievements of the company in line with its strategic

objectives.

7 Internal controls,

risks and

opportunities

This component of an integrated report describes the opportunities

and risks associated with value creation. It also discusses the

internal control mechanisms to counter such risks.

ii) Elements of the integrated report in the Nedbank Group Limited

The IIRC framework prepared Nedbank's 2017 integrated report. The report focused on provides

the stakeholders with a clear picture of the company's creation of sustainable value. The

integrated report comprises of critical components such as capitals, financial elements,

Financial Accounting 12

intellectual, human factor, social and relationships, business processes and structure, business

activities and their impact on natural resources, strategic focus areas, and stakeholders. For

instance, Nedbank's stakeholders are listed as the staff, shareholders, society, clients, and

regulators (Nedbank Group Limited, 2018, p. 43).

e) Bank of Queensland (BOQ) Limited 2018 sustainability report

Bank of Queensland Limited's 2018 sustainability report is based on five factors, namely

customers, community, governance, environment and people and culture. The company's

governance approach is to create value by using effective corporate governance and risk

management methods that promote the integrity of the operations. The environmental approach

focus on creating value by identifying the method of reducing the environmental impact of

operations. The community approach focus on creating value by contributing to the community's

wellbeing through donation programs and volunteering initiatives. The people and culture

approach seeks to create value by promoting social equality and justice (Bank of Queensland,

2019, p. 21).

BOQ engage in social justice and equality in several ways. One, the bank promotes employee

engagement by checking on them frequently. Two, BOQ has developed a diversified workforce

which provides benefits to the shareholders, customers, and society. Three, the banks have

created flexible work arrangements for its employees. BOQ sought to develop a productive and

satisfied workforce based on a positive work-life balance approach. The report also outlines the

respective relationships between BOQ and its stakeholders. Some of the listed stakeholders are

customers, shareholders, employees, regulators, government, Non-Government Organizations,

Suppliers, and community (Bank of Queensland, 2019, p. 66).

intellectual, human factor, social and relationships, business processes and structure, business

activities and their impact on natural resources, strategic focus areas, and stakeholders. For

instance, Nedbank's stakeholders are listed as the staff, shareholders, society, clients, and

regulators (Nedbank Group Limited, 2018, p. 43).

e) Bank of Queensland (BOQ) Limited 2018 sustainability report

Bank of Queensland Limited's 2018 sustainability report is based on five factors, namely

customers, community, governance, environment and people and culture. The company's

governance approach is to create value by using effective corporate governance and risk

management methods that promote the integrity of the operations. The environmental approach

focus on creating value by identifying the method of reducing the environmental impact of

operations. The community approach focus on creating value by contributing to the community's

wellbeing through donation programs and volunteering initiatives. The people and culture

approach seeks to create value by promoting social equality and justice (Bank of Queensland,

2019, p. 21).

BOQ engage in social justice and equality in several ways. One, the bank promotes employee

engagement by checking on them frequently. Two, BOQ has developed a diversified workforce

which provides benefits to the shareholders, customers, and society. Three, the banks have

created flexible work arrangements for its employees. BOQ sought to develop a productive and

satisfied workforce based on a positive work-life balance approach. The report also outlines the

respective relationships between BOQ and its stakeholders. Some of the listed stakeholders are

customers, shareholders, employees, regulators, government, Non-Government Organizations,

Suppliers, and community (Bank of Queensland, 2019, p. 66).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.