Advanced Financial Accounting: Westpac Annual Report Analysis

VerifiedAdded on 2022/11/17

|11

|3387

|371

Report

AI Summary

This report provides a comprehensive analysis of the accounting practices of Westpac Banking Corporation, focusing on its 2017-2018 annual report. It identifies and describes the accounting concepts applied by Westpac, such as conservatism, accrual, going concern, and matching principles, referencing specific examples from the annual report. The report also examines the changes introduced by AASB 16 regarding leases, discussing the implications for Westpac and the impact on its financial statements, including the recognition of lease assets and liabilities. Furthermore, the report summarizes the key disclosures made by Westpac on its accounting for leases, including the transitional provisions and the effects of transitioning from AASB 117, providing detailed examples from the company's financial statements. The analysis covers the application of various accounting standards and policies, including those related to financial instruments, revenue recognition, and taxation, highlighting the company's approach to financial reporting in accordance with Australian accounting standards and IFRS.

ADVANCED FINANCIAL ACCOUNTING

0

0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction

In this paper, the different accounting concepts which have been used by one of the Australian

bank named Westpac Banking Corporation in their annual report of 2017-2018 has been

analyzed in detail. Different accounting standards used by Westpac has also been evaluated. The

amended provision of the accounting standard 16 that is lease has also been discussed. The

important disclosures in respect of lease accounting have also been evaluated. The impact of new

terms on the entities has been examined. Westpac Banking Corporation is a well-known bank in

Australia situated in Sydney. It was founded in the year 1817. Headquarter of the bank is

situated at Westpac place in Australia. The bank provides financial services and different

banking services to its customers. It also provides services related to wealth management and

institutional services. The products of the bank are corporate banking, investment management,

consumer banking, insurance banking, private equity shares, mortgage banking, and management

of credit cards. The total number of branches of the Westpac throughout the world is 1204

branches and almost 3222 ATMs are installed throughout the world.

1)Accounting concepts used by Westpac Banking corporation

As there are different accounting concepts that are applied by entities of small size, medium-size,

and large organization. According to Kimmel et al. (2016, p-44), the different accounting

concepts are conservatism concepts, accrual concepts, matching concepts, concept of going

concern, cost concept, concept of business entity, concept of money measurement. While

analyzing the 2017-2018 annual report of Westpac it has been studied that the annual statement

of Westpac banking has been prepared as per the accounting standard issued by the Australian

board (AAS) and compliance of AAS means compliance of IFRS. The financial statement has

also been prepared considering the requirements of Banking Act, 1949 and the requirement of

Corporation Act, 2001. The financial statement of Westpac has been authorized by the directors

and the directors can reissue or amend the annual report of Westpac. The annual report of

Westpac has been prepared as per the relevant accounting policies. The management of Westpac

while preparing the annual report has followed the concept of historical cost. The securities

which are available for trading has been accounted at fair value. The financial liabilities and the

financial assets of the Westpac corporation have been recognized at fair value and which are

transferred at other comprehensive income categories (OCI). Different accounting assumptions,

1

In this paper, the different accounting concepts which have been used by one of the Australian

bank named Westpac Banking Corporation in their annual report of 2017-2018 has been

analyzed in detail. Different accounting standards used by Westpac has also been evaluated. The

amended provision of the accounting standard 16 that is lease has also been discussed. The

important disclosures in respect of lease accounting have also been evaluated. The impact of new

terms on the entities has been examined. Westpac Banking Corporation is a well-known bank in

Australia situated in Sydney. It was founded in the year 1817. Headquarter of the bank is

situated at Westpac place in Australia. The bank provides financial services and different

banking services to its customers. It also provides services related to wealth management and

institutional services. The products of the bank are corporate banking, investment management,

consumer banking, insurance banking, private equity shares, mortgage banking, and management

of credit cards. The total number of branches of the Westpac throughout the world is 1204

branches and almost 3222 ATMs are installed throughout the world.

1)Accounting concepts used by Westpac Banking corporation

As there are different accounting concepts that are applied by entities of small size, medium-size,

and large organization. According to Kimmel et al. (2016, p-44), the different accounting

concepts are conservatism concepts, accrual concepts, matching concepts, concept of going

concern, cost concept, concept of business entity, concept of money measurement. While

analyzing the 2017-2018 annual report of Westpac it has been studied that the annual statement

of Westpac banking has been prepared as per the accounting standard issued by the Australian

board (AAS) and compliance of AAS means compliance of IFRS. The financial statement has

also been prepared considering the requirements of Banking Act, 1949 and the requirement of

Corporation Act, 2001. The financial statement of Westpac has been authorized by the directors

and the directors can reissue or amend the annual report of Westpac. The annual report of

Westpac has been prepared as per the relevant accounting policies. The management of Westpac

while preparing the annual report has followed the concept of historical cost. The securities

which are available for trading has been accounted at fair value. The financial liabilities and the

financial assets of the Westpac corporation have been recognized at fair value and which are

transferred at other comprehensive income categories (OCI). Different accounting assumptions,

1

accounting policies have been applied while drafting the annual report. The estimates and the

relevant assumption which have been applied by the accountant of Westpac corporation are all

discussed at the audit committee of the company. While evaluating the going concern of

Westpac no indicators have been found which can prove that the company will shut down the

business soon. This implies that the company is following the going concern accounting

concepts. It has also been found that the corporation follows the accrual basis of doing an

accounting of company. According to Adhikari and Gårseth-Nesbakk (2016, p-125), the accrual

basis means that the company will recognize its revenue expenditure even if the amount of

expenditure has not been received and also the income will be recognized in the profit and loss

statement even if the income has not been received by the company.

The accounting of business combinations has been done by applying the acquisition method. The

accountant of the Westpac corporation has taken the fair value of all the assets at the time of

acquisition. The identifiable assets which have been acquired also measured and recognized at

fair value. Goodwill has been measured at the time of business combinations by comparing the

aggregate of consideration paid and share of minority interest with the amount of identifiable

assets. According to Klimczak et al. (2015, p-2017), if there is a loss in business combination

then it means that the company is paying more consideration to acquire the assets of the other

entity. The company has prepared the consolidated statement in its functional currency that is in

Australian dollar which is also the presentation currency of the company. The liabilities and

assets of the subsidiaries whose functional currency is not in Australian dollars are all converted

by using the exchange rate of the balance sheet date. The expenses and income of the company

are converted using the average rate of exchange of the year. The foreign exchange losses and

income of the corporation have been transferred to the income statements. The deferred income

which arises at the time of settlement of foreign transaction has been transferred to OCI. The

balance of equity of the foreign transactions are converted by applying the historical rate of

exchange.

The company has used different assumptions and different accounting estimates while doing

accounting of income tax, intangible assets, superannuation commitments, provisions. While

dong treatment of provisions related to the impairment charges company has also taken

significant estimates and assumptions. The company applied the provision of AASB-2016.

2

relevant assumption which have been applied by the accountant of Westpac corporation are all

discussed at the audit committee of the company. While evaluating the going concern of

Westpac no indicators have been found which can prove that the company will shut down the

business soon. This implies that the company is following the going concern accounting

concepts. It has also been found that the corporation follows the accrual basis of doing an

accounting of company. According to Adhikari and Gårseth-Nesbakk (2016, p-125), the accrual

basis means that the company will recognize its revenue expenditure even if the amount of

expenditure has not been received and also the income will be recognized in the profit and loss

statement even if the income has not been received by the company.

The accounting of business combinations has been done by applying the acquisition method. The

accountant of the Westpac corporation has taken the fair value of all the assets at the time of

acquisition. The identifiable assets which have been acquired also measured and recognized at

fair value. Goodwill has been measured at the time of business combinations by comparing the

aggregate of consideration paid and share of minority interest with the amount of identifiable

assets. According to Klimczak et al. (2015, p-2017), if there is a loss in business combination

then it means that the company is paying more consideration to acquire the assets of the other

entity. The company has prepared the consolidated statement in its functional currency that is in

Australian dollar which is also the presentation currency of the company. The liabilities and

assets of the subsidiaries whose functional currency is not in Australian dollars are all converted

by using the exchange rate of the balance sheet date. The expenses and income of the company

are converted using the average rate of exchange of the year. The foreign exchange losses and

income of the corporation have been transferred to the income statements. The deferred income

which arises at the time of settlement of foreign transaction has been transferred to OCI. The

balance of equity of the foreign transactions are converted by applying the historical rate of

exchange.

The company has used different assumptions and different accounting estimates while doing

accounting of income tax, intangible assets, superannuation commitments, provisions. While

dong treatment of provisions related to the impairment charges company has also taken

significant estimates and assumptions. The company applied the provision of AASB-2016.

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AASB-9 has been applied which is related to the treatment of financial instruments such as

financial liabilities, equities, financial assets, derivative contracts, hedging instruments. The

company has adopted the standard of AASB 9 so that the retained earning can be reduced by

709 million dollars The standard of financial instruments also can recognize the estimated losses

which are based on future information. The other accounting standard which has been applied is

AASB which deals with revenue arising from contract. This standard deals with all contracts

except insurance contracts, leases, and financial instruments. To deal with the treatment of lease,

financial instruments and insurance respective standards have been issued by AASB. The

accountant has applied the terms of the standard AASB-17 which provides the treatment of

insurance. The insurance standard will contain terms that are used for risk adjustment relating to

life insurance and general insurance taken by the corporation. The reinsurance contracts and the

liabilities associated with it have been treated separately by the accountant.

The amount of interest expense and interest income which arise from different financial

liabilities and financial are being recognized by applying the method of effective interest rate

(IRR). The total amortization costs are computed by using effective interest method (IRR). The

income from commission and fees are also recognized using IRR. The dividend income, trading

income, premium income, are also calculated by applying the method of effective interest. The

deferred tax and the current tax of the company are transfer to the statement of profit and loss.

The taxes which are directly recognized are transferred to OCI. Certain assumptions have been

applied by calculating the liability of current tax payable by the company. The volume variances

have been computed by using the average rate of the balances of liabilities and assets of Westpac

Corporation. Sales and purchases relating to assets of the company except for receivables and

loans of company have been recognized on the date of trading. The financial liabilities of the

corporation recorded in the balance sheet when there is an obligation to record the liabilities

arise. The accountant of Westpac derecognize the financial assets when the entity has received

cash from other entity or when rights have been expired to receive any cash due from the

financial assets. The amount of loan which carries both deposit and mortgage facilities are

recorded at gross value on balance sheet. The interested accrued from the loans are recorded on a

net basis. The Westpac groups record two types of provision for impairment of its loans which

are assessed collectively as well as individually. To assess the collective loan and the individual

loans the accountant have to use different assumptions which are necessary to show the real

3

financial liabilities, equities, financial assets, derivative contracts, hedging instruments. The

company has adopted the standard of AASB 9 so that the retained earning can be reduced by

709 million dollars The standard of financial instruments also can recognize the estimated losses

which are based on future information. The other accounting standard which has been applied is

AASB which deals with revenue arising from contract. This standard deals with all contracts

except insurance contracts, leases, and financial instruments. To deal with the treatment of lease,

financial instruments and insurance respective standards have been issued by AASB. The

accountant has applied the terms of the standard AASB-17 which provides the treatment of

insurance. The insurance standard will contain terms that are used for risk adjustment relating to

life insurance and general insurance taken by the corporation. The reinsurance contracts and the

liabilities associated with it have been treated separately by the accountant.

The amount of interest expense and interest income which arise from different financial

liabilities and financial are being recognized by applying the method of effective interest rate

(IRR). The total amortization costs are computed by using effective interest method (IRR). The

income from commission and fees are also recognized using IRR. The dividend income, trading

income, premium income, are also calculated by applying the method of effective interest. The

deferred tax and the current tax of the company are transfer to the statement of profit and loss.

The taxes which are directly recognized are transferred to OCI. Certain assumptions have been

applied by calculating the liability of current tax payable by the company. The volume variances

have been computed by using the average rate of the balances of liabilities and assets of Westpac

Corporation. Sales and purchases relating to assets of the company except for receivables and

loans of company have been recognized on the date of trading. The financial liabilities of the

corporation recorded in the balance sheet when there is an obligation to record the liabilities

arise. The accountant of Westpac derecognize the financial assets when the entity has received

cash from other entity or when rights have been expired to receive any cash due from the

financial assets. The amount of loan which carries both deposit and mortgage facilities are

recorded at gross value on balance sheet. The interested accrued from the loans are recorded on a

net basis. The Westpac groups record two types of provision for impairment of its loans which

are assessed collectively as well as individually. To assess the collective loan and the individual

loans the accountant have to use different assumptions which are necessary to show the real

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

value in the income statement. The assets of life insurance are recorded at fair value. The

liabilities of life insurance has also been recorded at fair value and different judgement and

assumption have been applied to record them.

The accounting policy which have been used for payables of Westpac group is that initially the

payables have been reported at fair value and the subsequent measurement has been done at

amortized cost. These measurement has been done by using the IRR method. The same

recognition policy has been used for other borrowings and deposits as in the case of payables.

The bills receivables of the company which arises from the issues of debt such as bonds,

debentures, notes and commercial paper initially recorded at discounted value and subsequently

recorded at rediscount value. Bonds, debentures, commercial paper are capital market

instruments which attract financial institutions, banks, potential investors, and government. The

accountant has also used the conservatism concept while recording the income and expenses of

entity. According to Biddle and Song (2016, p-15), the concept specifies that the company

should recognize the liabilities and expenses if there is any uncertain regarding the outcome. The

concept also specifies that one should record the revenue only when there is 100% assurance of

receiving the income. The accountant has also considered the requirement of matching principle

while recognizing the expenses and revenue of Westpac corporation. According to Collier (2015,

p-5), the concept of matching states that the company should recognize the revenue and the

expenses related to the revenue in the same period of reporting. The concept relating to

consistency has also been taken into consideration by the accountant. As opined by Bedford and

Ziegler (2016, p-2019), the consistency concepts state that once the method or accounting

principle has been adopted by the company then they should apply it consistently throughout the

period that is in future period of accounting. The intangible assets of Westpac have been initially

measured at cost and after that, the subsequent measurement has been done at amortized cost.

2) Changes in AASB 16- Leases

Different changes have been made in the new accounting standard of lease (AASB 16). The new

standard of AASB 16 was issued on January 2016 by the international board of accounting

standard. The changes will be effective from January 2019 and the entities of Australia have to

comply with the changes in the new standard issued by the Accounting standard board of

Australia. As per the new standard, the lessees are required to recognize all of their leases and

4

liabilities of life insurance has also been recorded at fair value and different judgement and

assumption have been applied to record them.

The accounting policy which have been used for payables of Westpac group is that initially the

payables have been reported at fair value and the subsequent measurement has been done at

amortized cost. These measurement has been done by using the IRR method. The same

recognition policy has been used for other borrowings and deposits as in the case of payables.

The bills receivables of the company which arises from the issues of debt such as bonds,

debentures, notes and commercial paper initially recorded at discounted value and subsequently

recorded at rediscount value. Bonds, debentures, commercial paper are capital market

instruments which attract financial institutions, banks, potential investors, and government. The

accountant has also used the conservatism concept while recording the income and expenses of

entity. According to Biddle and Song (2016, p-15), the concept specifies that the company

should recognize the liabilities and expenses if there is any uncertain regarding the outcome. The

concept also specifies that one should record the revenue only when there is 100% assurance of

receiving the income. The accountant has also considered the requirement of matching principle

while recognizing the expenses and revenue of Westpac corporation. According to Collier (2015,

p-5), the concept of matching states that the company should recognize the revenue and the

expenses related to the revenue in the same period of reporting. The concept relating to

consistency has also been taken into consideration by the accountant. As opined by Bedford and

Ziegler (2016, p-2019), the consistency concepts state that once the method or accounting

principle has been adopted by the company then they should apply it consistently throughout the

period that is in future period of accounting. The intangible assets of Westpac have been initially

measured at cost and after that, the subsequent measurement has been done at amortized cost.

2) Changes in AASB 16- Leases

Different changes have been made in the new accounting standard of lease (AASB 16). The new

standard of AASB 16 was issued on January 2016 by the international board of accounting

standard. The changes will be effective from January 2019 and the entities of Australia have to

comply with the changes in the new standard issued by the Accounting standard board of

Australia. As per the new standard, the lessees are required to recognize all of their leases and

4

the liabilities and assets on balance sheet. This recognition will provide transparency to the

leaseholders. The changes in the lease provision will impact the Australian entities those who

deal with operating lease of manufacturing equipment, aircraft, logistics services, and other

operating lease such as mining equipment. The entities who will implement the relevant changes

of the standard lease have to keep a depth knowledge and understanding of amended provisions

and should also review the impact of the standard on the company financial statements such

statement of cash flow, statement of income and balance sheet. At present, the accountant of

Westpac Corporation has adjusted the off-balance sheet transaction of lease in the financial

statements so that they can reflect the transaction of lease. Westpac should also consider

implications on important ratios, gearing ratios, and also on loan covenants. They should

consider the implications of the new standard on the schemes of remunerations.

Westpac after the implementation of the amended standard of lease will initially recognize the

liability and asset at fair value of lease payments which are non-cancellable. If there is a certainty

that the entity will exercise the option at present value then the payments will be made

periodically. All the leases which exist on Westpac balance sheet after the implementation of the

new provision will lead to interest expenses but the entity will be able to claim depreciation on

the leased assets. The new lease terms do not apply on leases which are short term that is lease

which is lease than 12 months or exactly 12 months. The new terms of the standard also does not

apply to underlying assets which carries a low value. The new standards also does not apply to

peppercorn leases. The new standard provide a model for both the lessee and lessor which are

comprehensive and the arrangement of lease can be identified easily which will help to recognize

the lease in the statement of financial position that is on balance sheet. New AASB 16 helps to

distinguish the service contracts with leases. According to the new standard the companies are

not entitled to incur reassessment cost. As per lessor point of view, the changes which have been

introduced by the Accounting standard board of Australia do not carry much importance. In case

of sublease contract, the lessor will not have to do any adjustment related to the lease transition.

The new lease allows the lessor and lessee to recognize a high amount in the early stage and the

balance will be recognized at a later stage with a low amount. Westpac corporation recognizes

the interest amount of lease under financing activities. There are different issues that whether the

changes will track individual lease or accumulated the significant information mandatorily for

disclosures. The other issue related to the new standard is whether the lease term will impact on

5

leaseholders. The changes in the lease provision will impact the Australian entities those who

deal with operating lease of manufacturing equipment, aircraft, logistics services, and other

operating lease such as mining equipment. The entities who will implement the relevant changes

of the standard lease have to keep a depth knowledge and understanding of amended provisions

and should also review the impact of the standard on the company financial statements such

statement of cash flow, statement of income and balance sheet. At present, the accountant of

Westpac Corporation has adjusted the off-balance sheet transaction of lease in the financial

statements so that they can reflect the transaction of lease. Westpac should also consider

implications on important ratios, gearing ratios, and also on loan covenants. They should

consider the implications of the new standard on the schemes of remunerations.

Westpac after the implementation of the amended standard of lease will initially recognize the

liability and asset at fair value of lease payments which are non-cancellable. If there is a certainty

that the entity will exercise the option at present value then the payments will be made

periodically. All the leases which exist on Westpac balance sheet after the implementation of the

new provision will lead to interest expenses but the entity will be able to claim depreciation on

the leased assets. The new lease terms do not apply on leases which are short term that is lease

which is lease than 12 months or exactly 12 months. The new terms of the standard also does not

apply to underlying assets which carries a low value. The new standards also does not apply to

peppercorn leases. The new standard provide a model for both the lessee and lessor which are

comprehensive and the arrangement of lease can be identified easily which will help to recognize

the lease in the statement of financial position that is on balance sheet. New AASB 16 helps to

distinguish the service contracts with leases. According to the new standard the companies are

not entitled to incur reassessment cost. As per lessor point of view, the changes which have been

introduced by the Accounting standard board of Australia do not carry much importance. In case

of sublease contract, the lessor will not have to do any adjustment related to the lease transition.

The new lease allows the lessor and lessee to recognize a high amount in the early stage and the

balance will be recognized at a later stage with a low amount. Westpac corporation recognizes

the interest amount of lease under financing activities. There are different issues that whether the

changes will track individual lease or accumulated the significant information mandatorily for

disclosures. The other issue related to the new standard is whether the lease term will impact on

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

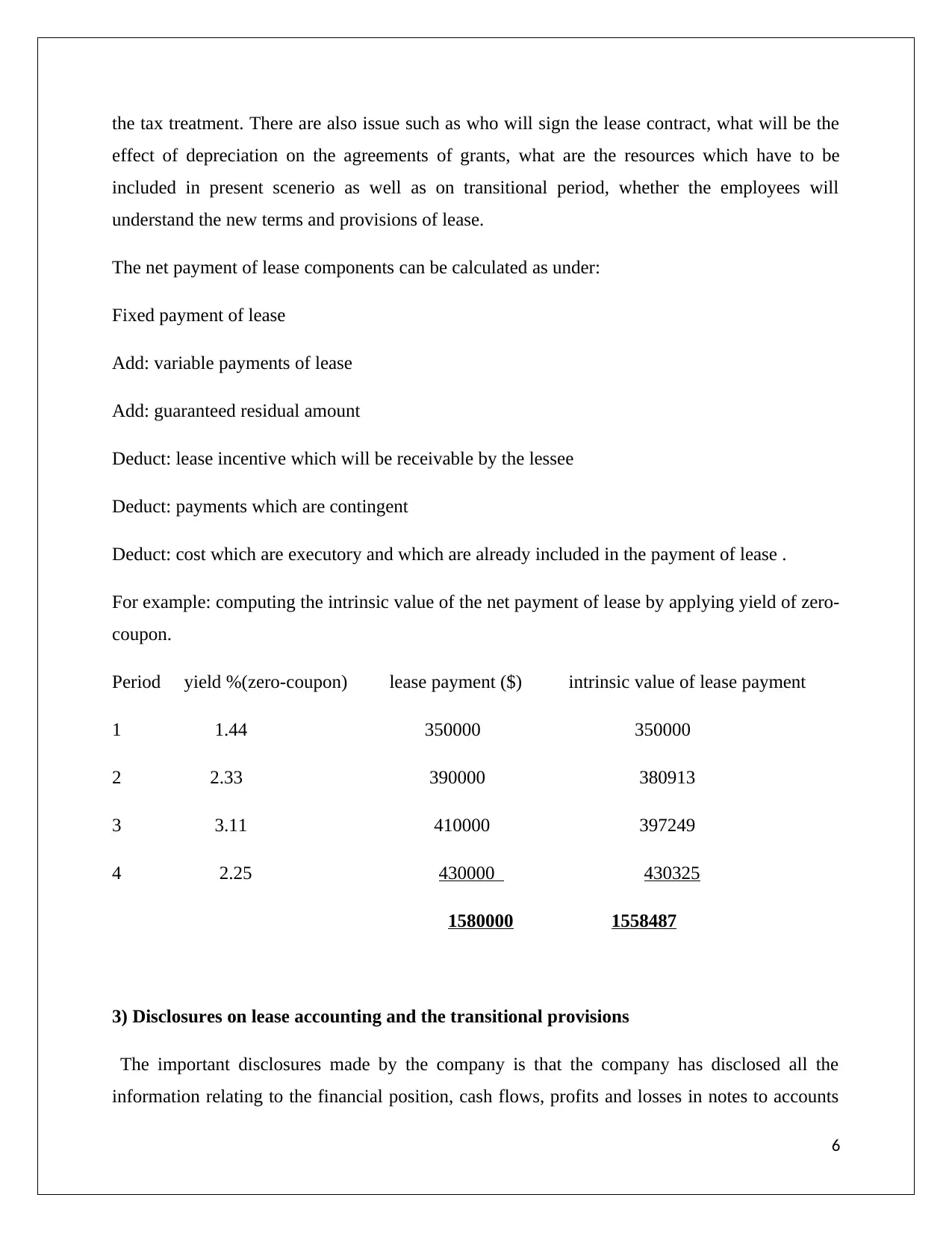

the tax treatment. There are also issue such as who will sign the lease contract, what will be the

effect of depreciation on the agreements of grants, what are the resources which have to be

included in present scenerio as well as on transitional period, whether the employees will

understand the new terms and provisions of lease.

The net payment of lease components can be calculated as under:

Fixed payment of lease

Add: variable payments of lease

Add: guaranteed residual amount

Deduct: lease incentive which will be receivable by the lessee

Deduct: payments which are contingent

Deduct: cost which are executory and which are already included in the payment of lease .

For example: computing the intrinsic value of the net payment of lease by applying yield of zero-

coupon.

Period yield %(zero-coupon) lease payment ($) intrinsic value of lease payment

1 1.44 350000 350000

2 2.33 390000 380913

3 3.11 410000 397249

4 2.25 430000 430325

1580000 1558487

3) Disclosures on lease accounting and the transitional provisions

The important disclosures made by the company is that the company has disclosed all the

information relating to the financial position, cash flows, profits and losses in notes to accounts

6

effect of depreciation on the agreements of grants, what are the resources which have to be

included in present scenerio as well as on transitional period, whether the employees will

understand the new terms and provisions of lease.

The net payment of lease components can be calculated as under:

Fixed payment of lease

Add: variable payments of lease

Add: guaranteed residual amount

Deduct: lease incentive which will be receivable by the lessee

Deduct: payments which are contingent

Deduct: cost which are executory and which are already included in the payment of lease .

For example: computing the intrinsic value of the net payment of lease by applying yield of zero-

coupon.

Period yield %(zero-coupon) lease payment ($) intrinsic value of lease payment

1 1.44 350000 350000

2 2.33 390000 380913

3 3.11 410000 397249

4 2.25 430000 430325

1580000 1558487

3) Disclosures on lease accounting and the transitional provisions

The important disclosures made by the company is that the company has disclosed all the

information relating to the financial position, cash flows, profits and losses in notes to accounts

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

so that they can assess and review the effect of the lease on the financial performance, cash flow,

and financial positions of lessee. A lessee is required to disclose vital information in a separate

note or a single note in the financial statement. The lessee should not provide any information

which has already been there in the notes to accounts. The following information shall be

disclosed by the lessee:

Interest amount on the lease contract

Outflows related to lease

Depreciation charged on the underlying assets

Profit or gains which have been arisen at the time of leaseback transaction or sale

Carrying amount of the lease assets at the end of the term of the lease

Residual value of the asset after the expiry of the lease contract

Variable expenses for the payment of lease

The maturity analysis shall be disclosed by the lessee. The lessee should also disclose the

quantitative and qualitative information of the activities of the lease. The other informations

which are to be disclosed so that the potential users of the statement of financial affairs can

assess the leasing activities are:

Termination option or the extension of lease term

Covenants and restrictions which are imposed by the provisions of standard

Transactions such as leaseback and sale

According to Asyaeva et al. (2016, p-96), the lessor are required to classify the lease as financial

lease or operating lease. A lease is said to be a financial lease when the risk has been transferred

to the lessee and at the expiry of the lease term the assets will be transferred to the party to the

lease. According to Wong and Joshi (2015, p-27), the asset is classified as financial lease when

the lease term equals the economic life of the leased assets. The dealers or manufacturers shall

record the finance lease when the fair value of asset is given and if the fair value of the asset is

not given then the dealer should disclose the finance lease at the present value by applying a

discounted rate. The lessor should recognize the finance income on a rational basis that is he

should record it as per the lease term. The specific transition which should be disclosed in the

7

and financial positions of lessee. A lessee is required to disclose vital information in a separate

note or a single note in the financial statement. The lessee should not provide any information

which has already been there in the notes to accounts. The following information shall be

disclosed by the lessee:

Interest amount on the lease contract

Outflows related to lease

Depreciation charged on the underlying assets

Profit or gains which have been arisen at the time of leaseback transaction or sale

Carrying amount of the lease assets at the end of the term of the lease

Residual value of the asset after the expiry of the lease contract

Variable expenses for the payment of lease

The maturity analysis shall be disclosed by the lessee. The lessee should also disclose the

quantitative and qualitative information of the activities of the lease. The other informations

which are to be disclosed so that the potential users of the statement of financial affairs can

assess the leasing activities are:

Termination option or the extension of lease term

Covenants and restrictions which are imposed by the provisions of standard

Transactions such as leaseback and sale

According to Asyaeva et al. (2016, p-96), the lessor are required to classify the lease as financial

lease or operating lease. A lease is said to be a financial lease when the risk has been transferred

to the lessee and at the expiry of the lease term the assets will be transferred to the party to the

lease. According to Wong and Joshi (2015, p-27), the asset is classified as financial lease when

the lease term equals the economic life of the leased assets. The dealers or manufacturers shall

record the finance lease when the fair value of asset is given and if the fair value of the asset is

not given then the dealer should disclose the finance lease at the present value by applying a

discounted rate. The lessor should recognize the finance income on a rational basis that is he

should record it as per the lease term. The specific transition which should be disclosed in the

7

statement of financial position such as exemption on short-term lease contract, assessment of

lease contract, and application of hindsight at the time of calculating lease term. The discounted

rate of borrowing should also be reported. If any country is doing transaction in different

currencies then the company can disclose all the different currencies used in the transactions.

The entity should record the transition effect with effect from retrospective basis. The adjustment

should be made by considering as the new standard was always there in force.

8

lease contract, and application of hindsight at the time of calculating lease term. The discounted

rate of borrowing should also be reported. If any country is doing transaction in different

currencies then the company can disclose all the different currencies used in the transactions.

The entity should record the transition effect with effect from retrospective basis. The adjustment

should be made by considering as the new standard was always there in force.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References

Adhikari, P. and Gårseth-Nesbakk, L., (2016), June. Implementing public sector accruals in

OECD member states: Major issues and challenges. In Accounting Forum (Vol. 40, No. 2, pp.

125-142). Taylor & Francis.

Asyaeva, E.A., Chizhankova, I.V., Bondaletova, N.F. and Makushkin, S.A., (2016). Methods for

assessing the credit risk of leasing assets. International Journal of Economics and Financial

Issues, 6(1S), pp.96-100.

Bedford, N.M. and Ziegler, R.E., (2016). The contributions of AC Littleton to accounting

thought and practice. Memorial Articles for 20th Century American Accounting Leaders, 49,

p.219.

Biddle, G.C., Ma, M.L. and Song, F.M., (2016). Accounting conservatism and bankruptcy risk.

Available at SSRN 1621272. Pp.15-19

Collier, P.M., (2015). Accounting for managers: Interpreting accounting information for

decision making. John Wiley & Sons. 51(1), p.25-29

Kimmel, P.D., Weygandt, J.J., Kieso, D.E. and Trenholm, B., (2016). Financial Accounting.

Wiley Custom Learning Solutions. 32(1), pp.44-65

Klimczak, M.K., Pikos, A., Dynel, M. and Językowej, Z.P., (2015). Uncertainty in the financial

statements: the study of goodwill disclosures in Polish. J. Krasodomska, K. Świetla (red.),

Współczesne uwarunkowania sprawozdawczości i rewizji finansowej, pp.217-226.

Wong, K. and Joshi, M., (2015). The impact of lease capitalisation on financial statements and

key ratios: Evidence from Australia. Australasian Accounting, Business and Finance Journal,

9(3), pp.27-44.

9

Adhikari, P. and Gårseth-Nesbakk, L., (2016), June. Implementing public sector accruals in

OECD member states: Major issues and challenges. In Accounting Forum (Vol. 40, No. 2, pp.

125-142). Taylor & Francis.

Asyaeva, E.A., Chizhankova, I.V., Bondaletova, N.F. and Makushkin, S.A., (2016). Methods for

assessing the credit risk of leasing assets. International Journal of Economics and Financial

Issues, 6(1S), pp.96-100.

Bedford, N.M. and Ziegler, R.E., (2016). The contributions of AC Littleton to accounting

thought and practice. Memorial Articles for 20th Century American Accounting Leaders, 49,

p.219.

Biddle, G.C., Ma, M.L. and Song, F.M., (2016). Accounting conservatism and bankruptcy risk.

Available at SSRN 1621272. Pp.15-19

Collier, P.M., (2015). Accounting for managers: Interpreting accounting information for

decision making. John Wiley & Sons. 51(1), p.25-29

Kimmel, P.D., Weygandt, J.J., Kieso, D.E. and Trenholm, B., (2016). Financial Accounting.

Wiley Custom Learning Solutions. 32(1), pp.44-65

Klimczak, M.K., Pikos, A., Dynel, M. and Językowej, Z.P., (2015). Uncertainty in the financial

statements: the study of goodwill disclosures in Polish. J. Krasodomska, K. Świetla (red.),

Współczesne uwarunkowania sprawozdawczości i rewizji finansowej, pp.217-226.

Wong, K. and Joshi, M., (2015). The impact of lease capitalisation on financial statements and

key ratios: Evidence from Australia. Australasian Accounting, Business and Finance Journal,

9(3), pp.27-44.

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

https://pkf.com.au/blog/2019/aasb-16-leases-what-is-the-impact/

10

10

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.