P30899: EMH Relevance to Corporate Managers - Finance

VerifiedAdded on 2022/08/15

|12

|3081

|16

Essay

AI Summary

This essay delves into the Efficient Market Hypothesis (EMH), a cornerstone of investment theory, examining its three forms: weak, semi-strong, and strong. It critiques the EMH's ability to adequately explain asset pricing, particularly regarding a firm's debt and equity, and discusses the operational, allocative, and informational efficiencies. The essay explores the EMH's relevance to corporate managers, considering mergers and acquisitions, financial policy timing, and creative accounting. It analyzes the EMH's impact on project evaluation based on net present value (NPV) and discusses the views of both proponents and opponents of EMH. The conclusion summarizes the limitations of EMH and its relevance in practical financial management.

Running Head: ADVANCED GLOBAL FINANCIAL MANAGEMENT

ADVANCED GLOBAL FINANCIAL MANAGEMENT

Name of the Student

Name of the University

Author Note

ADVANCED GLOBAL FINANCIAL MANAGEMENT

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ADVANCED GLOBAL FINANCIAL MANAGEMENT

Table of Contents

Introduction................................................................................................................................2

Three Forms of Efficient Markets..........................................................................................2

Literature Review.......................................................................................................................4

Efficient Market Hypothesis..................................................................................................4

EMH Relevance.....................................................................................................................6

Conclusion..................................................................................................................................8

Reference..................................................................................................................................10

Table of Contents

Introduction................................................................................................................................2

Three Forms of Efficient Markets..........................................................................................2

Literature Review.......................................................................................................................4

Efficient Market Hypothesis..................................................................................................4

EMH Relevance.....................................................................................................................6

Conclusion..................................................................................................................................8

Reference..................................................................................................................................10

2ADVANCED GLOBAL FINANCIAL MANAGEMENT

Introduction

“Efficient Markets Hypothesis” is theory of investment that is derived from the

concepts attributed to research of Eugene Fama. The book published by Fama “Efficient

Capital Markets” in 1970 has put basic set of idea that virtually it is not possible for beating

market on the consistent basis for making returns of investment that exceeds overall average

of market, as reflected by the key indexes of stock, for instance S&P 500 Index. EMH in the

community of investment is underlying reasons why investors choose passive strategy of

investment. It helps in explaining valid rationale to buy these exchange-traded funds and

passive mutual funds (Naseer & Bin Tariq, 2015). According to the theory of Fama, while

investors might be lucky and purchase stock, which brings huge profits of short-term over

long-term, the investors however, realistically cannot hope for achieving return on

investment, which is higher than average of market (Noda, 2016).

Three Forms of Efficient Markets

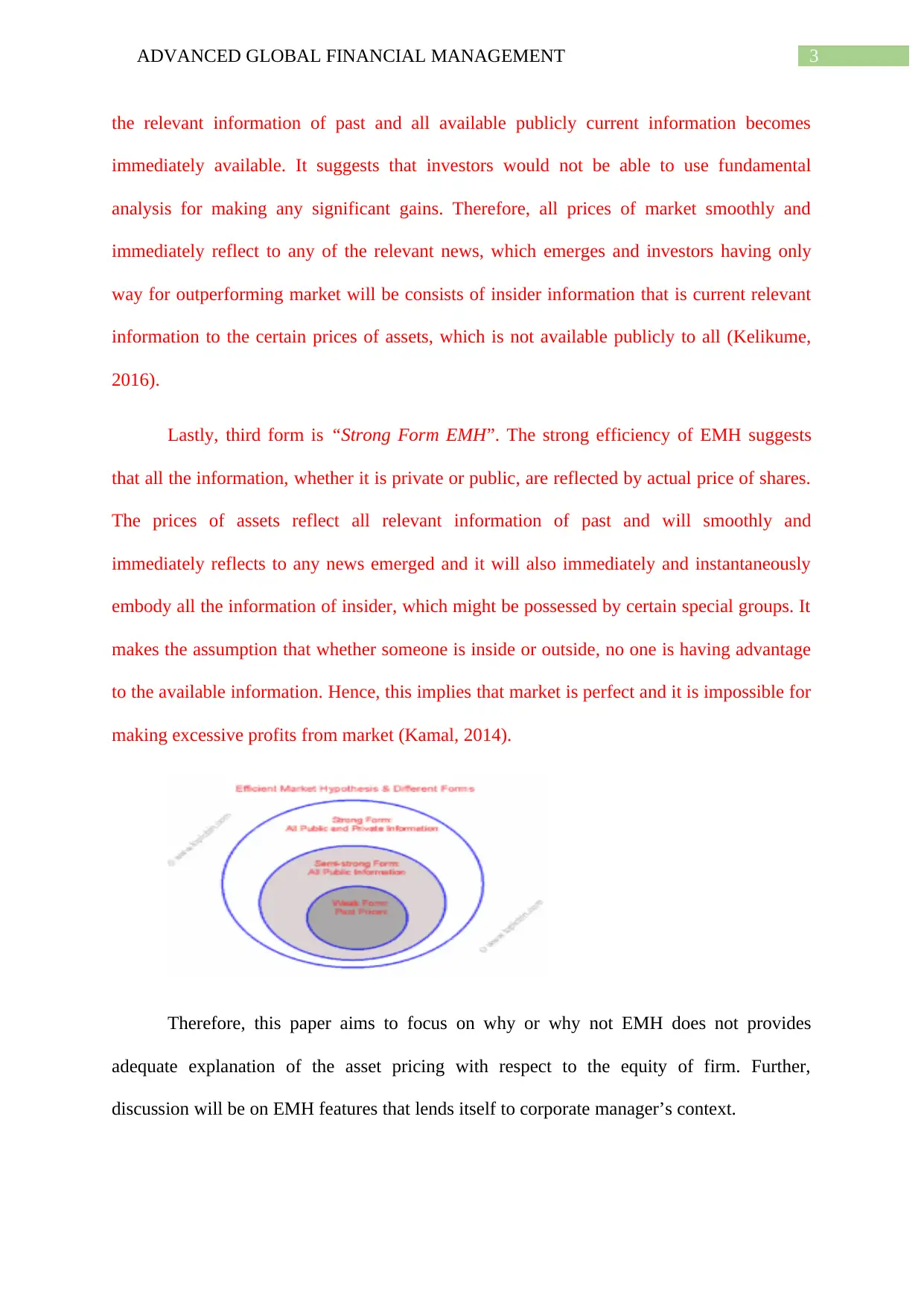

Fama has defined three major forms of the efficient market. “Weak-Form EMH” is

first form of the EMH. This form makes the claims that all the information of past is reflected

into actual price of share. The prices of assets embody all the relevant information of past

perfectly. The price movements of future cannot be predicted by using the prices of past. It

makes the assumption that for achieving returns, it is not possible to use technical analysis.

Further, there includes no such trends of long-trends, from which higher returns can be

earned by investors with the help of their detection. It is due to the fact that it held that all the

information of past is available completely in public and it is incorporated in the prices of

assets (Kelikume, 2016).

The second form is “Semi Form EMH”. This form claims that all the publicly

available information is reflected by actual price of shares. Further, prices of assets reflect all

Introduction

“Efficient Markets Hypothesis” is theory of investment that is derived from the

concepts attributed to research of Eugene Fama. The book published by Fama “Efficient

Capital Markets” in 1970 has put basic set of idea that virtually it is not possible for beating

market on the consistent basis for making returns of investment that exceeds overall average

of market, as reflected by the key indexes of stock, for instance S&P 500 Index. EMH in the

community of investment is underlying reasons why investors choose passive strategy of

investment. It helps in explaining valid rationale to buy these exchange-traded funds and

passive mutual funds (Naseer & Bin Tariq, 2015). According to the theory of Fama, while

investors might be lucky and purchase stock, which brings huge profits of short-term over

long-term, the investors however, realistically cannot hope for achieving return on

investment, which is higher than average of market (Noda, 2016).

Three Forms of Efficient Markets

Fama has defined three major forms of the efficient market. “Weak-Form EMH” is

first form of the EMH. This form makes the claims that all the information of past is reflected

into actual price of share. The prices of assets embody all the relevant information of past

perfectly. The price movements of future cannot be predicted by using the prices of past. It

makes the assumption that for achieving returns, it is not possible to use technical analysis.

Further, there includes no such trends of long-trends, from which higher returns can be

earned by investors with the help of their detection. It is due to the fact that it held that all the

information of past is available completely in public and it is incorporated in the prices of

assets (Kelikume, 2016).

The second form is “Semi Form EMH”. This form claims that all the publicly

available information is reflected by actual price of shares. Further, prices of assets reflect all

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ADVANCED GLOBAL FINANCIAL MANAGEMENT

the relevant information of past and all available publicly current information becomes

immediately available. It suggests that investors would not be able to use fundamental

analysis for making any significant gains. Therefore, all prices of market smoothly and

immediately reflect to any of the relevant news, which emerges and investors having only

way for outperforming market will be consists of insider information that is current relevant

information to the certain prices of assets, which is not available publicly to all (Kelikume,

2016).

Lastly, third form is “Strong Form EMH”. The strong efficiency of EMH suggests

that all the information, whether it is private or public, are reflected by actual price of shares.

The prices of assets reflect all relevant information of past and will smoothly and

immediately reflects to any news emerged and it will also immediately and instantaneously

embody all the information of insider, which might be possessed by certain special groups. It

makes the assumption that whether someone is inside or outside, no one is having advantage

to the available information. Hence, this implies that market is perfect and it is impossible for

making excessive profits from market (Kamal, 2014).

Therefore, this paper aims to focus on why or why not EMH does not provides

adequate explanation of the asset pricing with respect to the equity of firm. Further,

discussion will be on EMH features that lends itself to corporate manager’s context.

the relevant information of past and all available publicly current information becomes

immediately available. It suggests that investors would not be able to use fundamental

analysis for making any significant gains. Therefore, all prices of market smoothly and

immediately reflect to any of the relevant news, which emerges and investors having only

way for outperforming market will be consists of insider information that is current relevant

information to the certain prices of assets, which is not available publicly to all (Kelikume,

2016).

Lastly, third form is “Strong Form EMH”. The strong efficiency of EMH suggests

that all the information, whether it is private or public, are reflected by actual price of shares.

The prices of assets reflect all relevant information of past and will smoothly and

immediately reflects to any news emerged and it will also immediately and instantaneously

embody all the information of insider, which might be possessed by certain special groups. It

makes the assumption that whether someone is inside or outside, no one is having advantage

to the available information. Hence, this implies that market is perfect and it is impossible for

making excessive profits from market (Kamal, 2014).

Therefore, this paper aims to focus on why or why not EMH does not provides

adequate explanation of the asset pricing with respect to the equity of firm. Further,

discussion will be on EMH features that lends itself to corporate manager’s context.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ADVANCED GLOBAL FINANCIAL MANAGEMENT

Literature Review

Efficient Market Hypothesis

Fama stated that efficient market is market that rapidly adjusts to new information.

Fama concept is based on the fact that information efficient market is featured by securities

price at any time immediately and it fully reflects all the available information. According to

EMH, investors are not required to be rational rather they act in random way as a whole and

market is right always. The term efficient implies normal. For instance, it is normal to have

uncommon reaction to the uncommon information. In case, suddenly crowd run in the one

particular direction then it is normal for the people for running in that particular direction,

even if there includes no any causes for doing so. EMH does not explains that no investors

are able for beating the market. This hypothesis states that there include outliers, which can

beat averages of market. Although, outliers can dramatically lose to the market. Hence,

majority is much closer to median. Those are lucky, who wins and those are unlucky, who

loses (Manasseh, 2016). Following are the points that explains why and why not EMH does

not explains pricing of asset with the respect of firm’s equity:

Operational Efficiency

The operational efficiency includes cost related with operating business operations or

interest cost, charged by the lender for money borrowed. Generally, higher transaction cost is

interpreted as higher cost of dealing with financial markets. Therefore, for increase the

operational efficiency, the transactions should be at minimum. For this, the market players

who are mainly active, has to be increased (Fama et al. 1969).

Allocative Efficiency

The market is defined to be allocative efficiency, when direct saving is channeled

towards project that is considered to have efficient portfolios. The efficiency of company

Literature Review

Efficient Market Hypothesis

Fama stated that efficient market is market that rapidly adjusts to new information.

Fama concept is based on the fact that information efficient market is featured by securities

price at any time immediately and it fully reflects all the available information. According to

EMH, investors are not required to be rational rather they act in random way as a whole and

market is right always. The term efficient implies normal. For instance, it is normal to have

uncommon reaction to the uncommon information. In case, suddenly crowd run in the one

particular direction then it is normal for the people for running in that particular direction,

even if there includes no any causes for doing so. EMH does not explains that no investors

are able for beating the market. This hypothesis states that there include outliers, which can

beat averages of market. Although, outliers can dramatically lose to the market. Hence,

majority is much closer to median. Those are lucky, who wins and those are unlucky, who

loses (Manasseh, 2016). Following are the points that explains why and why not EMH does

not explains pricing of asset with the respect of firm’s equity:

Operational Efficiency

The operational efficiency includes cost related with operating business operations or

interest cost, charged by the lender for money borrowed. Generally, higher transaction cost is

interpreted as higher cost of dealing with financial markets. Therefore, for increase the

operational efficiency, the transactions should be at minimum. For this, the market players

who are mainly active, has to be increased (Fama et al. 1969).

Allocative Efficiency

The market is defined to be allocative efficiency, when direct saving is channeled

towards project that is considered to have efficient portfolios. The efficiency of company

5ADVANCED GLOBAL FINANCIAL MANAGEMENT

results into raising of funds that ultimately results into fostering economy. The prosperity of

economy is high, when saving is not channeled to the project. Financial intermediaries is

required to achieve allocative efficiency in the financial market. It is because funds are

allocated from the savers to main users (Hamid et al. 2017).

Informational Efficiency

Information efficiency is achieved when information is available to the users relating

to the reflection of future information or perspective of security in the present prices of the

security. When the security’s information is available to all the parties then doing

investigation or research on the security becomes fair to all the concerned users. This is

significant for the financial managers. It is due to the fact that management decisions is

reflected in the security’s prices. The EMH concept is based on efficiency of the information

processing. The proficiency of stock market depends on the information that is reflected in

accurate way in securities prices (Malkiel & Fama, 1970).

EMH continues to provide convincing explanation of the way prices of assets

responds to various information types. However, it does not provide very good account of

equity and debt of firm. CAPM has confronted with various criticism from the financial

scholars. There is close link of EMH with and CAPM and substitution theory of the

securities. CAPM has been used widely for measuring risk in the testing EMH. It is used for

testing different return and anomalies. Fama has criticized CAPM because of its inability for

giving true valuation of the return of stock and it works only on model of three-factor

(Khuntia & Pattanayak, 2018). As per Fama, CAPM clearly provides missing link from the

availability of information to actual prices of market. He stated that hypothesis, which prices

in proper way, helps in reflecting the availability of information and it is required to be tested

in the model context of the expected returns such as CAPM (Khan & Khan, 2016).

results into raising of funds that ultimately results into fostering economy. The prosperity of

economy is high, when saving is not channeled to the project. Financial intermediaries is

required to achieve allocative efficiency in the financial market. It is because funds are

allocated from the savers to main users (Hamid et al. 2017).

Informational Efficiency

Information efficiency is achieved when information is available to the users relating

to the reflection of future information or perspective of security in the present prices of the

security. When the security’s information is available to all the parties then doing

investigation or research on the security becomes fair to all the concerned users. This is

significant for the financial managers. It is due to the fact that management decisions is

reflected in the security’s prices. The EMH concept is based on efficiency of the information

processing. The proficiency of stock market depends on the information that is reflected in

accurate way in securities prices (Malkiel & Fama, 1970).

EMH continues to provide convincing explanation of the way prices of assets

responds to various information types. However, it does not provide very good account of

equity and debt of firm. CAPM has confronted with various criticism from the financial

scholars. There is close link of EMH with and CAPM and substitution theory of the

securities. CAPM has been used widely for measuring risk in the testing EMH. It is used for

testing different return and anomalies. Fama has criticized CAPM because of its inability for

giving true valuation of the return of stock and it works only on model of three-factor

(Khuntia & Pattanayak, 2018). As per Fama, CAPM clearly provides missing link from the

availability of information to actual prices of market. He stated that hypothesis, which prices

in proper way, helps in reflecting the availability of information and it is required to be tested

in the model context of the expected returns such as CAPM (Khan & Khan, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ADVANCED GLOBAL FINANCIAL MANAGEMENT

EMH Relevance

Opponents and supporters of EMH makes various cases for supporting their own set

of views. One long-term study analyzed that over ten-year time-period, the only actively

managed funds types that were able for outperforming index funds in half of the time were

US emerging markets funds and small growth funds (Fama et al. 1969). These data, questions

whole model of investment advisory business, which has investment firms paying huge

amounts to the top managers of fund on the basis of belief that these managers will generate

the returns above average overall return of market (Jovanovic, Andreadakis & Schinckus,

2016).

However, opponents of EMH provides the fact that investors and traders generate

returns on the investment consistently that dwarf overall market performance. As per EMH, it

is impossible other than the blind luck. Over long span of time, blind luck cannot suggest that

same people beat market over and over again by the wider margin. There are indeed times,

when excess pessimism or optimism in market drives the prices for trading are excessive

lower or higher prices. It clearly shows that there is not always trading of securities at its fair

market value (Hamid et al. 2017).

Most theories of capital market makes the assumption about behavior of investor and

largely ignores possibility that the theoretical models could influence economic agents’

behavior. The corporate managers are more exposed to EMH that exhibits greater prosperity

for managing index funds. While working for the active funds, the exposed managers always

tends for holding portfolios with the larger stocks numbers and deviates less from their

objective benchmarks of investment than the unexposed peers (Gabriela ğiĠan, 2015). The

familiarity with the EMH induces the active managers for taking more systematic risk.

However, exposure to academic idea not always results in the better performance rather it

helps the corporate managers for generating flows of capital, particularly when it belongs to

EMH Relevance

Opponents and supporters of EMH makes various cases for supporting their own set

of views. One long-term study analyzed that over ten-year time-period, the only actively

managed funds types that were able for outperforming index funds in half of the time were

US emerging markets funds and small growth funds (Fama et al. 1969). These data, questions

whole model of investment advisory business, which has investment firms paying huge

amounts to the top managers of fund on the basis of belief that these managers will generate

the returns above average overall return of market (Jovanovic, Andreadakis & Schinckus,

2016).

However, opponents of EMH provides the fact that investors and traders generate

returns on the investment consistently that dwarf overall market performance. As per EMH, it

is impossible other than the blind luck. Over long span of time, blind luck cannot suggest that

same people beat market over and over again by the wider margin. There are indeed times,

when excess pessimism or optimism in market drives the prices for trading are excessive

lower or higher prices. It clearly shows that there is not always trading of securities at its fair

market value (Hamid et al. 2017).

Most theories of capital market makes the assumption about behavior of investor and

largely ignores possibility that the theoretical models could influence economic agents’

behavior. The corporate managers are more exposed to EMH that exhibits greater prosperity

for managing index funds. While working for the active funds, the exposed managers always

tends for holding portfolios with the larger stocks numbers and deviates less from their

objective benchmarks of investment than the unexposed peers (Gabriela ğiĠan, 2015). The

familiarity with the EMH induces the active managers for taking more systematic risk.

However, exposure to academic idea not always results in the better performance rather it

helps the corporate managers for generating flows of capital, particularly when it belongs to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ADVANCED GLOBAL FINANCIAL MANAGEMENT

the larger families of multi-fund and the fund charges lower ratios of expenses (Dragotă &

Ţilică, 2014). The proponents of EMH concludes that due to market randomness, the

investors can do better with the help of investing in passive and low cost portfolios. For

instance, data compiled by the Morningstar in June 2019 Passive or Active Barometer study

has supported EMH. It compared returns of active managers in all the categories against

combined made of exchange-traded funds and related index funds (Rossi, 2015). This study

has found that over beginning of ten year period, only twenty-third percent of the active

managers were having ability for outperforming their passive peers. The rates of better

success were found in foreign bonds funds and equity funds (Dragota & Oprea, 2014). The

lower rates off success were found in the large cap funds. At some point of time, percentage

of the active managers outperforms passive funds, however, the investors’ faces challenges

for their ability to identify the ones that will do so over long-term (Degutis & Novickytė,

2014). Following points describes relevance of EMH in clear way:

Mergers & Acquisitions

In correct securities price, its purchasing would be consists of zero transaction of the

NPV. If this statement is true then the principles following mergers as well as takeovers

would be questioned. If company’s acquisition is at its exact equity’s value then it has to be

relied upon the synergy in economies of the scale for saving purpose (Urquhart &

McGroarty, 2016).

Timing of the Financial Policy

The timing plays important role in capital market and stock prices. It has been

argued that there is wrong and correct timing in issuing new securities. If marketer is efficient

but prices of securities is difficult to determine then it becomes tough for the financial

the larger families of multi-fund and the fund charges lower ratios of expenses (Dragotă &

Ţilică, 2014). The proponents of EMH concludes that due to market randomness, the

investors can do better with the help of investing in passive and low cost portfolios. For

instance, data compiled by the Morningstar in June 2019 Passive or Active Barometer study

has supported EMH. It compared returns of active managers in all the categories against

combined made of exchange-traded funds and related index funds (Rossi, 2015). This study

has found that over beginning of ten year period, only twenty-third percent of the active

managers were having ability for outperforming their passive peers. The rates of better

success were found in foreign bonds funds and equity funds (Dragota & Oprea, 2014). The

lower rates off success were found in the large cap funds. At some point of time, percentage

of the active managers outperforms passive funds, however, the investors’ faces challenges

for their ability to identify the ones that will do so over long-term (Degutis & Novickytė,

2014). Following points describes relevance of EMH in clear way:

Mergers & Acquisitions

In correct securities price, its purchasing would be consists of zero transaction of the

NPV. If this statement is true then the principles following mergers as well as takeovers

would be questioned. If company’s acquisition is at its exact equity’s value then it has to be

relied upon the synergy in economies of the scale for saving purpose (Urquhart &

McGroarty, 2016).

Timing of the Financial Policy

The timing plays important role in capital market and stock prices. It has been

argued that there is wrong and correct timing in issuing new securities. If marketer is efficient

but prices of securities is difficult to determine then it becomes tough for the financial

8ADVANCED GLOBAL FINANCIAL MANAGEMENT

managers to conclude on the particular day that whether prices of securities would be high or

low (Bahmani-Oskooee et al. 2016).

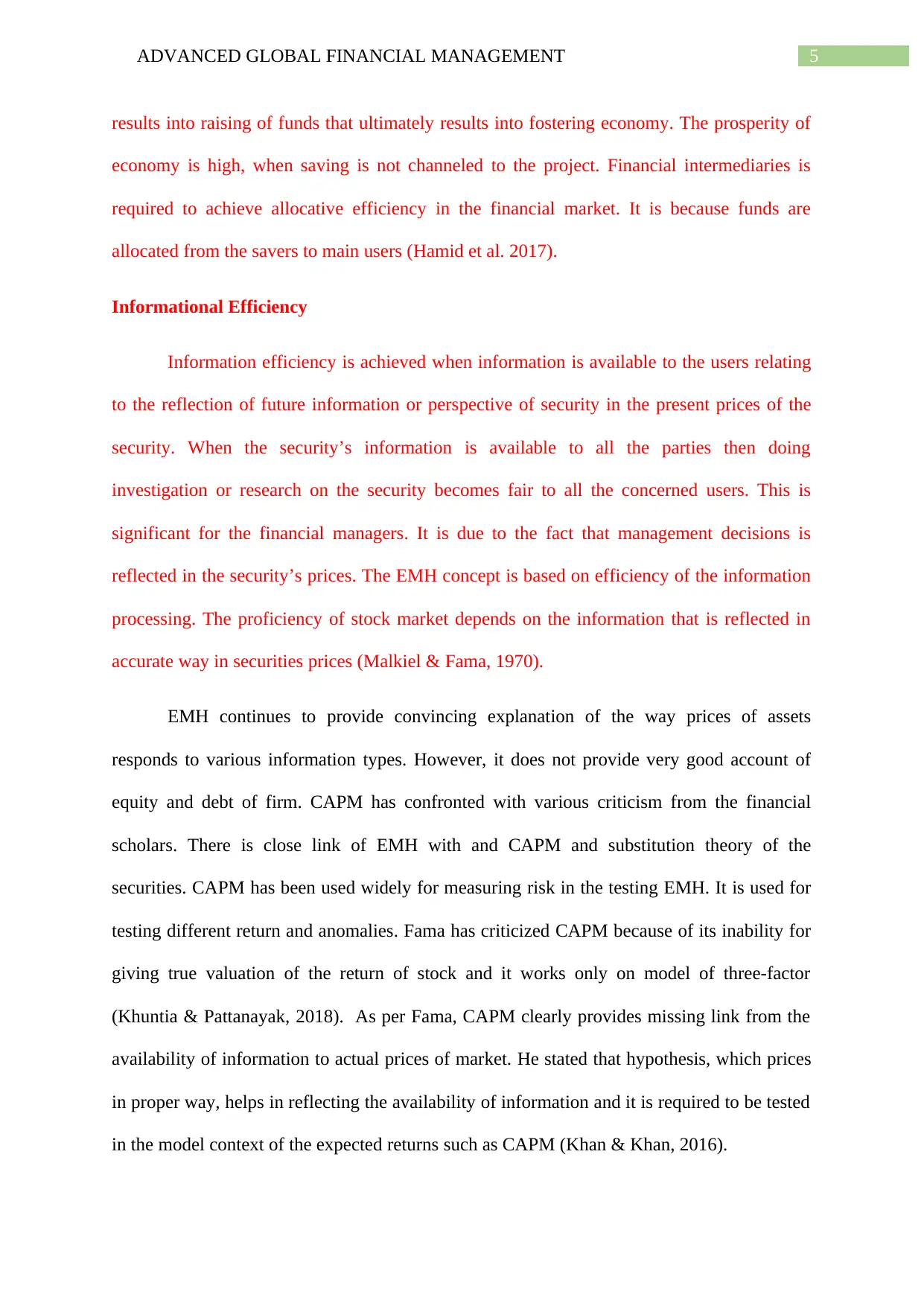

Creative Accounting

The prices of the securities are based on present value of expected cash flow of future

in efficient market. Further, securities price reflects availability of all current information to

users. This means that those organizations listed on the stock exchange do not make any

attempt to distort information as this is reflected in the stock of entity.

Evaluating Project on the basis of NPV

The financial manager evaluates the new investments by using securities required rate

of return that are traded in capital market. It is based on assumption that if there is efficient

market then assets pricing is based on risk that can be beard by them. In contrary to this, if

there is market inefficiencies then appraisal of project may get wrong by financial managers

due to unreliable NPV estimate (Malkiel & Fama, 1970).

Conclusion

Hence, this paper concludes that EMH is the theory that helps in describing

relationship in between prices of security and information. This hypothesis states that prices

of stock reflect all information available and it exactly trades at their fair value all times.

Therefore, it includes consistently choosing of stocks, which will beat return of overall

managers to conclude on the particular day that whether prices of securities would be high or

low (Bahmani-Oskooee et al. 2016).

Creative Accounting

The prices of the securities are based on present value of expected cash flow of future

in efficient market. Further, securities price reflects availability of all current information to

users. This means that those organizations listed on the stock exchange do not make any

attempt to distort information as this is reflected in the stock of entity.

Evaluating Project on the basis of NPV

The financial manager evaluates the new investments by using securities required rate

of return that are traded in capital market. It is based on assumption that if there is efficient

market then assets pricing is based on risk that can be beard by them. In contrary to this, if

there is market inefficiencies then appraisal of project may get wrong by financial managers

due to unreliable NPV estimate (Malkiel & Fama, 1970).

Conclusion

Hence, this paper concludes that EMH is the theory that helps in describing

relationship in between prices of security and information. This hypothesis states that prices

of stock reflect all information available and it exactly trades at their fair value all times.

Therefore, it includes consistently choosing of stocks, which will beat return of overall

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ADVANCED GLOBAL FINANCIAL MANAGEMENT

market of stock. Further, it has been explained in this paper that EMH comes in three forms,

which are known as “weak form”, “semi-strong form” and “strong form”. This theory

concludes that the stocks trade always at its fair market value. Hence, it is not possible

virtually for either buying undervalued stock at bargain or selling the overvalued stocks for

the extra profits. In addition, it can be said that there are more exposure of corporate

managers to the EMH, which helps in providing greater prosperity for managing funds.

market of stock. Further, it has been explained in this paper that EMH comes in three forms,

which are known as “weak form”, “semi-strong form” and “strong form”. This theory

concludes that the stocks trade always at its fair market value. Hence, it is not possible

virtually for either buying undervalued stock at bargain or selling the overvalued stocks for

the extra profits. In addition, it can be said that there are more exposure of corporate

managers to the EMH, which helps in providing greater prosperity for managing funds.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ADVANCED GLOBAL FINANCIAL MANAGEMENT

Reference

Bahmani-Oskooee, M., Chang, T., Chen, T. H., & Tzeng, H. W. (2016). Revisiting the

efficient market hypothesis in transition countries using quantile unit root

test. Economics Bulletin, 36(4), 2171-2182.

Degutis, A., & Novickytė, L. (2014). The efficient market hypothesis: A critical review of

literature and methodology. Ekonomika, 93, 7-23.

Dragota, V., & Oprea, D. S. (2014). Informational efficiency tests on the Romanian stock

market: a review of the literature. The Review of Finance and Banking, 6(1).

Dragotă, V., & Ţilică, E. V. (2014). Market efficiency of the Post Communist East European

stock markets. Central European Journal of Operations Research, 22(2), 307-337.

Fama, E. F., Fisher, L., Jensen, M. C., & Roll, R. (1969). The adjustment of stock prices to

new information. International economic review, 10(1), 1-21.

Gabriela ğiĠan, A. (2015). The efficient market hypothesis: Review of specialized literature

and empirical research. Procedia Economics and Finance, 32, 442-449.

Hamid, K., Suleman, M. T., Ali Shah, S. Z., Akash, I., & Shahid, R. (2017). Testing the weak

form of efficient market hypothesis: Empirical evidence from Asia-Pacific

markets. Available at SSRN 2912908.

Jovanovic, F., Andreadakis, S., & Schinckus, C. (2016). Efficient market hypothesis and

fraud on the market theory a new perspective for class actions. Research in

International Business and Finance, 38, 177-190.

Kamal, M. (2014). Studying the validity of the Efficient Market Hypothesis (EMH) in the

Egyptian exchange (EGX) after the 25th of January revolution.

Reference

Bahmani-Oskooee, M., Chang, T., Chen, T. H., & Tzeng, H. W. (2016). Revisiting the

efficient market hypothesis in transition countries using quantile unit root

test. Economics Bulletin, 36(4), 2171-2182.

Degutis, A., & Novickytė, L. (2014). The efficient market hypothesis: A critical review of

literature and methodology. Ekonomika, 93, 7-23.

Dragota, V., & Oprea, D. S. (2014). Informational efficiency tests on the Romanian stock

market: a review of the literature. The Review of Finance and Banking, 6(1).

Dragotă, V., & Ţilică, E. V. (2014). Market efficiency of the Post Communist East European

stock markets. Central European Journal of Operations Research, 22(2), 307-337.

Fama, E. F., Fisher, L., Jensen, M. C., & Roll, R. (1969). The adjustment of stock prices to

new information. International economic review, 10(1), 1-21.

Gabriela ğiĠan, A. (2015). The efficient market hypothesis: Review of specialized literature

and empirical research. Procedia Economics and Finance, 32, 442-449.

Hamid, K., Suleman, M. T., Ali Shah, S. Z., Akash, I., & Shahid, R. (2017). Testing the weak

form of efficient market hypothesis: Empirical evidence from Asia-Pacific

markets. Available at SSRN 2912908.

Jovanovic, F., Andreadakis, S., & Schinckus, C. (2016). Efficient market hypothesis and

fraud on the market theory a new perspective for class actions. Research in

International Business and Finance, 38, 177-190.

Kamal, M. (2014). Studying the validity of the Efficient Market Hypothesis (EMH) in the

Egyptian exchange (EGX) after the 25th of January revolution.

11ADVANCED GLOBAL FINANCIAL MANAGEMENT

Kelikume, I. (2016). New evidence from the efficient market hypothesis for the Nigerian

stock index using the wavelet unit root test approach. The Journal of Developing

Areas, 50(5), 185-197.

Khan, N. U., & Khan, S. (2016). Weak Form of Efficient Market Hypothesis â?? Evidence

from Pakistan. Business & Economic Review, 8(SE), 1-18.

Khuntia, S., & Pattanayak, J. K. (2018). Adaptive market hypothesis and evolving

predictability of bitcoin. Economics Letters, 167, 26-28.

Malkiel, B. G., & Fama, E. F. (1970). Efficient capital markets: A review of theory and

empirical work. The journal of Finance, 25(2), 383-417.

Manasseh, C. O. (2016). Efficient Market Hypothesis (Emh) and Nigerian Capital Market: an

Analysis of Bonus Issues and Dividend Announcement (Doctoral dissertation).

Naseer, M., & Bin Tariq, Y. (2015). The efficient market hypothesis: A critical review of the

literature. IUP Journal of Financial Risk Management, 12(4), 48-63.

Noda, A. (2016). A test of the adaptive market hypothesis using a time-varying AR model in

Japan. Finance Research Letters, 17, 66-71.

Rossi, M. (2015). The efficient market hypothesis and calendar anomalies: a literature

review. International Journal of Managerial and Financial Accounting, 7(3-4), 285-

296.

Urquhart, A., & McGroarty, F. (2016). Are stock markets really efficient? Evidence of the

adaptive market hypothesis. International Review of Financial Analysis, 47, 39-49.

Kelikume, I. (2016). New evidence from the efficient market hypothesis for the Nigerian

stock index using the wavelet unit root test approach. The Journal of Developing

Areas, 50(5), 185-197.

Khan, N. U., & Khan, S. (2016). Weak Form of Efficient Market Hypothesis â?? Evidence

from Pakistan. Business & Economic Review, 8(SE), 1-18.

Khuntia, S., & Pattanayak, J. K. (2018). Adaptive market hypothesis and evolving

predictability of bitcoin. Economics Letters, 167, 26-28.

Malkiel, B. G., & Fama, E. F. (1970). Efficient capital markets: A review of theory and

empirical work. The journal of Finance, 25(2), 383-417.

Manasseh, C. O. (2016). Efficient Market Hypothesis (Emh) and Nigerian Capital Market: an

Analysis of Bonus Issues and Dividend Announcement (Doctoral dissertation).

Naseer, M., & Bin Tariq, Y. (2015). The efficient market hypothesis: A critical review of the

literature. IUP Journal of Financial Risk Management, 12(4), 48-63.

Noda, A. (2016). A test of the adaptive market hypothesis using a time-varying AR model in

Japan. Finance Research Letters, 17, 66-71.

Rossi, M. (2015). The efficient market hypothesis and calendar anomalies: a literature

review. International Journal of Managerial and Financial Accounting, 7(3-4), 285-

296.

Urquhart, A., & McGroarty, F. (2016). Are stock markets really efficient? Evidence of the

adaptive market hypothesis. International Review of Financial Analysis, 47, 39-49.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.