Advanced Investment Management Project: Portfolio Analysis, BANK5030

VerifiedAdded on 2022/09/14

|13

|2827

|10

Project

AI Summary

This project delves into the intricacies of advanced investment management, beginning with detailed calculations and analysis of portfolio returns, standard deviations, and covariances for assets X and Y. The analysis extends to constructing various portfolios with different weightings in the two assets, calculating their expected returns and standard deviations, and plotting these relationships to identify the efficient frontier. The project then proceeds to determine the global minimum-variance portfolio. The discussion section evaluates the advice of two financial professionals, Anne and Paul, regarding investment strategies and diversification. The project concludes with an examination of Exchange Traded Funds (ETFs), assessing their significance as product innovations and their impact on market efficiency, highlighting their role in providing investors with a diversified and accessible investment tool, and assessing their impact on market efficiency and investor strategies.

Running head: ADVANCED INVESTMENT MANAGEMENT

Advanced Investment Management

Student Name:

Student Number:

Authors Note:

Advanced Investment Management

Student Name:

Student Number:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED INVESTMENT MANAGEMENT

Table of Contents

SECTION ONE: Calculations and Analysis:.............................................................................2

A. Calculating the expected return and standard deviation for the returns of each asset:.........2

B. Calculating the covariance between the returns of asset X and asset Y:...............................2

C. Completing the table below for the mean and standard deviation of the given portfolios:...2

D. Discussing the relevant results:.............................................................................................3

E. Using the chart formats provided in the appendix, sketch the following relationships:........3

F. Discussing the plots:..............................................................................................................4

G. Identifying the portfolios that are efficient:..........................................................................5

H. Calculating the global minimum-variance portfolio:............................................................5

I. Calculating the expected return and the standard deviation of the minimum-variance

portfolio:.....................................................................................................................................5

SECTION TWO: Discussions:..................................................................................................6

A. Indicating whether the relevant agreement is with Anne while giving relevant reasons in

detail:..........................................................................................................................................6

B. Indicating whether the relevant agreement is with Paul while giving relevant reasons in

detail:..........................................................................................................................................7

SECTION THREE: Analysis and Discussion:..........................................................................9

References:...............................................................................................................................12

Table of Contents

SECTION ONE: Calculations and Analysis:.............................................................................2

A. Calculating the expected return and standard deviation for the returns of each asset:.........2

B. Calculating the covariance between the returns of asset X and asset Y:...............................2

C. Completing the table below for the mean and standard deviation of the given portfolios:...2

D. Discussing the relevant results:.............................................................................................3

E. Using the chart formats provided in the appendix, sketch the following relationships:........3

F. Discussing the plots:..............................................................................................................4

G. Identifying the portfolios that are efficient:..........................................................................5

H. Calculating the global minimum-variance portfolio:............................................................5

I. Calculating the expected return and the standard deviation of the minimum-variance

portfolio:.....................................................................................................................................5

SECTION TWO: Discussions:..................................................................................................6

A. Indicating whether the relevant agreement is with Anne while giving relevant reasons in

detail:..........................................................................................................................................6

B. Indicating whether the relevant agreement is with Paul while giving relevant reasons in

detail:..........................................................................................................................................7

SECTION THREE: Analysis and Discussion:..........................................................................9

References:...............................................................................................................................12

ADVANCED INVESTMENT MANAGEMENT

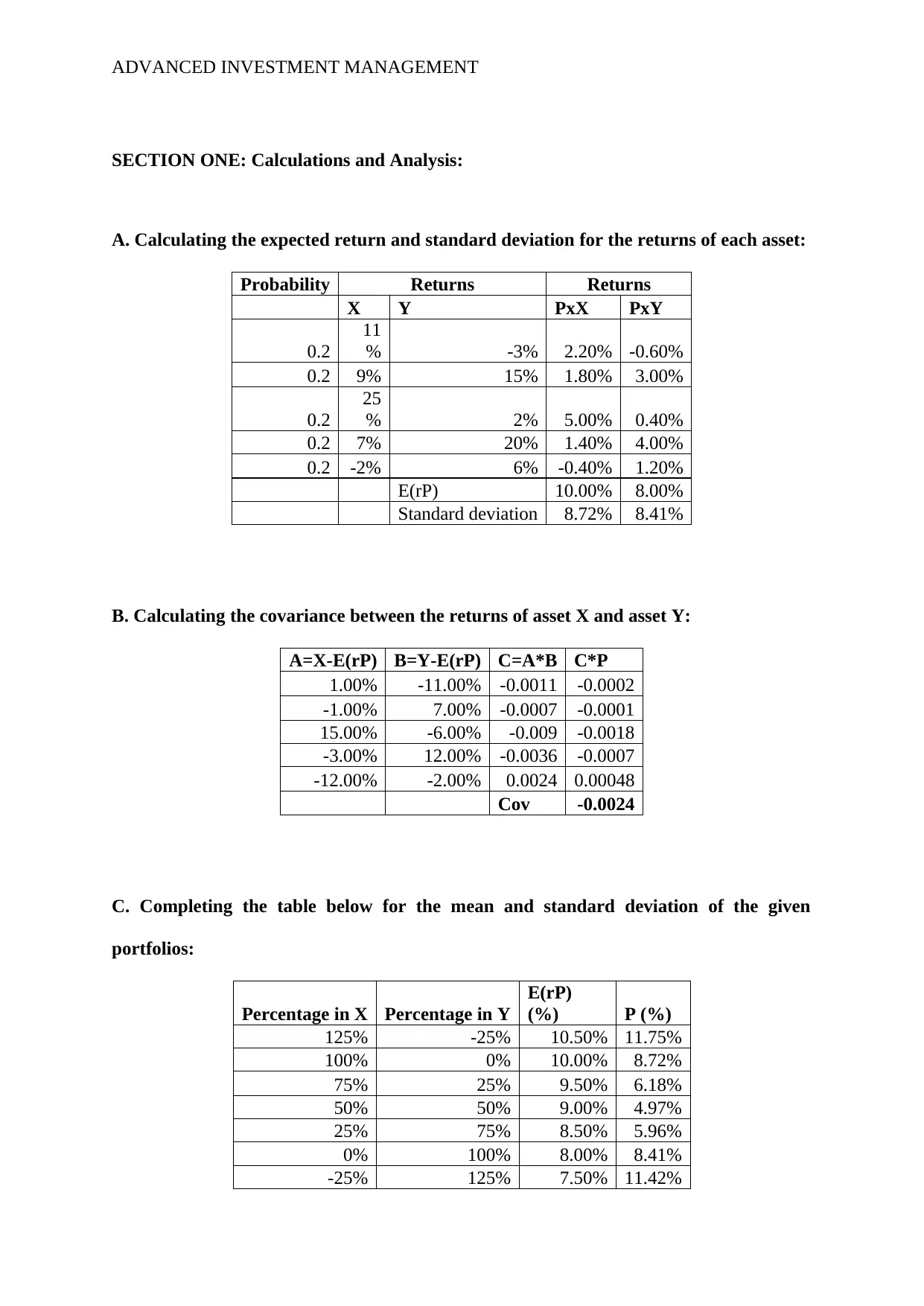

SECTION ONE: Calculations and Analysis:

A. Calculating the expected return and standard deviation for the returns of each asset:

Probability Returns Returns

X Y PxX PxY

0.2

11

% -3% 2.20% -0.60%

0.2 9% 15% 1.80% 3.00%

0.2

25

% 2% 5.00% 0.40%

0.2 7% 20% 1.40% 4.00%

0.2 -2% 6% -0.40% 1.20%

E(rP) 10.00% 8.00%

Standard deviation 8.72% 8.41%

B. Calculating the covariance between the returns of asset X and asset Y:

A=X-E(rP) B=Y-E(rP) C=A*B C*P

1.00% -11.00% -0.0011 -0.0002

-1.00% 7.00% -0.0007 -0.0001

15.00% -6.00% -0.009 -0.0018

-3.00% 12.00% -0.0036 -0.0007

-12.00% -2.00% 0.0024 0.00048

Cov -0.0024

C. Completing the table below for the mean and standard deviation of the given

portfolios:

Percentage in X Percentage in Y

E(rP)

(%) P (%)

125% -25% 10.50% 11.75%

100% 0% 10.00% 8.72%

75% 25% 9.50% 6.18%

50% 50% 9.00% 4.97%

25% 75% 8.50% 5.96%

0% 100% 8.00% 8.41%

-25% 125% 7.50% 11.42%

SECTION ONE: Calculations and Analysis:

A. Calculating the expected return and standard deviation for the returns of each asset:

Probability Returns Returns

X Y PxX PxY

0.2

11

% -3% 2.20% -0.60%

0.2 9% 15% 1.80% 3.00%

0.2

25

% 2% 5.00% 0.40%

0.2 7% 20% 1.40% 4.00%

0.2 -2% 6% -0.40% 1.20%

E(rP) 10.00% 8.00%

Standard deviation 8.72% 8.41%

B. Calculating the covariance between the returns of asset X and asset Y:

A=X-E(rP) B=Y-E(rP) C=A*B C*P

1.00% -11.00% -0.0011 -0.0002

-1.00% 7.00% -0.0007 -0.0001

15.00% -6.00% -0.009 -0.0018

-3.00% 12.00% -0.0036 -0.0007

-12.00% -2.00% 0.0024 0.00048

Cov -0.0024

C. Completing the table below for the mean and standard deviation of the given

portfolios:

Percentage in X Percentage in Y

E(rP)

(%) P (%)

125% -25% 10.50% 11.75%

100% 0% 10.00% 8.72%

75% 25% 9.50% 6.18%

50% 50% 9.00% 4.97%

25% 75% 8.50% 5.96%

0% 100% 8.00% 8.41%

-25% 125% 7.50% 11.42%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ADVANCED INVESTMENT MANAGEMENT

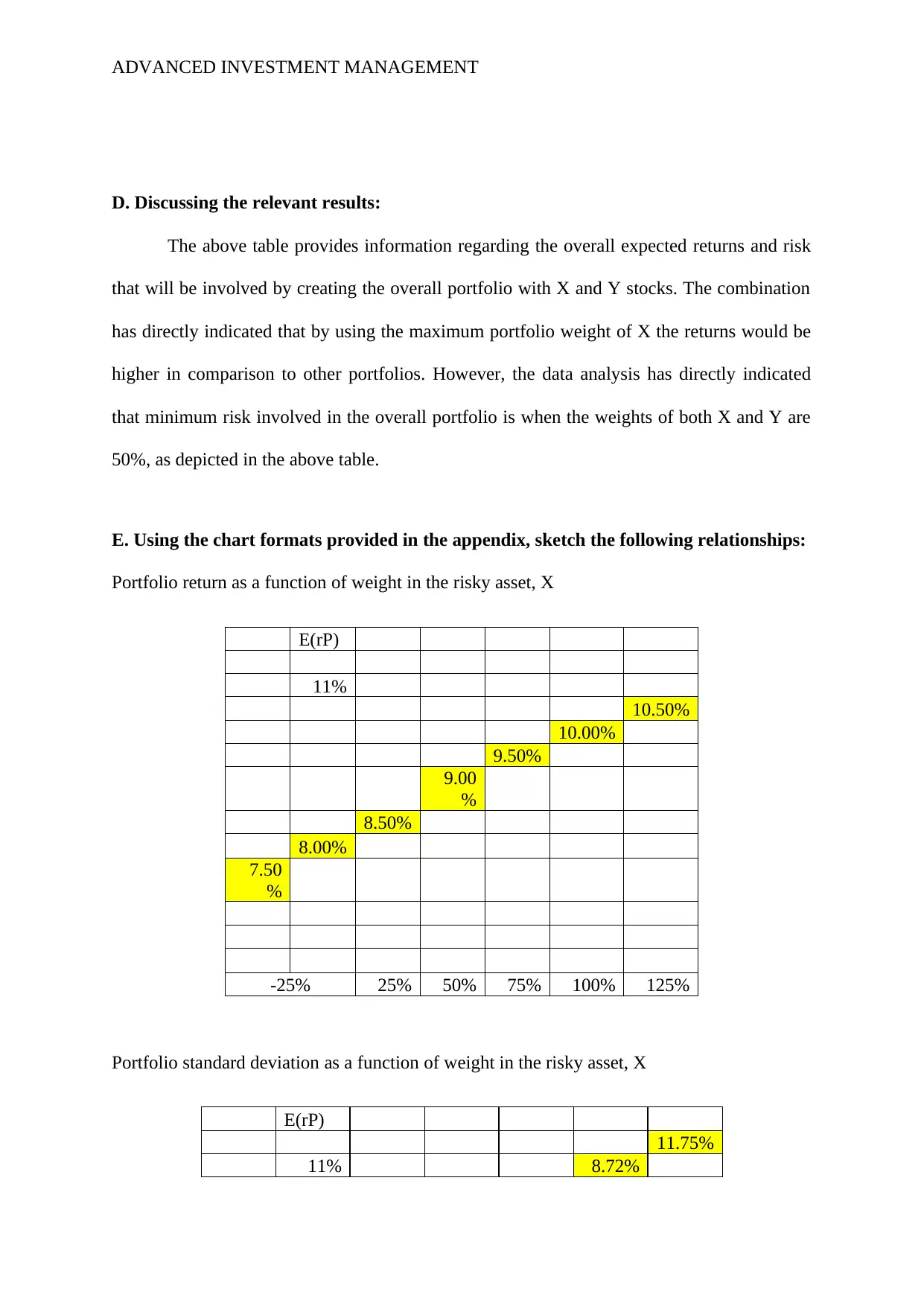

D. Discussing the relevant results:

The above table provides information regarding the overall expected returns and risk

that will be involved by creating the overall portfolio with X and Y stocks. The combination

has directly indicated that by using the maximum portfolio weight of X the returns would be

higher in comparison to other portfolios. However, the data analysis has directly indicated

that minimum risk involved in the overall portfolio is when the weights of both X and Y are

50%, as depicted in the above table.

E. Using the chart formats provided in the appendix, sketch the following relationships:

Portfolio return as a function of weight in the risky asset, X

E(rP)

11%

10.50%

10.00%

9.50%

9.00

%

8.50%

8.00%

7.50

%

-25% 25% 50% 75% 100% 125%

Portfolio standard deviation as a function of weight in the risky asset, X

E(rP)

11.75%

11% 8.72%

D. Discussing the relevant results:

The above table provides information regarding the overall expected returns and risk

that will be involved by creating the overall portfolio with X and Y stocks. The combination

has directly indicated that by using the maximum portfolio weight of X the returns would be

higher in comparison to other portfolios. However, the data analysis has directly indicated

that minimum risk involved in the overall portfolio is when the weights of both X and Y are

50%, as depicted in the above table.

E. Using the chart formats provided in the appendix, sketch the following relationships:

Portfolio return as a function of weight in the risky asset, X

E(rP)

11%

10.50%

10.00%

9.50%

9.00

%

8.50%

8.00%

7.50

%

-25% 25% 50% 75% 100% 125%

Portfolio standard deviation as a function of weight in the risky asset, X

E(rP)

11.75%

11% 8.72%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

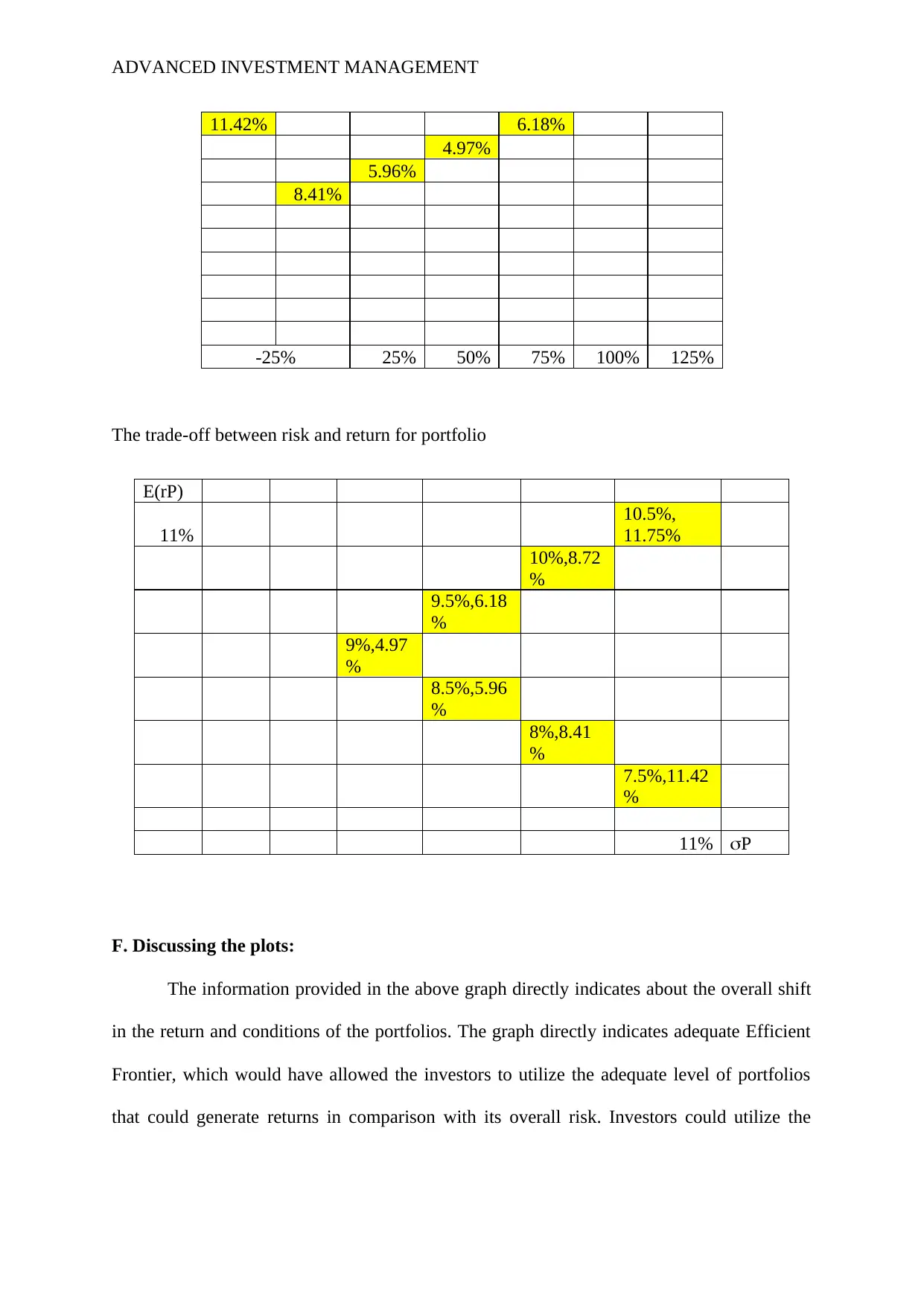

ADVANCED INVESTMENT MANAGEMENT

11.42% 6.18%

4.97%

5.96%

8.41%

-25% 25% 50% 75% 100% 125%

The trade-off between risk and return for portfolio

E(rP)

11%

10.5%,

11.75%

10%,8.72

%

9.5%,6.18

%

9%,4.97

%

8.5%,5.96

%

8%,8.41

%

7.5%,11.42

%

11% P

F. Discussing the plots:

The information provided in the above graph directly indicates about the overall shift

in the return and conditions of the portfolios. The graph directly indicates adequate Efficient

Frontier, which would have allowed the investors to utilize the adequate level of portfolios

that could generate returns in comparison with its overall risk. Investors could utilize the

11.42% 6.18%

4.97%

5.96%

8.41%

-25% 25% 50% 75% 100% 125%

The trade-off between risk and return for portfolio

E(rP)

11%

10.5%,

11.75%

10%,8.72

%

9.5%,6.18

%

9%,4.97

%

8.5%,5.96

%

8%,8.41

%

7.5%,11.42

%

11% P

F. Discussing the plots:

The information provided in the above graph directly indicates about the overall shift

in the return and conditions of the portfolios. The graph directly indicates adequate Efficient

Frontier, which would have allowed the investors to utilize the adequate level of portfolios

that could generate returns in comparison with its overall risk. Investors could utilize the

ADVANCED INVESTMENT MANAGEMENT

information depicted in the above chart to make relevant investment decisions, which support

their investment rationale.

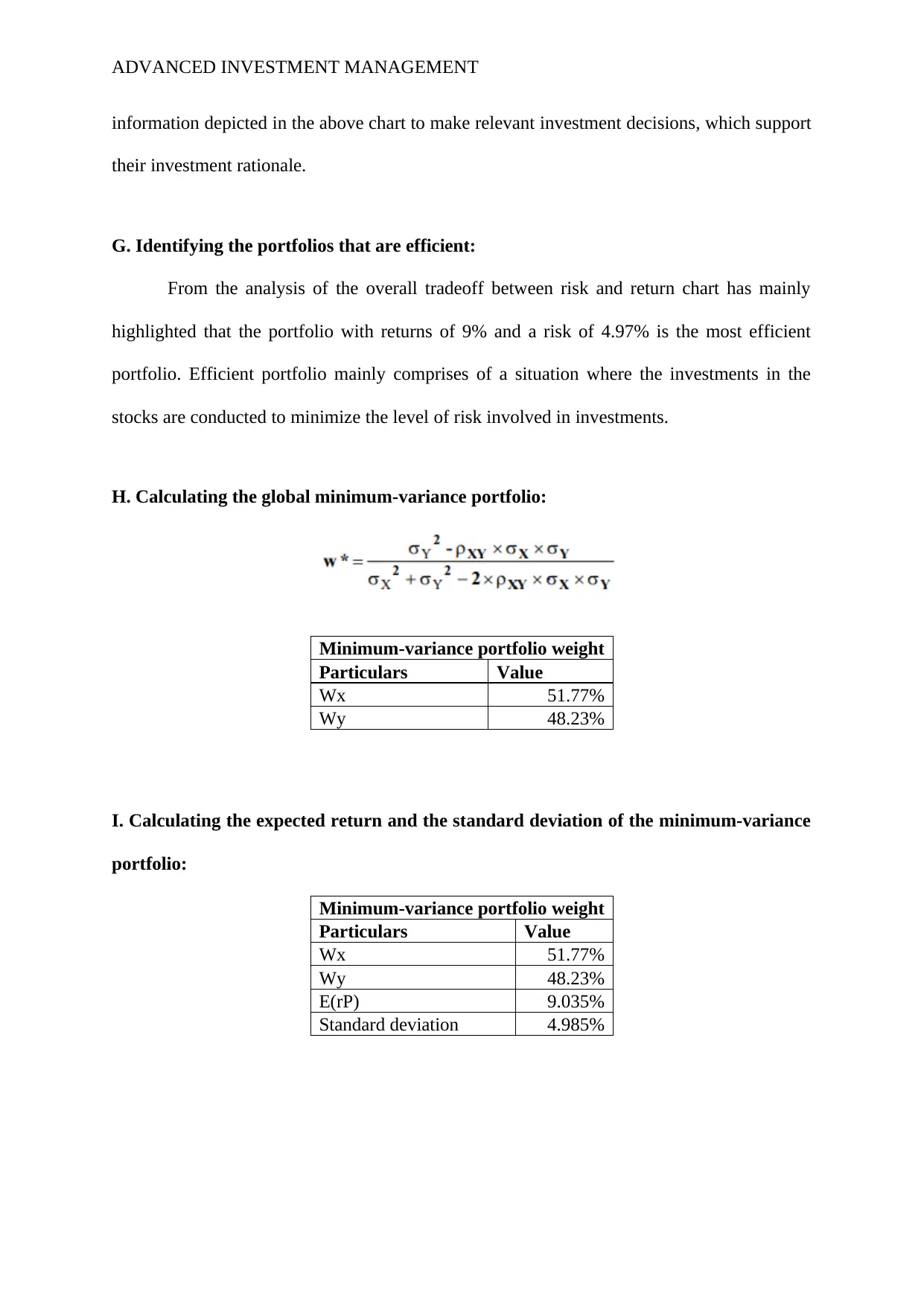

G. Identifying the portfolios that are efficient:

From the analysis of the overall tradeoff between risk and return chart has mainly

highlighted that the portfolio with returns of 9% and a risk of 4.97% is the most efficient

portfolio. Efficient portfolio mainly comprises of a situation where the investments in the

stocks are conducted to minimize the level of risk involved in investments.

H. Calculating the global minimum-variance portfolio:

Minimum-variance portfolio weight

Particulars Value

Wx 51.77%

Wy 48.23%

I. Calculating the expected return and the standard deviation of the minimum-variance

portfolio:

Minimum-variance portfolio weight

Particulars Value

Wx 51.77%

Wy 48.23%

E(rP) 9.035%

Standard deviation 4.985%

information depicted in the above chart to make relevant investment decisions, which support

their investment rationale.

G. Identifying the portfolios that are efficient:

From the analysis of the overall tradeoff between risk and return chart has mainly

highlighted that the portfolio with returns of 9% and a risk of 4.97% is the most efficient

portfolio. Efficient portfolio mainly comprises of a situation where the investments in the

stocks are conducted to minimize the level of risk involved in investments.

H. Calculating the global minimum-variance portfolio:

Minimum-variance portfolio weight

Particulars Value

Wx 51.77%

Wy 48.23%

I. Calculating the expected return and the standard deviation of the minimum-variance

portfolio:

Minimum-variance portfolio weight

Particulars Value

Wx 51.77%

Wy 48.23%

E(rP) 9.035%

Standard deviation 4.985%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ADVANCED INVESTMENT MANAGEMENT

SECTION TWO: Discussions:

A. Indicating whether the relevant agreement is with Anne while giving relevant

reasons in detail:

The information that was provided by Anne was not correct, as the safe investment is

not necessarily the best for any given client. The risk assessment needs to be conducted on

the proper client to identify the measures and future expectations. The recipe that she said

was related with not appropriate for oil fields of investors as the investments are conducted

on the basis of investment types, which ranges from conservative investors, aggressive

investors and moderate investors. The different types of investment risk are relatively

detected due to the aggressiveness or conservativeness of the investors, as the investors tend

to raise the level of risk to acquire assets that could generate the highest level of returns from

investment. The detail that was given by Anne was not adequate, as the safest investment is

not appropriate for the investors if they want to generate high level of returns.

The information provided by Anne was not related to the investment theory in which

the overall decision for risk and return approach has been described. Risk and return decision

for the client is relatively conducted through adequate questionnaires and assessment of their

risk supporting activities. Investors are relatively provided with an adequate question that has

relevant information leading towards the determination of the type of risk that the investor is

supportive to (Yang, Narayanan and De 2014). Employees of an investment management

firm can adequately determine the risk, return attributes that are demanded by the investors,

and create the port for you that is most suitable for their investment needs. The investment

theory is mainly a concept that is based on the consideration of different factors associated

with the process of investing which allows the investors to choose adequate investment

options that can support their portfolio creation process.

SECTION TWO: Discussions:

A. Indicating whether the relevant agreement is with Anne while giving relevant

reasons in detail:

The information that was provided by Anne was not correct, as the safe investment is

not necessarily the best for any given client. The risk assessment needs to be conducted on

the proper client to identify the measures and future expectations. The recipe that she said

was related with not appropriate for oil fields of investors as the investments are conducted

on the basis of investment types, which ranges from conservative investors, aggressive

investors and moderate investors. The different types of investment risk are relatively

detected due to the aggressiveness or conservativeness of the investors, as the investors tend

to raise the level of risk to acquire assets that could generate the highest level of returns from

investment. The detail that was given by Anne was not adequate, as the safest investment is

not appropriate for the investors if they want to generate high level of returns.

The information provided by Anne was not related to the investment theory in which

the overall decision for risk and return approach has been described. Risk and return decision

for the client is relatively conducted through adequate questionnaires and assessment of their

risk supporting activities. Investors are relatively provided with an adequate question that has

relevant information leading towards the determination of the type of risk that the investor is

supportive to (Yang, Narayanan and De 2014). Employees of an investment management

firm can adequately determine the risk, return attributes that are demanded by the investors,

and create the port for you that is most suitable for their investment needs. The investment

theory is mainly a concept that is based on the consideration of different factors associated

with the process of investing which allows the investors to choose adequate investment

options that can support their portfolio creation process.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED INVESTMENT MANAGEMENT

Thus, ignoring the recipe of any would be more preferable for an employee of an

investment management firm as there would be different clients that would require a high

level of returns for a moderate level of returns, which cannot be supported with a safest

investment type portfolio. Therefore, adequate investment theory measures need to be

followed while preparing the portfolio for the investors and clients. This would help in

creating the appropriate level of portfolio, which supports the investment risk and return

attributes of the investors (Lee and Kang 2015).

B. Indicating whether the relevant agreement is with Paul while giving relevant reasons

in detail:

The information provided by the manager Paul was also not adequate as he directly

instigated that diversification is important but it is not complicated. Moreover, he also stated

that by simply combining a large number of different stocks together to create a portfolio

could actually help in diversifying the overall investment. The statement made by Paul is not

adequate, as the diversification process is complicated and needs adequate attention of the

investors during the preparation of the portfolio with diversified stocks. The diversification of

a portfolio is only achieved when adequate measures are taken to detect the level of

correlation between the returns generated by the stocks within the portfolio. The

diversification process enables the investors to mitigate the risk conditions that are hampering

the overall portfolio and generate adequate level of returns in the process (Briere, Oosterlinck

and Szafarz 2015). The method is not simple and needs to be conducted with rigorous

calculations and assumptions regarding the future conditions of the overall stocks that are

being used in the portfolio.

The diversification process mainly comprises of relevant asset allocation in a way that

reduces the risk exposure of one particular stock. The diversification process enables the

Thus, ignoring the recipe of any would be more preferable for an employee of an

investment management firm as there would be different clients that would require a high

level of returns for a moderate level of returns, which cannot be supported with a safest

investment type portfolio. Therefore, adequate investment theory measures need to be

followed while preparing the portfolio for the investors and clients. This would help in

creating the appropriate level of portfolio, which supports the investment risk and return

attributes of the investors (Lee and Kang 2015).

B. Indicating whether the relevant agreement is with Paul while giving relevant reasons

in detail:

The information provided by the manager Paul was also not adequate as he directly

instigated that diversification is important but it is not complicated. Moreover, he also stated

that by simply combining a large number of different stocks together to create a portfolio

could actually help in diversifying the overall investment. The statement made by Paul is not

adequate, as the diversification process is complicated and needs adequate attention of the

investors during the preparation of the portfolio with diversified stocks. The diversification of

a portfolio is only achieved when adequate measures are taken to detect the level of

correlation between the returns generated by the stocks within the portfolio. The

diversification process enables the investors to mitigate the risk conditions that are hampering

the overall portfolio and generate adequate level of returns in the process (Briere, Oosterlinck

and Szafarz 2015). The method is not simple and needs to be conducted with rigorous

calculations and assumptions regarding the future conditions of the overall stocks that are

being used in the portfolio.

The diversification process mainly comprises of relevant asset allocation in a way that

reduces the risk exposure of one particular stock. The diversification process enables the

ADVANCED INVESTMENT MANAGEMENT

investors to mitigate the risk levels of a particular stock and create an investment scope that

could reduce the unexpected volatility of the capital market on the return generation

capability of the portfolio. The diversification process is relatively conducted with the help of

correlation, variance and weights of the different portfolio. There are adequate diversifiable

and non-diversifiable risks that need to be accommodated within the portfolio to identify the

overall risk involved in investment. Furthermore, the diversification process relatively utilizes

the different types of assets in a particular portfolio, as it helps the investors to spread wealth,

consider bond funds, and utilize risk-free assets (Marvin 2015).

The information provided by the manager Paul is relatively not appropriate, as the

diversification process is a lengthy endeavor, which requires adequate position and

calculation to derive the portfolio that would support the diversification conditions of the

investor. Therefore, the information that was provided by Paul cannot be used while creating

a portfolio for the investors, as it will not adequately create the investment exposure that is

required in the diversified portfolio.

investors to mitigate the risk levels of a particular stock and create an investment scope that

could reduce the unexpected volatility of the capital market on the return generation

capability of the portfolio. The diversification process is relatively conducted with the help of

correlation, variance and weights of the different portfolio. There are adequate diversifiable

and non-diversifiable risks that need to be accommodated within the portfolio to identify the

overall risk involved in investment. Furthermore, the diversification process relatively utilizes

the different types of assets in a particular portfolio, as it helps the investors to spread wealth,

consider bond funds, and utilize risk-free assets (Marvin 2015).

The information provided by the manager Paul is relatively not appropriate, as the

diversification process is a lengthy endeavor, which requires adequate position and

calculation to derive the portfolio that would support the diversification conditions of the

investor. Therefore, the information that was provided by Paul cannot be used while creating

a portfolio for the investors, as it will not adequately create the investment exposure that is

required in the diversified portfolio.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ADVANCED INVESTMENT MANAGEMENT

SECTION THREE: Analysis and Discussion:

The exchange-traded fund is relatively considered a collection of securities that

adequately tracks and underlying index. The exchange-traded fund is considered to be one of

the best-known investment options that have been created for the investors who can buy bulk

stocks and reduce the level of commissions on the particular investment. The ETFs are

relatively considered an adequate investment mechanism that allows the investors to invest

directly on different investment types such as commodities, stocks and bonds or a mixture of

all. The ETFs relatively offers low expense ratio in comparison to the buying of individual

stocks. Furthermore, with the help of the investors are able to sell and buy the stocks on a

particular time of a day as the prices fluctuate all day long and are not restricted as the mutual

fund's valuation, which is conducted only after the market close (Petajisto 2017). The ETFs

provide adequate advantage and opportunity to the investors regarding the buying and selling

of shares on daily basis without any hindrance or blockage of any type. Moreover, it is also

considered to be a combination of multiple underlying assets, which can allow the investors

to adequately diversify the investments on a single trade.

ETFs are a significant product innovation:

The above statement regarding the ETA being a significant product innovation is

relatively true. Investors after the creation of the ETFs were able to adequately utilize the

investment opportunity and diversify the investments on a single trade. Moreover, the

investors were provided with adequate opportunity to sell and by the stock within the trading

event and not wait like the mutual funds at the end of the day to detect the actual value of the

investment. This exposure relatively helps the ETFs to acquire additional investments and is

considered a significant product innovation, which allows the investors to adequately invest

in an instrument that underlines a particular index. The investment scope allows investors to

SECTION THREE: Analysis and Discussion:

The exchange-traded fund is relatively considered a collection of securities that

adequately tracks and underlying index. The exchange-traded fund is considered to be one of

the best-known investment options that have been created for the investors who can buy bulk

stocks and reduce the level of commissions on the particular investment. The ETFs are

relatively considered an adequate investment mechanism that allows the investors to invest

directly on different investment types such as commodities, stocks and bonds or a mixture of

all. The ETFs relatively offers low expense ratio in comparison to the buying of individual

stocks. Furthermore, with the help of the investors are able to sell and buy the stocks on a

particular time of a day as the prices fluctuate all day long and are not restricted as the mutual

fund's valuation, which is conducted only after the market close (Petajisto 2017). The ETFs

provide adequate advantage and opportunity to the investors regarding the buying and selling

of shares on daily basis without any hindrance or blockage of any type. Moreover, it is also

considered to be a combination of multiple underlying assets, which can allow the investors

to adequately diversify the investments on a single trade.

ETFs are a significant product innovation:

The above statement regarding the ETA being a significant product innovation is

relatively true. Investors after the creation of the ETFs were able to adequately utilize the

investment opportunity and diversify the investments on a single trade. Moreover, the

investors were provided with adequate opportunity to sell and by the stock within the trading

event and not wait like the mutual funds at the end of the day to detect the actual value of the

investment. This exposure relatively helps the ETFs to acquire additional investments and is

considered a significant product innovation, which allows the investors to adequately invest

in an instrument that underlines a particular index. The investment scope allows investors to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED INVESTMENT MANAGEMENT

minimize the level of risk endeavors from their investment. After the creation of the ETFs

investors were able to increase their exposure in the index funds, which relatively stated

about the overall condition of the capital market. This exposure of the capital market allowed

the investors to make relevant investment decisions regarding the current trajectory of the

stock market (Israeli, Lee and Sridharan 2017).

ETFs make the market more efficient:

The above statement regarding the efficiency of the market that has been boosted after

the adoption of ETF is relatively true. The creation of the ETFs relatively allowed the

investors to adequately sell and buy shares that underline the overall index. This method

mainly helps in deriving the overall efficiency of the market, which detect the actual price

level of the index due to the continuous selling and buying of the underline ETF. The

presence of the ETFs only allows the market to provide financial instruments to the investors

that can be used for improving their investment exposures and bank-on the diversification of

the investment. The investors with the ETS are able to conduct investment in bond, industry,

commodity, currency and inverse, which helps in identifying the value of the particular

investment and increases the efficiency of the market for determining and comprehending the

actual prices of a particular investment. Therefore, it could be understood that with the help

of ETFs the market efficiency has relatively improved as investors are provided with

adequate levels of information regarding the particular investment opportunity (Da and Shive

2018).

ETF trading creates mispricing that can be exploited by smart investors:

The statement regarding the creation of mispricing that is exploited by smart investors

is relatively true, as relevant fluctuations of the price are conducted throughout the day to

identify the adequate value for the overall ETF fund. The fund is relatively bought and sold

through brokerage where traders can effectively reap the benefit of mispricing, which is

minimize the level of risk endeavors from their investment. After the creation of the ETFs

investors were able to increase their exposure in the index funds, which relatively stated

about the overall condition of the capital market. This exposure of the capital market allowed

the investors to make relevant investment decisions regarding the current trajectory of the

stock market (Israeli, Lee and Sridharan 2017).

ETFs make the market more efficient:

The above statement regarding the efficiency of the market that has been boosted after

the adoption of ETF is relatively true. The creation of the ETFs relatively allowed the

investors to adequately sell and buy shares that underline the overall index. This method

mainly helps in deriving the overall efficiency of the market, which detect the actual price

level of the index due to the continuous selling and buying of the underline ETF. The

presence of the ETFs only allows the market to provide financial instruments to the investors

that can be used for improving their investment exposures and bank-on the diversification of

the investment. The investors with the ETS are able to conduct investment in bond, industry,

commodity, currency and inverse, which helps in identifying the value of the particular

investment and increases the efficiency of the market for determining and comprehending the

actual prices of a particular investment. Therefore, it could be understood that with the help

of ETFs the market efficiency has relatively improved as investors are provided with

adequate levels of information regarding the particular investment opportunity (Da and Shive

2018).

ETF trading creates mispricing that can be exploited by smart investors:

The statement regarding the creation of mispricing that is exploited by smart investors

is relatively true, as relevant fluctuations of the price are conducted throughout the day to

identify the adequate value for the overall ETF fund. The fund is relatively bought and sold

through brokerage where traders can effectively reap the benefit of mispricing, which is

ADVANCED INVESTMENT MANAGEMENT

conducted due to the continuous selling and buying process. The smart investors can

adequately identify the relevant Trend and detect the support and resistance levels, which

could help in generating returns from the mispricing situation. The mispricing situation is

relatively present in the stock market, which is the main reason why investors conduct

intraday trade to reap the benefits from the mispricing opportunity (Abner 2016). In a similar

case, the ETF can be mispriced and smart investors could take advantage of the situation and

make profits from their exposure to the ETF. Thus, ETF can be considered an adequate

investment opportunity for single investors who can adequately diversify their investments

and generate relevant returns in the process.

conducted due to the continuous selling and buying process. The smart investors can

adequately identify the relevant Trend and detect the support and resistance levels, which

could help in generating returns from the mispricing situation. The mispricing situation is

relatively present in the stock market, which is the main reason why investors conduct

intraday trade to reap the benefits from the mispricing opportunity (Abner 2016). In a similar

case, the ETF can be mispriced and smart investors could take advantage of the situation and

make profits from their exposure to the ETF. Thus, ETF can be considered an adequate

investment opportunity for single investors who can adequately diversify their investments

and generate relevant returns in the process.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.