Advanced Management Accounting Report: Explorer Boats, UK, Analysis

VerifiedAdded on 2021/02/21

|12

|3818

|73

Report

AI Summary

This report provides a comprehensive analysis of advanced management accounting principles, focusing on their application within the context of Explorer Boats, a UK-based boat manufacturing SME. The report begins with an introduction to the field, highlighting its role in providing financial information to various stakeholders, including internal stakeholders such as employees, management, and board of directors, as well as external stakeholders such as investors, creditors, the government, and society. The report then delves into the practical application of microeconomic techniques, such as cost analysis, cost-volume-profit analysis, and cost variance analysis, to assess the impact of microeconomic factors on the business. Furthermore, the report examines the concept and importance of variance analysis, including the use of actual and standard costs to control and correct variances. Finally, the report considers how changes in the business environment impact management accounting processes, offering insights into how companies can adapt to these changes. The report uses Kaplan and Atkinson's advanced management accounting principles and provides a practical framework for understanding and applying these concepts in a real-world business setting.

Advance Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

Overview of company:.................................................................................................................3

P1. Analyse the purpose for developing and presenting financial information:..........................3

TASK 2............................................................................................................................................6

P2. Use of different accounting microeconomic techniques:......................................................6

TASK 3............................................................................................................................................7

P3. Concept of variance analysis in its importance:....................................................................7

P4. Actual and standard costs to control and correct variances:..................................................8

TASK 4..........................................................................................................................................11

P5. Changing business environment's impacts on management accounting:............................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

Kaplan, R. S. and Atkinson, A. A., 2015. Advanced management accounting. PHI Learning.....13

INTRODUCTION...........................................................................................................................3

TASK...............................................................................................................................................3

Overview of company:.................................................................................................................3

P1. Analyse the purpose for developing and presenting financial information:..........................3

TASK 2............................................................................................................................................6

P2. Use of different accounting microeconomic techniques:......................................................6

TASK 3............................................................................................................................................7

P3. Concept of variance analysis in its importance:....................................................................7

P4. Actual and standard costs to control and correct variances:..................................................8

TASK 4..........................................................................................................................................11

P5. Changing business environment's impacts on management accounting:............................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

Kaplan, R. S. and Atkinson, A. A., 2015. Advanced management accounting. PHI Learning.....13

INTRODUCTION

Advanced management accounting relates to more advanced concepts, techniques and

methods which are organised around an action plan allow to focus on allocating problems and

identifies challenges. Moreover, its also deals with solving such challenges and issues. It is more

wide field of accounting, finance and management as it covers highly challenging tasks and

provides techniques to resolve them efficiently. Yearly fiscal budgets is proposed by companies

with help of management accounting tools and methods, which determines the ways of future

action plan, frameworks and strategies. It aims to present business information for managerial

tasks and assisting stakeholder (Kaplan and Atkinson, 2015). Study provide a discussion on

motive of presentation and framing of fiscal information and effective application of techniques

of management accounting in context of Explorer Boats, UK's Boat manufacturing company. It

is SME enjoying profitability and wants to make expansion in business. The study also analyse

the possible ways a change in factors of business environment affects adopted management

accounting processes.

TASK

Overview of company:

Explorer Boats is UK's small and medium enterprise. Company is manufacturer of boats

and iconic Turbojet. Company has unique range of boats and it also provides services of

customisation of boats as per customers specifications. It designs interior of boats and

manufactures different essential parts. Company known for manufacturing of affordable boats in

UK. It focus on making boats within customer's budget. It is moving forward in industry by

providing quality products.

P1. Analyse the purpose for developing and presenting financial information:

In current competitive business environment, every corporate putting their efforts to

increase the number of investors by attracting them. To bring new investments in business

companies presents their annual accounts and financial information. Investors using such

information decides what about holding and making investments. Developing information is

crucial element in management accounting as it provides basis for systematic presentation of

information. Organisational processes are designed by managerial personnel to ensure that

efficacious information is generated from such processes. Stakeholder are core user of that

Advanced management accounting relates to more advanced concepts, techniques and

methods which are organised around an action plan allow to focus on allocating problems and

identifies challenges. Moreover, its also deals with solving such challenges and issues. It is more

wide field of accounting, finance and management as it covers highly challenging tasks and

provides techniques to resolve them efficiently. Yearly fiscal budgets is proposed by companies

with help of management accounting tools and methods, which determines the ways of future

action plan, frameworks and strategies. It aims to present business information for managerial

tasks and assisting stakeholder (Kaplan and Atkinson, 2015). Study provide a discussion on

motive of presentation and framing of fiscal information and effective application of techniques

of management accounting in context of Explorer Boats, UK's Boat manufacturing company. It

is SME enjoying profitability and wants to make expansion in business. The study also analyse

the possible ways a change in factors of business environment affects adopted management

accounting processes.

TASK

Overview of company:

Explorer Boats is UK's small and medium enterprise. Company is manufacturer of boats

and iconic Turbojet. Company has unique range of boats and it also provides services of

customisation of boats as per customers specifications. It designs interior of boats and

manufactures different essential parts. Company known for manufacturing of affordable boats in

UK. It focus on making boats within customer's budget. It is moving forward in industry by

providing quality products.

P1. Analyse the purpose for developing and presenting financial information:

In current competitive business environment, every corporate putting their efforts to

increase the number of investors by attracting them. To bring new investments in business

companies presents their annual accounts and financial information. Investors using such

information decides what about holding and making investments. Developing information is

crucial element in management accounting as it provides basis for systematic presentation of

information. Organisational processes are designed by managerial personnel to ensure that

efficacious information is generated from such processes. Stakeholder are core user of that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

financial information. Following is discussion on main aim of presenting and developing fiscal

information in perspective of different stakeholders as follows:

For internal stakeholder: Internal stakeholders are referred as the people who are internal

to an organisation. They are the first one's who gets affected by any thing wrong happening in

the company. Internal stakeholders in any typical company consists majorly of employees, board

of directors, management and internal departments working as a single function. All these

stakeholders need to be satisfied with evident financial information so that they have some base

to uphold their stakes satisfactorily (Al-Dhubaibi and Abdullah, 2016). The need for financial

information for individual stakeholder arises because:

Employees: They are the backbone of any organisation. They toil every day to make the

organisation a successful identity. They seek financial information of the company to keep

themselves secured of their compensation, their bonus, incentives and the stability of their job. It

the company is doing bad; it will affect their life as well by non payment of salary or may be

retrenchment in some cases.

Management : They are the one's responsible for making strategies for the business. They

are the only responsible body for the functioning of the organisation; hence the relevance of

financial information is the greatest for the management of the company. They seek such

information to evaluate profitability, and design future policies and strategies for the business to

be conducted.

Board of directors: They are responsible for the good governance of the organisation.

They consist of few members who regulate the functioning of the business being internally but

behaving externally. They need financial information to check whether the organisation is

maintaining financial sanctity and upholding the interests of the investors. They present financial

reports to the public during general meetings, and for this reason they need to study the financial

data in advance (Machado and Alves, 2017).

Departments : Apart from an individual employee, the departments in an organisation

like marketing, production, HR, finance departments etc. seek financial information to analyse

how well they have contributed in the overall growth and what kind of future challenges they

may face. They wish to seek information to know the budget allocation for their respective

departments.

information in perspective of different stakeholders as follows:

For internal stakeholder: Internal stakeholders are referred as the people who are internal

to an organisation. They are the first one's who gets affected by any thing wrong happening in

the company. Internal stakeholders in any typical company consists majorly of employees, board

of directors, management and internal departments working as a single function. All these

stakeholders need to be satisfied with evident financial information so that they have some base

to uphold their stakes satisfactorily (Al-Dhubaibi and Abdullah, 2016). The need for financial

information for individual stakeholder arises because:

Employees: They are the backbone of any organisation. They toil every day to make the

organisation a successful identity. They seek financial information of the company to keep

themselves secured of their compensation, their bonus, incentives and the stability of their job. It

the company is doing bad; it will affect their life as well by non payment of salary or may be

retrenchment in some cases.

Management : They are the one's responsible for making strategies for the business. They

are the only responsible body for the functioning of the organisation; hence the relevance of

financial information is the greatest for the management of the company. They seek such

information to evaluate profitability, and design future policies and strategies for the business to

be conducted.

Board of directors: They are responsible for the good governance of the organisation.

They consist of few members who regulate the functioning of the business being internally but

behaving externally. They need financial information to check whether the organisation is

maintaining financial sanctity and upholding the interests of the investors. They present financial

reports to the public during general meetings, and for this reason they need to study the financial

data in advance (Machado and Alves, 2017).

Departments : Apart from an individual employee, the departments in an organisation

like marketing, production, HR, finance departments etc. seek financial information to analyse

how well they have contributed in the overall growth and what kind of future challenges they

may face. They wish to seek information to know the budget allocation for their respective

departments.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

External stakeholders : They are the one who are outsider to an organisation but not

actually are. They are the most affected by the actions of an organisation. They form part of

macro sphere around the company. External stakeholders include investors, creditors,

government and the society. They look for key financial information because:

Investors : They invest their hard earned in the company to provide it with capital. They

fulfil the working capital requirements of the business which it seeks to invest in its projects. In

favour they seek dividends, bonus shares and other benefits. Financial information of the

company is of high regard to them because they want to get ensured that they are being paid of

their dividends and their money wouldn't turn out to be a loss figure (Höglund and et. al., 2017).

Creditors : They provide raw materials, lease, money, loans on credit to the firm. They

put their stakes at high risk with the business. They seek financial information to rest assured of

the payment of their dues along with the interest. The wish that the company remains soluble and

profit making entity so that it can maintain healthy business relationship and maintain the credit

flow.

Government : Governments run on tax money they receive in the form of corporate tax.

And other concerns include capital gains taxes, income tax, custom and excise duties which all

accrues to the government from the corporates. It seeks financial information of companies to

check the overall health of the economy by clubbing individual organisations profits. Also, the

government wish to ensure that an entity keeps on paying taxes for greater good (DIANATI,

Alambeigi and Barzegar, 2016).

Society : Society by and large is the biggest stakeholder in a business. Society is what

made up of customers who pay money for the products. Society gets affected first for any wrong

doing from the companies. If a company fails, it indirectly affects majority of people who have

invested their money somewhere or the other sources indirectly affected by the company.

Businesses do CSR activities as the law requires them after crossing a threshold limit. Social

organisations keep a track on the business firms that the money directed for CSR has been

implemented for the welfare of the society and do not get siphoned to the illegal sources.

actually are. They are the most affected by the actions of an organisation. They form part of

macro sphere around the company. External stakeholders include investors, creditors,

government and the society. They look for key financial information because:

Investors : They invest their hard earned in the company to provide it with capital. They

fulfil the working capital requirements of the business which it seeks to invest in its projects. In

favour they seek dividends, bonus shares and other benefits. Financial information of the

company is of high regard to them because they want to get ensured that they are being paid of

their dividends and their money wouldn't turn out to be a loss figure (Höglund and et. al., 2017).

Creditors : They provide raw materials, lease, money, loans on credit to the firm. They

put their stakes at high risk with the business. They seek financial information to rest assured of

the payment of their dues along with the interest. The wish that the company remains soluble and

profit making entity so that it can maintain healthy business relationship and maintain the credit

flow.

Government : Governments run on tax money they receive in the form of corporate tax.

And other concerns include capital gains taxes, income tax, custom and excise duties which all

accrues to the government from the corporates. It seeks financial information of companies to

check the overall health of the economy by clubbing individual organisations profits. Also, the

government wish to ensure that an entity keeps on paying taxes for greater good (DIANATI,

Alambeigi and Barzegar, 2016).

Society : Society by and large is the biggest stakeholder in a business. Society is what

made up of customers who pay money for the products. Society gets affected first for any wrong

doing from the companies. If a company fails, it indirectly affects majority of people who have

invested their money somewhere or the other sources indirectly affected by the company.

Businesses do CSR activities as the law requires them after crossing a threshold limit. Social

organisations keep a track on the business firms that the money directed for CSR has been

implemented for the welfare of the society and do not get siphoned to the illegal sources.

TASK 2

P2. Use of different accounting microeconomic techniques:

Microeconomic techniques are specific business tools which assist in analysing impact of

different micro variables on business behaviour and trade practices. Corporations like Explorer

Boats adopts different micro-economics techniques to analyse the different aspects of entity

which are affected by micro factors. Primary area micro-economic tools is demand and supply of

company's products and evaluation of causes affecting essential factors of products demand and

supply (Cleary, 2015). Microeconomics is related with the evaluation of demand i.e. consumer

attitudes and the observation of supply i.e. behavioural aspects of individual producers and

suppliers. In this context following are most widely used micro-economic techniques in

respective company, as follows:

Cost analysis: This is most common method or technique concerned with

microeconomics. This techniques implies to assessment of unique relation between product's cost

and output produced by company. It help business managers in determining aggregate actual cost

incurred while hiring inputs as well as how efficiently such could be re-arranged to enhance

entire level of productivity. Cost analysis technique is mainly emphasises on ascertaining value

or cost of inputs like raw-material cost, labour cost etc. with aim to assess entire actual

Illustration 1: Stakeholders of Company

P2. Use of different accounting microeconomic techniques:

Microeconomic techniques are specific business tools which assist in analysing impact of

different micro variables on business behaviour and trade practices. Corporations like Explorer

Boats adopts different micro-economics techniques to analyse the different aspects of entity

which are affected by micro factors. Primary area micro-economic tools is demand and supply of

company's products and evaluation of causes affecting essential factors of products demand and

supply (Cleary, 2015). Microeconomics is related with the evaluation of demand i.e. consumer

attitudes and the observation of supply i.e. behavioural aspects of individual producers and

suppliers. In this context following are most widely used micro-economic techniques in

respective company, as follows:

Cost analysis: This is most common method or technique concerned with

microeconomics. This techniques implies to assessment of unique relation between product's cost

and output produced by company. It help business managers in determining aggregate actual cost

incurred while hiring inputs as well as how efficiently such could be re-arranged to enhance

entire level of productivity. Cost analysis technique is mainly emphasises on ascertaining value

or cost of inputs like raw-material cost, labour cost etc. with aim to assess entire actual

Illustration 1: Stakeholders of Company

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

production cost which ultimately assist in determining most optimal production level. In

Explorer Boats, managing personnels apply this technique to analyse the interconnection of

supply and demand in order to recognise existing and possible factors related to company's

product demand and supply (Nan, 2016).

Cost-volume profit analysis: Cost Volume Profit Analysis describes profit behaviour in

reaction to a product's cost and quantity or volume change. Simply, this is an assessment that

shows the effect on revenues of price and quantity. Commonly referred to as CVP Evaluation,

with this assessment, a management can determine the amount of revenues where business will

be in non-profit-free position. This position is termed level of break-even. Similarly, CVP

analysis may also demonstrate the number of sales-units needed to obtain a specific targeted

operating profit. Analysis (CVP) is being used to ascertain in what manner cost and quantity

shifts impact the operating profit as well as net earnings of a corporation. Analysis of the CVP

needs that all expenses of the corporation, including production, sales and administration

expenses, be recognized as varying or fixed. Explorer Boats also apply this technique to assess

the optimum production scale to avoid any potential adverse position. CVP analysis is quite

helpful for leadership as it offers an understanding into impacts and intra-relationship of

variables that affect the company's earnings. The connection between price, quantity and profit

constitutes an company's profit framework. Therefore, for financial planning as well as profit

management, CVP connection becomes crucial (Jermias, 2017).

Cost Variance: It is microeconomic techniques which mainly focuses on evaluation of

variations among budgeted and actual figures related to company's key business costs and

expenses. This simple and significant method under which management mainly analyse the

major variations which occurred in planed and actual performance of corporation in term of

costs. It assist in developing a framework for identification of factors which are responsible of

adverse variations in performance. In Explorer Boats, management conduct cost variance

analysis to enhance the overall productivity and identify adverse variables.

TASK 3

P3. Concept of variance analysis in its importance:

Variance Analysis can be described analysis of differentiation among previously planned

figures and actual figures. The total amount of all differences provides an general image of over-

Explorer Boats, managing personnels apply this technique to analyse the interconnection of

supply and demand in order to recognise existing and possible factors related to company's

product demand and supply (Nan, 2016).

Cost-volume profit analysis: Cost Volume Profit Analysis describes profit behaviour in

reaction to a product's cost and quantity or volume change. Simply, this is an assessment that

shows the effect on revenues of price and quantity. Commonly referred to as CVP Evaluation,

with this assessment, a management can determine the amount of revenues where business will

be in non-profit-free position. This position is termed level of break-even. Similarly, CVP

analysis may also demonstrate the number of sales-units needed to obtain a specific targeted

operating profit. Analysis (CVP) is being used to ascertain in what manner cost and quantity

shifts impact the operating profit as well as net earnings of a corporation. Analysis of the CVP

needs that all expenses of the corporation, including production, sales and administration

expenses, be recognized as varying or fixed. Explorer Boats also apply this technique to assess

the optimum production scale to avoid any potential adverse position. CVP analysis is quite

helpful for leadership as it offers an understanding into impacts and intra-relationship of

variables that affect the company's earnings. The connection between price, quantity and profit

constitutes an company's profit framework. Therefore, for financial planning as well as profit

management, CVP connection becomes crucial (Jermias, 2017).

Cost Variance: It is microeconomic techniques which mainly focuses on evaluation of

variations among budgeted and actual figures related to company's key business costs and

expenses. This simple and significant method under which management mainly analyse the

major variations which occurred in planed and actual performance of corporation in term of

costs. It assist in developing a framework for identification of factors which are responsible of

adverse variations in performance. In Explorer Boats, management conduct cost variance

analysis to enhance the overall productivity and identify adverse variables.

TASK 3

P3. Concept of variance analysis in its importance:

Variance Analysis can be described analysis of differentiation among previously planned

figures and actual figures. The total amount of all differences provides an general image of over-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

performance or under-performance in respect of specific period. In variance analysis different

factors like costs, income etc. are analysed by assessing the difference in figures actually attained

and figures budgeted. The main function of variance analysis is to bring down costs and improve

efficiency. The variances are efficiency-related. Efficiency demonstration leads to favourable

variance. In variance analysis difference measured are called as variances which can be adverse

by nature and significance or favourable (Christensen, Skærbæk and Tryggestad, 2016). An

adverse variance found in any area points out towards need of improvement while favourable

variations are considered as benchmarks for further analysis. Most corporations generate budgets

to monitor business objectives and enhance manufacturing and productivity improvements.

Budgets assist management to set benchmarks for potential enhancement measurement. Most

budgets begin with projected numbers of costs and sales. Management can assertively set all

such projections for the corporation's objectives. Other factors such as direct cost return

variation, fixed-cost efficiency variation, variable-cost efficiency variation, fixed cost capability

variation and many more may also be used by management.

Importance of variance analysis:

Variance analysis helps to effectively budget as managing personnels wants to have

reduced variances from scheduled budgets. Wishing a reduced deviation generally causes

executives to create budget choices that are comprehensive and forward-looking. It functions as a

structure for control. Evaluation of large variance on important products enables the business to

address reasons and enables management explore possible methods to prevent such variance.

Analysis of variance facilitates assignment of responsibilities and involves control mechanisms

in departments where necessary. For instance, if labour efficiency variation is considered

unfavourable or raw material price variance procurement is unfavourable, these divisions may be

controlled by management to boost effectiveness. It utilizes trends of previous company

information to build future performance principle. Variance information are contextualized

allowing managers to define variables such as holiday periods or seasonal effects as the

underlying cause of positively or negatively fluctuations. Relationships between pairs of

variables might also be identified when performing variance analysis. Positive and negative

correlations are important in business planning (Shil and Das, 2018). Variance analysis offers

hints about what occurring in the business's operating financial and competitive situations. The

start of any financial slowdown can reveal by adverse variances in business's monitoring

factors like costs, income etc. are analysed by assessing the difference in figures actually attained

and figures budgeted. The main function of variance analysis is to bring down costs and improve

efficiency. The variances are efficiency-related. Efficiency demonstration leads to favourable

variance. In variance analysis difference measured are called as variances which can be adverse

by nature and significance or favourable (Christensen, Skærbæk and Tryggestad, 2016). An

adverse variance found in any area points out towards need of improvement while favourable

variations are considered as benchmarks for further analysis. Most corporations generate budgets

to monitor business objectives and enhance manufacturing and productivity improvements.

Budgets assist management to set benchmarks for potential enhancement measurement. Most

budgets begin with projected numbers of costs and sales. Management can assertively set all

such projections for the corporation's objectives. Other factors such as direct cost return

variation, fixed-cost efficiency variation, variable-cost efficiency variation, fixed cost capability

variation and many more may also be used by management.

Importance of variance analysis:

Variance analysis helps to effectively budget as managing personnels wants to have

reduced variances from scheduled budgets. Wishing a reduced deviation generally causes

executives to create budget choices that are comprehensive and forward-looking. It functions as a

structure for control. Evaluation of large variance on important products enables the business to

address reasons and enables management explore possible methods to prevent such variance.

Analysis of variance facilitates assignment of responsibilities and involves control mechanisms

in departments where necessary. For instance, if labour efficiency variation is considered

unfavourable or raw material price variance procurement is unfavourable, these divisions may be

controlled by management to boost effectiveness. It utilizes trends of previous company

information to build future performance principle. Variance information are contextualized

allowing managers to define variables such as holiday periods or seasonal effects as the

underlying cause of positively or negatively fluctuations. Relationships between pairs of

variables might also be identified when performing variance analysis. Positive and negative

correlations are important in business planning (Shil and Das, 2018). Variance analysis offers

hints about what occurring in the business's operating financial and competitive situations. The

start of any financial slowdown can reveal by adverse variances in business's monitoring

quantitative classifications. In Explorer Boats, managing personnels are applying variance

analysis to find out what are key factors which may affect corporation's sales and production of

boats also help to identify factors which can boost company's sales. Also comparisons are

conducted by managers between current year’s variations and actual results with previous

periods results and variances.

P4. Actual and standard costs to control and correct variances:

Standard and actual costs are two major aspects of variance analysis which are required

to conduct variance analysis. Standard costs are expenses figures determined by management

based on their experience and past results. These costs act as benchmarks to assess company's

efficiencies and productivity level. In determination of standard costs managing personnels apply

their skills to determine appropriate rates in respect of income and expenses. Here most

considerable thing is that scope of standard costs should be within attainable criteria. In

Explorer Boats, standard costs are set by top managers as per company's existing capabilities

and resources. In company, standards for labour costs, material costs, administration costs, sales

promotion expenses are determined which is further used in farming budgets and analysis of

variances. While actual costs are actually incurred figures of expenses. Actual cost simply refers

to actual expenses related to business which are incurred in ordinary activities and functions. In

Explorer Boats managers list out all expenses along with amount actually incurred during

specific time-period thereafter these costs are compared with standard costs to assess variations

(Nuhu, Baird and Appuhami, 2016). These variations defines company's operating effectively in

effective manner, as shown in below example, as follows:

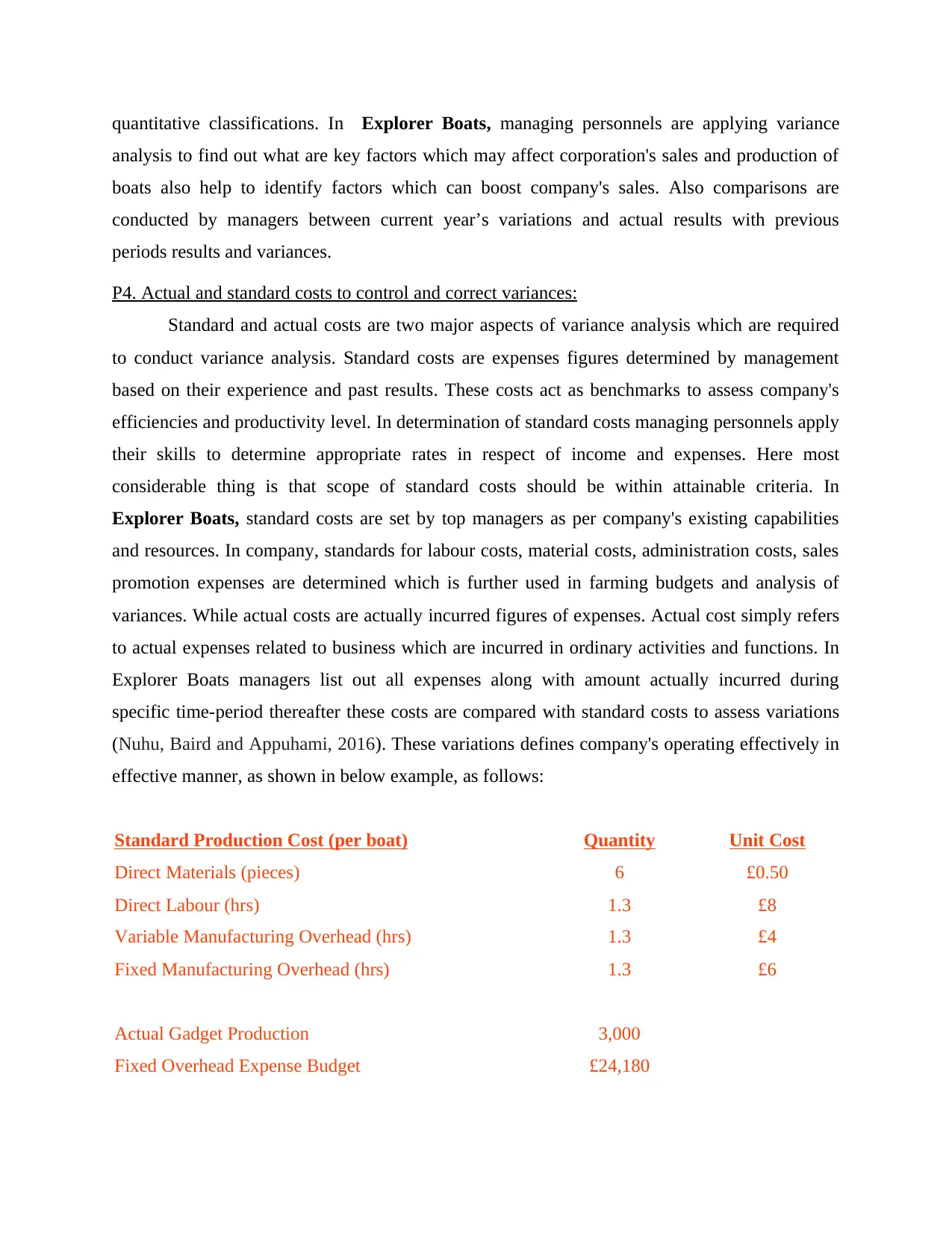

Standard Production Cost (per boat) Quantity Unit Cost

Direct Materials (pieces) 6 £0.50

Direct Labour (hrs) 1.3 £8

Variable Manufacturing Overhead (hrs) 1.3 £4

Fixed Manufacturing Overhead (hrs) 1.3 £6

Actual Gadget Production 3,000

Fixed Overhead Expense Budget £24,180

analysis to find out what are key factors which may affect corporation's sales and production of

boats also help to identify factors which can boost company's sales. Also comparisons are

conducted by managers between current year’s variations and actual results with previous

periods results and variances.

P4. Actual and standard costs to control and correct variances:

Standard and actual costs are two major aspects of variance analysis which are required

to conduct variance analysis. Standard costs are expenses figures determined by management

based on their experience and past results. These costs act as benchmarks to assess company's

efficiencies and productivity level. In determination of standard costs managing personnels apply

their skills to determine appropriate rates in respect of income and expenses. Here most

considerable thing is that scope of standard costs should be within attainable criteria. In

Explorer Boats, standard costs are set by top managers as per company's existing capabilities

and resources. In company, standards for labour costs, material costs, administration costs, sales

promotion expenses are determined which is further used in farming budgets and analysis of

variances. While actual costs are actually incurred figures of expenses. Actual cost simply refers

to actual expenses related to business which are incurred in ordinary activities and functions. In

Explorer Boats managers list out all expenses along with amount actually incurred during

specific time-period thereafter these costs are compared with standard costs to assess variations

(Nuhu, Baird and Appuhami, 2016). These variations defines company's operating effectively in

effective manner, as shown in below example, as follows:

Standard Production Cost (per boat) Quantity Unit Cost

Direct Materials (pieces) 6 £0.50

Direct Labour (hrs) 1.3 £8

Variable Manufacturing Overhead (hrs) 1.3 £4

Fixed Manufacturing Overhead (hrs) 1.3 £6

Actual Gadget Production 3,000

Fixed Overhead Expense Budget £24,180

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

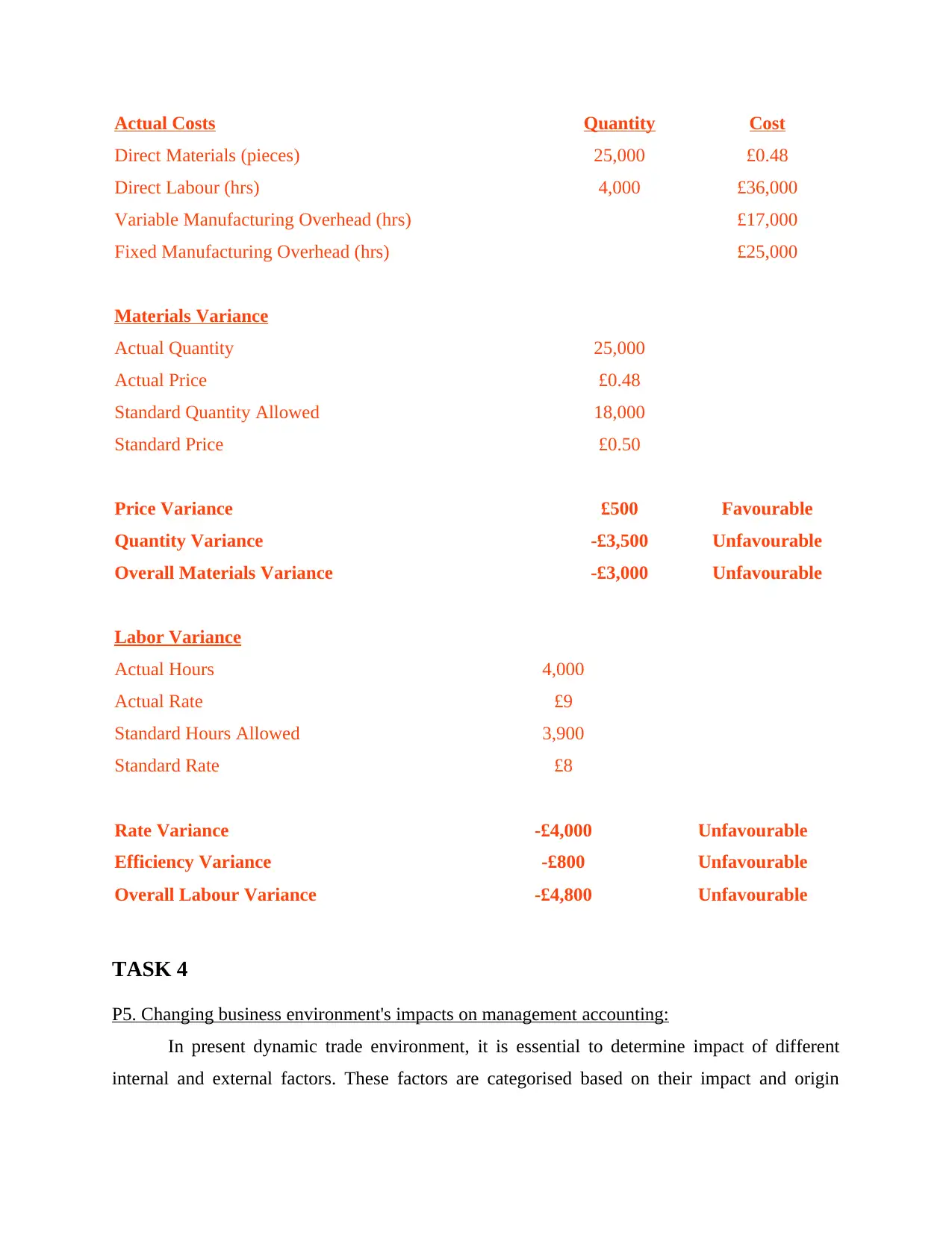

Actual Costs Quantity Cost

Direct Materials (pieces) 25,000 £0.48

Direct Labour (hrs) 4,000 £36,000

Variable Manufacturing Overhead (hrs) £17,000

Fixed Manufacturing Overhead (hrs) £25,000

Materials Variance

Actual Quantity 25,000

Actual Price £0.48

Standard Quantity Allowed 18,000

Standard Price £0.50

Price Variance £500 Favourable

Quantity Variance -£3,500 Unfavourable

Overall Materials Variance -£3,000 Unfavourable

Labor Variance

Actual Hours 4,000

Actual Rate £9

Standard Hours Allowed 3,900

Standard Rate £8

Rate Variance -£4,000 Unfavourable

Efficiency Variance -£800 Unfavourable

Overall Labour Variance -£4,800 Unfavourable

TASK 4

P5. Changing business environment's impacts on management accounting:

In present dynamic trade environment, it is essential to determine impact of different

internal and external factors. These factors are categorised based on their impact and origin

Direct Materials (pieces) 25,000 £0.48

Direct Labour (hrs) 4,000 £36,000

Variable Manufacturing Overhead (hrs) £17,000

Fixed Manufacturing Overhead (hrs) £25,000

Materials Variance

Actual Quantity 25,000

Actual Price £0.48

Standard Quantity Allowed 18,000

Standard Price £0.50

Price Variance £500 Favourable

Quantity Variance -£3,500 Unfavourable

Overall Materials Variance -£3,000 Unfavourable

Labor Variance

Actual Hours 4,000

Actual Rate £9

Standard Hours Allowed 3,900

Standard Rate £8

Rate Variance -£4,000 Unfavourable

Efficiency Variance -£800 Unfavourable

Overall Labour Variance -£4,800 Unfavourable

TASK 4

P5. Changing business environment's impacts on management accounting:

In present dynamic trade environment, it is essential to determine impact of different

internal and external factors. These factors are categorised based on their impact and origin

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

source. Currently, every firm is bound to create adjustments according to shift in business's

environment which assist them in achieving the highest advantage and survive within

competitive market situations. Following are major external and internal factors which affects

organisation's structure of management accounting, as follows:

External factors: These are factors which resides outside entity but considerably affect the

system of management accounting in context of Explorer Boats, as follows:

Economic Adversities: It is most important factor which determines company's

performance. Major economic adversities includes increasing inflation rate, adverse financial and

economic policies, decreasing in purchasing power of buyers. These adversities have direct

impact on corporation's management accounting established structure because it is difficult for

managers to identify these factors.

Competitiveness: With increase in customers demands, competitiveness in every sector

is increasing which act as external factor. It not only affects company's revenue and profits but

also affects managerial accounting structure. As with increasing competitiveness company's

strategy and stature related to different techniques of management accounting also affects

(Ismail, Isa and Mia, 2018).

Internal factors: These are closely linked with company's internal operations and management

structure. Following are some key internal variables are as follows:

Organisational Policies: Company's internal policies are acts as significant internal

factors which directly affects adopted techniques of management accounting and its structure. A

wrong or inappropriate policy can impact organisational functions which are dedicated towards

company's management accounting's structure.

Formulated action plans: It is also an internal factor which can affect management

accounting's structure. Company's actions plans defines company's performance in near future

and implementation of different techniques of management accounting.

CONCLUSION

From above study it has been articulated that management should properly develop and

present the financial information and reports as these assist in managerial decision-making

processes. Techniques concerned with field of management accounting also essential for

environment which assist them in achieving the highest advantage and survive within

competitive market situations. Following are major external and internal factors which affects

organisation's structure of management accounting, as follows:

External factors: These are factors which resides outside entity but considerably affect the

system of management accounting in context of Explorer Boats, as follows:

Economic Adversities: It is most important factor which determines company's

performance. Major economic adversities includes increasing inflation rate, adverse financial and

economic policies, decreasing in purchasing power of buyers. These adversities have direct

impact on corporation's management accounting established structure because it is difficult for

managers to identify these factors.

Competitiveness: With increase in customers demands, competitiveness in every sector

is increasing which act as external factor. It not only affects company's revenue and profits but

also affects managerial accounting structure. As with increasing competitiveness company's

strategy and stature related to different techniques of management accounting also affects

(Ismail, Isa and Mia, 2018).

Internal factors: These are closely linked with company's internal operations and management

structure. Following are some key internal variables are as follows:

Organisational Policies: Company's internal policies are acts as significant internal

factors which directly affects adopted techniques of management accounting and its structure. A

wrong or inappropriate policy can impact organisational functions which are dedicated towards

company's management accounting's structure.

Formulated action plans: It is also an internal factor which can affect management

accounting's structure. Company's actions plans defines company's performance in near future

and implementation of different techniques of management accounting.

CONCLUSION

From above study it has been articulated that management should properly develop and

present the financial information and reports as these assist in managerial decision-making

processes. Techniques concerned with field of management accounting also essential for

improvement in current operational performance of company. Business's external and internal

environment leads to some core factors which directly or indirectly affects organisation's

predefined objectives. Analysis of variations in company's performance variables like production

costs, administration costs etc. is most crucial as outcomes of analysis determines corporation's

future path in industry.

environment leads to some core factors which directly or indirectly affects organisation's

predefined objectives. Analysis of variations in company's performance variables like production

costs, administration costs etc. is most crucial as outcomes of analysis determines corporation's

future path in industry.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.