Advanced Management Accounting Report: CMI Safe Co Case Analysis

VerifiedAdded on 2023/06/07

|16

|2646

|397

Report

AI Summary

This management accounting report provides an in-depth analysis of CMI Safe Co's costing system, contrasting traditional costing methods with activity-based costing (ABC). The report examines the impact of cost allocation on product pricing, sales, and profitability, highlighting how incorrect costing can lead to suboptimal business decisions. Through a case study approach, the report demonstrates the application of management accounting techniques to solve business problems, evaluate financial information, and improve decision-making. The analysis includes calculations and comparisons of cost allocations under both costing methods, revealing the discrepancies in product costs and net margins. Ultimately, the report emphasizes the importance of selecting an appropriate costing system that aligns with the complexity of the production process to ensure accurate financial reporting and strategic decision-making. The report concludes with recommendations for CMI Safe Co to optimize its costing system and improve its overall financial performance.

Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The following assignment lays down the advanced understanding of management accounting

in the contemporary business environment. We have applied the management accounting

techniques to solve and analyse the business problems. The case study discussed in the

following discussion will help us adapt knowledge to new situations to develop approaches to

problem solving.

2

The following assignment lays down the advanced understanding of management accounting

in the contemporary business environment. We have applied the management accounting

techniques to solve and analyse the business problems. The case study discussed in the

following discussion will help us adapt knowledge to new situations to develop approaches to

problem solving.

2

Contents

Introduction...........................................................................................................................................3

Methods of costing- Traditional and Activity Based.............................................................................4

Traditional Costing................................................................................................................................5

Activity Based Costing..........................................................................................................................7

Analysis of Cost system of CMI Safe Co..............................................................................................9

Affect of Wrong allocation on Sales of product..................................................................................12

Affect of Wrong allocation on product cost and net margin................................................................13

Conclusion...........................................................................................................................................14

Bibliography........................................................................................................................................15

3

Introduction...........................................................................................................................................3

Methods of costing- Traditional and Activity Based.............................................................................4

Traditional Costing................................................................................................................................5

Activity Based Costing..........................................................................................................................7

Analysis of Cost system of CMI Safe Co..............................................................................................9

Affect of Wrong allocation on Sales of product..................................................................................12

Affect of Wrong allocation on product cost and net margin................................................................13

Conclusion...........................................................................................................................................14

Bibliography........................................................................................................................................15

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

The success of a production facility is very much dependent on the costing system it follows.

There are two major methods of cost allocation- traditional costing and activity based costing.

Depending on the complexity of the production process, the appropriate costing method is

applied. We have been provided with a situation of a safe manufacturing company, CMI Safe

Co, which follows the traditional method of costing. Recently the management has realised

that it is not satisfied with the results even though the business has increased in volume and

productivity.

In our discussion below, we have disused about the methods of costing and steps required by

the management of company to be taken in order to ensure optimum results.

4

The success of a production facility is very much dependent on the costing system it follows.

There are two major methods of cost allocation- traditional costing and activity based costing.

Depending on the complexity of the production process, the appropriate costing method is

applied. We have been provided with a situation of a safe manufacturing company, CMI Safe

Co, which follows the traditional method of costing. Recently the management has realised

that it is not satisfied with the results even though the business has increased in volume and

productivity.

In our discussion below, we have disused about the methods of costing and steps required by

the management of company to be taken in order to ensure optimum results.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Methods of costing- Traditional and Activity Based

In order to calculate the cost of a product, the management collects data on all the expenses.

The expenses which can be directly attributable to products are, directly added to the cost of

the products. There are other costs and services which are jointly incurred for various

products. These costs are required to be allocated to all the products based on some attribute.

Selection of this attribute is very important as it helps in determining the actual cost of

product. Cost data is used by the management in order to make pricing decision. The demand

and sale of the products are dependent on the price and cost. Therefore, we see that cost

allocation can have direct impact on the sale of product.

For example, there are two products Product A and B, the direct cost for Product A is $5 per

unit and that for product B is $ 8 per unit. The joint cost which are incurred for these products

are $5000. Now these costs are required to be allocated amongst the product A and B so that

total cost per product can be determined.

As mentioned earlier, these are the two widely implemented method of cost allocation. Both

of these methods have their respective pros and cons. We have discussed about these methods

in detail so that solution for CMI Safe Co can be arrived at.

5

In order to calculate the cost of a product, the management collects data on all the expenses.

The expenses which can be directly attributable to products are, directly added to the cost of

the products. There are other costs and services which are jointly incurred for various

products. These costs are required to be allocated to all the products based on some attribute.

Selection of this attribute is very important as it helps in determining the actual cost of

product. Cost data is used by the management in order to make pricing decision. The demand

and sale of the products are dependent on the price and cost. Therefore, we see that cost

allocation can have direct impact on the sale of product.

For example, there are two products Product A and B, the direct cost for Product A is $5 per

unit and that for product B is $ 8 per unit. The joint cost which are incurred for these products

are $5000. Now these costs are required to be allocated amongst the product A and B so that

total cost per product can be determined.

As mentioned earlier, these are the two widely implemented method of cost allocation. Both

of these methods have their respective pros and cons. We have discussed about these methods

in detail so that solution for CMI Safe Co can be arrived at.

5

Traditional Costing

Traditional costing is the old method of cost allocation, under which the joint cost incurred

are allocated amongst the product using one single factor. This factor may be machine hours,

labour hours, number of units etc. The point is, only one attribute for cost allocation is used

irrespective of consumption of service (Berry, 2009).

For example, in above if the joint cost of $5000 includes expense of $500 which are incurred

mostly for product A, then irrespective of usage, the cost will be allocated based on machine

hours.

Traditional method of costing is best suitable for production processes which are simple and

do not comprise of various functions. This method has both its pros and cons which have

been discussed below.

The traditional costing method of cost allocation is a very simplified. It does not involve huge

data collection. Since this system uses only one attribute for cost allocation the management

does not require details of various function and there consumption. This system is very easy

to understand and implement. The management need not appoint special personnel’s in order

to implement this system of cost allocation. Since this method can be easily implemented it

saves a lot of time. Since this method allocates all other costs to the product irrespective of

their nature, we can say that it recognizes the importance of fixed cost in the method of

production. This method in generally used while the financial statements are prepares,

therefore, not much reconciliation between the costs and accounting records is required when

absorption costing method is implemented.

Therefore we see that the traditional costing method is quiet advantageous. But apart from

benefits this method has its cons. Few of the cons of this method of cost allocation has been

listed below:

The traditional costing method is not suitable where there are many production functions

involved. Since the products use same functions it is important that charge of these expenses

should be allocated based on actual usage of these functions. If this method is implemented in

a production facility involving many functions, then it results in improper cost allocation,

which leads to wrong product pricing. This may then harm the demand of the product. Since

the overheads are allocated based on pre determined rate, it always results I over or under

6

Traditional costing is the old method of cost allocation, under which the joint cost incurred

are allocated amongst the product using one single factor. This factor may be machine hours,

labour hours, number of units etc. The point is, only one attribute for cost allocation is used

irrespective of consumption of service (Berry, 2009).

For example, in above if the joint cost of $5000 includes expense of $500 which are incurred

mostly for product A, then irrespective of usage, the cost will be allocated based on machine

hours.

Traditional method of costing is best suitable for production processes which are simple and

do not comprise of various functions. This method has both its pros and cons which have

been discussed below.

The traditional costing method of cost allocation is a very simplified. It does not involve huge

data collection. Since this system uses only one attribute for cost allocation the management

does not require details of various function and there consumption. This system is very easy

to understand and implement. The management need not appoint special personnel’s in order

to implement this system of cost allocation. Since this method can be easily implemented it

saves a lot of time. Since this method allocates all other costs to the product irrespective of

their nature, we can say that it recognizes the importance of fixed cost in the method of

production. This method in generally used while the financial statements are prepares,

therefore, not much reconciliation between the costs and accounting records is required when

absorption costing method is implemented.

Therefore we see that the traditional costing method is quiet advantageous. But apart from

benefits this method has its cons. Few of the cons of this method of cost allocation has been

listed below:

The traditional costing method is not suitable where there are many production functions

involved. Since the products use same functions it is important that charge of these expenses

should be allocated based on actual usage of these functions. If this method is implemented in

a production facility involving many functions, then it results in improper cost allocation,

which leads to wrong product pricing. This may then harm the demand of the product. Since

the overheads are allocated based on pre determined rate, it always results I over or under

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

recovery of overheads. This requires adjustment in the books, which is a lot of work. This

system fails to realise the importance of cost volume profit relationship as all the costs are

allocated to the product irrespective of their nature. Allocation of cost based on one attribute

results in wrong costing. This is the major con of this system.

Therefore, we see that the tradition system of cost allocation is easy to use, but it may affect

the profitability of the business. Not using correct cost data will result in wrong product

pricing which will end in absurd financial results. It is important that the costing system

implemented is according to the production requirements.

7

system fails to realise the importance of cost volume profit relationship as all the costs are

allocated to the product irrespective of their nature. Allocation of cost based on one attribute

results in wrong costing. This is the major con of this system.

Therefore, we see that the tradition system of cost allocation is easy to use, but it may affect

the profitability of the business. Not using correct cost data will result in wrong product

pricing which will end in absurd financial results. It is important that the costing system

implemented is according to the production requirements.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Activity Based Costing

Activity based costing is the modern costing system that tries to cover the disadvantages of

the activity based costing. Activity based costing as the name suggest, is the cost allocation

system that allocates the cost amongst the product based on actual consumption of the

activity. Under this system units consumed for each activity is individually calculated which

is then used as an attribute to allocate cost amongst the products (Atkinson, 2012).

For example, the two products A and B are required to be inspected for quality check at the

end of production. Product A requires more inspection than B. Number of total inspections

done are 20, out of which inspection solely contributed to product A is 15. If total cost for

inspection is $2000, then cost of $1500 will be charged to product A and $500 will be

charged to product B.

Just like the traditional costing system, activity based costing also has few advantages and

disadvantages.

Activity based costing takes into consideration the concept of actual usage or consumption of

activity. This system ensures that only that part of cost is allocated to the product which is

actually used by it. Activity based costing also helps the management to cut irrelevant cost.

Since the cost are all collected based on activities, the management can understand the nature

of cost, and this way they can eliminate the cost which are irrelevant or not required to be

incurred. Collection of huge cost data, cost drivers and various activities provide the

management with the insight in to total working of the organisation. This way any issues can

be noticed and resolved. Activity based costing helps in better decision making. Since this

allocation method allocates actual cost to the product, the management can use this data for

pricing policy. They can rely on the result of this system for decision making.

Activity based costing is the modern costing technique which ensures that only costs which

are actually incurred are allocated to the products. But this method also has a few

disadvantages.

ABC method requires collection of huge amount of data, like amount expense for each

activity, units consumed for each activity by each product, etc. this is a time consuming and

expensive process. This method can’t be easily implemented like any other costing method. It

requires professional knowledge and skill to be implemented. The management requires

8

Activity based costing is the modern costing system that tries to cover the disadvantages of

the activity based costing. Activity based costing as the name suggest, is the cost allocation

system that allocates the cost amongst the product based on actual consumption of the

activity. Under this system units consumed for each activity is individually calculated which

is then used as an attribute to allocate cost amongst the products (Atkinson, 2012).

For example, the two products A and B are required to be inspected for quality check at the

end of production. Product A requires more inspection than B. Number of total inspections

done are 20, out of which inspection solely contributed to product A is 15. If total cost for

inspection is $2000, then cost of $1500 will be charged to product A and $500 will be

charged to product B.

Just like the traditional costing system, activity based costing also has few advantages and

disadvantages.

Activity based costing takes into consideration the concept of actual usage or consumption of

activity. This system ensures that only that part of cost is allocated to the product which is

actually used by it. Activity based costing also helps the management to cut irrelevant cost.

Since the cost are all collected based on activities, the management can understand the nature

of cost, and this way they can eliminate the cost which are irrelevant or not required to be

incurred. Collection of huge cost data, cost drivers and various activities provide the

management with the insight in to total working of the organisation. This way any issues can

be noticed and resolved. Activity based costing helps in better decision making. Since this

allocation method allocates actual cost to the product, the management can use this data for

pricing policy. They can rely on the result of this system for decision making.

Activity based costing is the modern costing technique which ensures that only costs which

are actually incurred are allocated to the products. But this method also has a few

disadvantages.

ABC method requires collection of huge amount of data, like amount expense for each

activity, units consumed for each activity by each product, etc. this is a time consuming and

expensive process. This method can’t be easily implemented like any other costing method. It

requires professional knowledge and skill to be implemented. The management requires

8

appointing special skilled persons in order to implement ABC. This methods if implemented

then the cost data and accounting data required huge reconciliation. The implementation of

ABC is a complex process; it requires huge investment of human and financial resources

which makes it tiresome.

From the above we can see that though the process of ABC results in accurate and reliable

information, implementation of the process is very tiring and exhaustive. Continuous study of

the data and any changes are required to be incorporated in order to ensure appropriate

results. But this system helps the production enterprises with various functions to calculate

proper product cost.

9

then the cost data and accounting data required huge reconciliation. The implementation of

ABC is a complex process; it requires huge investment of human and financial resources

which makes it tiresome.

From the above we can see that though the process of ABC results in accurate and reliable

information, implementation of the process is very tiring and exhaustive. Continuous study of

the data and any changes are required to be incorporated in order to ensure appropriate

results. But this system helps the production enterprises with various functions to calculate

proper product cost.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

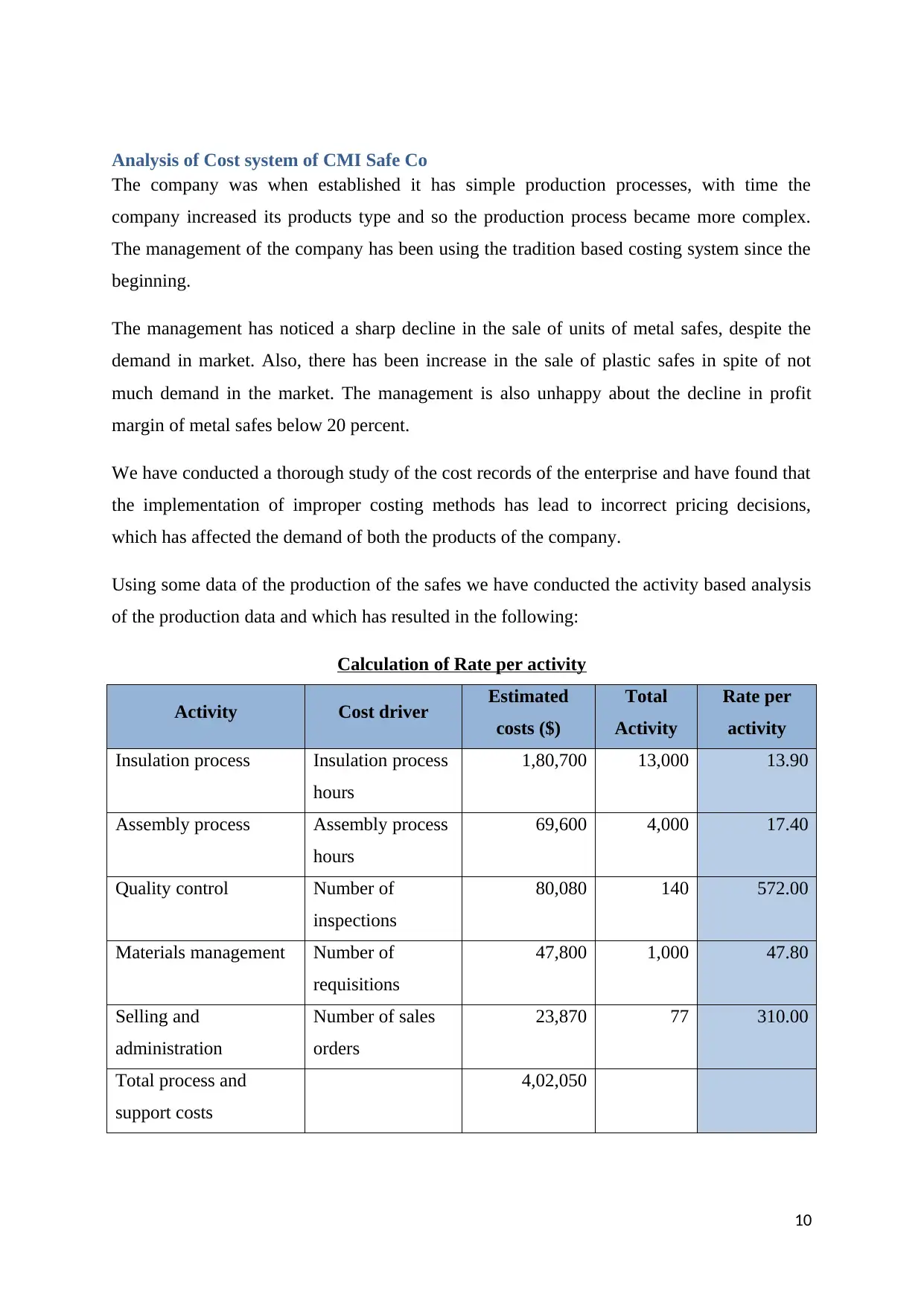

Analysis of Cost system of CMI Safe Co

The company was when established it has simple production processes, with time the

company increased its products type and so the production process became more complex.

The management of the company has been using the tradition based costing system since the

beginning.

The management has noticed a sharp decline in the sale of units of metal safes, despite the

demand in market. Also, there has been increase in the sale of plastic safes in spite of not

much demand in the market. The management is also unhappy about the decline in profit

margin of metal safes below 20 percent.

We have conducted a thorough study of the cost records of the enterprise and have found that

the implementation of improper costing methods has lead to incorrect pricing decisions,

which has affected the demand of both the products of the company.

Using some data of the production of the safes we have conducted the activity based analysis

of the production data and which has resulted in the following:

Calculation of Rate per activity

Activity Cost driver Estimated

costs ($)

Total

Activity

Rate per

activity

Insulation process Insulation process

hours

1,80,700 13,000 13.90

Assembly process Assembly process

hours

69,600 4,000 17.40

Quality control Number of

inspections

80,080 140 572.00

Materials management Number of

requisitions

47,800 1,000 47.80

Selling and

administration

Number of sales

orders

23,870 77 310.00

Total process and

support costs

4,02,050

10

The company was when established it has simple production processes, with time the

company increased its products type and so the production process became more complex.

The management of the company has been using the tradition based costing system since the

beginning.

The management has noticed a sharp decline in the sale of units of metal safes, despite the

demand in market. Also, there has been increase in the sale of plastic safes in spite of not

much demand in the market. The management is also unhappy about the decline in profit

margin of metal safes below 20 percent.

We have conducted a thorough study of the cost records of the enterprise and have found that

the implementation of improper costing methods has lead to incorrect pricing decisions,

which has affected the demand of both the products of the company.

Using some data of the production of the safes we have conducted the activity based analysis

of the production data and which has resulted in the following:

Calculation of Rate per activity

Activity Cost driver Estimated

costs ($)

Total

Activity

Rate per

activity

Insulation process Insulation process

hours

1,80,700 13,000 13.90

Assembly process Assembly process

hours

69,600 4,000 17.40

Quality control Number of

inspections

80,080 140 572.00

Materials management Number of

requisitions

47,800 1,000 47.80

Selling and

administration

Number of sales

orders

23,870 77 310.00

Total process and

support costs

4,02,050

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

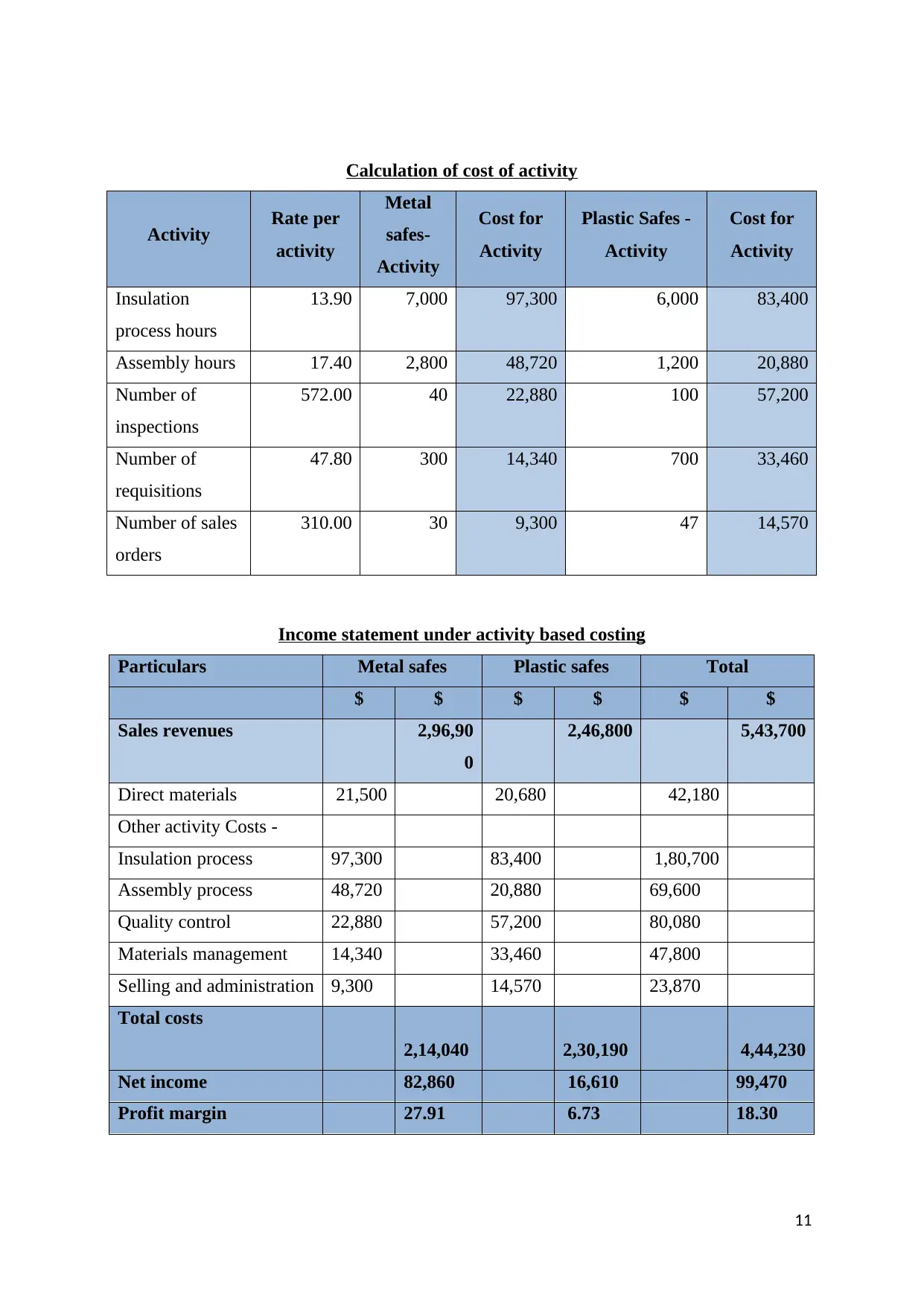

Calculation of cost of activity

Activity Rate per

activity

Metal

safes-

Activity

Cost for

Activity

Plastic Safes -

Activity

Cost for

Activity

Insulation

process hours

13.90 7,000 97,300 6,000 83,400

Assembly hours 17.40 2,800 48,720 1,200 20,880

Number of

inspections

572.00 40 22,880 100 57,200

Number of

requisitions

47.80 300 14,340 700 33,460

Number of sales

orders

310.00 30 9,300 47 14,570

Income statement under activity based costing

Particulars Metal safes Plastic safes Total

$ $ $ $ $ $

Sales revenues 2,96,90

0

2,46,800 5,43,700

Direct materials 21,500 20,680 42,180

Other activity Costs -

Insulation process 97,300 83,400 1,80,700

Assembly process 48,720 20,880 69,600

Quality control 22,880 57,200 80,080

Materials management 14,340 33,460 47,800

Selling and administration 9,300 14,570 23,870

Total costs

2,14,040 2,30,190 4,44,230

Net income 82,860 16,610 99,470

Profit margin 27.91 6.73 18.30

11

Activity Rate per

activity

Metal

safes-

Activity

Cost for

Activity

Plastic Safes -

Activity

Cost for

Activity

Insulation

process hours

13.90 7,000 97,300 6,000 83,400

Assembly hours 17.40 2,800 48,720 1,200 20,880

Number of

inspections

572.00 40 22,880 100 57,200

Number of

requisitions

47.80 300 14,340 700 33,460

Number of sales

orders

310.00 30 9,300 47 14,570

Income statement under activity based costing

Particulars Metal safes Plastic safes Total

$ $ $ $ $ $

Sales revenues 2,96,90

0

2,46,800 5,43,700

Direct materials 21,500 20,680 42,180

Other activity Costs -

Insulation process 97,300 83,400 1,80,700

Assembly process 48,720 20,880 69,600

Quality control 22,880 57,200 80,080

Materials management 14,340 33,460 47,800

Selling and administration 9,300 14,570 23,870

Total costs

2,14,040 2,30,190 4,44,230

Net income 82,860 16,610 99,470

Profit margin 27.91 6.73 18.30

11

Therefore, if we allocate the overhead cost as per actual usage of activity we see that the cost

allocated to metal safe is $192540 and that to plastic safe is $209510. But if we go with the

traditional costing system, the overhead allocated to metal safe is 231770 and that to plastic

safe is $170280.

More cost was allocated to metal safes which resulted in low profitability from this section.

12

allocated to metal safe is $192540 and that to plastic safe is $209510. But if we go with the

traditional costing system, the overhead allocated to metal safe is 231770 and that to plastic

safe is $170280.

More cost was allocated to metal safes which resulted in low profitability from this section.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.