Costing Techniques and ABC Implementation: Belle Clinique Report

VerifiedAdded on 2022/09/03

|11

|2193

|23

Report

AI Summary

This report evaluates the costing techniques and provides recommendations to the board of directors of Belle Clinique on the implementation and adoption of activity-based costing (ABC). The report analyzes the current costing system, which allocates overhead costs based on machine hours, and identifies that the system is contributing to increasing total overhead costs, particularly affecting the pricing and sales of the product IPL. The report compares the unit costs of products under traditional and ABC systems and recommends implementing ABC to address pricing issues and improve the profitability of IPL. It discusses arguments for and against ABC implementation, and provides an executive summary, introduction, discussion of ABC development, analysis of pricing pressures, comparison of costing methods, options for improving profitability, and a conclusion recommending the adoption of ABC to improve the company's financial performance. The report also includes references and an appendix with cost calculations.

Running head: ADVANCED MANAGEMENT ACCOUNTING

Advanced management accounting

Name of the Student

Name of the University

Author Note

Advanced management accounting

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED MANAGEMENT ACCOUNTING

Executive summary:

The report is prepared to demonstrate the importance of activity based costing technique to

the costing strategy of Belle Clinique. The information from the case study identifies that the

current costing system is not suitable as it is contributing to increasing the total overhead

costs. Facing the competitive pressure in terms of pricing the product, it has been found that

product IPL is not adequately priced as the sales of the product is falling continuously. The

reason is attributable to the rising overhead costs that has resulted in marking the price of the

product at certain percent of the mark up price. From the overall analysis of the facts of the

case, it has been ascertained that the adoption of activity based costing would assist Belle

Clinique in addressing the issue of pricing and increasing the sale of one of its product. It is

therefore recommended to implement the activity based costing system.

Executive summary:

The report is prepared to demonstrate the importance of activity based costing technique to

the costing strategy of Belle Clinique. The information from the case study identifies that the

current costing system is not suitable as it is contributing to increasing the total overhead

costs. Facing the competitive pressure in terms of pricing the product, it has been found that

product IPL is not adequately priced as the sales of the product is falling continuously. The

reason is attributable to the rising overhead costs that has resulted in marking the price of the

product at certain percent of the mark up price. From the overall analysis of the facts of the

case, it has been ascertained that the adoption of activity based costing would assist Belle

Clinique in addressing the issue of pricing and increasing the sale of one of its product. It is

therefore recommended to implement the activity based costing system.

ADVANCED MANAGEMENT ACCOUNTING

Table of Contents

Executive summary:...................................................................................................................1

Introduction:...............................................................................................................................2

Discussion:.................................................................................................................................2

Development and history of ABC system:.................................................................................2

Identifying the price pressure and contribution of the current costing system:.........................3

Comparing the unit cost of the two products under traditional volume based costing and

proposed ABC system:...............................................................................................................3

Five options for improving the profitability of the products:....................................................3

Identifying five arguments supporting the implementation of ABC and five options against

the adoption of ABC:.................................................................................................................4

Recommendation and conclusion:.............................................................................................6

Table of Contents

Executive summary:...................................................................................................................1

Introduction:...............................................................................................................................2

Discussion:.................................................................................................................................2

Development and history of ABC system:.................................................................................2

Identifying the price pressure and contribution of the current costing system:.........................3

Comparing the unit cost of the two products under traditional volume based costing and

proposed ABC system:...............................................................................................................3

Five options for improving the profitability of the products:....................................................3

Identifying five arguments supporting the implementation of ABC and five options against

the adoption of ABC:.................................................................................................................4

Recommendation and conclusion:.............................................................................................6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ADVANCED MANAGEMENT ACCOUNTING

Introduction:

The report is prepared for evaluating the costing techniques and make a

recommendations to the board of directors of Belle Clinique on the implementation and

adoption of activity based costing technique. The budgeted manufacturing overhead costs for

year 2020 is proposed to be analysed using the activity based costing. It has been found that

the company is facing the price pressure for one of its product that is ILP. On other hand,

increased sales is reported for its product HRL as the price of the product is very competitive.

Total manufacturing overhead is recorded at $ 8645000 and the budgeted machine hours is

910000 hours. The reason attributable to the significant production overhead is because of the

specialized equipment and significant automation. The overhead of production is allocated to

the products based on machine hours in the current costing system. Pricing of all the products

are don at cost and including the allocated production overhead.

Discussion:

Development and history of ABC system:

The inadequacy of the cost accounting resulted in the introduction of the activity

based costing technique and the objective of introducing such costing was to overcome the

difficulties of dividing the production into core activities. Increasing complexities of the

business resulted in devising a system that resulted in the allocation of cost that resulted in

assigning the cost accurately. One of the well-known system of management accounting in

the last twenty years is activity based costing. Allocation of costs is done in a better way and

the basis of assigning the cost are the different cost drivers (Almeida & Cunha, 2017). In the

mid 80’s, the method of activity based costing was perceived so that the misleading

allocation of overhead is corrected. It is admitted by many scholars and practitioners that

there are various pitfalls of activity based costing. It is also explained that the implementation

Introduction:

The report is prepared for evaluating the costing techniques and make a

recommendations to the board of directors of Belle Clinique on the implementation and

adoption of activity based costing technique. The budgeted manufacturing overhead costs for

year 2020 is proposed to be analysed using the activity based costing. It has been found that

the company is facing the price pressure for one of its product that is ILP. On other hand,

increased sales is reported for its product HRL as the price of the product is very competitive.

Total manufacturing overhead is recorded at $ 8645000 and the budgeted machine hours is

910000 hours. The reason attributable to the significant production overhead is because of the

specialized equipment and significant automation. The overhead of production is allocated to

the products based on machine hours in the current costing system. Pricing of all the products

are don at cost and including the allocated production overhead.

Discussion:

Development and history of ABC system:

The inadequacy of the cost accounting resulted in the introduction of the activity

based costing technique and the objective of introducing such costing was to overcome the

difficulties of dividing the production into core activities. Increasing complexities of the

business resulted in devising a system that resulted in the allocation of cost that resulted in

assigning the cost accurately. One of the well-known system of management accounting in

the last twenty years is activity based costing. Allocation of costs is done in a better way and

the basis of assigning the cost are the different cost drivers (Almeida & Cunha, 2017). In the

mid 80’s, the method of activity based costing was perceived so that the misleading

allocation of overhead is corrected. It is admitted by many scholars and practitioners that

there are various pitfalls of activity based costing. It is also explained that the implementation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED MANAGEMENT ACCOUNTING

of the costing system is expensive and particularly in the service industries, many failures

have been observed.

Identifying the price pressure and contribution of the current costing system:

IPL is the most popular product of the company and the pricing pressure is

experienced by the company in terms of higher price of this particular product compared to

its competitors. This in turn has resulted in falling sales of IPL. However, the specialized

product of the company such as HRL is competitive in the smaller market and increased sales

is being reported. In the current process of production, there is a requirement of specialized

equipment and significant automation and this has resulted in significantly increasing the

production overhead. The production overhead under the current system of costing is

allocated to the products based on machine hours (Chiwamit et al., 2017). This has resulted in

increasing the total overhead cost of the products as it can be observed that the machine hours

required to produce the product such as ILP is just double that machine hours required by the

product HRL.

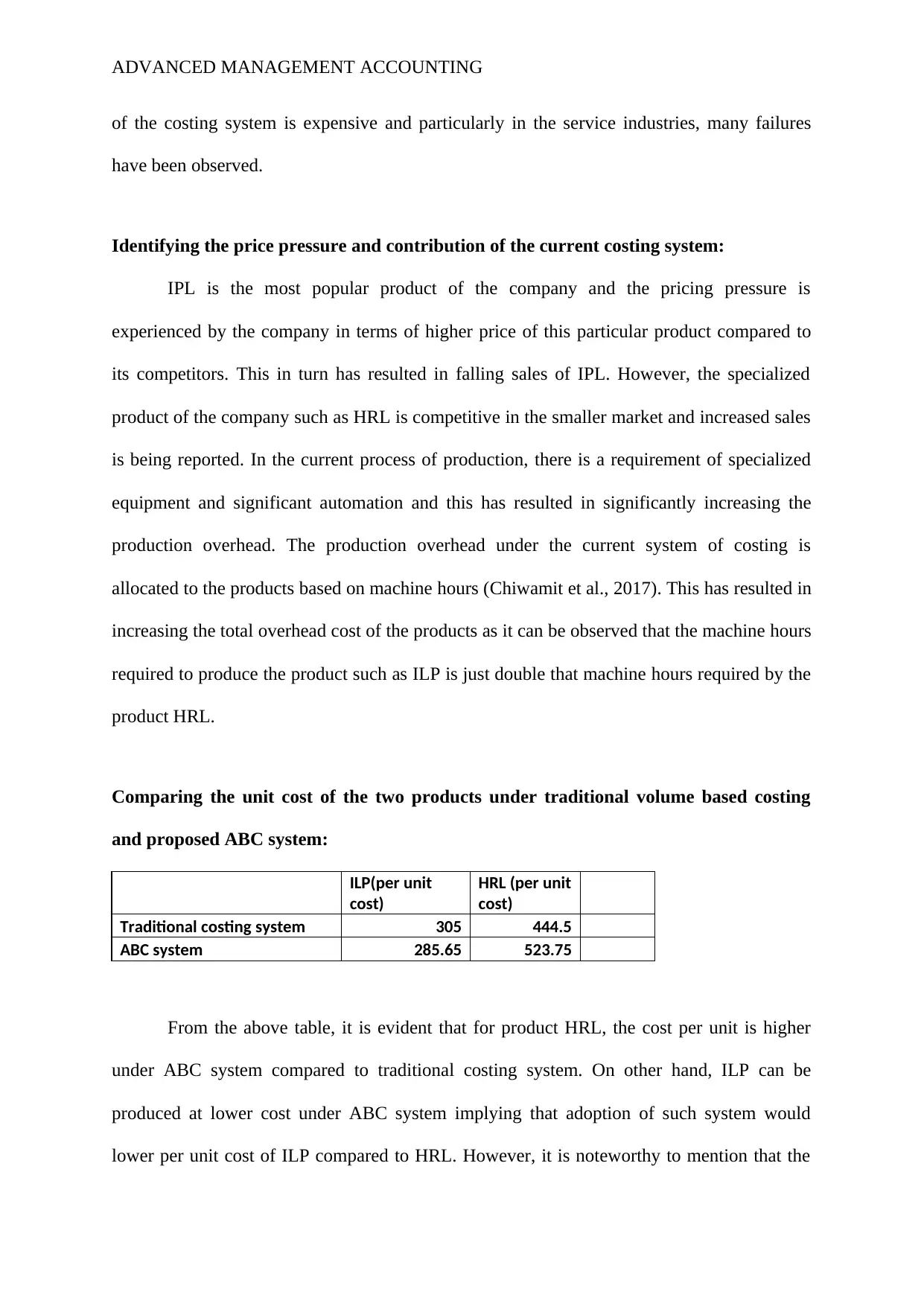

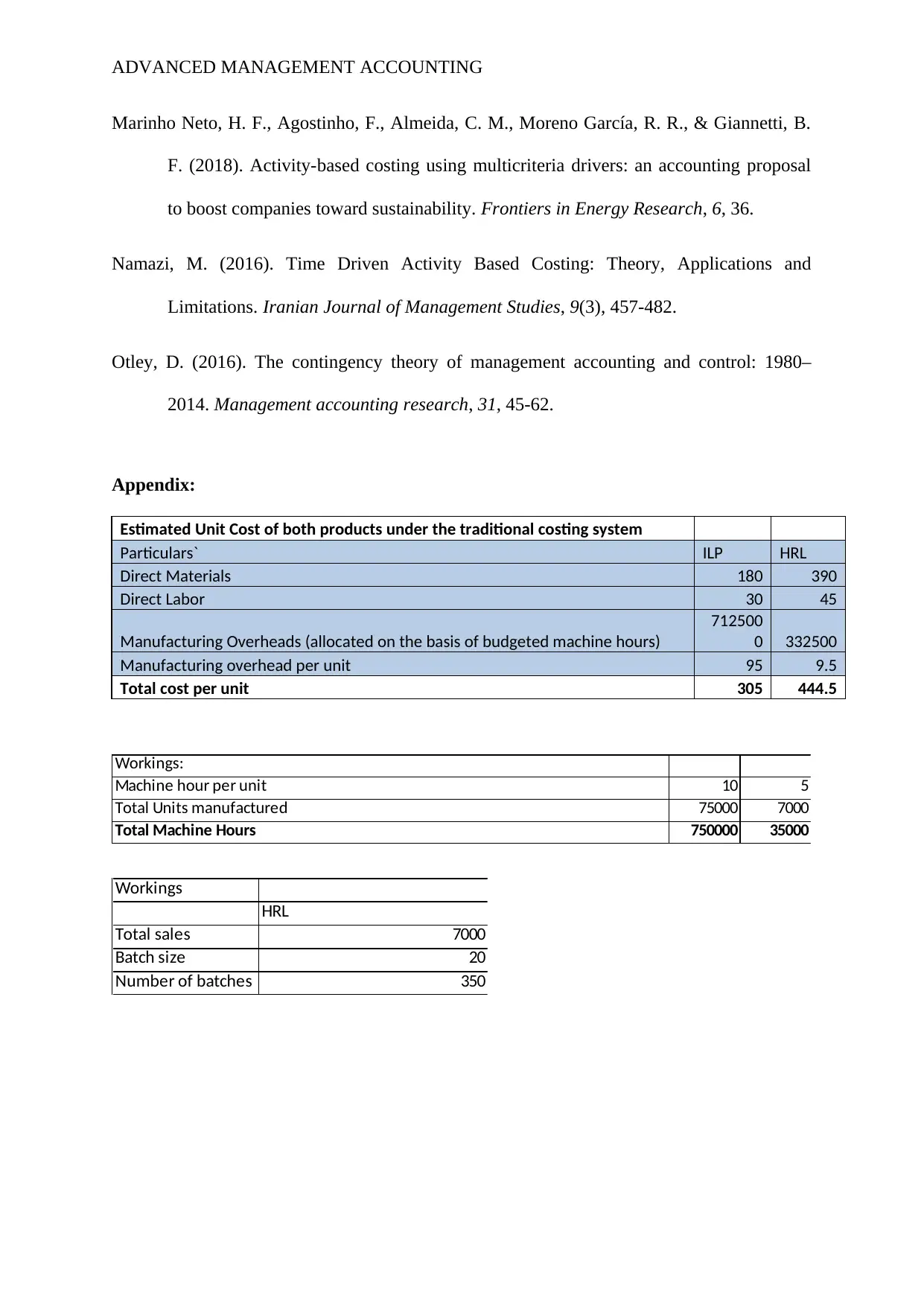

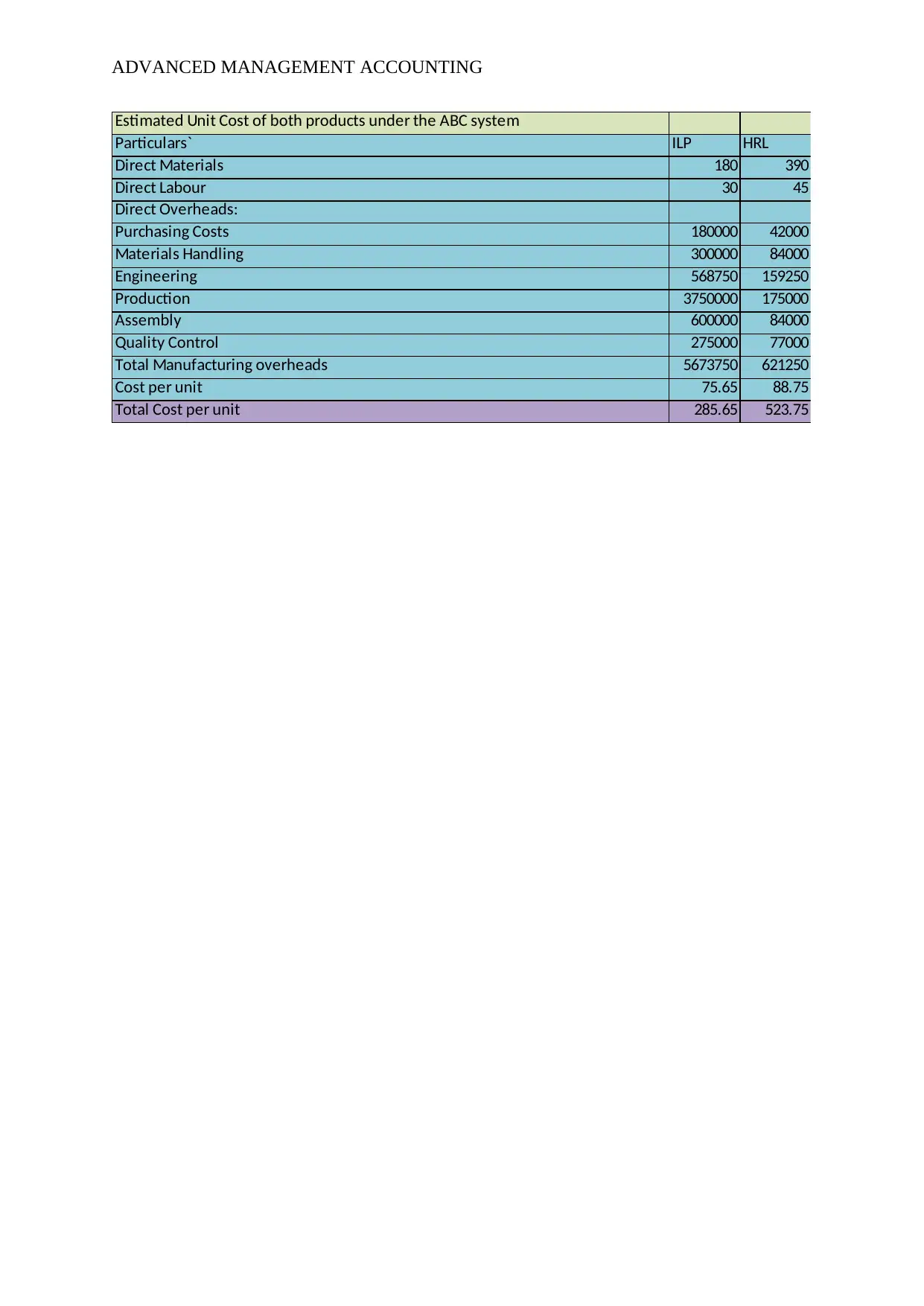

Comparing the unit cost of the two products under traditional volume based costing

and proposed ABC system:

ILP(per unit

cost)

HRL (per unit

cost)

Traditional costing system 305 444.5

ABC system 285.65 523.75

From the above table, it is evident that for product HRL, the cost per unit is higher

under ABC system compared to traditional costing system. On other hand, ILP can be

produced at lower cost under ABC system implying that adoption of such system would

lower per unit cost of ILP compared to HRL. However, it is noteworthy to mention that the

of the costing system is expensive and particularly in the service industries, many failures

have been observed.

Identifying the price pressure and contribution of the current costing system:

IPL is the most popular product of the company and the pricing pressure is

experienced by the company in terms of higher price of this particular product compared to

its competitors. This in turn has resulted in falling sales of IPL. However, the specialized

product of the company such as HRL is competitive in the smaller market and increased sales

is being reported. In the current process of production, there is a requirement of specialized

equipment and significant automation and this has resulted in significantly increasing the

production overhead. The production overhead under the current system of costing is

allocated to the products based on machine hours (Chiwamit et al., 2017). This has resulted in

increasing the total overhead cost of the products as it can be observed that the machine hours

required to produce the product such as ILP is just double that machine hours required by the

product HRL.

Comparing the unit cost of the two products under traditional volume based costing

and proposed ABC system:

ILP(per unit

cost)

HRL (per unit

cost)

Traditional costing system 305 444.5

ABC system 285.65 523.75

From the above table, it is evident that for product HRL, the cost per unit is higher

under ABC system compared to traditional costing system. On other hand, ILP can be

produced at lower cost under ABC system implying that adoption of such system would

lower per unit cost of ILP compared to HRL. However, it is noteworthy to mention that the

ADVANCED MANAGEMENT ACCOUNTING

total cost of the products under the traditional method is lower than ABC system.

Nevertheless, in order to make ILP competitive, it is recommended to adopt ABC.

Five options for improving the profitability of the products:

The pricing of the products should be done accurately so that the competitive pricing

is offered by the company and thereby helps in return maximization.

Profitability of the products can be improved by decreasing the total overhead costs. It

can be observed from the given case that the company is incurring a significant

overhead cost and this is perhaps attributable to higher machine hours for one of its

product. It is therefore required by the company to take measures to save the energy

by making running of the machinery for less hours.

It is also observed from the given case of Bell Clinique that the sale of one of its

product that is IPL has reduced and this has been due to the competitive pressure as

the competitors are selling the products at lower price. It is important for the company

to revise the selling price of the product and mark the price of the product

competitively so that the sales can be increased (Chiwamit et al., 2017).

Any increase in price should be selected along the product lines to some selected

market. It is important for the company to account for the change in pricing of the

product and price should only be increased until the demand for the same level offs.

Price should be set back if there is a fall in the cash generated due to fall in demand.

Some of the strategies of competitive pricing should be adopted so that the company

and its product stand above the competition. These strategies includes marking the

product pricing using the strategy of pricing below competition or pricing above

competition. In the case of pricing above competition, it is important for the company

total cost of the products under the traditional method is lower than ABC system.

Nevertheless, in order to make ILP competitive, it is recommended to adopt ABC.

Five options for improving the profitability of the products:

The pricing of the products should be done accurately so that the competitive pricing

is offered by the company and thereby helps in return maximization.

Profitability of the products can be improved by decreasing the total overhead costs. It

can be observed from the given case that the company is incurring a significant

overhead cost and this is perhaps attributable to higher machine hours for one of its

product. It is therefore required by the company to take measures to save the energy

by making running of the machinery for less hours.

It is also observed from the given case of Bell Clinique that the sale of one of its

product that is IPL has reduced and this has been due to the competitive pressure as

the competitors are selling the products at lower price. It is important for the company

to revise the selling price of the product and mark the price of the product

competitively so that the sales can be increased (Chiwamit et al., 2017).

Any increase in price should be selected along the product lines to some selected

market. It is important for the company to account for the change in pricing of the

product and price should only be increased until the demand for the same level offs.

Price should be set back if there is a fall in the cash generated due to fall in demand.

Some of the strategies of competitive pricing should be adopted so that the company

and its product stand above the competition. These strategies includes marking the

product pricing using the strategy of pricing below competition or pricing above

competition. In the case of pricing above competition, it is important for the company

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ADVANCED MANAGEMENT ACCOUNTING

to justify such higher price in terms of exclusivity, location and unique service to

customers (Namazi, 2016).

Identifying five arguments supporting the implementation of ABC and five options

against the adoption of ABC:

Five arguments supporting the implementation of ABC are as follows:

Customer activities can be effectively identified using such costing system and the

costs particularly allocated to certain customers are tracked using activity based

costing.

Costs of the product are determined reliably and accurately as the main focus of the

costing system is on cause and effect. This is because it is recognized by the costing

system that the activities are consumed by the product and costs is increased due to

the products. In the event of greater diversity amongst the manufactured products,

correct and reliable data on the product cost is provided by ABC system (Otley,

2016).

Since the main issue of the company is increasing overhead cost, it is considered

suitable to adopt the ABC system as the real and true nature of the costs can be

identified. The activities causing the overhead fixed cost can be easily tracked and can

be brought down to the profitable level (Allain & Laurin, 2018).

Activities cost is traced to the processes, managerial responsibility, departments and

customers beside the cost of the products.

Information on the volume of transaction and rates of cost drivers is provided by ABC

and the drivers can be used by the company in advantageous manner for the product

designing.

to justify such higher price in terms of exclusivity, location and unique service to

customers (Namazi, 2016).

Identifying five arguments supporting the implementation of ABC and five options

against the adoption of ABC:

Five arguments supporting the implementation of ABC are as follows:

Customer activities can be effectively identified using such costing system and the

costs particularly allocated to certain customers are tracked using activity based

costing.

Costs of the product are determined reliably and accurately as the main focus of the

costing system is on cause and effect. This is because it is recognized by the costing

system that the activities are consumed by the product and costs is increased due to

the products. In the event of greater diversity amongst the manufactured products,

correct and reliable data on the product cost is provided by ABC system (Otley,

2016).

Since the main issue of the company is increasing overhead cost, it is considered

suitable to adopt the ABC system as the real and true nature of the costs can be

identified. The activities causing the overhead fixed cost can be easily tracked and can

be brought down to the profitable level (Allain & Laurin, 2018).

Activities cost is traced to the processes, managerial responsibility, departments and

customers beside the cost of the products.

Information on the volume of transaction and rates of cost drivers is provided by ABC

and the drivers can be used by the company in advantageous manner for the product

designing.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED MANAGEMENT ACCOUNTING

A range of application can be resulted from the cost driver identification and activity

cost pooling. This would cause the cost reduction to foster and spare capacity

identification (Hopper & Bui, 2016).

Four arguments against the adoption of ABC system:

Numerous cost driver and cost pools makes the activity based costing system

complex.

For the implementation of the costing system, some measurement are required to have

in place for the allocation of costs.

Implementation of costing system is difficult due to assignment of common cost, cost

driver selection and varying rates of cost driver. Management is required to estimate

the cost for measuring and identifying the cost drivers so that the base of allocations

can be served (Marinho et al., 2018).

Application of activity based costing is not suitable when the overhead cost is

relatively low and it can be observed from the case of Belle Clinique that they have

significant overhead for one of the products. This costing system make use of

information technology as the allocation of cost requires to collect a lot of costing

data and for the information analysis. It is likely to increase the overhead cost of the

products sold.

Recommendation and conclusion:

From the analysis of the case of Belle Clinique, it is observed that the current system

of costing the products is not profitable for the product ILP as it is increasing the total

overhead cost. Adoption of activity based costing system would help in addressing the

ongoing issue of costing and pricing of the product for generating profits. It is therefore

recommended to implement and adopt activity based costing technique.

A range of application can be resulted from the cost driver identification and activity

cost pooling. This would cause the cost reduction to foster and spare capacity

identification (Hopper & Bui, 2016).

Four arguments against the adoption of ABC system:

Numerous cost driver and cost pools makes the activity based costing system

complex.

For the implementation of the costing system, some measurement are required to have

in place for the allocation of costs.

Implementation of costing system is difficult due to assignment of common cost, cost

driver selection and varying rates of cost driver. Management is required to estimate

the cost for measuring and identifying the cost drivers so that the base of allocations

can be served (Marinho et al., 2018).

Application of activity based costing is not suitable when the overhead cost is

relatively low and it can be observed from the case of Belle Clinique that they have

significant overhead for one of the products. This costing system make use of

information technology as the allocation of cost requires to collect a lot of costing

data and for the information analysis. It is likely to increase the overhead cost of the

products sold.

Recommendation and conclusion:

From the analysis of the case of Belle Clinique, it is observed that the current system

of costing the products is not profitable for the product ILP as it is increasing the total

overhead cost. Adoption of activity based costing system would help in addressing the

ongoing issue of costing and pricing of the product for generating profits. It is therefore

recommended to implement and adopt activity based costing technique.

ADVANCED MANAGEMENT ACCOUNTING

References list:

Abdel-Maksoud, A., Cheffi, W., & Ghoudi, K. (2016). The mediating effect of shop-floor

involvement on relations between advanced management accounting practices and

operational non-financial performance indicators. The British Accounting

Review, 48(2), 169-184.

Allain, E., & Laurin, C. (2018). Explaining implementation difficulties associated with

activity-based costing through system uses. Journal of Applied Accounting Research.

Almeida, A., & Cunha, J. (2017). The implementation of an Activity-Based Costing (ABC)

system in a manufacturing company. Procedia manufacturing, 13, 932-939.

Chiwamit, P., Modell, S., & Scapens, R. W. (2017). Regulation and adaptation of

management accounting innovations: The case of economic value added in Thai state-

owned enterprises. Management Accounting Research, 37, 30-48.

Hoozée, S., & Hansen, S. C. (2018). A comparison of activity-based costing and time-driven

activity-based costing. Journal of Management Accounting Research, 30(1), 143-167.

Hopper, T., & Bui, B. (2016). Has management accounting research been

critical?. Management Accounting Research, 31, 10-30.

References list:

Abdel-Maksoud, A., Cheffi, W., & Ghoudi, K. (2016). The mediating effect of shop-floor

involvement on relations between advanced management accounting practices and

operational non-financial performance indicators. The British Accounting

Review, 48(2), 169-184.

Allain, E., & Laurin, C. (2018). Explaining implementation difficulties associated with

activity-based costing through system uses. Journal of Applied Accounting Research.

Almeida, A., & Cunha, J. (2017). The implementation of an Activity-Based Costing (ABC)

system in a manufacturing company. Procedia manufacturing, 13, 932-939.

Chiwamit, P., Modell, S., & Scapens, R. W. (2017). Regulation and adaptation of

management accounting innovations: The case of economic value added in Thai state-

owned enterprises. Management Accounting Research, 37, 30-48.

Hoozée, S., & Hansen, S. C. (2018). A comparison of activity-based costing and time-driven

activity-based costing. Journal of Management Accounting Research, 30(1), 143-167.

Hopper, T., & Bui, B. (2016). Has management accounting research been

critical?. Management Accounting Research, 31, 10-30.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ADVANCED MANAGEMENT ACCOUNTING

Marinho Neto, H. F., Agostinho, F., Almeida, C. M., Moreno García, R. R., & Giannetti, B.

F. (2018). Activity-based costing using multicriteria drivers: an accounting proposal

to boost companies toward sustainability. Frontiers in Energy Research, 6, 36.

Namazi, M. (2016). Time Driven Activity Based Costing: Theory, Applications and

Limitations. Iranian Journal of Management Studies, 9(3), 457-482.

Otley, D. (2016). The contingency theory of management accounting and control: 1980–

2014. Management accounting research, 31, 45-62.

Appendix:

Estimated Unit Cost of both products under the traditional costing system

Particulars` ILP HRL

Direct Materials 180 390

Direct Labor 30 45

Manufacturing Overheads (allocated on the basis of budgeted machine hours)

712500

0 332500

Manufacturing overhead per unit 95 9.5

Total cost per unit 305 444.5

Workings:

Machine hour per unit 10 5

Total Units manufactured 75000 7000

Total Machine Hours 750000 35000

Workings

HRL

Total sales 7000

Batch size 20

Number of batches 350

Marinho Neto, H. F., Agostinho, F., Almeida, C. M., Moreno García, R. R., & Giannetti, B.

F. (2018). Activity-based costing using multicriteria drivers: an accounting proposal

to boost companies toward sustainability. Frontiers in Energy Research, 6, 36.

Namazi, M. (2016). Time Driven Activity Based Costing: Theory, Applications and

Limitations. Iranian Journal of Management Studies, 9(3), 457-482.

Otley, D. (2016). The contingency theory of management accounting and control: 1980–

2014. Management accounting research, 31, 45-62.

Appendix:

Estimated Unit Cost of both products under the traditional costing system

Particulars` ILP HRL

Direct Materials 180 390

Direct Labor 30 45

Manufacturing Overheads (allocated on the basis of budgeted machine hours)

712500

0 332500

Manufacturing overhead per unit 95 9.5

Total cost per unit 305 444.5

Workings:

Machine hour per unit 10 5

Total Units manufactured 75000 7000

Total Machine Hours 750000 35000

Workings

HRL

Total sales 7000

Batch size 20

Number of batches 350

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED MANAGEMENT ACCOUNTING

Estimated Unit Cost of both products under the ABC system

Particulars` ILP HRL

Direct Materials 180 390

Direct Labour 30 45

Direct Overheads:

Purchasing Costs 180000 42000

Materials Handling 300000 84000

Engineering 568750 159250

Production 3750000 175000

Assembly 600000 84000

Quality Control 275000 77000

Total Manufacturing overheads 5673750 621250

Cost per unit 75.65 88.75

Total Cost per unit 285.65 523.75

Estimated Unit Cost of both products under the ABC system

Particulars` ILP HRL

Direct Materials 180 390

Direct Labour 30 45

Direct Overheads:

Purchasing Costs 180000 42000

Materials Handling 300000 84000

Engineering 568750 159250

Production 3750000 175000

Assembly 600000 84000

Quality Control 275000 77000

Total Manufacturing overheads 5673750 621250

Cost per unit 75.65 88.75

Total Cost per unit 285.65 523.75

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.