Advanced Management Accounting Report: Role, Benefits, and Techniques

VerifiedAdded on 2023/06/04

|16

|3813

|173

Report

AI Summary

This report provides a comprehensive overview of advanced management accounting, beginning with an introduction to its core concepts and its relationship to cost accounting. The literature review examines both previous and current research, highlighting key developments and identifying gaps in the existing body of knowledge. The report then delves into the strategic role and benefits of management accounting, emphasizing its contribution to competitive advantage, market share improvement, and disciplined business practices. Strategic management accounting techniques, including Kaizen Costing, are discussed in detail. The report concludes by summarizing the key findings, outlining the significance of advanced management accounting, and suggesting areas for further study. The report also emphasizes the importance of strategic planning, decision-making frameworks, and the alignment of accounting practices with overall business objectives. The report is designed to provide students with a thorough understanding of the subject, and is available on Desklib, a platform offering past papers and solved assignments.

Running head- Advanced management accounting

ADVANCED MANAGEMENT ACCOUNTING

ADVANCED MANAGEMENT ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Advanced management accounting

Table of Contents

Part 1 Introduction...........................................................................................................................2

Part 2 Literature review...................................................................................................................3

Introduction..................................................................................................................................3

Evaluation of previous literature..................................................................................................3

Evaluation of current literature review........................................................................................4

Gap analysis.................................................................................................................................5

Part 3 Role and benefits of strategic management accounting........................................................5

Role of strategic management accounting...................................................................................5

Benefits of strategic accounting management:............................................................................6

Part 4 Strategic management accounting techniques.......................................................................7

Part 5 Summary...............................................................................................................................9

Advanced management accounting

Table of Contents

Part 1 Introduction...........................................................................................................................2

Part 2 Literature review...................................................................................................................3

Introduction..................................................................................................................................3

Evaluation of previous literature..................................................................................................3

Evaluation of current literature review........................................................................................4

Gap analysis.................................................................................................................................5

Part 3 Role and benefits of strategic management accounting........................................................5

Role of strategic management accounting...................................................................................5

Benefits of strategic accounting management:............................................................................6

Part 4 Strategic management accounting techniques.......................................................................7

Part 5 Summary...............................................................................................................................9

2

Advanced management accounting

Part 1 Introduction

Advanced management accounting is associated largely with cost accounting. It is mostly

said that management accounting begins from the point of the end of cost accounting. Cost

accounting is applicable when there is a requirement of measurement based on the performance

of business departments, concerning selling and purchase of goods and services. The

management accountant acts as an ‘information manager’ within the premise of business. The

accountant keeps the information in the record in order to assist management. The information

collected intends to organize and manage business operations that further help with decision-

making.

In order to fulfill the role, it is important to direct management in terms of precisely the

collection, significance, area, and requirement of the information. A significant part of advanced

management accounting is to help business manage the consequences and implications of a

strategic plan, project, mitigation or decision. Further, a lot of actions deal comes into facilitation

of future and predetermined systems. In such cases, budgetary control and standard costing are

taken into granted towards investigating actual performance. The information is strategically re-

arranged, evaluated in documenting change requirement and profit outcome. Both standard

costing and budget control actions using variances help in examining the result of actual

performance. Thereby, the risks and gaps between planned performances and actual performance

are discovered.

Managers in the contemporary period, sustaining the complex global situations, is currently

using management accounting information that not only helps to choose a strategy and make

relevant but ways to best to implement it. It is rightfully used in business to synchronize

decisions and objectives about organizing, building, packaging, manufacturing, producing and

marketing a product or service. The study explores advanced accounting management in 5 parts.

Part 1 introduces Strategic Management Accounting and areas that the study explores. Part 2

focuses on the literary review of advanced accounting management and practices from previous

and current study highlighting the gap between both. Part 3 identifies the role and benefits of

advanced and strategic accounting management. Part 4 details with the accounting techniques

Advanced management accounting

Part 1 Introduction

Advanced management accounting is associated largely with cost accounting. It is mostly

said that management accounting begins from the point of the end of cost accounting. Cost

accounting is applicable when there is a requirement of measurement based on the performance

of business departments, concerning selling and purchase of goods and services. The

management accountant acts as an ‘information manager’ within the premise of business. The

accountant keeps the information in the record in order to assist management. The information

collected intends to organize and manage business operations that further help with decision-

making.

In order to fulfill the role, it is important to direct management in terms of precisely the

collection, significance, area, and requirement of the information. A significant part of advanced

management accounting is to help business manage the consequences and implications of a

strategic plan, project, mitigation or decision. Further, a lot of actions deal comes into facilitation

of future and predetermined systems. In such cases, budgetary control and standard costing are

taken into granted towards investigating actual performance. The information is strategically re-

arranged, evaluated in documenting change requirement and profit outcome. Both standard

costing and budget control actions using variances help in examining the result of actual

performance. Thereby, the risks and gaps between planned performances and actual performance

are discovered.

Managers in the contemporary period, sustaining the complex global situations, is currently

using management accounting information that not only helps to choose a strategy and make

relevant but ways to best to implement it. It is rightfully used in business to synchronize

decisions and objectives about organizing, building, packaging, manufacturing, producing and

marketing a product or service. The study explores advanced accounting management in 5 parts.

Part 1 introduces Strategic Management Accounting and areas that the study explores. Part 2

focuses on the literary review of advanced accounting management and practices from previous

and current study highlighting the gap between both. Part 3 identifies the role and benefits of

advanced and strategic accounting management. Part 4 details with the accounting techniques

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Advanced management accounting

focusing on ‘Kaizen Costing’. Part 5 summarizes the learning outcome, outlining significance

and scope of the further study.

Part 2 Literature review

Introduction

The term advanced cost management is used mostly in maintaining the function of a business.

However, as per development in small-scale businesses in different countries, managers are

falling back on accounting management, today. There cannot be any uniform definition as it

branches onto different segments from financial data collection, accounting, decision-making,

and strategic planning to budget control procedures. The main aim of accounting management is

to provide management accurate and relevant information in the form of presented data such as

reports, fact sheets, cash flow, and spreadsheets.

Evaluation of previous literature

Managers are largely dependent on information accountant and management with which it is

helped to increase value for customers. Simultaneously, it paves the way to reduction of costs of

products and services. For example, within a business organization, managers make decisions

based on performance, market demand, amount and kind of substance, technological use, change

of planning and execution processes and product designs. But, the decision made by manager is

associated with information from cost management. Wherein, accounting systems investigate all

the activities surrounding selling and purchase, economic events and transitions, transactions and

budget control that allow sales representatives and production supervisors with current details of

product life-cycle (Van, 2016).

Advanced management accounting

focusing on ‘Kaizen Costing’. Part 5 summarizes the learning outcome, outlining significance

and scope of the further study.

Part 2 Literature review

Introduction

The term advanced cost management is used mostly in maintaining the function of a business.

However, as per development in small-scale businesses in different countries, managers are

falling back on accounting management, today. There cannot be any uniform definition as it

branches onto different segments from financial data collection, accounting, decision-making,

and strategic planning to budget control procedures. The main aim of accounting management is

to provide management accurate and relevant information in the form of presented data such as

reports, fact sheets, cash flow, and spreadsheets.

Evaluation of previous literature

Managers are largely dependent on information accountant and management with which it is

helped to increase value for customers. Simultaneously, it paves the way to reduction of costs of

products and services. For example, within a business organization, managers make decisions

based on performance, market demand, amount and kind of substance, technological use, change

of planning and execution processes and product designs. But, the decision made by manager is

associated with information from cost management. Wherein, accounting systems investigate all

the activities surrounding selling and purchase, economic events and transitions, transactions and

budget control that allow sales representatives and production supervisors with current details of

product life-cycle (Van, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Advanced management accounting

Figure 1- Components of management

(Source- Van, 2016)

Individual managers are largely dependent on information within the accounting system. The

accountant is to report budget plan and details differently both monthly and yearly. For example,

sales order information provides the total amount of sales to the manager that help to determine

the commissions that have to be paid (Van, 2016). Managers use strategic accounting practice

and management for the following reasons:

(a) To manage every activity within the functional area of responsibility

(b) To harmonize every activity within the targeted framework fulfilling the objective of

business

Evaluation of current literature review

Cost management, therefore, creates a broad focus. It aims at the continuous reduction of costs

using planning and control of costs. All the factors in making budget control is usually

inextricably profit planning, resources, target, and revenue. It is done by facilitating revenues

and profits, wherein additional costs are deliberately incurred towards product modifications. It,

therefore, becomes an important part of management strategies identifying effective

implementation (Ismail, Isa & Mia, 2018). With proper information come new changes that help

in product development and broadening targeted performance. This is associated with customer

Advanced management accounting

Figure 1- Components of management

(Source- Van, 2016)

Individual managers are largely dependent on information within the accounting system. The

accountant is to report budget plan and details differently both monthly and yearly. For example,

sales order information provides the total amount of sales to the manager that help to determine

the commissions that have to be paid (Van, 2016). Managers use strategic accounting practice

and management for the following reasons:

(a) To manage every activity within the functional area of responsibility

(b) To harmonize every activity within the targeted framework fulfilling the objective of

business

Evaluation of current literature review

Cost management, therefore, creates a broad focus. It aims at the continuous reduction of costs

using planning and control of costs. All the factors in making budget control is usually

inextricably profit planning, resources, target, and revenue. It is done by facilitating revenues

and profits, wherein additional costs are deliberately incurred towards product modifications. It,

therefore, becomes an important part of management strategies identifying effective

implementation (Ismail, Isa & Mia, 2018). With proper information come new changes that help

in product development and broadening targeted performance. This is associated with customer

5

Advanced management accounting

satisfaction and quality and promotion of new- product development. Strategic accounting is

based on the skills of an account manager who is required to succeed in the skills as follows:

1. Communication skills

2. Team coordination and re-building

3. Analytical mind and risk-solving skill

Critical mind with accuracy

4. A proper understanding of accounting

5. Able to foresee a change

6. Conduct timely and coordinated business functions

6. Computer skills and use of technology

Cost management also helps to conduct an economic transaction that is based on entails

collecting, validating, identifying, and analyzing. For example, within cost management, the

budget is taking into consideration based on cost categories that include resources, labor charge,

materials, and shipping. The information is summarized so that total costs can be examined

based on month, quarter, or year. It is here when it is found of change of price between years.

Thereby the financial statements such as balance sheet, cash flow, income statement,

performance reports are presented in identifying the cost of operating within the business. It has

been described (Honggowati, Rahmawati, Aryani & Probohudono, 2017)that accounting

management refers to various approaches and activities that are undertaken by managers in

building short-run and long-run decisions

Gap analysis

The growing employ of information technology in the prospect has had helped management

accountants to make an easy flow of information. Besides, they are able to spend a lower

proportion of time using financial statement (Honggowati et al., 2017). It helps to prepare proper

financial analysis developing the growth of the business. The three different strands of

management accounting are that has been missed in the previous literature review in comparison

to the current study are-

Advanced management accounting

satisfaction and quality and promotion of new- product development. Strategic accounting is

based on the skills of an account manager who is required to succeed in the skills as follows:

1. Communication skills

2. Team coordination and re-building

3. Analytical mind and risk-solving skill

Critical mind with accuracy

4. A proper understanding of accounting

5. Able to foresee a change

6. Conduct timely and coordinated business functions

6. Computer skills and use of technology

Cost management also helps to conduct an economic transaction that is based on entails

collecting, validating, identifying, and analyzing. For example, within cost management, the

budget is taking into consideration based on cost categories that include resources, labor charge,

materials, and shipping. The information is summarized so that total costs can be examined

based on month, quarter, or year. It is here when it is found of change of price between years.

Thereby the financial statements such as balance sheet, cash flow, income statement,

performance reports are presented in identifying the cost of operating within the business. It has

been described (Honggowati, Rahmawati, Aryani & Probohudono, 2017)that accounting

management refers to various approaches and activities that are undertaken by managers in

building short-run and long-run decisions

Gap analysis

The growing employ of information technology in the prospect has had helped management

accountants to make an easy flow of information. Besides, they are able to spend a lower

proportion of time using financial statement (Honggowati et al., 2017). It helps to prepare proper

financial analysis developing the growth of the business. The three different strands of

management accounting are that has been missed in the previous literature review in comparison

to the current study are-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

Advanced management accounting

Extension from internal activities within business management accounting

To investigate external information regarding the current market and competitors

Understanding from the relationship that exists between the strategic position and

demanded an emphasis on management accounting

Develop ways to gain viable improvement throughout exploiting connections within the

value chain.

While previous literature review focuses on the strategic role of management accounting that

helps in identifying, formulating and supporting the targeted demands of business using

strategies: current literature review conducts area of developments using an integrated

framework of accounting, enhancing performance and productivity.

Part 3 Role and benefits of strategic management accounting

Role of strategic management accounting

The strategic management is referred to as an effective process conducting activities of

management using strategic techniques fulfilling the vision of the business. It accompanies in

developing long-term strategies. Certainly, the role of strategic management accounting becomes

processes and resource allocation that is performed by an accountant manager to achieve

business goals. Strategic management plays an important role in fulfilling the needs of business’

long-term success using clear, strategic and well-defined plans (Rikhardsson & Yigitbasioglu,

2018). Using various information collected from different functional areas, it puts into action to

achieve its goals assessing employee performance, product/service value and business activities.

Managers have been dependent on building cost accounting so much so that they are able to

develop cost leadership strategies. The strategies are based on economic forecasts that help

business to improve and enhance its market share within a complex and competitive

marketplace. Management Accounting is different from Financial Accounting. It is dependent on

various factors that are kept into consideration such as product quality and demand,

organizational objectives, allocation of costs, sales, inventories and profit (Chiwamit, Modell &

Scapens, 2017). Accounting management is held responsible for allowing managers to generate

Advanced management accounting

Extension from internal activities within business management accounting

To investigate external information regarding the current market and competitors

Understanding from the relationship that exists between the strategic position and

demanded an emphasis on management accounting

Develop ways to gain viable improvement throughout exploiting connections within the

value chain.

While previous literature review focuses on the strategic role of management accounting that

helps in identifying, formulating and supporting the targeted demands of business using

strategies: current literature review conducts area of developments using an integrated

framework of accounting, enhancing performance and productivity.

Part 3 Role and benefits of strategic management accounting

Role of strategic management accounting

The strategic management is referred to as an effective process conducting activities of

management using strategic techniques fulfilling the vision of the business. It accompanies in

developing long-term strategies. Certainly, the role of strategic management accounting becomes

processes and resource allocation that is performed by an accountant manager to achieve

business goals. Strategic management plays an important role in fulfilling the needs of business’

long-term success using clear, strategic and well-defined plans (Rikhardsson & Yigitbasioglu,

2018). Using various information collected from different functional areas, it puts into action to

achieve its goals assessing employee performance, product/service value and business activities.

Managers have been dependent on building cost accounting so much so that they are able to

develop cost leadership strategies. The strategies are based on economic forecasts that help

business to improve and enhance its market share within a complex and competitive

marketplace. Management Accounting is different from Financial Accounting. It is dependent on

various factors that are kept into consideration such as product quality and demand,

organizational objectives, allocation of costs, sales, inventories and profit (Chiwamit, Modell &

Scapens, 2017). Accounting management is held responsible for allowing managers to generate

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

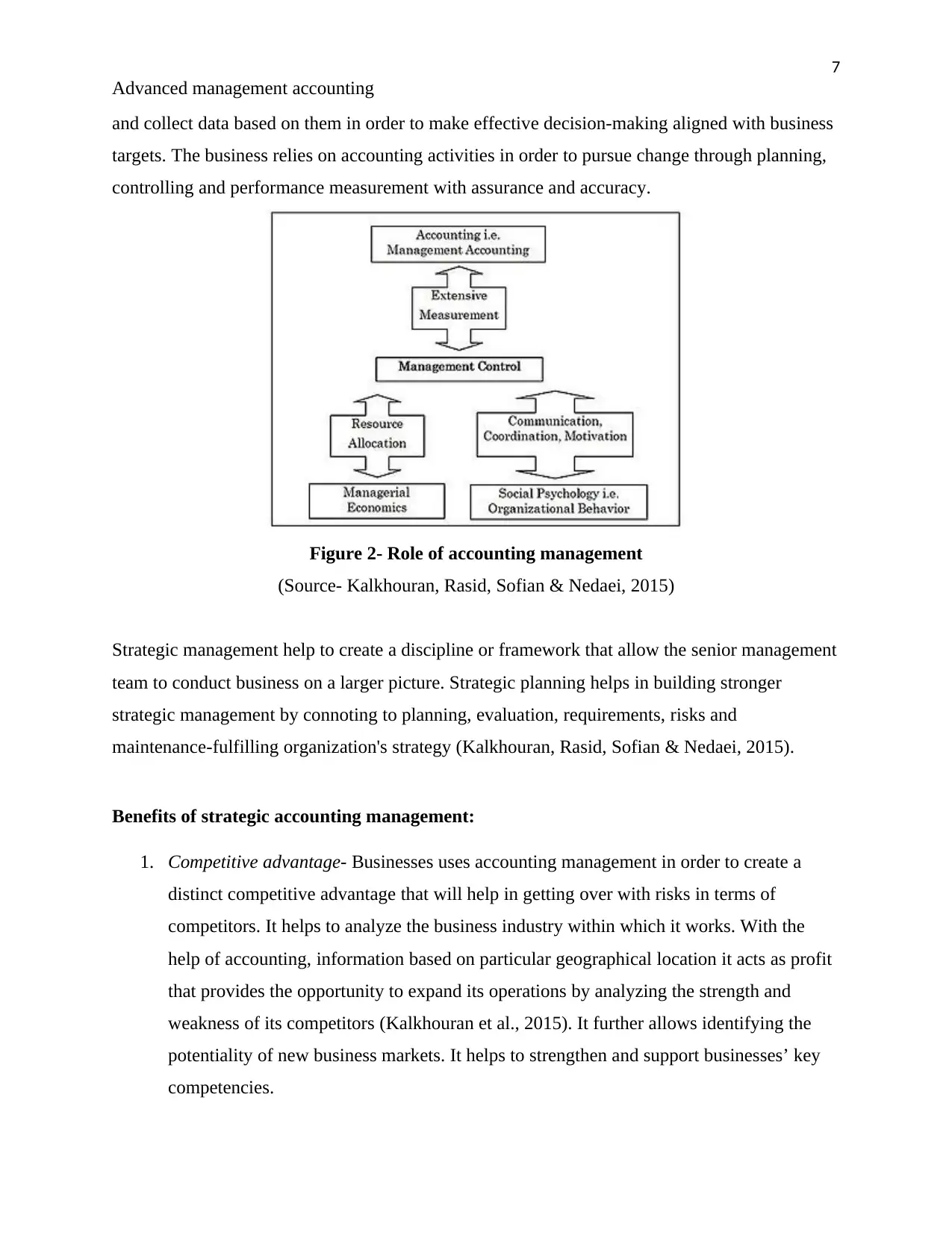

Advanced management accounting

and collect data based on them in order to make effective decision-making aligned with business

targets. The business relies on accounting activities in order to pursue change through planning,

controlling and performance measurement with assurance and accuracy.

Figure 2- Role of accounting management

(Source- Kalkhouran, Rasid, Sofian & Nedaei, 2015)

Strategic management help to create a discipline or framework that allow the senior management

team to conduct business on a larger picture. Strategic planning helps in building stronger

strategic management by connoting to planning, evaluation, requirements, risks and

maintenance-fulfilling organization's strategy (Kalkhouran, Rasid, Sofian & Nedaei, 2015).

Benefits of strategic accounting management:

1. Competitive advantage- Businesses uses accounting management in order to create a

distinct competitive advantage that will help in getting over with risks in terms of

competitors. It helps to analyze the business industry within which it works. With the

help of accounting, information based on particular geographical location it acts as profit

that provides the opportunity to expand its operations by analyzing the strength and

weakness of its competitors (Kalkhouran et al., 2015). It further allows identifying the

potentiality of new business markets. It helps to strengthen and support businesses’ key

competencies.

Advanced management accounting

and collect data based on them in order to make effective decision-making aligned with business

targets. The business relies on accounting activities in order to pursue change through planning,

controlling and performance measurement with assurance and accuracy.

Figure 2- Role of accounting management

(Source- Kalkhouran, Rasid, Sofian & Nedaei, 2015)

Strategic management help to create a discipline or framework that allow the senior management

team to conduct business on a larger picture. Strategic planning helps in building stronger

strategic management by connoting to planning, evaluation, requirements, risks and

maintenance-fulfilling organization's strategy (Kalkhouran, Rasid, Sofian & Nedaei, 2015).

Benefits of strategic accounting management:

1. Competitive advantage- Businesses uses accounting management in order to create a

distinct competitive advantage that will help in getting over with risks in terms of

competitors. It helps to analyze the business industry within which it works. With the

help of accounting, information based on particular geographical location it acts as profit

that provides the opportunity to expand its operations by analyzing the strength and

weakness of its competitors (Kalkhouran et al., 2015). It further allows identifying the

potentiality of new business markets. It helps to strengthen and support businesses’ key

competencies.

8

Advanced management accounting

2. Improve market share – business depends on accounting information to prepare cost

leadership strategies and to enhance strong economic forecasts. Both the actions help

business to improve its market share within the geography it works. It acts as an

advantage as it provides more profits for the business as it intends to expand its

operations. It helps to connect with SMEs that are emerging within the sector building in

smart market share.

3. Disciplined business- it is said that accounting management through strategic

implementation builds disciplined and organized performance. It bridges the gap

concerning risk and weakness, strengthens performance, and rewards for employees.

With its strategic planning and monitoring, business rationally grows aligned with its

financial feasibilities.

4. Framework for Decision-Making- Strategies are an integral part of building a framework

that can be sued by every manager to be used in daily operational decisions. It

investigates into the making of decisions ensuring that all are moving to business'

targeted direction. It is neither realistic nor practical to assume that every decision made

by the owner or Board of directors will be meeting targeted profit. Herein, strategic

accounting plays an important role by creating a plan examining the purpose and values

of an organization (Pan & Cao, 2016). It takes into consideration, profit, market demand,

sets objectives, threats and opportunities, in leveraging core strengths. It sets in a

framework aligned to these factors within boundaries of decisions that are being made.

The cumulative effects of decisions are aligned with the success of an organization.

Within the established framework, it becomes easier for the manager and directors to

make their decisions better that will support the organization's success.

Manager of a business unit complies with strategic management processes that are designed

towards long-term benefits. In following the advantages of the strategic accounting system, it

allows managers to find crisis within the business and foster prior changes (Pan & Cao, 2016).

The benefit outlines that a business unit or organization is provided a framework of objectives

and measures of success with the establishment of critical and strategic measures. It, therefore,

allows bringing in productivity, customer satisfaction, and profit.

Advanced management accounting

2. Improve market share – business depends on accounting information to prepare cost

leadership strategies and to enhance strong economic forecasts. Both the actions help

business to improve its market share within the geography it works. It acts as an

advantage as it provides more profits for the business as it intends to expand its

operations. It helps to connect with SMEs that are emerging within the sector building in

smart market share.

3. Disciplined business- it is said that accounting management through strategic

implementation builds disciplined and organized performance. It bridges the gap

concerning risk and weakness, strengthens performance, and rewards for employees.

With its strategic planning and monitoring, business rationally grows aligned with its

financial feasibilities.

4. Framework for Decision-Making- Strategies are an integral part of building a framework

that can be sued by every manager to be used in daily operational decisions. It

investigates into the making of decisions ensuring that all are moving to business'

targeted direction. It is neither realistic nor practical to assume that every decision made

by the owner or Board of directors will be meeting targeted profit. Herein, strategic

accounting plays an important role by creating a plan examining the purpose and values

of an organization (Pan & Cao, 2016). It takes into consideration, profit, market demand,

sets objectives, threats and opportunities, in leveraging core strengths. It sets in a

framework aligned to these factors within boundaries of decisions that are being made.

The cumulative effects of decisions are aligned with the success of an organization.

Within the established framework, it becomes easier for the manager and directors to

make their decisions better that will support the organization's success.

Manager of a business unit complies with strategic management processes that are designed

towards long-term benefits. In following the advantages of the strategic accounting system, it

allows managers to find crisis within the business and foster prior changes (Pan & Cao, 2016).

The benefit outlines that a business unit or organization is provided a framework of objectives

and measures of success with the establishment of critical and strategic measures. It, therefore,

allows bringing in productivity, customer satisfaction, and profit.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

Advanced management accounting

Part 4 Strategic management accounting techniques

With the advent of globalization and technological innovation, business is required to run

with a faster pace to meet customer demands. Besides, the competitive world market makes it

more difficult thereby information needs to be accurate and function-able ensuring proper flow

and productivity. The early detection of loopholes and risks will reduce the occurrence of

problems and bring in earlier solutions and targeted action (Rikhardsson & Yigitbasioglu, 2018).

From academic studies and review, it is gathered that in traditional management accounting the

techniques were quite different from what it is being used now. In fact, cost accounting

encountered continuous criticism as it used to provide information necessary for management,

performance while neglecting many significant documents and data (Rikhardsson &

Yigitbasioglu, 2018. It became difficult to generate reports with accuracy, as mostly it was

handwritten. It is claimed by researchers that it is interesting to conduct research study within the

field of management accounting (Chiwamit, Modell & Scapens, 2017). It has become strategic

by creating a link between accounting and management of contemporary organizations.

Advanced management accounting

Part 4 Strategic management accounting techniques

With the advent of globalization and technological innovation, business is required to run

with a faster pace to meet customer demands. Besides, the competitive world market makes it

more difficult thereby information needs to be accurate and function-able ensuring proper flow

and productivity. The early detection of loopholes and risks will reduce the occurrence of

problems and bring in earlier solutions and targeted action (Rikhardsson & Yigitbasioglu, 2018).

From academic studies and review, it is gathered that in traditional management accounting the

techniques were quite different from what it is being used now. In fact, cost accounting

encountered continuous criticism as it used to provide information necessary for management,

performance while neglecting many significant documents and data (Rikhardsson &

Yigitbasioglu, 2018. It became difficult to generate reports with accuracy, as mostly it was

handwritten. It is claimed by researchers that it is interesting to conduct research study within the

field of management accounting (Chiwamit, Modell & Scapens, 2017). It has become strategic

by creating a link between accounting and management of contemporary organizations.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

Advanced management accounting

(Self-made)

Strategic Management Accounting is associated with the following techniques that are used in

the contemporary period in building sustainable competitive advantage:

Strategic Cost Analysis

Target Costing

Cost management

Re-engineering of Business Process

Kaizen Costing

Action/activity-based management

Balanced scorecard

Life cycle costing

ManagementaccountingpracticeExternalOrienttationEmphasis-strategicpositioningcompetitieadvantgemarketshareInternalOrientationEmphasis-CostreductioncostmanagementandcontrolperformanceevaluationproductmanagementStrategicamnagementaccounting

Advanced management accounting

(Self-made)

Strategic Management Accounting is associated with the following techniques that are used in

the contemporary period in building sustainable competitive advantage:

Strategic Cost Analysis

Target Costing

Cost management

Re-engineering of Business Process

Kaizen Costing

Action/activity-based management

Balanced scorecard

Life cycle costing

ManagementaccountingpracticeExternalOrienttationEmphasis-strategicpositioningcompetitieadvantgemarketshareInternalOrientationEmphasis-CostreductioncostmanagementandcontrolperformanceevaluationproductmanagementStrategicamnagementaccounting

11

Advanced management accounting

Kaizen Costing

Kaizen costing has been defined by Yasuhiro Monden as the process that helps to maintain cost

levels for particular products that are manufactured using methodical efforts. It achieves the way

through which the desired cost level can be reduced (Clinton & England, 2016). The word kaizen

is a Japanese term that is used to describe continuous improvement (Nielsen, Mitchell &

Nørreklit, 2015). Within the area of business, it is referred cost reduction process. As per

Monden, there are two categories of kaizen costing that are described below:

1. Product based kaizen costing- in this costing method, the activities are carried out based

on exigencies of each sale, purchase, and dealing. Product model is derived in

understanding costing activities using value analysis.

2. An organization based on Kaizen costing- in this costing, the organization is focused on

understanding how far the cost of product help in reaching out market satisfaction. It

states whether the cost stands parallel to customer requirements. It also takes into

consideration the life-cycle of the product and its goal in reaching organizational

productivity.

Figure 3- Kaizen costing procedure

(Source- Cleary, 2015)

Advanced management accounting

Kaizen Costing

Kaizen costing has been defined by Yasuhiro Monden as the process that helps to maintain cost

levels for particular products that are manufactured using methodical efforts. It achieves the way

through which the desired cost level can be reduced (Clinton & England, 2016). The word kaizen

is a Japanese term that is used to describe continuous improvement (Nielsen, Mitchell &

Nørreklit, 2015). Within the area of business, it is referred cost reduction process. As per

Monden, there are two categories of kaizen costing that are described below:

1. Product based kaizen costing- in this costing method, the activities are carried out based

on exigencies of each sale, purchase, and dealing. Product model is derived in

understanding costing activities using value analysis.

2. An organization based on Kaizen costing- in this costing, the organization is focused on

understanding how far the cost of product help in reaching out market satisfaction. It

states whether the cost stands parallel to customer requirements. It also takes into

consideration the life-cycle of the product and its goal in reaching organizational

productivity.

Figure 3- Kaizen costing procedure

(Source- Cleary, 2015)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.