Advanced Management Accounting Report - Airdri Company Performance

VerifiedAdded on 2020/10/23

|17

|4463

|105

Report

AI Summary

This report provides a comprehensive analysis of advanced management accounting principles, using Airdri, a hand dryer manufacturing company, as a case study. It begins by examining the purpose and presentation of financial information from the perspective of various stakeholders, including investors, suppliers, and employees. The report then delves into different accounting microeconomic techniques, such as cost-volume-profit analysis, cost variance analysis, flexible budgeting, and activity-based costing, evaluating their application in supporting organizational performance and discussing their advantages and disadvantages. Furthermore, the report explores the concept of variance analysis and its importance for budgetary control, analyzing actual and standard costs to identify and correct variances. Finally, it addresses the impact of external and internal factors on management accounting, evaluating different types of decisions made in response to these changes and offering recommendations for future communication.

ADVANCED

MANAGEMENT

ACCOUNTING

MANAGEMENT

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Analysis of purpose and presentation of financial information from the perspective of

different stakeholders..................................................................................................................1

M1 Reasons of developing and appropriately presenting financial information to support

financial planning and decision making......................................................................................5

D1 Evaluation of Financial information.....................................................................................6

TASK 2 ...........................................................................................................................................6

P2 Evaluation of use of different accounting microeconomic techniques in application to

supporting organisational performance.......................................................................................6

M2 Advantages and disadvantages of accounting techniques....................................................7

TASK 3............................................................................................................................................8

P3 The concept of variance analysis and its importance for organisational budget control.......8

P4 Analysis of actual and standard costs which helps in control and correct variances.............9

M3 Advantages and disadvantages of different types of variances..........................................10

D2 Application of accounting techniques and variances..........................................................11

TASK 4..........................................................................................................................................11

P5 Impact of external and internal factors upon management accounting...............................11

M4 Impact of different types of decisions made to respond to these changes..........................12

D3 Impact of changes recommendations for future communication........................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Analysis of purpose and presentation of financial information from the perspective of

different stakeholders..................................................................................................................1

M1 Reasons of developing and appropriately presenting financial information to support

financial planning and decision making......................................................................................5

D1 Evaluation of Financial information.....................................................................................6

TASK 2 ...........................................................................................................................................6

P2 Evaluation of use of different accounting microeconomic techniques in application to

supporting organisational performance.......................................................................................6

M2 Advantages and disadvantages of accounting techniques....................................................7

TASK 3............................................................................................................................................8

P3 The concept of variance analysis and its importance for organisational budget control.......8

P4 Analysis of actual and standard costs which helps in control and correct variances.............9

M3 Advantages and disadvantages of different types of variances..........................................10

D2 Application of accounting techniques and variances..........................................................11

TASK 4..........................................................................................................................................11

P5 Impact of external and internal factors upon management accounting...............................11

M4 Impact of different types of decisions made to respond to these changes..........................12

D3 Impact of changes recommendations for future communication........................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is a process of preparing managerial accounts and statements

which are prepared by an organisation in order to serve managerial accounting information

information to related stakeholders such as creditors, investors, debtors, customers, employees

and may more. In order to understand the concept of management accounting, an organisation is

selected named Airdri. This company is hand dryer manufacturers which is considered as

underperforming organisation. As a management consultant, various aspects of this branch of

accounting are discussed in this report. Various purposes along with the presentation of financial

information is discussed in this project report in order to evaluate different accounting techniques

and its applications. The concept of budgetary control and variance analysis is also discussed in

detail in this project. External and internal factors which impacts management accounting of the

chosen company is mentioned in this report (Beams, 2017).

TASK 1

P1 Analysis of purpose and presentation of financial information from the perspective of

different stakeholders

Financial information is data related to monetary aspects of an organisation. This

information includes various financial statements and accounts. Any material information which

can affect functioning of a business is included in financial information. Airdri is a hand dryer

manufacturing company which operates in United Kingdom and maintains its financial

statements in order to serve reliable financial information to different stakeholders.

Purpose of financial information:

The primary purpose of financial information is to provide data about actual financial

position and performance of a company. Airdri is a hand dryer manufacturing company which is

facing several issues of intense competition and continuous technology up gradation due to

which they have are experiencing decline in their profitability and growth. Data which is gained

by financial information used by stakeholders of an organisation which includes investors,

employees, creditors, debtors, shareholders, suppliers and many more. Purpose of financial

information from the perspective of stakeholders of Airdri is described below:

Investors – Investors or prospect investors are the parties which invest their money in an

organisation. Investors of Airdri can assess the viability of investing in a company by evaluating

1

Management accounting is a process of preparing managerial accounts and statements

which are prepared by an organisation in order to serve managerial accounting information

information to related stakeholders such as creditors, investors, debtors, customers, employees

and may more. In order to understand the concept of management accounting, an organisation is

selected named Airdri. This company is hand dryer manufacturers which is considered as

underperforming organisation. As a management consultant, various aspects of this branch of

accounting are discussed in this report. Various purposes along with the presentation of financial

information is discussed in this project report in order to evaluate different accounting techniques

and its applications. The concept of budgetary control and variance analysis is also discussed in

detail in this project. External and internal factors which impacts management accounting of the

chosen company is mentioned in this report (Beams, 2017).

TASK 1

P1 Analysis of purpose and presentation of financial information from the perspective of

different stakeholders

Financial information is data related to monetary aspects of an organisation. This

information includes various financial statements and accounts. Any material information which

can affect functioning of a business is included in financial information. Airdri is a hand dryer

manufacturing company which operates in United Kingdom and maintains its financial

statements in order to serve reliable financial information to different stakeholders.

Purpose of financial information:

The primary purpose of financial information is to provide data about actual financial

position and performance of a company. Airdri is a hand dryer manufacturing company which is

facing several issues of intense competition and continuous technology up gradation due to

which they have are experiencing decline in their profitability and growth. Data which is gained

by financial information used by stakeholders of an organisation which includes investors,

employees, creditors, debtors, shareholders, suppliers and many more. Purpose of financial

information from the perspective of stakeholders of Airdri is described below:

Investors – Investors or prospect investors are the parties which invest their money in an

organisation. Investors of Airdri can assess the viability of investing in a company by evaluating

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the financial position of that company by their financial information. These parties interpret the

income statement of an organisation in order to check the income gaining capabilities of the

company so that they can make effective investment decisions (Fischer,2012).

Suppliers – Suppliers are the parties which supply their goods to an organisation so that

those goods can be further processed. From the financial information of Airdri such as cash flow

statement, suppliers can identify cash inflow and outflow of that company in order to determine

whether to supply goods on credit to them or not. Cash flow of an organisation has annual

inflows and outflows of cash from which manager of the company can ascertain liquidation

position of the company.

Government – Regularities and authorities which controls the organisation also needs

financial information of that company so that they can ascertain correctness of thei tax liabilities.

The main purpose of serving reliable financial information by Airdri is government of United

Kingdom and various other authorities.

Employees – All type of financial information is used by employees in order to develop

an understanding about the company where they are working. Employees of Airdri uses this

information for the purpose of identify their future remunerations. For example: By analysing

balance sheet of Airdri, their employees can ascertain if there is a possibility of annual bonus or

not.

Customers – The purpose behind using financial information such as sustainability

report of Airdri by their customers is to assess whether the company has resources to ensure

quality of goods and steady supply of goods or not (Maksy and Scott, 2015).

Presentation of Financial information:

Financial information of an organisation includes various statements and accounts but

some of them requires a certain specific format in which it should be presented so that it can

fulfil the purpose of stakeholders. This professional format is fixed by some international

regularities such as International Accounting Standards Board and others. The main objective

behind these formats is to bring uniformity in financial information of all the companies.

Presentation of few financial statements of Airdri is depicted below:

Income statements -

Income statements of a company shows revenues and expenses of a business. All

revenues and profits are recorded at the left or debit side of the statements and all the losses or

2

income statement of an organisation in order to check the income gaining capabilities of the

company so that they can make effective investment decisions (Fischer,2012).

Suppliers – Suppliers are the parties which supply their goods to an organisation so that

those goods can be further processed. From the financial information of Airdri such as cash flow

statement, suppliers can identify cash inflow and outflow of that company in order to determine

whether to supply goods on credit to them or not. Cash flow of an organisation has annual

inflows and outflows of cash from which manager of the company can ascertain liquidation

position of the company.

Government – Regularities and authorities which controls the organisation also needs

financial information of that company so that they can ascertain correctness of thei tax liabilities.

The main purpose of serving reliable financial information by Airdri is government of United

Kingdom and various other authorities.

Employees – All type of financial information is used by employees in order to develop

an understanding about the company where they are working. Employees of Airdri uses this

information for the purpose of identify their future remunerations. For example: By analysing

balance sheet of Airdri, their employees can ascertain if there is a possibility of annual bonus or

not.

Customers – The purpose behind using financial information such as sustainability

report of Airdri by their customers is to assess whether the company has resources to ensure

quality of goods and steady supply of goods or not (Maksy and Scott, 2015).

Presentation of Financial information:

Financial information of an organisation includes various statements and accounts but

some of them requires a certain specific format in which it should be presented so that it can

fulfil the purpose of stakeholders. This professional format is fixed by some international

regularities such as International Accounting Standards Board and others. The main objective

behind these formats is to bring uniformity in financial information of all the companies.

Presentation of few financial statements of Airdri is depicted below:

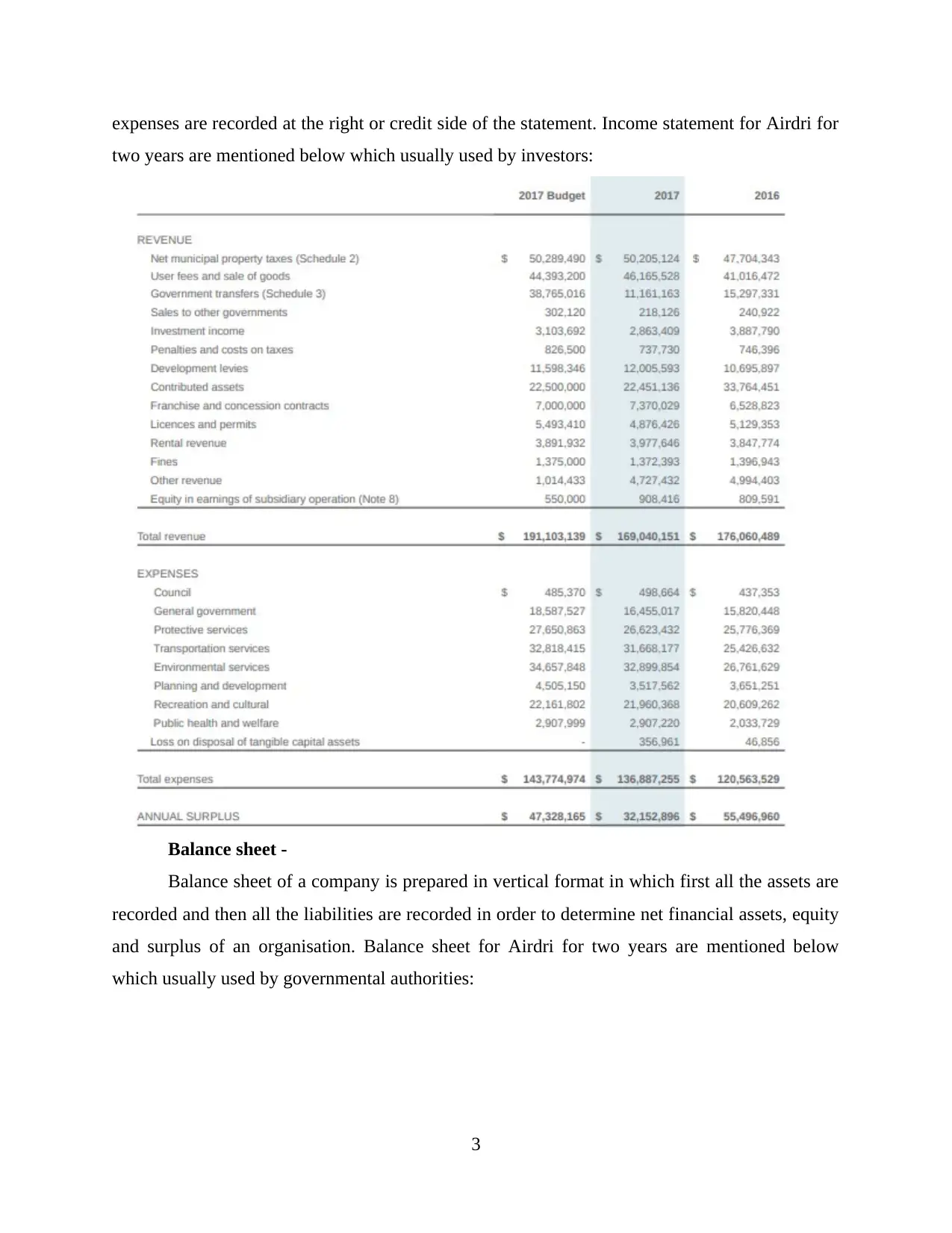

Income statements -

Income statements of a company shows revenues and expenses of a business. All

revenues and profits are recorded at the left or debit side of the statements and all the losses or

2

expenses are recorded at the right or credit side of the statement. Income statement for Airdri for

two years are mentioned below which usually used by investors:

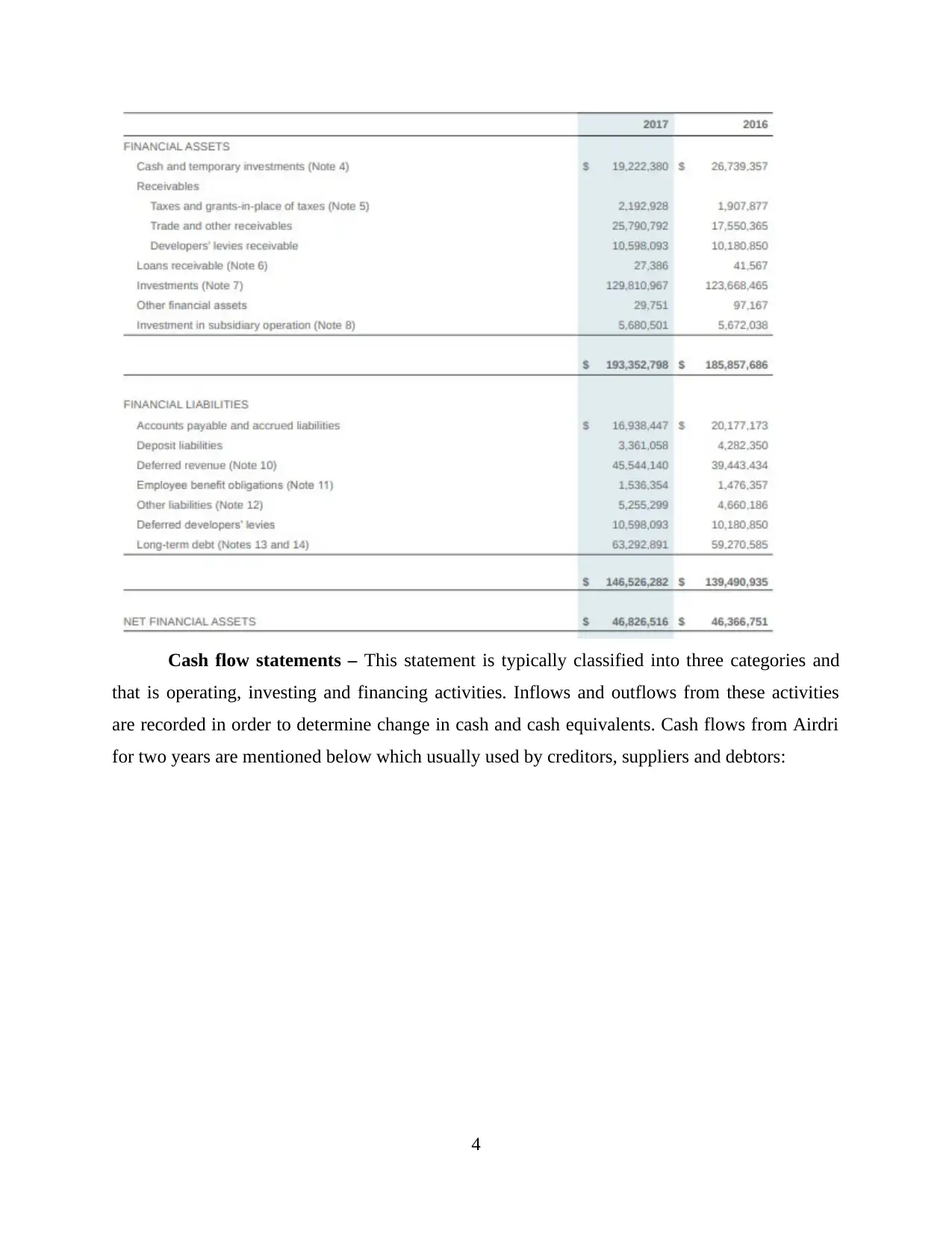

Balance sheet -

Balance sheet of a company is prepared in vertical format in which first all the assets are

recorded and then all the liabilities are recorded in order to determine net financial assets, equity

and surplus of an organisation. Balance sheet for Airdri for two years are mentioned below

which usually used by governmental authorities:

3

two years are mentioned below which usually used by investors:

Balance sheet -

Balance sheet of a company is prepared in vertical format in which first all the assets are

recorded and then all the liabilities are recorded in order to determine net financial assets, equity

and surplus of an organisation. Balance sheet for Airdri for two years are mentioned below

which usually used by governmental authorities:

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

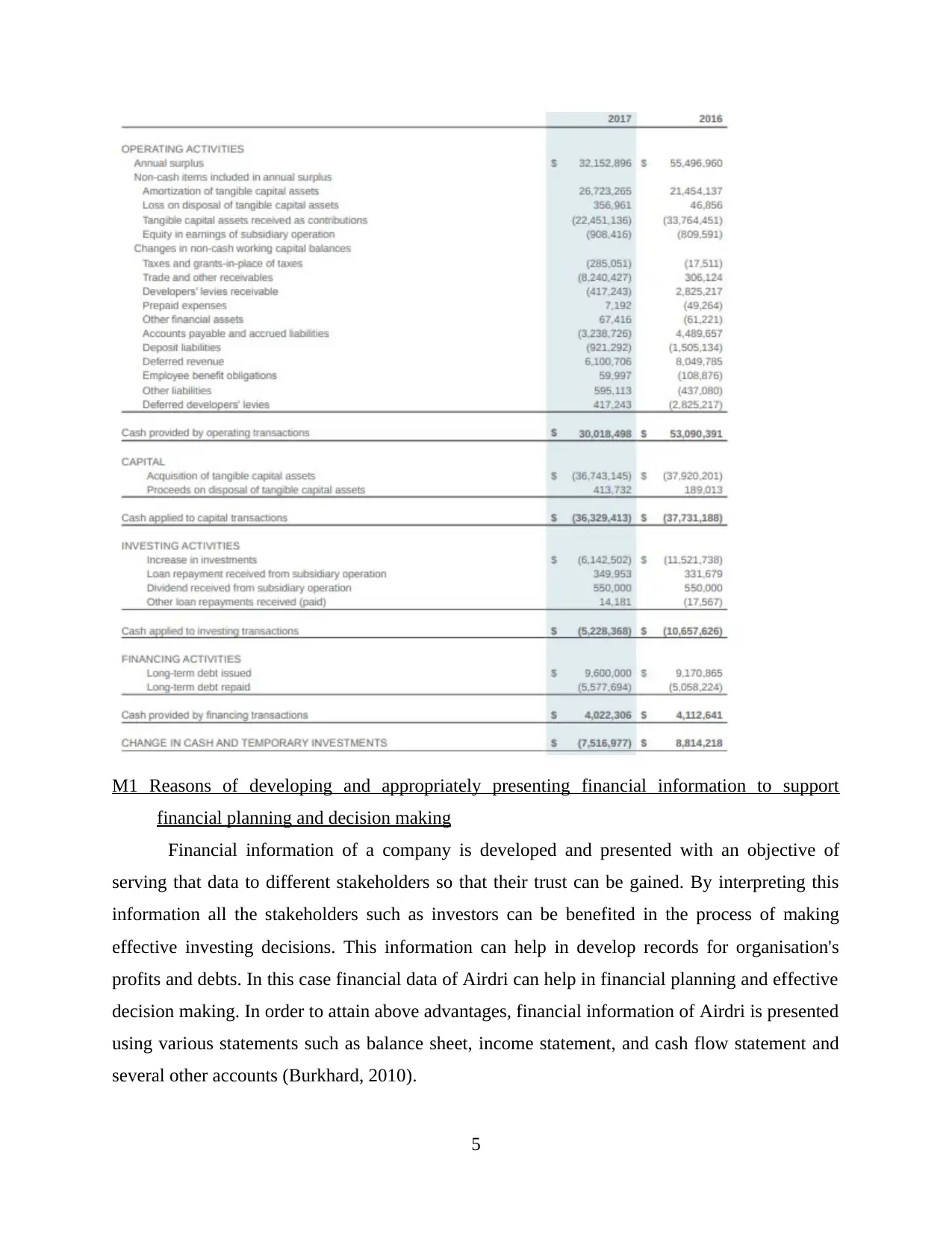

Cash flow statements – This statement is typically classified into three categories and

that is operating, investing and financing activities. Inflows and outflows from these activities

are recorded in order to determine change in cash and cash equivalents. Cash flows from Airdri

for two years are mentioned below which usually used by creditors, suppliers and debtors:

4

that is operating, investing and financing activities. Inflows and outflows from these activities

are recorded in order to determine change in cash and cash equivalents. Cash flows from Airdri

for two years are mentioned below which usually used by creditors, suppliers and debtors:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

M1 Reasons of developing and appropriately presenting financial information to support

financial planning and decision making

Financial information of a company is developed and presented with an objective of

serving that data to different stakeholders so that their trust can be gained. By interpreting this

information all the stakeholders such as investors can be benefited in the process of making

effective investing decisions. This information can help in develop records for organisation's

profits and debts. In this case financial data of Airdri can help in financial planning and effective

decision making. In order to attain above advantages, financial information of Airdri is presented

using various statements such as balance sheet, income statement, and cash flow statement and

several other accounts (Burkhard, 2010).

5

financial planning and decision making

Financial information of a company is developed and presented with an objective of

serving that data to different stakeholders so that their trust can be gained. By interpreting this

information all the stakeholders such as investors can be benefited in the process of making

effective investing decisions. This information can help in develop records for organisation's

profits and debts. In this case financial data of Airdri can help in financial planning and effective

decision making. In order to attain above advantages, financial information of Airdri is presented

using various statements such as balance sheet, income statement, and cash flow statement and

several other accounts (Burkhard, 2010).

5

D1 Evaluation of Financial information

According to Maria José da Silva Faria, financial information of an organisation holds

individual interests of various stakeholders. The core of this information is to create value for

group of stakeholders, not just individuals. This information is even more significant when the

position of an organisation is not sound. Financial information is different from managerial data

because it also records monetary transaction and follows quantitative approach rather than

qualitative approach.

TASK 2

P2 Evaluation of use of different accounting microeconomic techniques in application to

supporting organisational performance

Micro economic techniques of managerial accounting are the methods which are

concerned with micro economic issues of an organisation such as cost ascertainment, balance

between volume and profit and many more. The main aim of these techniques is to support

organisational performance. Types of these managerial accounting techniques along with their

uses are discussed below:

Cost volume profit analysis – This micro economic technique is used by organisations

like Airdri to determine the affect of changes of their costs and volume on company's operating

income and net income. This technique measures all the costs involved in all operations of the

company such as manufacturing, packaging, distributing and may more. The aim behind

measuring these costs is to analyse organisational current performance.

Cost variances analysis – This microeconomic technique is a performance evaluation

tool which evaluates cost center. This analysis is related with comparing actual costs to standard

costs in order to determine the variances and evaluate reasons of those changes. By conducting

this analysis, management of Airdri can ascertain what are the key reasons due to which situation

of variance has occurred. Airdri is a under performing organisation and this can be said by above

presented financial information, due to which analysis is most significant for them as they can

determine the reasons of their declining performance (Neubauer and Wood, 2013).

Flexible budgeting - This accounting microeconomic technique allows an organisation

to develop a cost measuring and tracking record which is prepared at the starting of an

accounting period but changes be change according to the unexpected expenses. Financial

6

According to Maria José da Silva Faria, financial information of an organisation holds

individual interests of various stakeholders. The core of this information is to create value for

group of stakeholders, not just individuals. This information is even more significant when the

position of an organisation is not sound. Financial information is different from managerial data

because it also records monetary transaction and follows quantitative approach rather than

qualitative approach.

TASK 2

P2 Evaluation of use of different accounting microeconomic techniques in application to

supporting organisational performance

Micro economic techniques of managerial accounting are the methods which are

concerned with micro economic issues of an organisation such as cost ascertainment, balance

between volume and profit and many more. The main aim of these techniques is to support

organisational performance. Types of these managerial accounting techniques along with their

uses are discussed below:

Cost volume profit analysis – This micro economic technique is used by organisations

like Airdri to determine the affect of changes of their costs and volume on company's operating

income and net income. This technique measures all the costs involved in all operations of the

company such as manufacturing, packaging, distributing and may more. The aim behind

measuring these costs is to analyse organisational current performance.

Cost variances analysis – This microeconomic technique is a performance evaluation

tool which evaluates cost center. This analysis is related with comparing actual costs to standard

costs in order to determine the variances and evaluate reasons of those changes. By conducting

this analysis, management of Airdri can ascertain what are the key reasons due to which situation

of variance has occurred. Airdri is a under performing organisation and this can be said by above

presented financial information, due to which analysis is most significant for them as they can

determine the reasons of their declining performance (Neubauer and Wood, 2013).

Flexible budgeting - This accounting microeconomic technique allows an organisation

to develop a cost measuring and tracking record which is prepared at the starting of an

accounting period but changes be change according to the unexpected expenses. Financial

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

performance of an organisation can also be ascertained by developing this record as it transacts

all budgeted and unexpected costs. For example, management of Airdri prepares this record in

order to identify variations between actual and budgeted costs which are usually unexpected

which helps to determine their actual financial performance.

Cost behaviour – In this technique of microeconomic managerial accounting, behaviour

of cost involvement is analysed in order to track and measure changes in incurred costs of an

organisation. Analysis of cost behaviour is a process in which changes and variances of costs are

measured and recorded in order to evaluate reasons of increase of organisational expenses due to

costs. For example: Airdri Limited uses this technique to look after their cost involvement in

their operations and activities so that they can ascertain their financial position.

Activity based costing – This technique of microeconomic accounting is important for

an organisation as it allows to determine costs involved in numerous activities of an organisation.

This ascertainment can help an organisation to identify which operation needs maximum costs

and the reasons of those high requirements. For example, Manager of Airdri can determine costs

involved in their all the operations in order to ascertain efficiency in their financial performance.

Above techniques are managerial accounting microeconomic techniques which are used

by Airdri to improve financial performance of their organisation. Costing techniques such as

marginal and standard costing helps an organisation to ascertain their cost involvement in

business operations. This cost involvement is classified as marginal and fixed cost which can

assist an organisation to maintain their performance as they can determine in which operation

costs needs to be reduced (Chen, 2012).

M2 Advantages and disadvantages of accounting techniques

The above discussed microeconomic managerial accounting techniques such as Activity

based costing, Cost volume profit analysis, Cost variances analysis has various advantages and

disadvantages which are mentioned below:

Advantages – These techniques helps in ascertaining cost occurred in organisational

operations and activities. These techniques can help in measuring financial performance of a

company and it also assists in controlling costs.

Disadvantages – Managerial accounting techniques requires certain skills and

knowledge which are not present in small scale organisations. Also organisations like Airdri has

7

all budgeted and unexpected costs. For example, management of Airdri prepares this record in

order to identify variations between actual and budgeted costs which are usually unexpected

which helps to determine their actual financial performance.

Cost behaviour – In this technique of microeconomic managerial accounting, behaviour

of cost involvement is analysed in order to track and measure changes in incurred costs of an

organisation. Analysis of cost behaviour is a process in which changes and variances of costs are

measured and recorded in order to evaluate reasons of increase of organisational expenses due to

costs. For example: Airdri Limited uses this technique to look after their cost involvement in

their operations and activities so that they can ascertain their financial position.

Activity based costing – This technique of microeconomic accounting is important for

an organisation as it allows to determine costs involved in numerous activities of an organisation.

This ascertainment can help an organisation to identify which operation needs maximum costs

and the reasons of those high requirements. For example, Manager of Airdri can determine costs

involved in their all the operations in order to ascertain efficiency in their financial performance.

Above techniques are managerial accounting microeconomic techniques which are used

by Airdri to improve financial performance of their organisation. Costing techniques such as

marginal and standard costing helps an organisation to ascertain their cost involvement in

business operations. This cost involvement is classified as marginal and fixed cost which can

assist an organisation to maintain their performance as they can determine in which operation

costs needs to be reduced (Chen, 2012).

M2 Advantages and disadvantages of accounting techniques

The above discussed microeconomic managerial accounting techniques such as Activity

based costing, Cost volume profit analysis, Cost variances analysis has various advantages and

disadvantages which are mentioned below:

Advantages – These techniques helps in ascertaining cost occurred in organisational

operations and activities. These techniques can help in measuring financial performance of a

company and it also assists in controlling costs.

Disadvantages – Managerial accounting techniques requires certain skills and

knowledge which are not present in small scale organisations. Also organisations like Airdri has

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

to employ much costs in order to use these techniques. The process of analysis requires ample of

time and money (Cory, 2011).

TASK 3

P3 The concept of variance analysis and its importance for organisational budget control

The term variance refers to the deviation between actual costs and standard costs of an

organisation. Variance analysis is a process of calculating the deviation between actual costs

which has incurred while manufacturing a product and standard costs which are budgeted by the

management that can be incurred by an organisation. The aim main of variance analysis is to

interpret the deviations in order to identify causes and reasons of variances. This process helps in

ascertaining magnitude of each variance and causes. In order to benefit the organisation from

budgetary control, various variances which can be ascertained are material, labour, overheads

and sales. Airdri Limited is a hand dryer manufacturer which uses variance analysis to look after

their budgetary control. Budgetary function of an organisation is the process in which

management of that company prepares several budgets using trend analyses in order to determine

the predicted costs (Siegel, 2010).

Importance of variance analysis for organisational budgetary control:

Budgetary control refers to the process of monitoring and controlling all the costs which

are incurred by an organisation in operations and activities. This process is for managers which

can get benefited by setting performance goals and budgets.

Variance analysis is a process which assist the managers of companies like Airdri to

control organisational budgets. This analysis is important as it manages budgets by controlling

budgeted versus actual costs. Aspects in which variance analysis helps in organisational

budgetary control are mentioned below:

Materiality – This aspect is related with material value which is ascertained while

calculating the variances and deviations. Materiality in the variance helps in controlling the

budgetary process. For example: Management of Airdri Limited has developed budget of cost

and by ascertaining variance they can analyse the reason behind the deviation. Variance is the

difference between actual and standard cost which can help organisation to ascertain reasons of

that deviations of that management of company can bring efficiency in their operations.

8

time and money (Cory, 2011).

TASK 3

P3 The concept of variance analysis and its importance for organisational budget control

The term variance refers to the deviation between actual costs and standard costs of an

organisation. Variance analysis is a process of calculating the deviation between actual costs

which has incurred while manufacturing a product and standard costs which are budgeted by the

management that can be incurred by an organisation. The aim main of variance analysis is to

interpret the deviations in order to identify causes and reasons of variances. This process helps in

ascertaining magnitude of each variance and causes. In order to benefit the organisation from

budgetary control, various variances which can be ascertained are material, labour, overheads

and sales. Airdri Limited is a hand dryer manufacturer which uses variance analysis to look after

their budgetary control. Budgetary function of an organisation is the process in which

management of that company prepares several budgets using trend analyses in order to determine

the predicted costs (Siegel, 2010).

Importance of variance analysis for organisational budgetary control:

Budgetary control refers to the process of monitoring and controlling all the costs which

are incurred by an organisation in operations and activities. This process is for managers which

can get benefited by setting performance goals and budgets.

Variance analysis is a process which assist the managers of companies like Airdri to

control organisational budgets. This analysis is important as it manages budgets by controlling

budgeted versus actual costs. Aspects in which variance analysis helps in organisational

budgetary control are mentioned below:

Materiality – This aspect is related with material value which is ascertained while

calculating the variances and deviations. Materiality in the variance helps in controlling the

budgetary process. For example: Management of Airdri Limited has developed budget of cost

and by ascertaining variance they can analyse the reason behind the deviation. Variance is the

difference between actual and standard cost which can help organisation to ascertain reasons of

that deviations of that management of company can bring efficiency in their operations.

8

Relationships – In this case of budgetary control, relationships are the relation between

actual and standard variables which are sometimes shoes deviations. In order to ascertain the

causes behind the variation between budgets and actual variables it is important to ascertain

relationship between those variables. For example: Airdri Limited is facing various issues in

recent years due to which they are considered as under performing company. Cost budgets of this

company are way lower than the actual costs and in order to improve their operations, this

company has to find reasons for deviation.

Forecasting – This is a technique in budgetary control in which organisation predicts

costs and expenses which can be occurred in future. Variance analysis is a procedure of

ascertaining deviations between actual and budgeted. In order to ascertain budgeted costs and

expenses for future, forecasting is the most important aspect (Daoud and Triki, 2013).

Range of techniques for decision making and investment:

NPV – Net present value is a measurement of profit which considers all future cash

flows. This method helps in making reliable decisions about investments as it helps in determine

which investment proposal is more profitable.

ARR - Accounting rate of return is also known as the simple or average rate of return,

measures the amount of profit, or return, expected on an investment. It divides the average profit

by the initial investment to derive the ratio or return that can be expected. ARR does not consider

the time value of money or cash flows, which can be an integral part of maintaining a business.

IRR – Internal rate of return is used in capital budgeting to determine profitability of

potential investments. This rate is a discounted rate that makes NPV of all cash flows from a

particular project equals to zero.

P4 Analysis of actual and standard costs which helps in control and correct variances

Actual and standard costs are the two variables which are used in ascertaining variances

of an organisation. These costs are determined from the financial information of an organisation.

Airdri is an organisation which uses these costs to control and correct their variances. Variances

are the deviations which occurred from the differences between actual and standard costs.

Actual costs – These costs are the expenses which are occurred from organisational

operations and activities. These costs are ascertained at the end of an accounting period when all

the expenses are already incurred. These costs are compared from standard costs in order to

9

actual and standard variables which are sometimes shoes deviations. In order to ascertain the

causes behind the variation between budgets and actual variables it is important to ascertain

relationship between those variables. For example: Airdri Limited is facing various issues in

recent years due to which they are considered as under performing company. Cost budgets of this

company are way lower than the actual costs and in order to improve their operations, this

company has to find reasons for deviation.

Forecasting – This is a technique in budgetary control in which organisation predicts

costs and expenses which can be occurred in future. Variance analysis is a procedure of

ascertaining deviations between actual and budgeted. In order to ascertain budgeted costs and

expenses for future, forecasting is the most important aspect (Daoud and Triki, 2013).

Range of techniques for decision making and investment:

NPV – Net present value is a measurement of profit which considers all future cash

flows. This method helps in making reliable decisions about investments as it helps in determine

which investment proposal is more profitable.

ARR - Accounting rate of return is also known as the simple or average rate of return,

measures the amount of profit, or return, expected on an investment. It divides the average profit

by the initial investment to derive the ratio or return that can be expected. ARR does not consider

the time value of money or cash flows, which can be an integral part of maintaining a business.

IRR – Internal rate of return is used in capital budgeting to determine profitability of

potential investments. This rate is a discounted rate that makes NPV of all cash flows from a

particular project equals to zero.

P4 Analysis of actual and standard costs which helps in control and correct variances

Actual and standard costs are the two variables which are used in ascertaining variances

of an organisation. These costs are determined from the financial information of an organisation.

Airdri is an organisation which uses these costs to control and correct their variances. Variances

are the deviations which occurred from the differences between actual and standard costs.

Actual costs – These costs are the expenses which are occurred from organisational

operations and activities. These costs are ascertained at the end of an accounting period when all

the expenses are already incurred. These costs are compared from standard costs in order to

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.