Advanced Management Accounting Analysis: Fletcher Building (FBU.NZ)

VerifiedAdded on 2020/04/07

|10

|3246

|85

Homework Assignment

AI Summary

This assignment provides a comprehensive analysis of Fletcher Building's management accounting practices. It begins by assessing the company's mission, vision, and strategy, proposing a new framework based on innovation, people, change, collaboration, industry belief, and transparency. The analysis then delves into activity-based costing (ABC) and its benefits for Fletcher Building, contrasting it with traditional methods and the Just-in-Time (JIT) system. The assignment further explores performance measurement systems, comparing integrated performance management systems with the balanced scorecard approach, and arguing for the latter's suitability. Finally, it examines the balanced scorecard in detail, outlining its four perspectives: financial, customer, internal, and innovation processes, and how Fletcher Building can leverage it to maximize its performance. The paper provides valuable insights into strategic management accounting for construction companies.

ADVANCED MANAGEMENT ACCOUNTING

Fletcher Building Ltd (FBU.NZ)

Fletcher Building Ltd (FBU.NZ)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fletcher building

Answer to 1

Mission and vision statement are the most vital ways that assist various companies to enact

change. Even companies already pursue their own mission, vision, and strategies, yet many lacks

or disregard some serious issues. In relation to this, a new mission, vision, and strategy for

Fletcher Building can be ascertained that can allow it to develop more in the future.

Fletcher building realizes that the best-performing companies always combine their strategies

with their mission and vision statement so that a great culture filled with accompanying values

can be created. Therefore, the best mission and vision would be the fulfillment of major six

values. Firstly, innovation wherein Fletcher must find new ways to advance and create new

opportunities so that it becomes effectively receptive to changes. Secondly, it must value people

by developing, identifying, and retaining individuals within their organization. Thirdly, Fletcher

must intend to focus on change and proceed by thinking big and starting small. Fourthly, it must

combine its skills and experience by operating collectively so that the company resources can be

easily leveraged with efficient communication. Fifthly, the company must aim to possess strong

beliefs in the entire industry (Fletcher building, 2017). This can be done by being enthusiastic

and considerate about its contribution to the overall community. Lastly, the company must

possess a transparency of its purpose so that it can easily do the right thing at the right time. With

the help of this new vision, Fletcher Building can easily cater to the needs of the entire

community. Besides, it can build better with the guidance of such new mission and vision

statement. Furthermore, the strategy adopted by the company does not allow it change and keep

pace with such change. This is very vital in the industry wherein the company operates because it

can not only survive but also develop with the help of a strategy that allows it to align with

market fluctuations. For such purpose, Fletcher Building may frame its strategy around four

building blocks of enhanced corporate performance. They are commercial transformation,

adoption of an asset-light approach, cost leadership, and sustainability respectively. Moreover, it

can be seen from the annual report of Fletcher Building that it has mature products that can allow

it to thrive in such competitive market. Thus, if the company successfully employs a harvest

strategy instead of a build strategy, it can easily attain its objectives of building better and

together (Vanderbeck, 2013). The reason behind this can be attributed to the fact that a harvest

strategy has more certainty, predictability, and change than a build strategy. Besides, a harvest

2

Answer to 1

Mission and vision statement are the most vital ways that assist various companies to enact

change. Even companies already pursue their own mission, vision, and strategies, yet many lacks

or disregard some serious issues. In relation to this, a new mission, vision, and strategy for

Fletcher Building can be ascertained that can allow it to develop more in the future.

Fletcher building realizes that the best-performing companies always combine their strategies

with their mission and vision statement so that a great culture filled with accompanying values

can be created. Therefore, the best mission and vision would be the fulfillment of major six

values. Firstly, innovation wherein Fletcher must find new ways to advance and create new

opportunities so that it becomes effectively receptive to changes. Secondly, it must value people

by developing, identifying, and retaining individuals within their organization. Thirdly, Fletcher

must intend to focus on change and proceed by thinking big and starting small. Fourthly, it must

combine its skills and experience by operating collectively so that the company resources can be

easily leveraged with efficient communication. Fifthly, the company must aim to possess strong

beliefs in the entire industry (Fletcher building, 2017). This can be done by being enthusiastic

and considerate about its contribution to the overall community. Lastly, the company must

possess a transparency of its purpose so that it can easily do the right thing at the right time. With

the help of this new vision, Fletcher Building can easily cater to the needs of the entire

community. Besides, it can build better with the guidance of such new mission and vision

statement. Furthermore, the strategy adopted by the company does not allow it change and keep

pace with such change. This is very vital in the industry wherein the company operates because it

can not only survive but also develop with the help of a strategy that allows it to align with

market fluctuations. For such purpose, Fletcher Building may frame its strategy around four

building blocks of enhanced corporate performance. They are commercial transformation,

adoption of an asset-light approach, cost leadership, and sustainability respectively. Moreover, it

can be seen from the annual report of Fletcher Building that it has mature products that can allow

it to thrive in such competitive market. Thus, if the company successfully employs a harvest

strategy instead of a build strategy, it can easily attain its objectives of building better and

together (Vanderbeck, 2013). The reason behind this can be attributed to the fact that a harvest

strategy has more certainty, predictability, and change than a build strategy. Besides, a harvest

2

Fletcher building

strategy is beneficial for organizations that possess mature products enjoying an enhanced share

of the market in lesser growth industries (Fletcher building, 2017). In addition to this, if Fletcher

Building adopts a harvest strategy, it can become more manageable and stagnant to maximize its

flow of cash and profitability. Therefore, this is the reason why a harvest strategy would be more

beneficial in the case of Fletcher Buildings.

Answer to 2

Fletcher Buildings is utilizing the activity-based costing system in order to derive more

explained information regarding the cost. Such system are not needed for the purpose of external

financial reporting, activity based costing is done apart from the process or job-order costing. In

this scenario, the company is using manufacturing, as well as non-manufacturing costs (Fletcher

building, 2017). Fletcher Buildings is engaged in the manufacturing and distribution of building

materials and might incur costs in the process of ordering, setting up of machinery, packaging

and post sale processes of customer services. In the case of Fletcher Buildings the ordering cost

is assigned like the ordering system to products. When the ordering gets completed, the costs can

be added to the cost of the product till the time the entire project gets completed (Drury, 2013).

Activity-based costing leads to an accurate way of product or service costing thereby providing a

better decision based on pricing. The understanding of the overheads gets enhanced along with

the cost drivers and thereby makes costly and non-value activities to be more visible in nature.

Hence, it allows managers to lessen them. ABC leads to an effective challenge when it comes to

the process of operating costs so that better means can be traced and overheads can be

eliminated. It even helps in enhancement of the product and the profitability evaluation of the

company manifolds (Marsh, 2009). The performance management notions of the company

enhance and continuous improvement can be projected. The system of ABC leads to direct

allocation of the indirect costs that are based on the cost driver of the product or the factors that

develop the cost (Drury, 2013). When the costs are allocated in terms of the product then the

scenario starts to develop in terms of the processes that is performing in a strong manner and the

ones that need to be enhanced. ABC can be utilized to trace the non-valued activities and can

lead to better allocation of the resources to efficient, as well as activities that are profitable in

nature. Further, the utilization of ABC for Fletcher Buildings can lead to the value addition and

regular enhancement in the process of the business. The best move for the company is to have

3

strategy is beneficial for organizations that possess mature products enjoying an enhanced share

of the market in lesser growth industries (Fletcher building, 2017). In addition to this, if Fletcher

Building adopts a harvest strategy, it can become more manageable and stagnant to maximize its

flow of cash and profitability. Therefore, this is the reason why a harvest strategy would be more

beneficial in the case of Fletcher Buildings.

Answer to 2

Fletcher Buildings is utilizing the activity-based costing system in order to derive more

explained information regarding the cost. Such system are not needed for the purpose of external

financial reporting, activity based costing is done apart from the process or job-order costing. In

this scenario, the company is using manufacturing, as well as non-manufacturing costs (Fletcher

building, 2017). Fletcher Buildings is engaged in the manufacturing and distribution of building

materials and might incur costs in the process of ordering, setting up of machinery, packaging

and post sale processes of customer services. In the case of Fletcher Buildings the ordering cost

is assigned like the ordering system to products. When the ordering gets completed, the costs can

be added to the cost of the product till the time the entire project gets completed (Drury, 2013).

Activity-based costing leads to an accurate way of product or service costing thereby providing a

better decision based on pricing. The understanding of the overheads gets enhanced along with

the cost drivers and thereby makes costly and non-value activities to be more visible in nature.

Hence, it allows managers to lessen them. ABC leads to an effective challenge when it comes to

the process of operating costs so that better means can be traced and overheads can be

eliminated. It even helps in enhancement of the product and the profitability evaluation of the

company manifolds (Marsh, 2009). The performance management notions of the company

enhance and continuous improvement can be projected. The system of ABC leads to direct

allocation of the indirect costs that are based on the cost driver of the product or the factors that

develop the cost (Drury, 2013). When the costs are allocated in terms of the product then the

scenario starts to develop in terms of the processes that is performing in a strong manner and the

ones that need to be enhanced. ABC can be utilized to trace the non-valued activities and can

lead to better allocation of the resources to efficient, as well as activities that are profitable in

nature. Further, the utilization of ABC for Fletcher Buildings can lead to the value addition and

regular enhancement in the process of the business. The best move for the company is to have

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Fletcher building

activity-based costing system as it is refined and provides better scope to the company. The

activities are settled and help the company in making the best out of the resource. Conventionally

is orthodox and hence, would not be able to cope with the prevailing situation as the environment

is dynamic in nature.

Just-in-time is majorly related to the batch size and reduces them on the other hand, the Activity-

based costing (ABC) is related to the calculation of the entire cost activities that is in tune with

the batches. JIT system will be a strong move as it will lead to a better association with the batch

size and will help the company to deliver.

Answer to 3

In the present dynamic business environment, performance measurement has become extremely

significant. Furthermore, even though financial measures have been the major focus in the past,

much more emphasis is being exerted upon non-financial approaches like the Balanced

Scorecard and Integrated Performance Measurement Systems. In relation to Fletcher Building

Ltd, it can be seen that the company has also used both these performance measurement systems.

An integrated performance management system is that measure which can easily integrate the

operational performance of an enterprise both vertically and horizontally, in a way that all the

activities support the strategic objectives and goals of the organization. Furthermore, this

measure reflects the collaboration and tight coupling of loosely associated business activities that

are interconnected with investment decision-making, strategic planning, forecasting, budgeting,

and reporting of performance. Fletcher Building Ltd utilizes such method in order to assess their

performance so that they can analyze whether their strategic goals and objectives are adequately

met or not. Besides, it can also be witnessed from the annual report of the company that it has

utilized non-GAAP measures as well, to evaluate its level of performance. Such emphasis on

non-financial measures has largely been witnessed in the case of most of the organizations

operating in New Zealand. On the other hand, a balanced scorecard is also a measure that can be

utilized to assess the level of performance of an organization. In relation to Fletcher Building

Ltd, it can be observed that the company has used such concept within its framework by

implementing several strategies, measuring performance, and compensating the employees by

4

activity-based costing system as it is refined and provides better scope to the company. The

activities are settled and help the company in making the best out of the resource. Conventionally

is orthodox and hence, would not be able to cope with the prevailing situation as the environment

is dynamic in nature.

Just-in-time is majorly related to the batch size and reduces them on the other hand, the Activity-

based costing (ABC) is related to the calculation of the entire cost activities that is in tune with

the batches. JIT system will be a strong move as it will lead to a better association with the batch

size and will help the company to deliver.

Answer to 3

In the present dynamic business environment, performance measurement has become extremely

significant. Furthermore, even though financial measures have been the major focus in the past,

much more emphasis is being exerted upon non-financial approaches like the Balanced

Scorecard and Integrated Performance Measurement Systems. In relation to Fletcher Building

Ltd, it can be seen that the company has also used both these performance measurement systems.

An integrated performance management system is that measure which can easily integrate the

operational performance of an enterprise both vertically and horizontally, in a way that all the

activities support the strategic objectives and goals of the organization. Furthermore, this

measure reflects the collaboration and tight coupling of loosely associated business activities that

are interconnected with investment decision-making, strategic planning, forecasting, budgeting,

and reporting of performance. Fletcher Building Ltd utilizes such method in order to assess their

performance so that they can analyze whether their strategic goals and objectives are adequately

met or not. Besides, it can also be witnessed from the annual report of the company that it has

utilized non-GAAP measures as well, to evaluate its level of performance. Such emphasis on

non-financial measures has largely been witnessed in the case of most of the organizations

operating in New Zealand. On the other hand, a balanced scorecard is also a measure that can be

utilized to assess the level of performance of an organization. In relation to Fletcher Building

Ltd, it can be observed that the company has used such concept within its framework by

implementing several strategies, measuring performance, and compensating the employees by

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fletcher building

framing objectives along different perspectives, and thereafter, linking them collectively with the

mission, vision, and strategy of the firm.

In comparison to both the previously mentioned performance measurement approaches, it must

be noted that balanced scorecard approach would be more suitable and effective for Fletcher

Building Ltd. The reason behind this can be attributed to the fact that a balanced scorecard

approach incorporates or takes into account both financial and non-financial measures within its

framework that is a positive indicator in terms of better evaluation of performance. The second

best advantage of using a balanced scorecard approach is that it is adequately designed to

compensate the lower-level employees (Horngren & Foster, 2008). This is a major positive

indicator because addressing lower level employees can prove to be immensely benefited for the

entire organization, as it not only takes into account cost issues but also attracts talented

employees that can enhance the organization’s productivity. Lastly, a balanced scorecard is

better than an integrated performance measurement system because it offers relevant details of

the performance of a company beyond that attained from the market-ascertained measures. This

clearly concludes the fact that a balanced scorecard approach is better and advantageous than an

integrated performance management system (Horngren & Foster, 2008). Therefore, adoption of

such measure would be more likely to assess performance in a better way than any other system.

Answer to 4

The balanced scorecard approach has widely been adopted by many organizations and is

observed as a strategic management approach in framing a performance management system.

Further, it has been identified that traditional financial approaches do not forecast the future

performance of an organization, as financial measures are ineffective indicators that are

subjected towards past performance. Nonetheless, by including non-financial measures, the

balanced scorecard approach attempts to offer managers with more material information than

that offered by financial measures about affairs they are presently managing (Larry &

Christopher, 2012). Moreover, this approach suggests that an organization’s capability to

generate value in the future will be driven by four significant viewpoints like internal learning

and process, customer, financial, and growth. Overall, this approach explains the knowledge,

systems, and skills that employees require to build and enhance the right strategic abilities and

efficiencies (Venanci, 2012).

5

framing objectives along different perspectives, and thereafter, linking them collectively with the

mission, vision, and strategy of the firm.

In comparison to both the previously mentioned performance measurement approaches, it must

be noted that balanced scorecard approach would be more suitable and effective for Fletcher

Building Ltd. The reason behind this can be attributed to the fact that a balanced scorecard

approach incorporates or takes into account both financial and non-financial measures within its

framework that is a positive indicator in terms of better evaluation of performance. The second

best advantage of using a balanced scorecard approach is that it is adequately designed to

compensate the lower-level employees (Horngren & Foster, 2008). This is a major positive

indicator because addressing lower level employees can prove to be immensely benefited for the

entire organization, as it not only takes into account cost issues but also attracts talented

employees that can enhance the organization’s productivity. Lastly, a balanced scorecard is

better than an integrated performance measurement system because it offers relevant details of

the performance of a company beyond that attained from the market-ascertained measures. This

clearly concludes the fact that a balanced scorecard approach is better and advantageous than an

integrated performance management system (Horngren & Foster, 2008). Therefore, adoption of

such measure would be more likely to assess performance in a better way than any other system.

Answer to 4

The balanced scorecard approach has widely been adopted by many organizations and is

observed as a strategic management approach in framing a performance management system.

Further, it has been identified that traditional financial approaches do not forecast the future

performance of an organization, as financial measures are ineffective indicators that are

subjected towards past performance. Nonetheless, by including non-financial measures, the

balanced scorecard approach attempts to offer managers with more material information than

that offered by financial measures about affairs they are presently managing (Larry &

Christopher, 2012). Moreover, this approach suggests that an organization’s capability to

generate value in the future will be driven by four significant viewpoints like internal learning

and process, customer, financial, and growth. Overall, this approach explains the knowledge,

systems, and skills that employees require to build and enhance the right strategic abilities and

efficiencies (Venanci, 2012).

5

Fletcher building

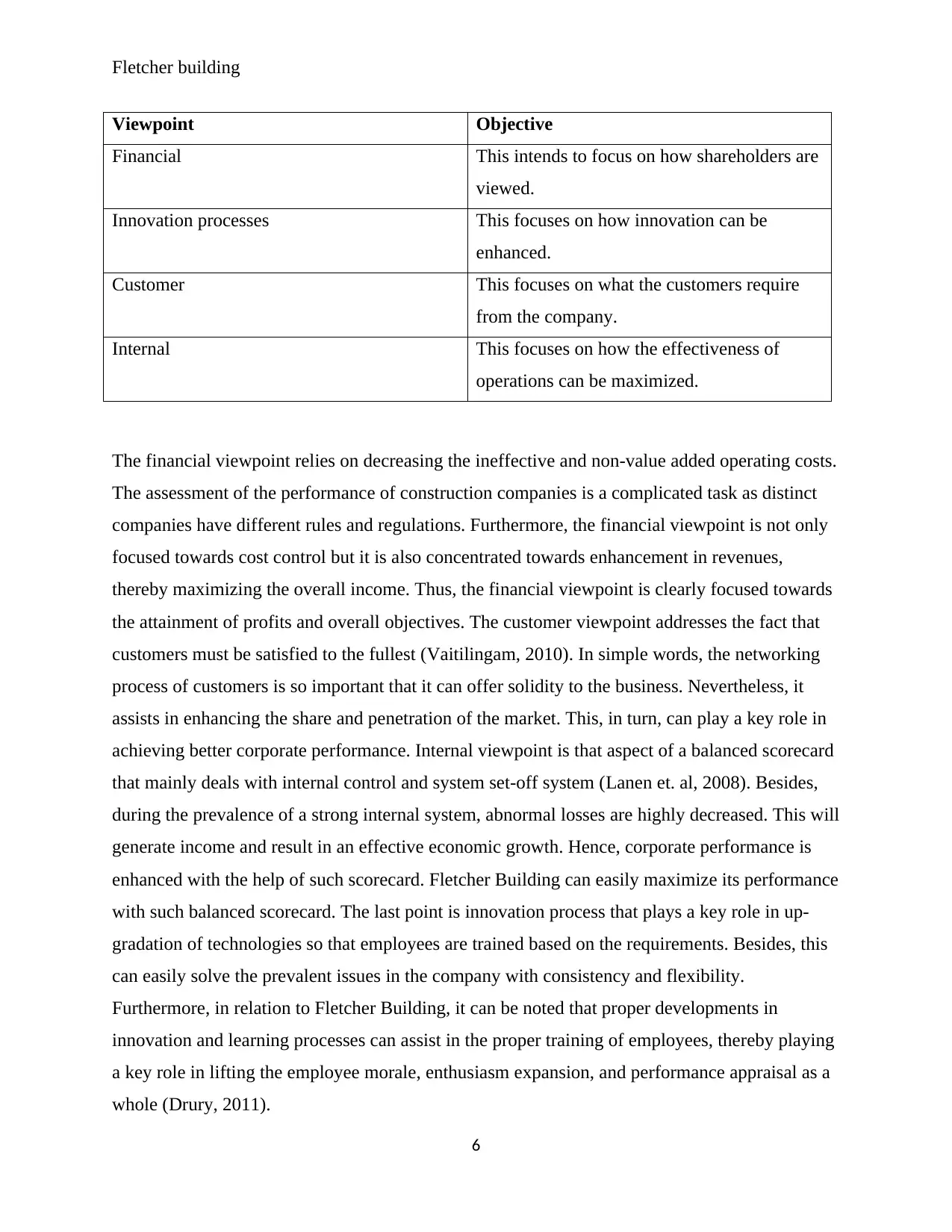

Viewpoint Objective

Financial This intends to focus on how shareholders are

viewed.

Innovation processes This focuses on how innovation can be

enhanced.

Customer This focuses on what the customers require

from the company.

Internal This focuses on how the effectiveness of

operations can be maximized.

The financial viewpoint relies on decreasing the ineffective and non-value added operating costs.

The assessment of the performance of construction companies is a complicated task as distinct

companies have different rules and regulations. Furthermore, the financial viewpoint is not only

focused towards cost control but it is also concentrated towards enhancement in revenues,

thereby maximizing the overall income. Thus, the financial viewpoint is clearly focused towards

the attainment of profits and overall objectives. The customer viewpoint addresses the fact that

customers must be satisfied to the fullest (Vaitilingam, 2010). In simple words, the networking

process of customers is so important that it can offer solidity to the business. Nevertheless, it

assists in enhancing the share and penetration of the market. This, in turn, can play a key role in

achieving better corporate performance. Internal viewpoint is that aspect of a balanced scorecard

that mainly deals with internal control and system set-off system (Lanen et. al, 2008). Besides,

during the prevalence of a strong internal system, abnormal losses are highly decreased. This will

generate income and result in an effective economic growth. Hence, corporate performance is

enhanced with the help of such scorecard. Fletcher Building can easily maximize its performance

with such balanced scorecard. The last point is innovation process that plays a key role in up-

gradation of technologies so that employees are trained based on the requirements. Besides, this

can easily solve the prevalent issues in the company with consistency and flexibility.

Furthermore, in relation to Fletcher Building, it can be noted that proper developments in

innovation and learning processes can assist in the proper training of employees, thereby playing

a key role in lifting the employee morale, enthusiasm expansion, and performance appraisal as a

whole (Drury, 2011).

6

Viewpoint Objective

Financial This intends to focus on how shareholders are

viewed.

Innovation processes This focuses on how innovation can be

enhanced.

Customer This focuses on what the customers require

from the company.

Internal This focuses on how the effectiveness of

operations can be maximized.

The financial viewpoint relies on decreasing the ineffective and non-value added operating costs.

The assessment of the performance of construction companies is a complicated task as distinct

companies have different rules and regulations. Furthermore, the financial viewpoint is not only

focused towards cost control but it is also concentrated towards enhancement in revenues,

thereby maximizing the overall income. Thus, the financial viewpoint is clearly focused towards

the attainment of profits and overall objectives. The customer viewpoint addresses the fact that

customers must be satisfied to the fullest (Vaitilingam, 2010). In simple words, the networking

process of customers is so important that it can offer solidity to the business. Nevertheless, it

assists in enhancing the share and penetration of the market. This, in turn, can play a key role in

achieving better corporate performance. Internal viewpoint is that aspect of a balanced scorecard

that mainly deals with internal control and system set-off system (Lanen et. al, 2008). Besides,

during the prevalence of a strong internal system, abnormal losses are highly decreased. This will

generate income and result in an effective economic growth. Hence, corporate performance is

enhanced with the help of such scorecard. Fletcher Building can easily maximize its performance

with such balanced scorecard. The last point is innovation process that plays a key role in up-

gradation of technologies so that employees are trained based on the requirements. Besides, this

can easily solve the prevalent issues in the company with consistency and flexibility.

Furthermore, in relation to Fletcher Building, it can be noted that proper developments in

innovation and learning processes can assist in the proper training of employees, thereby playing

a key role in lifting the employee morale, enthusiasm expansion, and performance appraisal as a

whole (Drury, 2011).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Fletcher building

Thus, these are the viewpoints that can be framed in a balanced scorecard and that can be utilized

by construction companies like Fletcher Building Ltd to assess its performance and development

respectively. Besides, to ensure success, such key performance indicators must be assessed on a

regular basis by the company.

Answer to 5

In relation to strategic management and marketing, competitor analysis can be defined as the

assessment of weaknesses and strengths of present and potential competitors. This evaluation

plays a key role in offering both a defensive and offensive strategic context to recognize threats

and opportunities. Furthermore, competitor analysis is an effective attribute of corporate strategy

and it has been argued that most organizations do not implement such type of analysis. Instead,

many organizations operate on what are defined conjectures, informal expressions, and intuition

attained through information tidbits about competitors every single manager continuously attains

(Maher, 2005). In relation to Fletcher Buildings Ltd, its main competitors are Boral Limited and

LafargeHolcim Ltd respectively.

As the new leader of the global world, LafargeHolcim addresses the challenges for building and

construction material industries, climate change, preservation of climate, increasing urban

development, etc by offering what really matters, a place to rest and work, spaces to live and

learn, and innovation that sustains the supply of energy. Similarly, Boral Ltd is also engaged in

the provision of construction and building materials. Furthermore, its building solutions also

consist of commercial and infrastructure solutions. Boral also offers services like material

technical services, roof tilling installers, etc. Both these companies give a huge competition to

Fletcher Building Ltd in the construction industry. Aggressive marketing, infrastructure, new

services, rebranding and branding, the performance of employees, quality of materials, etc are

considered the essential success factors for competitive analysis in this industry. After evaluating

the competitors of Fletcher, it can be stated that based on competitor analysis, Fletcher has a

competitive advantage in effective management, supply chain, size factors, and name or

recognition of brand value. Nonetheless, Fletcher must take effective steps in maintaining such

competitive advantages and must also make way for innovation so that additional competitive

advantages can be gained (Horngren, 2011). Besides, there are also factors that enhance the

threat of such competitors like Boral into the construction industry. These factors are generally

7

Thus, these are the viewpoints that can be framed in a balanced scorecard and that can be utilized

by construction companies like Fletcher Building Ltd to assess its performance and development

respectively. Besides, to ensure success, such key performance indicators must be assessed on a

regular basis by the company.

Answer to 5

In relation to strategic management and marketing, competitor analysis can be defined as the

assessment of weaknesses and strengths of present and potential competitors. This evaluation

plays a key role in offering both a defensive and offensive strategic context to recognize threats

and opportunities. Furthermore, competitor analysis is an effective attribute of corporate strategy

and it has been argued that most organizations do not implement such type of analysis. Instead,

many organizations operate on what are defined conjectures, informal expressions, and intuition

attained through information tidbits about competitors every single manager continuously attains

(Maher, 2005). In relation to Fletcher Buildings Ltd, its main competitors are Boral Limited and

LafargeHolcim Ltd respectively.

As the new leader of the global world, LafargeHolcim addresses the challenges for building and

construction material industries, climate change, preservation of climate, increasing urban

development, etc by offering what really matters, a place to rest and work, spaces to live and

learn, and innovation that sustains the supply of energy. Similarly, Boral Ltd is also engaged in

the provision of construction and building materials. Furthermore, its building solutions also

consist of commercial and infrastructure solutions. Boral also offers services like material

technical services, roof tilling installers, etc. Both these companies give a huge competition to

Fletcher Building Ltd in the construction industry. Aggressive marketing, infrastructure, new

services, rebranding and branding, the performance of employees, quality of materials, etc are

considered the essential success factors for competitive analysis in this industry. After evaluating

the competitors of Fletcher, it can be stated that based on competitor analysis, Fletcher has a

competitive advantage in effective management, supply chain, size factors, and name or

recognition of brand value. Nonetheless, Fletcher must take effective steps in maintaining such

competitive advantages and must also make way for innovation so that additional competitive

advantages can be gained (Horngren, 2011). Besides, there are also factors that enhance the

threat of such competitors like Boral into the construction industry. These factors are generally

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fletcher building

the weaknesses of Fletcher Building Ltd that must be improved by the company as soon as

possible. Besides, if these weaknesses are not being taken into account, Fletcher Building will

lose its competitive advantage in respect of the previously mentioned areas, thereby granting an

opportunity to the competitors to rise in the market (Robinson & Last, 2009). These factors are

outdated technology, failure to maintain a significant online presence, and a high turnover of

staff prevents the company to compete in the market effectively. Furthermore, these factors can

also have a long-term negative influence on the company that deducts from its value. In simple

words, these qualitative factors will altogether result in an increment in company’s costs (Shim

& Siegel, 2009).

Based on the competitive analysis, it can be stated that the weaknesses of Fletcher Buildings Ltd

must be improved so that competitors like Boral Ltd and LafargeHolcim cannot attain

competitive advantage and pose a threat to the company. Moreover, the company has immense

capability to retain competitive advantage in this industry because it has extreme financial

leverage in comparison to others. This can also grant the company to expand on an international

level so that it can enhance its goodwill and brand image as a whole.

8

the weaknesses of Fletcher Building Ltd that must be improved by the company as soon as

possible. Besides, if these weaknesses are not being taken into account, Fletcher Building will

lose its competitive advantage in respect of the previously mentioned areas, thereby granting an

opportunity to the competitors to rise in the market (Robinson & Last, 2009). These factors are

outdated technology, failure to maintain a significant online presence, and a high turnover of

staff prevents the company to compete in the market effectively. Furthermore, these factors can

also have a long-term negative influence on the company that deducts from its value. In simple

words, these qualitative factors will altogether result in an increment in company’s costs (Shim

& Siegel, 2009).

Based on the competitive analysis, it can be stated that the weaknesses of Fletcher Buildings Ltd

must be improved so that competitors like Boral Ltd and LafargeHolcim cannot attain

competitive advantage and pose a threat to the company. Moreover, the company has immense

capability to retain competitive advantage in this industry because it has extreme financial

leverage in comparison to others. This can also grant the company to expand on an international

level so that it can enhance its goodwill and brand image as a whole.

8

Fletcher building

References

Drury, C. (2011). Cost and management accounting. Andover, Hampshire, UK: South-Western

Cengage Learning.

Drury, C. M. (2013). Management and cost accounting. Springer.

Fletcher building. (2017). Fletcher building 2017 annual report and accounts. Accessed October

11, 2017 from http://www.fletcherbuilding.com/investor-centre/reports-and-

presentation/2016-full-year-results-2/

Horngren, C T & Foster, G. (2008). Cost Accounting: A Managerial Emphasis. United States

Edition

Horngren, C. (2011). Cost accounting. Frenchs Forest, N.S.W.: Pearson Australia.

Lanen, W. N, Anderson, S & Maher, M. W. (2008). Fundamentals of cost accounting. NY: Hang

Loose press.

Larry M. W & Christopher J. S. (2012). Managerial and Cost Accounting. Pearson Press

Maher, L. (2005). Fundamentals of Cost Accounting. McGraw-Hill

Marsh, C. (2009). Mastering financial management. Harlow: Financial Times Prentice Hall

Robinson, M & Last, D. (2009). Budgetary Control Model: The Process of Translation.

Accounting, Organization, and Society. NY Press

Shim, J. K & Siegel, J G. (2009). Modern Cost Management and Analysis. Barron's Education

Series

Needles, B. E.& Powers, M. (2013). Principles of Financial Accounting. New York Press

Needles, S. C. (2011). Managerial Accounting, USA: South-Western Cengage Learning .

Parrino, R, Kidwell, D. & Bates, T. (2012). Fundamentals of corporate finance. Hoboken,

Shim, J. K & Siegel, J G. (2009). Modern Cost Management and Analysis. Barron's Education

Series

9

References

Drury, C. (2011). Cost and management accounting. Andover, Hampshire, UK: South-Western

Cengage Learning.

Drury, C. M. (2013). Management and cost accounting. Springer.

Fletcher building. (2017). Fletcher building 2017 annual report and accounts. Accessed October

11, 2017 from http://www.fletcherbuilding.com/investor-centre/reports-and-

presentation/2016-full-year-results-2/

Horngren, C T & Foster, G. (2008). Cost Accounting: A Managerial Emphasis. United States

Edition

Horngren, C. (2011). Cost accounting. Frenchs Forest, N.S.W.: Pearson Australia.

Lanen, W. N, Anderson, S & Maher, M. W. (2008). Fundamentals of cost accounting. NY: Hang

Loose press.

Larry M. W & Christopher J. S. (2012). Managerial and Cost Accounting. Pearson Press

Maher, L. (2005). Fundamentals of Cost Accounting. McGraw-Hill

Marsh, C. (2009). Mastering financial management. Harlow: Financial Times Prentice Hall

Robinson, M & Last, D. (2009). Budgetary Control Model: The Process of Translation.

Accounting, Organization, and Society. NY Press

Shim, J. K & Siegel, J G. (2009). Modern Cost Management and Analysis. Barron's Education

Series

Needles, B. E.& Powers, M. (2013). Principles of Financial Accounting. New York Press

Needles, S. C. (2011). Managerial Accounting, USA: South-Western Cengage Learning .

Parrino, R, Kidwell, D. & Bates, T. (2012). Fundamentals of corporate finance. Hoboken,

Shim, J. K & Siegel, J G. (2009). Modern Cost Management and Analysis. Barron's Education

Series

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Fletcher building

Vaitilingam, R. (2010). The Financial Times Guide to Using the Financial Pages. London: FT

Prentice Hall.

Vanderbeck, E J. (2013). Principles of Cost Accounting. Oxford university press

Venanci, D. (2012). Financial Performance Measures and Value Creation. State of art . New

York: Springer.

10

Vaitilingam, R. (2010). The Financial Times Guide to Using the Financial Pages. London: FT

Prentice Hall.

Vanderbeck, E J. (2013). Principles of Cost Accounting. Oxford university press

Venanci, D. (2012). Financial Performance Measures and Value Creation. State of art . New

York: Springer.

10

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.