AFM050: Advanced Management Accounting Report on Performance Analysis

VerifiedAdded on 2023/06/10

|13

|4162

|337

Report

AI Summary

This report provides an in-depth analysis of advanced management accounting, focusing on performance measurement, performance management, and pricing strategies. It begins by differentiating between performance measurement and management, then explores crucial factors in defining the scope of performance measurement schemes. The report critically evaluates various strategies, including Total Quality Management (TQM), the Theory of Constraints (TOC), divisional performance measurement, and the Balanced Scorecard (BSC), discussing their advantages and limitations. It also examines two pricing strategies suitable for AMA Ltd, considering factors influencing their adoption. The report incorporates relevant academic sources to support its findings, offering a comprehensive overview of key concepts in advanced management accounting. This report aims to provide a detailed understanding of these concepts and strategies to improve business performance.

Advanced

Management

Accounting

Management

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

A. Justify the differences between performance measurement and performance management

................................................................................................................................................3

B. Explain the various matters that should be taken into consideration while defining the

scope of performance measurement and management scheme..............................................4

C. Critically Evaluation of nature and rational of each of following and explain its advantages

and limitations........................................................................................................................5

D. Two Pricing strategies that can be adopted by AMA Ltd and also discuss various factors

that consider while adopting these strategies.........................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

A. Justify the differences between performance measurement and performance management

................................................................................................................................................3

B. Explain the various matters that should be taken into consideration while defining the

scope of performance measurement and management scheme..............................................4

C. Critically Evaluation of nature and rational of each of following and explain its advantages

and limitations........................................................................................................................5

D. Two Pricing strategies that can be adopted by AMA Ltd and also discuss various factors

that consider while adopting these strategies.........................................................................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

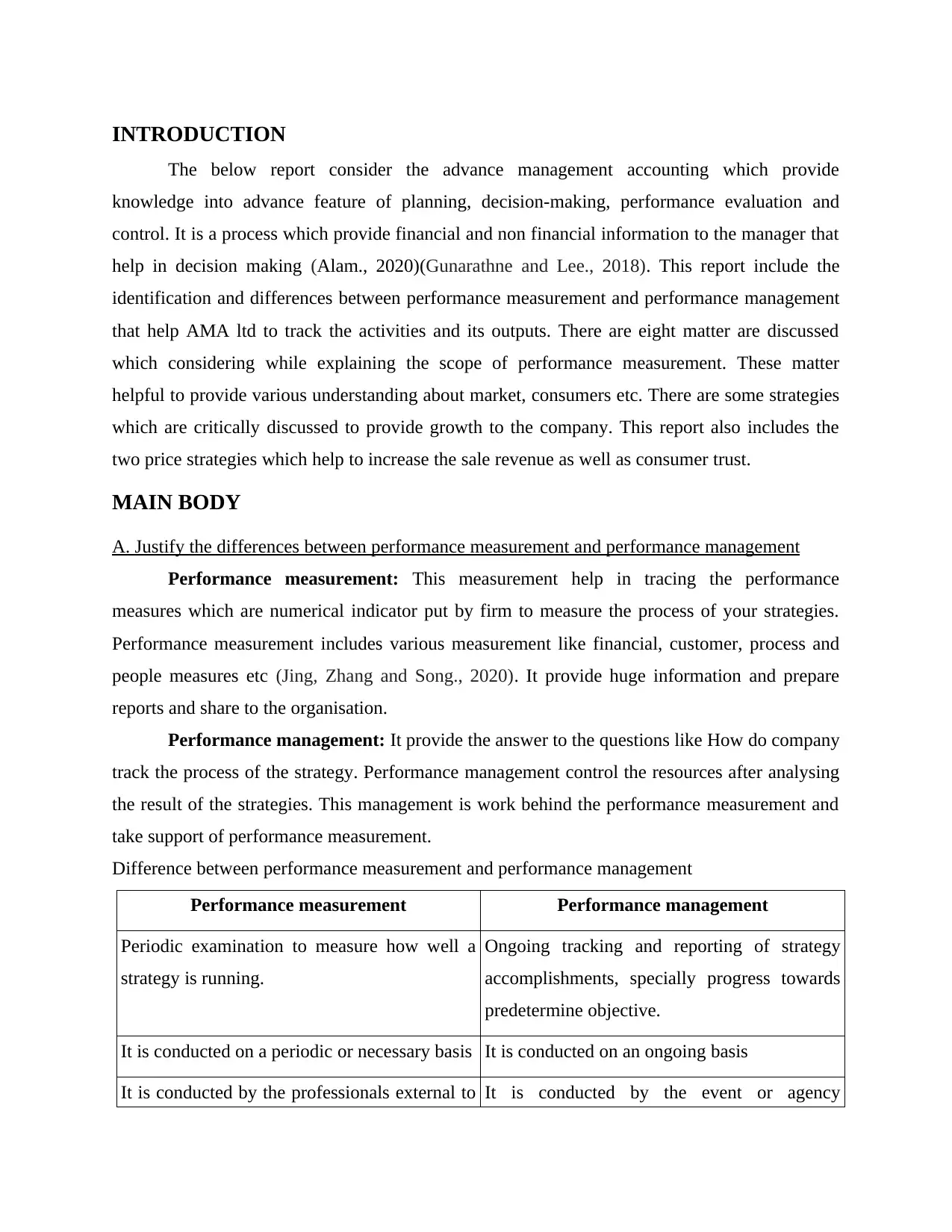

INTRODUCTION

The below report consider the advance management accounting which provide

knowledge into advance feature of planning, decision-making, performance evaluation and

control. It is a process which provide financial and non financial information to the manager that

help in decision making (Alam., 2020)(Gunarathne and Lee., 2018). This report include the

identification and differences between performance measurement and performance management

that help AMA ltd to track the activities and its outputs. There are eight matter are discussed

which considering while explaining the scope of performance measurement. These matter

helpful to provide various understanding about market, consumers etc. There are some strategies

which are critically discussed to provide growth to the company. This report also includes the

two price strategies which help to increase the sale revenue as well as consumer trust.

MAIN BODY

A. Justify the differences between performance measurement and performance management

Performance measurement: This measurement help in tracing the performance

measures which are numerical indicator put by firm to measure the process of your strategies.

Performance measurement includes various measurement like financial, customer, process and

people measures etc (Jing, Zhang and Song., 2020). It provide huge information and prepare

reports and share to the organisation.

Performance management: It provide the answer to the questions like How do company

track the process of the strategy. Performance management control the resources after analysing

the result of the strategies. This management is work behind the performance measurement and

take support of performance measurement.

Difference between performance measurement and performance management

Performance measurement Performance management

Periodic examination to measure how well a

strategy is running.

Ongoing tracking and reporting of strategy

accomplishments, specially progress towards

predetermine objective.

It is conducted on a periodic or necessary basis It is conducted on an ongoing basis

It is conducted by the professionals external to It is conducted by the event or agency

The below report consider the advance management accounting which provide

knowledge into advance feature of planning, decision-making, performance evaluation and

control. It is a process which provide financial and non financial information to the manager that

help in decision making (Alam., 2020)(Gunarathne and Lee., 2018). This report include the

identification and differences between performance measurement and performance management

that help AMA ltd to track the activities and its outputs. There are eight matter are discussed

which considering while explaining the scope of performance measurement. These matter

helpful to provide various understanding about market, consumers etc. There are some strategies

which are critically discussed to provide growth to the company. This report also includes the

two price strategies which help to increase the sale revenue as well as consumer trust.

MAIN BODY

A. Justify the differences between performance measurement and performance management

Performance measurement: This measurement help in tracing the performance

measures which are numerical indicator put by firm to measure the process of your strategies.

Performance measurement includes various measurement like financial, customer, process and

people measures etc (Jing, Zhang and Song., 2020). It provide huge information and prepare

reports and share to the organisation.

Performance management: It provide the answer to the questions like How do company

track the process of the strategy. Performance management control the resources after analysing

the result of the strategies. This management is work behind the performance measurement and

take support of performance measurement.

Difference between performance measurement and performance management

Performance measurement Performance management

Periodic examination to measure how well a

strategy is running.

Ongoing tracking and reporting of strategy

accomplishments, specially progress towards

predetermine objective.

It is conducted on a periodic or necessary basis It is conducted on an ongoing basis

It is conducted by the professionals external to It is conducted by the event or agency

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

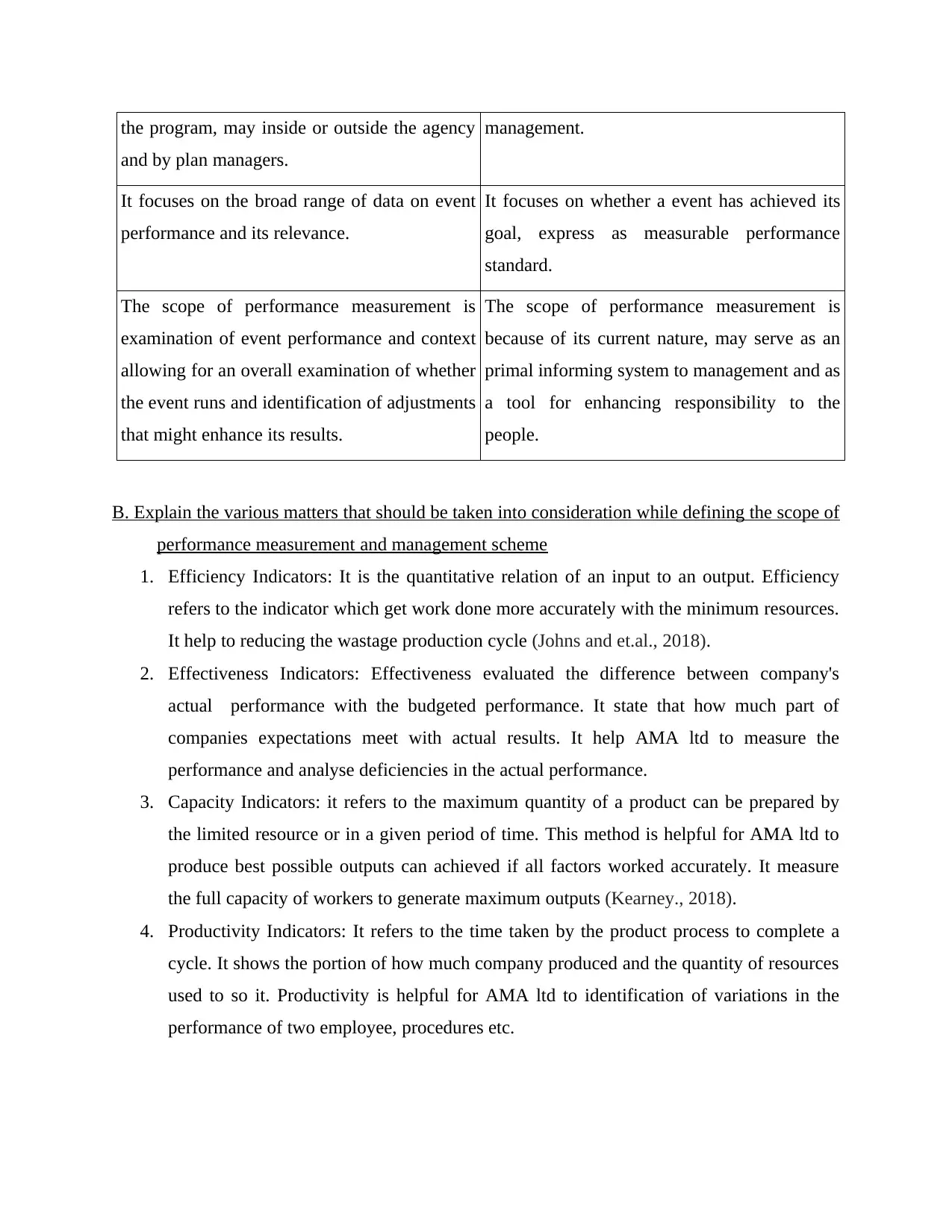

the program, may inside or outside the agency

and by plan managers.

management.

It focuses on the broad range of data on event

performance and its relevance.

It focuses on whether a event has achieved its

goal, express as measurable performance

standard.

The scope of performance measurement is

examination of event performance and context

allowing for an overall examination of whether

the event runs and identification of adjustments

that might enhance its results.

The scope of performance measurement is

because of its current nature, may serve as an

primal informing system to management and as

a tool for enhancing responsibility to the

people.

B. Explain the various matters that should be taken into consideration while defining the scope of

performance measurement and management scheme

1. Efficiency Indicators: It is the quantitative relation of an input to an output. Efficiency

refers to the indicator which get work done more accurately with the minimum resources.

It help to reducing the wastage production cycle (Johns and et.al., 2018).

2. Effectiveness Indicators: Effectiveness evaluated the difference between company's

actual performance with the budgeted performance. It state that how much part of

companies expectations meet with actual results. It help AMA ltd to measure the

performance and analyse deficiencies in the actual performance.

3. Capacity Indicators: it refers to the maximum quantity of a product can be prepared by

the limited resource or in a given period of time. This method is helpful for AMA ltd to

produce best possible outputs can achieved if all factors worked accurately. It measure

the full capacity of workers to generate maximum outputs (Kearney., 2018).

4. Productivity Indicators: It refers to the time taken by the product process to complete a

cycle. It shows the portion of how much company produced and the quantity of resources

used to so it. Productivity is helpful for AMA ltd to identification of variations in the

performance of two employee, procedures etc.

and by plan managers.

management.

It focuses on the broad range of data on event

performance and its relevance.

It focuses on whether a event has achieved its

goal, express as measurable performance

standard.

The scope of performance measurement is

examination of event performance and context

allowing for an overall examination of whether

the event runs and identification of adjustments

that might enhance its results.

The scope of performance measurement is

because of its current nature, may serve as an

primal informing system to management and as

a tool for enhancing responsibility to the

people.

B. Explain the various matters that should be taken into consideration while defining the scope of

performance measurement and management scheme

1. Efficiency Indicators: It is the quantitative relation of an input to an output. Efficiency

refers to the indicator which get work done more accurately with the minimum resources.

It help to reducing the wastage production cycle (Johns and et.al., 2018).

2. Effectiveness Indicators: Effectiveness evaluated the difference between company's

actual performance with the budgeted performance. It state that how much part of

companies expectations meet with actual results. It help AMA ltd to measure the

performance and analyse deficiencies in the actual performance.

3. Capacity Indicators: it refers to the maximum quantity of a product can be prepared by

the limited resource or in a given period of time. This method is helpful for AMA ltd to

produce best possible outputs can achieved if all factors worked accurately. It measure

the full capacity of workers to generate maximum outputs (Kearney., 2018).

4. Productivity Indicators: It refers to the time taken by the product process to complete a

cycle. It shows the portion of how much company produced and the quantity of resources

used to so it. Productivity is helpful for AMA ltd to identification of variations in the

performance of two employee, procedures etc.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5. Quality Indicators: It mainly focuses on the product quality. It measure the how many

products it produced according to the required quality. The main motive of such indicator

is to provide instructions regarding the quality of the product.

6. Profitability Indicators: This is an important indicator that evaluate the relationship

between the sale revenue of the firm and the cost of production spend on the sale units.

This indicator help AMA ltd to generate maximum profits which cover the overall cost

incurred on the production.

7. Competitiveness Indicators: This metrics mainly focuses on the competitors at the

marketplace. It shows the competition among the various companies (Khan and et.al.,

2018). It states the consumer behaviours, trend and attitude etc. which help AMA ltd to

provide goods and services according to the needs of consumer.

8. Value Indicators: This metric provide understanding about how much a firms product is

worthy in the asked price. Every product has good as well as bad value which depends on

factors such as location, requirement and competition.

C. Critically Evaluation of nature and rational of each of following and explain its advantages

and limitations.

1. Total Quality Management

It is a continuous process of tracing and decreasing or destroying the faults in

manufacturing, supply chain management, improving consumer satisfaction and checking

employees are up to their maximum efficiency with training (Kumar., 2018). The main motive of

TQM is to hold all parties active in the process of manufacturing of product to its final stage.

Advantages of TQM:

Customer satisfaction: It increase the consumer satisfaction by providing better service to

them. It is helpful in understanding about consumer needs and wants and also provide

consumer feedbacks, correct any deficiency at the same stage. It help firm to improve the

quality of the products and services and also recommand to launch a new product.

Employee engagement: TQM help AMA Ltd to attract maximum number of people. It

ensure the work capacity of the employee and motivate them to work more effectively

and efficiently. It enhance the performance of the company by improving their existing

products. It manges the wastage of resources.

Disadvantage of TQM:

products it produced according to the required quality. The main motive of such indicator

is to provide instructions regarding the quality of the product.

6. Profitability Indicators: This is an important indicator that evaluate the relationship

between the sale revenue of the firm and the cost of production spend on the sale units.

This indicator help AMA ltd to generate maximum profits which cover the overall cost

incurred on the production.

7. Competitiveness Indicators: This metrics mainly focuses on the competitors at the

marketplace. It shows the competition among the various companies (Khan and et.al.,

2018). It states the consumer behaviours, trend and attitude etc. which help AMA ltd to

provide goods and services according to the needs of consumer.

8. Value Indicators: This metric provide understanding about how much a firms product is

worthy in the asked price. Every product has good as well as bad value which depends on

factors such as location, requirement and competition.

C. Critically Evaluation of nature and rational of each of following and explain its advantages

and limitations.

1. Total Quality Management

It is a continuous process of tracing and decreasing or destroying the faults in

manufacturing, supply chain management, improving consumer satisfaction and checking

employees are up to their maximum efficiency with training (Kumar., 2018). The main motive of

TQM is to hold all parties active in the process of manufacturing of product to its final stage.

Advantages of TQM:

Customer satisfaction: It increase the consumer satisfaction by providing better service to

them. It is helpful in understanding about consumer needs and wants and also provide

consumer feedbacks, correct any deficiency at the same stage. It help firm to improve the

quality of the products and services and also recommand to launch a new product.

Employee engagement: TQM help AMA Ltd to attract maximum number of people. It

ensure the work capacity of the employee and motivate them to work more effectively

and efficiently. It enhance the performance of the company by improving their existing

products. It manges the wastage of resources.

Disadvantage of TQM:

Increase the cost of production: This process is costly for AMA Ltd because if they try to

adopt new changes for bettering the performance, there are always hidden costs involved

in this and sometimes it might be higher than usual.

Difficult and time consuming process: Applying total quantity management not a simple

process. It is very time consuming process and require large number of resources such as

natural and financial. Implementation of TQM would affect the whole business

operations form top to down and it is necessary to change the business proceeds and

procedures which is very difficult and time consuming (Kumari and et.al., 2020).

2. Theory of constraints and throughput contribution

The main purpose of the strategy is to enhance productivity while conserving or falling of

inventory and operational expenditure. Every operation in a manufacturing or service unit is

formed by a series of associated actions, according to the idea of constraints. Every connection in

the sequence should serve its objectives as efficiently as possible to improve the overall

performance of the process. The theory states that among all the linkages, there is at least one

weak link that acts as a restraining factor which affects the whole business (Moharir and

Tembhurkar., 2018). The organisation must concentrate on handling the process's limiting

constraint with the aim of enhancing or increasing its performance.

Advantages:

Provide better understanding: The principle of constraints is straightforward and simple

to follow which makes it more accessible for the management. The theory follows a fixed

pattern which gives the user the focus more on the region that requires attention.

Effective results: It works well in changing corporate situations because it helps in faster

outcomes by abolishing or decreasing the restraining factor in a process. The theory of

constraints leads to an instant rise in the efficiency of the functional aspects as well as a

boost the company's earnings. The cause being that the theory's major objective is to

improve the constraints that are present in the system, which leads to a reduction in the

time it takes to provide a service (in a service firm) and reduces construction time, lead

time, and other factors (in a manufacturing process), resulting in an increase in the

finished goods production.

Disadvantages:

adopt new changes for bettering the performance, there are always hidden costs involved

in this and sometimes it might be higher than usual.

Difficult and time consuming process: Applying total quantity management not a simple

process. It is very time consuming process and require large number of resources such as

natural and financial. Implementation of TQM would affect the whole business

operations form top to down and it is necessary to change the business proceeds and

procedures which is very difficult and time consuming (Kumari and et.al., 2020).

2. Theory of constraints and throughput contribution

The main purpose of the strategy is to enhance productivity while conserving or falling of

inventory and operational expenditure. Every operation in a manufacturing or service unit is

formed by a series of associated actions, according to the idea of constraints. Every connection in

the sequence should serve its objectives as efficiently as possible to improve the overall

performance of the process. The theory states that among all the linkages, there is at least one

weak link that acts as a restraining factor which affects the whole business (Moharir and

Tembhurkar., 2018). The organisation must concentrate on handling the process's limiting

constraint with the aim of enhancing or increasing its performance.

Advantages:

Provide better understanding: The principle of constraints is straightforward and simple

to follow which makes it more accessible for the management. The theory follows a fixed

pattern which gives the user the focus more on the region that requires attention.

Effective results: It works well in changing corporate situations because it helps in faster

outcomes by abolishing or decreasing the restraining factor in a process. The theory of

constraints leads to an instant rise in the efficiency of the functional aspects as well as a

boost the company's earnings. The cause being that the theory's major objective is to

improve the constraints that are present in the system, which leads to a reduction in the

time it takes to provide a service (in a service firm) and reduces construction time, lead

time, and other factors (in a manufacturing process), resulting in an increase in the

finished goods production.

Disadvantages:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Difficult in implementing: The theorys approach is continuous, and it might get difficult

to keep up. This is because the implementation of this theory requires alterations in

corporate operations, which may be difficult to sustain in the long run. When a

corporation handles one limitation, another constraint unfolds, making achieving an

flawless level of all operations difficult.

Beneficial for short-term: Although the idea of constraints performs admirably in the

real-world conditions that commercial organisations face, its effects are not permanent. In

certain businesses, the idea emphasizes on real-time process improvement, although it's

possible that the constraint on which the firm concentrates is for a shorter period of time

and hence it will not have long term merits (Nayak, Misra and Behera., 2018).

3. Divisional performance measurement and transfer pricing issues

Divisional performance assessment is useful to ensure that a business plan is implemented

successfully by observing a division's efficiency in completing its predefined targets or

stakeholder requests. Non-financial as well as financial data may be used to measure divisional

success.

Advantages:

Provide motivation: The ability to make decisions presents a challenge for those in

charge of the division, and it may inspire them to work harder to achieve success. They

will be in charge of both asset and employee investments, giving them a sense of

command over the entire organisation rather than being trapped between those who make

the choices and those who must put them into action (Ng and Harrison, 2021).

Disadvantages:

Create communication gap: By putting too much emphasis on the divisional structure,

people in each division may fail to identify with the organisation as a whole, and senior

management may become disconnected from the day-to-day activity of the many

segments of the broader business. In such situations, communication and motivation may

become more important in attaining good management.

The cost of putting down another division, subsidiary, or holding company for the services

delivered is calculated by a transfer price. The current market price of the goods or service is

usually shown in transfer pricing. Intellectual property, including as research, patents, and

royalties, can also be subject to transfer pricing.

to keep up. This is because the implementation of this theory requires alterations in

corporate operations, which may be difficult to sustain in the long run. When a

corporation handles one limitation, another constraint unfolds, making achieving an

flawless level of all operations difficult.

Beneficial for short-term: Although the idea of constraints performs admirably in the

real-world conditions that commercial organisations face, its effects are not permanent. In

certain businesses, the idea emphasizes on real-time process improvement, although it's

possible that the constraint on which the firm concentrates is for a shorter period of time

and hence it will not have long term merits (Nayak, Misra and Behera., 2018).

3. Divisional performance measurement and transfer pricing issues

Divisional performance assessment is useful to ensure that a business plan is implemented

successfully by observing a division's efficiency in completing its predefined targets or

stakeholder requests. Non-financial as well as financial data may be used to measure divisional

success.

Advantages:

Provide motivation: The ability to make decisions presents a challenge for those in

charge of the division, and it may inspire them to work harder to achieve success. They

will be in charge of both asset and employee investments, giving them a sense of

command over the entire organisation rather than being trapped between those who make

the choices and those who must put them into action (Ng and Harrison, 2021).

Disadvantages:

Create communication gap: By putting too much emphasis on the divisional structure,

people in each division may fail to identify with the organisation as a whole, and senior

management may become disconnected from the day-to-day activity of the many

segments of the broader business. In such situations, communication and motivation may

become more important in attaining good management.

The cost of putting down another division, subsidiary, or holding company for the services

delivered is calculated by a transfer price. The current market price of the goods or service is

usually shown in transfer pricing. Intellectual property, including as research, patents, and

royalties, can also be subject to transfer pricing.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantages:

Easily accessible: The goods are made on the premises of the business and other

departments don't need to count on suppliers since items are already accessible in the

firm, saving the organization from ill treatment by the goods providers.

Disadvantages:

Inter-departmental animosity: It may subject to an artificial gap between departments as

they might think that they are losing profit because market prices are greater than transfer

rates by which departments that supply commodities to other departments will get

demotivated to supply. (Nitsas and Koronaki., 2018).

4. The Balanced Scorecard

The balanced scorecard (BSC) is a strategy formulation performance indicator that is

used to point out and amplify a number of internal company processes as well as the external

consequences that arise. Learning and growth, company processes, consumers, and money are all

measured using the balanced scorecard. BSCs let businesses to merge data into a single report,

providing an understanding into quality of service in addition to financial performance, and aid

in the upgrading of efficiency.

Advantages:

* It facilitates communication: When everyone speaks the same dialect, communication

across the teams and departments becomes unchallenging. In other words, having a well-

organized performance assessment system will make it easier to scrutinize strategy and

success of the company.

* Provides structure to a company's strategy: Different departments within a company have

their own methods for analysing performance and determining what metrics are crucial

for them. Different executives and departments can still customize their performance

assessment with a balanced scorecard, but it all should fit under a specific format that can

be understood across the firm. It provides a central location for everyone in the firm to

track their progress (Sakamoto and et.al., 2021).

Disadvantages:

* It must be customized to the company's needs: A balanced scorecard is designed to give a

framework for working, but it will still need to be modified according to the firm who

Easily accessible: The goods are made on the premises of the business and other

departments don't need to count on suppliers since items are already accessible in the

firm, saving the organization from ill treatment by the goods providers.

Disadvantages:

Inter-departmental animosity: It may subject to an artificial gap between departments as

they might think that they are losing profit because market prices are greater than transfer

rates by which departments that supply commodities to other departments will get

demotivated to supply. (Nitsas and Koronaki., 2018).

4. The Balanced Scorecard

The balanced scorecard (BSC) is a strategy formulation performance indicator that is

used to point out and amplify a number of internal company processes as well as the external

consequences that arise. Learning and growth, company processes, consumers, and money are all

measured using the balanced scorecard. BSCs let businesses to merge data into a single report,

providing an understanding into quality of service in addition to financial performance, and aid

in the upgrading of efficiency.

Advantages:

* It facilitates communication: When everyone speaks the same dialect, communication

across the teams and departments becomes unchallenging. In other words, having a well-

organized performance assessment system will make it easier to scrutinize strategy and

success of the company.

* Provides structure to a company's strategy: Different departments within a company have

their own methods for analysing performance and determining what metrics are crucial

for them. Different executives and departments can still customize their performance

assessment with a balanced scorecard, but it all should fit under a specific format that can

be understood across the firm. It provides a central location for everyone in the firm to

track their progress (Sakamoto and et.al., 2021).

Disadvantages:

* It must be customized to the company's needs: A balanced scorecard is designed to give a

framework for working, but it will still need to be modified according to the firm who

uses it. This can take a lot of effort, and while examples are useful, they can't be

reproduced exactly because each and every company has its own set of demands.

* It necessitates a large amount of data: Balanced scorecards frequently ask managers and

team members to give information, which necessitates data tracking. A lot of people

dislike this because they consider it boring, and it can also demotivate them from

performing to reach their goals.

5. Six Sigma

This is a series of action which facilitates business operations by increasing business capabilities

and by lowering the risk of errors. Six sigma is a data-driven strategy to problem elimination,

defect reduction, and profit enhancement that employs a statistical technique.

Advantages:

Enhance quality of product: it has a evidence of serving value and assuring efficiency and

effectiveness to the the organisation. It may also have helped in betterment of customer

satisfaction.

Reduce losses: it is a dynamic series of activities that identifies risk and give solution to

the upcoming problem and dynamic risks before such hurdles effect the organisation . Six

sigma can be used at number of field inside the company,for better functioning and cost

saving.(Sakamoto and et.al., 2021).

Disadvantages:

Costly and time consuming process: it is a process which monitors each and every

process happening inside the company due to which vast data is accumulated, therefore

makes it complicated to process. Also such process increases operation cost too .

Difficult to understand: Organisation must either determine qualified Six Sigma

establishment or execute onboard training without recognised accreditation to make their

employees learn the techniques. In any situation, the cost of employing six sigma in a

small organisation is huge not everyone can bear it. In fact big companies have to provide

training sessions to its employee to work on the system.

D. Two Pricing strategies that can be adopted by AMA Ltd and also discuss various factors that

consider while adopting these strategies

The practices and techniques that organisations uses to determine prices for their

deliverables in the market are referred to as pricing strategies. Product selling price is the

reproduced exactly because each and every company has its own set of demands.

* It necessitates a large amount of data: Balanced scorecards frequently ask managers and

team members to give information, which necessitates data tracking. A lot of people

dislike this because they consider it boring, and it can also demotivate them from

performing to reach their goals.

5. Six Sigma

This is a series of action which facilitates business operations by increasing business capabilities

and by lowering the risk of errors. Six sigma is a data-driven strategy to problem elimination,

defect reduction, and profit enhancement that employs a statistical technique.

Advantages:

Enhance quality of product: it has a evidence of serving value and assuring efficiency and

effectiveness to the the organisation. It may also have helped in betterment of customer

satisfaction.

Reduce losses: it is a dynamic series of activities that identifies risk and give solution to

the upcoming problem and dynamic risks before such hurdles effect the organisation . Six

sigma can be used at number of field inside the company,for better functioning and cost

saving.(Sakamoto and et.al., 2021).

Disadvantages:

Costly and time consuming process: it is a process which monitors each and every

process happening inside the company due to which vast data is accumulated, therefore

makes it complicated to process. Also such process increases operation cost too .

Difficult to understand: Organisation must either determine qualified Six Sigma

establishment or execute onboard training without recognised accreditation to make their

employees learn the techniques. In any situation, the cost of employing six sigma in a

small organisation is huge not everyone can bear it. In fact big companies have to provide

training sessions to its employee to work on the system.

D. Two Pricing strategies that can be adopted by AMA Ltd and also discuss various factors that

consider while adopting these strategies

The practices and techniques that organisations uses to determine prices for their

deliverables in the market are referred to as pricing strategies. Product selling price is the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

amount that company ask for the good and services it is providing pricing strategy is method to

determine that amount need to be charged from the customer. AMA Ltd consider two pricing

strategies which is most suitable for their growth and expansion purpose. These strategies may

increase the sale volume of AMA Ltd by attracting maximum number of people. These strategies

are:

Value-based pricing

Value based pricing approach is a customer based approach where the company decideds

its goods and services price based on the consumer's perception. Basically here company

figures out customers worth for the product and accordingly fixes the selling price. This

strategy helpful for AMA Ltd. to sustain in the competitive market. This help company to

measure the value of product in the eyes of consumers. This strategy is basically used in

the market where owning the product provide luxury to the customer, and their

willingness to own the product provides a sensed value for the product which throws a

high impact on the selling price of the product.(Shafi, Raina and Haq., 2019).

Importance of value based pricing for AMA ltd.

1. Brand value has increased: setting high price to the product makes a perception in the

mind of the customer that the product offered is of high quality and owning such product

will increase their status in the society which ultimately increase the organisation's brand

value.

2. Customer loyalty is important: when a customer put a extra money on a product because

of its brand value it connects the customer to the organisation emotionally. This

sentiments results in customer loyalty for the brand and customer stays connected to the

company.

3. Increased profit margins: when the customers are willing to pay a higher price for the

product it is so obvious that company will earn a supernormal profit. Higher the

perception of the price greater profit to the company.

Cost-plus pricing

Markup pricing is another name for cost-plus pricing. It is that fixed margin of profit

which is added to the cost that the company desires to earn on every unit sold (unit cost).

The resultant figure is the product's selling price. For firms that desire to pursue a cost-

leadership strategy, the cost-plus pricing system is a suitable option. When a is company

determine that amount need to be charged from the customer. AMA Ltd consider two pricing

strategies which is most suitable for their growth and expansion purpose. These strategies may

increase the sale volume of AMA Ltd by attracting maximum number of people. These strategies

are:

Value-based pricing

Value based pricing approach is a customer based approach where the company decideds

its goods and services price based on the consumer's perception. Basically here company

figures out customers worth for the product and accordingly fixes the selling price. This

strategy helpful for AMA Ltd. to sustain in the competitive market. This help company to

measure the value of product in the eyes of consumers. This strategy is basically used in

the market where owning the product provide luxury to the customer, and their

willingness to own the product provides a sensed value for the product which throws a

high impact on the selling price of the product.(Shafi, Raina and Haq., 2019).

Importance of value based pricing for AMA ltd.

1. Brand value has increased: setting high price to the product makes a perception in the

mind of the customer that the product offered is of high quality and owning such product

will increase their status in the society which ultimately increase the organisation's brand

value.

2. Customer loyalty is important: when a customer put a extra money on a product because

of its brand value it connects the customer to the organisation emotionally. This

sentiments results in customer loyalty for the brand and customer stays connected to the

company.

3. Increased profit margins: when the customers are willing to pay a higher price for the

product it is so obvious that company will earn a supernormal profit. Higher the

perception of the price greater profit to the company.

Cost-plus pricing

Markup pricing is another name for cost-plus pricing. It is that fixed margin of profit

which is added to the cost that the company desires to earn on every unit sold (unit cost).

The resultant figure is the product's selling price. For firms that desire to pursue a cost-

leadership strategy, the cost-plus pricing system is a suitable option. When a is company

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

transparent to its customer it attracts customer trust and helps building image of the

company.

Importance of cost-plus pricing for AMA Ltd

1. It is a convenient method of pricing, in order to fix price there is no requirement of

massive research, easily summing up all the expenses and adding profit margin to it all

that's required. (Zhang, Song and Jiang., 2020).

2. The cost plus pricing enables a company to justify to its customer about the changes in

price since profit margin clearly conveyed to them, rise in price due to other factors are

justifiable.

3. The rate of return of the company is pre determined which is brings stability and helps in

further decision making.

Factors that consider while adopting pricing strategies

1. Costs: Every company has to analyse the cost system before adopting price strategies.

AMA Ltd. Has to charge a price which cover its overall expenses incurred in the

production, distribution and selling the product and also include a favourable return on

the product for company's efforts.

2. Marketing mix strategy: Price is the one of important tool in the market mix. Decisions

made on other market mix tool affect the pricing policies and decisions. AMA Ltd has to

charge higher prices so that they can cover its expenses and generate profits (Zuo and

et.al., 2018).

CONCLUSION

Form the above report it can be concluded that the advance management accounting plays

important role to provide growth to the company. This accounting technique increase the sale

volume by lower the cost of production, resulting increase in the profits. Profitability and

controlling both are important in order to measure performance and finding any deficiencies.

Company is recommanded to use two price strategies that may increase the company value and

profitability. These strategies helpful to provide better consumer satisfaction by producing

products according to the needs and wants of the consumer.

company.

Importance of cost-plus pricing for AMA Ltd

1. It is a convenient method of pricing, in order to fix price there is no requirement of

massive research, easily summing up all the expenses and adding profit margin to it all

that's required. (Zhang, Song and Jiang., 2020).

2. The cost plus pricing enables a company to justify to its customer about the changes in

price since profit margin clearly conveyed to them, rise in price due to other factors are

justifiable.

3. The rate of return of the company is pre determined which is brings stability and helps in

further decision making.

Factors that consider while adopting pricing strategies

1. Costs: Every company has to analyse the cost system before adopting price strategies.

AMA Ltd. Has to charge a price which cover its overall expenses incurred in the

production, distribution and selling the product and also include a favourable return on

the product for company's efforts.

2. Marketing mix strategy: Price is the one of important tool in the market mix. Decisions

made on other market mix tool affect the pricing policies and decisions. AMA Ltd has to

charge higher prices so that they can cover its expenses and generate profits (Zuo and

et.al., 2018).

CONCLUSION

Form the above report it can be concluded that the advance management accounting plays

important role to provide growth to the company. This accounting technique increase the sale

volume by lower the cost of production, resulting increase in the profits. Profitability and

controlling both are important in order to measure performance and finding any deficiencies.

Company is recommanded to use two price strategies that may increase the company value and

profitability. These strategies helpful to provide better consumer satisfaction by producing

products according to the needs and wants of the consumer.

REFERENCES

Books and Journals

Alam, M., 2020. Organisational processes and COVID-19 pandemic: implications for job

design. Journal of Accounting & Organizational Change.

Gunarathne, N. and Lee, K.H., 2018. Institutional pressures and corporate environmental

management maturity. Management of Environmental Quality: An International

Journal.

Jing, C., Zhang, J. and Song, B., 2020. An innovative evaluation method for performance of in-

service asphalt pavement with semi-rigid base. Construction and Building

Materials. 235, p.117376.

Johns, A. and et.al., 2018, May. Performance evaluation of bent heat pipes. In 2018 17th IEEE

Intersociety Conference on Thermal and Thermomechanical Phenomena in Electronic

Systems (ITherm) (pp. 302-310). IEEE.

Kearney, R., 2018. Public sector performance: management, motivation, and measurement.

routledge.

Khan, W. and et.al., 2018. Performance evaluation of Khyber Pakhtunkhwa Rice Husk Ash

(RHA) in improving mechanical behavior of cement. Construction and Building

Materials. 176, pp.89-102.

Kumar, B., 2018. Comparative performance evaluation of MMSE-based speech enhancement

techniques through simulation and real-time implementation. International Journal of

Speech Technology. 21(4), pp.1033-1044.

Kumari, U. and et.al., 2020. Calcium and zirconium modified acid activated alumina for

adsorptive removal of fluoride: Performance evaluation, kinetics, isotherm,

characterization and industrial wastewater treatment. Advanced Powder

Technology. 31(5), pp.2045-2060.

Moharir, P.V. and Tembhurkar, A.R., 2018. Comparative performance evaluation of novel

polystyrene membrane with ultrex as Proton Exchange Membranes in Microbial Fuel

Cell for bioelectricity production from food waste. Bioresource technology. 266,

pp.291-296.

Nayak, S.C., Misra, B.B. and Behera, H.S., 2018. On developing and performance evaluation of

adaptive second order neural network with GA-based training (ASONN-GA) for

financial time series prediction. In Advancements in Applied Metaheuristic

Computing (pp. 231-263). IGI global.

Ng, F. and Harrison, J., 2021. Preserving transferable skills in the accounting curriculum during

the COVID-19 pandemic. Accounting Research Journal.

Nitsas, M.T. and Koronaki, I.P., 2018. Experimental and theoretical performance evaluation of

evacuated tube collectors under Mediterranean climate conditions. Thermal Science and

Engineering Progress, 8. pp.457-469.

Sakamoto, Shinji, and et.al., 2021. "Performance evaluation of WMNs by WMN-PSOHC system

considering random inertia weight and linearly decreasing inertia weight replacement

methods." In International Conference on Innovative Mobile and Internet Services in

Ubiquitous Computing, pp. 39-48. Springer, Cham, 2019.

Sakamoto, Shinji and et.al., 2021. "Performance evaluation of WMNs WMN-PSOHC system

considering constriction and linearly decreasing inertia weight replacement methods."

Books and Journals

Alam, M., 2020. Organisational processes and COVID-19 pandemic: implications for job

design. Journal of Accounting & Organizational Change.

Gunarathne, N. and Lee, K.H., 2018. Institutional pressures and corporate environmental

management maturity. Management of Environmental Quality: An International

Journal.

Jing, C., Zhang, J. and Song, B., 2020. An innovative evaluation method for performance of in-

service asphalt pavement with semi-rigid base. Construction and Building

Materials. 235, p.117376.

Johns, A. and et.al., 2018, May. Performance evaluation of bent heat pipes. In 2018 17th IEEE

Intersociety Conference on Thermal and Thermomechanical Phenomena in Electronic

Systems (ITherm) (pp. 302-310). IEEE.

Kearney, R., 2018. Public sector performance: management, motivation, and measurement.

routledge.

Khan, W. and et.al., 2018. Performance evaluation of Khyber Pakhtunkhwa Rice Husk Ash

(RHA) in improving mechanical behavior of cement. Construction and Building

Materials. 176, pp.89-102.

Kumar, B., 2018. Comparative performance evaluation of MMSE-based speech enhancement

techniques through simulation and real-time implementation. International Journal of

Speech Technology. 21(4), pp.1033-1044.

Kumari, U. and et.al., 2020. Calcium and zirconium modified acid activated alumina for

adsorptive removal of fluoride: Performance evaluation, kinetics, isotherm,

characterization and industrial wastewater treatment. Advanced Powder

Technology. 31(5), pp.2045-2060.

Moharir, P.V. and Tembhurkar, A.R., 2018. Comparative performance evaluation of novel

polystyrene membrane with ultrex as Proton Exchange Membranes in Microbial Fuel

Cell for bioelectricity production from food waste. Bioresource technology. 266,

pp.291-296.

Nayak, S.C., Misra, B.B. and Behera, H.S., 2018. On developing and performance evaluation of

adaptive second order neural network with GA-based training (ASONN-GA) for

financial time series prediction. In Advancements in Applied Metaheuristic

Computing (pp. 231-263). IGI global.

Ng, F. and Harrison, J., 2021. Preserving transferable skills in the accounting curriculum during

the COVID-19 pandemic. Accounting Research Journal.

Nitsas, M.T. and Koronaki, I.P., 2018. Experimental and theoretical performance evaluation of

evacuated tube collectors under Mediterranean climate conditions. Thermal Science and

Engineering Progress, 8. pp.457-469.

Sakamoto, Shinji, and et.al., 2021. "Performance evaluation of WMNs by WMN-PSOHC system

considering random inertia weight and linearly decreasing inertia weight replacement

methods." In International Conference on Innovative Mobile and Internet Services in

Ubiquitous Computing, pp. 39-48. Springer, Cham, 2019.

Sakamoto, Shinji and et.al., 2021. "Performance evaluation of WMNs WMN-PSOHC system

considering constriction and linearly decreasing inertia weight replacement methods."

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.