Advanced Management Accounting Report: Business Environment Impact

VerifiedAdded on 2020/07/23

|17

|5233

|39

Report

AI Summary

This report delves into the intricacies of advanced management accounting, examining the purpose and presentation of financial information from a stakeholder perspective, including investors, senior management, banks, and creditors. It evaluates various microeconomic techniques, such as cost-volume-profit analysis, absorption costing, marginal costing, break-even analysis, and flexible budgeting, illustrating their application in supporting organizational structures. The report also explores variance analysis, emphasizing its significance in organizational budget control, along with the analysis of actual and standard costs to manage and correct variances. Furthermore, it assesses the impact of both external and internal factors, such as changing business environments, on management accounting practices, providing a comprehensive overview of the subject.

ADVANCED MANAGEMNET

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Purpose and presentation of financial information from stakeholder perspective............1

TASK 2............................................................................................................................................3

P2 Evaluate the different type of accounting microeconomic techniques in application to

support organisation...............................................................................................................3

TASK 3............................................................................................................................................7

P3 the concept of variance analysis and its importance for organizational budget control. . .7

P4 Analyse the actual and standard costs to control and correct variances............................9

TASK 4..........................................................................................................................................11

P5 How external and internal factors changing the business environment impact upon

management accounting ......................................................................................................11

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Purpose and presentation of financial information from stakeholder perspective............1

TASK 2............................................................................................................................................3

P2 Evaluate the different type of accounting microeconomic techniques in application to

support organisation...............................................................................................................3

TASK 3............................................................................................................................................7

P3 the concept of variance analysis and its importance for organizational budget control. . .7

P4 Analyse the actual and standard costs to control and correct variances............................9

TASK 4..........................................................................................................................................11

P5 How external and internal factors changing the business environment impact upon

management accounting ......................................................................................................11

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Management accounting is become a crucial element subject to managing and operating

the business. This is considered as an internal part and section of business which assist mangers

and accountants to manage departments and section of organisation, this report is prepared to

understand the dynamics of advanced management accounting system subject to operating and

management of business operations (Watts and McNair-Connolly, 2012). Purpose and

presentation of financial information from stakeholders prospective defined in this context.

Various type of accounting microeconomics techniques in application to assist organisational

structure explained briefly.

Variance analysis and its importance subject to making budgets elaborated in

organisational context. Actual and standard cost is defined in this context with the environmental

impact upon management accoutring also defined in this context. How external and internal

factors changing the business environment impact upon management accounting.

TASK 1

P1 Purpose and presentation of financial information from stakeholder perspective

In organisational context stake holders are the persons which retain significant interest in

the growth and development of organisation. These are the parties which has some certain needs

and requirement in terms of financial and non-financial interest. Putting the interest of

stakeholders first is one of the essential retirement of organization. Because these are the person

who only remain responsible for sustainable development and growth of organisation.

Presentation of financial information become more important and crucial task for organisations

for stakeholders. Stakeholders can be found in various form such as share

Purpose of financial information and presentation

Building communication and shared with stakeholders organisation is one of the key

objective of financial representation. Making financial records and presenting financial

information is also one of the key aspect in organisational context. To attain stake holder’s

interest and make accounting viability of the organisation in effective and optimum manner.

Purpose of financial representation can be bifurcated in following aspect’s;

1

Management accounting is become a crucial element subject to managing and operating

the business. This is considered as an internal part and section of business which assist mangers

and accountants to manage departments and section of organisation, this report is prepared to

understand the dynamics of advanced management accounting system subject to operating and

management of business operations (Watts and McNair-Connolly, 2012). Purpose and

presentation of financial information from stakeholders prospective defined in this context.

Various type of accounting microeconomics techniques in application to assist organisational

structure explained briefly.

Variance analysis and its importance subject to making budgets elaborated in

organisational context. Actual and standard cost is defined in this context with the environmental

impact upon management accoutring also defined in this context. How external and internal

factors changing the business environment impact upon management accounting.

TASK 1

P1 Purpose and presentation of financial information from stakeholder perspective

In organisational context stake holders are the persons which retain significant interest in

the growth and development of organisation. These are the parties which has some certain needs

and requirement in terms of financial and non-financial interest. Putting the interest of

stakeholders first is one of the essential retirement of organization. Because these are the person

who only remain responsible for sustainable development and growth of organisation.

Presentation of financial information become more important and crucial task for organisations

for stakeholders. Stakeholders can be found in various form such as share

Purpose of financial information and presentation

Building communication and shared with stakeholders organisation is one of the key

objective of financial representation. Making financial records and presenting financial

information is also one of the key aspect in organisational context. To attain stake holder’s

interest and make accounting viability of the organisation in effective and optimum manner.

Purpose of financial representation can be bifurcated in following aspect’s;

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

To Build credibility: there are to major characteristics remain associated with reporting

task, first is qualitative and second is quantitative. These concepts remain based upon concepts

in respect of presenting financial information to stakeholders of organisation (Jakobsen, 2012).

To Make accoutring structure viable: This is also one of the major purpose of

presenting financial reports in front of internal stake holders. It helps to make the organisation’s

structure flexible by gathering interest of employees and managers of organization.

Reliability: It contains the observation in respect of presenting information by following

all the legal structure, legislation and terms. Which policies and structure is being used is

disclosed in front of stakeholders.

Intangibility: This objective remains associated with representing information and

details in terms of complex business structure which contains some technical knowledge and

subject.

Financial information from stakeholders perspective

Investors: these information helps stakeholders to analyse the liquidity position and how

much flow generated by activities. This helps to make investment plan for better execution.

Financial representations is systematic procedure that contains a logical and regional aspects

while preparing and presenting financial statements to stakeholders and managers. This

information remains important for the investors subject to analyse the liquidity and flow of cash

for to give credits and manage the operations. Financial projection and analysing the

performance depends upon capital structure of organization. Investors mainly analyse the

financial position, capital structure, reserves and surplus ratio and return on investments.

Senior management: Financial information is required to justify the financial position of

business to senior management. It helps to determine the change in equity as the base of share

capital, reserve and surplus. How much control and ownership is distributed in the hands of

members and share holders is required to determine for stakeholders. Presenting financial

information for stakeholders is one of the complex task for senior managers and Accountants

because it contains large responsibility and credibility subject to presenting financial statements

and financial reports. Their main perspective mainly associated with presenting true and fair

report to external stakeholders and other associated parties.

Banks: The overall performance is presented in the form of financial position of

organisation. financial institutions and firms remain associated with analysing the requirement of

2

task, first is qualitative and second is quantitative. These concepts remain based upon concepts

in respect of presenting financial information to stakeholders of organisation (Jakobsen, 2012).

To Make accoutring structure viable: This is also one of the major purpose of

presenting financial reports in front of internal stake holders. It helps to make the organisation’s

structure flexible by gathering interest of employees and managers of organization.

Reliability: It contains the observation in respect of presenting information by following

all the legal structure, legislation and terms. Which policies and structure is being used is

disclosed in front of stakeholders.

Intangibility: This objective remains associated with representing information and

details in terms of complex business structure which contains some technical knowledge and

subject.

Financial information from stakeholders perspective

Investors: these information helps stakeholders to analyse the liquidity position and how

much flow generated by activities. This helps to make investment plan for better execution.

Financial representations is systematic procedure that contains a logical and regional aspects

while preparing and presenting financial statements to stakeholders and managers. This

information remains important for the investors subject to analyse the liquidity and flow of cash

for to give credits and manage the operations. Financial projection and analysing the

performance depends upon capital structure of organization. Investors mainly analyse the

financial position, capital structure, reserves and surplus ratio and return on investments.

Senior management: Financial information is required to justify the financial position of

business to senior management. It helps to determine the change in equity as the base of share

capital, reserve and surplus. How much control and ownership is distributed in the hands of

members and share holders is required to determine for stakeholders. Presenting financial

information for stakeholders is one of the complex task for senior managers and Accountants

because it contains large responsibility and credibility subject to presenting financial statements

and financial reports. Their main perspective mainly associated with presenting true and fair

report to external stakeholders and other associated parties.

Banks: The overall performance is presented in the form of financial position of

organisation. financial institutions and firms remain associated with analysing the requirement of

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

financial resources within the organisation and provide financial help as per requirement.

Stakeholders as investors and banks invest in those organisation which retain strong capital base

and structure. To aware the stakeholders in term of capital and assets base financial position is

required. Banks and financial institutions evaluate the credit ratings of organisations. It analyse

whether organisation is able to repay loans and credits to banks on time or not. Information form

cash flow statement remain more important for banks and financial institutions.

Creditors: It is important for creditors to analyse the effectiveness of business. Creditors

seek for best earning companies to invest their amount and get good returns on time or recover

their lending in desirable time. To provide accurate information and data subject to financial

growth and development of organisation is one of the key perspective associated with creditors

for sustainable development and growth. If an organisation is adhering proper credit policy and

payment system then credibility of that organisation increased more. Creditors put their interest

only those organisations.

Form the past years it is observed that the rules and regulations regarding financial

representation has become more authenticated. Professional accounting organisations are

becoming the part of legalised accounting format and structure. ISAB, European commission are

authorities which provides a basis legal structure subject to presenting financial information to

stakeholders of organisation and outer parties. Accoutring and financial presentation provides

overview and vision of organisation that where the organisations stands and where to go. It

makes accounting credibility, tangibility and credibility of organisation.

TASK 2

P2 Evaluate the different type of accounting microeconomic techniques in application to support

organisation

Microeconomic techniques in management accounting

This is one of the essential aspect in respect of analysing the performance of organisation

these are the main concepts which are considered in manage met accounting system. There are

type of techniques which are used in management accoutring as microeconomic costing

techniques;

Cost volume profit: cost volume and profit are a concept which is considered as

essential in respect of understating. A perfect combination of cost volume and profit helps

3

Stakeholders as investors and banks invest in those organisation which retain strong capital base

and structure. To aware the stakeholders in term of capital and assets base financial position is

required. Banks and financial institutions evaluate the credit ratings of organisations. It analyse

whether organisation is able to repay loans and credits to banks on time or not. Information form

cash flow statement remain more important for banks and financial institutions.

Creditors: It is important for creditors to analyse the effectiveness of business. Creditors

seek for best earning companies to invest their amount and get good returns on time or recover

their lending in desirable time. To provide accurate information and data subject to financial

growth and development of organisation is one of the key perspective associated with creditors

for sustainable development and growth. If an organisation is adhering proper credit policy and

payment system then credibility of that organisation increased more. Creditors put their interest

only those organisations.

Form the past years it is observed that the rules and regulations regarding financial

representation has become more authenticated. Professional accounting organisations are

becoming the part of legalised accounting format and structure. ISAB, European commission are

authorities which provides a basis legal structure subject to presenting financial information to

stakeholders of organisation and outer parties. Accoutring and financial presentation provides

overview and vision of organisation that where the organisations stands and where to go. It

makes accounting credibility, tangibility and credibility of organisation.

TASK 2

P2 Evaluate the different type of accounting microeconomic techniques in application to support

organisation

Microeconomic techniques in management accounting

This is one of the essential aspect in respect of analysing the performance of organisation

these are the main concepts which are considered in manage met accounting system. There are

type of techniques which are used in management accoutring as microeconomic costing

techniques;

Cost volume profit: cost volume and profit are a concept which is considered as

essential in respect of understating. A perfect combination of cost volume and profit helps

3

accountants and managers to make strategies and plans for generating income. This is one of the

effective and optimum technique in terms of analysing the profit margin and cost for production.

This technique is centralised around three major aspects such as margin of safety, break even

point in units and break even point in sales (Grabner and Moers, 2013).

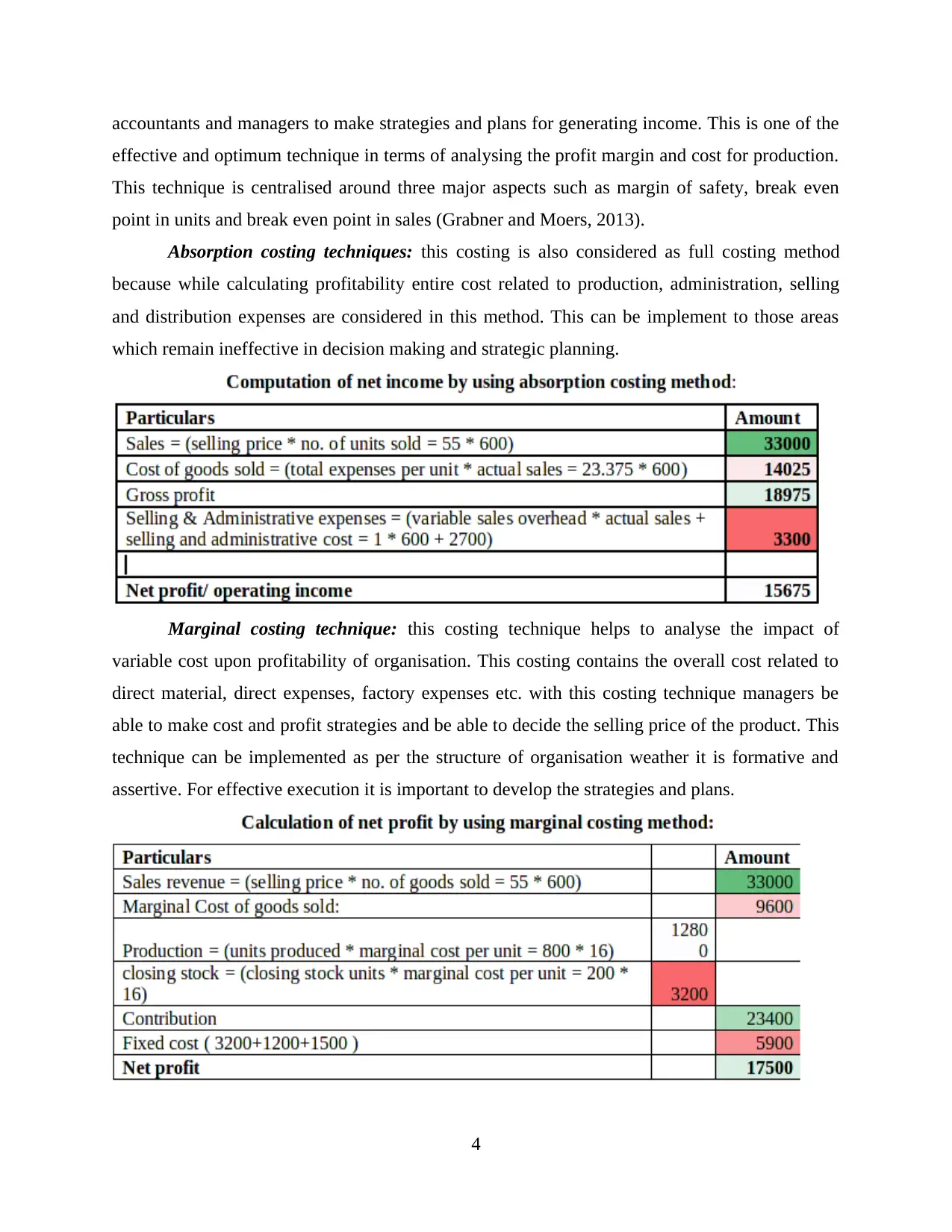

Absorption costing techniques: this costing is also considered as full costing method

because while calculating profitability entire cost related to production, administration, selling

and distribution expenses are considered in this method. This can be implement to those areas

which remain ineffective in decision making and strategic planning.

Marginal costing technique: this costing technique helps to analyse the impact of

variable cost upon profitability of organisation. This costing contains the overall cost related to

direct material, direct expenses, factory expenses etc. with this costing technique managers be

able to make cost and profit strategies and be able to decide the selling price of the product. This

technique can be implemented as per the structure of organisation weather it is formative and

assertive. For effective execution it is important to develop the strategies and plans.

4

effective and optimum technique in terms of analysing the profit margin and cost for production.

This technique is centralised around three major aspects such as margin of safety, break even

point in units and break even point in sales (Grabner and Moers, 2013).

Absorption costing techniques: this costing is also considered as full costing method

because while calculating profitability entire cost related to production, administration, selling

and distribution expenses are considered in this method. This can be implement to those areas

which remain ineffective in decision making and strategic planning.

Marginal costing technique: this costing technique helps to analyse the impact of

variable cost upon profitability of organisation. This costing contains the overall cost related to

direct material, direct expenses, factory expenses etc. with this costing technique managers be

able to make cost and profit strategies and be able to decide the selling price of the product. This

technique can be implemented as per the structure of organisation weather it is formative and

assertive. For effective execution it is important to develop the strategies and plans.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

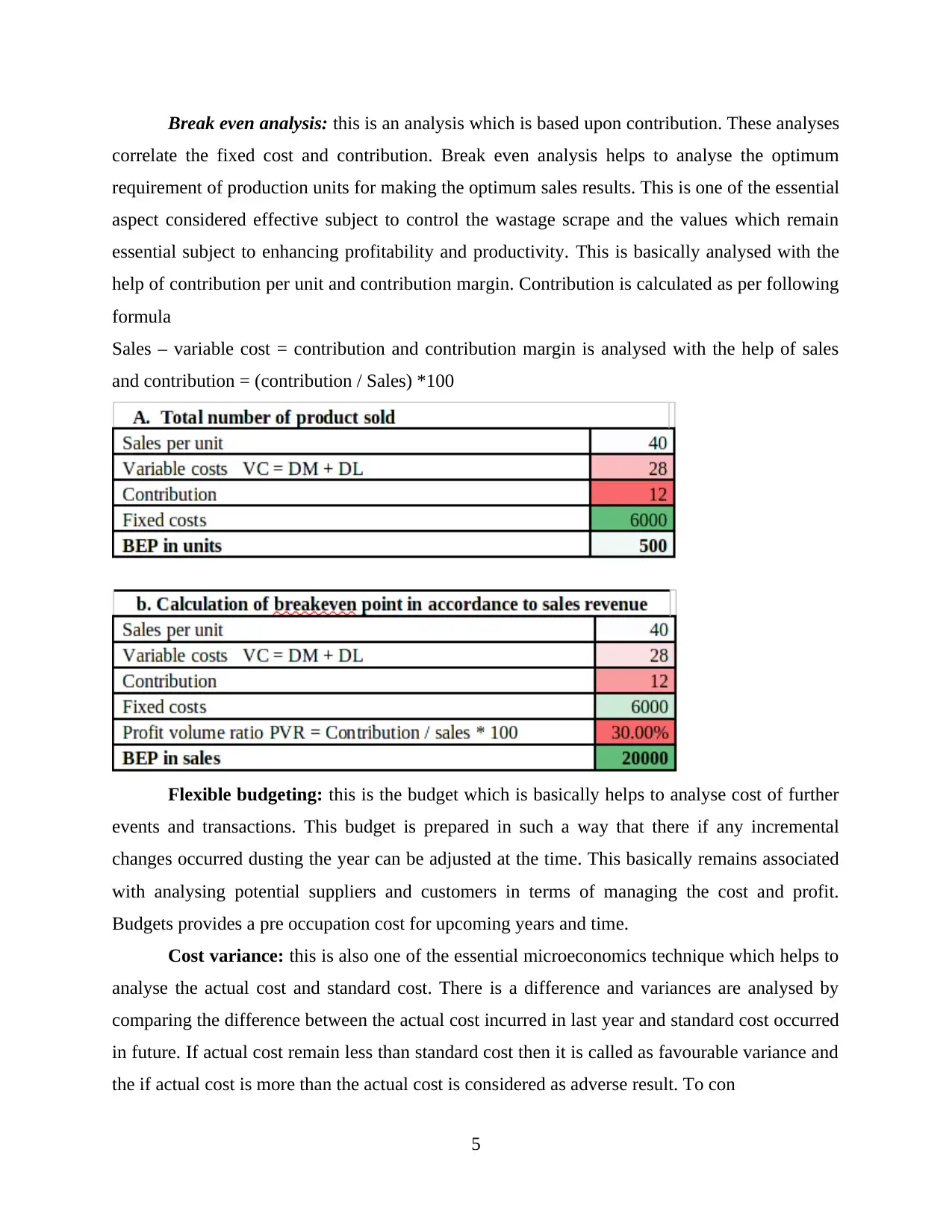

Break even analysis: this is an analysis which is based upon contribution. These analyses

correlate the fixed cost and contribution. Break even analysis helps to analyse the optimum

requirement of production units for making the optimum sales results. This is one of the essential

aspect considered effective subject to control the wastage scrape and the values which remain

essential subject to enhancing profitability and productivity. This is basically analysed with the

help of contribution per unit and contribution margin. Contribution is calculated as per following

formula

Sales – variable cost = contribution and contribution margin is analysed with the help of sales

and contribution = (contribution / Sales) *100

Flexible budgeting: this is the budget which is basically helps to analyse cost of further

events and transactions. This budget is prepared in such a way that there if any incremental

changes occurred dusting the year can be adjusted at the time. This basically remains associated

with analysing potential suppliers and customers in terms of managing the cost and profit.

Budgets provides a pre occupation cost for upcoming years and time.

Cost variance: this is also one of the essential microeconomics technique which helps to

analyse the actual cost and standard cost. There is a difference and variances are analysed by

comparing the difference between the actual cost incurred in last year and standard cost occurred

in future. If actual cost remain less than standard cost then it is called as favourable variance and

the if actual cost is more than the actual cost is considered as adverse result. To con

5

correlate the fixed cost and contribution. Break even analysis helps to analyse the optimum

requirement of production units for making the optimum sales results. This is one of the essential

aspect considered effective subject to control the wastage scrape and the values which remain

essential subject to enhancing profitability and productivity. This is basically analysed with the

help of contribution per unit and contribution margin. Contribution is calculated as per following

formula

Sales – variable cost = contribution and contribution margin is analysed with the help of sales

and contribution = (contribution / Sales) *100

Flexible budgeting: this is the budget which is basically helps to analyse cost of further

events and transactions. This budget is prepared in such a way that there if any incremental

changes occurred dusting the year can be adjusted at the time. This basically remains associated

with analysing potential suppliers and customers in terms of managing the cost and profit.

Budgets provides a pre occupation cost for upcoming years and time.

Cost variance: this is also one of the essential microeconomics technique which helps to

analyse the actual cost and standard cost. There is a difference and variances are analysed by

comparing the difference between the actual cost incurred in last year and standard cost occurred

in future. If actual cost remain less than standard cost then it is called as favourable variance and

the if actual cost is more than the actual cost is considered as adverse result. To con

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost allocation and appropriation on the basis of absorption costing

Absorption costing technique remains associated with the allocation or divination of cost

at different cost centres. Such as allocation of direct cost depends upon manufacturing and

production cost. This is one of the complex task in respect of managers and accountant because

they have to identify the relevance of the particular department and section (Fullerton, Kennedy

and Widener, 2013).

Discounted cash flow methods

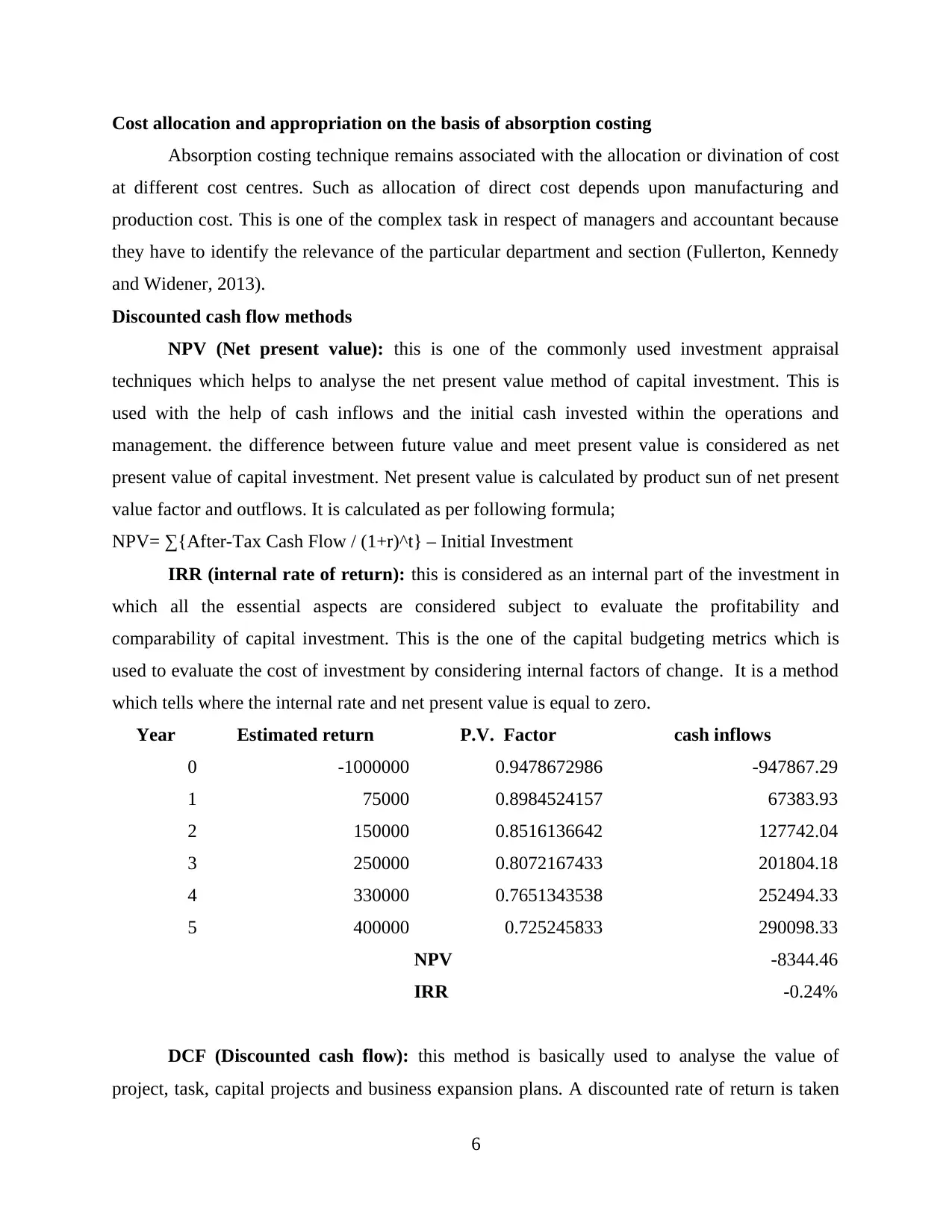

NPV (Net present value): this is one of the commonly used investment appraisal

techniques which helps to analyse the net present value method of capital investment. This is

used with the help of cash inflows and the initial cash invested within the operations and

management. the difference between future value and meet present value is considered as net

present value of capital investment. Net present value is calculated by product sun of net present

value factor and outflows. It is calculated as per following formula;

NPV= ∑{After-Tax Cash Flow / (1+r)^t} – Initial Investment

IRR (internal rate of return): this is considered as an internal part of the investment in

which all the essential aspects are considered subject to evaluate the profitability and

comparability of capital investment. This is the one of the capital budgeting metrics which is

used to evaluate the cost of investment by considering internal factors of change. It is a method

which tells where the internal rate and net present value is equal to zero.

Year Estimated return P.V. Factor cash inflows

0 -1000000 0.9478672986 -947867.29

1 75000 0.8984524157 67383.93

2 150000 0.8516136642 127742.04

3 250000 0.8072167433 201804.18

4 330000 0.7651343538 252494.33

5 400000 0.725245833 290098.33

NPV -8344.46

IRR -0.24%

DCF (Discounted cash flow): this method is basically used to analyse the value of

project, task, capital projects and business expansion plans. A discounted rate of return is taken

6

Absorption costing technique remains associated with the allocation or divination of cost

at different cost centres. Such as allocation of direct cost depends upon manufacturing and

production cost. This is one of the complex task in respect of managers and accountant because

they have to identify the relevance of the particular department and section (Fullerton, Kennedy

and Widener, 2013).

Discounted cash flow methods

NPV (Net present value): this is one of the commonly used investment appraisal

techniques which helps to analyse the net present value method of capital investment. This is

used with the help of cash inflows and the initial cash invested within the operations and

management. the difference between future value and meet present value is considered as net

present value of capital investment. Net present value is calculated by product sun of net present

value factor and outflows. It is calculated as per following formula;

NPV= ∑{After-Tax Cash Flow / (1+r)^t} – Initial Investment

IRR (internal rate of return): this is considered as an internal part of the investment in

which all the essential aspects are considered subject to evaluate the profitability and

comparability of capital investment. This is the one of the capital budgeting metrics which is

used to evaluate the cost of investment by considering internal factors of change. It is a method

which tells where the internal rate and net present value is equal to zero.

Year Estimated return P.V. Factor cash inflows

0 -1000000 0.9478672986 -947867.29

1 75000 0.8984524157 67383.93

2 150000 0.8516136642 127742.04

3 250000 0.8072167433 201804.18

4 330000 0.7651343538 252494.33

5 400000 0.725245833 290098.33

NPV -8344.46

IRR -0.24%

DCF (Discounted cash flow): this method is basically used to analyse the value of

project, task, capital projects and business expansion plans. A discounted rate of return is taken

6

to calculate the discounted cash flow. This is one of the valuable method which is used to

estimate and measure the future opportunities for capital investment. This basically remain

associated with the decreasing the value of net cash outflows and inflows for better

understanding. This is calculated with the help of discounted cash flow.

Non- discounted cash flow methods

Payback period: this method provides an opportunity for better growth and sustainable

of investment made on particular project or section. It assists mangers and accountants that how

much time it will take to recover the amount incurred on capital investment (Ernstberger, Stich

and Vogler, 2012).

ARR (Average rate of return): This is the method which mainly used to calculate the of

return on the basis of average profit and average investment. It identifies the average returns is

being earned by organisation for a particular period.

TASK 3

P3 the concept of variance analysis and its importance for organizational budget control

Variance analysis as a concept and a technique

This is the qualitative technique of analysing the difference between the planned and

actual behaviour (DRURY, 2013). This analysis is basically used to maintain and control the

overall operational and management cost. It is considered by the example such as is budgeted as

a sales figure for the year of 2018 but an actual cost was recorded as 8000. Now the variance

yield is calculated as the difference of 2000. It is better understandable on variance analysis at

trend line. There are type of variances used in variance analysis technique like purchase price

variance, labour cost variance, variable hover head spending variance and fixed variance.

Favourable and unfavourable variances

There are two results can be found with the analysis of variance analysis such as positive

and negative variance. If actual results remain more then the budgeted results then it is

considered as the negative variance or unfavourable variance and if the budgeted variance

remains high then the actual results then it is considered as positive variance or favourable

variance.

Controlling and correcting variances

7

estimate and measure the future opportunities for capital investment. This basically remain

associated with the decreasing the value of net cash outflows and inflows for better

understanding. This is calculated with the help of discounted cash flow.

Non- discounted cash flow methods

Payback period: this method provides an opportunity for better growth and sustainable

of investment made on particular project or section. It assists mangers and accountants that how

much time it will take to recover the amount incurred on capital investment (Ernstberger, Stich

and Vogler, 2012).

ARR (Average rate of return): This is the method which mainly used to calculate the of

return on the basis of average profit and average investment. It identifies the average returns is

being earned by organisation for a particular period.

TASK 3

P3 the concept of variance analysis and its importance for organizational budget control

Variance analysis as a concept and a technique

This is the qualitative technique of analysing the difference between the planned and

actual behaviour (DRURY, 2013). This analysis is basically used to maintain and control the

overall operational and management cost. It is considered by the example such as is budgeted as

a sales figure for the year of 2018 but an actual cost was recorded as 8000. Now the variance

yield is calculated as the difference of 2000. It is better understandable on variance analysis at

trend line. There are type of variances used in variance analysis technique like purchase price

variance, labour cost variance, variable hover head spending variance and fixed variance.

Favourable and unfavourable variances

There are two results can be found with the analysis of variance analysis such as positive

and negative variance. If actual results remain more then the budgeted results then it is

considered as the negative variance or unfavourable variance and if the budgeted variance

remains high then the actual results then it is considered as positive variance or favourable

variance.

Controlling and correcting variances

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This is basically used to analyse the difference and identifying the difference creating

factors. By analysing the differences and reason precautions can be taken on time to control cost.

With the help of variance analysis there is a report prepared called as variance analysis report.

This report is use to take important decisions and decision-making process.

Integrating variance analysis into budget monitoring across an organisation: this is

also one of the essential aspect in terms of analysing the difference and figure out the result.

These results are used in making important strategies and plans in order to make accurate

budgets and policies.

Schedule variance vs cost variance

Schedule variance is basically used to keep the project on schedule. It basically helps to

make schedule and plan for better effectiveness of task and projects. It assists managers and

accountants to track the project schedule and keep align the cost allocation process. It is

calculated as per following formula;

Schedule Variance = Earned Value – Planned Value

It is also considered essential in terms of approving the budget and complete the

task on time. It is observed that excess estimation of budget is not good for stakeholders and

organisation too. It mainly deals with the budget prepared for a particular project.

Cost Variance = Earned Value – Actual Cost

There are some examples of variance analysis given below

Material cost variance: standard cost - actual cost

= 408000-552000

= 144000(A)

Material price variance: actual quantity*(standard price - actual price)

= 240000*(2-2.3)

=72000(A)

Material usage variance: standard price*(standard quantity-actual quantity)

= 2*(204000-240000)

= 72000(A)

Calculation of labour variances

Labour cost variance: standard labour cost – actual labour cost

= 1062500-1400000

8

factors. By analysing the differences and reason precautions can be taken on time to control cost.

With the help of variance analysis there is a report prepared called as variance analysis report.

This report is use to take important decisions and decision-making process.

Integrating variance analysis into budget monitoring across an organisation: this is

also one of the essential aspect in terms of analysing the difference and figure out the result.

These results are used in making important strategies and plans in order to make accurate

budgets and policies.

Schedule variance vs cost variance

Schedule variance is basically used to keep the project on schedule. It basically helps to

make schedule and plan for better effectiveness of task and projects. It assists managers and

accountants to track the project schedule and keep align the cost allocation process. It is

calculated as per following formula;

Schedule Variance = Earned Value – Planned Value

It is also considered essential in terms of approving the budget and complete the

task on time. It is observed that excess estimation of budget is not good for stakeholders and

organisation too. It mainly deals with the budget prepared for a particular project.

Cost Variance = Earned Value – Actual Cost

There are some examples of variance analysis given below

Material cost variance: standard cost - actual cost

= 408000-552000

= 144000(A)

Material price variance: actual quantity*(standard price - actual price)

= 240000*(2-2.3)

=72000(A)

Material usage variance: standard price*(standard quantity-actual quantity)

= 2*(204000-240000)

= 72000(A)

Calculation of labour variances

Labour cost variance: standard labour cost – actual labour cost

= 1062500-1400000

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

= 337500(A)

Labour efficiency variance: standard rate*(standard time-actual time)

= 5*(212500-250000)

=187500(A)

Labour rate/pay variance: actual time*(standard rate-actual rate)

= 250000*(5-5.6)

= 150000(A)

Importance of variances in budgetary control

Variances plays vital role in budgetary control and decision making process. Variances

helps in determining the balance and gap between the actual and projected aspects.

It assist the management accounting which provides a firm's cost structure and revenue

process.

By variance analysis required areas of changes can be easily find out and provisions can

be made accordingly.

This helps to identify the idle areas to control the extra cost which remain ineffective as

production perspective in budgetary control process.

Appropriate variance analysis helps in understanding the changes and requirement of

additional sources for assessment of tasks and projects.

P4 Analyse the actual and standard costs to control and correct variances

Actual Costs: It refers to the actual amount paid or incurred in order to acquire an asset.

It is an accounting term that is mainly taken into account in order to determine actual amount of

money paid by business owner to acquire a product or assetsIt includes the cost of raw material,

overhead expenses and labour cost for the particular accounting year. It is one of the simplest

and most common method to taken into consideration by companies as it mainly works on

computing actual cost and does not need any pre-planning or any pre-defined standards

(Driouchi and Bennett, 2012). For example: For a plant producing pencil, company needs to take

into account factors like total working hour consumes, overhead cost, raw material cost so to

figure out actual cost of one pencil or total pencil

How actual cost is determined:

Actual Direct Cost Actual cost rates* Actual quantities used

Actual Indirect Cost Allocated Indirect Cost Rates*Actual

9

Labour efficiency variance: standard rate*(standard time-actual time)

= 5*(212500-250000)

=187500(A)

Labour rate/pay variance: actual time*(standard rate-actual rate)

= 250000*(5-5.6)

= 150000(A)

Importance of variances in budgetary control

Variances plays vital role in budgetary control and decision making process. Variances

helps in determining the balance and gap between the actual and projected aspects.

It assist the management accounting which provides a firm's cost structure and revenue

process.

By variance analysis required areas of changes can be easily find out and provisions can

be made accordingly.

This helps to identify the idle areas to control the extra cost which remain ineffective as

production perspective in budgetary control process.

Appropriate variance analysis helps in understanding the changes and requirement of

additional sources for assessment of tasks and projects.

P4 Analyse the actual and standard costs to control and correct variances

Actual Costs: It refers to the actual amount paid or incurred in order to acquire an asset.

It is an accounting term that is mainly taken into account in order to determine actual amount of

money paid by business owner to acquire a product or assetsIt includes the cost of raw material,

overhead expenses and labour cost for the particular accounting year. It is one of the simplest

and most common method to taken into consideration by companies as it mainly works on

computing actual cost and does not need any pre-planning or any pre-defined standards

(Driouchi and Bennett, 2012). For example: For a plant producing pencil, company needs to take

into account factors like total working hour consumes, overhead cost, raw material cost so to

figure out actual cost of one pencil or total pencil

How actual cost is determined:

Actual Direct Cost Actual cost rates* Actual quantities used

Actual Indirect Cost Allocated Indirect Cost Rates*Actual

9

Quantities of the Cost Allocation Bases.

How it is different from estimated and standard cost:

Actual Cost Estimated Cost Standard Cost

It determine actual cost

after evaluating each and

every aspect related with

acquiring a new asset.

It presumes what will the

total cost

It focuses on “What should

be actual cost”

It is flexible in nature as it

depends upon the cost of

other factors raw material,

overhead, labour etc.

It is also flexible in nature

and changed at every change

in particular situation.

It is more stable in nature

It can only be computed

once the cost of another

factor is determined

It can be taken into account

in every situation

It can only be used once the

total cost of data is available

Standard Cost: It can be defined as an estimated expense that normally takes place or

occurs at the time of producing a product or performance of service. In simple words, it

described the total sum of money a business will have to spend in order to produce a product or

perform a service. It is also referred as present costs because it is mainly computed on the basis

of management and statistics experience (Meaning of managerial account, 2017). These costs

are often used as target costs and are normally generated from analysis of historical data.

Standard Cost always vary from actual costs because every time situation has some

unpredictable factors.

How does it determined: (direct material+ direct labour + Overhead costs)*Price Rate*Quantity

Hours= Standard Cost.

Labour variance is also considered in above context and as per the above analysis the

labour cost variance was evaluated as 337500 adverse due to standard labour cost of 1062500

and actual labour cost of 1400000.

Labour efficiency variance is defined as 187500 adverse due to standard time of 212500

and actual time of 250000. this is calculated on the basis of standard rate of 5. labour rate is

calculated as 150000 adverse by differentiate standard rate of 5 and actual rate of 5.6.

10

How it is different from estimated and standard cost:

Actual Cost Estimated Cost Standard Cost

It determine actual cost

after evaluating each and

every aspect related with

acquiring a new asset.

It presumes what will the

total cost

It focuses on “What should

be actual cost”

It is flexible in nature as it

depends upon the cost of

other factors raw material,

overhead, labour etc.

It is also flexible in nature

and changed at every change

in particular situation.

It is more stable in nature

It can only be computed

once the cost of another

factor is determined

It can be taken into account

in every situation

It can only be used once the

total cost of data is available

Standard Cost: It can be defined as an estimated expense that normally takes place or

occurs at the time of producing a product or performance of service. In simple words, it

described the total sum of money a business will have to spend in order to produce a product or

perform a service. It is also referred as present costs because it is mainly computed on the basis

of management and statistics experience (Meaning of managerial account, 2017). These costs

are often used as target costs and are normally generated from analysis of historical data.

Standard Cost always vary from actual costs because every time situation has some

unpredictable factors.

How does it determined: (direct material+ direct labour + Overhead costs)*Price Rate*Quantity

Hours= Standard Cost.

Labour variance is also considered in above context and as per the above analysis the

labour cost variance was evaluated as 337500 adverse due to standard labour cost of 1062500

and actual labour cost of 1400000.

Labour efficiency variance is defined as 187500 adverse due to standard time of 212500

and actual time of 250000. this is calculated on the basis of standard rate of 5. labour rate is

calculated as 150000 adverse by differentiate standard rate of 5 and actual rate of 5.6.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.