Advanced Management Accounting Report: ABC Ltd Expansion Strategy

VerifiedAdded on 2021/02/20

|20

|5781

|68

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles, focusing on the case of ABC Ltd., a small to medium-sized enterprise (SME) planning international expansion. It begins by examining the purpose of financial information for various stakeholders, including internal stakeholders like employees and the management board, and external stakeholders such as investors and creditors. The report then delves into the development of financial statements for planning and decision-making, including budgeting, capital assessment, and risk assessment. It critically evaluates financial information, acknowledging its limitations while highlighting its strategic value. The report further explores microeconomic accounting techniques like cost analysis, cost-volume-profit analysis, and cost variances. Finally, it examines the impact of internal and external factors on management accounting, including change management and recommendations for adapting to these changes. The conclusion summarizes the key findings and emphasizes the importance of management accounting in strategic decision-making.

Advanced Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1- Purpose of financial information for different stakeholders.................................................1

M1- developing financial information for planning and decision-making..................................3

D1- Critical evaluation of financial information........................................................................6

TASK 2............................................................................................................................................7

P2- Evaluation of different microeconomic accounting techniques............................................7

M2- Advantages and disadvantages of accounting techniques....................................................9

D2- Application of different accounting techniques and variances...........................................11

TASK 4 .........................................................................................................................................11

P5- External and internal factors impact on management accounting.......................................11

M4- Impact of different types of changes and responses to such changes................................14

D3- Critical evaluation of change and recommendations on acceptance of change..................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1- Purpose of financial information for different stakeholders.................................................1

M1- developing financial information for planning and decision-making..................................3

D1- Critical evaluation of financial information........................................................................6

TASK 2............................................................................................................................................7

P2- Evaluation of different microeconomic accounting techniques............................................7

M2- Advantages and disadvantages of accounting techniques....................................................9

D2- Application of different accounting techniques and variances...........................................11

TASK 4 .........................................................................................................................................11

P5- External and internal factors impact on management accounting.......................................11

M4- Impact of different types of changes and responses to such changes................................14

D3- Critical evaluation of change and recommendations on acceptance of change..................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management Accounting is a professional attribute of core accounting which aligns with the

management body of the business in formulation of strategic policies and decision making

criterion for the future. To better understand, the contextual literature of management accounting

in business, ABC Ltd., a profitable SME planning to expand abroad is chosen to develop a deep

understanding of various Management accounting systems, processes, principles, fundamental

tools and techniques which shall be preferred by the decision making body of ABC Ltd. To

understand the need of it in developing a profound system and monitoring business growth with

the help of critical financial information provided by management accounting (Bhimani, 2009).

Advancement in management accounting as a system helps business in taking accounting

knowledge more vibrantly and seriously to regulate its functions, processes and future decision-

making criterion.

TASK 1

P1- Purpose of financial information for different stakeholders

Financial information: It is the information derived from financial statements of the

firm. Financial statements which comprises mainly of profit & loss statement, balance sheet and

cash flow statements etc. provide key business related information which helps the managers and

stakeholders in inferring about the health and wealth of the business. Financial information is

highly used for the purpose of meeting reporting standards as a legal requirement by regulatory

body of the respective business nation (Chenhall and Moers, 2015). ABC Ltd Is surrounded by

various stakeholders who seek constructive financial information of the business which is

discussed as follows:

Internal stakeholders: These are the stakeholders who are internal to ABC Ltd., who are

the first ones to be directly associated with the information. They are concerned with generating

true and fair statements, making agendas for the business to be conducted, and ensuring

compliance requirements by abiding to the procedural norms of preparing sound financial

statements (Andriof and Waddock, 2017). They typically include:

Employees: They form the most important element of business as they are the ones who

help a company in growing exponentially. The purpose of financial information for employees is

to ensure sustained financial health of the entity because the health of the firm is directly related

1

Management Accounting is a professional attribute of core accounting which aligns with the

management body of the business in formulation of strategic policies and decision making

criterion for the future. To better understand, the contextual literature of management accounting

in business, ABC Ltd., a profitable SME planning to expand abroad is chosen to develop a deep

understanding of various Management accounting systems, processes, principles, fundamental

tools and techniques which shall be preferred by the decision making body of ABC Ltd. To

understand the need of it in developing a profound system and monitoring business growth with

the help of critical financial information provided by management accounting (Bhimani, 2009).

Advancement in management accounting as a system helps business in taking accounting

knowledge more vibrantly and seriously to regulate its functions, processes and future decision-

making criterion.

TASK 1

P1- Purpose of financial information for different stakeholders

Financial information: It is the information derived from financial statements of the

firm. Financial statements which comprises mainly of profit & loss statement, balance sheet and

cash flow statements etc. provide key business related information which helps the managers and

stakeholders in inferring about the health and wealth of the business. Financial information is

highly used for the purpose of meeting reporting standards as a legal requirement by regulatory

body of the respective business nation (Chenhall and Moers, 2015). ABC Ltd Is surrounded by

various stakeholders who seek constructive financial information of the business which is

discussed as follows:

Internal stakeholders: These are the stakeholders who are internal to ABC Ltd., who are

the first ones to be directly associated with the information. They are concerned with generating

true and fair statements, making agendas for the business to be conducted, and ensuring

compliance requirements by abiding to the procedural norms of preparing sound financial

statements (Andriof and Waddock, 2017). They typically include:

Employees: They form the most important element of business as they are the ones who

help a company in growing exponentially. The purpose of financial information for employees is

to ensure sustained financial health of the entity because the health of the firm is directly related

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

to their individual as well as collective stakes of compensation, bonuses, employment security,

growth and learning etc. They toil effortlessly in order to establish foundation of the business so

as they can receive their monetary and non-monetary participation, to ensure this they are highly

concerned with the quantitative analysis of the business performance. Information about salary

deductions and additional benefits and fringe benefits are essential and supplied in the form of

income statement.

Management Board: Board of directors and management body seeks financial

information because they are responsible beings for ensuring longevity and development of the

business and to do that they would need quantitative data. They are watchdog of corporate

governance principle under the aegis of which comes the financial governance structure (Kaplan

and Atkinson, 2015). The purpose of financial information from the point of view of

management board is to construct policy making framework for the future and satisfy

stakeholders by assuring them with appropriate compliance and keeping their stakes at the

highest priority by devising sound business policies. Divided proposed for the current year,

remuneration to directors and audit plans are few major information presented crucial for

management and board.

External stakeholders: They are outside the organisation and act as external to it. They

act as pressure groups on the business to ensure that it functions ethically and sustainably. They

are indirectly affected by the decisions of the firm. They form the larger part of the business

environment surrounded by several micro & macro factors. If a business falls, it affects external

stakeholders deeply because their concerns are aligned with majority proportion (CLOR‐

PROELL and Maines, 2014). Financial information as proposed capital to and paid up capital,

debenture interests and return on investment are few essential information which are presented to

external stakeholders in the form of balance sheet. The list includes investors, creditors,

government, and society at large.

Investors: Investors long for financial information of the business because they provide

capital to the business for its operations expansion and wishes to receive dividends, which is

possible when firm is doing good in capital markets which ensures profitable returns, hence they

seek financial information. The purpose of financial information for investors is to ensure

themselves with better return on equity, bonus shares, rights issues, better interests on

redemption of debt capital etc. All this is possible only when businesses perform exceptionally

2

growth and learning etc. They toil effortlessly in order to establish foundation of the business so

as they can receive their monetary and non-monetary participation, to ensure this they are highly

concerned with the quantitative analysis of the business performance. Information about salary

deductions and additional benefits and fringe benefits are essential and supplied in the form of

income statement.

Management Board: Board of directors and management body seeks financial

information because they are responsible beings for ensuring longevity and development of the

business and to do that they would need quantitative data. They are watchdog of corporate

governance principle under the aegis of which comes the financial governance structure (Kaplan

and Atkinson, 2015). The purpose of financial information from the point of view of

management board is to construct policy making framework for the future and satisfy

stakeholders by assuring them with appropriate compliance and keeping their stakes at the

highest priority by devising sound business policies. Divided proposed for the current year,

remuneration to directors and audit plans are few major information presented crucial for

management and board.

External stakeholders: They are outside the organisation and act as external to it. They

act as pressure groups on the business to ensure that it functions ethically and sustainably. They

are indirectly affected by the decisions of the firm. They form the larger part of the business

environment surrounded by several micro & macro factors. If a business falls, it affects external

stakeholders deeply because their concerns are aligned with majority proportion (CLOR‐

PROELL and Maines, 2014). Financial information as proposed capital to and paid up capital,

debenture interests and return on investment are few essential information which are presented to

external stakeholders in the form of balance sheet. The list includes investors, creditors,

government, and society at large.

Investors: Investors long for financial information of the business because they provide

capital to the business for its operations expansion and wishes to receive dividends, which is

possible when firm is doing good in capital markets which ensures profitable returns, hence they

seek financial information. The purpose of financial information for investors is to ensure

themselves with better return on equity, bonus shares, rights issues, better interests on

redemption of debt capital etc. All this is possible only when businesses perform exceptionally

2

well at capital markets. Their purpose to seek financial data is to appraise the investment option

in the business. Earnings per share, growth rate and trends are presented in annual report that

elaborate the quantitative information to investors.

Creditors: They consists of banks, financial institutions, venture capitalists and

institutional credit facilities which provide loans and advances for the funding requirements. The

purpose of financial information for creditors is to ascertain that business is performing well

which ensures repayment capacity along with interest to them. They have two faced alignments

with the depositors and business debtors. Their stakes are considered highest during winding up

process (Yang, 2014). Creditors remain secured from the possible debt failure of business, for

this purpose they conduct financial pedagogy of the debtor business. Credit policies and the

credit notes and changes in rates and charges information presented to creditors in the form of

annual report.

M1- developing financial information for planning and decision-making

Need for developing financial statements: A business needs to develop financial

statements to provide constructive data set which helps in analysing the profitability and liquidity

position of the firm along with getting insights about how has the invested capital performed

during a period (Carraher and Van Auken, 2013). Apart from these objectives financial

statements helps a business in growing other facets of financial needs which are as follows:

Budgeting: Financial statements show forecasted sales and revenue figures of the

business for a brief period which aids in designing budgetary control device for the business. It

helps in budgeting accordingly for the future expenses of each departmental unit and their

relative profit making capacity. Budgeting sales and revenue figures helps firms in identification

of possible routes through which such figures could be achieved and paves a way for policy

making system (De Baerdemaeker and Bruggeman, 2015).

Assessing capital requirement: Based on the sales figures and revenue generation

capacity of products, financial statements provide insights regarding the capital acquisition needs

to the business and the possible avenues from which such capital needs can be fulfilled such as

debt-equity options. Capital needs fulfilment is basic feature of every business and having a

system which enables it to acquire capital through proper channels is really crucial.

Risk assessment: With the help of financial ratios and other indexes prepared based on

the financial information provided by financial statements, a business can identify the risk

3

in the business. Earnings per share, growth rate and trends are presented in annual report that

elaborate the quantitative information to investors.

Creditors: They consists of banks, financial institutions, venture capitalists and

institutional credit facilities which provide loans and advances for the funding requirements. The

purpose of financial information for creditors is to ascertain that business is performing well

which ensures repayment capacity along with interest to them. They have two faced alignments

with the depositors and business debtors. Their stakes are considered highest during winding up

process (Yang, 2014). Creditors remain secured from the possible debt failure of business, for

this purpose they conduct financial pedagogy of the debtor business. Credit policies and the

credit notes and changes in rates and charges information presented to creditors in the form of

annual report.

M1- developing financial information for planning and decision-making

Need for developing financial statements: A business needs to develop financial

statements to provide constructive data set which helps in analysing the profitability and liquidity

position of the firm along with getting insights about how has the invested capital performed

during a period (Carraher and Van Auken, 2013). Apart from these objectives financial

statements helps a business in growing other facets of financial needs which are as follows:

Budgeting: Financial statements show forecasted sales and revenue figures of the

business for a brief period which aids in designing budgetary control device for the business. It

helps in budgeting accordingly for the future expenses of each departmental unit and their

relative profit making capacity. Budgeting sales and revenue figures helps firms in identification

of possible routes through which such figures could be achieved and paves a way for policy

making system (De Baerdemaeker and Bruggeman, 2015).

Assessing capital requirement: Based on the sales figures and revenue generation

capacity of products, financial statements provide insights regarding the capital acquisition needs

to the business and the possible avenues from which such capital needs can be fulfilled such as

debt-equity options. Capital needs fulfilment is basic feature of every business and having a

system which enables it to acquire capital through proper channels is really crucial.

Risk assessment: With the help of financial ratios and other indexes prepared based on

the financial information provided by financial statements, a business can identify the risk

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

portion associated with particular investment and the mechanisms needed to reduce the impact of

risk (Chenhall, 2012). Hedging risks is need of every business firm and through advanced

financial information documents and channels risks could be sidelined to a great extent.

Presentation of financial information: Financial information will be meaningless until

it is presented in clear & concised formats. Information is inferred with the help of preparation of

key financial statements prepared by accounts department of ABC Ltd. The major statements

prepared are :

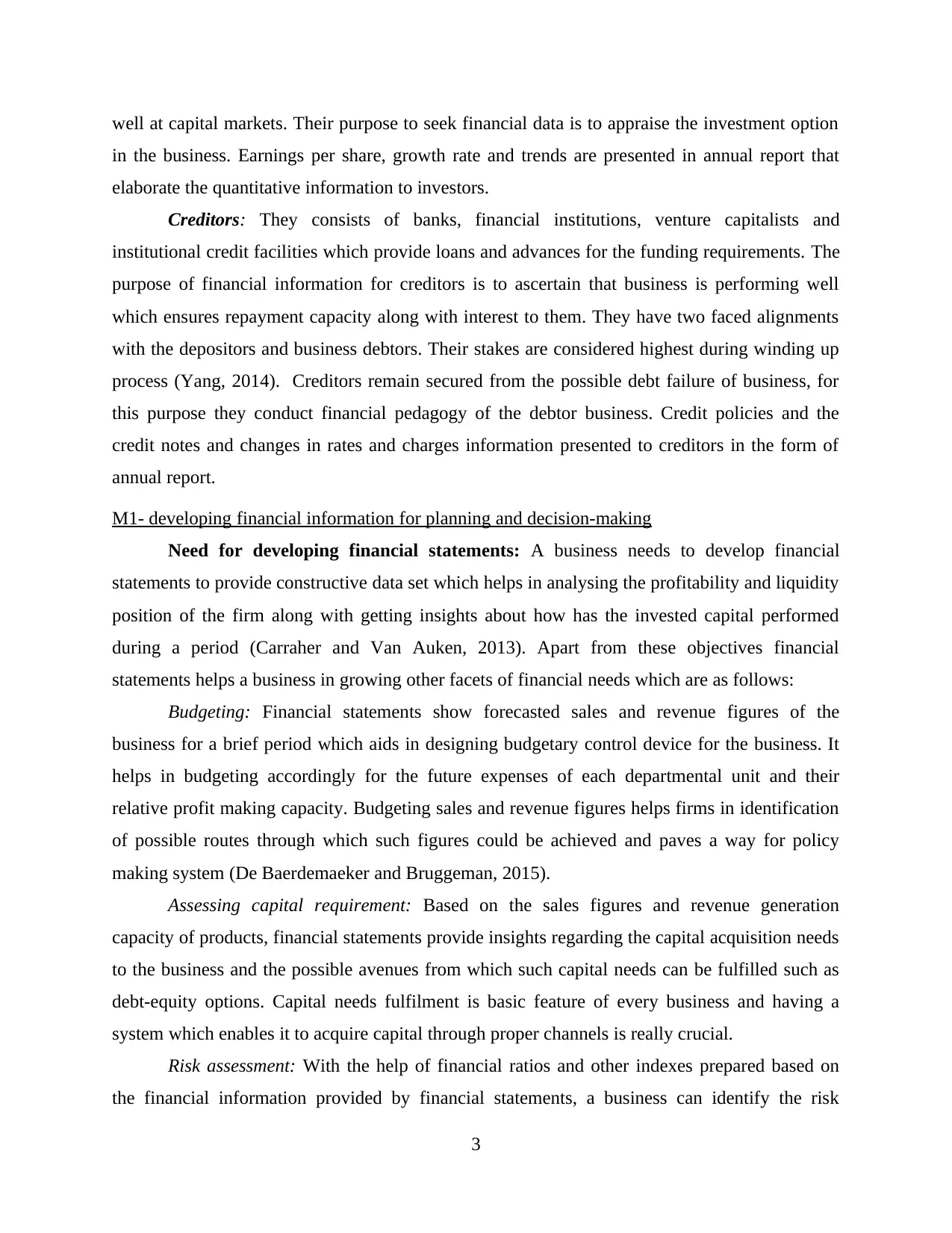

Profit & loss accounts: It is a financial statement which is prepared to ascertain revenues,

expenses and costs incurred during a fiscal year. It is often regarded as income statement. It

provides information about the company's propensity to generate profits by increasing sales or

reducing costs.

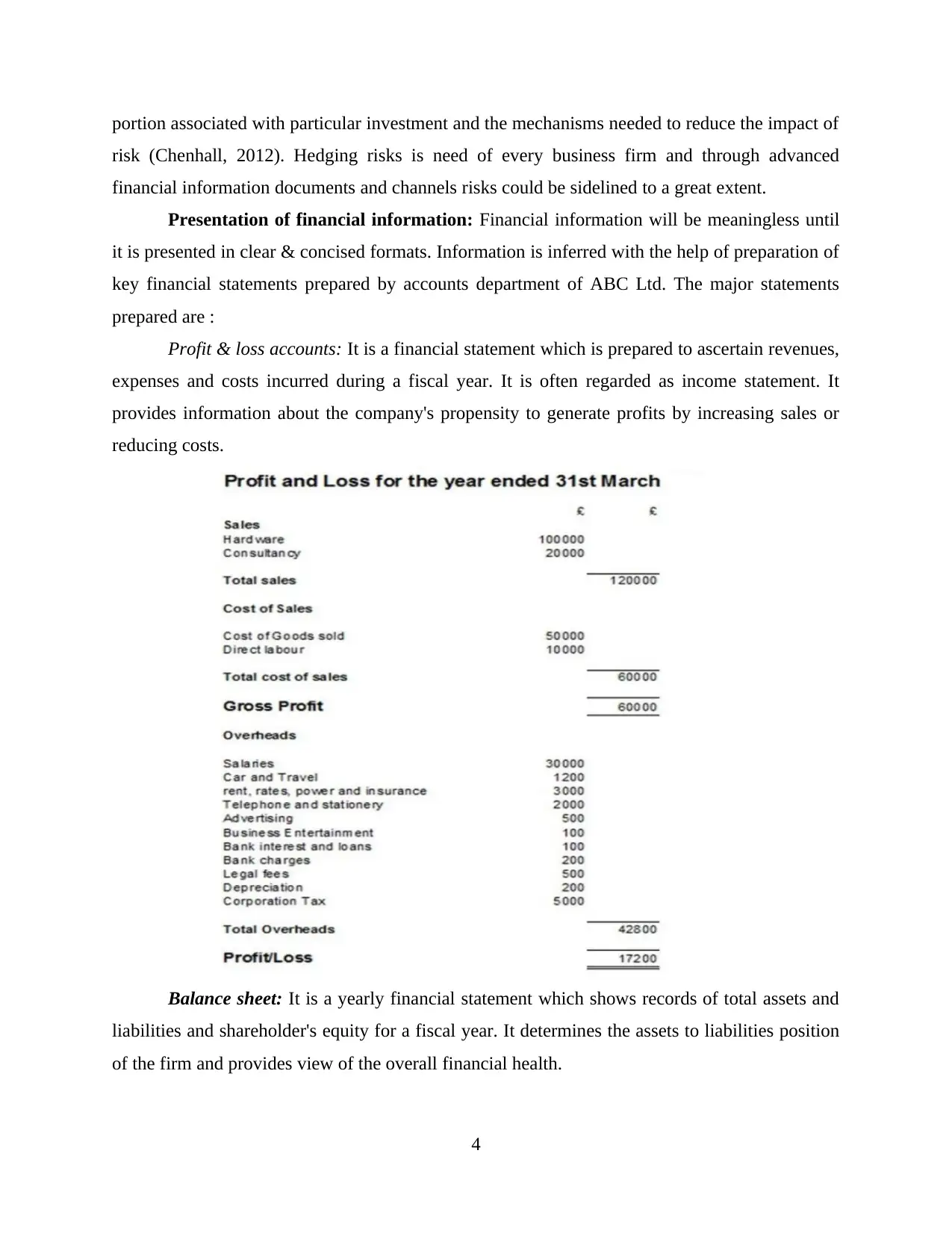

Balance sheet: It is a yearly financial statement which shows records of total assets and

liabilities and shareholder's equity for a fiscal year. It determines the assets to liabilities position

of the firm and provides view of the overall financial health.

4

risk (Chenhall, 2012). Hedging risks is need of every business firm and through advanced

financial information documents and channels risks could be sidelined to a great extent.

Presentation of financial information: Financial information will be meaningless until

it is presented in clear & concised formats. Information is inferred with the help of preparation of

key financial statements prepared by accounts department of ABC Ltd. The major statements

prepared are :

Profit & loss accounts: It is a financial statement which is prepared to ascertain revenues,

expenses and costs incurred during a fiscal year. It is often regarded as income statement. It

provides information about the company's propensity to generate profits by increasing sales or

reducing costs.

Balance sheet: It is a yearly financial statement which shows records of total assets and

liabilities and shareholder's equity for a fiscal year. It determines the assets to liabilities position

of the firm and provides view of the overall financial health.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

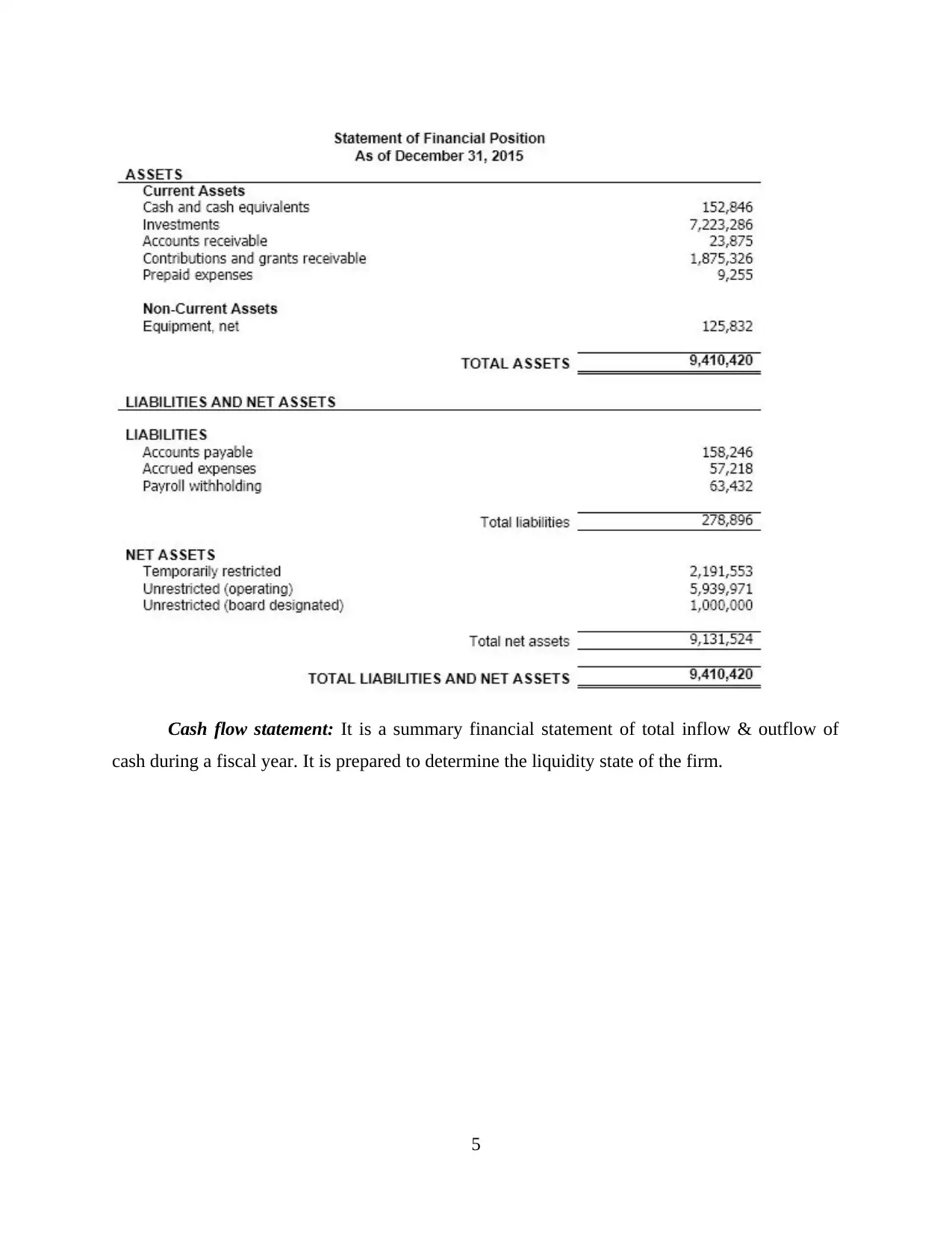

Cash flow statement: It is a summary financial statement of total inflow & outflow of

cash during a fiscal year. It is prepared to determine the liquidity state of the firm.

5

cash during a fiscal year. It is prepared to determine the liquidity state of the firm.

5

D1- Critical evaluation of financial information

Financial information disseminated by financial statements provides a brief view about

the economic health of a business. It aids the managers as a supportive function to assist in the

development of financial literacy and planning for future investment & decision making

criterion. However, often critique has been drawn on the fair reliance of financial statements for

judging a business functioning because statements are averse to inflation and have an

indifference to market prices. They are born out of pure accounting science but in real market

situations their applications differ from the modern economics (Palepu and Healy, 2013).

Inflationary outcomes affect a business by enforcing moulding on prices and demands for the

products, despite the judgemental capacity of accounting, factual study considering the external

6

Financial information disseminated by financial statements provides a brief view about

the economic health of a business. It aids the managers as a supportive function to assist in the

development of financial literacy and planning for future investment & decision making

criterion. However, often critique has been drawn on the fair reliance of financial statements for

judging a business functioning because statements are averse to inflation and have an

indifference to market prices. They are born out of pure accounting science but in real market

situations their applications differ from the modern economics (Palepu and Healy, 2013).

Inflationary outcomes affect a business by enforcing moulding on prices and demands for the

products, despite the judgemental capacity of accounting, factual study considering the external

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

economic environment alone is not probable with financial statements. However, Financial

statements provides a wide range of possibilities for the management to dwell in to find out

rationale behind skewness and discrepancies in data which aids in strategy formulation.

TASK 2

P2- Evaluation of different microeconomic accounting techniques

Microeconomic techniques: Microeconomics is the study of individual factor, or a

single unit which affects total economic units. It is dominated by quantitative models which are

used to study the behaviour of individuals and their overall role in affecting the macro economic

factors. This study majorly involves demand supply gap, their coefficients, household utility

analysis, consumer preferences, production function and a lot of different theories which define

the scope of economics in relation with the managerial capacity of the businesses (Cowell,

2018). In modern management accounting philosophy, microeconomic techniques play a crucial

role in measuring the profitability indexes of the business. Some majorly favoured

microeconomic tools are discussed as follows:

Cost analysis: In economics literature, Cost analysis is done to study the relationship

between input cost to output ratio. ABC Ltd cost analysts study the interrelationship between the

factor input costs incurred on the production and the relative output derived from such analysis.

It is mainly done to identify whether costs incurred are resulting in profitability of the production

or whether they are burdening the cost structure? It is defined as the calculation of money value

of inputs (Wickramasinghe and Alawattage2012). This analysis helps ABC Ltd. in identifying

the optimum level of production where the firm can reach and identify possible bundles of cost

reduction and profit maximisation which increases the overall organisational performance graph.

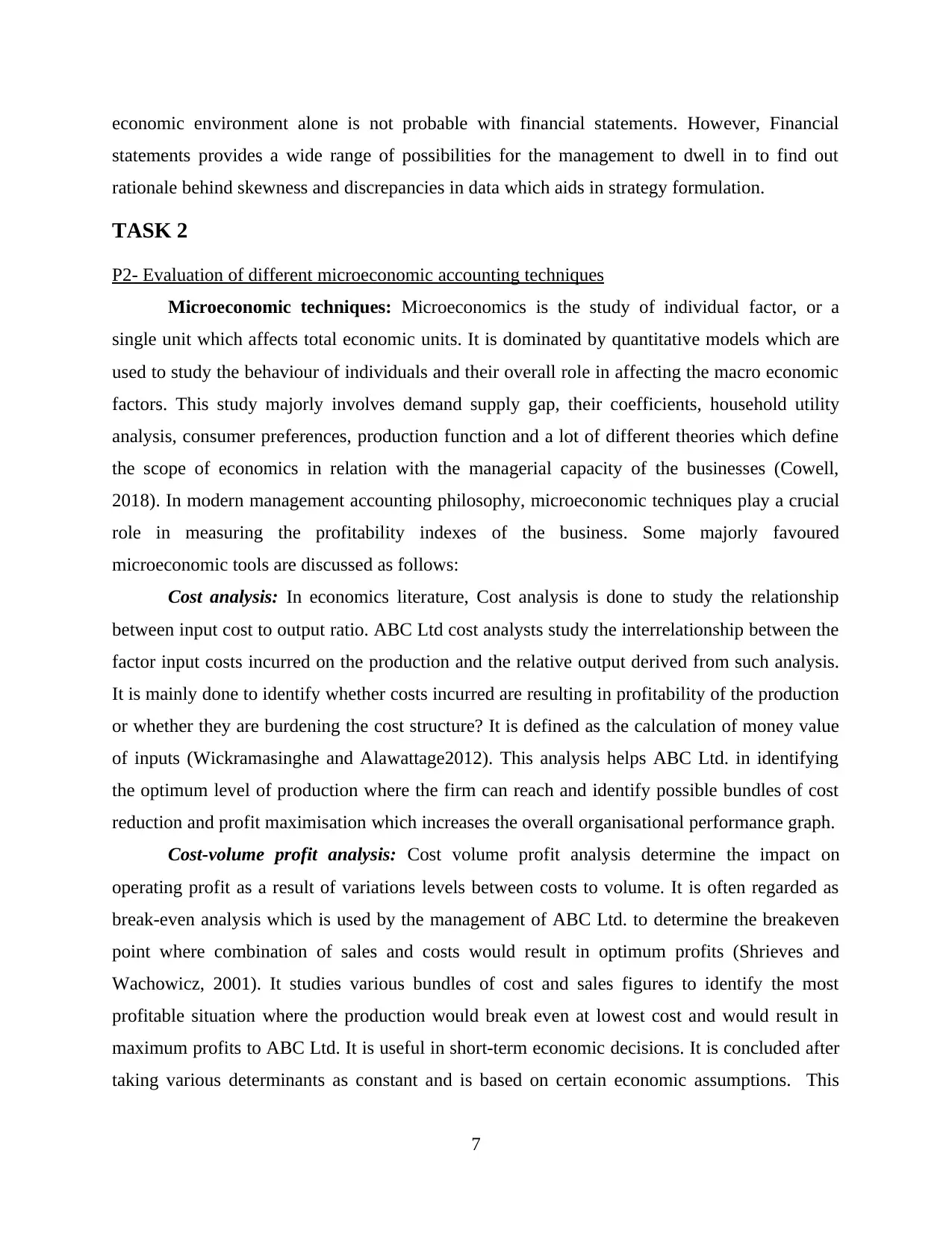

Cost-volume profit analysis: Cost volume profit analysis determine the impact on

operating profit as a result of variations levels between costs to volume. It is often regarded as

break-even analysis which is used by the management of ABC Ltd. to determine the breakeven

point where combination of sales and costs would result in optimum profits (Shrieves and

Wachowicz, 2001). It studies various bundles of cost and sales figures to identify the most

profitable situation where the production would break even at lowest cost and would result in

maximum profits to ABC Ltd. It is useful in short-term economic decisions. It is concluded after

taking various determinants as constant and is based on certain economic assumptions. This

7

statements provides a wide range of possibilities for the management to dwell in to find out

rationale behind skewness and discrepancies in data which aids in strategy formulation.

TASK 2

P2- Evaluation of different microeconomic accounting techniques

Microeconomic techniques: Microeconomics is the study of individual factor, or a

single unit which affects total economic units. It is dominated by quantitative models which are

used to study the behaviour of individuals and their overall role in affecting the macro economic

factors. This study majorly involves demand supply gap, their coefficients, household utility

analysis, consumer preferences, production function and a lot of different theories which define

the scope of economics in relation with the managerial capacity of the businesses (Cowell,

2018). In modern management accounting philosophy, microeconomic techniques play a crucial

role in measuring the profitability indexes of the business. Some majorly favoured

microeconomic tools are discussed as follows:

Cost analysis: In economics literature, Cost analysis is done to study the relationship

between input cost to output ratio. ABC Ltd cost analysts study the interrelationship between the

factor input costs incurred on the production and the relative output derived from such analysis.

It is mainly done to identify whether costs incurred are resulting in profitability of the production

or whether they are burdening the cost structure? It is defined as the calculation of money value

of inputs (Wickramasinghe and Alawattage2012). This analysis helps ABC Ltd. in identifying

the optimum level of production where the firm can reach and identify possible bundles of cost

reduction and profit maximisation which increases the overall organisational performance graph.

Cost-volume profit analysis: Cost volume profit analysis determine the impact on

operating profit as a result of variations levels between costs to volume. It is often regarded as

break-even analysis which is used by the management of ABC Ltd. to determine the breakeven

point where combination of sales and costs would result in optimum profits (Shrieves and

Wachowicz, 2001). It studies various bundles of cost and sales figures to identify the most

profitable situation where the production would break even at lowest cost and would result in

maximum profits to ABC Ltd. It is useful in short-term economic decisions. It is concluded after

taking various determinants as constant and is based on certain economic assumptions. This

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

technique increases organisational performance by helping it in identifying points which

determine profitability for it.

Cost variances: It is the study of deviations between the budgeted cost structure for the

production plan and the actual costs incurred. It can be performed for various factors of

production. Such differences help the management body ABC Ltd. in studying the relationship

between budgeted to actual cost levels. In order to conduct a cost variance analysis, at the

beginning stage of production standard costs needs to be established which provides a scope for

the deviation analysis (Moores and Yuen, 2001). It results into favourable and unfavourable

variances based on the positive and negative skewness. It is used to study the positive flow of

finances as the project progresses and identification of loopholes which daunts the funds of the

business. This technique increases organisational performance for ABC Ltd by helping it analyse

performance standards for its processes and projects.

Absorption & marginal costing: Under absorption costing all costs related to

manufacturing process are subsumed into the process. Or, all the costs related to production

which may be fixed costs or flexible costs are considered as costs despite their actual use

(Williams and Dobelman, 2017). While, in marginal costing method, the additional costs

incurred in producing are charged against the cost units whereas the fixed cost which make a part

of the relevant period are written off against the contribution in full. It is also considered as

incremental cost. It is the one additional unit of cost incurred by the firm as the result of addition

in one more unit consumption of the product by the consumers. These techniques helps ABC

8

determine profitability for it.

Cost variances: It is the study of deviations between the budgeted cost structure for the

production plan and the actual costs incurred. It can be performed for various factors of

production. Such differences help the management body ABC Ltd. in studying the relationship

between budgeted to actual cost levels. In order to conduct a cost variance analysis, at the

beginning stage of production standard costs needs to be established which provides a scope for

the deviation analysis (Moores and Yuen, 2001). It results into favourable and unfavourable

variances based on the positive and negative skewness. It is used to study the positive flow of

finances as the project progresses and identification of loopholes which daunts the funds of the

business. This technique increases organisational performance for ABC Ltd by helping it analyse

performance standards for its processes and projects.

Absorption & marginal costing: Under absorption costing all costs related to

manufacturing process are subsumed into the process. Or, all the costs related to production

which may be fixed costs or flexible costs are considered as costs despite their actual use

(Williams and Dobelman, 2017). While, in marginal costing method, the additional costs

incurred in producing are charged against the cost units whereas the fixed cost which make a part

of the relevant period are written off against the contribution in full. It is also considered as

incremental cost. It is the one additional unit of cost incurred by the firm as the result of addition

in one more unit consumption of the product by the consumers. These techniques helps ABC

8

Ltd. Management in ascertaining cost allocation for production plan and designing cost

allocation techniques for its processes.

Flexible budgeting: It is a budgetary mechanism under which costs are allocated as per

the variation in the production level. It focuses mainly on the variable costs associated with the

production. As the level of production may vary from the current level to a different level the

variable cost per unit will also shift to that level. It is a cost saving mechanism which is highly

regarded in ABC Ltd. where cost control framework is quite important to save extra cost burden

on the business. Flexible budget considers revenues and expenditures incurred in current period

as a baseline so as to identify How revenues and expenditure will change as a result in variation

of such estimation. It increases organisational performance of ABC Ltd. By helping it budget

resources judiciously and save extra costs from getting wasted.

Organisational performance and microeconomic techniques: All the micro economic

techniques discussed above has an influence on organisational development and performance

increasing. Cost-volume profit analysis aids the business in identifying the profit margin portion

after that the fixed costs and variable costs are covered. Variance analysis helps in determining

the variation between two factorial points or costs (Dwivedi, 2016). It aids through cost

reduction hence improves organisational efficiency and effectiveness. Same benefits are

produced by using techniques like flexible budgeting, cost allocation method, various costing

techniques helps a business in developing strategic intent and content for the future endeavours

through planning for multi level production by channelizing processes into elegant systems.

M2- Advantages and disadvantages of accounting techniques

Management accounting education provides a lot of management accounting tools and

techniques which has secured exponential benefits for ABC Ltd. These accounting techniques

has a wide range of value to the management accounting literature and has proved quite

satisfactorily to the organisation as well but they come with some pros and cons which are

discussed here in as:

Marginal costing: It is the deviation in total cost as an outcome of change in one extra

unit production.

Advantages

This method of costing is very easy to comprehend for ABC Ltd's analysts and put to use

as it eliminates the element of fixed costs and their apportionment.

9

allocation techniques for its processes.

Flexible budgeting: It is a budgetary mechanism under which costs are allocated as per

the variation in the production level. It focuses mainly on the variable costs associated with the

production. As the level of production may vary from the current level to a different level the

variable cost per unit will also shift to that level. It is a cost saving mechanism which is highly

regarded in ABC Ltd. where cost control framework is quite important to save extra cost burden

on the business. Flexible budget considers revenues and expenditures incurred in current period

as a baseline so as to identify How revenues and expenditure will change as a result in variation

of such estimation. It increases organisational performance of ABC Ltd. By helping it budget

resources judiciously and save extra costs from getting wasted.

Organisational performance and microeconomic techniques: All the micro economic

techniques discussed above has an influence on organisational development and performance

increasing. Cost-volume profit analysis aids the business in identifying the profit margin portion

after that the fixed costs and variable costs are covered. Variance analysis helps in determining

the variation between two factorial points or costs (Dwivedi, 2016). It aids through cost

reduction hence improves organisational efficiency and effectiveness. Same benefits are

produced by using techniques like flexible budgeting, cost allocation method, various costing

techniques helps a business in developing strategic intent and content for the future endeavours

through planning for multi level production by channelizing processes into elegant systems.

M2- Advantages and disadvantages of accounting techniques

Management accounting education provides a lot of management accounting tools and

techniques which has secured exponential benefits for ABC Ltd. These accounting techniques

has a wide range of value to the management accounting literature and has proved quite

satisfactorily to the organisation as well but they come with some pros and cons which are

discussed here in as:

Marginal costing: It is the deviation in total cost as an outcome of change in one extra

unit production.

Advantages

This method of costing is very easy to comprehend for ABC Ltd's analysts and put to use

as it eliminates the element of fixed costs and their apportionment.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.