Monarch Institute: ADFP Module 4 Advanced Strategy Advice

VerifiedAdded on 2021/04/16

|26

|6791

|52

Homework Assignment

AI Summary

This assignment solution addresses the key concepts of financial planning, particularly focusing on superannuation strategies, estate planning, and the implications of the Transfer Balance Account (TBA). The scenario involves Damien and Maxine, a couple seeking advice on maximizing their superannuation benefits and estate planning in light of changes effective from July 1, 2017. The solution explores how Damien can leverage the TBA rules and existing superannuation balances to optimize their financial position, especially in the event of Maxine's death. The response provides detailed explanations and figures, addressing strategies to keep as much money as possible inside the superannuation environment and take full advantage of pension benefit caps. It covers the creation of a death benefit income stream, consolidating superannuation interests, and utilizing the remaining capacity within the TBA to maximize tax benefits. The solution demonstrates an understanding of the new superannuation policies, including the $1.6 million cap, and provides practical steps for Damien to manage his and Maxine's superannuation accounts effectively.

ADFP Module 4 Advanced Strategy Advice assignment

1707

ADFP Module 4

Advanced Strategy Advice

Submission Instructions:

Key steps that must be followed:

Please complete the Declaration of Authenticity at the

bottom of this page.

Once you have completed all parts of the assessment and saved

it (e.g. to your desktop computer), login to the Monarch

Learning Management System (LMS) to submit your

assessment.

In the LMS, click on the file ”Submit ADFP Module 4 Advanced

Strategy Advice” in the Module 4 section of your course and

upload your assessment file/s by following the prompts.

Please be sure to click “Continue” after clicking

“submit”. This ensures your assessor receives notification –

very important!

Declaration of Understanding and Authenticity *

I have read and understood the assessment instructions provided to me in the Learning

Management System.

I certify that the attached material is my original work. No other person’s work has been

used without due acknowledgement. I understand that the work submitted may be

reproduced and/or communicated for the purpose of detecting plagiarism.

Student Name*: Date: 26/2/18Dan Raja

1707

ADFP Module 4

Advanced Strategy Advice

Submission Instructions:

Key steps that must be followed:

Please complete the Declaration of Authenticity at the

bottom of this page.

Once you have completed all parts of the assessment and saved

it (e.g. to your desktop computer), login to the Monarch

Learning Management System (LMS) to submit your

assessment.

In the LMS, click on the file ”Submit ADFP Module 4 Advanced

Strategy Advice” in the Module 4 section of your course and

upload your assessment file/s by following the prompts.

Please be sure to click “Continue” after clicking

“submit”. This ensures your assessor receives notification –

very important!

Declaration of Understanding and Authenticity *

I have read and understood the assessment instructions provided to me in the Learning

Management System.

I certify that the attached material is my original work. No other person’s work has been

used without due acknowledgement. I understand that the work submitted may be

reproduced and/or communicated for the purpose of detecting plagiarism.

Student Name*: Date: 26/2/18Dan Raja

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADFP Module 4 Advanced Strategy Advice assignment

1707

* I understand that by typing my name or inserting a digital signature into this box that I

agree and am bound by the above student declaration.

1707

* I understand that by typing my name or inserting a digital signature into this box that I

agree and am bound by the above student declaration.

ADFP Module 4 Advanced Strategy Advice assignment

1707

Units: FNSFPL603, FNSFPL606, FNSPRM601

Important assessment information

Aims of this assessment

This assessment activity is conducted to the standard expected in the

workplace in order to demonstrate consistent performance of typical

activities experienced in the financial services industry.

You are expected to have a good working knowledge of superannuation

from having completed your Diploma of Financial Planning, although

superannuation notes are included as part of this module.

This assessment focuses primarily on strategic recommendations in a

financial planning context. It encompasses your knowledge base acquired

across previous modules within the Diploma of Financial Planning and the

Advanced Diploma of Financial Planning.

The assessment brings together the interaction of key financial areas

such as Centrelink, superannuation and estate planning

Marking and feedback

This assignment contains 3 assessment activities each containing specific

instructions.

This particular assessment forms part of your overall assessment for the

following units of competency:

FNSFPL603

FNSFPL606

FNSPRM601

Grading for this assessment will be deemed “competent” or “not-yet-

competent” in line with specified educational standards under the

Australian Qualifications Framework.

What does “competent” mean?

These answers contain relevant and accurate information in response to

the question/s with limited serious errors in fact or application. If incorrect

information is contained in an answer, it must be fundamentally

outweighed by the accurate information provided. This will be assessed

against a marking guide provided to assessors for their determination.

1707

Units: FNSFPL603, FNSFPL606, FNSPRM601

Important assessment information

Aims of this assessment

This assessment activity is conducted to the standard expected in the

workplace in order to demonstrate consistent performance of typical

activities experienced in the financial services industry.

You are expected to have a good working knowledge of superannuation

from having completed your Diploma of Financial Planning, although

superannuation notes are included as part of this module.

This assessment focuses primarily on strategic recommendations in a

financial planning context. It encompasses your knowledge base acquired

across previous modules within the Diploma of Financial Planning and the

Advanced Diploma of Financial Planning.

The assessment brings together the interaction of key financial areas

such as Centrelink, superannuation and estate planning

Marking and feedback

This assignment contains 3 assessment activities each containing specific

instructions.

This particular assessment forms part of your overall assessment for the

following units of competency:

FNSFPL603

FNSFPL606

FNSPRM601

Grading for this assessment will be deemed “competent” or “not-yet-

competent” in line with specified educational standards under the

Australian Qualifications Framework.

What does “competent” mean?

These answers contain relevant and accurate information in response to

the question/s with limited serious errors in fact or application. If incorrect

information is contained in an answer, it must be fundamentally

outweighed by the accurate information provided. This will be assessed

against a marking guide provided to assessors for their determination.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ADFP Module 4 Advanced Strategy Advice assignment

1707

Units: FNSFPL603, FNSFPL606, FNSPRM601

What does “not-yet-competent” mean?

This occurs when an assessment does not meet the marking guide

standards provided to assessors. These answers either do not address

the question specifically, or are wrong from a legislative perspective, or

are incorrectly applied. Answers that omit to provide a response to any

significant issue (where multiple issues must be addressed in a question)

may also be deemed not-yet-competent. Answers that have faulty

reasoning, a poor standard of expression or include plagiarism may also

be deemed not-yet-competent.

Please note, additional information regarding Monarch’s plagiarism policy

is contained in the Student Information Guide which can be found here:

http://www.monarch.edu.au/student-info/

What happens if you are deemed not-yet-competent?

In the event you do not achieve competency by your assessor on this

assessment, you will be given one more opportunity to re-submit the

assessment after consultation with your Trainer/ Assessor. You will know

your assessment is deemed ‘not-yet-competent’ if your grade book in the

Monarch LMS says “NYC” after you have received an email from your

assessor advising your assessment has been graded.

Important: It is your responsibility to ensure your assessment

resubmission addresses all areas deemed unsatisfactory by your

assessor. Please note, if you are still unsuccessful in meeting competency

after resubmitting your assessment, you will be required to repeat those

units.

In the event that you have concerns about the assessment decision then

you can refer to our Complaints & Appeals process also contained within

the Student Information Guide.

Expectations from your assessor when answering different types

of assessment questions

Knowledge based questions:

1707

Units: FNSFPL603, FNSFPL606, FNSPRM601

What does “not-yet-competent” mean?

This occurs when an assessment does not meet the marking guide

standards provided to assessors. These answers either do not address

the question specifically, or are wrong from a legislative perspective, or

are incorrectly applied. Answers that omit to provide a response to any

significant issue (where multiple issues must be addressed in a question)

may also be deemed not-yet-competent. Answers that have faulty

reasoning, a poor standard of expression or include plagiarism may also

be deemed not-yet-competent.

Please note, additional information regarding Monarch’s plagiarism policy

is contained in the Student Information Guide which can be found here:

http://www.monarch.edu.au/student-info/

What happens if you are deemed not-yet-competent?

In the event you do not achieve competency by your assessor on this

assessment, you will be given one more opportunity to re-submit the

assessment after consultation with your Trainer/ Assessor. You will know

your assessment is deemed ‘not-yet-competent’ if your grade book in the

Monarch LMS says “NYC” after you have received an email from your

assessor advising your assessment has been graded.

Important: It is your responsibility to ensure your assessment

resubmission addresses all areas deemed unsatisfactory by your

assessor. Please note, if you are still unsuccessful in meeting competency

after resubmitting your assessment, you will be required to repeat those

units.

In the event that you have concerns about the assessment decision then

you can refer to our Complaints & Appeals process also contained within

the Student Information Guide.

Expectations from your assessor when answering different types

of assessment questions

Knowledge based questions:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADFP Module 4 Advanced Strategy Advice assignment

1707

Units: FNSFPL603, FNSFPL606, FNSPRM601

A knowledge based question requires you to clearly identify and cover

the key subject matter areas raised in the question in full as part of the

response.

Skill based questions:

Where you are asked to write as though you are speaking to a client,

your answers must show your ability to:

understand your client’s concerns/perspective/views

show empathy

display a professional response

explain ideas clearly and simply so your client can understand the

issues

Good luck

Finally, good luck with your learning and assessments and remember

your trainers are here to assist you

1707

Units: FNSFPL603, FNSFPL606, FNSPRM601

A knowledge based question requires you to clearly identify and cover

the key subject matter areas raised in the question in full as part of the

response.

Skill based questions:

Where you are asked to write as though you are speaking to a client,

your answers must show your ability to:

understand your client’s concerns/perspective/views

show empathy

display a professional response

explain ideas clearly and simply so your client can understand the

issues

Good luck

Finally, good luck with your learning and assessments and remember

your trainers are here to assist you

ADFP Module 4 Advanced Strategy Advice assignment

1707

Units: FNSFPL603, FNSFPL606, FNSPRM601

IMPORTANT INFORMATION

Please note: All relevant social security rates and threshold limits have

been provided with the questions so you are not required to look these

up.

You will need to draw upon your previous knowledge gained from the Diploma of

Financial Planning in Superannuation and the Advanced Diploma of Financial

Planning in Social Security.

The relevant Superannuation course notes have also been included in Module 4,

including the updates effective from 1 July 2017.

The Superannuation workbook from the Diploma of Financial Planning is also

included on the LMS for you to revise this topic.

Superannuation and Social Security are two of the biggest areas of knowledge

required in retirement planning.

1707

Units: FNSFPL603, FNSFPL606, FNSPRM601

IMPORTANT INFORMATION

Please note: All relevant social security rates and threshold limits have

been provided with the questions so you are not required to look these

up.

You will need to draw upon your previous knowledge gained from the Diploma of

Financial Planning in Superannuation and the Advanced Diploma of Financial

Planning in Social Security.

The relevant Superannuation course notes have also been included in Module 4,

including the updates effective from 1 July 2017.

The Superannuation workbook from the Diploma of Financial Planning is also

included on the LMS for you to revise this topic.

Superannuation and Social Security are two of the biggest areas of knowledge

required in retirement planning.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ADFP Module 4 Advanced Strategy Advice assignment

1707

Units: FNSFPL603, FNSFPL606, FNSPRM601

Activity instructions to candidates

This is an open book assessment activity.

You are required to read this assessment and answer all 6 questions that

follow.

Please type your answers in the spaces provided.

Please ensure you have read “Important assessment information” at the

front of this assessment

Estimated time for completion of this assessment activity: 2-3 hours

Assessment Activity 1

Knowledge Base: Reversionary & Non-reversionary

Beneficiaries

Strategies: Transfer Balance Account & Centrelink

1707

Units: FNSFPL603, FNSFPL606, FNSPRM601

Activity instructions to candidates

This is an open book assessment activity.

You are required to read this assessment and answer all 6 questions that

follow.

Please type your answers in the spaces provided.

Please ensure you have read “Important assessment information” at the

front of this assessment

Estimated time for completion of this assessment activity: 2-3 hours

Assessment Activity 1

Knowledge Base: Reversionary & Non-reversionary

Beneficiaries

Strategies: Transfer Balance Account & Centrelink

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADFP Module 4 Advanced Strategy Advice assignment

1707

Units: FNSFPL603, FNSFPL606, FNSPRM601

PART A: TRANSFER BALANCE ACCOUNT

Your clients, Damien, age 72 and Maxine, age 70 have made an appointment to see

you to discuss the superannuation changes effective from 1 July 2017. They each

have an existing income stream in the form of an account-based pension which is in

the retirement phase. They are particularly concerned with the new rules around

the Transfer Balance Account being maintained by the ATO. As they, in their words,

'are not getting any younger', they would like you to address strategies around

estate planning and the transfer balance account.

Damien and Maxine have elected each other to receive a reversionary pension in

the event that either one of them dies.

As at 30 June 2017 the balance of their account-based pensions is $1.4 million for

Damien and $950,000 for Maxine.

Damien withdraws a lump sum commutation of $100,000 from his pension account

on 31 July 2017 and Maxine withdraws a lump sum commutation of $50,000 from

her pension account on 1 August 2017 so they can travel around the world in

comfort.

Damien and Maxine also have substantial investments outside the superannuation

environment so it would be beneficial to leave as much money as possible inside

super to take advantage of the generous tax concessions.

Scenario 1:

If Maxine passed away on 20th December 2017, what action could Damien take to

ensure that:

a) as much money as possible remains inside the superannuation

environment, and

b) he takes full advantage of the pension benefit caps

Required:

1707

Units: FNSFPL603, FNSFPL606, FNSPRM601

PART A: TRANSFER BALANCE ACCOUNT

Your clients, Damien, age 72 and Maxine, age 70 have made an appointment to see

you to discuss the superannuation changes effective from 1 July 2017. They each

have an existing income stream in the form of an account-based pension which is in

the retirement phase. They are particularly concerned with the new rules around

the Transfer Balance Account being maintained by the ATO. As they, in their words,

'are not getting any younger', they would like you to address strategies around

estate planning and the transfer balance account.

Damien and Maxine have elected each other to receive a reversionary pension in

the event that either one of them dies.

As at 30 June 2017 the balance of their account-based pensions is $1.4 million for

Damien and $950,000 for Maxine.

Damien withdraws a lump sum commutation of $100,000 from his pension account

on 31 July 2017 and Maxine withdraws a lump sum commutation of $50,000 from

her pension account on 1 August 2017 so they can travel around the world in

comfort.

Damien and Maxine also have substantial investments outside the superannuation

environment so it would be beneficial to leave as much money as possible inside

super to take advantage of the generous tax concessions.

Scenario 1:

If Maxine passed away on 20th December 2017, what action could Damien take to

ensure that:

a) as much money as possible remains inside the superannuation

environment, and

b) he takes full advantage of the pension benefit caps

Required:

ADFP Module 4 Advanced Strategy Advice assignment

1707

Units: FNSFPL603, FNSFPL606, FNSPRM601

1.1 Provide a detailed explanation of the actions that Damien could

take, including figures.

Scenario 2:

(a) The changes that have taken place in the superannuation policies have

been incorporated in order to enhance the flexibility, sustainability and

integrity of the super system in Australia. The changes have been effective

from 1st July 2017 and the changes in accordance to the transfer balance

account has been that there has been a new limitation on the amount of

super one can transfer and in the tax free retirement accounts. The cap that

is given is initially set at $1.6 million. According to the case study, it is seen

that Maxine and Damien have balance in their account based pension with a

value of $1.4 million for Damien and $950,000 for Maxine. In case Maxine

passes away on 20th December 2017, then Damien can transfer the

additional investment income that is outside the superannuation

environment within the superannuation balance as the cap that is

constructed is $1.6 million and in the Maxine’s account a total balance of

$950,000 is available. Therefore, Damien can create a new income stream

which is a death benefit income stream. This can take place when the two

income streams of the couple are rolled over from two different funds to a

new portfolio in order to permit Damien to consolidate their interests of the

superannuation. This is an effective process with the help of which the

additional income that is outside the super can be brought in and tax free

components can be increased according to the new cap that is determined.

The overall death benefit of Maxine is directly rolled in to another account

and the new fund requires to have a death benefit income stream and the

amount is paid out of the super as a lump sum amount. The death benefits

that are rolled out will not lose their tax treatment related to the death

benefit.

(b) Damien can even take advantage of the pension benefit caps as it is stated

that a cap of $1.6 million has been incorporated. The case study shows that

the amount in the super for Damien is $1.4 million and for Maxine is

$950,000. Hence, Damien can take their superannuation value up to $1.6

1707

Units: FNSFPL603, FNSFPL606, FNSPRM601

1.1 Provide a detailed explanation of the actions that Damien could

take, including figures.

Scenario 2:

(a) The changes that have taken place in the superannuation policies have

been incorporated in order to enhance the flexibility, sustainability and

integrity of the super system in Australia. The changes have been effective

from 1st July 2017 and the changes in accordance to the transfer balance

account has been that there has been a new limitation on the amount of

super one can transfer and in the tax free retirement accounts. The cap that

is given is initially set at $1.6 million. According to the case study, it is seen

that Maxine and Damien have balance in their account based pension with a

value of $1.4 million for Damien and $950,000 for Maxine. In case Maxine

passes away on 20th December 2017, then Damien can transfer the

additional investment income that is outside the superannuation

environment within the superannuation balance as the cap that is

constructed is $1.6 million and in the Maxine’s account a total balance of

$950,000 is available. Therefore, Damien can create a new income stream

which is a death benefit income stream. This can take place when the two

income streams of the couple are rolled over from two different funds to a

new portfolio in order to permit Damien to consolidate their interests of the

superannuation. This is an effective process with the help of which the

additional income that is outside the super can be brought in and tax free

components can be increased according to the new cap that is determined.

The overall death benefit of Maxine is directly rolled in to another account

and the new fund requires to have a death benefit income stream and the

amount is paid out of the super as a lump sum amount. The death benefits

that are rolled out will not lose their tax treatment related to the death

benefit.

(b) Damien can even take advantage of the pension benefit caps as it is stated

that a cap of $1.6 million has been incorporated. The case study shows that

the amount in the super for Damien is $1.4 million and for Maxine is

$950,000. Hence, Damien can take their superannuation value up to $1.6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ADFP Module 4 Advanced Strategy Advice assignment

1707

Units: FNSFPL603, FNSFPL606, FNSPRM601

In this scenario, let us assume that there was no reversionary nomination in place

for Damien and Maxine's pensions.

Instead, the trustees of the superannuation fund, due to the powers available to

them under the trust deed, make the decision to pay Maxine's death benefit to

Damien in the form of an income stream.

To be clear, this is classified as a non-reversionary death benefit.

Naturally, Maxine's death benefit would not be paid out on 20th December 2017 as

it can take a while to be processed. Between the date of death and the date of

payment, 5th May 2018, returns of 8% have been credited to Maxine's account, and

returns of 7% have been credited to Damien's account. Therefore, the balance of

Damien's income stream account is $1,391,000, and the balance of Maxine's

income stream account is $972,000.

Under Scenario 2, if Maxine passed away on 20th December 2017, what action

could Damien take to ensure that:

a) as much money as possible remains inside super and

b) he takes full advantage of the pension benefit caps

Required:

1.2 Provide a detailed explanation of the action that Damien could take,

including figures.

(a) In case the super is a non-revisionary death benefit income streams for

Damien and Maxine, and if Maxine passes away on 20th December 2017,

then the money that is existent within the other super accounts and the

other amounts the super provider has looked to pay as a death benefit

income stream. The lump sum amount is paid in the account of Damien

and furthermore Damien can increase their super amount up to the value

of $1.6 million cap in order to successfully make use of the cap and

increase their income.

(b) Damien can even take full advantage of the pension benefit caps by

successfully bringing the money that is received as a death benefit for

Maxine within the account and thereafter utilize the pension benefit caps.

1707

Units: FNSFPL603, FNSFPL606, FNSPRM601

In this scenario, let us assume that there was no reversionary nomination in place

for Damien and Maxine's pensions.

Instead, the trustees of the superannuation fund, due to the powers available to

them under the trust deed, make the decision to pay Maxine's death benefit to

Damien in the form of an income stream.

To be clear, this is classified as a non-reversionary death benefit.

Naturally, Maxine's death benefit would not be paid out on 20th December 2017 as

it can take a while to be processed. Between the date of death and the date of

payment, 5th May 2018, returns of 8% have been credited to Maxine's account, and

returns of 7% have been credited to Damien's account. Therefore, the balance of

Damien's income stream account is $1,391,000, and the balance of Maxine's

income stream account is $972,000.

Under Scenario 2, if Maxine passed away on 20th December 2017, what action

could Damien take to ensure that:

a) as much money as possible remains inside super and

b) he takes full advantage of the pension benefit caps

Required:

1.2 Provide a detailed explanation of the action that Damien could take,

including figures.

(a) In case the super is a non-revisionary death benefit income streams for

Damien and Maxine, and if Maxine passes away on 20th December 2017,

then the money that is existent within the other super accounts and the

other amounts the super provider has looked to pay as a death benefit

income stream. The lump sum amount is paid in the account of Damien

and furthermore Damien can increase their super amount up to the value

of $1.6 million cap in order to successfully make use of the cap and

increase their income.

(b) Damien can even take full advantage of the pension benefit caps by

successfully bringing the money that is received as a death benefit for

Maxine within the account and thereafter utilize the pension benefit caps.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADFP Module 4 Advanced Strategy Advice assignment

1707

Units: FNSFPL603, FNSFPL606, FNSPRM601

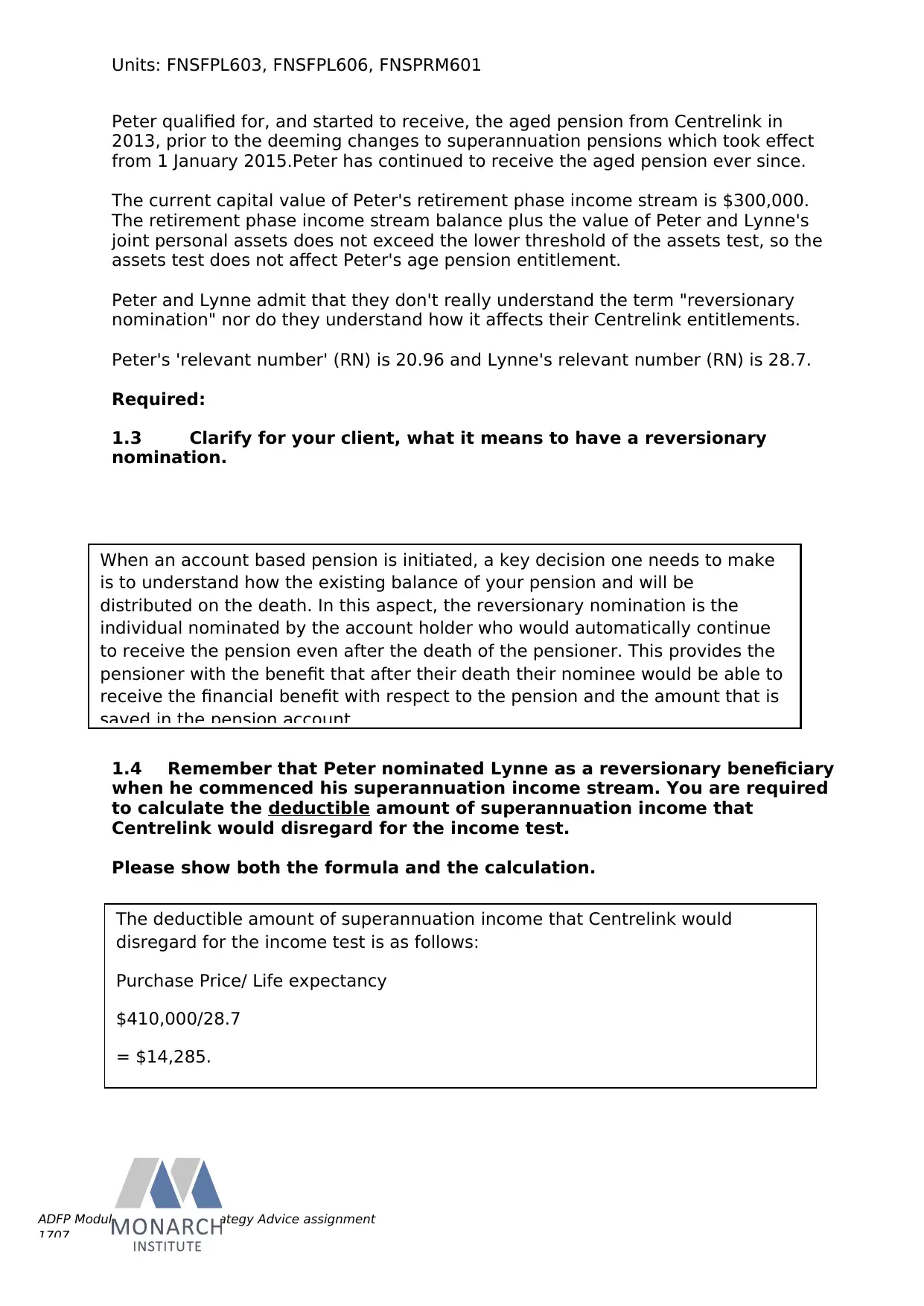

PART B: CENTRELINK

In a financial planning practice it is imperative, whether you are a planner, an

assistant, or an administrator, that you never complete something on a form or

"tick" a box that you do not understand the meaning of.

The following automatic reversion nomination is taken from a form for the BT

Classic Lifetime-Flexible Pension:

Your clients are Peter, age 69 and Lynne, age 64.

Peter retired in 2010 at the age of 62 and used his super balance of $410,000 to

commence a retirement phase income stream. At that time, Lynne was age 57.

When Peter commenced his income stream he nominated Lynne as a reversionary

beneficiary.

1707

Units: FNSFPL603, FNSFPL606, FNSPRM601

PART B: CENTRELINK

In a financial planning practice it is imperative, whether you are a planner, an

assistant, or an administrator, that you never complete something on a form or

"tick" a box that you do not understand the meaning of.

The following automatic reversion nomination is taken from a form for the BT

Classic Lifetime-Flexible Pension:

Your clients are Peter, age 69 and Lynne, age 64.

Peter retired in 2010 at the age of 62 and used his super balance of $410,000 to

commence a retirement phase income stream. At that time, Lynne was age 57.

When Peter commenced his income stream he nominated Lynne as a reversionary

beneficiary.

ADFP Module 4 Advanced Strategy Advice assignment

1707

Units: FNSFPL603, FNSFPL606, FNSPRM601

Peter qualified for, and started to receive, the aged pension from Centrelink in

2013, prior to the deeming changes to superannuation pensions which took effect

from 1 January 2015.Peter has continued to receive the aged pension ever since.

The current capital value of Peter's retirement phase income stream is $300,000.

The retirement phase income stream balance plus the value of Peter and Lynne's

joint personal assets does not exceed the lower threshold of the assets test, so the

assets test does not affect Peter's age pension entitlement.

Peter and Lynne admit that they don't really understand the term "reversionary

nomination" nor do they understand how it affects their Centrelink entitlements.

Peter's 'relevant number' (RN) is 20.96 and Lynne's relevant number (RN) is 28.7.

Required:

1.3 Clarify for your client, what it means to have a reversionary

nomination.

1.4 Remember that Peter nominated Lynne as a reversionary beneficiary

when he commenced his superannuation income stream. You are required

to calculate the deductible amount of superannuation income that

Centrelink would disregard for the income test.

Please show both the formula and the calculation.

When an account based pension is initiated, a key decision one needs to make

is to understand how the existing balance of your pension and will be

distributed on the death. In this aspect, the reversionary nomination is the

individual nominated by the account holder who would automatically continue

to receive the pension even after the death of the pensioner. This provides the

pensioner with the benefit that after their death their nominee would be able to

receive the financial benefit with respect to the pension and the amount that is

saved in the pension account.

The deductible amount of superannuation income that Centrelink would

disregard for the income test is as follows:

Purchase Price/ Life expectancy

$410,000/28.7

= $14,285.

1707

Units: FNSFPL603, FNSFPL606, FNSPRM601

Peter qualified for, and started to receive, the aged pension from Centrelink in

2013, prior to the deeming changes to superannuation pensions which took effect

from 1 January 2015.Peter has continued to receive the aged pension ever since.

The current capital value of Peter's retirement phase income stream is $300,000.

The retirement phase income stream balance plus the value of Peter and Lynne's

joint personal assets does not exceed the lower threshold of the assets test, so the

assets test does not affect Peter's age pension entitlement.

Peter and Lynne admit that they don't really understand the term "reversionary

nomination" nor do they understand how it affects their Centrelink entitlements.

Peter's 'relevant number' (RN) is 20.96 and Lynne's relevant number (RN) is 28.7.

Required:

1.3 Clarify for your client, what it means to have a reversionary

nomination.

1.4 Remember that Peter nominated Lynne as a reversionary beneficiary

when he commenced his superannuation income stream. You are required

to calculate the deductible amount of superannuation income that

Centrelink would disregard for the income test.

Please show both the formula and the calculation.

When an account based pension is initiated, a key decision one needs to make

is to understand how the existing balance of your pension and will be

distributed on the death. In this aspect, the reversionary nomination is the

individual nominated by the account holder who would automatically continue

to receive the pension even after the death of the pensioner. This provides the

pensioner with the benefit that after their death their nominee would be able to

receive the financial benefit with respect to the pension and the amount that is

saved in the pension account.

The deductible amount of superannuation income that Centrelink would

disregard for the income test is as follows:

Purchase Price/ Life expectancy

$410,000/28.7

= $14,285.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.