Advanced Taxation: Tax Policy's Role in Reducing Inequality in Society

VerifiedAdded on 2023/04/11

|13

|2454

|169

Report

AI Summary

This report critically discusses the extent to which tax policy should be used to reduce inequality in society, focusing on the UK's experience since 1970. It begins by outlining normative arguments for addressing income inequality, emphasizing that growing income inequality is not unavoidable and can be addressed through concrete proposals. The report then analyzes the proportion of tax revenue raised by different types of taxes, including direct and indirect taxes, and how these have changed over time. The core of the report examines specific tax policies implemented by the UK government since the 1970s to reduce inequality, including progressive income tax bands, cash benefits, and the impact of indirect taxes. The analysis considers the principles of horizontal and vertical equity in the UK tax system and the effects of these policies on the Gini coefficient. The report concludes by summarizing the effectiveness of these measures and their impact on income distribution.

Running head: ADVANCED TAXATION

Advanced Taxation

Name of the Student

Name of the University

Authors Note

Course ID

Advanced Taxation

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ADVANCED TAXATION

Table of Contents

Introduction:...............................................................................................................................2

Normative arguments:................................................................................................................2

Proportion of tax revenue raised by different types of taxes.....................................................5

Tax policies used by UK government to reduce inequality since 1970:....................................7

Conclusion:..............................................................................................................................10

References:...............................................................................................................................11

Table of Contents

Introduction:...............................................................................................................................2

Normative arguments:................................................................................................................2

Proportion of tax revenue raised by different types of taxes.....................................................5

Tax policies used by UK government to reduce inequality since 1970:....................................7

Conclusion:..............................................................................................................................10

References:...............................................................................................................................11

2ADVANCED TAXATION

Introduction:

With increasing inequality among the rich nations it has now become a matter of

concern because it is social, political and economic outcomes. As argued by Solt (2016)

growing concerns of income inequality is not unavoidable but the same can be overturned

through the concrete proposal. The proposal contains a wide ranging span that can extend

beyond the traditional redistributive tools but also comprises of the substantial rise in the

direct redistribution through the income tax and social transfer schemes and increase in the

minimum wages. The paper aims to address the measures of reducing the income inequality

in the society. Furthermore, detailed suggestions are outlined for the UK government to

reduce the income inequality through appropriate tax policy.

Normative arguments:

The rapid expansion of the rising economies over the past decade has successfully

lifted millions out of the absolute poverty and lower disparities in income all through the

world as whole. Meanwhile, before the global financial crisis of 2008, there were several

economies that were expanding as well (Sturm and De Haan 2015). However, inside the

OECD and the rising economies not all the people have gained equal benefit from the growth

periods. In contrast to this, the income distribution among the people become more uneven.

Predictably, especially following the beginning of crisis, the uneven distribution of

income trends has grown the salience of fairness into the political debate in several nations,

both in respect of the opportunity and consequences for consumption and household earnings.

Very few doubt that fairness is considered vital (Steele 2015). However, the understanding of

what constitutes fair differs and may in parts portray the historical trends for income

distribution, that can increasingly differ among countries. With that being said, over the long

Introduction:

With increasing inequality among the rich nations it has now become a matter of

concern because it is social, political and economic outcomes. As argued by Solt (2016)

growing concerns of income inequality is not unavoidable but the same can be overturned

through the concrete proposal. The proposal contains a wide ranging span that can extend

beyond the traditional redistributive tools but also comprises of the substantial rise in the

direct redistribution through the income tax and social transfer schemes and increase in the

minimum wages. The paper aims to address the measures of reducing the income inequality

in the society. Furthermore, detailed suggestions are outlined for the UK government to

reduce the income inequality through appropriate tax policy.

Normative arguments:

The rapid expansion of the rising economies over the past decade has successfully

lifted millions out of the absolute poverty and lower disparities in income all through the

world as whole. Meanwhile, before the global financial crisis of 2008, there were several

economies that were expanding as well (Sturm and De Haan 2015). However, inside the

OECD and the rising economies not all the people have gained equal benefit from the growth

periods. In contrast to this, the income distribution among the people become more uneven.

Predictably, especially following the beginning of crisis, the uneven distribution of

income trends has grown the salience of fairness into the political debate in several nations,

both in respect of the opportunity and consequences for consumption and household earnings.

Very few doubt that fairness is considered vital (Steele 2015). However, the understanding of

what constitutes fair differs and may in parts portray the historical trends for income

distribution, that can increasingly differ among countries. With that being said, over the long

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ADVANCED TAXATION

period of time large number of income inequality may be considered unwelcoming to growth

and development.

As argued by (Shariff, Wiwad and Aknin (2016) strengthening the social insurance

would help in building and reinforcing the current structures. Nevertheless, social insurance

might have difficulty in dealing with with the broadly conversed new social risks that are

related to lower pay, uncertain irregular employment and family dissolution. It also poses a

major challenge to the insurance model. Increasing the social insurance rates would create an

impact on those that are entitled to benefits, whereas spreading coverage might not result in

immediate impact if the added entitlements should be built up by added contributions.

In the meanwhile, Neumayer and Plümper (2016) argues that paying basic income to

each people irrespective of the earnings and living situation has been encouraged from the

diverse philosophies and the same is presently being debated seriously in numerous nations.

This would create broader impact instead of strengthening the social insurance and may

provide some advantages in relation to new social risks particularly. Wider coverage signifies

that it might be either very costly or less generous while resulting more important structural

transformation. The relative merits of such alternative on work incentives, in comparison to

more dependence on the means testing also plays a central role in debate.

As stated by Alt and Iversen (2017) inequality are usually less noticeable in the

OECD nations than other parts of the world, despite the fact that in recent decades the

distribution of disposable income has turned out to be more uneven. During the mid-1970s,

the Gini coefficient, whereby 0 being the perfectly equivalent stood relatively at 0.28 amid

the working age people on average basis in the OECD nation. However, by the mid-2000s, it

became highly unequal and rose to 0.31.

period of time large number of income inequality may be considered unwelcoming to growth

and development.

As argued by (Shariff, Wiwad and Aknin (2016) strengthening the social insurance

would help in building and reinforcing the current structures. Nevertheless, social insurance

might have difficulty in dealing with with the broadly conversed new social risks that are

related to lower pay, uncertain irregular employment and family dissolution. It also poses a

major challenge to the insurance model. Increasing the social insurance rates would create an

impact on those that are entitled to benefits, whereas spreading coverage might not result in

immediate impact if the added entitlements should be built up by added contributions.

In the meanwhile, Neumayer and Plümper (2016) argues that paying basic income to

each people irrespective of the earnings and living situation has been encouraged from the

diverse philosophies and the same is presently being debated seriously in numerous nations.

This would create broader impact instead of strengthening the social insurance and may

provide some advantages in relation to new social risks particularly. Wider coverage signifies

that it might be either very costly or less generous while resulting more important structural

transformation. The relative merits of such alternative on work incentives, in comparison to

more dependence on the means testing also plays a central role in debate.

As stated by Alt and Iversen (2017) inequality are usually less noticeable in the

OECD nations than other parts of the world, despite the fact that in recent decades the

distribution of disposable income has turned out to be more uneven. During the mid-1970s,

the Gini coefficient, whereby 0 being the perfectly equivalent stood relatively at 0.28 amid

the working age people on average basis in the OECD nation. However, by the mid-2000s, it

became highly unequal and rose to 0.31.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ADVANCED TAXATION

According to the OECD experts and several other tax reformations and economic

growth have placed an emphasis on the need to weigh up the degree to which higher marginal

tax rate on income can act as the disincentive. For instance, making an investment on the

human capital and progressive income tax can be regarded as the main way of reforming the

distributions of income among the people. For several nations potential trade-offs among the

economic expansion agenda and equity are presently critical.

The impact of tax on income delivery should be viewed in context of trade off among

the growth and equity. This signifies gauging into the overall impact of reformation on the

financial regimes as a whole and not simply focusing whether the individual taxes are

regressive or progressive in nature (Trump 2018). The main reason is that allocation of

disposal income is reliant on both the benefits and taxes. For example, increasing the indirect

taxes is usually regressive as the burden of taxes generally falls on the consumption of goods

and services which forms large portion of the budgets of poor people than the richer class

households. However, the overall impact of the financial reformation can be progressive,

provided these impacts are offset by benefits and tax changes.

According to Dabla-Norris et al. (2015) benefits related to income is considered as

more efficient method of raising the disposable income of the households that are poor

instead of adopting the lower VAT rates. As opinion by Sands (2017) VAT is not necessarily

considered bad for redistribution purpose. This is evident in developing nations where there is

a relatively higher dependence on the indirect taxes that might make their system of taxation

more regressive. While consumption taxes namely VAT might be the only method of

financing a strongly progressive spending. There are some nations that have insufficient

administrative capacity for making welfare transfers to the households and that may be

considered as the case for differentiating the structure of VAT rate to impose tax on the

necessities at the lower rate.

According to the OECD experts and several other tax reformations and economic

growth have placed an emphasis on the need to weigh up the degree to which higher marginal

tax rate on income can act as the disincentive. For instance, making an investment on the

human capital and progressive income tax can be regarded as the main way of reforming the

distributions of income among the people. For several nations potential trade-offs among the

economic expansion agenda and equity are presently critical.

The impact of tax on income delivery should be viewed in context of trade off among

the growth and equity. This signifies gauging into the overall impact of reformation on the

financial regimes as a whole and not simply focusing whether the individual taxes are

regressive or progressive in nature (Trump 2018). The main reason is that allocation of

disposal income is reliant on both the benefits and taxes. For example, increasing the indirect

taxes is usually regressive as the burden of taxes generally falls on the consumption of goods

and services which forms large portion of the budgets of poor people than the richer class

households. However, the overall impact of the financial reformation can be progressive,

provided these impacts are offset by benefits and tax changes.

According to Dabla-Norris et al. (2015) benefits related to income is considered as

more efficient method of raising the disposable income of the households that are poor

instead of adopting the lower VAT rates. As opinion by Sands (2017) VAT is not necessarily

considered bad for redistribution purpose. This is evident in developing nations where there is

a relatively higher dependence on the indirect taxes that might make their system of taxation

more regressive. While consumption taxes namely VAT might be the only method of

financing a strongly progressive spending. There are some nations that have insufficient

administrative capacity for making welfare transfers to the households and that may be

considered as the case for differentiating the structure of VAT rate to impose tax on the

necessities at the lower rate.

5ADVANCED TAXATION

Majority of the developed nations have formed a well-developed regime that on

average raises the tax revenue that is equal to 35% of the GDP. The extent of tax revenues

has the capacity of attaining a noteworthy sum of redistribution. However, it is also capable

of restructuring the tax policies that are designed poorly and are detrimental to the economic

performance.

During the 1980s there were number of nations that were concerned of the higher

marginal tax rates that contributed to the slower economic development in several countries

than in 1970s. In addition to this, higher rate of taxes was encouraging the growth of selective

tax reliefs that distorted investment decisions and aggressive tax planning by taking

advantage of loopholes contracted the tax base.

On being faced with the challenges of restoring the sustainable public finance and

growth of output after the 2008 financial crisis, the question originated what tax policies must

be adopted to reduce the income inequalities (Acemoglu et al. 2015). Simply increasing the

marginal rates of personal income tax on high income people would not yield extra revenues

due to the impact on work intensity, tax avoidance and other forms of behavioural responses.

There are number of ways where tax policy reformations can contribute to the social equity.

There is a scope for raising the residential property taxes as it is lightly taxed in several

nations. The reformation and revaluation can make the property taxes fair and less distortive.

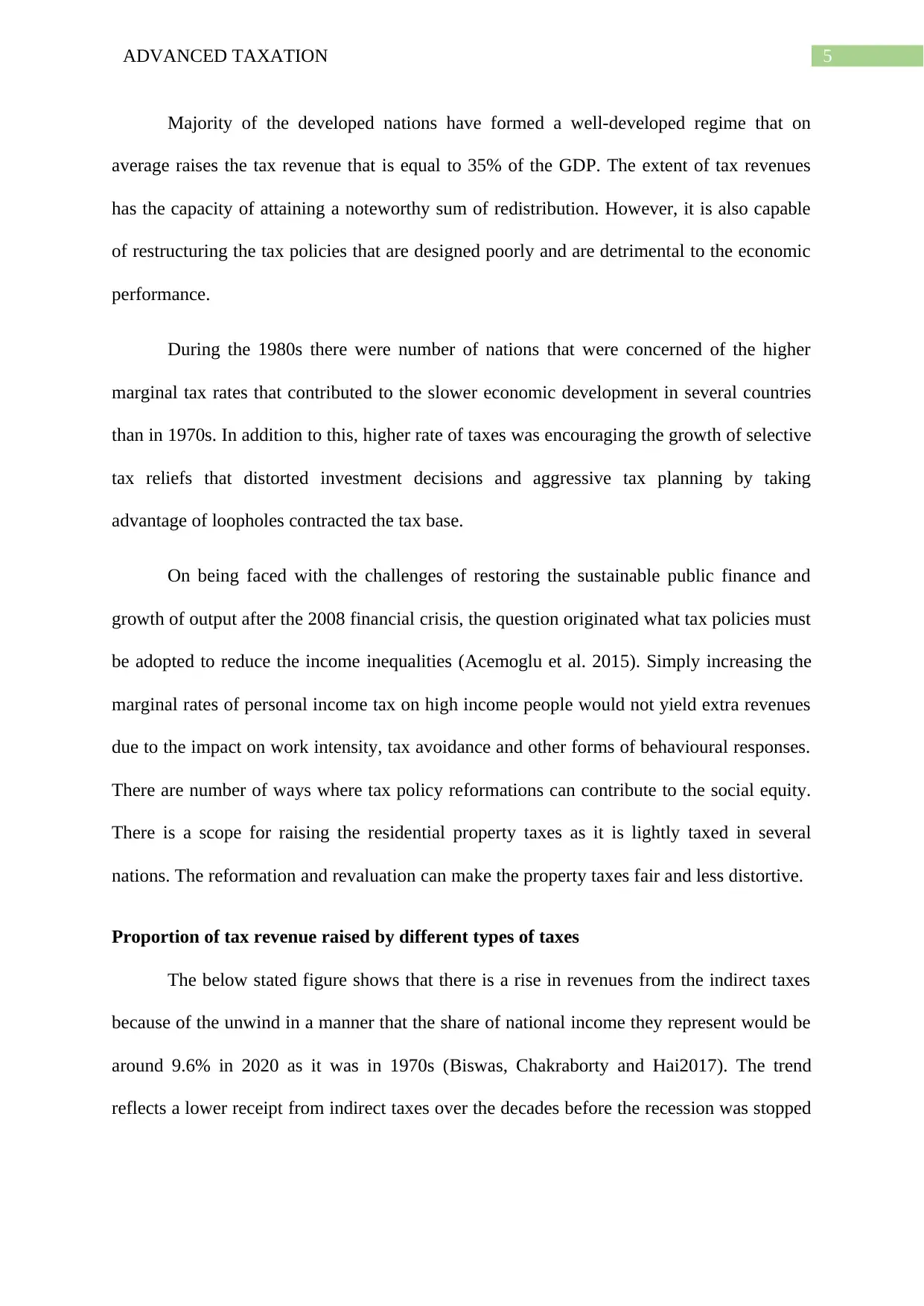

Proportion of tax revenue raised by different types of taxes

The below stated figure shows that there is a rise in revenues from the indirect taxes

because of the unwind in a manner that the share of national income they represent would be

around 9.6% in 2020 as it was in 1970s (Biswas, Chakraborty and Hai2017). The trend

reflects a lower receipt from indirect taxes over the decades before the recession was stopped

Majority of the developed nations have formed a well-developed regime that on

average raises the tax revenue that is equal to 35% of the GDP. The extent of tax revenues

has the capacity of attaining a noteworthy sum of redistribution. However, it is also capable

of restructuring the tax policies that are designed poorly and are detrimental to the economic

performance.

During the 1980s there were number of nations that were concerned of the higher

marginal tax rates that contributed to the slower economic development in several countries

than in 1970s. In addition to this, higher rate of taxes was encouraging the growth of selective

tax reliefs that distorted investment decisions and aggressive tax planning by taking

advantage of loopholes contracted the tax base.

On being faced with the challenges of restoring the sustainable public finance and

growth of output after the 2008 financial crisis, the question originated what tax policies must

be adopted to reduce the income inequalities (Acemoglu et al. 2015). Simply increasing the

marginal rates of personal income tax on high income people would not yield extra revenues

due to the impact on work intensity, tax avoidance and other forms of behavioural responses.

There are number of ways where tax policy reformations can contribute to the social equity.

There is a scope for raising the residential property taxes as it is lightly taxed in several

nations. The reformation and revaluation can make the property taxes fair and less distortive.

Proportion of tax revenue raised by different types of taxes

The below stated figure shows that there is a rise in revenues from the indirect taxes

because of the unwind in a manner that the share of national income they represent would be

around 9.6% in 2020 as it was in 1970s (Biswas, Chakraborty and Hai2017). The trend

reflects a lower receipt from indirect taxes over the decades before the recession was stopped

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ADVANCED TAXATION

by the rise in VAT however it may start again due to the decline in revenues from the other

indirect taxes.

Figure 1: Revenue raised by different types of taxes

Source: (Ifs.org.uk 2019)

by the rise in VAT however it may start again due to the decline in revenues from the other

indirect taxes.

Figure 1: Revenue raised by different types of taxes

Source: (Ifs.org.uk 2019)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ADVANCED TAXATION

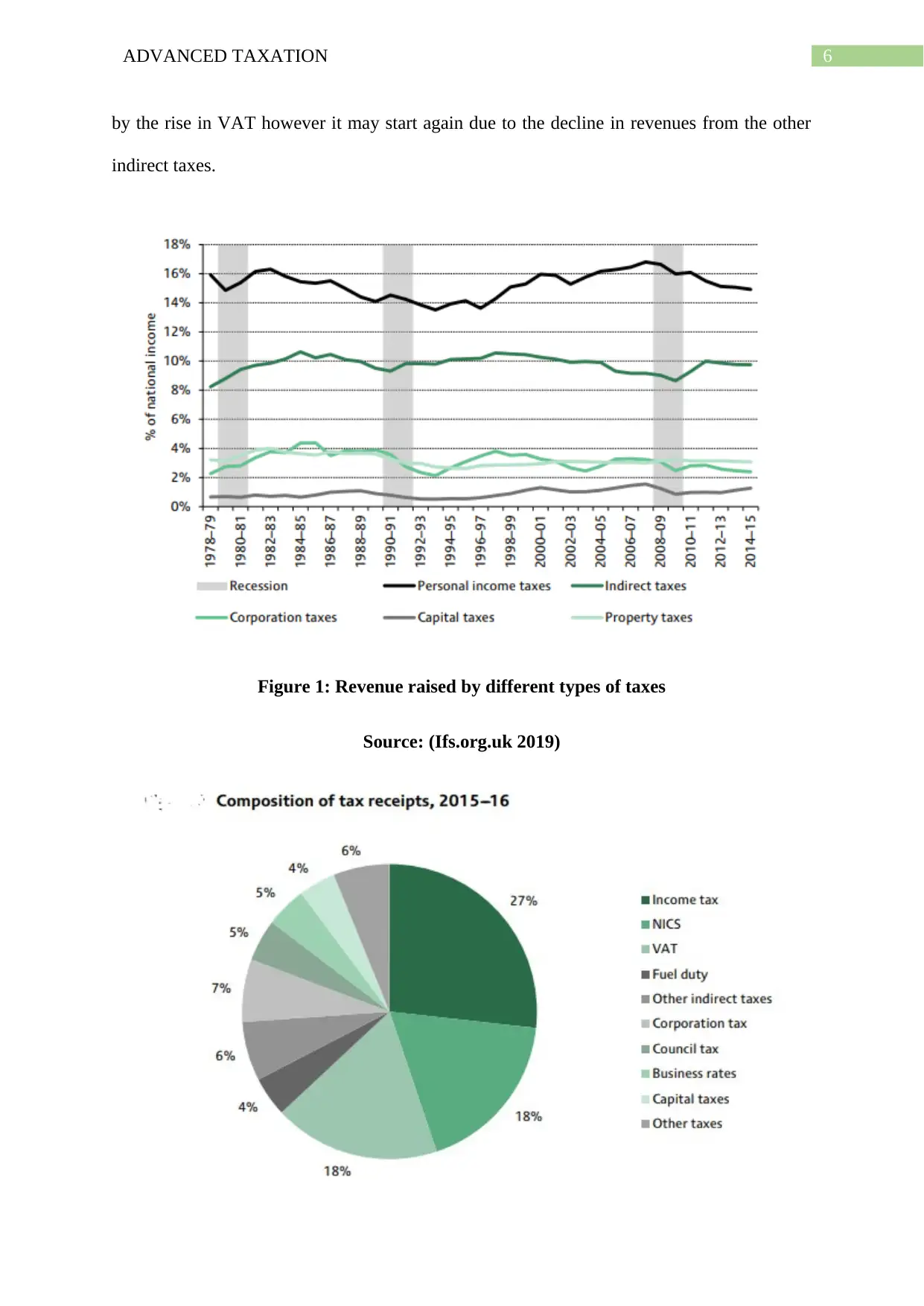

Figure 2: Figure representing composition of tax receipts

Source: (Ifs.org.uk 2019)

Figure 2 represents the breakdown of the UK tax revenues during the year 2015-16.

Presently UK raises approximately 45% of its receipts from the income tax and National

Insurance Contributions while it also raises around 28% from the VAT and other direct taxes.

The government raises revenue around 7% from the corporation tax while the taxes on

property contributes 5%. The rest of the 4% revenues comes to the government from the

smaller set of taxes that are classified as capital taxes.

Tax policies used by UK government to reduce inequality since 1970:

Reducing the poverty and inequality by promoting equity is the most vital macro-

economic objectives of the UK government. The increasing income gap among the rich and

poor has highlighted the need for understanding the reasons that contributed to inequality. As

the measure of reducing income inequality the UK government has adopted the principles of

horizontal and vertical equity (Economicsonline.co.uk 2019). The policies towards the

inequality and poverty is generally influenced by the desire of attaining both the horizontal

and vertical equity.

The tax system of UK like many other countries tries to attain both the horizontal and

vertical equity. Income tax in UK is computed as the percentage of earnings so with the

increase in income the tax also rises. This implies that persons that are earning same income

would be taxed at the same rate and those that are earning more or less would be paying more

or less taxes. The UK government has used the tax system to create a bands of tax that

contains a tax free allowances to ensure that very low income people are not required to pay

taxes and for higher income earnings high upper tax band would be applicable (Hoynes and

Patel 2015). This implies that higher earning individuals would be getting the same tax free

Figure 2: Figure representing composition of tax receipts

Source: (Ifs.org.uk 2019)

Figure 2 represents the breakdown of the UK tax revenues during the year 2015-16.

Presently UK raises approximately 45% of its receipts from the income tax and National

Insurance Contributions while it also raises around 28% from the VAT and other direct taxes.

The government raises revenue around 7% from the corporation tax while the taxes on

property contributes 5%. The rest of the 4% revenues comes to the government from the

smaller set of taxes that are classified as capital taxes.

Tax policies used by UK government to reduce inequality since 1970:

Reducing the poverty and inequality by promoting equity is the most vital macro-

economic objectives of the UK government. The increasing income gap among the rich and

poor has highlighted the need for understanding the reasons that contributed to inequality. As

the measure of reducing income inequality the UK government has adopted the principles of

horizontal and vertical equity (Economicsonline.co.uk 2019). The policies towards the

inequality and poverty is generally influenced by the desire of attaining both the horizontal

and vertical equity.

The tax system of UK like many other countries tries to attain both the horizontal and

vertical equity. Income tax in UK is computed as the percentage of earnings so with the

increase in income the tax also rises. This implies that persons that are earning same income

would be taxed at the same rate and those that are earning more or less would be paying more

or less taxes. The UK government has used the tax system to create a bands of tax that

contains a tax free allowances to ensure that very low income people are not required to pay

taxes and for higher income earnings high upper tax band would be applicable (Hoynes and

Patel 2015). This implies that higher earning individuals would be getting the same tax free

8ADVANCED TAXATION

allowance to those of low paid and would be paying taxes at the similar rate as others pay

over the different bands of income.

The government of UK have used the progressive tax which proportionately takes

more amount of tax from those that earning higher income and redistributing the benefits of

welfare among the lower incomes. The income tax in UK is mildly considered progressive as

it helps in redistributing the income (Saez 2017). This is due to the persons on lower income

pays no tax on income. The UK government in 2014 made the tax free personal allowance to

£10,000. Any amount beyond this would result the income earners to pay taxes at the basic

rate which is presently 20%. Those falling on the higher income are required to pay taxes on

income at a higher tax rate of 40%. A higher tax rate of 45% is implemented on those that

have the earnings of more than £150,000 of assessable income. Such type of tax bands assists

in reducing the gap in income and simultaneously help in reducing inequality.

The UK government policy of cash benefits has played a vital role in lowering the

inequality of income. All through the late 1970s and early 1980s the effect of cash benefits on

lowering the inequality have increased as cash benefits has resulted in 16.9% reduction in the

Gini Coefficient.

allowance to those of low paid and would be paying taxes at the similar rate as others pay

over the different bands of income.

The government of UK have used the progressive tax which proportionately takes

more amount of tax from those that earning higher income and redistributing the benefits of

welfare among the lower incomes. The income tax in UK is mildly considered progressive as

it helps in redistributing the income (Saez 2017). This is due to the persons on lower income

pays no tax on income. The UK government in 2014 made the tax free personal allowance to

£10,000. Any amount beyond this would result the income earners to pay taxes at the basic

rate which is presently 20%. Those falling on the higher income are required to pay taxes on

income at a higher tax rate of 40%. A higher tax rate of 45% is implemented on those that

have the earnings of more than £150,000 of assessable income. Such type of tax bands assists

in reducing the gap in income and simultaneously help in reducing inequality.

The UK government policy of cash benefits has played a vital role in lowering the

inequality of income. All through the late 1970s and early 1980s the effect of cash benefits on

lowering the inequality have increased as cash benefits has resulted in 16.9% reduction in the

Gini Coefficient.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ADVANCED TAXATION

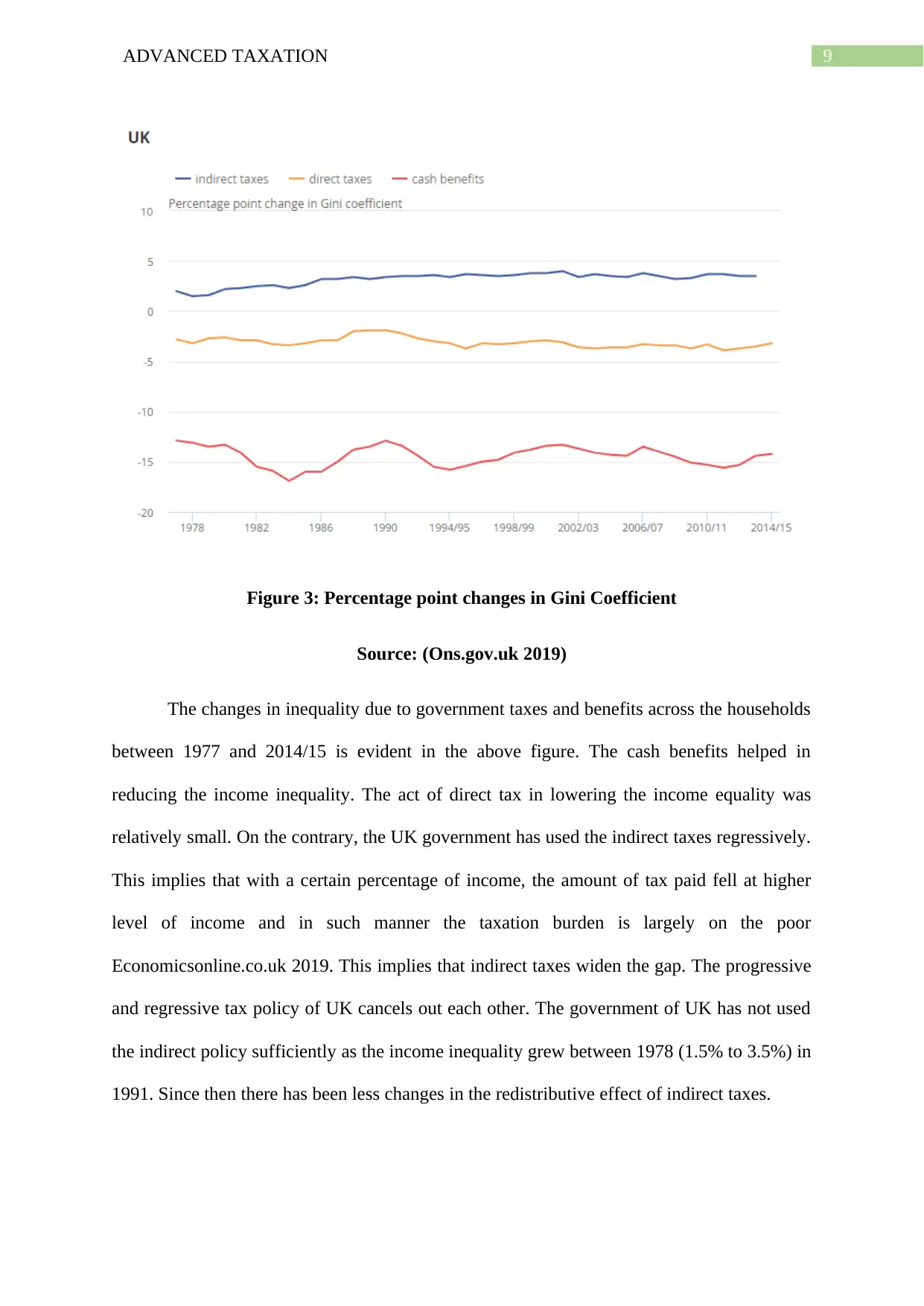

Figure 3: Percentage point changes in Gini Coefficient

Source: (Ons.gov.uk 2019)

The changes in inequality due to government taxes and benefits across the households

between 1977 and 2014/15 is evident in the above figure. The cash benefits helped in

reducing the income inequality. The act of direct tax in lowering the income equality was

relatively small. On the contrary, the UK government has used the indirect taxes regressively.

This implies that with a certain percentage of income, the amount of tax paid fell at higher

level of income and in such manner the taxation burden is largely on the poor

Economicsonline.co.uk 2019. This implies that indirect taxes widen the gap. The progressive

and regressive tax policy of UK cancels out each other. The government of UK has not used

the indirect policy sufficiently as the income inequality grew between 1978 (1.5% to 3.5%) in

1991. Since then there has been less changes in the redistributive effect of indirect taxes.

Figure 3: Percentage point changes in Gini Coefficient

Source: (Ons.gov.uk 2019)

The changes in inequality due to government taxes and benefits across the households

between 1977 and 2014/15 is evident in the above figure. The cash benefits helped in

reducing the income inequality. The act of direct tax in lowering the income equality was

relatively small. On the contrary, the UK government has used the indirect taxes regressively.

This implies that with a certain percentage of income, the amount of tax paid fell at higher

level of income and in such manner the taxation burden is largely on the poor

Economicsonline.co.uk 2019. This implies that indirect taxes widen the gap. The progressive

and regressive tax policy of UK cancels out each other. The government of UK has not used

the indirect policy sufficiently as the income inequality grew between 1978 (1.5% to 3.5%) in

1991. Since then there has been less changes in the redistributive effect of indirect taxes.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ADVANCED TAXATION

Conclusion:

On a conclusive note, the taxes and benefits have evidently compensated towards the

failure of the labour market to offer adequate source income for all the peoples. The source of

concern is the degree of UK government policy changes that are made in the ad hoc fashion

with inadequate attention paid towards tax design. There is a lack of apparent and

communication strategy and the same is increasingly reflected in the UK complex system of

taxation.

Conclusion:

On a conclusive note, the taxes and benefits have evidently compensated towards the

failure of the labour market to offer adequate source income for all the peoples. The source of

concern is the degree of UK government policy changes that are made in the ad hoc fashion

with inadequate attention paid towards tax design. There is a lack of apparent and

communication strategy and the same is increasingly reflected in the UK complex system of

taxation.

11ADVANCED TAXATION

References:

Acemoglu, D., Naidu, S., Restrepo, P. and Robinson, J.A., 2015. Democracy, redistribution,

and inequality. In Handbook of income distribution (Vol. 2, pp. 1885-1966). Elsevier.

Alt, J. and Iversen, T., 2017. Inequality, labor market segmentation, and preferences for

redistribution. American Journal of Political Science, 61(1), pp.21-36.

Biswas, S., Chakraborty, I. and Hai, R., 2017. Income inequality, tax policy, and economic

growth. The Economic Journal, 127(601), pp.688-727.

Dabla-Norris, M.E., Kochhar, M.K., Suphaphiphat, M.N., Ricka, M.F. and Tsounta, E.,

2015. Causes and consequences of income inequality: A global perspective. International

Monetary Fund.

Economicsonline.co.uk. (2019). Policies to reduce inequality | Economics Online. [online]

Available at:

https://www.economicsonline.co.uk/Managing_the_economy/Policies_to_reduce_inequality_

and_poverty.html [Accessed 23 Mar. 2019].

Hoynes, H.W. and Patel, A.J., 2015. Effective policy for reducing inequality? The earned

income tax credit and the distribution of income (No. w21340). National Bureau of Economic

Research.

Ifs.org.uk. (2019). www.ifs.org.uk. [online] Available at:

https://www.ifs.org.uk/uploads/publications/bns/BN_182.pdf [Accessed 23 Mar. 2019].

Neumayer, E. and Plümper, T., 2016. Inequalities of income and inequalities of longevity: A

cross-country study. American journal of public health, 106(1), pp.160-165.

Ons.gov.uk. (2019). Home - Office for National Statistics. [online] Available at:

https://www.ons.gov.uk/ [Accessed 23 Mar. 2019].

References:

Acemoglu, D., Naidu, S., Restrepo, P. and Robinson, J.A., 2015. Democracy, redistribution,

and inequality. In Handbook of income distribution (Vol. 2, pp. 1885-1966). Elsevier.

Alt, J. and Iversen, T., 2017. Inequality, labor market segmentation, and preferences for

redistribution. American Journal of Political Science, 61(1), pp.21-36.

Biswas, S., Chakraborty, I. and Hai, R., 2017. Income inequality, tax policy, and economic

growth. The Economic Journal, 127(601), pp.688-727.

Dabla-Norris, M.E., Kochhar, M.K., Suphaphiphat, M.N., Ricka, M.F. and Tsounta, E.,

2015. Causes and consequences of income inequality: A global perspective. International

Monetary Fund.

Economicsonline.co.uk. (2019). Policies to reduce inequality | Economics Online. [online]

Available at:

https://www.economicsonline.co.uk/Managing_the_economy/Policies_to_reduce_inequality_

and_poverty.html [Accessed 23 Mar. 2019].

Hoynes, H.W. and Patel, A.J., 2015. Effective policy for reducing inequality? The earned

income tax credit and the distribution of income (No. w21340). National Bureau of Economic

Research.

Ifs.org.uk. (2019). www.ifs.org.uk. [online] Available at:

https://www.ifs.org.uk/uploads/publications/bns/BN_182.pdf [Accessed 23 Mar. 2019].

Neumayer, E. and Plümper, T., 2016. Inequalities of income and inequalities of longevity: A

cross-country study. American journal of public health, 106(1), pp.160-165.

Ons.gov.uk. (2019). Home - Office for National Statistics. [online] Available at:

https://www.ons.gov.uk/ [Accessed 23 Mar. 2019].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.