Analysis of Advanced Taxation in the UK: A Comprehensive Report

VerifiedAdded on 2021/01/22

|10

|2330

|97

Report

AI Summary

This report provides a detailed analysis of the advanced taxation system in the United Kingdom. It begins by examining the current practices of the UK tax system, focusing on how taxes and related charges are used to influence corporate behavior, with specific examples like the 'sugar tax' and 'sin tax'. The report then evaluates the increasing use of hypothecation in organizing government revenue and expenditure, including the impact of previous government policies. A critical evaluation of the extent to which the current UK system fulfills desirable tax characteristics, such as fairness, transparency, and economic growth, is also provided. The analysis covers various aspects, including corporation tax, personal allowances, and the impact of these policies on revenue collection and public behavior. The report concludes by summarizing the strengths and weaknesses of the UK's taxation system, highlighting its effectiveness in achieving policy goals and maintaining a trustworthy system.

Advanced Taxation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1. Current practice of UK tax system as to influence the behaviour of recent focus of UK

government and evaluation of taxes and related charges as ways of influencing the behaviour.

.....................................................................................................................................................1

2. Increasing hypothecation as a better way to organise government's revenue and expenditure

system and policies of previous government along with their impact on taxes..........................2

3. Critical evaluation of the extent at which the current UK system fulfils the desirable tax

characteristics..............................................................................................................................4

CONCLUSION................................................................................................................................4

REFERENCES................................................................................................................................6

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1. Current practice of UK tax system as to influence the behaviour of recent focus of UK

government and evaluation of taxes and related charges as ways of influencing the behaviour.

.....................................................................................................................................................1

2. Increasing hypothecation as a better way to organise government's revenue and expenditure

system and policies of previous government along with their impact on taxes..........................2

3. Critical evaluation of the extent at which the current UK system fulfils the desirable tax

characteristics..............................................................................................................................4

CONCLUSION................................................................................................................................4

REFERENCES................................................................................................................................6

INTRODUCTION

Advanced taxation refers to payment of part of tax in advance. It is a kind of income tax

which is payable to the Government in case the tax liability of the assesses exceeds a certain

limit set by the tax department of the government (Jones, 2016). In the present study, current tax

practice in UK for influencing the behaviour of recent focus of the government along with some

popular way to influence the behaviour is being discussed. It includes an evaluation of

increasing hypothecation in the tax for betterment of government's revenue and expenditure

system. Further, the study also shows a critical evaluation of extent of the UK tax system to fulfil

the characteristics of desirable tax system.

MAIN BODY

1. Current practice of UK tax system as to influence the behaviour of recent focus of UK

government and evaluation of taxes and related charges as ways of influencing the

behaviour.

The corporation tax of UK is applicable on all incorporated companies. Currently,

Government of UK is focusing on maintaining healthiness within all over the country.

Government has tried influence the behaviour of corporations by imposing charges and taxes on

them (Veerman and et.al., 2016). Therefore, Government imposed 'sugar tax' on sweetened

drinks with an objective to reduce the sugar content in the drinks.

UK believes in working indirectly. In this regard it has set different rates for the

corporations based on the amount of sugar added by them in their drinks. It has imposed extra

charges on different amount of added sugar containing drinks as under:

Added sugar Charges

8 gram per 100ml 24p per litre

5-8 gram per 100 ml 18p per litre

The imposing of 'Sugar tax' helped the Government in reducing the added sugar by 40%.

Government evaluated that imposition of tax results in increasing the sugar added products by

10% as a result of which the consumption of these products reduced upto 7%. in this order,

various health diseases such as, diabetes has been controlled by the government.

1

Advanced taxation refers to payment of part of tax in advance. It is a kind of income tax

which is payable to the Government in case the tax liability of the assesses exceeds a certain

limit set by the tax department of the government (Jones, 2016). In the present study, current tax

practice in UK for influencing the behaviour of recent focus of the government along with some

popular way to influence the behaviour is being discussed. It includes an evaluation of

increasing hypothecation in the tax for betterment of government's revenue and expenditure

system. Further, the study also shows a critical evaluation of extent of the UK tax system to fulfil

the characteristics of desirable tax system.

MAIN BODY

1. Current practice of UK tax system as to influence the behaviour of recent focus of UK

government and evaluation of taxes and related charges as ways of influencing the

behaviour.

The corporation tax of UK is applicable on all incorporated companies. Currently,

Government of UK is focusing on maintaining healthiness within all over the country.

Government has tried influence the behaviour of corporations by imposing charges and taxes on

them (Veerman and et.al., 2016). Therefore, Government imposed 'sugar tax' on sweetened

drinks with an objective to reduce the sugar content in the drinks.

UK believes in working indirectly. In this regard it has set different rates for the

corporations based on the amount of sugar added by them in their drinks. It has imposed extra

charges on different amount of added sugar containing drinks as under:

Added sugar Charges

8 gram per 100ml 24p per litre

5-8 gram per 100 ml 18p per litre

The imposing of 'Sugar tax' helped the Government in reducing the added sugar by 40%.

Government evaluated that imposition of tax results in increasing the sugar added products by

10% as a result of which the consumption of these products reduced upto 7%. in this order,

various health diseases such as, diabetes has been controlled by the government.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

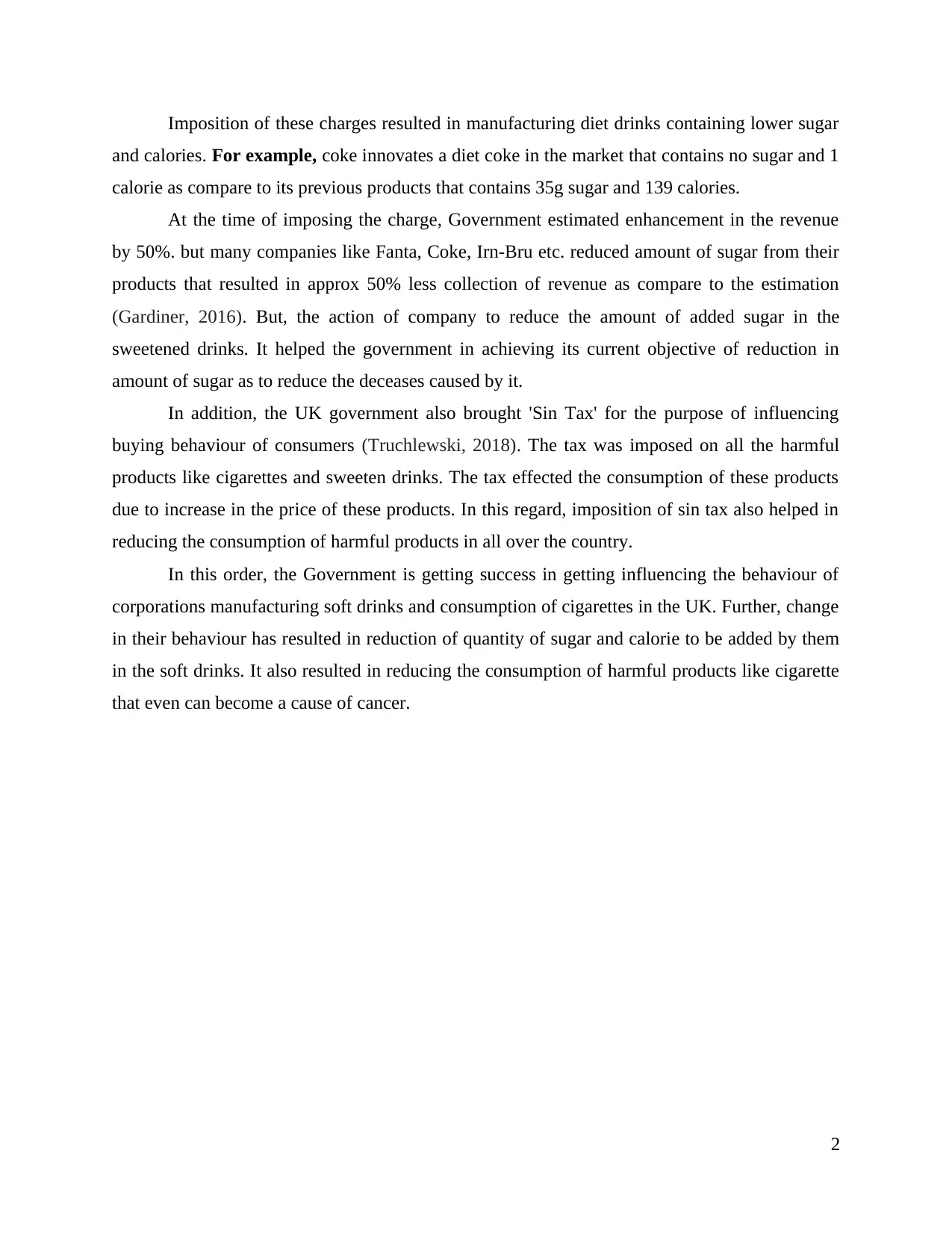

Imposition of these charges resulted in manufacturing diet drinks containing lower sugar

and calories. For example, coke innovates a diet coke in the market that contains no sugar and 1

calorie as compare to its previous products that contains 35g sugar and 139 calories.

At the time of imposing the charge, Government estimated enhancement in the revenue

by 50%. but many companies like Fanta, Coke, Irn-Bru etc. reduced amount of sugar from their

products that resulted in approx 50% less collection of revenue as compare to the estimation

(Gardiner, 2016). But, the action of company to reduce the amount of added sugar in the

sweetened drinks. It helped the government in achieving its current objective of reduction in

amount of sugar as to reduce the deceases caused by it.

In addition, the UK government also brought 'Sin Tax' for the purpose of influencing

buying behaviour of consumers (Truchlewski, 2018). The tax was imposed on all the harmful

products like cigarettes and sweeten drinks. The tax effected the consumption of these products

due to increase in the price of these products. In this regard, imposition of sin tax also helped in

reducing the consumption of harmful products in all over the country.

In this order, the Government is getting success in getting influencing the behaviour of

corporations manufacturing soft drinks and consumption of cigarettes in the UK. Further, change

in their behaviour has resulted in reduction of quantity of sugar and calorie to be added by them

in the soft drinks. It also resulted in reducing the consumption of harmful products like cigarette

that even can become a cause of cancer.

2

and calories. For example, coke innovates a diet coke in the market that contains no sugar and 1

calorie as compare to its previous products that contains 35g sugar and 139 calories.

At the time of imposing the charge, Government estimated enhancement in the revenue

by 50%. but many companies like Fanta, Coke, Irn-Bru etc. reduced amount of sugar from their

products that resulted in approx 50% less collection of revenue as compare to the estimation

(Gardiner, 2016). But, the action of company to reduce the amount of added sugar in the

sweetened drinks. It helped the government in achieving its current objective of reduction in

amount of sugar as to reduce the deceases caused by it.

In addition, the UK government also brought 'Sin Tax' for the purpose of influencing

buying behaviour of consumers (Truchlewski, 2018). The tax was imposed on all the harmful

products like cigarettes and sweeten drinks. The tax effected the consumption of these products

due to increase in the price of these products. In this regard, imposition of sin tax also helped in

reducing the consumption of harmful products in all over the country.

In this order, the Government is getting success in getting influencing the behaviour of

corporations manufacturing soft drinks and consumption of cigarettes in the UK. Further, change

in their behaviour has resulted in reduction of quantity of sugar and calorie to be added by them

in the soft drinks. It also resulted in reducing the consumption of harmful products like cigarette

that even can become a cause of cancer.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3

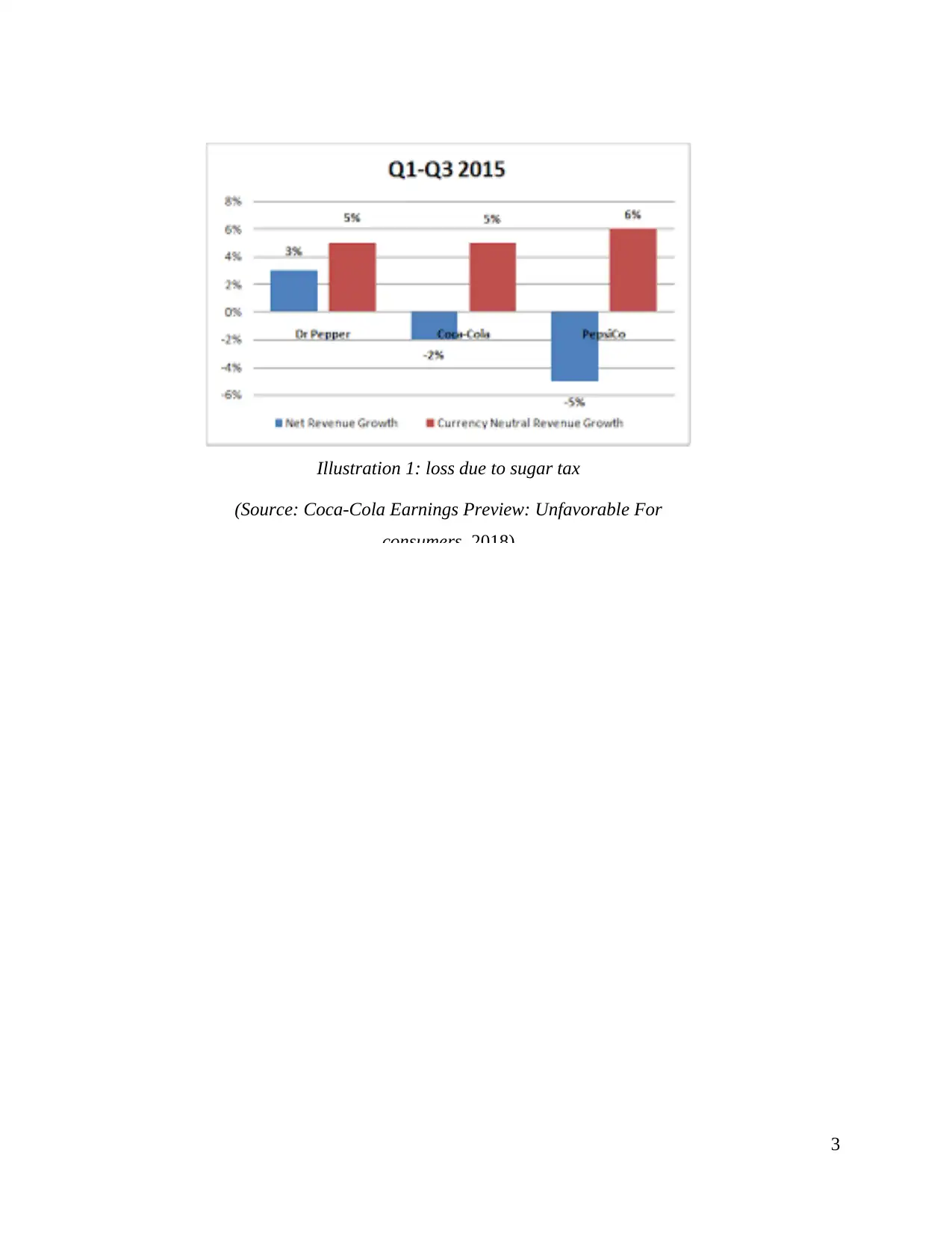

Illustration 1: loss due to sugar tax

(Source: Coca-Cola Earnings Preview: Unfavorable For

consumers. 2018)

Illustration 1: loss due to sugar tax

(Source: Coca-Cola Earnings Preview: Unfavorable For

consumers. 2018)

Government can influences the behaviour of both manufacturer and consumers for

reducing the consumption of harmful products in all over the world. Their behaviour can be

influenced by increasing the value of taxes and charges to be imposed on them. As, the

imposition of taxes and charges enhances the price of products, that directly influences demand

and consumption of products (Timmins, 2018). Further, imposition of taxes also results in

increasing the cost of manufacturer, that makes them to take actions as to reduce the burden of

tax.

On the other hand, this tax has been said as the regressive tax as, due to the sugar tax the

price of soft drinks has risen. It has resulted in the enhancement of inflation rate in the country,

which has directly affected the pocket of consumers.

4

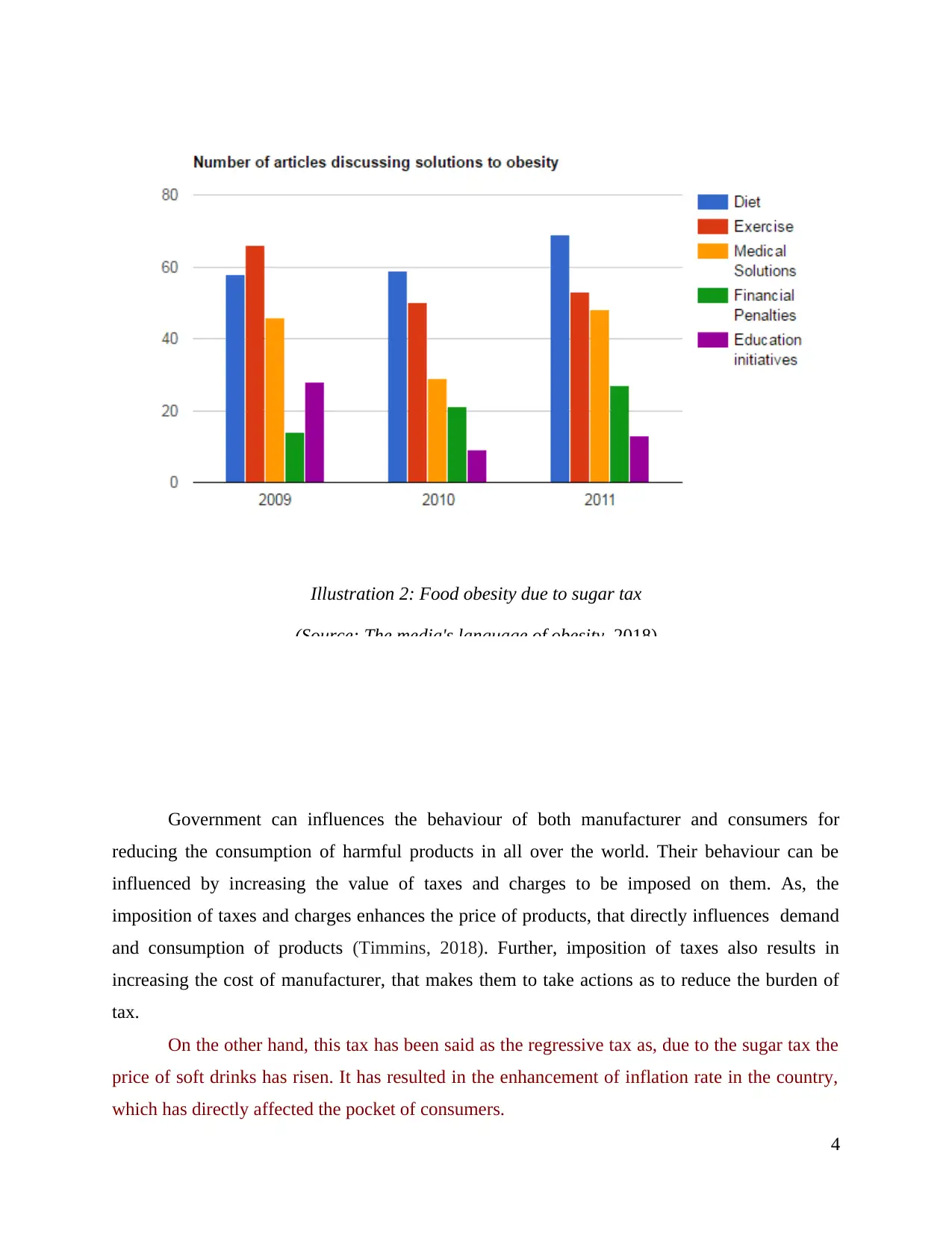

Illustration 2: Food obesity due to sugar tax

(Source: The media's language of obesity, 2018)

reducing the consumption of harmful products in all over the world. Their behaviour can be

influenced by increasing the value of taxes and charges to be imposed on them. As, the

imposition of taxes and charges enhances the price of products, that directly influences demand

and consumption of products (Timmins, 2018). Further, imposition of taxes also results in

increasing the cost of manufacturer, that makes them to take actions as to reduce the burden of

tax.

On the other hand, this tax has been said as the regressive tax as, due to the sugar tax the

price of soft drinks has risen. It has resulted in the enhancement of inflation rate in the country,

which has directly affected the pocket of consumers.

4

Illustration 2: Food obesity due to sugar tax

(Source: The media's language of obesity, 2018)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In this regard, it can be evaluated that currently the main focus of the UK government is

to control the harmful deceases in the country and to maintain healthiness as well.

2. Increasing hypothecation as a better way to organise government's revenue and expenditure

system and policies of previous government along with their impact on taxes

Hypothecation in tax system

Hypothecation of tax refers to reduction the revenues from some taxes as to make a

particular expenditure. In this process, the amount of tax is collected by the Government as to

use it in some specific purpose rather than for numerous purposes (Hypothecation of tax revenue

for health, 2018). This tax system can be termed as an effective system as to organise the

revenue and expenditure of the government as it will decide the use of revenues earned by the

government as to utilise it in proper way.

Tax is a major part of revenues of the Government. Further, the amount of revenue

earned by the government effects the ability of government to make expenditure for the country.

Government of UK applies hypothecation taxes in its tax system. It helps in managing the funds

of taxed in most effective way. In hypothecation system, the government makes a fixed plan for

collection of tax revenues and areas where the specific revenue is going to be used. This tax

system of UK has also helped it in maintaining accountability in the collection of tax and

enhancing the trust of public in the government.

When the government have a set plan to expend the revenues earned by it, the

organisation will automatically become more effective as having a specific plan reduces the

confusion of decide the area of expenditure (Martin and et.al., 2016). Further, This system helps

the government in UK reducing the conflict among the government in expending the collection

of tax.

On the other hand, the sugar tax may also increase the revenue of the Govt. at high level,

as companies may absorb some increase in cost without enhancing that much of price of the

product with the help of implementing strong strategies for the business.

In this regard, it can be analysed that the Hypothecation system of tax helps in effective

organisation of revenues and expenditure of the government in terms of tax funds.

Impact of Government policies on tax system of UK

In April 2018, Government made several changes in their policies, due to which the tax

system of UK also got effected. For example, Government changed amount of personal

5

to control the harmful deceases in the country and to maintain healthiness as well.

2. Increasing hypothecation as a better way to organise government's revenue and expenditure

system and policies of previous government along with their impact on taxes

Hypothecation in tax system

Hypothecation of tax refers to reduction the revenues from some taxes as to make a

particular expenditure. In this process, the amount of tax is collected by the Government as to

use it in some specific purpose rather than for numerous purposes (Hypothecation of tax revenue

for health, 2018). This tax system can be termed as an effective system as to organise the

revenue and expenditure of the government as it will decide the use of revenues earned by the

government as to utilise it in proper way.

Tax is a major part of revenues of the Government. Further, the amount of revenue

earned by the government effects the ability of government to make expenditure for the country.

Government of UK applies hypothecation taxes in its tax system. It helps in managing the funds

of taxed in most effective way. In hypothecation system, the government makes a fixed plan for

collection of tax revenues and areas where the specific revenue is going to be used. This tax

system of UK has also helped it in maintaining accountability in the collection of tax and

enhancing the trust of public in the government.

When the government have a set plan to expend the revenues earned by it, the

organisation will automatically become more effective as having a specific plan reduces the

confusion of decide the area of expenditure (Martin and et.al., 2016). Further, This system helps

the government in UK reducing the conflict among the government in expending the collection

of tax.

On the other hand, the sugar tax may also increase the revenue of the Govt. at high level,

as companies may absorb some increase in cost without enhancing that much of price of the

product with the help of implementing strong strategies for the business.

In this regard, it can be analysed that the Hypothecation system of tax helps in effective

organisation of revenues and expenditure of the government in terms of tax funds.

Impact of Government policies on tax system of UK

In April 2018, Government made several changes in their policies, due to which the tax

system of UK also got effected. For example, Government changed amount of personal

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

allowances to £1,075. person earning a sum less than it need not to pay any tax. It directly

affected the revenue of the government (Fairbrother, 2017). Further, the government made a

policy to enhance the charges and rate of taxes over the sweetened drink manufacturer as to

reduce the consumption of high level of sugar and calories. It also enhanced the tax revenue of

government by 25%.

In addition, charging higher amount tax also resulted in reducing the transparency and

accountability of the UK tax system.

In this regard, the policy of government potentially impacted the overall tax system of

UK.

3. Critical evaluation of the extent at which the current UK system fulfils the desirable tax

characteristics

A most desirable characteristics of an effective tax system is to collect a fair amount of

tax and maintain transparency and simplicity in the overall tax system. Further, the tax system

should be framed in such a way so that it could provide economic growth to the country and have

fiscal adequacy.

In the current tax system of the UK, the Government has tried to maintain the

transparency and effectiveness of organising the collection of tax and its expenditure. Its

collection and expending system of tax funds is easy to understand (Burman and et.al., 2017).

The UK government imposes extra charge over all the harmful articles that helps it in imposing

control over the selling and consumption of these articles. But imposition of too much taxes also

attracts the fraudulent activities for payment of taxes. It also result in reduction of transparency

in the tax payment system of UK.

Further, decision of enhancing the limit of personal allowances resulted in reducing the

burden of public to pay income tax. It may result in enhancement of transparency in the tax

system. In UK, the duty over fuels is charged @ 57.95% per litre. It will help in maintenance of

income of the household and businesses by keeping the less burden of tax over them. It may help

the Government in maintaining the faith of public over the tax system of country.

In this regard, it can be analysed that the current tax system is an effective system that

helps the government in achieving all the characteristics of a desirable tax system (Timmins,

2018). With the help of it the government has enabled to create a simple and trustworthy system

6

affected the revenue of the government (Fairbrother, 2017). Further, the government made a

policy to enhance the charges and rate of taxes over the sweetened drink manufacturer as to

reduce the consumption of high level of sugar and calories. It also enhanced the tax revenue of

government by 25%.

In addition, charging higher amount tax also resulted in reducing the transparency and

accountability of the UK tax system.

In this regard, the policy of government potentially impacted the overall tax system of

UK.

3. Critical evaluation of the extent at which the current UK system fulfils the desirable tax

characteristics

A most desirable characteristics of an effective tax system is to collect a fair amount of

tax and maintain transparency and simplicity in the overall tax system. Further, the tax system

should be framed in such a way so that it could provide economic growth to the country and have

fiscal adequacy.

In the current tax system of the UK, the Government has tried to maintain the

transparency and effectiveness of organising the collection of tax and its expenditure. Its

collection and expending system of tax funds is easy to understand (Burman and et.al., 2017).

The UK government imposes extra charge over all the harmful articles that helps it in imposing

control over the selling and consumption of these articles. But imposition of too much taxes also

attracts the fraudulent activities for payment of taxes. It also result in reduction of transparency

in the tax payment system of UK.

Further, decision of enhancing the limit of personal allowances resulted in reducing the

burden of public to pay income tax. It may result in enhancement of transparency in the tax

system. In UK, the duty over fuels is charged @ 57.95% per litre. It will help in maintenance of

income of the household and businesses by keeping the less burden of tax over them. It may help

the Government in maintaining the faith of public over the tax system of country.

In this regard, it can be analysed that the current tax system is an effective system that

helps the government in achieving all the characteristics of a desirable tax system (Timmins,

2018). With the help of it the government has enabled to create a simple and trustworthy system

6

of the government. On the other hand, the imposition of higher amount of tax may result in

reduction in the transparency in the overall tax system of UK.

CONCLUSION

From the above analysis, it can be concluded that the UK has built a strong taxation

system. It has enabled to reduce the selling and consumption of the harmful products in UK by

imposing charges and taxes on them. It has also included hypothecation system as to make the

revenues and expenditure more effective. Further, the UK has built a strong taxation system that

has helped in achieving the desirable characteristics.

7

reduction in the transparency in the overall tax system of UK.

CONCLUSION

From the above analysis, it can be concluded that the UK has built a strong taxation

system. It has enabled to reduce the selling and consumption of the harmful products in UK by

imposing charges and taxes on them. It has also included hypothecation system as to make the

revenues and expenditure more effective. Further, the UK has built a strong taxation system that

has helped in achieving the desirable characteristics.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Burman, E. and et.al., 2017. Subjects of, or subject to, policy reform? A Foucauldian discourse

analysis of regulation and resistance in UK narratives of educational impacts of welfare

cuts: The case of the ‘bedroom tax’. education policy analysis archives. 25. p.26.

Fairbrother, M., 2017. When will people pay to pollute? Environmental taxes, political trust and

experimental evidence from Britain. British Journal of Political Science, pp.1-22.

Gardiner, A., 2016. Implications of a sugar tax in New Zealand: Incidence and

effectiveness (No. 16/09). New Zealand Treasury.

Jones, C. M., 2016. The UK sugar tax–a healthy start?. British dental journal. 221(2). p.59.

Martin, R. and et.al., 2016. Spatially rebalancing the UK economy: towards a new policy

model?. Regional Studies. 50(2). pp.342-357.

Timmins, N., 2018, October. Securing Funds for the Proposed NHS Multi-year Funding: The

Feasibility of Using a Hypothecated Tax. In Seminar Briefings (No. 002074). Office of

Health Economics.

Truchlewski, Z., 2018. ‘Oh, what a tangled web we weave’ How tax linkages shape

responsiveness in the United Kingdom and France. Party politics, p.1354068818764017.

Veerman, J. L. and et.al., 2016. The impact of a tax on sugar-sweetened beverages on health and

health care costs: a modelling study. PloS one. 11(4). p.e0151460.

Online

Hypothecation of tax revenue for health. 2018. [Online] Available Through:

<https://www.who.int/healthsystems/topics/financing/healthreport/51Hypothecation.pdf

>

The media's language of obesity. 2018. [Online] Available Through:

<http://www.democraticaudit.com/2016/04/05/the-medias-language-of-obesity-may-have-made-

the-sugar-tax-inevitable/>

Coca-Cola Earnings Preview: Unfavorable For consumers. 2018. [Online] Available Through:

<https://www.forbes.com/sites/greatspeculations/2016/02/08/coca-cola-earnings-preview-

unfavorable-foreign-exchange-to-dampen-organic-growth/>

8

Books and Journals

Burman, E. and et.al., 2017. Subjects of, or subject to, policy reform? A Foucauldian discourse

analysis of regulation and resistance in UK narratives of educational impacts of welfare

cuts: The case of the ‘bedroom tax’. education policy analysis archives. 25. p.26.

Fairbrother, M., 2017. When will people pay to pollute? Environmental taxes, political trust and

experimental evidence from Britain. British Journal of Political Science, pp.1-22.

Gardiner, A., 2016. Implications of a sugar tax in New Zealand: Incidence and

effectiveness (No. 16/09). New Zealand Treasury.

Jones, C. M., 2016. The UK sugar tax–a healthy start?. British dental journal. 221(2). p.59.

Martin, R. and et.al., 2016. Spatially rebalancing the UK economy: towards a new policy

model?. Regional Studies. 50(2). pp.342-357.

Timmins, N., 2018, October. Securing Funds for the Proposed NHS Multi-year Funding: The

Feasibility of Using a Hypothecated Tax. In Seminar Briefings (No. 002074). Office of

Health Economics.

Truchlewski, Z., 2018. ‘Oh, what a tangled web we weave’ How tax linkages shape

responsiveness in the United Kingdom and France. Party politics, p.1354068818764017.

Veerman, J. L. and et.al., 2016. The impact of a tax on sugar-sweetened beverages on health and

health care costs: a modelling study. PloS one. 11(4). p.e0151460.

Online

Hypothecation of tax revenue for health. 2018. [Online] Available Through:

<https://www.who.int/healthsystems/topics/financing/healthreport/51Hypothecation.pdf

>

The media's language of obesity. 2018. [Online] Available Through:

<http://www.democraticaudit.com/2016/04/05/the-medias-language-of-obesity-may-have-made-

the-sugar-tax-inevitable/>

Coca-Cola Earnings Preview: Unfavorable For consumers. 2018. [Online] Available Through:

<https://www.forbes.com/sites/greatspeculations/2016/02/08/coca-cola-earnings-preview-

unfavorable-foreign-exchange-to-dampen-organic-growth/>

8

1 out of 10

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.