Analyzing Balanced Scorecard: A Report on Advantages and Critique

VerifiedAdded on 2023/06/11

|7

|1086

|454

Report

AI Summary

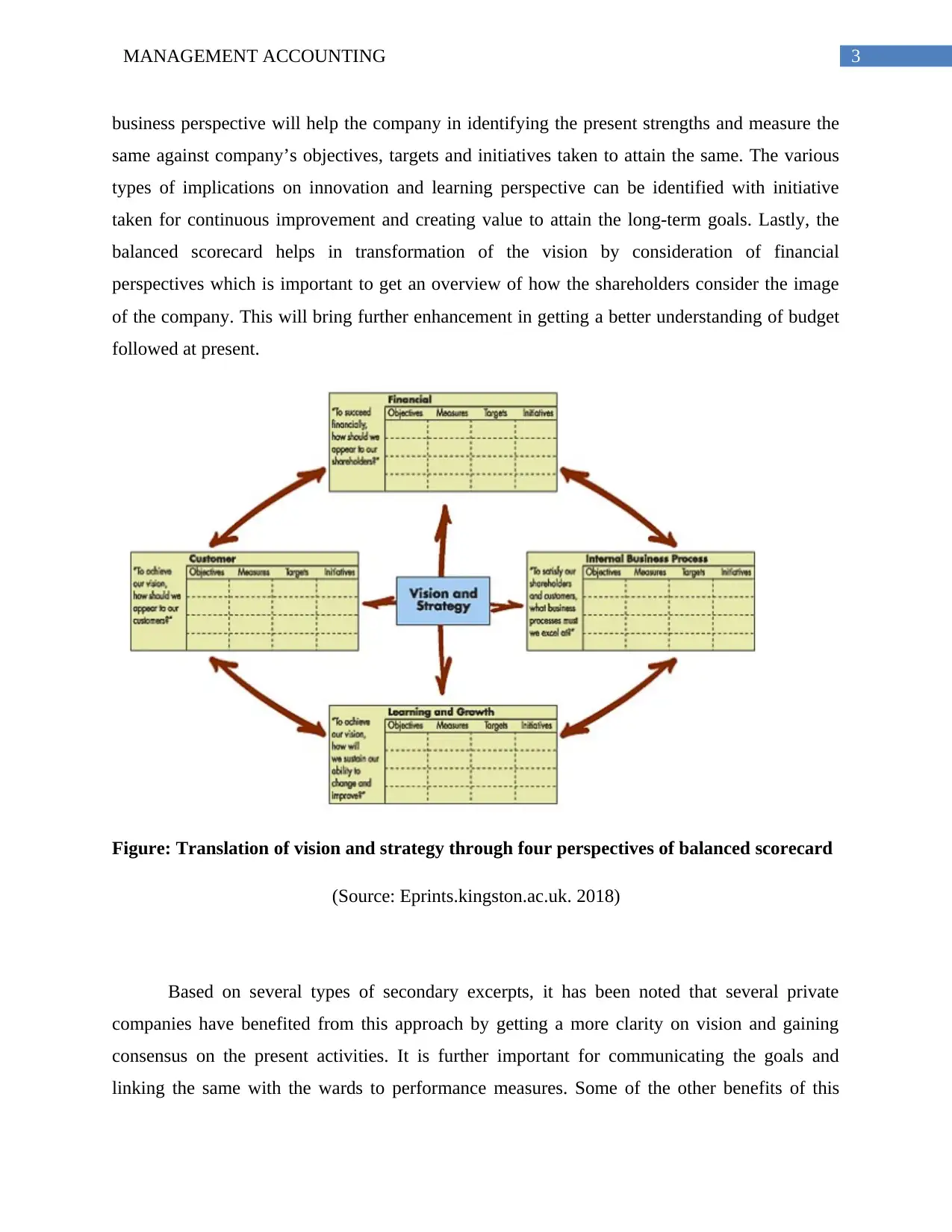

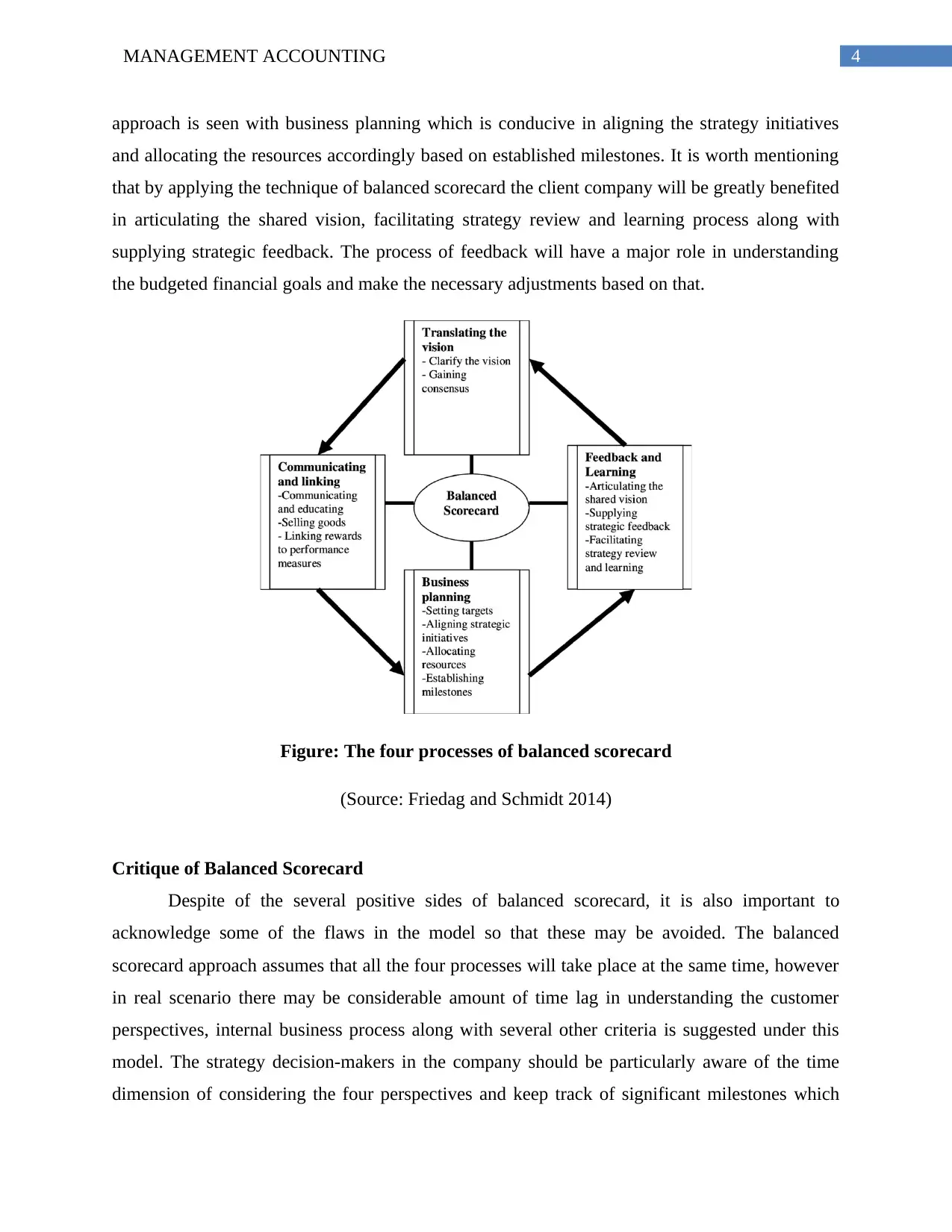

This report provides a detailed analysis of the balanced scorecard, a performance measurement and strategic management system developed by Dr. Robert Kaplan and Dr. David Norton. It emphasizes the benefits of using a balanced scorecard, including the incorporation of both financial and non-financial performance measures for a comprehensive overview of a company's performance. The report discusses the four perspectives of the balanced scorecard: customer, internal business, innovation and learning, and financial, highlighting how each contributes to achieving long-term organizational goals. It also acknowledges the limitations of the balanced scorecard, such as the assumption that all processes occur simultaneously and the neglect of technological advancements. The report concludes that despite these challenges, the balanced scorecard can be a valuable tool for private companies when continuously monitored and updated.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.