Analysis of Audit, Assurance, and Compliance for ADX Energy Limited

VerifiedAdded on 2023/06/06

|16

|3822

|254

Report

AI Summary

This report provides an in-depth analysis of the audit, assurance, and compliance aspects of ADX Energy Limited. It begins with an executive summary and table of contents, followed by an introduction to the audit process. The report examines the company's compliance with auditor independence requirements, non-audit services, and auditor remuneration, along with key audit matters. It discusses the audit committee's roles and responsibilities, the audit opinion provided, and the responsibilities of both management and the auditor. The report also addresses material subsequent events, the effectiveness of reported information, and any missing or under-reported information. The report concludes with follow-up questions for the auditor and a final conclusion. The report analyzes the financial statements, focusing on aspects like cash, and the auditor's opinion, which was unqualified. The report also highlights the importance of independence and the roles of the audit committee and management in the audit process.

Student name:

Student ID:

Assignment Title:

Date:

Word count: 2500 words

Company name: ADX energy limited

1

Student ID:

Assignment Title:

Date:

Word count: 2500 words

Company name: ADX energy limited

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

HI6026 Audit, Assurance, and Compliance

2

2

Executive summary

In this report, the matters in relation to the auditing are considered and explained in the

context of ADX energy limited. All of the important aspects such as the independence of the

auditor and the non-audit services have been taken into account. The remuneration which is

paid to auditors is also taken into account and with that, the audit committee involved is

considered and is identified that it is not present. There is a determination of the opinion which

is provided by the auditor in respect of the financial statements of the company. The auditor’s

and management’s responsibilities are also identified and with that the importance of

information for the third parties is ascertained.

3

In this report, the matters in relation to the auditing are considered and explained in the

context of ADX energy limited. All of the important aspects such as the independence of the

auditor and the non-audit services have been taken into account. The remuneration which is

paid to auditors is also taken into account and with that, the audit committee involved is

considered and is identified that it is not present. There is a determination of the opinion which

is provided by the auditor in respect of the financial statements of the company. The auditor’s

and management’s responsibilities are also identified and with that the importance of

information for the third parties is ascertained.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Table of Contents

Introduction:....................................................................................................................................5

Compliance with Independence requirements...........................................................................6

Non-audit services and their nature............................................................................................6

Analysis of Auditor’s remuneration.............................................................................................7

Key audit matters.........................................................................................................................8

The audit committee and its roles and responsibilities...............................................................8

Audit Opinion...............................................................................................................................9

Management and auditor Responsibilities................................................................................10

Material subsequent events......................................................................................................10

The effectiveness of the material information reported...........................................................11

Missing or under-reported Material information.....................................................................11

Follow-up questions for auditor................................................................................................11

Conclusion:....................................................................................................................................13

References.....................................................................................................................................14

4

Introduction:....................................................................................................................................5

Compliance with Independence requirements...........................................................................6

Non-audit services and their nature............................................................................................6

Analysis of Auditor’s remuneration.............................................................................................7

Key audit matters.........................................................................................................................8

The audit committee and its roles and responsibilities...............................................................8

Audit Opinion...............................................................................................................................9

Management and auditor Responsibilities................................................................................10

Material subsequent events......................................................................................................10

The effectiveness of the material information reported...........................................................11

Missing or under-reported Material information.....................................................................11

Follow-up questions for auditor................................................................................................11

Conclusion:....................................................................................................................................13

References.....................................................................................................................................14

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction:

The financial accounts which are prepared in the company represent the position of the

company and for that auditing are required to be undertaken. The same has been carried by

ADX energy which is the company listed on ASX and was incorporated in 1987. It is dealing in oil

and gas exploration in Western Australia. The company is expanding itself by making the

addition to its business activities. All of the concepts which will be providing the assurance

regarding the statements are involved in this report. The proper evaluation is made by the

auditor of all the information and then by proper study and findings which are obtained they

present the opinion in relation to the same. The remuneration is paid to them for all the

services and that will be identified and also the key matters which will be covered by them will

also be discussed. There will be follow up which will be processed and for that questions will be

provided in the last section.

5

The financial accounts which are prepared in the company represent the position of the

company and for that auditing are required to be undertaken. The same has been carried by

ADX energy which is the company listed on ASX and was incorporated in 1987. It is dealing in oil

and gas exploration in Western Australia. The company is expanding itself by making the

addition to its business activities. All of the concepts which will be providing the assurance

regarding the statements are involved in this report. The proper evaluation is made by the

auditor of all the information and then by proper study and findings which are obtained they

present the opinion in relation to the same. The remuneration is paid to them for all the

services and that will be identified and also the key matters which will be covered by them will

also be discussed. There will be follow up which will be processed and for that questions will be

provided in the last section.

5

Compliance with Independence requirements

The business is carried out by the involvement of various operations and it is required that

operations are made in the correct manner. All of the information which is there in relation to

all the activities will be incorporated in the accounts of the company on the basis of which

several decisions will be made (Dawuda, et. al., 2015). It will be required that the accuracy of

them shall be evaluated in a proper manner and for that, company will be an undertaking of the

auditing process. In that auditor will be required to perform the verification of the statements

so that they can present the opinion in respect of their true position (Tepalagul & Lin, 2015).

For performing the best manner it is required that the auditor shall be provided with complete

independence. In that, they will not be restricted by anything and can carry on the process in

the manner they wish. There shall be no interest of the auditors in the company as by that the

effectiveness of the audit and opinion will be affected (Xie, 2016). If they will be having any kind

of personal interest then the opinion will be made in such manner which will be beneficial to

them and so this will be affecting the business in an adverse manner. All of the misstatements

or errors which arise in the business will be determined and reported in a proper manner so

that they are in the notice of all and actions to eliminate the same can be taken by

management (Corplaw, 2018).

In the case of ADX energy, the auditors are independent and there is no restriction which is

imposed on them. They are allowed to take their decisions as per the best of their knowledge

and findings. For the same, a declaration has been made by them in which it is stated that they

are independent and all the requirements of corporation act have been met (ADX energy

limited, 2018). The professional conduct is also followed and the opinion which is made by

them is free from any bias.

Non-audit services and their nature

The auditor of the company performs the audit services but in the company, there are various

other services also which are required and they are classified as non-audit services (Berg &

Moré, 2016). Auditor of the company is not allowed to perform any such service by which the

6

The business is carried out by the involvement of various operations and it is required that

operations are made in the correct manner. All of the information which is there in relation to

all the activities will be incorporated in the accounts of the company on the basis of which

several decisions will be made (Dawuda, et. al., 2015). It will be required that the accuracy of

them shall be evaluated in a proper manner and for that, company will be an undertaking of the

auditing process. In that auditor will be required to perform the verification of the statements

so that they can present the opinion in respect of their true position (Tepalagul & Lin, 2015).

For performing the best manner it is required that the auditor shall be provided with complete

independence. In that, they will not be restricted by anything and can carry on the process in

the manner they wish. There shall be no interest of the auditors in the company as by that the

effectiveness of the audit and opinion will be affected (Xie, 2016). If they will be having any kind

of personal interest then the opinion will be made in such manner which will be beneficial to

them and so this will be affecting the business in an adverse manner. All of the misstatements

or errors which arise in the business will be determined and reported in a proper manner so

that they are in the notice of all and actions to eliminate the same can be taken by

management (Corplaw, 2018).

In the case of ADX energy, the auditors are independent and there is no restriction which is

imposed on them. They are allowed to take their decisions as per the best of their knowledge

and findings. For the same, a declaration has been made by them in which it is stated that they

are independent and all the requirements of corporation act have been met (ADX energy

limited, 2018). The professional conduct is also followed and the opinion which is made by

them is free from any bias.

Non-audit services and their nature

The auditor of the company performs the audit services but in the company, there are various

other services also which are required and they are classified as non-audit services (Berg &

Moré, 2016). Auditor of the company is not allowed to perform any such service by which the

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

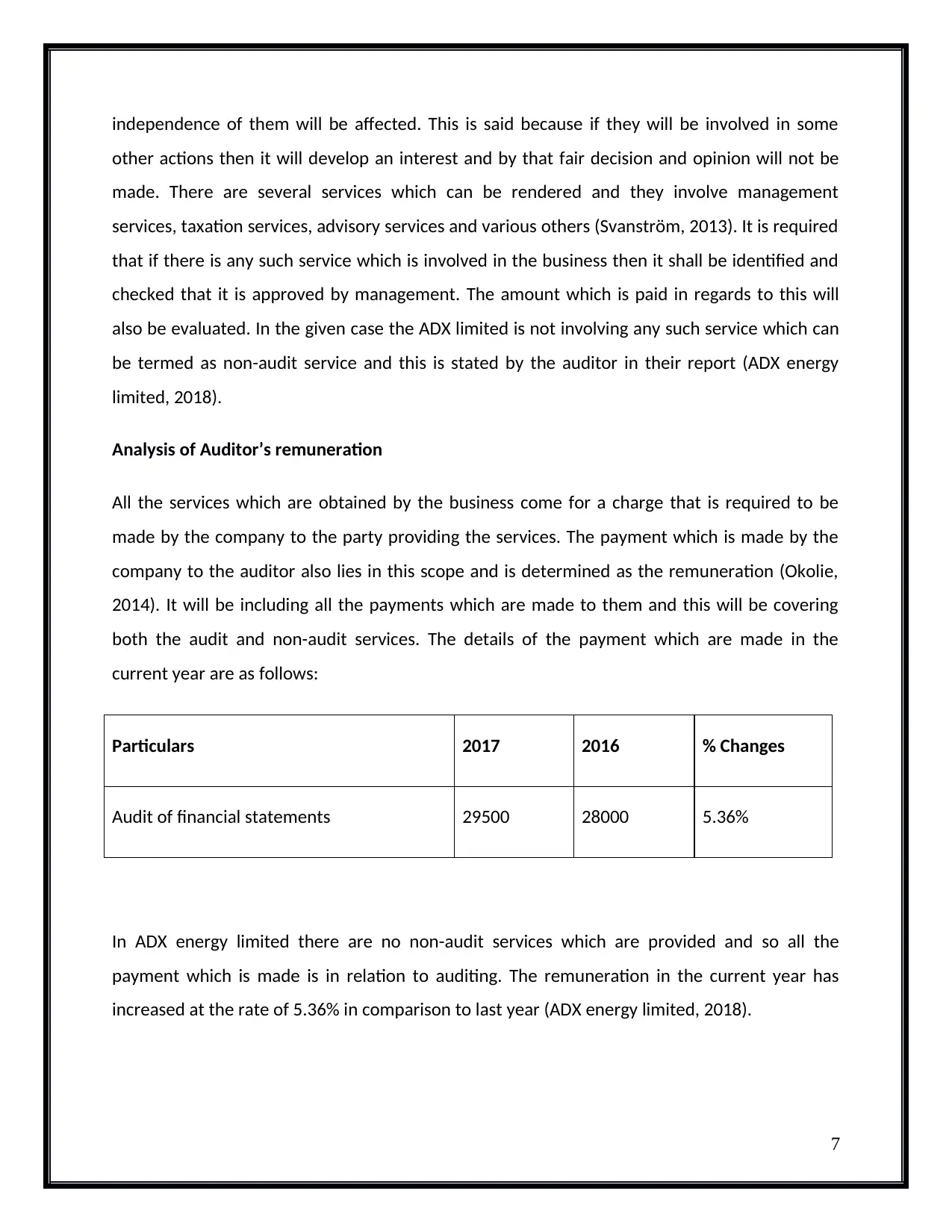

independence of them will be affected. This is said because if they will be involved in some

other actions then it will develop an interest and by that fair decision and opinion will not be

made. There are several services which can be rendered and they involve management

services, taxation services, advisory services and various others (Svanström, 2013). It is required

that if there is any such service which is involved in the business then it shall be identified and

checked that it is approved by management. The amount which is paid in regards to this will

also be evaluated. In the given case the ADX limited is not involving any such service which can

be termed as non-audit service and this is stated by the auditor in their report (ADX energy

limited, 2018).

Analysis of Auditor’s remuneration

All the services which are obtained by the business come for a charge that is required to be

made by the company to the party providing the services. The payment which is made by the

company to the auditor also lies in this scope and is determined as the remuneration (Okolie,

2014). It will be including all the payments which are made to them and this will be covering

both the audit and non-audit services. The details of the payment which are made in the

current year are as follows:

Particulars 2017 2016 % Changes

Audit of financial statements 29500 28000 5.36%

In ADX energy limited there are no non-audit services which are provided and so all the

payment which is made is in relation to auditing. The remuneration in the current year has

increased at the rate of 5.36% in comparison to last year (ADX energy limited, 2018).

7

other actions then it will develop an interest and by that fair decision and opinion will not be

made. There are several services which can be rendered and they involve management

services, taxation services, advisory services and various others (Svanström, 2013). It is required

that if there is any such service which is involved in the business then it shall be identified and

checked that it is approved by management. The amount which is paid in regards to this will

also be evaluated. In the given case the ADX limited is not involving any such service which can

be termed as non-audit service and this is stated by the auditor in their report (ADX energy

limited, 2018).

Analysis of Auditor’s remuneration

All the services which are obtained by the business come for a charge that is required to be

made by the company to the party providing the services. The payment which is made by the

company to the auditor also lies in this scope and is determined as the remuneration (Okolie,

2014). It will be including all the payments which are made to them and this will be covering

both the audit and non-audit services. The details of the payment which are made in the

current year are as follows:

Particulars 2017 2016 % Changes

Audit of financial statements 29500 28000 5.36%

In ADX energy limited there are no non-audit services which are provided and so all the

payment which is made is in relation to auditing. The remuneration in the current year has

increased at the rate of 5.36% in comparison to last year (ADX energy limited, 2018).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Key audit matters

The auditor is required to consider all the aspects of the business but there are certain key

matters which are more relevant and it is needed that they are considered in a more effective

manner. They are to be involved as the opinion which is made by the auditor will be based on

this also and so it will be important to have the proper information in relation to them. The

procedures are followed so that they can be dealt with in the best manner and there is no issue

which is faced due to them in the coming period. For that, they are to be identified and the

same in the given case are as follows:

Cash: In the company, there is a high amount of the cash and that constitutes the 92% of the

total assets which are held by the company. In the carrying out of all the activities and

operations, this is considered to be a most important element. This is one of the most liquid

assets and due to this, it is considered that there is no high amount of risk which is involved in

relation to it and there is no judgment which is required to be made in relation to this (ADX

energy limited, 2018). In the given case this is most important as this will be affecting all the

processes involved in the business such as the allocation of the resources and all the other

strategies which are made in the company. In the completion of the audit, it will be required

that they shall be taken into consideration in an appropriate manner. There are various

procedures which are adopted in the company in which the completeness, valuation, and

existence of the balance are ensured. There were proper confirmations which are obtained

from the client so that the balance which is there can be evaluated (ADX energy limited, 2018).

All the disclosures which are made in the reports in this context are assessed so that their

appropriateness is considered. Proper entries in relation to them are provided in the notes

which are made in relation to them.

The audit committee and its roles and responsibilities

In the audit process, there are various requirements which are to be met by the auditor and for

that, they will be requiring the assistance of the board. In order to fulfill this condition, it is

required that there shall be a proper committee which shall be framed so that they can deal

8

The auditor is required to consider all the aspects of the business but there are certain key

matters which are more relevant and it is needed that they are considered in a more effective

manner. They are to be involved as the opinion which is made by the auditor will be based on

this also and so it will be important to have the proper information in relation to them. The

procedures are followed so that they can be dealt with in the best manner and there is no issue

which is faced due to them in the coming period. For that, they are to be identified and the

same in the given case are as follows:

Cash: In the company, there is a high amount of the cash and that constitutes the 92% of the

total assets which are held by the company. In the carrying out of all the activities and

operations, this is considered to be a most important element. This is one of the most liquid

assets and due to this, it is considered that there is no high amount of risk which is involved in

relation to it and there is no judgment which is required to be made in relation to this (ADX

energy limited, 2018). In the given case this is most important as this will be affecting all the

processes involved in the business such as the allocation of the resources and all the other

strategies which are made in the company. In the completion of the audit, it will be required

that they shall be taken into consideration in an appropriate manner. There are various

procedures which are adopted in the company in which the completeness, valuation, and

existence of the balance are ensured. There were proper confirmations which are obtained

from the client so that the balance which is there can be evaluated (ADX energy limited, 2018).

All the disclosures which are made in the reports in this context are assessed so that their

appropriateness is considered. Proper entries in relation to them are provided in the notes

which are made in relation to them.

The audit committee and its roles and responsibilities

In the audit process, there are various requirements which are to be met by the auditor and for

that, they will be requiring the assistance of the board. In order to fulfill this condition, it is

required that there shall be a proper committee which shall be framed so that they can deal

8

with this (Al-Matari, et. al., 2017). It will be possible and for that audit committee is established

in which there are members of the board of the company. They will be required to ensure that

the auditor is independent and they are provided with all the required assistance which helps

them in performing an audit in a proper manner (AICD, 2018). There is the charter which is

framed for them in which all the information in relation to the committee and the

responsibilities which are to be met by them are presented.

The company which is selected is ADX and it is small in size and there are not much of the

operations which are performed by it (ADX energy limited, 2018). Due to this factor, there is no

requirement to have the separate audit committee in the company and the tasks will be

managed by the board itself. in this, they will be ensuring the integrity and checking all the

statements and the requirements will also be fulfilled by them.

Audit Opinion

The audit is carried in the company so that all of the aspects which are involved and the reports

that are made by the company can be evaluated in the most effective manner. They will be

reviewing them with the help of the information which is available and then the opinion will be

presented by them (Tian & Xin, 2017). This will be specified about the accuracy of the financial

information that is provided in the financial statements. There are various opinions which can

be framed and if the auditor is of the view that the reports of the company are presenting the

true position of the business then the unqualified opinion will be provided (Narvas, 2018). In

case of the issues which are there and there is no proper information which is identified in

relation to them then the qualified opinion will be framed (Public Company Accounting

Oversight Board (PCAOB), 2013). There will be making of the adverse opinion of the situation in

which the reports are representing the errors and mistakes and they will be having the adverse

impact on the company.

The auditor has provided the unqualified opinion in the current year of ADX energy and for that

declaration has also been made. they have accepted and assured that by the financial

statements there is the true and fair view which is attained about the position of the company

9

in which there are members of the board of the company. They will be required to ensure that

the auditor is independent and they are provided with all the required assistance which helps

them in performing an audit in a proper manner (AICD, 2018). There is the charter which is

framed for them in which all the information in relation to the committee and the

responsibilities which are to be met by them are presented.

The company which is selected is ADX and it is small in size and there are not much of the

operations which are performed by it (ADX energy limited, 2018). Due to this factor, there is no

requirement to have the separate audit committee in the company and the tasks will be

managed by the board itself. in this, they will be ensuring the integrity and checking all the

statements and the requirements will also be fulfilled by them.

Audit Opinion

The audit is carried in the company so that all of the aspects which are involved and the reports

that are made by the company can be evaluated in the most effective manner. They will be

reviewing them with the help of the information which is available and then the opinion will be

presented by them (Tian & Xin, 2017). This will be specified about the accuracy of the financial

information that is provided in the financial statements. There are various opinions which can

be framed and if the auditor is of the view that the reports of the company are presenting the

true position of the business then the unqualified opinion will be provided (Narvas, 2018). In

case of the issues which are there and there is no proper information which is identified in

relation to them then the qualified opinion will be framed (Public Company Accounting

Oversight Board (PCAOB), 2013). There will be making of the adverse opinion of the situation in

which the reports are representing the errors and mistakes and they will be having the adverse

impact on the company.

The auditor has provided the unqualified opinion in the current year of ADX energy and for that

declaration has also been made. they have accepted and assured that by the financial

statements there is the true and fair view which is attained about the position of the company

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(ADX energy limited, 2018). All of the requirements of the corporation act 2001 has been

complied with and also the standards which are framed by the government are also taken into

account in the making of the financial statements.

Management and auditor Responsibilities

Management responsibility: The main role which is to be played by the management is in

relation to the making of the financial reports in which all of the information will be presented

with accuracy (Clikeman, 2018). They will be ensuring that they are made by following all the

accounting standards and also true and fair view is provided by accounts. They will be

evaluating and making such internal control by which proper reporting will be made possible.

By the help of evaluation made, it will be confirmed that the financial statements are free from

any kind of error and misstatements. The various other aspects which are relevant will also be

taken into consideration in this process and that involves disclosures, going concern and other

matters in relation to them.

Auditor’s Responsibility: The main aim of the auditor is to obtain the assurance in relation to

the accuracy of the financial statements. They will be reviewing that the accounts of the

company are free from any misstatements and errors which are caused (Turnkey, 2018). On the

basis of the findings which will be made by them, there will be an opinion which will be

presented. There is the assurance which will be provided but then also there may be some

misstatement which has remained from being detected. There will be the identification of them

and then the opinion about the position of the company will be provided in the report

prepared.

Material subsequent events

In the business, there are various activities which are undertaken and out of them some of

them take place after the making of the accounts and they are considered as subsequent

events (Ozdemir & Gokcen, 2016). It will be essential that the identification of them is made so

that they can be dealt with in accordance with the standards which are specified. There will be

adjusting and non-adjusting events which take place and the treatment of them will be made

10

complied with and also the standards which are framed by the government are also taken into

account in the making of the financial statements.

Management and auditor Responsibilities

Management responsibility: The main role which is to be played by the management is in

relation to the making of the financial reports in which all of the information will be presented

with accuracy (Clikeman, 2018). They will be ensuring that they are made by following all the

accounting standards and also true and fair view is provided by accounts. They will be

evaluating and making such internal control by which proper reporting will be made possible.

By the help of evaluation made, it will be confirmed that the financial statements are free from

any kind of error and misstatements. The various other aspects which are relevant will also be

taken into consideration in this process and that involves disclosures, going concern and other

matters in relation to them.

Auditor’s Responsibility: The main aim of the auditor is to obtain the assurance in relation to

the accuracy of the financial statements. They will be reviewing that the accounts of the

company are free from any misstatements and errors which are caused (Turnkey, 2018). On the

basis of the findings which will be made by them, there will be an opinion which will be

presented. There is the assurance which will be provided but then also there may be some

misstatement which has remained from being detected. There will be the identification of them

and then the opinion about the position of the company will be provided in the report

prepared.

Material subsequent events

In the business, there are various activities which are undertaken and out of them some of

them take place after the making of the accounts and they are considered as subsequent

events (Ozdemir & Gokcen, 2016). It will be essential that the identification of them is made so

that they can be dealt with in accordance with the standards which are specified. There will be

adjusting and non-adjusting events which take place and the treatment of them will be made

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

accordingly (Al Nawaiseh & Jaber, 2015). By them, the balances in the company will be affected

if they will be incorporated in the accounts of the company (ACCA, 2018).

In ADX energy there are some of the transactions which are identified and will be considered as

the subsequent events. There is the issue of the shares which has been made after the closing

of the accounts (ADX energy limited, 2018). Also, there is the agreement which has been

entered by the company, in respect of the investment which is made.

The effectiveness of the material information reported

In the company, there are several parties which are associated with it and it is required that

interest of all shall be taken into consideration. The third party stakeholders will also be

covered and they will be making the use of the information for the taking of right decisions

(Drogalas, et. al., 2017). In this, the employees, customers, investors, and government will be

included. They are to be provided with the required information so that can use them as per

their needs. The government will be ascertaining the tax amount and investors can take the

decision in relation to the investment which is to be made. The information will be very

important for them and so shall be provided with accuracy.

Missing or under-reported Material information

In the making of the report, all of the areas have been considered in relation to the audit which

is taking place. In this process, there is a requirement of a lot of information and sometimes

there is such information which is required to be present but is not made (Kipp, 2017). The

company is disclosing all the required information in a proper manner and there is no such data

seemed to be underreported. All of the data is provided in the required details and is

understandable in a proper manner.

Follow-up questions for auditor

The company will be required to have the follow up for the shareholders in which they will be

provided with the opportunity to clarify the doubts which they have. For this, they will be

11

if they will be incorporated in the accounts of the company (ACCA, 2018).

In ADX energy there are some of the transactions which are identified and will be considered as

the subsequent events. There is the issue of the shares which has been made after the closing

of the accounts (ADX energy limited, 2018). Also, there is the agreement which has been

entered by the company, in respect of the investment which is made.

The effectiveness of the material information reported

In the company, there are several parties which are associated with it and it is required that

interest of all shall be taken into consideration. The third party stakeholders will also be

covered and they will be making the use of the information for the taking of right decisions

(Drogalas, et. al., 2017). In this, the employees, customers, investors, and government will be

included. They are to be provided with the required information so that can use them as per

their needs. The government will be ascertaining the tax amount and investors can take the

decision in relation to the investment which is to be made. The information will be very

important for them and so shall be provided with accuracy.

Missing or under-reported Material information

In the making of the report, all of the areas have been considered in relation to the audit which

is taking place. In this process, there is a requirement of a lot of information and sometimes

there is such information which is required to be present but is not made (Kipp, 2017). The

company is disclosing all the required information in a proper manner and there is no such data

seemed to be underreported. All of the data is provided in the required details and is

understandable in a proper manner.

Follow-up questions for auditor

The company will be required to have the follow up for the shareholders in which they will be

provided with the opportunity to clarify the doubts which they have. For this, they will be

11

interacting with the auditor in the annual general meeting and asking them with the required

questions. Some of the sample questions are provided hereunder:

Did you come across any kind of internal control issues in the company?

Are there any factors by which your audit independence is affected?

Have you determined any errors which are required to be reported as they will be affecting

the company in a great manner?

12

questions. Some of the sample questions are provided hereunder:

Did you come across any kind of internal control issues in the company?

Are there any factors by which your audit independence is affected?

Have you determined any errors which are required to be reported as they will be affecting

the company in a great manner?

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.