AFCP8001 Term 1 2020: Epeus Portfolio Stock Pricing Analysis

VerifiedAdded on 2022/08/14

|15

|2430

|15

Project

AI Summary

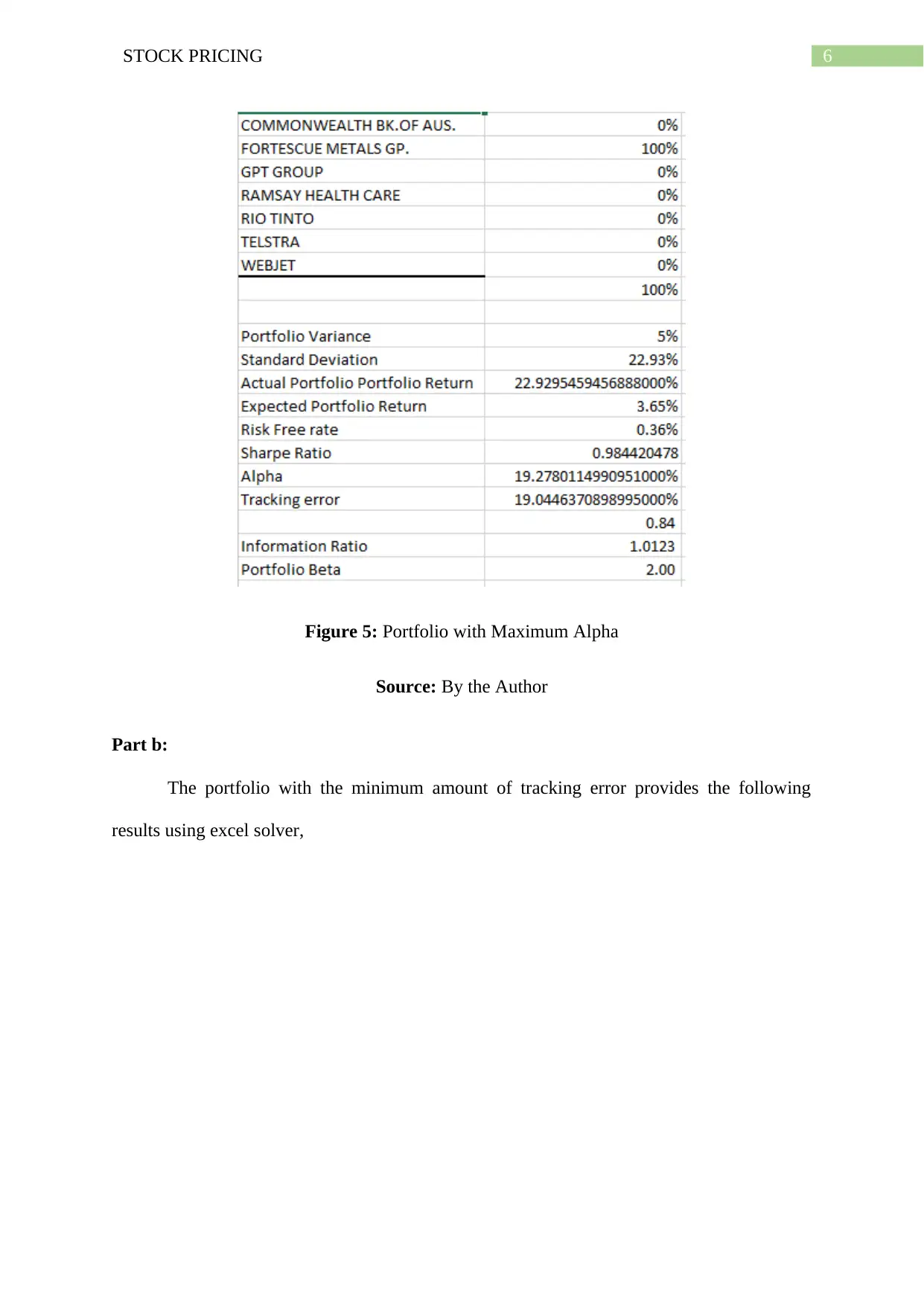

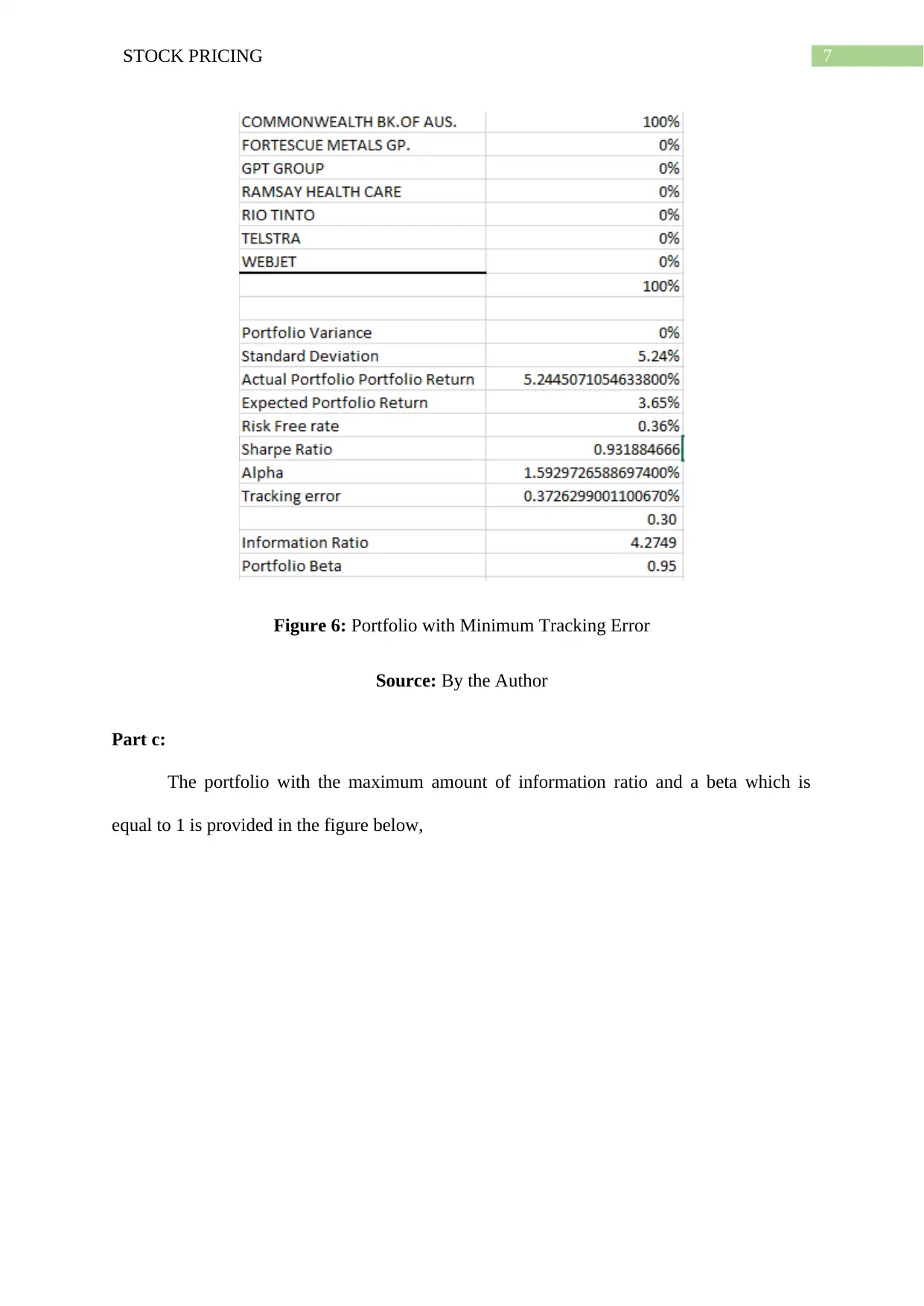

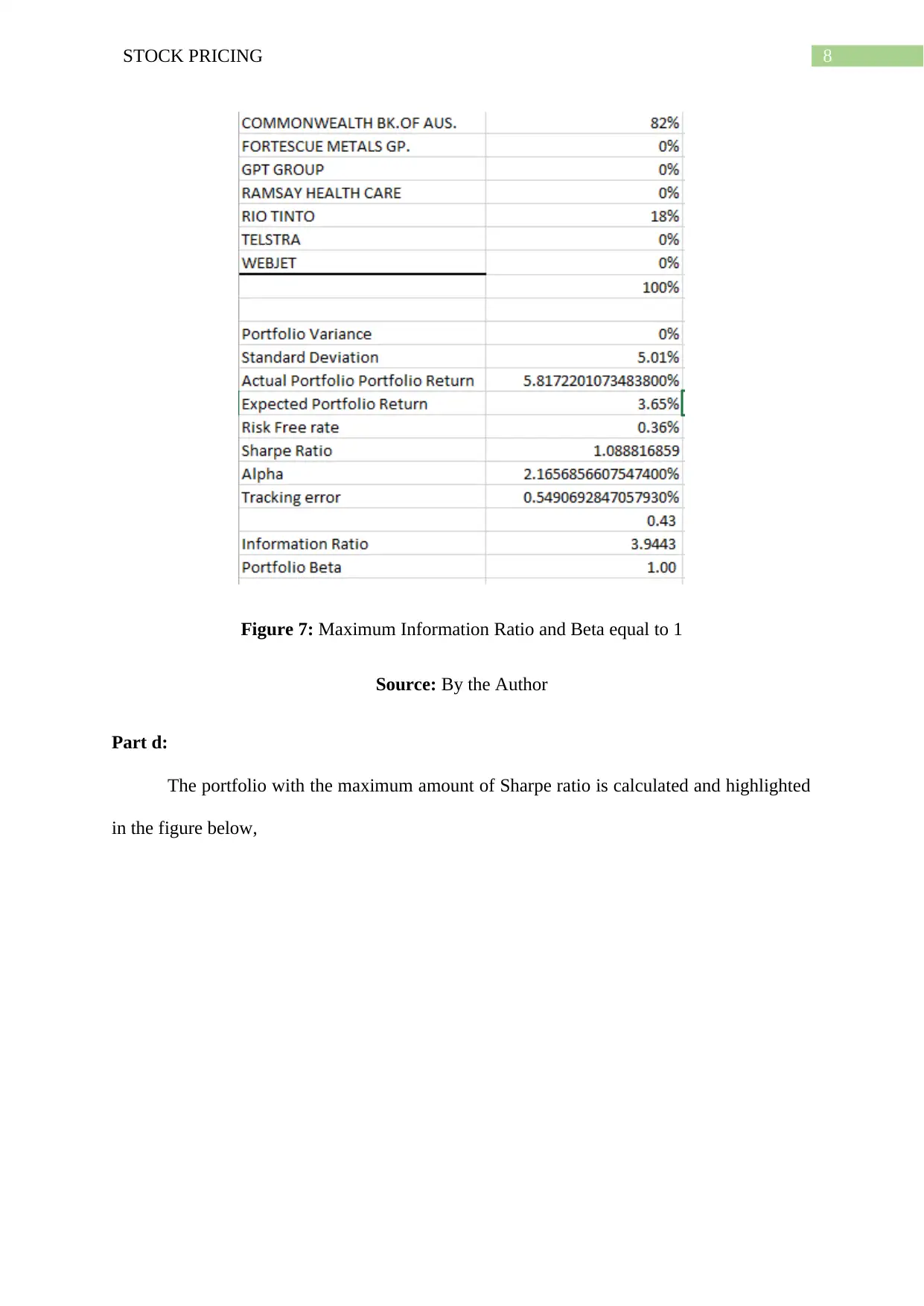

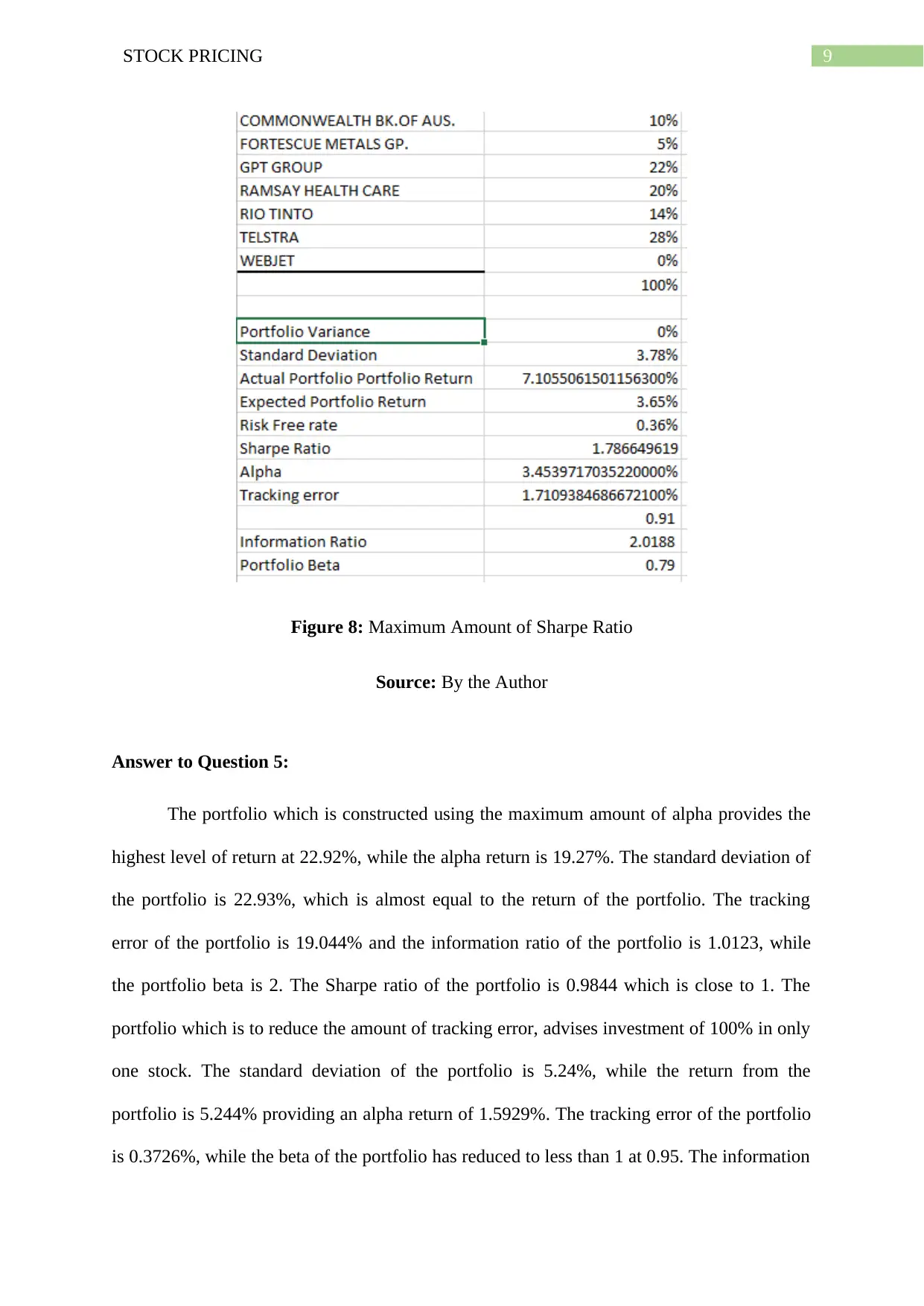

This assignment analyzes stock pricing models, portfolio construction, and the use of robo-advisors. The analysis begins with calculating key metrics like alpha, beta, Sharpe ratio, and tracking error using both single and multi-factor models. The student then explores portfolio optimization techniques to maximize returns and minimize risks, including constructing portfolios with maximum alpha, minimum tracking error, maximum information ratio (with beta = 1), and maximum Sharpe ratio. The assignment also delves into the application of robo-advisors in the investment industry, comparing their efficiency and effectiveness with traditional advisors. The student provides recommendations for Epeus Portfolio Management based on the findings, highlighting the benefits of robo-advisors and the importance of diversification and risk management. The project uses Excel Solver to optimize portfolio weights, generate capital allocation lines, and analyze efficient frontiers, providing a practical application of financial concepts.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.