AFIN270 Assignment: Analyzing Probability, Correlation, and Modeling

VerifiedAdded on 2022/11/26

|7

|1079

|355

Homework Assignment

AI Summary

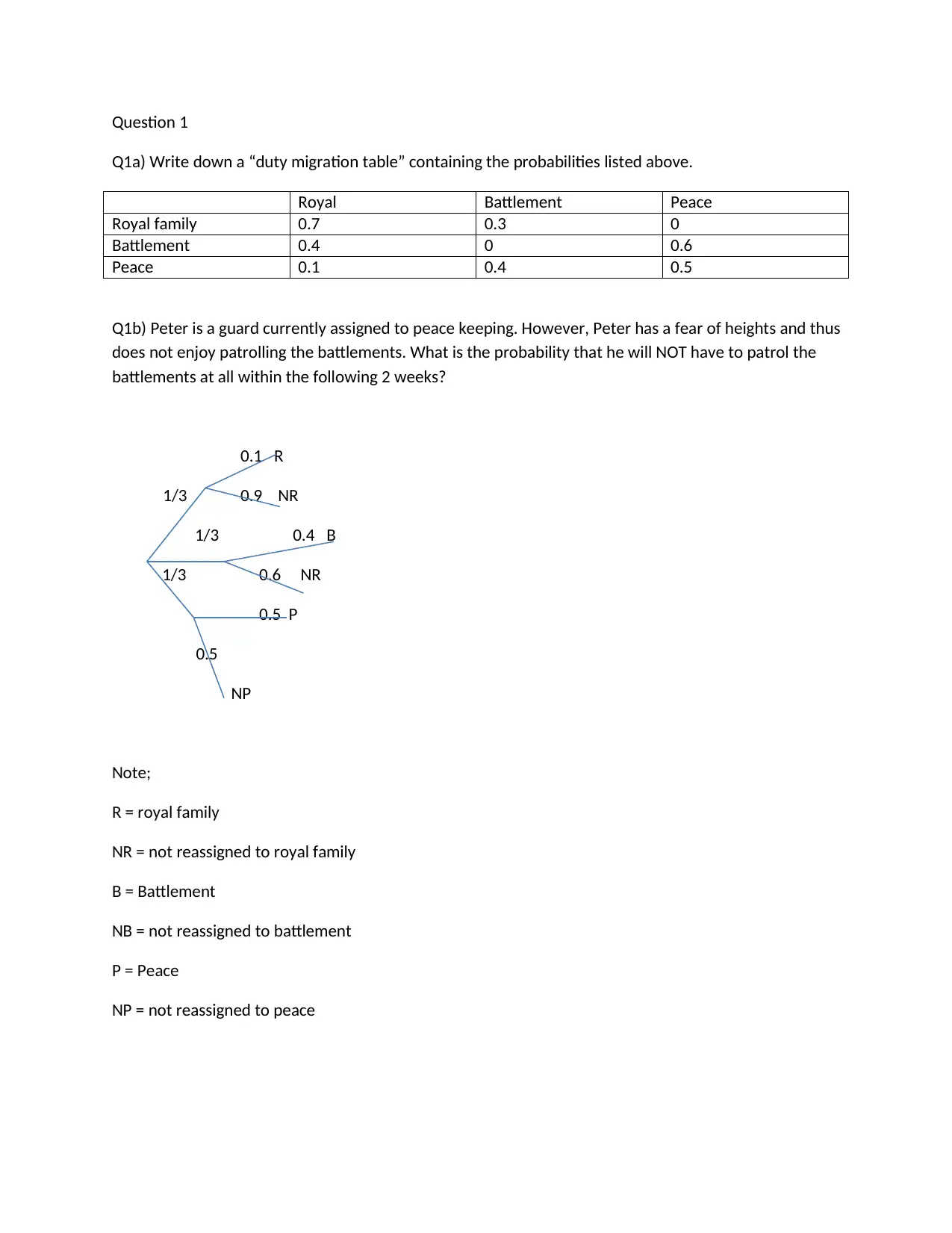

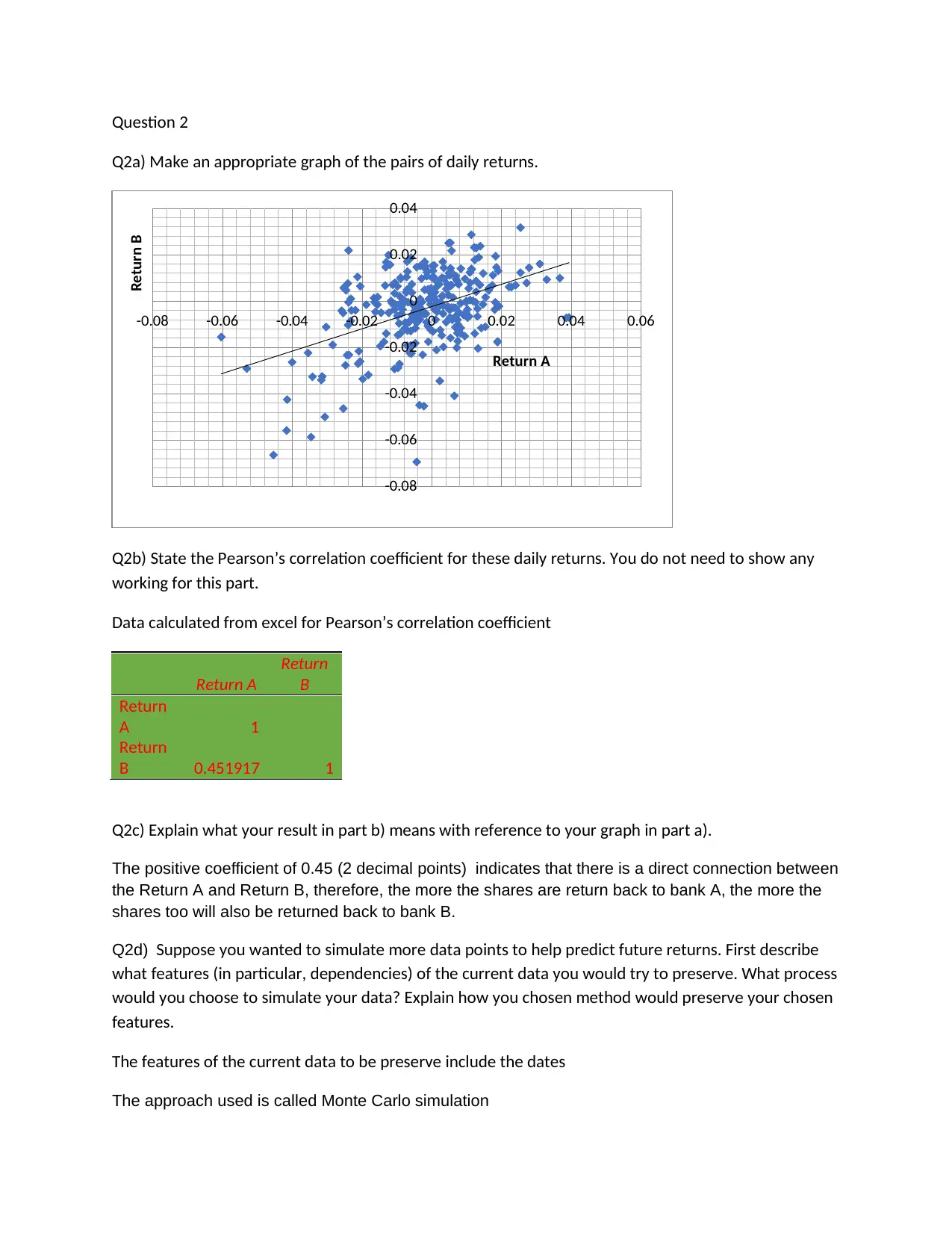

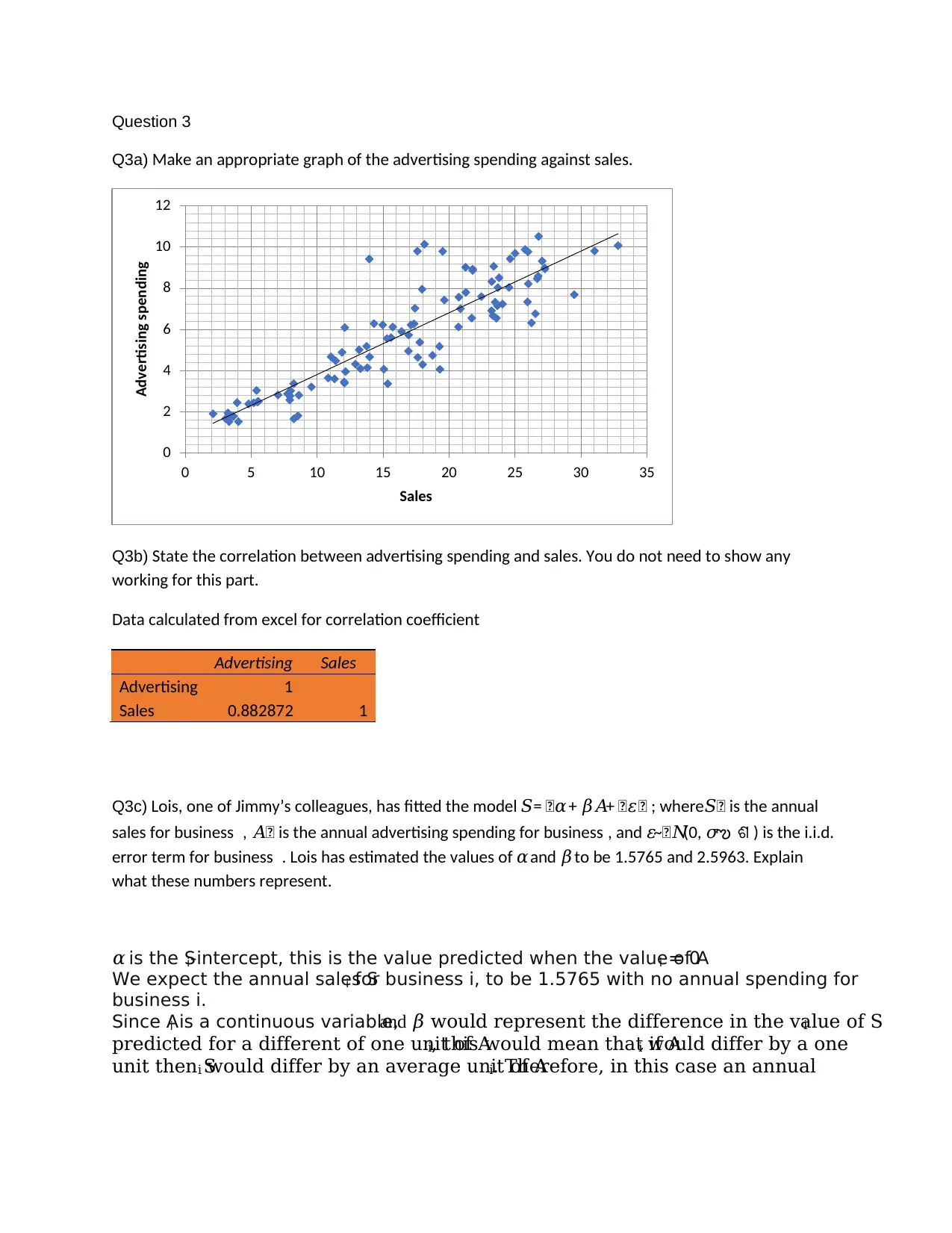

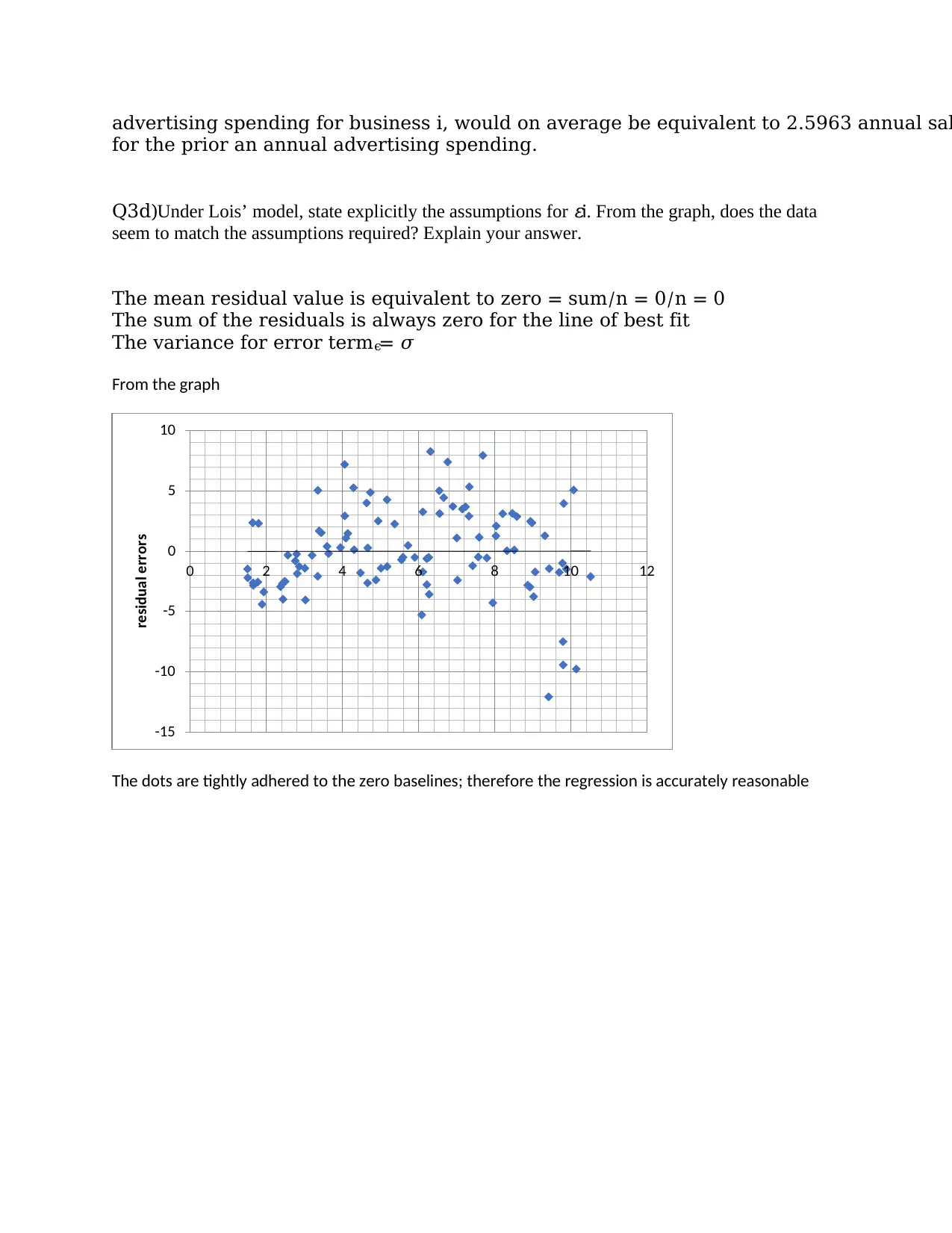

This assignment solution for AFIN270 covers a range of financial concepts including probability, correlation, and statistical modeling. Question 1 explores probability calculations related to a guard's duties in Camelot, including the construction of a duty migration table and the calculation of probabilities for specific scenarios. Question 2 delves into the analysis of daily returns for two assets, involving the creation of a scatter plot, the calculation and interpretation of Pearson's correlation coefficient, and a discussion of data simulation techniques using Monte Carlo methods to preserve data features. Question 3 focuses on the relationship between advertising spending and sales, including the creation of a scatter plot, the calculation of the correlation coefficient, and the interpretation of a linear regression model's parameters and assumptions. Finally, Question 4 examines the application of a Fréchet distribution to model monthly returns for shares, involving the derivation of the cumulative distribution function (CDF) and the calculation of probabilities based on the given distribution parameters. The solution demonstrates a practical application of statistical methods to financial problems.

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.