Coursework: Accounting and Financial Management (AFMA7074) Summer 2019

VerifiedAdded on 2022/11/03

|10

|1978

|88

Essay

AI Summary

This essay provides an overview of accounting and financial management, focusing on operating budgets, master budgets, and investment appraisal techniques. It begins by defining budgets and explaining operating budgets, including sales, production, and cost of goods sold budgets, and the benefits of the master budget in consolidating all operational budgets. The essay then discusses various investment appraisal techniques like Payback Period (PBP), Accounting Rate of Return (ARR), Net Present Value (NPV), and Internal Rate of Return (IRR), highlighting their importance in long-term financial decision-making. The study aims to provide an understanding of the different financial and accounting concepts, and their practical application in a business context. An appendix with a master budget example is also included.

RUNNING HEAD: ACCOUNTING AND FINANCE 0

Accounting and Financial

Management

August 18

2019

Accounting and Financial

Management

August 18

2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING AND FINANCE 1

Table of Contents

Introduction................................................................................................................................2

Discussion on operating budgets................................................................................................2

Discussion on the benefits of Master Budget.............................................................................4

Discussion on the need of investment appraisal techniques for the financial decision making

in long run..................................................................................................................................4

Conclusion..................................................................................................................................6

References..................................................................................................................................7

Appendix....................................................................................................................................9

Table of Contents

Introduction................................................................................................................................2

Discussion on operating budgets................................................................................................2

Discussion on the benefits of Master Budget.............................................................................4

Discussion on the need of investment appraisal techniques for the financial decision making

in long run..................................................................................................................................4

Conclusion..................................................................................................................................6

References..................................................................................................................................7

Appendix....................................................................................................................................9

ACCOUNTING AND FINANCE 2

Introduction

The study is conducted to explain the concept of accounting and management in the

organizational context. It explains the meaning and importance of different types of budgets

operating in the company. It also discusses the process of developing budgets in an

enterprise. It provides the evaluation of the importance and benefits of Master budgets in an

entity. The discussion is being provided on the investment appraisal techniques such as; Pay-

back period (PBP), internal rate of return (IRR), Net present value (NPV) and others. The

discussion highlights the importance of investment appraisal practices in making the long

term financial decision of the entity.

Discussion on operating budgets

A budget is defined as the statement which consists of the future predicted values of the

incomes and expenses for a particular period. It is a significant tool used by the managers for

goal setting and decision making (Blinova, 2016). Operating budgets is a category of budgets

in which the operational income and expenses of the business are predicted for the period. In

the given case, the operating expenses and income of the product are provided using which

the different types of operating budgets can be prepared. The operating budgets determine the

profit generated by an enterprise and show the short term budgeted planning of entity which

defines the operational efficiency of the business. The operating budgets are prepared to

identify the profits of the company which is prepared with the help of the following processor

parts of the operating budget.

Sales Budget: Sales budget determines the estimated amount of transactions for the

business. It determines the targeted sales to be achieved by the entity during the

period (Zimmerman, and House, 2016).

Introduction

The study is conducted to explain the concept of accounting and management in the

organizational context. It explains the meaning and importance of different types of budgets

operating in the company. It also discusses the process of developing budgets in an

enterprise. It provides the evaluation of the importance and benefits of Master budgets in an

entity. The discussion is being provided on the investment appraisal techniques such as; Pay-

back period (PBP), internal rate of return (IRR), Net present value (NPV) and others. The

discussion highlights the importance of investment appraisal practices in making the long

term financial decision of the entity.

Discussion on operating budgets

A budget is defined as the statement which consists of the future predicted values of the

incomes and expenses for a particular period. It is a significant tool used by the managers for

goal setting and decision making (Blinova, 2016). Operating budgets is a category of budgets

in which the operational income and expenses of the business are predicted for the period. In

the given case, the operating expenses and income of the product are provided using which

the different types of operating budgets can be prepared. The operating budgets determine the

profit generated by an enterprise and show the short term budgeted planning of entity which

defines the operational efficiency of the business. The operating budgets are prepared to

identify the profits of the company which is prepared with the help of the following processor

parts of the operating budget.

Sales Budget: Sales budget determines the estimated amount of transactions for the

business. It determines the targeted sales to be achieved by the entity during the

period (Zimmerman, and House, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING AND FINANCE 3

Production Budget: This budget determines the quantity of product is manufactured

by the entity to fulfill the requirement of consumers which is predicted in the budget

of sales. Therefore, the production budget identifies the production of goods for

meeting the sales requirements.

Direct labor budget: It demonstrates the budgeted hours of labor required by the entity

to fulfill the production budget requirements.

Overhead Budget: It shows the number of expenses that are expected to occur while

producing the requisite quantity of production budget except for the material and

labor expenses (Telecký, Čejka, and Guchenko, 2018).

Direct material purchase budget: This depicts the quantity of material required for the

production of the quantity estimated in the budget for production to fulfill the

estimated market demand.

Finished goods inventory budget: It determines cost of per unit for the production of

the goods produced by the entity according to the predicted amount of expenses.

Cost of goods sold budget: It is developed when the trade has opening and closing

amount of inventory. In such case, a cost of goods sold budget is made to conclude

the cost element in the sales made by the trade (Katsinas, D'Amico, Friedel, Adair,

Warner, and Malley, 2016).

Selling and administrative expenses budget: The fixed and variable expenditures apart

from the production costs are estimated in this budget.

Budgeted income statement: The presentation of all the budgets explained above in a

single format is termed as a budgeted income statement which shows the profit of the

business (Maduekwe, and Kamala, 2016). It is prepared after the preparation of all the

components of the operating budget.

Production Budget: This budget determines the quantity of product is manufactured

by the entity to fulfill the requirement of consumers which is predicted in the budget

of sales. Therefore, the production budget identifies the production of goods for

meeting the sales requirements.

Direct labor budget: It demonstrates the budgeted hours of labor required by the entity

to fulfill the production budget requirements.

Overhead Budget: It shows the number of expenses that are expected to occur while

producing the requisite quantity of production budget except for the material and

labor expenses (Telecký, Čejka, and Guchenko, 2018).

Direct material purchase budget: This depicts the quantity of material required for the

production of the quantity estimated in the budget for production to fulfill the

estimated market demand.

Finished goods inventory budget: It determines cost of per unit for the production of

the goods produced by the entity according to the predicted amount of expenses.

Cost of goods sold budget: It is developed when the trade has opening and closing

amount of inventory. In such case, a cost of goods sold budget is made to conclude

the cost element in the sales made by the trade (Katsinas, D'Amico, Friedel, Adair,

Warner, and Malley, 2016).

Selling and administrative expenses budget: The fixed and variable expenditures apart

from the production costs are estimated in this budget.

Budgeted income statement: The presentation of all the budgets explained above in a

single format is termed as a budgeted income statement which shows the profit of the

business (Maduekwe, and Kamala, 2016). It is prepared after the preparation of all the

components of the operating budget.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING AND FINANCE 4

Discussion on the benefits of Master Budget

A master budget is defined as the budget which acts as a summary budget that consists of all

the expenses including fixed and variable and all the income of the enterprise to determine

the budgeted profit of the business for the period (Golooba-Mutebi, and Hickey, 2016). The

master budget includes the budgets like budgeted statement of income or the budgeted

financial position statement. The advantages of preparing these budgets are pointed as below:

It provides all the operational budgets of the company in a single format.

It is a summary of all the activities of the business.

It provides for the audit of operational budgets with the master budget to determine

any differences in budgeted data.

It shows the profit estimation of the business in a single report (Golooba-Mutebi, and

Hickey, 2016).

It provides information for the generation of the estimated balance sheet of the entity.

It is used by high-level management for decision making.

It is used to evaluate the efficiency and effectiveness in the performance of the

enterprise.

It acts as a basis for calculating the variances in production, overheads, and sales.

It provides for advance planning for the organization (Golooba-Mutebi, and Hickey,

2016).

It also acts as a motivator and controlling element in the business organization.

Discussion on the need of investment appraisal techniques for the financial decision

making in long run

The financial decision-making process is also called the capital budgeting in terms of

financial management. The investment appraisal techniques are the tools and methods of the

Discussion on the benefits of Master Budget

A master budget is defined as the budget which acts as a summary budget that consists of all

the expenses including fixed and variable and all the income of the enterprise to determine

the budgeted profit of the business for the period (Golooba-Mutebi, and Hickey, 2016). The

master budget includes the budgets like budgeted statement of income or the budgeted

financial position statement. The advantages of preparing these budgets are pointed as below:

It provides all the operational budgets of the company in a single format.

It is a summary of all the activities of the business.

It provides for the audit of operational budgets with the master budget to determine

any differences in budgeted data.

It shows the profit estimation of the business in a single report (Golooba-Mutebi, and

Hickey, 2016).

It provides information for the generation of the estimated balance sheet of the entity.

It is used by high-level management for decision making.

It is used to evaluate the efficiency and effectiveness in the performance of the

enterprise.

It acts as a basis for calculating the variances in production, overheads, and sales.

It provides for advance planning for the organization (Golooba-Mutebi, and Hickey,

2016).

It also acts as a motivator and controlling element in the business organization.

Discussion on the need of investment appraisal techniques for the financial decision

making in long run

The financial decision-making process is also called the capital budgeting in terms of

financial management. The investment appraisal techniques are the tools and methods of the

ACCOUNTING AND FINANCE 5

capital budgeting that are used by the management for efficient decision making. Various

techniques of capital budgeting are used for efficient investment decision making. Some of

these are explained as below:

Payback Period (PBP): It determines the investment decision by examining the period

in which the project or investment can return the amount initially invested in the

project to the business (Al Ani, 2015). According to this approach, the project which

has the least payback period should be selected for the investment purpose.

Accounting Rate of Return (ARR): The accounting proportion is defined as the

percentage of accounting income earned by the business from the investment project.

This approach suggests that the accounting rate of return for the available alternatives

should be calculated by dividing the accounting profit with the initial investments

made in the project (Chaysin, Daengdej, and Tangjitprom, 2016). According to this

technique, the option with the maximum of the ARR should be selected.

Net Present Value (NPV): It is one of the most important tools of capital budgeting

that is used for making better investment decisions. In the NPV technique, the

investment plan with the highest of the net present value is selected (Champathed,

2015). The NPV is the difference between the present value of the cash inflows and

cash outflows of the business. This method is considered as most effective and used

by different businesses while taking investment appraisal decisions.

Internal Rate of Return (IRR): The internal rate of return is explained as the

percentage of amount which is earned by the project for the business. The project or

investment opportunity which has the highest IRR should be selected for efficient

decision making (Su, Lee, Chou, Yeh, and Thi, 2018). The project with the highest of

IRR will provide the maximum profit to the entity.

capital budgeting that are used by the management for efficient decision making. Various

techniques of capital budgeting are used for efficient investment decision making. Some of

these are explained as below:

Payback Period (PBP): It determines the investment decision by examining the period

in which the project or investment can return the amount initially invested in the

project to the business (Al Ani, 2015). According to this approach, the project which

has the least payback period should be selected for the investment purpose.

Accounting Rate of Return (ARR): The accounting proportion is defined as the

percentage of accounting income earned by the business from the investment project.

This approach suggests that the accounting rate of return for the available alternatives

should be calculated by dividing the accounting profit with the initial investments

made in the project (Chaysin, Daengdej, and Tangjitprom, 2016). According to this

technique, the option with the maximum of the ARR should be selected.

Net Present Value (NPV): It is one of the most important tools of capital budgeting

that is used for making better investment decisions. In the NPV technique, the

investment plan with the highest of the net present value is selected (Champathed,

2015). The NPV is the difference between the present value of the cash inflows and

cash outflows of the business. This method is considered as most effective and used

by different businesses while taking investment appraisal decisions.

Internal Rate of Return (IRR): The internal rate of return is explained as the

percentage of amount which is earned by the project for the business. The project or

investment opportunity which has the highest IRR should be selected for efficient

decision making (Su, Lee, Chou, Yeh, and Thi, 2018). The project with the highest of

IRR will provide the maximum profit to the entity.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING AND FINANCE 6

Conclusion

The study explained the usage and meaning of budget in the business. It has provided the

discussion on the operating budgets which included the meaning and definition of the

operating budget. The various components of operating budgets that are used for the

preparation of the budgeted income statement have been discussed. It contains the points

which define the benefits of master budgets for the enterprise. It has defined the different

investment appraisal techniques which are used by the business enterprises for efficient

financial decision making. It has explained the concepts of IRR, ARR, NPV, and PBP in the

given study. Thus, this study provided an understanding of the different financial and

accounting concepts.

Conclusion

The study explained the usage and meaning of budget in the business. It has provided the

discussion on the operating budgets which included the meaning and definition of the

operating budget. The various components of operating budgets that are used for the

preparation of the budgeted income statement have been discussed. It contains the points

which define the benefits of master budgets for the enterprise. It has defined the different

investment appraisal techniques which are used by the business enterprises for efficient

financial decision making. It has explained the concepts of IRR, ARR, NPV, and PBP in the

given study. Thus, this study provided an understanding of the different financial and

accounting concepts.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING AND FINANCE 7

References

Al Ani, M.K. (2015) A strategic framework to use payback period (PBP) in evaluating the

capital budgeting in energy and oil and gas sectors in Oman. International journal of

economics and financial issues, 5(2), pp.469-475.

Blinova, T. (2016) The improving of the heat networks operating process under the

conditions of the energy efficiency providing. In MATEC Web of Conferences (Vol. 73, p.

07023). EDP Sciences.

Champathed, K. (2015) Capital Budgeting Practice of Thai Firms. Information Management

and Business Review, 7(1), pp.59-66.

Chaysin, P., Daengdej, J. and Tangjitprom, N. (2016) Survey on Available Methods to

Evaluate IT Investment. Electronic Journal Information Systems Evaluation Volume, 19(1).

Golooba-Mutebi, F. and Hickey, S. (2016) The master of institutional multiplicity? The

shifting politics of regime survival, state-building and democratisation in Museveni’s

Uganda. Journal of Eastern African Studies, 10(4), pp.601-618.

Katsinas, S.G., D'Amico, M.M., Friedel, J.N., Adair, J.L., Warner, J.L. and Malley, M.S.

(2016) After the Great Recession: Higher Education's New Normal: An Analysis of National

Surveys of Access and Finance Issues, 2011 to 2015.

Maduekwe, C.C. and Kamala, P. (2016) The use of budgets by small and medium enterprises

in Cape Metropolis, South Africa. Problems and Perspectives in Management, 14(1), pp.183-

191.

References

Al Ani, M.K. (2015) A strategic framework to use payback period (PBP) in evaluating the

capital budgeting in energy and oil and gas sectors in Oman. International journal of

economics and financial issues, 5(2), pp.469-475.

Blinova, T. (2016) The improving of the heat networks operating process under the

conditions of the energy efficiency providing. In MATEC Web of Conferences (Vol. 73, p.

07023). EDP Sciences.

Champathed, K. (2015) Capital Budgeting Practice of Thai Firms. Information Management

and Business Review, 7(1), pp.59-66.

Chaysin, P., Daengdej, J. and Tangjitprom, N. (2016) Survey on Available Methods to

Evaluate IT Investment. Electronic Journal Information Systems Evaluation Volume, 19(1).

Golooba-Mutebi, F. and Hickey, S. (2016) The master of institutional multiplicity? The

shifting politics of regime survival, state-building and democratisation in Museveni’s

Uganda. Journal of Eastern African Studies, 10(4), pp.601-618.

Katsinas, S.G., D'Amico, M.M., Friedel, J.N., Adair, J.L., Warner, J.L. and Malley, M.S.

(2016) After the Great Recession: Higher Education's New Normal: An Analysis of National

Surveys of Access and Finance Issues, 2011 to 2015.

Maduekwe, C.C. and Kamala, P. (2016) The use of budgets by small and medium enterprises

in Cape Metropolis, South Africa. Problems and Perspectives in Management, 14(1), pp.183-

191.

ACCOUNTING AND FINANCE 8

Su, S.H., Lee, H.L., Chou, J.J., Yeh, J.Y. and Thi, M.H.V. (2018) Application and effects of

capital budgeting among the manufacturing companies in Vietnam. International Journal of

Organizational Innovation (Online), 10(4), pp.111-120.

Telecký, M., Čejka, J. and Guchenko, M. (2018) Determining of Provable Loss in Municipal

Bus Transport and Its Influence on Public Budgets in Sparsely Populated Areas of the Czech

Republic. LOGI-Scientific Journal on Transport and Logistics, 9(1), pp.105-113.

Zimmerman, D.M. and House, P. (2016) Medication safety: Simulation education for new

RNs promises an excellent return on investment. Nursing economics, 34(1), p.49.

Su, S.H., Lee, H.L., Chou, J.J., Yeh, J.Y. and Thi, M.H.V. (2018) Application and effects of

capital budgeting among the manufacturing companies in Vietnam. International Journal of

Organizational Innovation (Online), 10(4), pp.111-120.

Telecký, M., Čejka, J. and Guchenko, M. (2018) Determining of Provable Loss in Municipal

Bus Transport and Its Influence on Public Budgets in Sparsely Populated Areas of the Czech

Republic. LOGI-Scientific Journal on Transport and Logistics, 9(1), pp.105-113.

Zimmerman, D.M. and House, P. (2016) Medication safety: Simulation education for new

RNs promises an excellent return on investment. Nursing economics, 34(1), p.49.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCOUNTING AND FINANCE 9

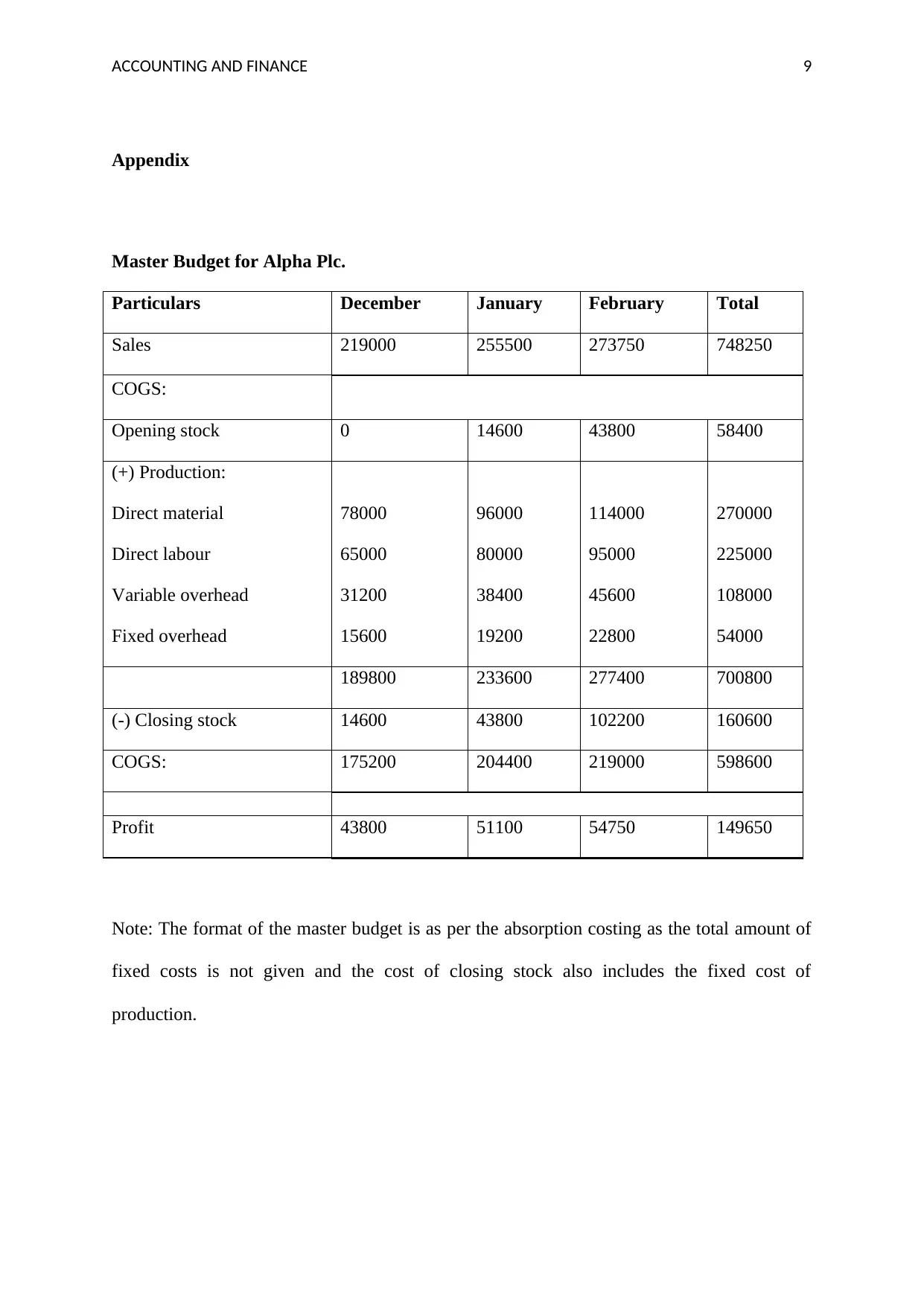

Appendix

Master Budget for Alpha Plc.

Particulars December January February Total

Sales 219000 255500 273750 748250

COGS:

Opening stock 0 14600 43800 58400

(+) Production:

Direct material 78000 96000 114000 270000

Direct labour 65000 80000 95000 225000

Variable overhead 31200 38400 45600 108000

Fixed overhead 15600 19200 22800 54000

189800 233600 277400 700800

(-) Closing stock 14600 43800 102200 160600

COGS: 175200 204400 219000 598600

Profit 43800 51100 54750 149650

Note: The format of the master budget is as per the absorption costing as the total amount of

fixed costs is not given and the cost of closing stock also includes the fixed cost of

production.

Appendix

Master Budget for Alpha Plc.

Particulars December January February Total

Sales 219000 255500 273750 748250

COGS:

Opening stock 0 14600 43800 58400

(+) Production:

Direct material 78000 96000 114000 270000

Direct labour 65000 80000 95000 225000

Variable overhead 31200 38400 45600 108000

Fixed overhead 15600 19200 22800 54000

189800 233600 277400 700800

(-) Closing stock 14600 43800 102200 160600

COGS: 175200 204400 219000 598600

Profit 43800 51100 54750 149650

Note: The format of the master budget is as per the absorption costing as the total amount of

fixed costs is not given and the cost of closing stock also includes the fixed cost of

production.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.