Accounting Theory and Issues: Afterpay Financial Reporting Analysis

VerifiedAdded on 2020/03/16

|10

|2474

|38

Report

AI Summary

This report provides an executive summary and detailed analysis of Afterpay Limited's accounting policies and financial reporting practices. It begins by identifying key accounting policies, including those related to AASB and IFRS standards, and assesses the company's accounting flexibility and strategic choices. The report evaluates the quality of financial disclosures, highlighting the importance of transparency and compliance with accounting frameworks. It then identifies potential red flags within Afterpay's annual report, such as non-compliance with standard amendments, unusual revenue and trade receivables increases, and the impact of mergers. The report concludes by examining Afterpay's adherence to the conceptual framework of financial reporting, emphasizing the significance of normative theory in selecting relevant accounting procedures. The analysis covers various aspects of the company's financial statements, including segment disclosures and related party transactions, offering a comprehensive overview of Afterpay's accounting practices.

Accounting Theory and Issues

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The report has been developed for demonstrating the significance of adopting standard

accounting policies for developing high-quality financial reports. In this context, the annual

disclosures of an ASX listed company that is Afterpay Limited, has been examined and

evaluated in the present report. This is done for developing an understanding of the accounting

policies adopted by the company for development of its financial reports.

The report has been developed for demonstrating the significance of adopting standard

accounting policies for developing high-quality financial reports. In this context, the annual

disclosures of an ASX listed company that is Afterpay Limited, has been examined and

evaluated in the present report. This is done for developing an understanding of the accounting

policies adopted by the company for development of its financial reports.

Introduction

The company Afterpay Touch Group Limited was incorporated for the purpose of merger

between Touchgroup Limited and Afterpay Holdings Limited. The company came into existence

on 30 March 2017. The company has experienced an incredible journey of from Afterpay to now

Afterpay Touch (Annual Report, 2017). The company is driven by passion and compassion to

serve its customers the best retail experience. Since its commercialization in the year 2015 there

are various and rapid changes that have taken place in the company. The company has grown

rapidly and its initial public offering has also been launched in the year 2016. In this short period

of time the company has partnered with the most privilege retail brands of Australia and also

many global leading brands that have helped the company to become the first choice of its

customers. The company has become Australia leading Buy Now and Pay Later service (Annual

Report, 2017). The company has successfully created a retail community which is delivering

incremental value to all its customers and key stakeholders. The report analyses the major

accounting policies that has been used by the firm and the manner in which its financial

statements are prepared. In addition to this to gain a better perspective, various other areas are

also analyzed and assessed.

Section 1: Identify Key Accounting Policies

The financial statements presented by the company Afterpay Touch has been prepared in

accordance with the standards and norms explained by the AASB. The securities of the Afterpay

Touch company is listed on the Australian Securities Exchange ltd. In June 2017 the company

has completed its merger of Afterpay Holdings Ltd and Touchcorp Ltd. The accounting policies

of the company are in compliance with the guidelines prescribed by the Australian Accounting

Standards Board and other authoritative pronouncements of the Australian Board (Annual

Report, 2017). The financial statements are prepared on the basis of historical cost. The

company is also following the accounting policies discussed by the IFRS (International Financial

Reporting Standards).

Afterpay Touch’s major accounting policy is AASB 2014-4 which constitutes of

Acceptable Methods of Depreciation and Amortization. The accounting policy has been

amended, once it was called AASB116 and AASB 138. In addition to this there are other

The company Afterpay Touch Group Limited was incorporated for the purpose of merger

between Touchgroup Limited and Afterpay Holdings Limited. The company came into existence

on 30 March 2017. The company has experienced an incredible journey of from Afterpay to now

Afterpay Touch (Annual Report, 2017). The company is driven by passion and compassion to

serve its customers the best retail experience. Since its commercialization in the year 2015 there

are various and rapid changes that have taken place in the company. The company has grown

rapidly and its initial public offering has also been launched in the year 2016. In this short period

of time the company has partnered with the most privilege retail brands of Australia and also

many global leading brands that have helped the company to become the first choice of its

customers. The company has become Australia leading Buy Now and Pay Later service (Annual

Report, 2017). The company has successfully created a retail community which is delivering

incremental value to all its customers and key stakeholders. The report analyses the major

accounting policies that has been used by the firm and the manner in which its financial

statements are prepared. In addition to this to gain a better perspective, various other areas are

also analyzed and assessed.

Section 1: Identify Key Accounting Policies

The financial statements presented by the company Afterpay Touch has been prepared in

accordance with the standards and norms explained by the AASB. The securities of the Afterpay

Touch company is listed on the Australian Securities Exchange ltd. In June 2017 the company

has completed its merger of Afterpay Holdings Ltd and Touchcorp Ltd. The accounting policies

of the company are in compliance with the guidelines prescribed by the Australian Accounting

Standards Board and other authoritative pronouncements of the Australian Board (Annual

Report, 2017). The financial statements are prepared on the basis of historical cost. The

company is also following the accounting policies discussed by the IFRS (International Financial

Reporting Standards).

Afterpay Touch’s major accounting policy is AASB 2014-4 which constitutes of

Acceptable Methods of Depreciation and Amortization. The accounting policy has been

amended, once it was called AASB116 and AASB 138. In addition to this there are other

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

accounting principles and standards used by the business organsation. The company is also

following AASB 2015-3, which is an amendment to the Australian Accounting Standards arising

from the withdrawal of AASB 1031 Materiality (Annual Report, 2017). Apart from this AASB

2015-4, amendment to Australian Accounting Standard is also implemented which requires

financial reporting requirement for Australian groups that have a parent company in foreign.

After adopting these standards and accounting policies the financial statement of the company

has become more effective and requires fewer changes to be made.

In addition to this there are some other accounting policies that are being use by the

company such as AASB 9. This accounting policy has replaced the AASB 139. This accounting

policy includes the classification and measurements of expected loss occurred through the

damage of assets. AASB 15 is also implemented in the accounting policies; it is related with the

revenue from contracts with the customers (Annual Report, 2017). This accounting policy is

made in compliance with the IFRS and international Accounting Standards Board (IASB). This

method specifies the revenue that has been raised from the revenue contracts.

Section 2: Assess Accounting Flexibility

The company after merger has become more competitive and efficient in its operations.

The top level management of the company has become more responsible towards their decision

making power. The company has also showed responsible behavior towards its customer base.

The management of the company is the one which is responsible for the implementation of the

accounting policies in the company. In Afterpay Touch the task of formulating accounting policy

is also done by the top management of the company (Annual Report, 2017). Before formulating

the accounting policies, the top level management analyses varied spectrum of the information

and data about the accounting standards that are prevalent in the regional and in the international

market. It is quite important for a business organsation to select and adopt such accounting

policy that works in compliance with the international standards because it is very significant to

maintain harmony in the accounting principles.

The organization Afterpay Touch has adopted various kinds of accounting policies which

is popular in the international market in order to remain competitive and efficient in

performance. The company is working on the guidelines of AASB and in addition to this the

following AASB 2015-3, which is an amendment to the Australian Accounting Standards arising

from the withdrawal of AASB 1031 Materiality (Annual Report, 2017). Apart from this AASB

2015-4, amendment to Australian Accounting Standard is also implemented which requires

financial reporting requirement for Australian groups that have a parent company in foreign.

After adopting these standards and accounting policies the financial statement of the company

has become more effective and requires fewer changes to be made.

In addition to this there are some other accounting policies that are being use by the

company such as AASB 9. This accounting policy has replaced the AASB 139. This accounting

policy includes the classification and measurements of expected loss occurred through the

damage of assets. AASB 15 is also implemented in the accounting policies; it is related with the

revenue from contracts with the customers (Annual Report, 2017). This accounting policy is

made in compliance with the IFRS and international Accounting Standards Board (IASB). This

method specifies the revenue that has been raised from the revenue contracts.

Section 2: Assess Accounting Flexibility

The company after merger has become more competitive and efficient in its operations.

The top level management of the company has become more responsible towards their decision

making power. The company has also showed responsible behavior towards its customer base.

The management of the company is the one which is responsible for the implementation of the

accounting policies in the company. In Afterpay Touch the task of formulating accounting policy

is also done by the top management of the company (Annual Report, 2017). Before formulating

the accounting policies, the top level management analyses varied spectrum of the information

and data about the accounting standards that are prevalent in the regional and in the international

market. It is quite important for a business organsation to select and adopt such accounting

policy that works in compliance with the international standards because it is very significant to

maintain harmony in the accounting principles.

The organization Afterpay Touch has adopted various kinds of accounting policies which

is popular in the international market in order to remain competitive and efficient in

performance. The company is working on the guidelines of AASB and in addition to this the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

company has also adopted accounting policies that are in compliance with the IFRS (Annual

Report, 2017). In addition to this the company has also formulated its accounting policies in

compliance with the Accounting Standards of America. This shows the company has adopted a

flexible approach towards the accounting policies. However this approach is completely valid as

this is a kind of consolidated approach of all the known accounting standards (Wolk, Dodd and

Rozycki, 2012). This is being done in order to gain competitive edge over its competitors and

achieve efficiency in its performance so that it can become more competitive in the international

market.

Section 3: Evaluate Accounting Strategy

The flexibility in the accounting policies allows the managers to plan their future courses

of action in a strategic manner. The company is facing acute competition with Zippay. It is

another company operating in Australia and is serving its customers with the same concept of

buying before and paying for the same later period. The company has also gained a large

customer base and is giving tough competition to Afterpay Touch. The accounting norms of

Zippay are quite different from Afterpay Touch (Review of Buy Now Pay Later Solutions for

Australian Merchants – Afterpay Vs Zippay, 2017) The company has prepared its financial

statement in accordance with the Corporations Act 2001 (Annual Report 2016). Zippay’s

accounting principles are made in compliance with the AASB and IFRS, whereas, Afterpay

Touch has formulated its accounting policies in accordance to both AASB and IFRS, apart from

this it also has also made its accounting policies on the guidelines of Accounting Standards of

America. This made Afterpay Touch more efficient and effective in the international market.

The company has constructed a Remuneration Committee in which a fixed remuneration

and variable remuneration for short term or long term incentive is established for the managers

and executive officers. For the purpose of distributing and deciding revenue an external

individual is appointed so that no bias decision can be made (Sheridan, 2016). A Share based

plan is also formulated by the organsation in which the share option plan is made in order to

align the objective of the firm with the individual objectives. The management of the company

has identified some accounting policies for which significant judgment and estimates are made.

Share based payment transactions is one area for the same. The accounting estimates and

assumptions related to equity settled share based payments would have no impact on the carrying

Report, 2017). In addition to this the company has also formulated its accounting policies in

compliance with the Accounting Standards of America. This shows the company has adopted a

flexible approach towards the accounting policies. However this approach is completely valid as

this is a kind of consolidated approach of all the known accounting standards (Wolk, Dodd and

Rozycki, 2012). This is being done in order to gain competitive edge over its competitors and

achieve efficiency in its performance so that it can become more competitive in the international

market.

Section 3: Evaluate Accounting Strategy

The flexibility in the accounting policies allows the managers to plan their future courses

of action in a strategic manner. The company is facing acute competition with Zippay. It is

another company operating in Australia and is serving its customers with the same concept of

buying before and paying for the same later period. The company has also gained a large

customer base and is giving tough competition to Afterpay Touch. The accounting norms of

Zippay are quite different from Afterpay Touch (Review of Buy Now Pay Later Solutions for

Australian Merchants – Afterpay Vs Zippay, 2017) The company has prepared its financial

statement in accordance with the Corporations Act 2001 (Annual Report 2016). Zippay’s

accounting principles are made in compliance with the AASB and IFRS, whereas, Afterpay

Touch has formulated its accounting policies in accordance to both AASB and IFRS, apart from

this it also has also made its accounting policies on the guidelines of Accounting Standards of

America. This made Afterpay Touch more efficient and effective in the international market.

The company has constructed a Remuneration Committee in which a fixed remuneration

and variable remuneration for short term or long term incentive is established for the managers

and executive officers. For the purpose of distributing and deciding revenue an external

individual is appointed so that no bias decision can be made (Sheridan, 2016). A Share based

plan is also formulated by the organsation in which the share option plan is made in order to

align the objective of the firm with the individual objectives. The management of the company

has identified some accounting policies for which significant judgment and estimates are made.

Share based payment transactions is one area for the same. The accounting estimates and

assumptions related to equity settled share based payments would have no impact on the carrying

amount of assets and liabilities (Annual Report, 2017). In addition to this, estimation of useful

lives of intangible assets is another aspect in which adjustments regarding the judgments and

estimations are done.

The damage to intangible assets, the carrying cost of the intangible asset is analyzed

against its recoverable amount. Assumptions, judgments and estimations are used in the

calculation aspect. Another aspect of estimations and judgment is calculated in the taxation

aspect of the firm. Differences arising between the actual results and the estimations made. This

can also make changes in the future adjustments of taxes (Annual Report, 2017). The accounting

policies of the Afterpay Touch is formulated and designed by the top level management. They

are formulated in such a way that they can help the company in achieving their long term and

short term objective in an effective manner.

Section 4: Evaluate the Quality of Disclosure

The disclosure provided is quite adequate and it has covered various aspects of the

company. The financial statements have provided a detailed analysis of several aspects that can

help the firm in gaining competitive edge in the market (Mintz, 2013). The footnotes have

provided information about the accounting policies that has been followed in the firm. In

addition to this, it has also discussed the amendments that have been done in the accounting

policies. The accounting policies and standards followed in the firm were based on GAAP

standard either directly or indirectly and it did not restrict the firm (Walton, 2011). The segment

disclosure has covered various aspects and has explained the same in detailed manner. The

segment aspect has discussed that the date for merger was decided to be 30th June and the

statements of Comprehensive Income includes only the transactions of the company (Annual

Report, 2017).

Section 5: Identify Potential Red Flags

The annual report of Afterpay though provides all the necessary financial information

required by the end-users for making decisions. However, there are some issues of concern

identified in the annual report of the company that requires more disclosure discussed as red

flags in the present section. There is some unexplained changes in accounting such as the

company is not yet complying with the changes made in the methods of calculating deprecation

lives of intangible assets is another aspect in which adjustments regarding the judgments and

estimations are done.

The damage to intangible assets, the carrying cost of the intangible asset is analyzed

against its recoverable amount. Assumptions, judgments and estimations are used in the

calculation aspect. Another aspect of estimations and judgment is calculated in the taxation

aspect of the firm. Differences arising between the actual results and the estimations made. This

can also make changes in the future adjustments of taxes (Annual Report, 2017). The accounting

policies of the Afterpay Touch is formulated and designed by the top level management. They

are formulated in such a way that they can help the company in achieving their long term and

short term objective in an effective manner.

Section 4: Evaluate the Quality of Disclosure

The disclosure provided is quite adequate and it has covered various aspects of the

company. The financial statements have provided a detailed analysis of several aspects that can

help the firm in gaining competitive edge in the market (Mintz, 2013). The footnotes have

provided information about the accounting policies that has been followed in the firm. In

addition to this, it has also discussed the amendments that have been done in the accounting

policies. The accounting policies and standards followed in the firm were based on GAAP

standard either directly or indirectly and it did not restrict the firm (Walton, 2011). The segment

disclosure has covered various aspects and has explained the same in detailed manner. The

segment aspect has discussed that the date for merger was decided to be 30th June and the

statements of Comprehensive Income includes only the transactions of the company (Annual

Report, 2017).

Section 5: Identify Potential Red Flags

The annual report of Afterpay though provides all the necessary financial information

required by the end-users for making decisions. However, there are some issues of concern

identified in the annual report of the company that requires more disclosure discussed as red

flags in the present section. There is some unexplained changes in accounting such as the

company is not yet complying with the changes made in the methods of calculating deprecation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and amortization as per amendments introduced in AASB 116 and AASB 138. The company has

stated in its annual report that the amendments made in AASB standards are not yet effective in

the current reporting period of the company. As such, the company needs to provide more

disclosure regarding the reasons for its non-compliance with the AASB standards amendments.

There is also unusual increase in the revenue amount of the company in the year 2017 as

analyzed from its income statement that requires proper disclosure explaining the transactions

that lead to huge increase in its gross profit in the year 2017that can be depicted as follows from

the income statement (Annual Report: Afterpay, 2017):

Source: https://www.afterpaytouch.com/images/APT_2017_4E_Annual-Report.pdf

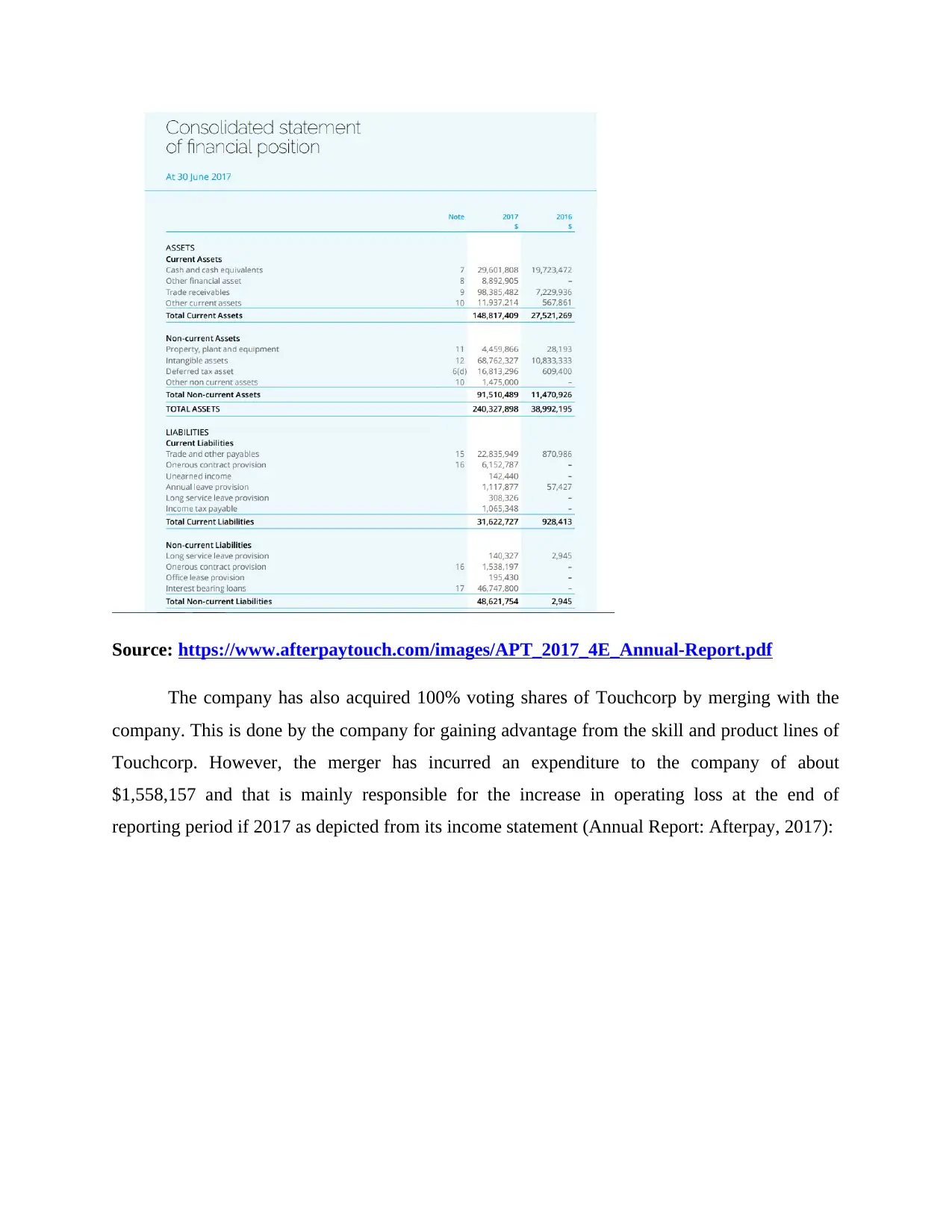

Also, there is unusual increase in its trade receivables of the company in the year 2017 as

compared to the year 2016 depicted from its balance sheet as follows:

stated in its annual report that the amendments made in AASB standards are not yet effective in

the current reporting period of the company. As such, the company needs to provide more

disclosure regarding the reasons for its non-compliance with the AASB standards amendments.

There is also unusual increase in the revenue amount of the company in the year 2017 as

analyzed from its income statement that requires proper disclosure explaining the transactions

that lead to huge increase in its gross profit in the year 2017that can be depicted as follows from

the income statement (Annual Report: Afterpay, 2017):

Source: https://www.afterpaytouch.com/images/APT_2017_4E_Annual-Report.pdf

Also, there is unusual increase in its trade receivables of the company in the year 2017 as

compared to the year 2016 depicted from its balance sheet as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Source: https://www.afterpaytouch.com/images/APT_2017_4E_Annual-Report.pdf

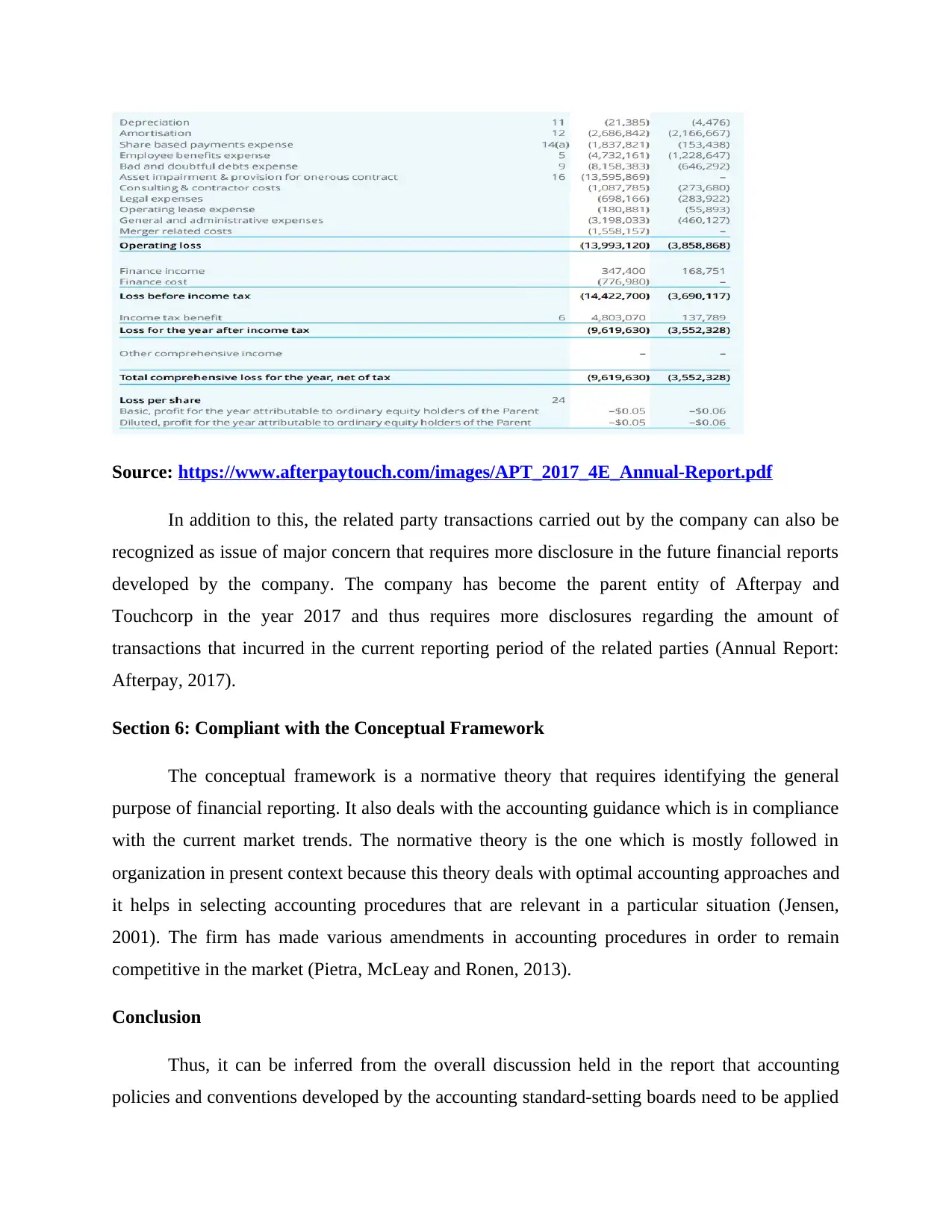

The company has also acquired 100% voting shares of Touchcorp by merging with the

company. This is done by the company for gaining advantage from the skill and product lines of

Touchcorp. However, the merger has incurred an expenditure to the company of about

$1,558,157 and that is mainly responsible for the increase in operating loss at the end of

reporting period if 2017 as depicted from its income statement (Annual Report: Afterpay, 2017):

The company has also acquired 100% voting shares of Touchcorp by merging with the

company. This is done by the company for gaining advantage from the skill and product lines of

Touchcorp. However, the merger has incurred an expenditure to the company of about

$1,558,157 and that is mainly responsible for the increase in operating loss at the end of

reporting period if 2017 as depicted from its income statement (Annual Report: Afterpay, 2017):

Source: https://www.afterpaytouch.com/images/APT_2017_4E_Annual-Report.pdf

In addition to this, the related party transactions carried out by the company can also be

recognized as issue of major concern that requires more disclosure in the future financial reports

developed by the company. The company has become the parent entity of Afterpay and

Touchcorp in the year 2017 and thus requires more disclosures regarding the amount of

transactions that incurred in the current reporting period of the related parties (Annual Report:

Afterpay, 2017).

Section 6: Compliant with the Conceptual Framework

The conceptual framework is a normative theory that requires identifying the general

purpose of financial reporting. It also deals with the accounting guidance which is in compliance

with the current market trends. The normative theory is the one which is mostly followed in

organization in present context because this theory deals with optimal accounting approaches and

it helps in selecting accounting procedures that are relevant in a particular situation (Jensen,

2001). The firm has made various amendments in accounting procedures in order to remain

competitive in the market (Pietra, McLeay and Ronen, 2013).

Conclusion

Thus, it can be inferred from the overall discussion held in the report that accounting

policies and conventions developed by the accounting standard-setting boards need to be applied

In addition to this, the related party transactions carried out by the company can also be

recognized as issue of major concern that requires more disclosure in the future financial reports

developed by the company. The company has become the parent entity of Afterpay and

Touchcorp in the year 2017 and thus requires more disclosures regarding the amount of

transactions that incurred in the current reporting period of the related parties (Annual Report:

Afterpay, 2017).

Section 6: Compliant with the Conceptual Framework

The conceptual framework is a normative theory that requires identifying the general

purpose of financial reporting. It also deals with the accounting guidance which is in compliance

with the current market trends. The normative theory is the one which is mostly followed in

organization in present context because this theory deals with optimal accounting approaches and

it helps in selecting accounting procedures that are relevant in a particular situation (Jensen,

2001). The firm has made various amendments in accounting procedures in order to remain

competitive in the market (Pietra, McLeay and Ronen, 2013).

Conclusion

Thus, it can be inferred from the overall discussion held in the report that accounting

policies and conventions developed by the accounting standard-setting boards need to be applied

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

by the businesses for developing the financial reports. This is essential to promote transparency

in the business operations and thus achieve the trust of shareholders.

References

Annual Report 2016. Zip Money. [Online] Available at:

file:///C:/Users/user/Downloads/nASX4v6RFb_ZML_1476166439.pdf

Annual Report. 2017. Afterpay Touch Group Limited. [Online] Available at:

https://www.afterpaytouch.com/images/APT_2017_4E_Annual-Report.pdf

Jensen, M.C. 2001. Foundations of Organizational Strategy. Harvard University Press.

Mintz, S. 2013. Accounting for the Public Interest: Perspectives on Accountability,

Professionalism and Role in Society. Springer Science & Business Media.

Pietra, R., McLeay, S and Ronen, J. 2013. Accounting and Regulation: New Insights on

Governance, Markets and Institutions. Springer Science & Business Media.

Review of Buy Now Pay Later Solutions for Australian Merchants – Afterpay Vs Zippay. 2017.

[Online] Available at: https://magenable.com.au/researches-2/review-of-buy-now-pay-later-

solutions-for-australian-merchants -afterpay-zippay-touch-payments/

Sheridan, T. 2016. Managerial Fraud: Executive Impression Management, Beyond Red Flags.

Routledge.

Walton, P. 2011. A Global History of Accounting, Financial Reporting and Public Policy: Asia

and Oceania. Emerald Group Publishing.

Wolk, H.I., Dodd, J.L. and Rozycki, J.J. 2012. Accounting Theory: Conceptual Issues in a

Political and Economic Environment. SAGE.

in the business operations and thus achieve the trust of shareholders.

References

Annual Report 2016. Zip Money. [Online] Available at:

file:///C:/Users/user/Downloads/nASX4v6RFb_ZML_1476166439.pdf

Annual Report. 2017. Afterpay Touch Group Limited. [Online] Available at:

https://www.afterpaytouch.com/images/APT_2017_4E_Annual-Report.pdf

Jensen, M.C. 2001. Foundations of Organizational Strategy. Harvard University Press.

Mintz, S. 2013. Accounting for the Public Interest: Perspectives on Accountability,

Professionalism and Role in Society. Springer Science & Business Media.

Pietra, R., McLeay, S and Ronen, J. 2013. Accounting and Regulation: New Insights on

Governance, Markets and Institutions. Springer Science & Business Media.

Review of Buy Now Pay Later Solutions for Australian Merchants – Afterpay Vs Zippay. 2017.

[Online] Available at: https://magenable.com.au/researches-2/review-of-buy-now-pay-later-

solutions-for-australian-merchants -afterpay-zippay-touch-payments/

Sheridan, T. 2016. Managerial Fraud: Executive Impression Management, Beyond Red Flags.

Routledge.

Walton, P. 2011. A Global History of Accounting, Financial Reporting and Public Policy: Asia

and Oceania. Emerald Group Publishing.

Wolk, H.I., Dodd, J.L. and Rozycki, J.J. 2012. Accounting Theory: Conceptual Issues in a

Political and Economic Environment. SAGE.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.