Advanced Financial Accounting Report: Afterpay Touch Evaluation

VerifiedAdded on 2022/08/25

|12

|2775

|21

Report

AI Summary

This report provides a comprehensive analysis of Afterpay Touch Group's financial statements, focusing on its classification as a reporting entity and the application of key accounting principles. The analysis begins with an introduction that sets the scope of the study, followed by a detailed discussion of the reporting entity concept, including its definition and criteria. The report then evaluates Afterpay Touch's financial characteristics, size, and indebtedness to determine if it meets the requirements of a reporting entity. Furthermore, the report examines the relevance and faithful representation of financial information, considering the qualitative characteristics of useful information as defined in the conceptual framework. The report assesses whether the financial information disclosed by Afterpay Touch is relevant and faithfully represented, evaluating the unit of measurement basis, recognition criteria, and factors considered when selecting the measurement basis. The report concludes by summarizing the key findings and implications of the analysis.

Running head: ADVANCED FINANCIAL ACCOUNTING

Advanced financial accounting

Name of the Student

Name of the University

Author Note

Advanced financial accounting

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED FINANCIAL ACCOUNTING

Table of Contents

Introduction:..................................................................................................................1

Discussion:...................................................................................................................2

Description of reporting entity:......................................................................................2

Evaluating the criteria of reporting entity of AfterPay touch limited:.............................2

Describing the relevance and faithful representation in relation to the useful

information of the financial statements:........................................................................3

Conclusion:...................................................................................................................4

References list:.............................................................................................................5

Table of Contents

Introduction:..................................................................................................................1

Discussion:...................................................................................................................2

Description of reporting entity:......................................................................................2

Evaluating the criteria of reporting entity of AfterPay touch limited:.............................2

Describing the relevance and faithful representation in relation to the useful

information of the financial statements:........................................................................3

Conclusion:...................................................................................................................4

References list:.............................................................................................................5

ADVANCED FINANCIAL ACCOUNTING

Introduction:

The study is undertaken to provide a detailed discussion on the criteria and

the factors of reporting entity and evaluating the fact that the chosen company is a

reporting entity or not. The selected company for analysing its criteria of reporting

entity or not is AfterPay Touch group which is a payment company driven by

technology operating globally. It was in June, 2017, Afterpay Touch was established

after the merger of Touch group and Afterpay. The financial report published by the

company has been assessed for evaluating the faithful representation and relevance

in relation to the useful information.

Discussion:

Description of reporting entity:

The system of differential reporting by the entities in Australia is founded by

the concept of reporting entity. The issue pertaining to differential reporting was

addressed by IASB (International accounting standard board) and in this regard, the

concept of reporting entities and its principles was proposed in the exposure draft.

Reporting entities concept was introduced for ensuing that the financial reports

based on full GAAP is prepared by more economically, larger and politically

significant entities (Aasb.gov.au 2020).

Any organization can be categorized into a reporting entity if they can produce

the general purpose financial reports. Any organization or entity cannot be qualified

as reporting entity because of statutory authority, organizational structure and

creation of company. For an entity being classified as reporting entity so that it fulfils

all the criteria requires to make the judgment. All the entities of which the users gain

information from the general purpose financial reports that assist them in evaluation

and making of the decision regarding the allocation of the scarce resources

available. It is important and required by all the reporting entities to prepare general

purpose financial reports” (Birt et al. 2019). Preparation of such reports should be

done complying with the requirement of the accounting standards and accounting

concepts statement. Entities producing less complicated financial reports and special

purpose financial reports that does not complies with the accounting standards or

are based on lesser reporting standards are not classified as reporting entities.

Therefore, the classification of entities as reporting entities is primary dependent on

the fact of the dependency of the potential users of the financial statements of the

users on the financial reports issued for general report to base their investment

decisions. The principle guiding the classification of entity as reporting entity is the

separation of economic interest from the management and the entities more

financially, economically and politically significant, it is more likely that the users

would be dependent upon their financial statements to base their decisions (Adams

et al. 2017).

Evaluating the criteria of reporting entity of AfterPay touch limited:

The fulfilment of criteria to be classified as a reporting entity has been

evaluated by reviewing notes to the financial statements and the financial report

published by AfterPay Touch Group. AfterPay touch group was established as a

profit entity and the concept being tied to the objectives of general purpose financial

Introduction:

The study is undertaken to provide a detailed discussion on the criteria and

the factors of reporting entity and evaluating the fact that the chosen company is a

reporting entity or not. The selected company for analysing its criteria of reporting

entity or not is AfterPay Touch group which is a payment company driven by

technology operating globally. It was in June, 2017, Afterpay Touch was established

after the merger of Touch group and Afterpay. The financial report published by the

company has been assessed for evaluating the faithful representation and relevance

in relation to the useful information.

Discussion:

Description of reporting entity:

The system of differential reporting by the entities in Australia is founded by

the concept of reporting entity. The issue pertaining to differential reporting was

addressed by IASB (International accounting standard board) and in this regard, the

concept of reporting entities and its principles was proposed in the exposure draft.

Reporting entities concept was introduced for ensuing that the financial reports

based on full GAAP is prepared by more economically, larger and politically

significant entities (Aasb.gov.au 2020).

Any organization can be categorized into a reporting entity if they can produce

the general purpose financial reports. Any organization or entity cannot be qualified

as reporting entity because of statutory authority, organizational structure and

creation of company. For an entity being classified as reporting entity so that it fulfils

all the criteria requires to make the judgment. All the entities of which the users gain

information from the general purpose financial reports that assist them in evaluation

and making of the decision regarding the allocation of the scarce resources

available. It is important and required by all the reporting entities to prepare general

purpose financial reports” (Birt et al. 2019). Preparation of such reports should be

done complying with the requirement of the accounting standards and accounting

concepts statement. Entities producing less complicated financial reports and special

purpose financial reports that does not complies with the accounting standards or

are based on lesser reporting standards are not classified as reporting entities.

Therefore, the classification of entities as reporting entities is primary dependent on

the fact of the dependency of the potential users of the financial statements of the

users on the financial reports issued for general report to base their investment

decisions. The principle guiding the classification of entity as reporting entity is the

separation of economic interest from the management and the entities more

financially, economically and politically significant, it is more likely that the users

would be dependent upon their financial statements to base their decisions (Adams

et al. 2017).

Evaluating the criteria of reporting entity of AfterPay touch limited:

The fulfilment of criteria to be classified as a reporting entity has been

evaluated by reviewing notes to the financial statements and the financial report

published by AfterPay Touch Group. AfterPay touch group was established as a

profit entity and the concept being tied to the objectives of general purpose financial

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

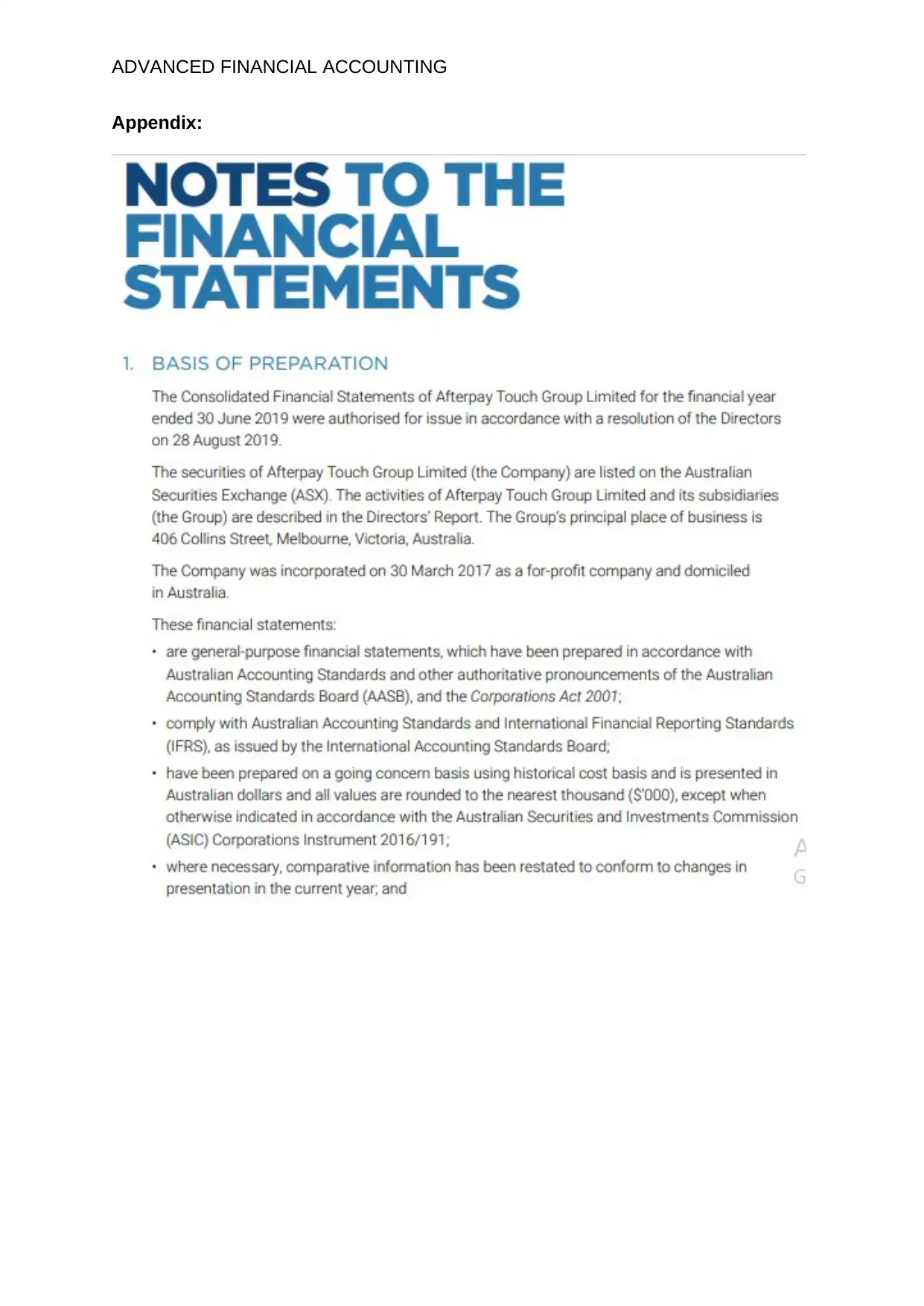

ADVANCED FINANCIAL ACCOUNTING

reporting. Financial report of the company is prepared by complying with the

requirements of the general purpose financial report” (Afterpaytouch.com 2020).

AfterPay prepares general purpose financial statements that complies with the

requirements and other authoritative pronouncements of AASB (Australian

accounting standard board). In addition to this, entity has used a going concern basis

of accounting using historical cost. Any necessary and comparative information has

been restated s that ant changes in the presentation of the information is conformed.

It can be inferred from the fact that the company prepares general purpose financial

statements is that the users base their economic decisions based on the information

provided in the financial report (Herath and Albarqi 2017).

The financial statements establishing the reporting entity concept is found to

be associated with the information requirements of the users of the statements of

AfterPay Touch group in evaluating and making the decision of resource allocation.

In addition to this, the reporting entity boundaries is determined for the information

provision for the purpose outlined in the criteria. Afterpay Touch group comprise of a

group of entities and all the other entities are controlled by one of the entities within

the group so that their objectives are consistent (Afterpaytouch.com 2020).

Another factor evaluating the dependency of users on the general purpose

financial statements for allocating the resources is the size of the firm and its

indebtedness. Greater the size of indebtedness and greater the size of the firm,

users are more likely to depend upon such financial statements to base their

investment decision. It is quite evident from the consolidated statement of financial

position of Afterpay Touch that the total level of indebtedness in the current reporting

year has increased considerably along with increase in the total size of the company.

This has the implication from one of the factors determining the reporting entity

concept that users or investors are reliable on the financial statements produced by

the entity to base their decision. The particular basis represents the financial

characteristics of establishing the decision using the general purpose financial

reports (Afterpaytouch.com 2020). From the overall analysis of the facts gathered

from the financial report, it is inferred that Afterpay Touch Group is classified as a

reporting entity.

Describing the relevance and faithful representation in relation to the useful

information of the financial statements:

The qualitative characteristics of the useful information is set out in the

conceptual framework. The two fundamental qualitative characteristics determining

the understandability, timeliness, comparability and verifiability of the financial

information provided by the reporting entities are faithful representation and

faithfulness. The decision making requirement of the users are supposed to be

relevant to the given financial information. The auditors and the accountants of the

organization need to be focused on the financial information which impacts the

user’s decision. The primary need of the organization is expected to have a fair and

faithful representation which in order words can be said to be free from any

misstatements. On other hand, faithful representation is the most primary feature

which requires the financial information to be honest and fair meaning it should be

free from all kinds of misstatements. A balance is stroke between faithful

representation and faithfulness so that the users are provided with the useful

financial information (Janowicz 2018). It is required by the reporting entity to replace

reporting. Financial report of the company is prepared by complying with the

requirements of the general purpose financial report” (Afterpaytouch.com 2020).

AfterPay prepares general purpose financial statements that complies with the

requirements and other authoritative pronouncements of AASB (Australian

accounting standard board). In addition to this, entity has used a going concern basis

of accounting using historical cost. Any necessary and comparative information has

been restated s that ant changes in the presentation of the information is conformed.

It can be inferred from the fact that the company prepares general purpose financial

statements is that the users base their economic decisions based on the information

provided in the financial report (Herath and Albarqi 2017).

The financial statements establishing the reporting entity concept is found to

be associated with the information requirements of the users of the statements of

AfterPay Touch group in evaluating and making the decision of resource allocation.

In addition to this, the reporting entity boundaries is determined for the information

provision for the purpose outlined in the criteria. Afterpay Touch group comprise of a

group of entities and all the other entities are controlled by one of the entities within

the group so that their objectives are consistent (Afterpaytouch.com 2020).

Another factor evaluating the dependency of users on the general purpose

financial statements for allocating the resources is the size of the firm and its

indebtedness. Greater the size of indebtedness and greater the size of the firm,

users are more likely to depend upon such financial statements to base their

investment decision. It is quite evident from the consolidated statement of financial

position of Afterpay Touch that the total level of indebtedness in the current reporting

year has increased considerably along with increase in the total size of the company.

This has the implication from one of the factors determining the reporting entity

concept that users or investors are reliable on the financial statements produced by

the entity to base their decision. The particular basis represents the financial

characteristics of establishing the decision using the general purpose financial

reports (Afterpaytouch.com 2020). From the overall analysis of the facts gathered

from the financial report, it is inferred that Afterpay Touch Group is classified as a

reporting entity.

Describing the relevance and faithful representation in relation to the useful

information of the financial statements:

The qualitative characteristics of the useful information is set out in the

conceptual framework. The two fundamental qualitative characteristics determining

the understandability, timeliness, comparability and verifiability of the financial

information provided by the reporting entities are faithful representation and

faithfulness. The decision making requirement of the users are supposed to be

relevant to the given financial information. The auditors and the accountants of the

organization need to be focused on the financial information which impacts the

user’s decision. The primary need of the organization is expected to have a fair and

faithful representation which in order words can be said to be free from any

misstatements. On other hand, faithful representation is the most primary feature

which requires the financial information to be honest and fair meaning it should be

free from all kinds of misstatements. A balance is stroke between faithful

representation and faithfulness so that the users are provided with the useful

financial information (Janowicz 2018). It is required by the reporting entity to replace

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED FINANCIAL ACCOUNTING

the information having high degree of uncertainty with the information that has fewer

uncertainty when it comes to providing explanations (Ifrs.org 2020). The substance

of financial information must be represented faithfully and should be relevant so as to

make such information useful.

Measurement basis of organization should be selected accounting for the key

characteristics of financial information such as faithful representation and usefulness.

Information disclosed in the financial report of the entity is regarded as relevant if it

can cause a difference to the user’s decision and for this such information should

have confirmatory or predictive value. On other hand, information is regarded to be

represented faithfully if it is neutral, complete and error free to the maximum extent

possible. Any uncertainty in the level of measurement affects the faithful

representation of information. A faithful representation of any event or transaction

that has caused arising of any income, assets, expenses or liabilities is provided by

the unit of account. An information that is represented faithfully need not be accurate

in all the respect and usefulness of the financial information should not be weakened

by the use of estimates that forms an important and essential part of preparing the

financial statements (Iasplus.com 2020).

Relevance of information is determined by choosing a unit of account so that

users are provided with the relevant information about liabilities and assets and any

related expenses and income. The recognition criteria also determines the relevance

of information such as whether any recognition criteria causes any existence of

uncertainty or flow of any economic benefits has a low probability ( Ifrs.org 2020). In

addition to this, whether there is any faithful representation of recognizing any item

and the representation is affected by recognition uncertainty, measurement

uncertainty and disclosure and presentation. Reporting entity when selecting the

basis of measurement should have a faithful representation and relevant in order to

enhance the qualitative characteristics of the information’s provided to the users

(Velte and Stawinoga 2017). Some factors impacting the faithful representation of

the information disclosed includes inconsistency in recognition, measurement

uncertainty and disclosure and presentation. Any liabilities or assets that is faithfully

represented is required to be derecognized with appropriate disclosure and

presentation

Whether the information produced or disclosed by Afterpay Touch group in

their financial report has been represented faithfully or not and whether the

information disclosed is relevant or not has been identified by evaluating the unit of

measurement basis of the items to be measured, criteria of recognition and factors

accounted when selecting the basis of measurement.

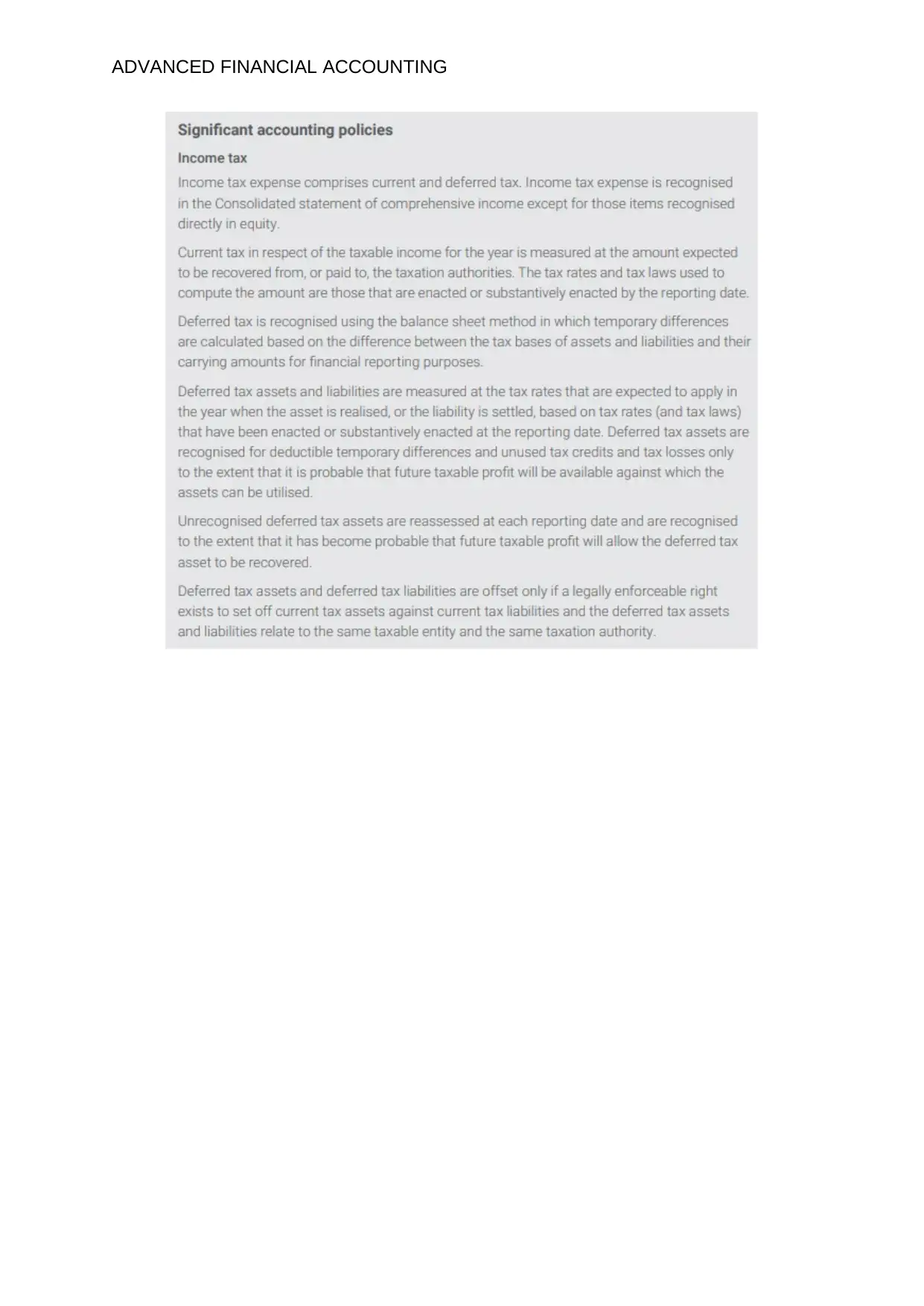

The recognition criteria used by the company to measure assets and liabilities

is considered to be appropriate if relevant information is produced about the

liabilities, assets, expenses, and income. This can be explained by taking examples

of various items in the financial statements such as income, tax and revenue.

Recognition of income tax expense is done using the method of balance sheet that

compute the temporary differences based on the carrying amount of financial

liabilities and assets and tax bases for liabilities and assets (Afterpaytouch.com

2020). However, the financial report mentions about the existence of uncertainties

with respect to the tax regulations interpretation and timing and amount of future

income to be taxed. The treatment of income tax is uncertain, although the

the information having high degree of uncertainty with the information that has fewer

uncertainty when it comes to providing explanations (Ifrs.org 2020). The substance

of financial information must be represented faithfully and should be relevant so as to

make such information useful.

Measurement basis of organization should be selected accounting for the key

characteristics of financial information such as faithful representation and usefulness.

Information disclosed in the financial report of the entity is regarded as relevant if it

can cause a difference to the user’s decision and for this such information should

have confirmatory or predictive value. On other hand, information is regarded to be

represented faithfully if it is neutral, complete and error free to the maximum extent

possible. Any uncertainty in the level of measurement affects the faithful

representation of information. A faithful representation of any event or transaction

that has caused arising of any income, assets, expenses or liabilities is provided by

the unit of account. An information that is represented faithfully need not be accurate

in all the respect and usefulness of the financial information should not be weakened

by the use of estimates that forms an important and essential part of preparing the

financial statements (Iasplus.com 2020).

Relevance of information is determined by choosing a unit of account so that

users are provided with the relevant information about liabilities and assets and any

related expenses and income. The recognition criteria also determines the relevance

of information such as whether any recognition criteria causes any existence of

uncertainty or flow of any economic benefits has a low probability ( Ifrs.org 2020). In

addition to this, whether there is any faithful representation of recognizing any item

and the representation is affected by recognition uncertainty, measurement

uncertainty and disclosure and presentation. Reporting entity when selecting the

basis of measurement should have a faithful representation and relevant in order to

enhance the qualitative characteristics of the information’s provided to the users

(Velte and Stawinoga 2017). Some factors impacting the faithful representation of

the information disclosed includes inconsistency in recognition, measurement

uncertainty and disclosure and presentation. Any liabilities or assets that is faithfully

represented is required to be derecognized with appropriate disclosure and

presentation

Whether the information produced or disclosed by Afterpay Touch group in

their financial report has been represented faithfully or not and whether the

information disclosed is relevant or not has been identified by evaluating the unit of

measurement basis of the items to be measured, criteria of recognition and factors

accounted when selecting the basis of measurement.

The recognition criteria used by the company to measure assets and liabilities

is considered to be appropriate if relevant information is produced about the

liabilities, assets, expenses, and income. This can be explained by taking examples

of various items in the financial statements such as income, tax and revenue.

Recognition of income tax expense is done using the method of balance sheet that

compute the temporary differences based on the carrying amount of financial

liabilities and assets and tax bases for liabilities and assets (Afterpaytouch.com

2020). However, the financial report mentions about the existence of uncertainties

with respect to the tax regulations interpretation and timing and amount of future

income to be taxed. The treatment of income tax is uncertain, although the

ADVANCED FINANCIAL ACCOUNTING

measurement and recognition criteria is applied as per AASB 112 income tax

(Mbobo and Ekpo 2016).

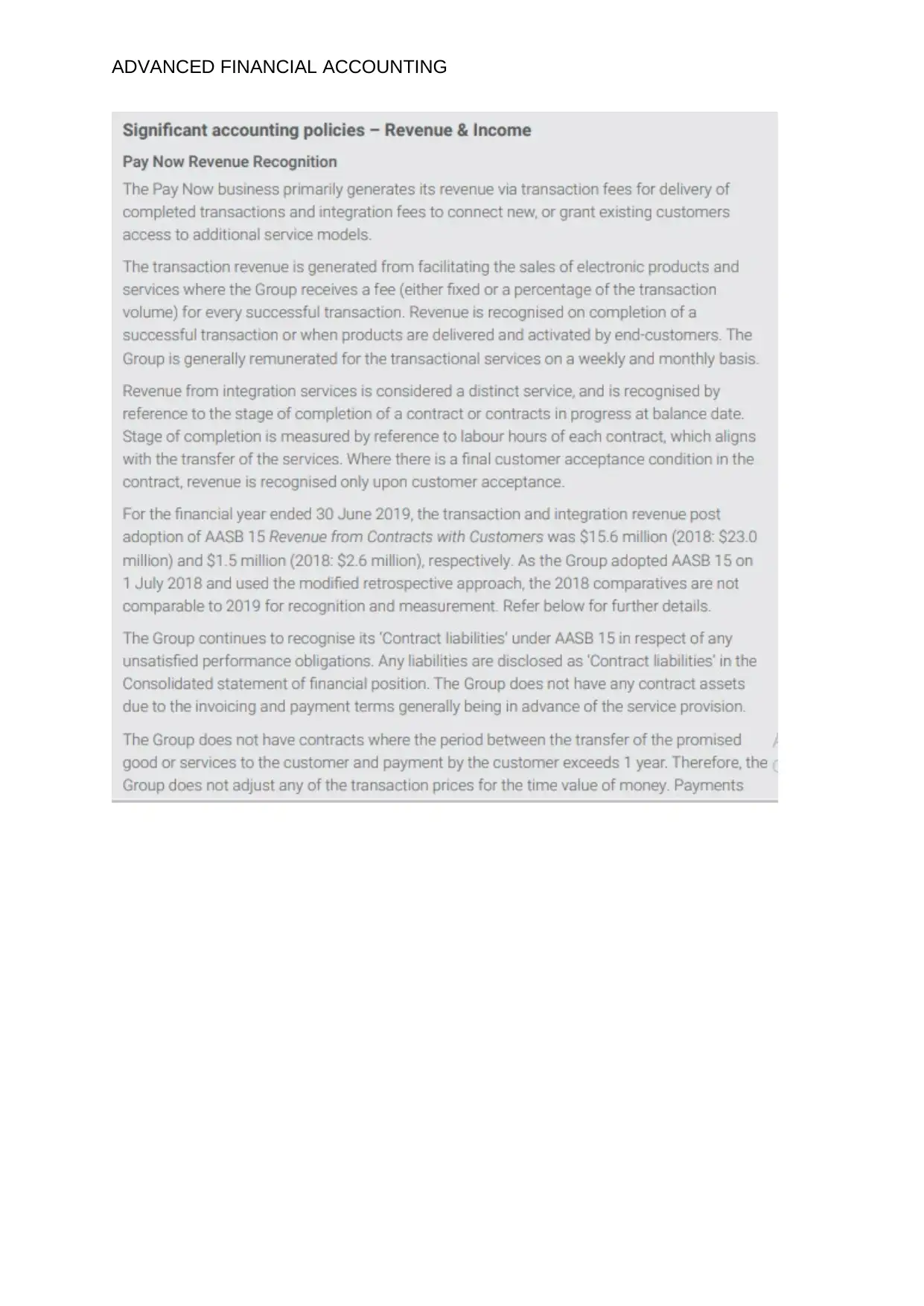

The basis of measurement of revenue generated from different sources such

as from integration services and transaction revenue are specified. Recognition of

revenue generated from integration services is done by referring to the contracts in

progress or on completion of contracts. On other hand, recognition of transaction

revenue is done when a transaction is completed successfully. It is mentioned that

due to the payment and invoicing terms, no contract assets are owned by the group

(Beerbaum et al. 2019). Moreover, adjustment of any transaction price to the time

value of money is not done. Therefore, there exist lower probability of having

economic benefits flow.

The provision matrix established based on the historical credit experience of

the group is adjusted for the economic environment and other factors that is forward

looking and is established specifically to debtors (Afterpaytouch.com 2020). This

implies that the information provided relating to the provision of matrix is relevant as

the users are provided with more predictive information by identifying some variation

in the current value (Jana and Schmidt 2018).

Any change in the current value of liabilities and income recognized in the

statement of other comprehensive income would enhance the faithful representation

and relevance of the information disclosed about the liability or assets. The faithful

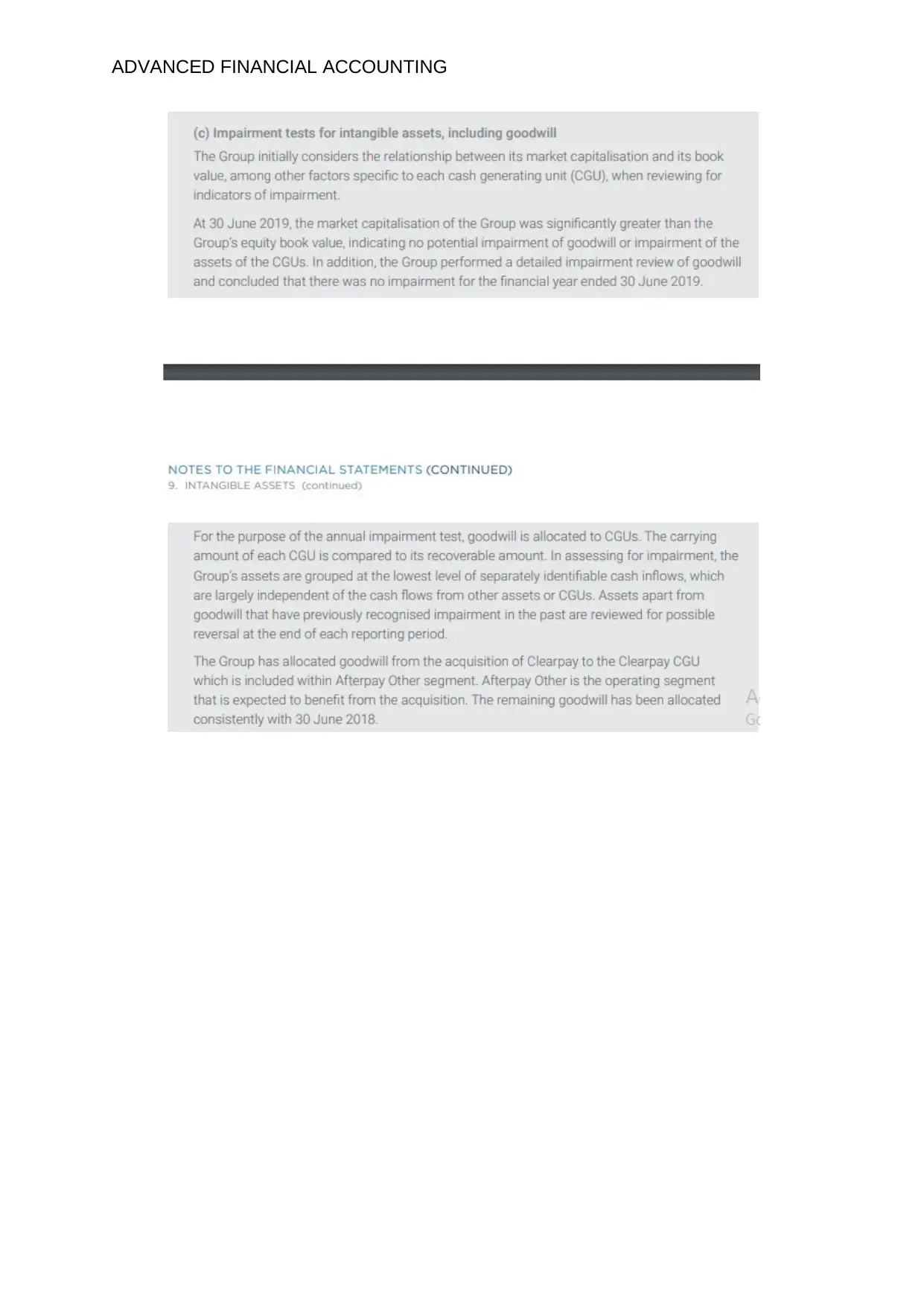

representation can be identified from the impairment testing of the goodwill. It is

mentioned by the group that any indicators of impairment is reviewed by accounting

for the factors specific to cash generating unit and relationship between book value

and market capitalization. A detailed impairment review has been performed by the

group concerning the goodwill (Gaynor et al. 2016). This implies that the information

is faithfully represented and is relevant for the investors in their investment decision

making.

Conclusion:

The report discussing about the evaluation of the factors of reporting entity

has identified various criteria for determining the reporting entity concept. Afterpay

Touch group has been classified as reporting entity based on the financial

characteristics, ownership characteristics and size of entity. Afterpay Touch group

has been classified as a reporting entity because of the preparation of general

purpose financial statements that adheres to the requirements of the applicable and

relevant accounting standards. In addition to this, account for assets and liabilities

have been done by using the different basis of measurement and recognition criteria

that implies that the information provided with faithfully represented and is relevant to

the investment and financial decision making process of investors.

measurement and recognition criteria is applied as per AASB 112 income tax

(Mbobo and Ekpo 2016).

The basis of measurement of revenue generated from different sources such

as from integration services and transaction revenue are specified. Recognition of

revenue generated from integration services is done by referring to the contracts in

progress or on completion of contracts. On other hand, recognition of transaction

revenue is done when a transaction is completed successfully. It is mentioned that

due to the payment and invoicing terms, no contract assets are owned by the group

(Beerbaum et al. 2019). Moreover, adjustment of any transaction price to the time

value of money is not done. Therefore, there exist lower probability of having

economic benefits flow.

The provision matrix established based on the historical credit experience of

the group is adjusted for the economic environment and other factors that is forward

looking and is established specifically to debtors (Afterpaytouch.com 2020). This

implies that the information provided relating to the provision of matrix is relevant as

the users are provided with more predictive information by identifying some variation

in the current value (Jana and Schmidt 2018).

Any change in the current value of liabilities and income recognized in the

statement of other comprehensive income would enhance the faithful representation

and relevance of the information disclosed about the liability or assets. The faithful

representation can be identified from the impairment testing of the goodwill. It is

mentioned by the group that any indicators of impairment is reviewed by accounting

for the factors specific to cash generating unit and relationship between book value

and market capitalization. A detailed impairment review has been performed by the

group concerning the goodwill (Gaynor et al. 2016). This implies that the information

is faithfully represented and is relevant for the investors in their investment decision

making.

Conclusion:

The report discussing about the evaluation of the factors of reporting entity

has identified various criteria for determining the reporting entity concept. Afterpay

Touch group has been classified as reporting entity based on the financial

characteristics, ownership characteristics and size of entity. Afterpay Touch group

has been classified as a reporting entity because of the preparation of general

purpose financial statements that adheres to the requirements of the applicable and

relevant accounting standards. In addition to this, account for assets and liabilities

have been done by using the different basis of measurement and recognition criteria

that implies that the information provided with faithfully represented and is relevant to

the investment and financial decision making process of investors.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ADVANCED FINANCIAL ACCOUNTING

References list:

Aasb.gov.au., 2020. [online] Available at:

https://www.aasb.gov.au/admin/file/content102/c3/SAC1_8-90_2001V.pdf [Accessed

26 Jan. 2020].

Adams, R., Houldin, M. and Slomp, S., 2017. Towards a generally accepted

framework for environmental reporting. In Sustainable Measures (pp. 314-329).

Routledge.

Afterpaytouch.com., 2020. [online] Available at:

https://www.afterpaytouch.com/images/28082019-FY2019-Appendix-4E-and-Annual-

Report.pdf [Accessed 26 Jan. 2020].

Beerbaum, D., Piechocki, M. and Puaschunder, J.M., 2019. Accounting Reporting

Complexity Measured Behaviorally. Internal Auditing and Risk Management, 56(4),

pp.35-47.

Birt, J., Chalmers, K., Maloney, S., Brooks, A., Oliver, J. and Bond, D.,

2019. Accounting: Business reporting for decision making. John Wiley & Sons.

Gaynor, L.M., Kelton, A.S., Mercer, M. and Yohn, T.L., 2016. Understanding the

relation between financial reporting quality and audit quality. Auditing: A Journal of

Practice & Theory, 35(4), pp.1-22.

Grigoras-Ichim, C.E. and Morosan-Danila, L., 2016. Hierarchy of accounting

information qualitative characteristics in financial reporting. The USV Annals of

Economics and Public Administration, 16(1 (23)), pp.183-191.

Herath, S.K. and Albarqi, N., 2017. Financial reporting quality: A literature

review. Int. J. Bus. Manag. Commer, 2(2), pp.1-14.

Iasplus.com., 2020. Conceptual Framework Phase A – Objective and qualitative

characteristics. [online] Available at:

https://www.iasplus.com/en/projects/completed/framework/framework-a [Accessed

26 Jan. 2020].

Ifrs.org., 2020. [online] Available at: https://www.ifrs.org/-/media/project/conceptual-

framework/fact-sheet-project-summary-and-feedback-statement/conceptual-

framework-project-summary.pdf [Accessed 26 Jan. 2020].

Jana, S. and Schmidt, M., 2018. Model-based fair values for financial instruments:

relevance or reliability? Conjoint measurement-based evidence. Conjoint

Measurement-Based Evidence (July 13, 2018).

Janowicz, M., 2018. The quality of information about business combinations under

common control (BCUCC) disclosed under International Financial Reporting

Standards (IFRS). Finanse, Rynki Finansowe, Ubezpieczenia, 94(4 (1)), pp.99-107.

References list:

Aasb.gov.au., 2020. [online] Available at:

https://www.aasb.gov.au/admin/file/content102/c3/SAC1_8-90_2001V.pdf [Accessed

26 Jan. 2020].

Adams, R., Houldin, M. and Slomp, S., 2017. Towards a generally accepted

framework for environmental reporting. In Sustainable Measures (pp. 314-329).

Routledge.

Afterpaytouch.com., 2020. [online] Available at:

https://www.afterpaytouch.com/images/28082019-FY2019-Appendix-4E-and-Annual-

Report.pdf [Accessed 26 Jan. 2020].

Beerbaum, D., Piechocki, M. and Puaschunder, J.M., 2019. Accounting Reporting

Complexity Measured Behaviorally. Internal Auditing and Risk Management, 56(4),

pp.35-47.

Birt, J., Chalmers, K., Maloney, S., Brooks, A., Oliver, J. and Bond, D.,

2019. Accounting: Business reporting for decision making. John Wiley & Sons.

Gaynor, L.M., Kelton, A.S., Mercer, M. and Yohn, T.L., 2016. Understanding the

relation between financial reporting quality and audit quality. Auditing: A Journal of

Practice & Theory, 35(4), pp.1-22.

Grigoras-Ichim, C.E. and Morosan-Danila, L., 2016. Hierarchy of accounting

information qualitative characteristics in financial reporting. The USV Annals of

Economics and Public Administration, 16(1 (23)), pp.183-191.

Herath, S.K. and Albarqi, N., 2017. Financial reporting quality: A literature

review. Int. J. Bus. Manag. Commer, 2(2), pp.1-14.

Iasplus.com., 2020. Conceptual Framework Phase A – Objective and qualitative

characteristics. [online] Available at:

https://www.iasplus.com/en/projects/completed/framework/framework-a [Accessed

26 Jan. 2020].

Ifrs.org., 2020. [online] Available at: https://www.ifrs.org/-/media/project/conceptual-

framework/fact-sheet-project-summary-and-feedback-statement/conceptual-

framework-project-summary.pdf [Accessed 26 Jan. 2020].

Jana, S. and Schmidt, M., 2018. Model-based fair values for financial instruments:

relevance or reliability? Conjoint measurement-based evidence. Conjoint

Measurement-Based Evidence (July 13, 2018).

Janowicz, M., 2018. The quality of information about business combinations under

common control (BCUCC) disclosed under International Financial Reporting

Standards (IFRS). Finanse, Rynki Finansowe, Ubezpieczenia, 94(4 (1)), pp.99-107.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED FINANCIAL ACCOUNTING

Lin, S., Riccardi, W.N., Wang, C., Hopkins, P.E. and Kabureck, G., 2019. Relative

effects of IFRS adoption and IFRS convergence on financial statement

comparability. Contemporary Accounting Research, 36(2), pp.588-628.

Mbobo, M.E. and Ekpo, N.B., 2016. Operationalising the qualitative characteristics of

financial reporting. International Journal of Finance and Accounting, 5(4), pp.184-

192.

Velte, P. and Stawinoga, M., 2017. Integrated reporting: The current state of

empirical research, limitations and future research implications. Journal of

Management Control, 28(3), pp.275-320.

Lin, S., Riccardi, W.N., Wang, C., Hopkins, P.E. and Kabureck, G., 2019. Relative

effects of IFRS adoption and IFRS convergence on financial statement

comparability. Contemporary Accounting Research, 36(2), pp.588-628.

Mbobo, M.E. and Ekpo, N.B., 2016. Operationalising the qualitative characteristics of

financial reporting. International Journal of Finance and Accounting, 5(4), pp.184-

192.

Velte, P. and Stawinoga, M., 2017. Integrated reporting: The current state of

empirical research, limitations and future research implications. Journal of

Management Control, 28(3), pp.275-320.

ADVANCED FINANCIAL ACCOUNTING

Appendix:

Appendix:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ADVANCED FINANCIAL ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ADVANCED FINANCIAL ACCOUNTING

ADVANCED FINANCIAL ACCOUNTING

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.