Corporate Governance: Agency Theory, Transparency, and Regulations

VerifiedAdded on 2023/06/19

|13

|3907

|145

Essay

AI Summary

This essay delves into the agency theory, examining the relationship between principals and agents within a corporate governance framework. It addresses potential conflicts of interest and moral hazards that arise when agents do not act in the best interests of their principals. The essay highlights the importance of transparency, restrictions on agent capabilities, and appropriate commission structures to mitigate these issues. It further discusses corporate governance rules designed to align the interests of executives and shareholders, emphasizing the role of accounting regulations and public interest theories in ensuring effective governance. The analysis extends to the costs associated with agency problems, such as incentive programs and administrative inquiries, and concludes by advocating for measures that promote transparency and accountability in corporate management. Desklib offers this assignment solution and many other resources for students.

[Document title]

[Document subtitle]

[DATE]

[Company name]

[Company address]

[Document subtitle]

[DATE]

[Company name]

[Company address]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Contents

Question no: 1.............................................................................................................................................1

Full transparency:....................................................................................................................................2

Restrictions on agent’s capabilities:........................................................................................................2

Commission and bonus structure:...........................................................................................................2

Examples:................................................................................................................................................3

Corporate governance used:.......................................................................................................................3

Question: 2..................................................................................................................................................5

Accounting regulations:...............................................................................................................................5

Public interest theories:...........................................................................................................................9

References:................................................................................................................................................11

Contents

Question no: 1.............................................................................................................................................1

Full transparency:....................................................................................................................................2

Restrictions on agent’s capabilities:........................................................................................................2

Commission and bonus structure:...........................................................................................................2

Examples:................................................................................................................................................3

Corporate governance used:.......................................................................................................................3

Question: 2..................................................................................................................................................5

Accounting regulations:...............................................................................................................................5

Public interest theories:...........................................................................................................................9

References:................................................................................................................................................11

2

Question no: 1

The agency theory was used to obtain the link between the specialist and the principal. Experts

speak to the center in specific commercial exchanges and are expected to speak to the best

interfaces without respecting their own interests. The unique interface of the delegator and

operator can be a source of struggle as some specialists may not be able to perform well in the

best interface for the delegator. The emergence of miscommunication and conflict can lead to

different problems and conflicts within the company. Inconsistent requirements can create

divisions between each partner and lead to wasteful and budgetary mishaps. This leads to a

principal-agent problem.

The principal-agent problem occurs when the interfaces of important people and experts collide.

Companies should seek to downplay these situations through strong corporate arrangements.

These conflicts show that generally moral people have opportunities for moral danger. Dynamics

can be used to shift operator behavior to realign these interfaces with the principal's concerns.

Company management can be used to change the rules of the specialist's work and rebuild the

principal's interface. Importantly, by using an operator-to-principal interface dialogue, the need

for data to perform tasks almost as an agent must be overcome. Experts must be motivated so

that they can act in unison with the principal's interface. The office hypothesized that these

motivations could be properly planned by considering what interface would persuade experts to

act. Motivations for off-base behavior must be dislodged, and frustrating moral hazard rules must

be enacted.

Decide whether an operator is acting in

the best interests of its principals, the

criterion of "organizational misfortune"

has developed into a commonly used

measure. Fully characterized, office

misfortune is the contrast between the

paramount ideal and the outcome of the

agent's actions. For example, when a

specialist often works with the principal's

Question no: 1

The agency theory was used to obtain the link between the specialist and the principal. Experts

speak to the center in specific commercial exchanges and are expected to speak to the best

interfaces without respecting their own interests. The unique interface of the delegator and

operator can be a source of struggle as some specialists may not be able to perform well in the

best interface for the delegator. The emergence of miscommunication and conflict can lead to

different problems and conflicts within the company. Inconsistent requirements can create

divisions between each partner and lead to wasteful and budgetary mishaps. This leads to a

principal-agent problem.

The principal-agent problem occurs when the interfaces of important people and experts collide.

Companies should seek to downplay these situations through strong corporate arrangements.

These conflicts show that generally moral people have opportunities for moral danger. Dynamics

can be used to shift operator behavior to realign these interfaces with the principal's concerns.

Company management can be used to change the rules of the specialist's work and rebuild the

principal's interface. Importantly, by using an operator-to-principal interface dialogue, the need

for data to perform tasks almost as an agent must be overcome. Experts must be motivated so

that they can act in unison with the principal's interface. The office hypothesized that these

motivations could be properly planned by considering what interface would persuade experts to

act. Motivations for off-base behavior must be dislodged, and frustrating moral hazard rules must

be enacted.

Decide whether an operator is acting in

the best interests of its principals, the

criterion of "organizational misfortune"

has developed into a commonly used

measure. Fully characterized, office

misfortune is the contrast between the

paramount ideal and the outcome of the

agent's actions. For example, when a

specialist often works with the principal's

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

most interesting intelligence, there is zero misfortune in the office. However, the office has

unfortunately become more prominent by encouraging the activities of the agent to be separated

from the best interface of the principal.

Full transparency:

Organizational issues are most prominent when there are differences in information between

experts and centers. It is easy and tempting for operators to abuse information gaps for personal

pickups. When an agent-principal connection arises in your transaction, honing in on complete

candor can help near information gaps and avoid the development of office problems. Expert

Instead of clearing you in the dark, you should be taught, Central, about everything that's going

on while the experts make the choice for you.

Restrictions on agent’s capabilities:

Giving experts more control to take action opens the door to future challenges and can lead to

poor choices financial advisors may make. The most effective government hone checks and

balances because it eases control over any one person or substance, keeping devaluation to a

minimum. By limiting operator control, you will be able to hone the same standards in your

business.

Commission and bonus structure:

Perhaps the only strategy for solving organizational problems is to remove the monetary motive

that fuels conflict of interest. Going back to the budget consultant example, there are

organizational issues in this case because the consultant's compensation is tied to the specific

monetary item he provides you. The item that pays the highest commission is not your

(customer) primary choice. A consultant is often forced to choose between doing the right thing

for his client and maximizing his salary. If consultants receive fixed compensation or receive

commissions based on the sum of management resources rather than specific project

transactions, the office problem disappears. Office problems arise when conflicting interests

prevent one party from acting within the best interests of the other party. By taking specific steps

and staying organized, you will be able to minimize the chances of this happening in your

business.

most interesting intelligence, there is zero misfortune in the office. However, the office has

unfortunately become more prominent by encouraging the activities of the agent to be separated

from the best interface of the principal.

Full transparency:

Organizational issues are most prominent when there are differences in information between

experts and centers. It is easy and tempting for operators to abuse information gaps for personal

pickups. When an agent-principal connection arises in your transaction, honing in on complete

candor can help near information gaps and avoid the development of office problems. Expert

Instead of clearing you in the dark, you should be taught, Central, about everything that's going

on while the experts make the choice for you.

Restrictions on agent’s capabilities:

Giving experts more control to take action opens the door to future challenges and can lead to

poor choices financial advisors may make. The most effective government hone checks and

balances because it eases control over any one person or substance, keeping devaluation to a

minimum. By limiting operator control, you will be able to hone the same standards in your

business.

Commission and bonus structure:

Perhaps the only strategy for solving organizational problems is to remove the monetary motive

that fuels conflict of interest. Going back to the budget consultant example, there are

organizational issues in this case because the consultant's compensation is tied to the specific

monetary item he provides you. The item that pays the highest commission is not your

(customer) primary choice. A consultant is often forced to choose between doing the right thing

for his client and maximizing his salary. If consultants receive fixed compensation or receive

commissions based on the sum of management resources rather than specific project

transactions, the office problem disappears. Office problems arise when conflicting interests

prevent one party from acting within the best interests of the other party. By taking specific steps

and staying organized, you will be able to minimize the chances of this happening in your

business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Examples:

One of the most common cases of office theory can be seen in the capabilities of national

governments. The masses choose political agents to run the country in ways that maximize their

interface. Agents of different political parties assure voters of change in the country's

surveillance demonstrations. In any case, voters in almost all sovereign countries find themselves

deceived because the candidates they choose have behaved in corrupt ways in anticipation of

taking office. Here, voters act as principals, and they choose government agents as their experts.

Another common example of an office assumption is between workers and bosses in an

organization. Representatives are recruited to align with the goals of the organization. Still, a

growing number of corporate shenanigans seem to suggest that the relationship doesn't always

work out the way it's implied. Workers work against the ethics of the organization, causing

enormous monetary and reputational damage. Every now and then, the misfortune caused by this

fallen employee is beyond repair, and an organization should wind up its business entirely.

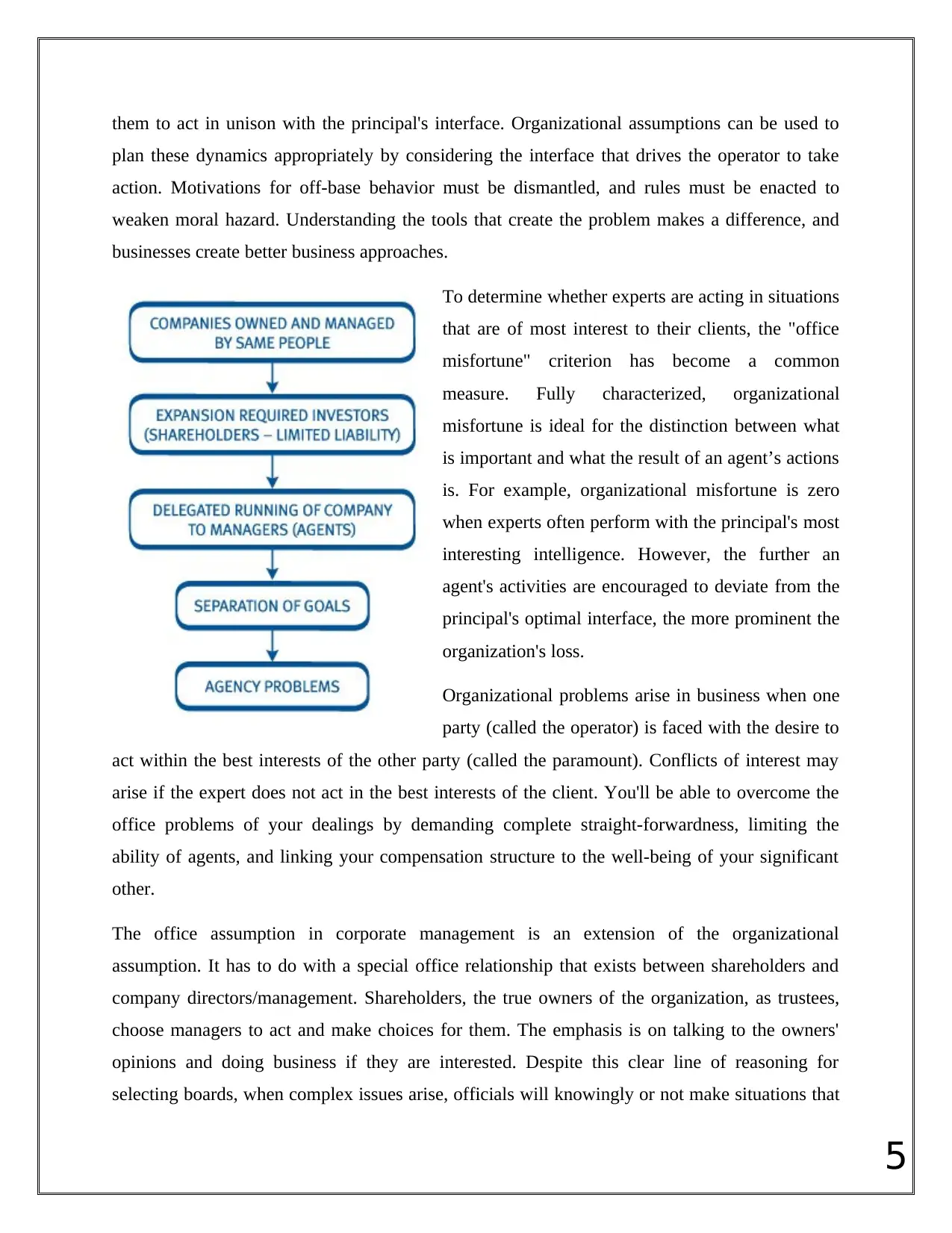

Corporate governance used:

Organizational assumptions consider the firm to be an expert on its shareholders. That is,

shareholders contribute with company property and then hand over their assets to the CEO and

officers of the organization for management. In large corporations, there is often a distinct

distinction between the short-term and long-term interests of managers and shareholders.

Essentially due to short-term interest requirements and asymmetry in executive and executive

versus shareholder data. Differences in the interests of officers, directors, and shareholders are

thought to influence the activities and choices of officers and directors who may ultimately be

isolated from the shareholder interface.

Corporate governance rules seek to create a legal system comparable to the agency-principal

relationship. These rules are designed to align the dynamics of executives and principals with

those of shareholders. They seek to establish standards and traditions to avoid confrontation with

unique corporate interfaces. Senior, the office assumes obligations lent to officers or supervisors

to the business.

Company management can be used to change the rules of the specialist's work and rebuild the

principal's interface. Crucially, by leveraging the expert-principal interface dialogue, the need for

data to be performed by the agent must be overcome. Operators must have incentives that allow

Examples:

One of the most common cases of office theory can be seen in the capabilities of national

governments. The masses choose political agents to run the country in ways that maximize their

interface. Agents of different political parties assure voters of change in the country's

surveillance demonstrations. In any case, voters in almost all sovereign countries find themselves

deceived because the candidates they choose have behaved in corrupt ways in anticipation of

taking office. Here, voters act as principals, and they choose government agents as their experts.

Another common example of an office assumption is between workers and bosses in an

organization. Representatives are recruited to align with the goals of the organization. Still, a

growing number of corporate shenanigans seem to suggest that the relationship doesn't always

work out the way it's implied. Workers work against the ethics of the organization, causing

enormous monetary and reputational damage. Every now and then, the misfortune caused by this

fallen employee is beyond repair, and an organization should wind up its business entirely.

Corporate governance used:

Organizational assumptions consider the firm to be an expert on its shareholders. That is,

shareholders contribute with company property and then hand over their assets to the CEO and

officers of the organization for management. In large corporations, there is often a distinct

distinction between the short-term and long-term interests of managers and shareholders.

Essentially due to short-term interest requirements and asymmetry in executive and executive

versus shareholder data. Differences in the interests of officers, directors, and shareholders are

thought to influence the activities and choices of officers and directors who may ultimately be

isolated from the shareholder interface.

Corporate governance rules seek to create a legal system comparable to the agency-principal

relationship. These rules are designed to align the dynamics of executives and principals with

those of shareholders. They seek to establish standards and traditions to avoid confrontation with

unique corporate interfaces. Senior, the office assumes obligations lent to officers or supervisors

to the business.

Company management can be used to change the rules of the specialist's work and rebuild the

principal's interface. Crucially, by leveraging the expert-principal interface dialogue, the need for

data to be performed by the agent must be overcome. Operators must have incentives that allow

5

them to act in unison with the principal's interface. Organizational assumptions can be used to

plan these dynamics appropriately by considering the interface that drives the operator to take

action. Motivations for off-base behavior must be dismantled, and rules must be enacted to

weaken moral hazard. Understanding the tools that create the problem makes a difference, and

businesses create better business approaches.

To determine whether experts are acting in situations

that are of most interest to their clients, the "office

misfortune" criterion has become a common

measure. Fully characterized, organizational

misfortune is ideal for the distinction between what

is important and what the result of an agent’s actions

is. For example, organizational misfortune is zero

when experts often perform with the principal's most

interesting intelligence. However, the further an

agent's activities are encouraged to deviate from the

principal's optimal interface, the more prominent the

organization's loss.

Organizational problems arise in business when one

party (called the operator) is faced with the desire to

act within the best interests of the other party (called the paramount). Conflicts of interest may

arise if the expert does not act in the best interests of the client. You'll be able to overcome the

office problems of your dealings by demanding complete straight-forwardness, limiting the

ability of agents, and linking your compensation structure to the well-being of your significant

other.

The office assumption in corporate management is an extension of the organizational

assumption. It has to do with a special office relationship that exists between shareholders and

company directors/management. Shareholders, the true owners of the organization, as trustees,

choose managers to act and make choices for them. The emphasis is on talking to the owners'

opinions and doing business if they are interested. Despite this clear line of reasoning for

selecting boards, when complex issues arise, officials will knowingly or not make situations that

them to act in unison with the principal's interface. Organizational assumptions can be used to

plan these dynamics appropriately by considering the interface that drives the operator to take

action. Motivations for off-base behavior must be dismantled, and rules must be enacted to

weaken moral hazard. Understanding the tools that create the problem makes a difference, and

businesses create better business approaches.

To determine whether experts are acting in situations

that are of most interest to their clients, the "office

misfortune" criterion has become a common

measure. Fully characterized, organizational

misfortune is ideal for the distinction between what

is important and what the result of an agent’s actions

is. For example, organizational misfortune is zero

when experts often perform with the principal's most

interesting intelligence. However, the further an

agent's activities are encouraged to deviate from the

principal's optimal interface, the more prominent the

organization's loss.

Organizational problems arise in business when one

party (called the operator) is faced with the desire to

act within the best interests of the other party (called the paramount). Conflicts of interest may

arise if the expert does not act in the best interests of the client. You'll be able to overcome the

office problems of your dealings by demanding complete straight-forwardness, limiting the

ability of agents, and linking your compensation structure to the well-being of your significant

other.

The office assumption in corporate management is an extension of the organizational

assumption. It has to do with a special office relationship that exists between shareholders and

company directors/management. Shareholders, the true owners of the organization, as trustees,

choose managers to act and make choices for them. The emphasis is on talking to the owners'

opinions and doing business if they are interested. Despite this clear line of reasoning for

selecting boards, when complex issues arise, officials will knowingly or not make situations that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

do not reflect the choices that are most interesting to shareholders. Office costs are largely

derived from the practice of principals observing specialists and can, from a financial standpoint,

assets be swallowed up or check time. Fees are borne by the center, but may be in a roundabout

way due to operators spending their time and assets on certain exercises. Examples of costs

include: Incentive programs and compensation for directors bundling administrative costs

providing annual reporting information, such as committee changes and opportunities,

administrative inquiries, and the cost of obtaining critical investigations of this data costs of

meeting with budget investigators and central shareholders tolerating higher acquisition

companies Operating in a way that is more risky than shareholders want.

That is, shareholders contribute capital in the form of sole proprietorship of the company and in

this way give their assets to the management of the executives and officers of the business. In

larger organizations, there is often a sharp distinction between the short-term and long-term

interests of managers and shareholders. Often fundamentally caused by short-term interest

demands and asymmetries in officers and supervisors compared to shareholder data. Differences

in interests among executives, executives, and shareholders are thought to influence the activities

and choices of executives and executives, who may withdraw from the shareholder interface.

Question: 2

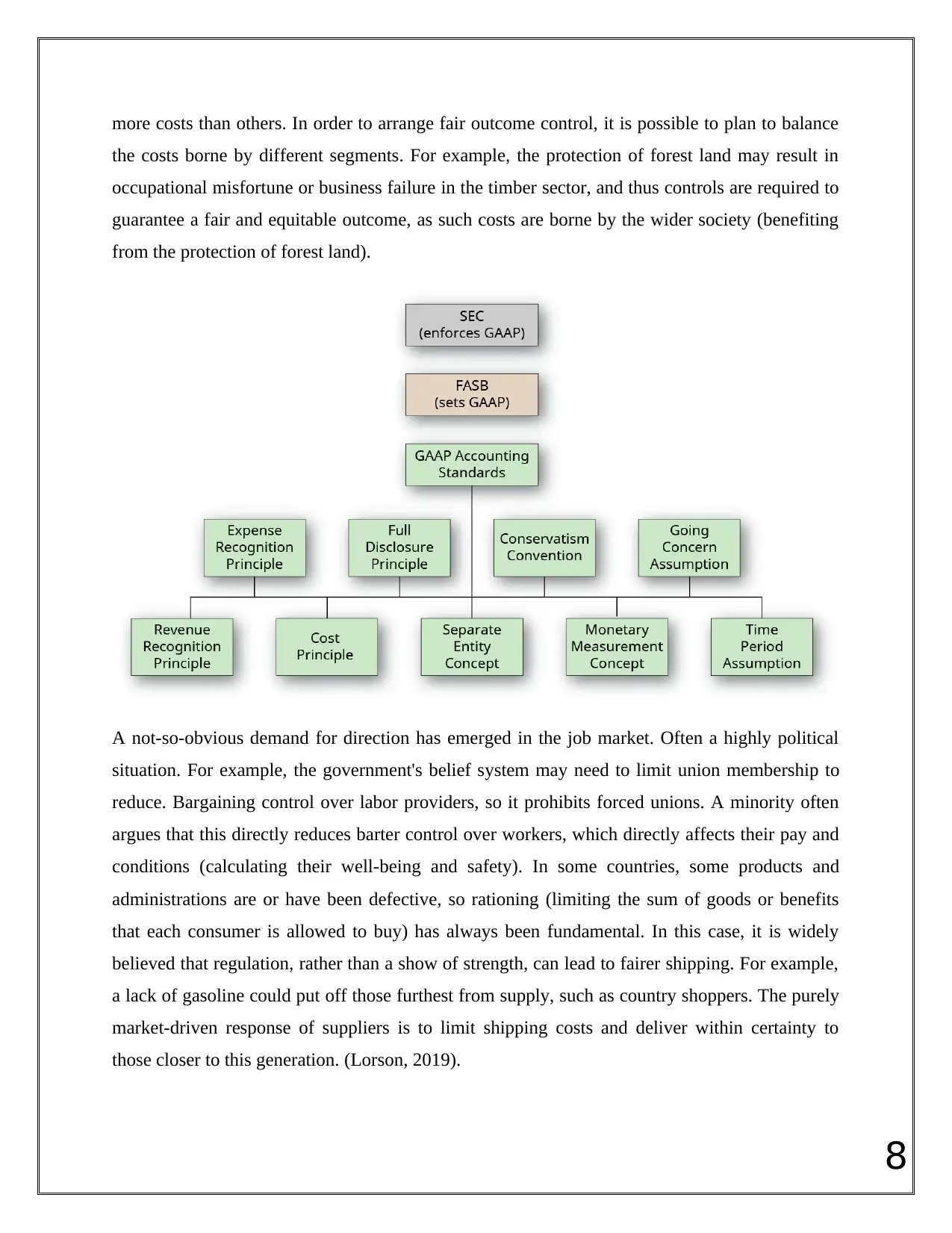

Accounting regulations:

There are two broad conventions regarding financial speculation in direction. The first tradition

holds that the controller has sufficient data and authorization powers to effectively advance the

interest of openness. The convention also expects the controller to be benevolent and point to

seeking open interest. Financial assumptions derived from these assumptions are often referred

to in this way as "regulatory speculation of public interest". Another tradition in the financial

world holds that the direction comes from a different assumption. Regulators do not have enough

data on fees, requirements, quality and other aspects of corporate conduct. They can then

incompletely advance the public interest in controlling corporate or social activity. In this

Convention, these information, controls and requirements also apply to other financial operators,

such as legislators, voters or customers. And, more importantly, all financial agents in general

are expected to pursue the interests they have, which may or may not include an open interest

component. Under these suspicions, there is no reason to conclude that controls will be of public

do not reflect the choices that are most interesting to shareholders. Office costs are largely

derived from the practice of principals observing specialists and can, from a financial standpoint,

assets be swallowed up or check time. Fees are borne by the center, but may be in a roundabout

way due to operators spending their time and assets on certain exercises. Examples of costs

include: Incentive programs and compensation for directors bundling administrative costs

providing annual reporting information, such as committee changes and opportunities,

administrative inquiries, and the cost of obtaining critical investigations of this data costs of

meeting with budget investigators and central shareholders tolerating higher acquisition

companies Operating in a way that is more risky than shareholders want.

That is, shareholders contribute capital in the form of sole proprietorship of the company and in

this way give their assets to the management of the executives and officers of the business. In

larger organizations, there is often a sharp distinction between the short-term and long-term

interests of managers and shareholders. Often fundamentally caused by short-term interest

demands and asymmetries in officers and supervisors compared to shareholder data. Differences

in interests among executives, executives, and shareholders are thought to influence the activities

and choices of executives and executives, who may withdraw from the shareholder interface.

Question: 2

Accounting regulations:

There are two broad conventions regarding financial speculation in direction. The first tradition

holds that the controller has sufficient data and authorization powers to effectively advance the

interest of openness. The convention also expects the controller to be benevolent and point to

seeking open interest. Financial assumptions derived from these assumptions are often referred

to in this way as "regulatory speculation of public interest". Another tradition in the financial

world holds that the direction comes from a different assumption. Regulators do not have enough

data on fees, requirements, quality and other aspects of corporate conduct. They can then

incompletely advance the public interest in controlling corporate or social activity. In this

Convention, these information, controls and requirements also apply to other financial operators,

such as legislators, voters or customers. And, more importantly, all financial agents in general

are expected to pursue the interests they have, which may or may not include an open interest

component. Under these suspicions, there is no reason to conclude that controls will be of public

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

interest. The contrasting objectives of financial experts and the costs involved in their

interactions may lead some operators to imagine the interfaces they have, perhaps out of an open

interest. Therefore, the financial speculation that arises from these last-mentioned suspicions is

often referred to as "regulatory speculation of private curiosity". (Deegan, 2019).

The key to publicizing interesting hypotheses is to demonstrate disappointment and effective

government intervention. Agreeing with these assumptions, controlling for increments elucidates

social welfare. Take control from funny group behavior. In addition, exchanging wealth with the

more efficient Cabal also often reduces social welfare. Interested groups can be companies,

groups of consumers or customers, controllers or their employees, legislators, trade unions, etc.

Privately curious speculations about direction in this way encompass many assumptions within

the realm of open choice, and thus feasibly become hypotheses of political activity. Depending

on the efficiency of political preparation, social welfare will either increase or decrease. The

main part of this paper discusses common assumptions of direction of open and private interest,

and the critiques against them.

In some cases, direction is critical to ensure that "profit grabbing" does not occur. Oftentimes,

when suppliers will provide customers with returns that result in the most noteworthy profits

while ignoring supply to others. Usually the core question about privatization. The government

must ensure that media transmission management continues to be available to all Australians in

as equal and reasonable a manner as possible, no matter where they live; provincial or municipal.

This situation, although it may be, is not a single event, and there are many other, lesser-known,

comparable cases in which controls are used to guarantee progress and the availability of benefits

under the premise of fairness. Essentially, they are used as a precautionary measure and prohibit

such practices in what is seen as anti-competitive and ruthless pricing regulation. Microsoft has

been accused of doing this in the US (source code for the windows stage), the government sued

to overcome me.

Orientation is also crucial in the legitimacy and coordination of financial activities in order to

classify actions or businesses in an efficient manner. An example is the marketing of many

necessities, such as wool boards or horns or meat, through a central display organization. There

is comparative thinking, and some of these central arrangements are crucial. This is again

typically key when considering the environmental impact of exercises that require a few to bear

interest. The contrasting objectives of financial experts and the costs involved in their

interactions may lead some operators to imagine the interfaces they have, perhaps out of an open

interest. Therefore, the financial speculation that arises from these last-mentioned suspicions is

often referred to as "regulatory speculation of private curiosity". (Deegan, 2019).

The key to publicizing interesting hypotheses is to demonstrate disappointment and effective

government intervention. Agreeing with these assumptions, controlling for increments elucidates

social welfare. Take control from funny group behavior. In addition, exchanging wealth with the

more efficient Cabal also often reduces social welfare. Interested groups can be companies,

groups of consumers or customers, controllers or their employees, legislators, trade unions, etc.

Privately curious speculations about direction in this way encompass many assumptions within

the realm of open choice, and thus feasibly become hypotheses of political activity. Depending

on the efficiency of political preparation, social welfare will either increase or decrease. The

main part of this paper discusses common assumptions of direction of open and private interest,

and the critiques against them.

In some cases, direction is critical to ensure that "profit grabbing" does not occur. Oftentimes,

when suppliers will provide customers with returns that result in the most noteworthy profits

while ignoring supply to others. Usually the core question about privatization. The government

must ensure that media transmission management continues to be available to all Australians in

as equal and reasonable a manner as possible, no matter where they live; provincial or municipal.

This situation, although it may be, is not a single event, and there are many other, lesser-known,

comparable cases in which controls are used to guarantee progress and the availability of benefits

under the premise of fairness. Essentially, they are used as a precautionary measure and prohibit

such practices in what is seen as anti-competitive and ruthless pricing regulation. Microsoft has

been accused of doing this in the US (source code for the windows stage), the government sued

to overcome me.

Orientation is also crucial in the legitimacy and coordination of financial activities in order to

classify actions or businesses in an efficient manner. An example is the marketing of many

necessities, such as wool boards or horns or meat, through a central display organization. There

is comparative thinking, and some of these central arrangements are crucial. This is again

typically key when considering the environmental impact of exercises that require a few to bear

8

more costs than others. In order to arrange fair outcome control, it is possible to plan to balance

the costs borne by different segments. For example, the protection of forest land may result in

occupational misfortune or business failure in the timber sector, and thus controls are required to

guarantee a fair and equitable outcome, as such costs are borne by the wider society (benefiting

from the protection of forest land).

A not-so-obvious demand for direction has emerged in the job market. Often a highly political

situation. For example, the government's belief system may need to limit union membership to

reduce. Bargaining control over labor providers, so it prohibits forced unions. A minority often

argues that this directly reduces barter control over workers, which directly affects their pay and

conditions (calculating their well-being and safety). In some countries, some products and

administrations are or have been defective, so rationing (limiting the sum of goods or benefits

that each consumer is allowed to buy) has always been fundamental. In this case, it is widely

believed that regulation, rather than a show of strength, can lead to fairer shipping. For example,

a lack of gasoline could put off those furthest from supply, such as country shoppers. The purely

market-driven response of suppliers is to limit shipping costs and deliver within certainty to

those closer to this generation. (Lorson, 2019).

more costs than others. In order to arrange fair outcome control, it is possible to plan to balance

the costs borne by different segments. For example, the protection of forest land may result in

occupational misfortune or business failure in the timber sector, and thus controls are required to

guarantee a fair and equitable outcome, as such costs are borne by the wider society (benefiting

from the protection of forest land).

A not-so-obvious demand for direction has emerged in the job market. Often a highly political

situation. For example, the government's belief system may need to limit union membership to

reduce. Bargaining control over labor providers, so it prohibits forced unions. A minority often

argues that this directly reduces barter control over workers, which directly affects their pay and

conditions (calculating their well-being and safety). In some countries, some products and

administrations are or have been defective, so rationing (limiting the sum of goods or benefits

that each consumer is allowed to buy) has always been fundamental. In this case, it is widely

believed that regulation, rather than a show of strength, can lead to fairer shipping. For example,

a lack of gasoline could put off those furthest from supply, such as country shoppers. The purely

market-driven response of suppliers is to limit shipping costs and deliver within certainty to

those closer to this generation. (Lorson, 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

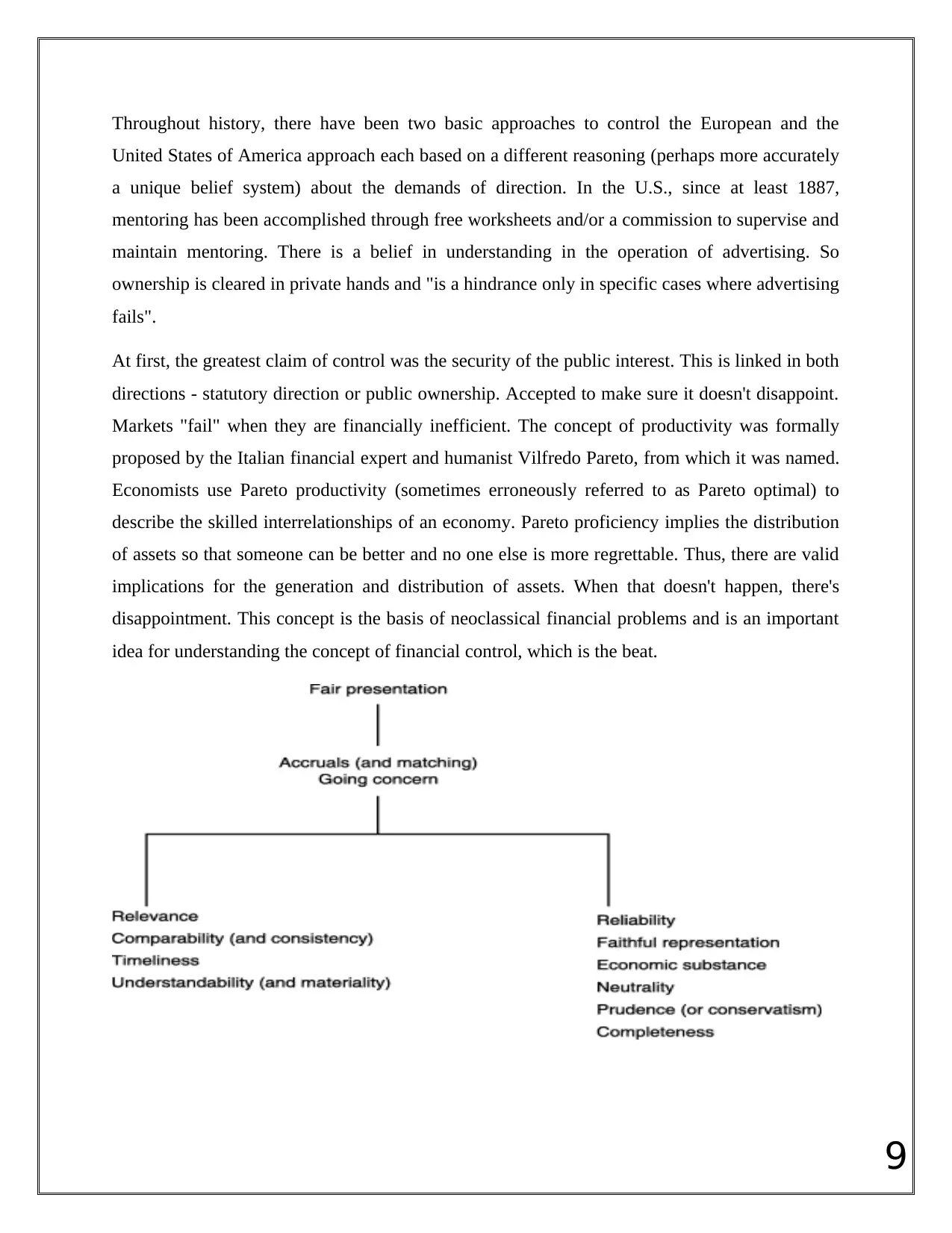

Throughout history, there have been two basic approaches to control the European and the

United States of America approach each based on a different reasoning (perhaps more accurately

a unique belief system) about the demands of direction. In the U.S., since at least 1887,

mentoring has been accomplished through free worksheets and/or a commission to supervise and

maintain mentoring. There is a belief in understanding in the operation of advertising. So

ownership is cleared in private hands and "is a hindrance only in specific cases where advertising

fails".

At first, the greatest claim of control was the security of the public interest. This is linked in both

directions - statutory direction or public ownership. Accepted to make sure it doesn't disappoint.

Markets "fail" when they are financially inefficient. The concept of productivity was formally

proposed by the Italian financial expert and humanist Vilfredo Pareto, from which it was named.

Economists use Pareto productivity (sometimes erroneously referred to as Pareto optimal) to

describe the skilled interrelationships of an economy. Pareto proficiency implies the distribution

of assets so that someone can be better and no one else is more regrettable. Thus, there are valid

implications for the generation and distribution of assets. When that doesn't happen, there's

disappointment. This concept is the basis of neoclassical financial problems and is an important

idea for understanding the concept of financial control, which is the beat.

Throughout history, there have been two basic approaches to control the European and the

United States of America approach each based on a different reasoning (perhaps more accurately

a unique belief system) about the demands of direction. In the U.S., since at least 1887,

mentoring has been accomplished through free worksheets and/or a commission to supervise and

maintain mentoring. There is a belief in understanding in the operation of advertising. So

ownership is cleared in private hands and "is a hindrance only in specific cases where advertising

fails".

At first, the greatest claim of control was the security of the public interest. This is linked in both

directions - statutory direction or public ownership. Accepted to make sure it doesn't disappoint.

Markets "fail" when they are financially inefficient. The concept of productivity was formally

proposed by the Italian financial expert and humanist Vilfredo Pareto, from which it was named.

Economists use Pareto productivity (sometimes erroneously referred to as Pareto optimal) to

describe the skilled interrelationships of an economy. Pareto proficiency implies the distribution

of assets so that someone can be better and no one else is more regrettable. Thus, there are valid

implications for the generation and distribution of assets. When that doesn't happen, there's

disappointment. This concept is the basis of neoclassical financial problems and is an important

idea for understanding the concept of financial control, which is the beat.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

Public interest theories:

Proponents of the openly interested control hypothesis argue that the reason is that some public

desired result is achieved that would not have been obtained if given the chance to show it. The

regulation was developed in response to the requirement to publicly correct waste. And unfair

markets. In this way, open directions are sought, contradicting private, interest-related

destinations. This was the popular direction until the 1960s, and many disciples remain today.

Determining what constitutes public interest is considered to be a normative statement in most

cases, so advocates of active speculation will challenge this approach if they acknowledge that

the objective goals of determining regulation are unthinkable; no A prerequisite for a fair

distinction between open positions. There are other charges at the foot of the open-ended,

engaging approach. These include attention coordinated with the controller itself.

Often, the controller will make it clear which exercises are considered acceptable and which

cannot be fully implemented, with the last mentioned imposing extreme penalties. Examples

include work and safety controls that businesses must adhere to enforcing strict standards. There

are some problems with this administrative procedure. First, controllers may be targeted for

capture due to the close connection between controllers and supervised development. Walker

(1987) argues that this is what happened in the early improvement cases of the Australian

Accounting Standards Audit Committee. Furthermore, such procedures often lead to overly

restrictive and inflexible, and even to extension of the rules. Third, choosing the right measure is

often very troublesome. In this case, standard setting should be balanced against the possibility

of anticompetitive behavior that is, requiring the standard to be so uniform that it is different.

(Alsharari, 2019).

High-quality execution by proficient bookkeepers benefits the economy and society by

facilitating the productive distribution and management of private and public sector assets, as

well as the operation of budgets and capital markets, and through these benefiting a generation.

For a long time to come, how to control bookkeeping calls was the topic of much talk, and a lot

of noteworthy happened as skilled accountants, their clients, skilled bookkeepers and

governments sought assurances the change. The major continues to provide high-quality

management and contribute to financial growth and development.

Public interest theories:

Proponents of the openly interested control hypothesis argue that the reason is that some public

desired result is achieved that would not have been obtained if given the chance to show it. The

regulation was developed in response to the requirement to publicly correct waste. And unfair

markets. In this way, open directions are sought, contradicting private, interest-related

destinations. This was the popular direction until the 1960s, and many disciples remain today.

Determining what constitutes public interest is considered to be a normative statement in most

cases, so advocates of active speculation will challenge this approach if they acknowledge that

the objective goals of determining regulation are unthinkable; no A prerequisite for a fair

distinction between open positions. There are other charges at the foot of the open-ended,

engaging approach. These include attention coordinated with the controller itself.

Often, the controller will make it clear which exercises are considered acceptable and which

cannot be fully implemented, with the last mentioned imposing extreme penalties. Examples

include work and safety controls that businesses must adhere to enforcing strict standards. There

are some problems with this administrative procedure. First, controllers may be targeted for

capture due to the close connection between controllers and supervised development. Walker

(1987) argues that this is what happened in the early improvement cases of the Australian

Accounting Standards Audit Committee. Furthermore, such procedures often lead to overly

restrictive and inflexible, and even to extension of the rules. Third, choosing the right measure is

often very troublesome. In this case, standard setting should be balanced against the possibility

of anticompetitive behavior that is, requiring the standard to be so uniform that it is different.

(Alsharari, 2019).

High-quality execution by proficient bookkeepers benefits the economy and society by

facilitating the productive distribution and management of private and public sector assets, as

well as the operation of budgets and capital markets, and through these benefiting a generation.

For a long time to come, how to control bookkeeping calls was the topic of much talk, and a lot

of noteworthy happened as skilled accountants, their clients, skilled bookkeepers and

governments sought assurances the change. The major continues to provide high-quality

management and contribute to financial growth and development.

11

Recognizing the importance of this issue, the International Federation of Accountants

(IFAC) has formalized in this dossier skilled bookkeepers, acting within a public

interest, and must play an active role.

Each occupation is characterized by the information, competence, demeanor and ethics of

the profession. Control over a calling may be a specific response to the requirements that the

calling individual must meet certain criteria. The requirements and nature of such

regulations are subordinate to the specific calling and advertising conditions under which

they operate. Like other professions, the maintainability of a bookkeeping profession

depends on the quality of its personal management and the ability of the profession to

respond effectively and efficiently to economic and social demands. Control seeks to ensure

correctness and consistency in the quality of accounting services. (Anderson, 2021).

There are a number of reasons why guidance may be needed to ensure that appropriate

quality is provided within the scope of the project Advertise accounting services. This

includes enforcing ethical rules and professional benchmarks, and must communicate with

non-contracted clients of bookkeeping, such as financial specialists and leaseholders. For

example, in later years, the moral failure of the called few and the resulting need for

certainty in budget announcements led to changes in many parts of the world within the

calling's control.

References:

1. Deegan, C. M. (2019). Legitimacy theory: Despite its enduring popularity and

contribution, time is right for a necessary makeover. Accounting, Auditing &

Accountability Journal.

2. Beske, F., Haustein, E., & Lorson, P. C. (2019). Materiality analysis in sustainability

and integrated reports. Sustainability Accounting, Management and Policy Journal.

3. Uscinski, J. E. (2020). Conspiracy theories: A primer. Rowman & Littlefield

Publishers.

4. Adams, C. A., & Larrinaga, C. (2019). Progress: engaging with organisations in

pursuit of improved sustainability accounting and performance. Accounting,

Auditing & Accountability Journal.

Recognizing the importance of this issue, the International Federation of Accountants

(IFAC) has formalized in this dossier skilled bookkeepers, acting within a public

interest, and must play an active role.

Each occupation is characterized by the information, competence, demeanor and ethics of

the profession. Control over a calling may be a specific response to the requirements that the

calling individual must meet certain criteria. The requirements and nature of such

regulations are subordinate to the specific calling and advertising conditions under which

they operate. Like other professions, the maintainability of a bookkeeping profession

depends on the quality of its personal management and the ability of the profession to

respond effectively and efficiently to economic and social demands. Control seeks to ensure

correctness and consistency in the quality of accounting services. (Anderson, 2021).

There are a number of reasons why guidance may be needed to ensure that appropriate

quality is provided within the scope of the project Advertise accounting services. This

includes enforcing ethical rules and professional benchmarks, and must communicate with

non-contracted clients of bookkeeping, such as financial specialists and leaseholders. For

example, in later years, the moral failure of the called few and the resulting need for

certainty in budget announcements led to changes in many parts of the world within the

calling's control.

References:

1. Deegan, C. M. (2019). Legitimacy theory: Despite its enduring popularity and

contribution, time is right for a necessary makeover. Accounting, Auditing &

Accountability Journal.

2. Beske, F., Haustein, E., & Lorson, P. C. (2019). Materiality analysis in sustainability

and integrated reports. Sustainability Accounting, Management and Policy Journal.

3. Uscinski, J. E. (2020). Conspiracy theories: A primer. Rowman & Littlefield

Publishers.

4. Adams, C. A., & Larrinaga, C. (2019). Progress: engaging with organisations in

pursuit of improved sustainability accounting and performance. Accounting,

Auditing & Accountability Journal.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.