Agency Theory in Compensation and Audit Gaps: An Analytical Review

VerifiedAdded on 2020/06/03

|13

|3685

|42

AI Summary

The essay evaluates the impact of agency theory within business management, particularly focusing on its application in designing compensation packages. It discusses how agency theory's focus on aligning interests between principals (shareholders) and agents (managers) influences compensation structures to mitigate risks associated with manager risk aversion. Furthermore, the analysis delves into the audit expectations gap, examining how stakeholder perceptions of auditor performance can lead to misunderstandings between auditors' roles and stakeholders' expectations. By contrasting agency theory with stewardship theory, which assumes that managers inherently act in the best interests of shareholders, this essay highlights the potential for stewardship theory to address deficiencies observed under agency theory. The investigation uses a variety of academic sources, including journal articles and books, alongside practical examples from corporate practices to provide a comprehensive understanding of how these theoretical frameworks can be effectively applied within organizational settings.

Research in Accounting Practice

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

QUESTION 1: INTERNET FINANCIAL REPORTING...............................................................1

a. Giving detailed information from the statistical tests mentioned in the article.......................1

b. Stating the advantages and disadvantages of the approaches mentioned in the study............1

c. Explaining which approach is better along with the purpose of studies..................................2

QUESTION 2: AGENCY THEORY, STEWARDSHIP AND EXECUTIVE COMPENSATION

.........................................................................................................................................................3

a. Presenting the assumptions of traditional (positive) agency theory........................................3

b. Assessing the impact of agency theory on the structuring aspect of compensation packages 3

c. Stating employee’s attitude towards the risk and their desired compensation package..........4

d. Identifying internal problems which company might face if executive compensation is

viewed as excessive.....................................................................................................................4

e. Stating the challenge associated with the assumption of agency theory...............................4

f. Explaining the deficiencies in agency theory and presenting alternative theories that can be

undertaken to overcome the same................................................................................................5

g. Assessing the extent to which reporting which is required for stewardship changed over

time..............................................................................................................................................5

QUESTION 3 RESEARCH IN AUDITING http://growingscience.com/beta/ac/2334-the-

expectation-gap-in-auditing.html.....................................................................................................6

a....................................................................................................................................................6

b...................................................................................................................................................7

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

QUESTION 1: INTERNET FINANCIAL REPORTING...............................................................1

a. Giving detailed information from the statistical tests mentioned in the article.......................1

b. Stating the advantages and disadvantages of the approaches mentioned in the study............1

c. Explaining which approach is better along with the purpose of studies..................................2

QUESTION 2: AGENCY THEORY, STEWARDSHIP AND EXECUTIVE COMPENSATION

.........................................................................................................................................................3

a. Presenting the assumptions of traditional (positive) agency theory........................................3

b. Assessing the impact of agency theory on the structuring aspect of compensation packages 3

c. Stating employee’s attitude towards the risk and their desired compensation package..........4

d. Identifying internal problems which company might face if executive compensation is

viewed as excessive.....................................................................................................................4

e. Stating the challenge associated with the assumption of agency theory...............................4

f. Explaining the deficiencies in agency theory and presenting alternative theories that can be

undertaken to overcome the same................................................................................................5

g. Assessing the extent to which reporting which is required for stewardship changed over

time..............................................................................................................................................5

QUESTION 3 RESEARCH IN AUDITING http://growingscience.com/beta/ac/2334-the-

expectation-gap-in-auditing.html.....................................................................................................6

a....................................................................................................................................................6

b...................................................................................................................................................7

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

In the present era, accounting is one of the main function that is undertaken by the

business units to record, measure, classify, summarize, interpret and communicating monetary

information. Along with this, auditing is another aspect which in turn highly associated and

based on accounting information. Now, stakeholders lay high level of emphasis on undertaking

audited statements for decision making. Thus, by considering such aspect every business unit

makes focus on conducting audit of financial statements at the end of accounting year. The

present report is based on different scholarly articles which will shed light on the aspects of

agency theory, stewardship and executive compensation. Besides this, report will provide deeper

insight about the extent to which specific articles have furnished appropriate information

concerning the issue.

QUESTION 1: INTERNET FINANCIAL REPORTING

a. Giving detailed information from the statistical tests mentioned in the article

From the evaluation of article, Kuruppu et al. (2015), it has been assessed that along with

the percentage, table 3 also depicts the views of respondents. Hence, in the various categories

such as company history, products & services as well as financial information views of

respondents have also been presented by the researcher through statistical test (Kuruppu and

et.al., 2015). Thus, by doing evaluation of extra information reader can get information about

respondent’s views in different category.

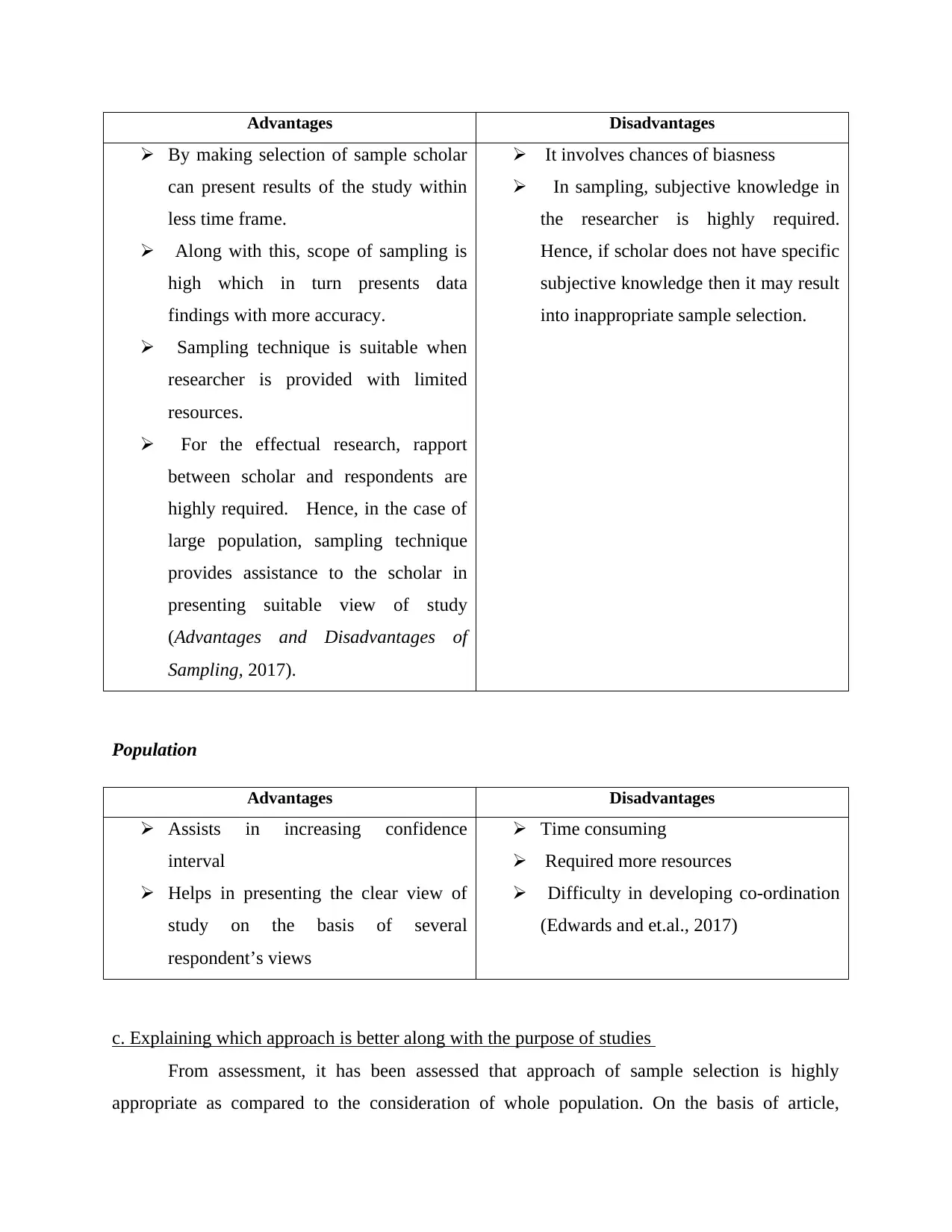

b. Stating the advantages and disadvantages of the approaches mentioned in the study

On the basis of the given case situation, one study considers sample, whereas other lays

emphasis on considering the whole population. Both the aspects have following advantages and

disadvantages such as:

Sampling: In sampling, scholar makes selection of group of people out of the whole population

for meeting the research goals as well as objectives.

In the present era, accounting is one of the main function that is undertaken by the

business units to record, measure, classify, summarize, interpret and communicating monetary

information. Along with this, auditing is another aspect which in turn highly associated and

based on accounting information. Now, stakeholders lay high level of emphasis on undertaking

audited statements for decision making. Thus, by considering such aspect every business unit

makes focus on conducting audit of financial statements at the end of accounting year. The

present report is based on different scholarly articles which will shed light on the aspects of

agency theory, stewardship and executive compensation. Besides this, report will provide deeper

insight about the extent to which specific articles have furnished appropriate information

concerning the issue.

QUESTION 1: INTERNET FINANCIAL REPORTING

a. Giving detailed information from the statistical tests mentioned in the article

From the evaluation of article, Kuruppu et al. (2015), it has been assessed that along with

the percentage, table 3 also depicts the views of respondents. Hence, in the various categories

such as company history, products & services as well as financial information views of

respondents have also been presented by the researcher through statistical test (Kuruppu and

et.al., 2015). Thus, by doing evaluation of extra information reader can get information about

respondent’s views in different category.

b. Stating the advantages and disadvantages of the approaches mentioned in the study

On the basis of the given case situation, one study considers sample, whereas other lays

emphasis on considering the whole population. Both the aspects have following advantages and

disadvantages such as:

Sampling: In sampling, scholar makes selection of group of people out of the whole population

for meeting the research goals as well as objectives.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Advantages Disadvantages

By making selection of sample scholar

can present results of the study within

less time frame.

Along with this, scope of sampling is

high which in turn presents data

findings with more accuracy.

Sampling technique is suitable when

researcher is provided with limited

resources.

For the effectual research, rapport

between scholar and respondents are

highly required. Hence, in the case of

large population, sampling technique

provides assistance to the scholar in

presenting suitable view of study

(Advantages and Disadvantages of

Sampling, 2017).

It involves chances of biasness

In sampling, subjective knowledge in

the researcher is highly required.

Hence, if scholar does not have specific

subjective knowledge then it may result

into inappropriate sample selection.

Population

Advantages Disadvantages

Assists in increasing confidence

interval

Helps in presenting the clear view of

study on the basis of several

respondent’s views

Time consuming

Required more resources

Difficulty in developing co-ordination

(Edwards and et.al., 2017)

c. Explaining which approach is better along with the purpose of studies

From assessment, it has been assessed that approach of sample selection is highly

appropriate as compared to the consideration of whole population. On the basis of article,

By making selection of sample scholar

can present results of the study within

less time frame.

Along with this, scope of sampling is

high which in turn presents data

findings with more accuracy.

Sampling technique is suitable when

researcher is provided with limited

resources.

For the effectual research, rapport

between scholar and respondents are

highly required. Hence, in the case of

large population, sampling technique

provides assistance to the scholar in

presenting suitable view of study

(Advantages and Disadvantages of

Sampling, 2017).

It involves chances of biasness

In sampling, subjective knowledge in

the researcher is highly required.

Hence, if scholar does not have specific

subjective knowledge then it may result

into inappropriate sample selection.

Population

Advantages Disadvantages

Assists in increasing confidence

interval

Helps in presenting the clear view of

study on the basis of several

respondent’s views

Time consuming

Required more resources

Difficulty in developing co-ordination

(Edwards and et.al., 2017)

c. Explaining which approach is better along with the purpose of studies

From assessment, it has been assessed that approach of sample selection is highly

appropriate as compared to the consideration of whole population. On the basis of article,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

presented by Kuruppu et al. (2015), sample section approach is highly significant because due to

having limitations of time, money and other resources it is not possible for the researcher to lay

emphasis on whole Sri Lanka.

QUESTION 2: AGENCY THEORY, STEWARDSHIP AND EXECUTIVE

COMPENSATION

a. Presenting the assumptions of traditional (positive) agency theory

Agency theory presents relationship that takes place between principals and agents in the

business. This theory of accounting makes focus on dealing with specific problems such as way

to align goals of principal which in turn may result into no conflicting situation.

Agency theory is based on the assumption that both principal and agents are motivated

through self-interest. On the basis of such aspect, if both the parties are motivated by

self-interest then agent will undertake self-interested objectives. In this, there is the

possibility that goals considered by the agent will in contrast to the principal

(Assumptions of agency theory, 2017). However, it is assumed that agents are performing

activities in the sole interest of principals.

Along with this, another assumption presents that principal has information regarding the

consequences of activities which are performed by agents.

Thus, both the above mentioned aspects may be served as an assumption on which agency

theory is based.

b. Assessing the impact of agency theory on the structuring aspect of compensation packages

From assessment, it has been identified that executive compensation is an agency

contract that takes place between the firm and its manager. The main motives of such contract

are to align the interest of both the parties such as owners and managers. Agency theory has

significant impact on compensation packages because it includes incentive, risk and decision

horizon considerations. Further, managers are considered as risk but in comparison to the

investors they do not prefer to diversify compensation risk (Bahli and Rivard, 2017). Hence, the

main issue which is associated with the designing of compensation contract is that usually

having limitations of time, money and other resources it is not possible for the researcher to lay

emphasis on whole Sri Lanka.

QUESTION 2: AGENCY THEORY, STEWARDSHIP AND EXECUTIVE

COMPENSATION

a. Presenting the assumptions of traditional (positive) agency theory

Agency theory presents relationship that takes place between principals and agents in the

business. This theory of accounting makes focus on dealing with specific problems such as way

to align goals of principal which in turn may result into no conflicting situation.

Agency theory is based on the assumption that both principal and agents are motivated

through self-interest. On the basis of such aspect, if both the parties are motivated by

self-interest then agent will undertake self-interested objectives. In this, there is the

possibility that goals considered by the agent will in contrast to the principal

(Assumptions of agency theory, 2017). However, it is assumed that agents are performing

activities in the sole interest of principals.

Along with this, another assumption presents that principal has information regarding the

consequences of activities which are performed by agents.

Thus, both the above mentioned aspects may be served as an assumption on which agency

theory is based.

b. Assessing the impact of agency theory on the structuring aspect of compensation packages

From assessment, it has been identified that executive compensation is an agency

contract that takes place between the firm and its manager. The main motives of such contract

are to align the interest of both the parties such as owners and managers. Agency theory has

significant impact on compensation packages because it includes incentive, risk and decision

horizon considerations. Further, managers are considered as risk but in comparison to the

investors they do not prefer to diversify compensation risk (Bahli and Rivard, 2017). Hence, the

main issue which is associated with the designing of compensation contract is that usually

current manager’s efforts not easily observable in the form of time. Due to which, problems are

occurred in relation to formation of basis for incentive contract.

Further, payoff observability aspect becomes difficult when it is assessed that manager’s

effort are set of activities rather than the single one. Along with this, some of the manager’s

activities have long run implications over others. Hence, for the attainment of an efficient

contract it is required to include both share price and net income. Thus, by considering all the

above depicted aspects it can be said that structuring aspect of compensation packages are highly

influenced from agency theory.

c. Stating employee’s attitude towards the risk and their desired compensation package

By doing analysis of agency theory, it has found that employees less prefers to take risk

which in turn shows that they are risk adverse. Hence, executive compensation plans or packages

are designed with the motive to control risk. Hence, for the development of desired

compensation plan or packages employees or executives lay focus on the adoption of risk

reducing approaches. Hence, it places emphasis on the inclusion of more than one performance

measure. Further, risk reducing approaches also include threshold level of performance in the

bonus plan (Nevo, Nevo and Pinsonneault, 2016). Desired compensation package of employees

spotlights on making available of stock options which in turn downsides the risk level

significantly. Along with this, employees also want that compensation committee sets the

amount by using relative performance evaluation technique.

d. Identifying internal problems which company might face if executive compensation is viewed

as excessive

The main problem which business unit faces in the case of executive compensation is the

misalignment of incentives between shareholders and their executive agents. When executive’s

compensation is viewed as excessive then firm faces conflicting situation from the side of

shareholders (Shi, Connelly and Hoskisson, 2017). In this regard, by offering shares to the

executives in the form of compensation firm can manage the interest of both the stakeholders.

e. Stating the challenge associated with the assumption of agency theory

Assumption of agency theory in relation to the motivational aspect of principal and

agent on the basis of their self-interest has been challenged. In other words, agency theory is

occurred in relation to formation of basis for incentive contract.

Further, payoff observability aspect becomes difficult when it is assessed that manager’s

effort are set of activities rather than the single one. Along with this, some of the manager’s

activities have long run implications over others. Hence, for the attainment of an efficient

contract it is required to include both share price and net income. Thus, by considering all the

above depicted aspects it can be said that structuring aspect of compensation packages are highly

influenced from agency theory.

c. Stating employee’s attitude towards the risk and their desired compensation package

By doing analysis of agency theory, it has found that employees less prefers to take risk

which in turn shows that they are risk adverse. Hence, executive compensation plans or packages

are designed with the motive to control risk. Hence, for the development of desired

compensation plan or packages employees or executives lay focus on the adoption of risk

reducing approaches. Hence, it places emphasis on the inclusion of more than one performance

measure. Further, risk reducing approaches also include threshold level of performance in the

bonus plan (Nevo, Nevo and Pinsonneault, 2016). Desired compensation package of employees

spotlights on making available of stock options which in turn downsides the risk level

significantly. Along with this, employees also want that compensation committee sets the

amount by using relative performance evaluation technique.

d. Identifying internal problems which company might face if executive compensation is viewed

as excessive

The main problem which business unit faces in the case of executive compensation is the

misalignment of incentives between shareholders and their executive agents. When executive’s

compensation is viewed as excessive then firm faces conflicting situation from the side of

shareholders (Shi, Connelly and Hoskisson, 2017). In this regard, by offering shares to the

executives in the form of compensation firm can manage the interest of both the stakeholders.

e. Stating the challenge associated with the assumption of agency theory

Assumption of agency theory in relation to the motivational aspect of principal and

agent on the basis of their self-interest has been challenged. In other words, agency theory is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

objected on the basis of assumption pertaining to self-interested agents who are making efforts to

maximize their personal economic wealth (Assumptions of agency theory, 2017). The main

reason behind such aspect is that interest level of both principal and agents differ significantly.

Along with this, it is the accountability of manager to either set aside their self-interest or

perform activities in such a manner that enhances the wealth of principal. In accordance with

such aspect assumption of agency theory is criticized and emphasis has been laid on the

employment of stewardship framework.

f. Explaining the deficiencies in agency theory and presenting alternative theories that can be

undertaken to overcome the same

Agency theory presents or facilitates obedience at different levels and assists in aligning

managerial aspects with diffused stakeholders. Along with this, agency theory helps in

presenting unexplainable action through the means of agentic and autonomous state. It may be

served as a market and process driven approach which in turn helps in controlling the

performance in an effectual way. However, along with the above benefits there are some aspects

which in turn closely influence the significance of agency theory. In the context of ethical

aspects or implications, agency theory removes personal accountabilities from the individuals

who commit violence related activities under pressure (Agency theory, 2017). In addition to this,

anti-social implications are other main aspects that affect the importance of agency theory.

Moreover, sometimes this theory is undertaken by the manager in negative context through the

manipulation into agentic state.

Hence, by undertaking stakeholder and stewardship theory business unit can overcome

the deficiencies of agency framework. Moreover, stakeholder theory is highly associated with the

aspect of organizational management as well as ethics. Such theoretical framework directly

addresses morals and ethical values through which organizational aspects can be managed in a

prominent way. Along with this, stewardship theory may be served as a best alternative of

agency framework (Prosman and et.al., 2016). This theory presents certain mechanism which in

turn helps in reducing agency loss pertaining to executive compensation, benefits etc. Moreover,

on the basis of such theory firm rewards manager through financially or offering shares. This in

turn aligns financial interest of executives and encourages them to make their best efforts while

carry out business activities as well as functions.

maximize their personal economic wealth (Assumptions of agency theory, 2017). The main

reason behind such aspect is that interest level of both principal and agents differ significantly.

Along with this, it is the accountability of manager to either set aside their self-interest or

perform activities in such a manner that enhances the wealth of principal. In accordance with

such aspect assumption of agency theory is criticized and emphasis has been laid on the

employment of stewardship framework.

f. Explaining the deficiencies in agency theory and presenting alternative theories that can be

undertaken to overcome the same

Agency theory presents or facilitates obedience at different levels and assists in aligning

managerial aspects with diffused stakeholders. Along with this, agency theory helps in

presenting unexplainable action through the means of agentic and autonomous state. It may be

served as a market and process driven approach which in turn helps in controlling the

performance in an effectual way. However, along with the above benefits there are some aspects

which in turn closely influence the significance of agency theory. In the context of ethical

aspects or implications, agency theory removes personal accountabilities from the individuals

who commit violence related activities under pressure (Agency theory, 2017). In addition to this,

anti-social implications are other main aspects that affect the importance of agency theory.

Moreover, sometimes this theory is undertaken by the manager in negative context through the

manipulation into agentic state.

Hence, by undertaking stakeholder and stewardship theory business unit can overcome

the deficiencies of agency framework. Moreover, stakeholder theory is highly associated with the

aspect of organizational management as well as ethics. Such theoretical framework directly

addresses morals and ethical values through which organizational aspects can be managed in a

prominent way. Along with this, stewardship theory may be served as a best alternative of

agency framework (Prosman and et.al., 2016). This theory presents certain mechanism which in

turn helps in reducing agency loss pertaining to executive compensation, benefits etc. Moreover,

on the basis of such theory firm rewards manager through financially or offering shares. This in

turn aligns financial interest of executives and encourages them to make their best efforts while

carry out business activities as well as functions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

g. Assessing the extent to which reporting which is required for stewardship changed over time

Through investigation, it has been identified that, financial reporting aspect helps in

meeting the objectives pertaining to both accountability and stewardship assessment. Hence,

from evaluation it has found that within the less than three decades financial reporting aspect

shifted to new paradigm. It mainly includes two new premises which in turn decrease the role of

P&L to the significant level. Moreover, new paradigm entails that accounting is basically

valuation rather than a measurement system (Krzeminska and Zeyen, 2017). In addition to this,

new aspect highlights the importance of balance sheet as it offers or provides investors with

summarized information regarding the expected outcomes pertaining to the future.

QUESTION 3 RESEARCH IN AUDITING

a.

i. Introduction and literature

In the introductory section, researcher depicted that auditors and public has different

opinions regarding the roles as well as accountability of auditors. However, in the literature

review section high level of emphasis has been placed by the scholar of management and audit

group rather than other stakeholders such as public, investors etc. Hence, by developing specific

themes on the basis of research aims and objectives researcher would become able to present

findings in a prominent way.

ii. Methodology

In order to identify and evaluate the expectation gap in auditing survey has been

conducted by the researcher. Hence, survey technique is highly effectual which in turn helps in

deriving suitable solution. However, in survey, emphasis has been laid by the researcher on

assessing the viewpoints of auditors or group and management of privately held firms. Hence,

investors or shareholders are the main stakeholders who consider audited statements and having

some expectation in relation to the roles and responsibilities of auditors (Kangarluie and

Aalizadeh, 2017). Thus, scholar would become able to gain deeper insight about audit

expectation gap if investors also take part in survey.

Through investigation, it has been identified that, financial reporting aspect helps in

meeting the objectives pertaining to both accountability and stewardship assessment. Hence,

from evaluation it has found that within the less than three decades financial reporting aspect

shifted to new paradigm. It mainly includes two new premises which in turn decrease the role of

P&L to the significant level. Moreover, new paradigm entails that accounting is basically

valuation rather than a measurement system (Krzeminska and Zeyen, 2017). In addition to this,

new aspect highlights the importance of balance sheet as it offers or provides investors with

summarized information regarding the expected outcomes pertaining to the future.

QUESTION 3 RESEARCH IN AUDITING

a.

i. Introduction and literature

In the introductory section, researcher depicted that auditors and public has different

opinions regarding the roles as well as accountability of auditors. However, in the literature

review section high level of emphasis has been placed by the scholar of management and audit

group rather than other stakeholders such as public, investors etc. Hence, by developing specific

themes on the basis of research aims and objectives researcher would become able to present

findings in a prominent way.

ii. Methodology

In order to identify and evaluate the expectation gap in auditing survey has been

conducted by the researcher. Hence, survey technique is highly effectual which in turn helps in

deriving suitable solution. However, in survey, emphasis has been laid by the researcher on

assessing the viewpoints of auditors or group and management of privately held firms. Hence,

investors or shareholders are the main stakeholders who consider audited statements and having

some expectation in relation to the roles and responsibilities of auditors (Kangarluie and

Aalizadeh, 2017). Thus, scholar would become able to gain deeper insight about audit

expectation gap if investors also take part in survey.

iii. Hypotheses

Article which is considered for the purpose of such presents two hypotheses. One

hypothesis in related to differences in the perception of management and audit group regarding

roles as well as responsibilities of auditors. Further, other hypothesis is developed by the

researcher to assess the relationship in management and audit groups perception in relation to the

independence of an auditor. However, on the critical note, it can be mentioned that hypothesis

can be improved by the scholar through making focus on specific roles and responsibilities

identified under literature review section.

iv. Results

By doing analysis and on the basis of assessed outcome researcher mentioned that there is

the existence of significant statistical difference between the perception of management

(privately held companies) and audit group’s perception. Further, results shows that meaningful

relationship do not exist between management and audit group’s perception in relation to

auditor’s independence. Hence, result section can be improved by the researcher through

development of suitable hypothesis in line with the objectives and questions. Further, by

presenting findings in APA format researcher can enhance the effectualness of study.

v. Conclusion

In the concerned article, scholar concluded that expectation gap takes place in auditing

pertaining to the roles and responsibilities of auditors. However, in this section, conclusion has

not been mentioned by the researcher in accordance with the aims and objectives. Thus, scholar

can improve such section by presenting al the summary in a structured way on the basis of aims

and objectives.

b.

i. Defining population

By doing evaluation of research article, it has found that the population of concerned

study includes auditors, auditees and audit beneficiaries in Nigeria (Adeyemi and Olowookere

2011). Hence, in the concerned research paper efforts have been made by the researcher to

assess the audit expectation gaps that take place in Nigeria. On the basis of such aspect

Article which is considered for the purpose of such presents two hypotheses. One

hypothesis in related to differences in the perception of management and audit group regarding

roles as well as responsibilities of auditors. Further, other hypothesis is developed by the

researcher to assess the relationship in management and audit groups perception in relation to the

independence of an auditor. However, on the critical note, it can be mentioned that hypothesis

can be improved by the scholar through making focus on specific roles and responsibilities

identified under literature review section.

iv. Results

By doing analysis and on the basis of assessed outcome researcher mentioned that there is

the existence of significant statistical difference between the perception of management

(privately held companies) and audit group’s perception. Further, results shows that meaningful

relationship do not exist between management and audit group’s perception in relation to

auditor’s independence. Hence, result section can be improved by the researcher through

development of suitable hypothesis in line with the objectives and questions. Further, by

presenting findings in APA format researcher can enhance the effectualness of study.

v. Conclusion

In the concerned article, scholar concluded that expectation gap takes place in auditing

pertaining to the roles and responsibilities of auditors. However, in this section, conclusion has

not been mentioned by the researcher in accordance with the aims and objectives. Thus, scholar

can improve such section by presenting al the summary in a structured way on the basis of aims

and objectives.

b.

i. Defining population

By doing evaluation of research article, it has found that the population of concerned

study includes auditors, auditees and audit beneficiaries in Nigeria (Adeyemi and Olowookere

2011). Hence, in the concerned research paper efforts have been made by the researcher to

assess the audit expectation gaps that take place in Nigeria. On the basis of such aspect

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

population considered by the researcher is appropriate. Further, information provided can be

improved by the researcher through including accounting department authorities, which propose

rules, in the survey. The rationale behind this, such authorities have better idea regarding the

deficiencies that require or demand for improvement in the field of auditing.

ii. Validation of research instrument

Article considered for the evaluation purpose shows that identical methods have been

considered by the researcher with the motive to conduct reliable assessment. Such method is

highly effectual which in turn helps in making comparison of results with the prior study or

framework. In addition to this, for presenting the fair view of study and conducting survey in an

appropriate manner questions regarding responsibility, reliability etc. have been included by the

scholar in questionnaire. In this, there are some deficiencies which in turn affect the significance

of findings to some extent. Hence, improvement which is required in relation to questionnaire

includes question pertaining to recommendation and gap which respondents think in auditing

system irrespective of gb

iii. Stating the extent to which research questions and hypothesis is linked

Given article pertaining to Adeyemi and Olowookere (2011), shows that research

objectives or questions are highly linked with hypothesis. Moreover, the main objective behind

conducting investigation is to identify the extent to which audit exception gap takes place in

Nigeria from the viewpoints of respondents. Hence, hypothesis 2 was laid focus on evaluating

only one aspect in relation to reasonable assurance. . However, along with such gap some other

deficiencies take place in auditing. Thus, such study can be improved by the researcher by

placing emphasis on more than one factor which is considered or recognized as gap. Apart from

this, main objective of study is to get deeper insight about the existing responsibilities of

auditors, in the context of Nigeria. Such objective is highly associated with hypothesis 1 which

focuses on accountabilities i.e. fraud detection as well as prevention from the viewpoints of

respondents. Along with this, there are several accountabilities which auditors are expected to

fulfill. Thus, study and its findings can be improved by the scholar through making focus on

more than one factor.

iv. Aligning research questions with hypothesis

improved by the researcher through including accounting department authorities, which propose

rules, in the survey. The rationale behind this, such authorities have better idea regarding the

deficiencies that require or demand for improvement in the field of auditing.

ii. Validation of research instrument

Article considered for the evaluation purpose shows that identical methods have been

considered by the researcher with the motive to conduct reliable assessment. Such method is

highly effectual which in turn helps in making comparison of results with the prior study or

framework. In addition to this, for presenting the fair view of study and conducting survey in an

appropriate manner questions regarding responsibility, reliability etc. have been included by the

scholar in questionnaire. In this, there are some deficiencies which in turn affect the significance

of findings to some extent. Hence, improvement which is required in relation to questionnaire

includes question pertaining to recommendation and gap which respondents think in auditing

system irrespective of gb

iii. Stating the extent to which research questions and hypothesis is linked

Given article pertaining to Adeyemi and Olowookere (2011), shows that research

objectives or questions are highly linked with hypothesis. Moreover, the main objective behind

conducting investigation is to identify the extent to which audit exception gap takes place in

Nigeria from the viewpoints of respondents. Hence, hypothesis 2 was laid focus on evaluating

only one aspect in relation to reasonable assurance. . However, along with such gap some other

deficiencies take place in auditing. Thus, such study can be improved by the researcher by

placing emphasis on more than one factor which is considered or recognized as gap. Apart from

this, main objective of study is to get deeper insight about the existing responsibilities of

auditors, in the context of Nigeria. Such objective is highly associated with hypothesis 1 which

focuses on accountabilities i.e. fraud detection as well as prevention from the viewpoints of

respondents. Along with this, there are several accountabilities which auditors are expected to

fulfill. Thus, study and its findings can be improved by the scholar through making focus on

more than one factor.

iv. Aligning research questions with hypothesis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Research questions

Q.1 What gap users of financial statements have assessed that take place in the auditing aspect of

Nigeria?

Q.2 What are the duties, roles and responsibilities of auditors in Nigeria?

Q.3 How audit exception gap can be reduced in Nigeria?

Hence, all the above depicted questions are highly associated with hypotheses mentioned

in the study. Moreover, hypothesis 1 and 2 placed emphasis on auditor’s responsibilities as well

as gap in accordance with financial statements users. This aspect shows that hypothesis and

research questions are highly aligned.

CONCLUSION

By summing up this report, it has been articulated that agency theory has greater

influence on the designing aspect of compensation package. Thus, firm needs to consider the

aspects of agency theory when setting compensation. It can be summarized from agency theory

that personnel of firm have risk averse attitude which in turn influences shareholder’s wealth.

Besides this, it can be inferred that stewardship theory is the best framework which in turn assists

in avoiding the deficiencies of others. Further, it can be stated that by following APA style and

undertaking suitable methods researcher can present the fair view of investigation.

Q.1 What gap users of financial statements have assessed that take place in the auditing aspect of

Nigeria?

Q.2 What are the duties, roles and responsibilities of auditors in Nigeria?

Q.3 How audit exception gap can be reduced in Nigeria?

Hence, all the above depicted questions are highly associated with hypotheses mentioned

in the study. Moreover, hypothesis 1 and 2 placed emphasis on auditor’s responsibilities as well

as gap in accordance with financial statements users. This aspect shows that hypothesis and

research questions are highly aligned.

CONCLUSION

By summing up this report, it has been articulated that agency theory has greater

influence on the designing aspect of compensation package. Thus, firm needs to consider the

aspects of agency theory when setting compensation. It can be summarized from agency theory

that personnel of firm have risk averse attitude which in turn influences shareholder’s wealth.

Besides this, it can be inferred that stewardship theory is the best framework which in turn assists

in avoiding the deficiencies of others. Further, it can be stated that by following APA style and

undertaking suitable methods researcher can present the fair view of investigation.

REFERENCES

Books and Journals

Adeyemi, SB & Olowookere, JK 2011, 'Stakeholders' perception of audit performance gap in

Nigeria', International Journal of Accounting and Financial Reporting, vol. 1, no. 1, pp. 152-

72. Kangarluie, S & Aalizadeh, A 2017, 'The expectation gap in auditing', Accounting, vol.

3, no. 1, pp. 19-22.

Bahli, B. and Rivard, S., 2017. The Information Technology Outsourcing Risk: A Transaction

Cost and Agency Theory-Based Perspective. In Outsourcing and Offshoring Business

Services(pp. 53-77). Palgrave Macmillan, Cham.

Edwards, B. and et.al., 2017. Building research and evaluation capacity in population health: the

NSW Health approach. Health Promotion Journal of Australia. 27(3). pp.264-267.

Krzeminska, A. and Zeyen, A., 2017. A Stewardship Cost Perspective on the Governance of

Delegation Relationships: The Case of Social Franchising. Nonprofit and Voluntary Sector

Quarterly. 46(1). pp.71-91.

Kuruppu, N, Oyelere, P & Al-Jabri, H 2015, 'Internet financial reporting and disclosure practices

of publicly traded corporations: evidence from Sri Lanka', Accounting & Taxation, vol. 7,

no. 1, pp. 75-91.

Nevo, S., Nevo, D. and Pinsonneault, A., 2016. A Temporally Situated Self-Agency Theory of

Information Technology Reinvention. Mis Quarterly. 40(1).

Prosman, E. J. and et.al., 2016. Dealing with defaulting suppliers using behavioral based

governance methods: an agency theory perspective. Supply Chain Management: An

International Journal. 21(4). pp.499-511.

Shi, W., Connelly, B. L. and Hoskisson, R. E., 2017. External corporate governance and

financial fraud: cognitive evaluation theory insights on agency theory

prescriptions. Strategic Management Journal. 38(6). pp.1268-1286.

Books and Journals

Adeyemi, SB & Olowookere, JK 2011, 'Stakeholders' perception of audit performance gap in

Nigeria', International Journal of Accounting and Financial Reporting, vol. 1, no. 1, pp. 152-

72. Kangarluie, S & Aalizadeh, A 2017, 'The expectation gap in auditing', Accounting, vol.

3, no. 1, pp. 19-22.

Bahli, B. and Rivard, S., 2017. The Information Technology Outsourcing Risk: A Transaction

Cost and Agency Theory-Based Perspective. In Outsourcing and Offshoring Business

Services(pp. 53-77). Palgrave Macmillan, Cham.

Edwards, B. and et.al., 2017. Building research and evaluation capacity in population health: the

NSW Health approach. Health Promotion Journal of Australia. 27(3). pp.264-267.

Krzeminska, A. and Zeyen, A., 2017. A Stewardship Cost Perspective on the Governance of

Delegation Relationships: The Case of Social Franchising. Nonprofit and Voluntary Sector

Quarterly. 46(1). pp.71-91.

Kuruppu, N, Oyelere, P & Al-Jabri, H 2015, 'Internet financial reporting and disclosure practices

of publicly traded corporations: evidence from Sri Lanka', Accounting & Taxation, vol. 7,

no. 1, pp. 75-91.

Nevo, S., Nevo, D. and Pinsonneault, A., 2016. A Temporally Situated Self-Agency Theory of

Information Technology Reinvention. Mis Quarterly. 40(1).

Prosman, E. J. and et.al., 2016. Dealing with defaulting suppliers using behavioral based

governance methods: an agency theory perspective. Supply Chain Management: An

International Journal. 21(4). pp.499-511.

Shi, W., Connelly, B. L. and Hoskisson, R. E., 2017. External corporate governance and

financial fraud: cognitive evaluation theory insights on agency theory

prescriptions. Strategic Management Journal. 38(6). pp.1268-1286.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.