Managerial Accounting: Budgeting, Approaches & AGL Energy Ltd Analysis

VerifiedAdded on 2023/04/22

|17

|4252

|433

Report

AI Summary

This report provides a detailed analysis of budgeting in managerial accounting, focusing on the elements of a master budget and a comparison of top-down and bottom-up budgeting approaches. It discusses the application of these approaches to AGL Energy Ltd, ultimately recommending the most suitable method for the company. The report includes a budgeted income statement for AGL Energy Ltd for the financial year 2019, projecting business growth, and offers a comparative data analysis of actual and budgeted income statements for 2018 and 2019. The analysis concludes with evidence supporting the chosen budgeting approach for AGL Energy Ltd.

Running head: MANAGERIAL ACCOUNTING

Managerial Accounting

Name of the Student

Name of the University

Authors Note

Course ID

Managerial Accounting

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGERIAL ACCOUNTING

Executive Summary:

The current report is based on understanding the concept of budget. The report would place

focus on the master budgets and the elements that are involved in the master budget. An

explanatory statement would be accompanied regarding the top down budgeting approach

and the bottom down budgeting approach and selecting the best approach for AGL Energy

Ltd as the selected company for the report. Finally, a budgeted income statement for the

financial year of 2019 would be produced to project the growth of business. A conclusive

evidence for the analysis would be presented to accompany the best suitable choice of

budgeting approach for the AGL Energy Ltd.

Executive Summary:

The current report is based on understanding the concept of budget. The report would place

focus on the master budgets and the elements that are involved in the master budget. An

explanatory statement would be accompanied regarding the top down budgeting approach

and the bottom down budgeting approach and selecting the best approach for AGL Energy

Ltd as the selected company for the report. Finally, a budgeted income statement for the

financial year of 2019 would be produced to project the growth of business. A conclusive

evidence for the analysis would be presented to accompany the best suitable choice of

budgeting approach for the AGL Energy Ltd.

2MANAGERIAL ACCOUNTING

Table of Contents

Introduction:...............................................................................................................................3

Explanation of Elements of Budget:..........................................................................................3

Elements of Master Budget are as follows:............................................................................4

Comparison of Top Down and Bottom Up approach to budgeting procedure:.........................8

Top Down Budgeting in AGL Energy Ltd................................................................................9

Budgeted Income Statement of AGL Energy Ltd for 2019:....................................................11

Comparative data analysis of Actual and Budgeted Income Statement for 2018 & 2019:......11

Conclusion:..............................................................................................................................12

References:...............................................................................................................................14

Table of Contents

Introduction:...............................................................................................................................3

Explanation of Elements of Budget:..........................................................................................3

Elements of Master Budget are as follows:............................................................................4

Comparison of Top Down and Bottom Up approach to budgeting procedure:.........................8

Top Down Budgeting in AGL Energy Ltd................................................................................9

Budgeted Income Statement of AGL Energy Ltd for 2019:....................................................11

Comparative data analysis of Actual and Budgeted Income Statement for 2018 & 2019:......11

Conclusion:..............................................................................................................................12

References:...............................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGERIAL ACCOUNTING

Introduction:

The procedure of preparing and using budgets generally differs from company to

company. There are several important requirements in designing of budget planning and

control procedure. Budgeting acts as the means of co-ordinating the overall business

activities. While preparing the budgets there are numerous factors such as production

capacity, possibilities of sales, procurement of material and labour are balanced and co-

ordinated in a manner where all the activities are in respect of the objectives (Wildavsky,

2017). As a result of this budgeting committee is created that includes all the heads of

departments for solving a common problem. The necessity for co-ordinating the procedure of

planning is enormous.

The interrelation among the functional budgets represents that the budget cannot be

completed without referring to several others. Managers that are performing their job on day

to basis are most likely to create a better idea of what is attainable that is most likely to take

place in the upcoming period, local trading conditions (Rubin, 2015). The budget holders are

more likely inclined towards working a budget in which they are involved.

The present report is based on providing an explanation to the elements of master

budget. The report would also accompany a comparative analysis of the top down and bottom

up approach to the process of budgeting. Following the comparative analysis of the company

top down and bottom down approach the report would also provide a suitable discussion

regarding the application of either of the budgeting procedure in AGL Energy Ltd as the

chosen company for this report.

Explanation of Elements of Budget:

Master Budget

Introduction:

The procedure of preparing and using budgets generally differs from company to

company. There are several important requirements in designing of budget planning and

control procedure. Budgeting acts as the means of co-ordinating the overall business

activities. While preparing the budgets there are numerous factors such as production

capacity, possibilities of sales, procurement of material and labour are balanced and co-

ordinated in a manner where all the activities are in respect of the objectives (Wildavsky,

2017). As a result of this budgeting committee is created that includes all the heads of

departments for solving a common problem. The necessity for co-ordinating the procedure of

planning is enormous.

The interrelation among the functional budgets represents that the budget cannot be

completed without referring to several others. Managers that are performing their job on day

to basis are most likely to create a better idea of what is attainable that is most likely to take

place in the upcoming period, local trading conditions (Rubin, 2015). The budget holders are

more likely inclined towards working a budget in which they are involved.

The present report is based on providing an explanation to the elements of master

budget. The report would also accompany a comparative analysis of the top down and bottom

up approach to the process of budgeting. Following the comparative analysis of the company

top down and bottom down approach the report would also provide a suitable discussion

regarding the application of either of the budgeting procedure in AGL Energy Ltd as the

chosen company for this report.

Explanation of Elements of Budget:

Master Budget

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGERIAL ACCOUNTING

The master budget is regarded as the aggregation of all the lower level budgets that is

produced by an organization’s numerous financial areas which also includes the budgeted

financial statements, cash forecast and financial plan. Master budget is presented typically

either on monthly or quarterly basis and generally covers the company’s entire financial year

(Brown et al., 2016). While preparing the master budget an explanatory text might be

included that provides an explanation to an organizations strategic direction and how the

master budget would help in attaining the specific goals and the actions of management that

is required to achieve the budget. The master budget also includes the discussions regarding

the changes in the headcounts that is needed to attain the budget.

As stated by Schick, (2015) master budget is viewed as the central tool of planning for

the management team that is used to direct the activities of the corporation and also judging

the performance of its numerous responsibility centres. For the senior manager’s team, it is

customary for the team to review the number of repetitions of the master budget and

incorporating the modifications till it arrives at the budget which allocates the funds for

attaining the desired goals. Optimistically, a business uses the participative budgeting to

arrive at the final budget, but may also be imposed on the organizations by the senior

management with minute input from other employees (Ho, 2018). Once the master budget is

finalized the accounting staff might enter into the accounting software procedure with the

objective that the software can provide financial reports by comparing the budgets with the

actual results.

The master budget is regarded as the plan that is created to management the

manufacturing and sales activity for meeting the profitability and cash flow goals (Hernandez

et al., 2017). Creation of master budget needs careful coordination of the numerous budgets

that covers all the parts of a firm which makes the master budget realistic but not complacent.

The master budget is regarded as the aggregation of all the lower level budgets that is

produced by an organization’s numerous financial areas which also includes the budgeted

financial statements, cash forecast and financial plan. Master budget is presented typically

either on monthly or quarterly basis and generally covers the company’s entire financial year

(Brown et al., 2016). While preparing the master budget an explanatory text might be

included that provides an explanation to an organizations strategic direction and how the

master budget would help in attaining the specific goals and the actions of management that

is required to achieve the budget. The master budget also includes the discussions regarding

the changes in the headcounts that is needed to attain the budget.

As stated by Schick, (2015) master budget is viewed as the central tool of planning for

the management team that is used to direct the activities of the corporation and also judging

the performance of its numerous responsibility centres. For the senior manager’s team, it is

customary for the team to review the number of repetitions of the master budget and

incorporating the modifications till it arrives at the budget which allocates the funds for

attaining the desired goals. Optimistically, a business uses the participative budgeting to

arrive at the final budget, but may also be imposed on the organizations by the senior

management with minute input from other employees (Ho, 2018). Once the master budget is

finalized the accounting staff might enter into the accounting software procedure with the

objective that the software can provide financial reports by comparing the budgets with the

actual results.

The master budget is regarded as the plan that is created to management the

manufacturing and sales activity for meeting the profitability and cash flow goals (Hernandez

et al., 2017). Creation of master budget needs careful coordination of the numerous budgets

that covers all the parts of a firm which makes the master budget realistic but not complacent.

5MANAGERIAL ACCOUNTING

Elements of Master Budget are as follows:

The master budget comprises of the following elements that are as follows;

a. Sales Budget

b. Direct Materials Budget

c. Direct Labour Budget

d. Production Budget

e. Manufacturing Overhead Budget

f. Selling and administrative budget

g. Capital acquisition budget

h. Cash Budget

i. Budgeted financial statements

Sales Budget: Sales budget provides an estimation that the sales unit along with the

estimated earnings from these sales. Budgeting is regarded as vital element for any business.

A business makes the use of sales budgets to help in development of goals, estimation of

earnings and forecasting of the production requirements. The sales budget creates an impact

on both the operating budgets and the overall master budget of an organization. Sales budget

is generally divided into quarterly estimations (Gallani et al., 2016). The critical elements of

the sales budget is the estimation of the unit of sales, price per unit and the allowance for

returns and discounts. Sales budget is often created by the management by considering the

market factors, present economic conditions and business specific production capacities.

Direct Materials Budget: The direct materials budget computes the materials that should be

purchased based on the time period, to meet the requirements of the production budget

(Downs, 2017). The production budget is presented either on the monthly basis or on the

annual basis. In the business that sells the products, the production budget may comprise of

Elements of Master Budget are as follows:

The master budget comprises of the following elements that are as follows;

a. Sales Budget

b. Direct Materials Budget

c. Direct Labour Budget

d. Production Budget

e. Manufacturing Overhead Budget

f. Selling and administrative budget

g. Capital acquisition budget

h. Cash Budget

i. Budgeted financial statements

Sales Budget: Sales budget provides an estimation that the sales unit along with the

estimated earnings from these sales. Budgeting is regarded as vital element for any business.

A business makes the use of sales budgets to help in development of goals, estimation of

earnings and forecasting of the production requirements. The sales budget creates an impact

on both the operating budgets and the overall master budget of an organization. Sales budget

is generally divided into quarterly estimations (Gallani et al., 2016). The critical elements of

the sales budget is the estimation of the unit of sales, price per unit and the allowance for

returns and discounts. Sales budget is often created by the management by considering the

market factors, present economic conditions and business specific production capacities.

Direct Materials Budget: The direct materials budget computes the materials that should be

purchased based on the time period, to meet the requirements of the production budget

(Downs, 2017). The production budget is presented either on the monthly basis or on the

annual basis. In the business that sells the products, the production budget may comprise of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGERIAL ACCOUNTING

all the costs that is occurred by the company and must be complied with reasonable care

(Kaplan & Atkinson, 2015). Or else, the outcome obtained might erroneously reflect an

excessive higher or lower requirements of cash to fund the purchase of materials.

Production Budgets: The production budget computes the number of units of products that

should be manufactured and it is obtained from the combination of sales forecast along with

the planned quantity of finished goods inventory to have in hand. Production budget as the

element of master budget is typically prepared to push the manufacturing system that is used

in the material requirements planning situation (Langfield-Smith et al., 2017). The production

budget is classically presented in either the monthly or quarterly format.

Manufacturing Overhead Budget: The manufacturing overhead budget comprises of all the

manufacturing costs apart from the other costs of direct materials and direct labour. The

information in the manufacturing overhead budget turns out the cost of goods sold that are in

line with the master budget (Elliott, 2017). The information presented in the manufacturing

overhead budget is treated as the most important for all the department because it might

comprise of large portion of total amount of company expenses.

Selling and administrative budget: This budget comprises of all the non-manufacturing

departments namely the sales, marketing, engineering and facilities department. In the

aggregate this budget is rival to the size of the production budget and requires considerable

attention (Otley, 2016). The selling and administrative expense budget is generally presented

either in the monthly or quarterly layout. Managers use the general level of the business

activities to ascertain the necessary level of expenditure. This comprises of the activity based

costing to ascertain the activities that are most likely to be required for sales level and capital

expenditure change.

all the costs that is occurred by the company and must be complied with reasonable care

(Kaplan & Atkinson, 2015). Or else, the outcome obtained might erroneously reflect an

excessive higher or lower requirements of cash to fund the purchase of materials.

Production Budgets: The production budget computes the number of units of products that

should be manufactured and it is obtained from the combination of sales forecast along with

the planned quantity of finished goods inventory to have in hand. Production budget as the

element of master budget is typically prepared to push the manufacturing system that is used

in the material requirements planning situation (Langfield-Smith et al., 2017). The production

budget is classically presented in either the monthly or quarterly format.

Manufacturing Overhead Budget: The manufacturing overhead budget comprises of all the

manufacturing costs apart from the other costs of direct materials and direct labour. The

information in the manufacturing overhead budget turns out the cost of goods sold that are in

line with the master budget (Elliott, 2017). The information presented in the manufacturing

overhead budget is treated as the most important for all the department because it might

comprise of large portion of total amount of company expenses.

Selling and administrative budget: This budget comprises of all the non-manufacturing

departments namely the sales, marketing, engineering and facilities department. In the

aggregate this budget is rival to the size of the production budget and requires considerable

attention (Otley, 2016). The selling and administrative expense budget is generally presented

either in the monthly or quarterly layout. Managers use the general level of the business

activities to ascertain the necessary level of expenditure. This comprises of the activity based

costing to ascertain the activities that are most likely to be required for sales level and capital

expenditure change.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGERIAL ACCOUNTING

Capital Acquisition Budget: The capital acquisition budget can be defined as the sub-set of

the capital outlay for the purpose of defence that normally consists of the two theoretical

categories. The funds that are set aside for satisfying the committed liabilities based on the

contracts signed in the earlier years and the funds that are meant for paying in relation to the

new acquisition relating to which contracts are signed in the present year (Renz, 2016). In

majority of the cases the delivery schedule of the capital assets spans for number of years. In

majority of the cases the delivery schedule of the capital assets ranges for numerous years

only the advance payment that is made during the year based on which the contract is signed

and the payment of outstanding amount is related to the pre-defined milestones and stages.

Under the capital acquisition budget if the delivery schedule is to be completed all through

the year then the contract that is signed represents the full amount that is paid for the notional

allocation of the new schemes.

Cash Budget: Cash budget forms the written statement of estimation relating to the future

cash position of the business. The budget predicts the amount of future period of cash receipts

received by the business from the future sources, cash disbursement for different purposes

and the resultant cash position usually on the monthly basis as the period of budgets develops

(Eldenburg et al., 2016). The cash budget is helpful in depicting the movement of cash where

the projected income statement offers all the sources of income to be recorded and for all the

class of expenditure that would be incurred during the stated period that shows the amount of

profit that is anticipated to be earned in the future period. The cash budget shows all the

anticipated inflow of cash together with the income and non-income sources namely the

receipts from the sale of stocks and the bonds that is received from the disposal of fixed

assets.

Budgeted Financial Statement: Budgeted financial statements might comprise of the

complete set of financial statements that includes the

Capital Acquisition Budget: The capital acquisition budget can be defined as the sub-set of

the capital outlay for the purpose of defence that normally consists of the two theoretical

categories. The funds that are set aside for satisfying the committed liabilities based on the

contracts signed in the earlier years and the funds that are meant for paying in relation to the

new acquisition relating to which contracts are signed in the present year (Renz, 2016). In

majority of the cases the delivery schedule of the capital assets spans for number of years. In

majority of the cases the delivery schedule of the capital assets ranges for numerous years

only the advance payment that is made during the year based on which the contract is signed

and the payment of outstanding amount is related to the pre-defined milestones and stages.

Under the capital acquisition budget if the delivery schedule is to be completed all through

the year then the contract that is signed represents the full amount that is paid for the notional

allocation of the new schemes.

Cash Budget: Cash budget forms the written statement of estimation relating to the future

cash position of the business. The budget predicts the amount of future period of cash receipts

received by the business from the future sources, cash disbursement for different purposes

and the resultant cash position usually on the monthly basis as the period of budgets develops

(Eldenburg et al., 2016). The cash budget is helpful in depicting the movement of cash where

the projected income statement offers all the sources of income to be recorded and for all the

class of expenditure that would be incurred during the stated period that shows the amount of

profit that is anticipated to be earned in the future period. The cash budget shows all the

anticipated inflow of cash together with the income and non-income sources namely the

receipts from the sale of stocks and the bonds that is received from the disposal of fixed

assets.

Budgeted Financial Statement: Budgeted financial statements might comprise of the

complete set of financial statements that includes the

8MANAGERIAL ACCOUNTING

a. Income statement

b. Balance Sheet

c. Cash flow statement

d. Retained earnings statement

The budgeted financial statement is compiled from the yearly budgeting model of the

business. They are regarded as useful estimation of the financial results, financial position

and cash flow statement of the business for numerous dates in future. The budgeted financial

statement is useful in creation of new budgeting model as one can understand the impact of

adjustment to the budgeting model of the financial statements (Cooper et al., 2017). The

management team while preparing the budgeted model introduces the financial statements

that are line with the financial expectations and what the business is financially capable of

attaining.

Comparison of Top Down and Bottom Up approach to budgeting procedure:

As stated by Kihn & Ihantola, (2015) the top down approach is regarded as the

starting point in the authoritative decision. A top down budgeting procedure implies that the

binding decision on budget aggregates is undertake before assigning the budgeting

expenditure inside the aggregate. As a concrete means the top down budgeting procedure

serves as the means of decisions that are taken in the cascading manner. The level of total

expenditure is ascertained prior to the allocation amid the main policies or before setting the

sectorial ceilings for the detailed division of expenditure inside each sector.

Under the top down approach the main actors are treated as the decision makers that

are responsible for formulating the efficient statute to suit the current problems. While

incorporating the budgeting, the top down budgeting approach involves the team of senior

management for developing a higher level budget for the whole organization (Malmi, 2016).

a. Income statement

b. Balance Sheet

c. Cash flow statement

d. Retained earnings statement

The budgeted financial statement is compiled from the yearly budgeting model of the

business. They are regarded as useful estimation of the financial results, financial position

and cash flow statement of the business for numerous dates in future. The budgeted financial

statement is useful in creation of new budgeting model as one can understand the impact of

adjustment to the budgeting model of the financial statements (Cooper et al., 2017). The

management team while preparing the budgeted model introduces the financial statements

that are line with the financial expectations and what the business is financially capable of

attaining.

Comparison of Top Down and Bottom Up approach to budgeting procedure:

As stated by Kihn & Ihantola, (2015) the top down approach is regarded as the

starting point in the authoritative decision. A top down budgeting procedure implies that the

binding decision on budget aggregates is undertake before assigning the budgeting

expenditure inside the aggregate. As a concrete means the top down budgeting procedure

serves as the means of decisions that are taken in the cascading manner. The level of total

expenditure is ascertained prior to the allocation amid the main policies or before setting the

sectorial ceilings for the detailed division of expenditure inside each sector.

Under the top down approach the main actors are treated as the decision makers that

are responsible for formulating the efficient statute to suit the current problems. While

incorporating the budgeting, the top down budgeting approach involves the team of senior

management for developing a higher level budget for the whole organization (Malmi, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGERIAL ACCOUNTING

Upon the creation of this budget, the values are allocated to the different departments and the

departments should take those numbers must create their own corresponding budgets inside

the confines of executive level.

Under the top down budget, the executive team is only involved and the lower

management are not required to participate in the budget. This helps in saving a significant

amount of time for those that are involved in the daily business activities instead of the

overall strategies of the organization (Henderson et al., 2015). However, under the top down

approach of budgeting those that are creating budget might not be involved in the daily

activities as a result of this it might not be aware of the specific expenditure needed. This

might give rise to problems for the departments that are looking for the resources that simply

does not fit in the top down budgeting.

The bottom approach on the other hand represents the process that of starting up the

individual department where the managers form a budget and then it forwards the budget

upwards for approval. The budget is either approved or revised or the same is sent back for

modification purpose and a master budget is created for numerous departments (Macve,

2015). As a general rule, the result of the approach increases the ownership of the budget

because the employees are acquainted with every department that is creating the budget. This

helps in promoting increased understanding communications and commitment on behalf of

the managers since they are directly engaged in the budgeting procedure.

Normally, the bottom up approach would lead to higher spending targets in

comparison to the top down approach and hence the reconciliation procedure would be

needed to generate the company wide budget where all the parts are added up appropriately.

Upon the creation of this budget, the values are allocated to the different departments and the

departments should take those numbers must create their own corresponding budgets inside

the confines of executive level.

Under the top down budget, the executive team is only involved and the lower

management are not required to participate in the budget. This helps in saving a significant

amount of time for those that are involved in the daily business activities instead of the

overall strategies of the organization (Henderson et al., 2015). However, under the top down

approach of budgeting those that are creating budget might not be involved in the daily

activities as a result of this it might not be aware of the specific expenditure needed. This

might give rise to problems for the departments that are looking for the resources that simply

does not fit in the top down budgeting.

The bottom approach on the other hand represents the process that of starting up the

individual department where the managers form a budget and then it forwards the budget

upwards for approval. The budget is either approved or revised or the same is sent back for

modification purpose and a master budget is created for numerous departments (Macve,

2015). As a general rule, the result of the approach increases the ownership of the budget

because the employees are acquainted with every department that is creating the budget. This

helps in promoting increased understanding communications and commitment on behalf of

the managers since they are directly engaged in the budgeting procedure.

Normally, the bottom up approach would lead to higher spending targets in

comparison to the top down approach and hence the reconciliation procedure would be

needed to generate the company wide budget where all the parts are added up appropriately.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGERIAL ACCOUNTING

Top Down Budgeting in AGL Energy Ltd

To apply the concept of Top Down Process in the AGL Energy the beginning point of

the preparing the budget represents the decision on the total expenditure. Instead of large

amount of individual spending, AGL Energy Ltd can aggregate expenses is ascertained with

the help of autonomous consideration relating to the size of budget (Khan, 2015). After this,

AGL Energy Ltd can allocate the total expenses to a number of vital sectors. For AGL

Energy Ltd under the top down approach the sales can be forecasted by using the wider

categories of products or components by breaking into successive narrow categories and

eventually under specific items. With the help of this method AGL Energy Ltd can approach

the factors such as sales channels, geographical regions of sales, customer categories or even

the specific customers that contributes significantly to AGL Energy Ltd sales revenue.

For AGL Energy Ltd, top down approach is more suitable for the company because it

may help in projecting the large aggregate such as GDP and the use of historical relation to

obtain the components of total namely the personal consumption expenses (Mullinova, 2016).

AGL Energy Ltd can consider the top down approach for using the macroeconomic

indicators for forecasting the total amount of sales and profit. The top down approach for

AGL Energy Ltd is more suitable in the preparation of budget where the role of finance

department may be centrally focused on establishing or monitoring the total expenses.

The division of available resources under every sector of AGL Energy Ltd can open

the door for discussion and the responsible line of departments may be provided with the

substantial freedom to propose the changes in the allocation within the organization (Dutta &

Patatoukas, 2016). The main purpose of implementing the top down budget in AGL Energy

Ltd is to introduce financial sustainability that are in consideration to the forefront of the

budgeting procedure. It can promote more informed decision for the aggregate level of

expenses to project revenue.

Top Down Budgeting in AGL Energy Ltd

To apply the concept of Top Down Process in the AGL Energy the beginning point of

the preparing the budget represents the decision on the total expenditure. Instead of large

amount of individual spending, AGL Energy Ltd can aggregate expenses is ascertained with

the help of autonomous consideration relating to the size of budget (Khan, 2015). After this,

AGL Energy Ltd can allocate the total expenses to a number of vital sectors. For AGL

Energy Ltd under the top down approach the sales can be forecasted by using the wider

categories of products or components by breaking into successive narrow categories and

eventually under specific items. With the help of this method AGL Energy Ltd can approach

the factors such as sales channels, geographical regions of sales, customer categories or even

the specific customers that contributes significantly to AGL Energy Ltd sales revenue.

For AGL Energy Ltd, top down approach is more suitable for the company because it

may help in projecting the large aggregate such as GDP and the use of historical relation to

obtain the components of total namely the personal consumption expenses (Mullinova, 2016).

AGL Energy Ltd can consider the top down approach for using the macroeconomic

indicators for forecasting the total amount of sales and profit. The top down approach for

AGL Energy Ltd is more suitable in the preparation of budget where the role of finance

department may be centrally focused on establishing or monitoring the total expenses.

The division of available resources under every sector of AGL Energy Ltd can open

the door for discussion and the responsible line of departments may be provided with the

substantial freedom to propose the changes in the allocation within the organization (Dutta &

Patatoukas, 2016). The main purpose of implementing the top down budget in AGL Energy

Ltd is to introduce financial sustainability that are in consideration to the forefront of the

budgeting procedure. It can promote more informed decision for the aggregate level of

expenses to project revenue.

11MANAGERIAL ACCOUNTING

The top down approach of budgeting is regarded as more suitable for the AGL Energy

Ltd because it has the potential of promoting clarity while setting priorities for the revenue

producing sector by assuring that the budget allocation comprises of constant setting of

priorities (Warren & Jones, 2018). For AGL Energy Ltd, while preparing the detailed items

which makes up the budget, there is a higher risks of losing sight for larger picture. There is

certain level of aggregation at the preliminary stages of budgeting, however AGL Energy Ltd

can allocate total expenses to some vital sectors that can help in detaching the policy issues

from the perspective of technical or operative character. Therefore, the top down procedure

for AGL Energy Ltd can result in creation of wider understanding and support the financial

policy issues amid the decision makers.

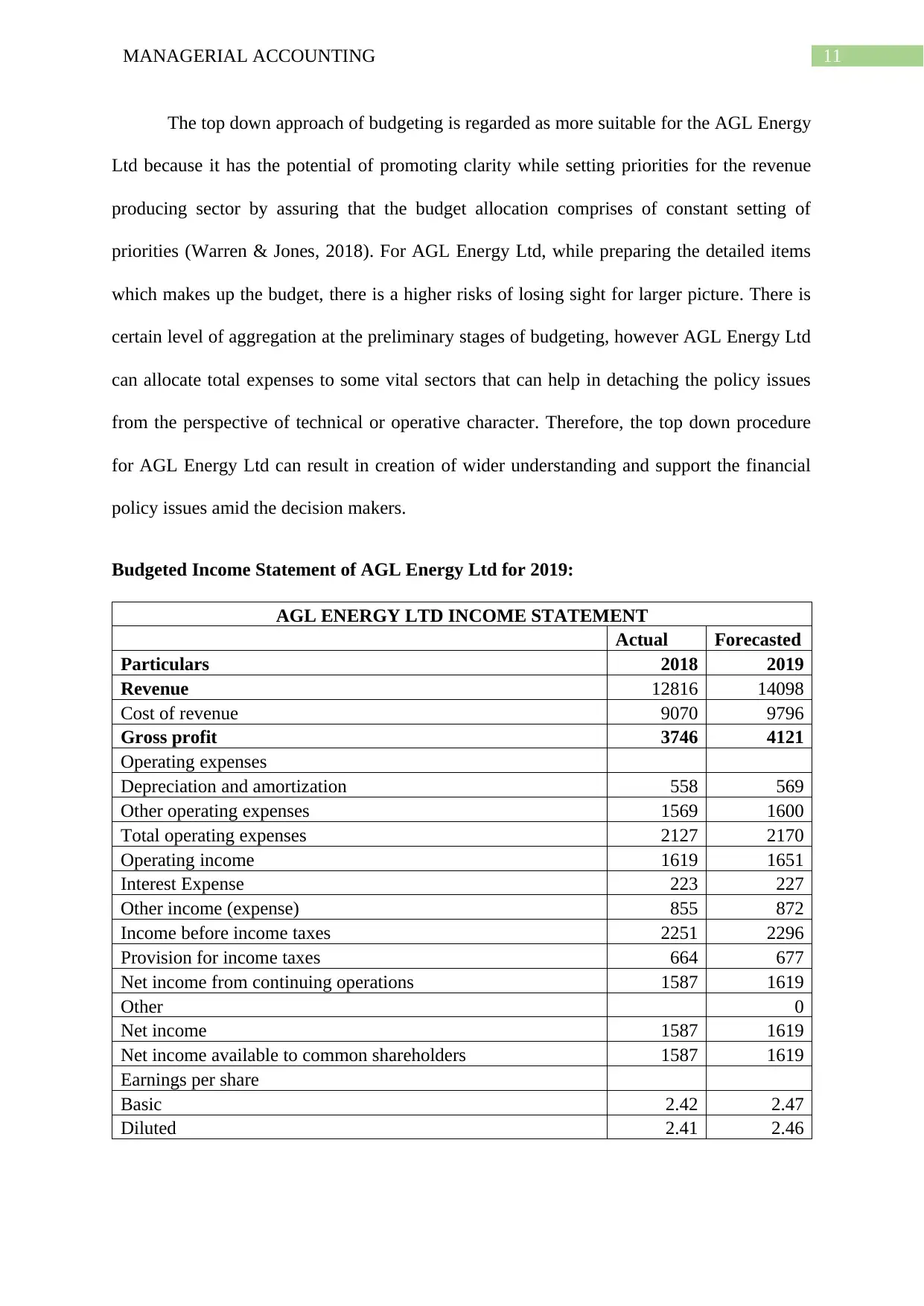

Budgeted Income Statement of AGL Energy Ltd for 2019:

AGL ENERGY LTD INCOME STATEMENT

Actual Forecasted

Particulars 2018 2019

Revenue 12816 14098

Cost of revenue 9070 9796

Gross profit 3746 4121

Operating expenses

Depreciation and amortization 558 569

Other operating expenses 1569 1600

Total operating expenses 2127 2170

Operating income 1619 1651

Interest Expense 223 227

Other income (expense) 855 872

Income before income taxes 2251 2296

Provision for income taxes 664 677

Net income from continuing operations 1587 1619

Other 0

Net income 1587 1619

Net income available to common shareholders 1587 1619

Earnings per share

Basic 2.42 2.47

Diluted 2.41 2.46

The top down approach of budgeting is regarded as more suitable for the AGL Energy

Ltd because it has the potential of promoting clarity while setting priorities for the revenue

producing sector by assuring that the budget allocation comprises of constant setting of

priorities (Warren & Jones, 2018). For AGL Energy Ltd, while preparing the detailed items

which makes up the budget, there is a higher risks of losing sight for larger picture. There is

certain level of aggregation at the preliminary stages of budgeting, however AGL Energy Ltd

can allocate total expenses to some vital sectors that can help in detaching the policy issues

from the perspective of technical or operative character. Therefore, the top down procedure

for AGL Energy Ltd can result in creation of wider understanding and support the financial

policy issues amid the decision makers.

Budgeted Income Statement of AGL Energy Ltd for 2019:

AGL ENERGY LTD INCOME STATEMENT

Actual Forecasted

Particulars 2018 2019

Revenue 12816 14098

Cost of revenue 9070 9796

Gross profit 3746 4121

Operating expenses

Depreciation and amortization 558 569

Other operating expenses 1569 1600

Total operating expenses 2127 2170

Operating income 1619 1651

Interest Expense 223 227

Other income (expense) 855 872

Income before income taxes 2251 2296

Provision for income taxes 664 677

Net income from continuing operations 1587 1619

Other 0

Net income 1587 1619

Net income available to common shareholders 1587 1619

Earnings per share

Basic 2.42 2.47

Diluted 2.41 2.46

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.