Corporate Accounting and Financial Analysis of AGL Energy Limited

VerifiedAdded on 2023/06/11

|12

|2996

|247

Report

AI Summary

This report provides a detailed corporate accounting analysis of AGL Energy Limited, an ASX-listed public company. It examines the company's cash flow statement, dissecting operating, investing, and financing activities, and analyzes changes in these areas over three years (2015-2017). The report also covers other comprehensive income statement items such as gains/losses on defined benefit plans and cash flow hedges. Furthermore, it delves into the accounting for corporate income tax, including tax expenses, benefits, deferred tax assets, and liabilities. The analysis includes insights into the company's financial strategies, such as share buybacks and dividend payments, and their impact on cash flow and shareholder value.

Running head: CORPORATE ACCOUNTING FOR AGL ENERGY LIMITED

Corporate Accounting for AGL Enrergy Limited

Name of the University:

Name of the Student:

Authosr Note:

Corporate Accounting for AGL Enrergy Limited

Name of the University:

Name of the Student:

Authosr Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE ACCOUNTING FOR AGL ENERGY LIMITED

Table of Contents

Cash Flow Statement.........................................................................................................2

Requirement (i):...............................................................................................................2

Requirement (ii):..............................................................................................................4

Other Comprehensive Income Statement:...........................................................................5

Requirement (iii):.............................................................................................................5

Requirement (iv):.............................................................................................................5

Requirement (v):..............................................................................................................6

Accounting for Corporate Income Tax:..........................................................................6

Requirement (vi):.............................................................................................................6

Requirement (vii):............................................................................................................6

Requirement (viii):...........................................................................................................7

Requirement ix.................................................................................................................7

Requirement x..................................................................................................................8

Requirement xi.................................................................................................................8

References..........................................................................................................................10

Table of Contents

Cash Flow Statement.........................................................................................................2

Requirement (i):...............................................................................................................2

Requirement (ii):..............................................................................................................4

Other Comprehensive Income Statement:...........................................................................5

Requirement (iii):.............................................................................................................5

Requirement (iv):.............................................................................................................5

Requirement (v):..............................................................................................................6

Accounting for Corporate Income Tax:..........................................................................6

Requirement (vi):.............................................................................................................6

Requirement (vii):............................................................................................................6

Requirement (viii):...........................................................................................................7

Requirement ix.................................................................................................................7

Requirement x..................................................................................................................8

Requirement xi.................................................................................................................8

References..........................................................................................................................10

2CORPORATE ACCOUNTING FOR AGL ENERGY LIMITED

Cash Flow Statement

Requirement (i):

AGL Energy Limited is the organization that has been selected for this assignment. AGL

Energy Limited is one of the major power suppliers in Australian and is a public company which

is listed on the Australian Securities Exchange (ASX) with a ticker symbol of AGL

(AGLEnergyLimited.com. 2018). The cash flow statement of an organization is the statement

which reflects the cash generating capacity of an organization through three different activities.

The cash flow statement of this organization is differentiated into three sections of activities that

are operational activities, investing activities and financial activities. The line item of the cash

flow statement and their segregation as per the activities are as follows:

Cash Flow from Operating Activities:

The line items within this section of the cash flow statement are mostly the direct

expenses or income associated to the operations (Balakrishnan, Watts and Zuo 2016). The items

which are included in the cash flow from operations are payment to the employees or the

suppliers, finance income, receipts from customers, any operational costs paid and other payment

or receipts during normal operation of the organization. The receipts from the customer are the

amount that is gained from credit sales. AGL Energy limited has $13,552 million of due from

customers in 2017 against $11,903 million in 2016 (Reid and Myddelton 2017). The payment to

the suppliers and the employees of the organization are its obligation against credit purchase and

salaries paid to employees. AGL Energy Limited observed a hike in the payment to suppliers and

employees as it implies further purchase and recruiting more people to its team. Finance income

on the other hand, is the amount which is repaid on demand within a specific timeline. The

Cash Flow Statement

Requirement (i):

AGL Energy Limited is the organization that has been selected for this assignment. AGL

Energy Limited is one of the major power suppliers in Australian and is a public company which

is listed on the Australian Securities Exchange (ASX) with a ticker symbol of AGL

(AGLEnergyLimited.com. 2018). The cash flow statement of an organization is the statement

which reflects the cash generating capacity of an organization through three different activities.

The cash flow statement of this organization is differentiated into three sections of activities that

are operational activities, investing activities and financial activities. The line item of the cash

flow statement and their segregation as per the activities are as follows:

Cash Flow from Operating Activities:

The line items within this section of the cash flow statement are mostly the direct

expenses or income associated to the operations (Balakrishnan, Watts and Zuo 2016). The items

which are included in the cash flow from operations are payment to the employees or the

suppliers, finance income, receipts from customers, any operational costs paid and other payment

or receipts during normal operation of the organization. The receipts from the customer are the

amount that is gained from credit sales. AGL Energy limited has $13,552 million of due from

customers in 2017 against $11,903 million in 2016 (Reid and Myddelton 2017). The payment to

the suppliers and the employees of the organization are its obligation against credit purchase and

salaries paid to employees. AGL Energy Limited observed a hike in the payment to suppliers and

employees as it implies further purchase and recruiting more people to its team. Finance income

on the other hand, is the amount which is repaid on demand within a specific timeline. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE ACCOUNTING FOR AGL ENERGY LIMITED

finance income of the company remained stable in 2017 in contrast to 2016. Finance cost on the

other hand is the liability of the organization which has increased for AGL Energy Limited in

2017. The dividend received by the company has also increased in 2017 against 2016.

Cash Flow from Investing Activities:

The line items under this section of the cash flow statement are generally the payment as

well as proceeds from property, plants & equipment, payment for investment in associates and

joint ventures, payment for other assets (Warren and Jones 2018). Such assets are the symbol of

the economic situation of the organization which provides the organization with economic

benefit. It is clearly seen that AGL Energy Limited has used a lot of cash in the investing

activities which implies that the company has been investing in plant, property and equipment

which is the sign of expansion. In case of this organization, the activities from investments have

both sale as well as purchase of plant and property but the purchase is much higher than the sale.

Other than this, the company has invested in other assets, associates and joint ventures and even

purchased some financial assets. The government grants received in 2017 is lower than that of

2016 (Watson 2015).

Cash Flow from Financial Activities:

The line items under this section are the payment of or the proceedings from the

borrowings, equity distributions as well as some other items. The line item ‘borrowing’ could be

defined as the amount paid to a borrower in the term of lending under the loan agreement. The

AGL Energy Limited clearly signifies that both the proceeding from as well as repayment of

borrowing has been increased significantly on the yearly basis (Brown, Preiato and Tarca 2014).

The company has paid a huge amount for buying back its own shares. This could be considered

finance income of the company remained stable in 2017 in contrast to 2016. Finance cost on the

other hand is the liability of the organization which has increased for AGL Energy Limited in

2017. The dividend received by the company has also increased in 2017 against 2016.

Cash Flow from Investing Activities:

The line items under this section of the cash flow statement are generally the payment as

well as proceeds from property, plants & equipment, payment for investment in associates and

joint ventures, payment for other assets (Warren and Jones 2018). Such assets are the symbol of

the economic situation of the organization which provides the organization with economic

benefit. It is clearly seen that AGL Energy Limited has used a lot of cash in the investing

activities which implies that the company has been investing in plant, property and equipment

which is the sign of expansion. In case of this organization, the activities from investments have

both sale as well as purchase of plant and property but the purchase is much higher than the sale.

Other than this, the company has invested in other assets, associates and joint ventures and even

purchased some financial assets. The government grants received in 2017 is lower than that of

2016 (Watson 2015).

Cash Flow from Financial Activities:

The line items under this section are the payment of or the proceedings from the

borrowings, equity distributions as well as some other items. The line item ‘borrowing’ could be

defined as the amount paid to a borrower in the term of lending under the loan agreement. The

AGL Energy Limited clearly signifies that both the proceeding from as well as repayment of

borrowing has been increased significantly on the yearly basis (Brown, Preiato and Tarca 2014).

The company has paid a huge amount for buying back its own shares. This could be considered

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE ACCOUNTING FOR AGL ENERGY LIMITED

as a strategic move of the organization wherein the company avoids some other party to interfere

with their internal matter through their power of holding the company’s share. Moreover, the

company also paid a massive amount as dividend to keep the loyalty and trust of its shareholders.

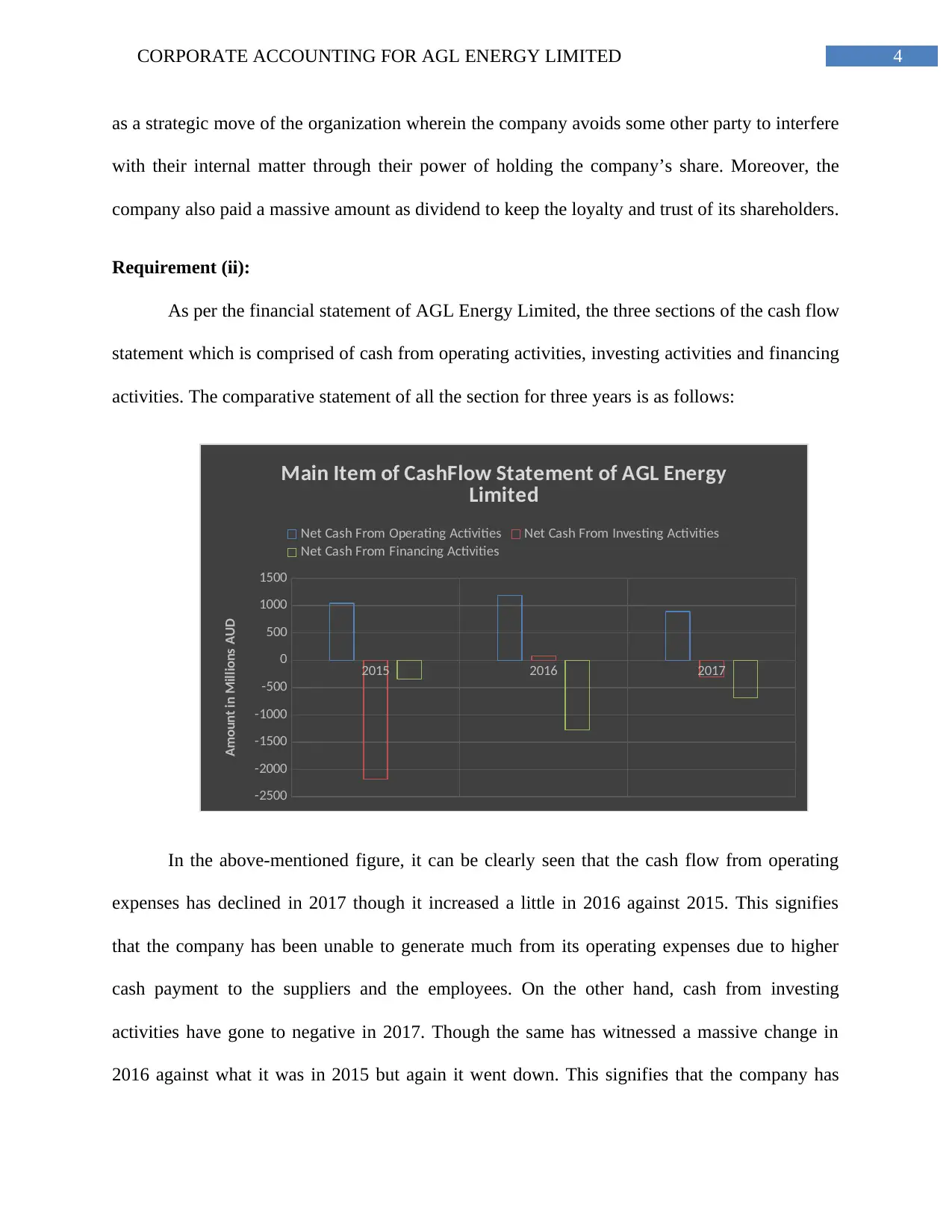

Requirement (ii):

As per the financial statement of AGL Energy Limited, the three sections of the cash flow

statement which is comprised of cash from operating activities, investing activities and financing

activities. The comparative statement of all the section for three years is as follows:

2015 2016 2017

-2500

-2000

-1500

-1000

-500

0

500

1000

1500

Main Item of CashFlow Statement of AGL Energy

Limited

Net Cash From Operating Activities Net Cash From Investing Activities

Net Cash From Financing Activities

Amount in Millions AUD

In the above-mentioned figure, it can be clearly seen that the cash flow from operating

expenses has declined in 2017 though it increased a little in 2016 against 2015. This signifies

that the company has been unable to generate much from its operating expenses due to higher

cash payment to the suppliers and the employees. On the other hand, cash from investing

activities have gone to negative in 2017. Though the same has witnessed a massive change in

2016 against what it was in 2015 but again it went down. This signifies that the company has

as a strategic move of the organization wherein the company avoids some other party to interfere

with their internal matter through their power of holding the company’s share. Moreover, the

company also paid a massive amount as dividend to keep the loyalty and trust of its shareholders.

Requirement (ii):

As per the financial statement of AGL Energy Limited, the three sections of the cash flow

statement which is comprised of cash from operating activities, investing activities and financing

activities. The comparative statement of all the section for three years is as follows:

2015 2016 2017

-2500

-2000

-1500

-1000

-500

0

500

1000

1500

Main Item of CashFlow Statement of AGL Energy

Limited

Net Cash From Operating Activities Net Cash From Investing Activities

Net Cash From Financing Activities

Amount in Millions AUD

In the above-mentioned figure, it can be clearly seen that the cash flow from operating

expenses has declined in 2017 though it increased a little in 2016 against 2015. This signifies

that the company has been unable to generate much from its operating expenses due to higher

cash payment to the suppliers and the employees. On the other hand, cash from investing

activities have gone to negative in 2017. Though the same has witnessed a massive change in

2016 against what it was in 2015 but again it went down. This signifies that the company has

5CORPORATE ACCOUNTING FOR AGL ENERGY LIMITED

been investing highly in purchase so as to expand its business and improve its operations further.

Finally, the cash from the financing activities also saw a huge decline in 2017. The same has

been negative consecutively from three years from 2015 to 2017 but the same has decreased in

comparison to the 2016 (Schaltegger and Burritt 2017). Hence, in 2017, AGL Energy Limited

saw decline cash from operating activities, negative cash flow from investing activities and

financing activities.

Other Comprehensive Income Statement:

Requirement (iii):

The line items within the comprehensive income statement of GL Energy Limited

comprises of gain or loss on the defined benefit plans, income tax benefit or expense, cash flow

hedges reserve (Chen, Ding and Xu 2014).

Requirement (iv):

The gain or loss on the defined benefit plans in other terms known as the actuarial gain or

loss. It could be considered as the actual evaluation of the value of the organization’s defied

obligation which might include pension plan (Nejad and Ahmad 2017). Such value is highly

influenced by the discount rate of the benefit payment’s present value or its rate of return. As this

is an actual assumption, hence the gains or losses from the same are amortized through the

comprehensive income statement in the annual reports. Moreover, the cash flow hedge that is

present in the statement is the step to contain the risk exposure due to parity in assets and

liabilities in cash flow (Christensen, Lee, Walker and Zeng 2015).

been investing highly in purchase so as to expand its business and improve its operations further.

Finally, the cash from the financing activities also saw a huge decline in 2017. The same has

been negative consecutively from three years from 2015 to 2017 but the same has decreased in

comparison to the 2016 (Schaltegger and Burritt 2017). Hence, in 2017, AGL Energy Limited

saw decline cash from operating activities, negative cash flow from investing activities and

financing activities.

Other Comprehensive Income Statement:

Requirement (iii):

The line items within the comprehensive income statement of GL Energy Limited

comprises of gain or loss on the defined benefit plans, income tax benefit or expense, cash flow

hedges reserve (Chen, Ding and Xu 2014).

Requirement (iv):

The gain or loss on the defined benefit plans in other terms known as the actuarial gain or

loss. It could be considered as the actual evaluation of the value of the organization’s defied

obligation which might include pension plan (Nejad and Ahmad 2017). Such value is highly

influenced by the discount rate of the benefit payment’s present value or its rate of return. As this

is an actual assumption, hence the gains or losses from the same are amortized through the

comprehensive income statement in the annual reports. Moreover, the cash flow hedge that is

present in the statement is the step to contain the risk exposure due to parity in assets and

liabilities in cash flow (Christensen, Lee, Walker and Zeng 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE ACCOUNTING FOR AGL ENERGY LIMITED

Requirement (v):

The comprehensive income statement could be considered as the expansion to the net

income. AGL Energy Limited provides this statement in order to reflect the detailed information

about the aforementioned items and their appropriate values. The primary reason of listing such

items to the comprehensive statement is that such items provide a holistic overview of the factors

that influences the operations of the business (De Simone 2016). However, being comprehensive

and holistic in nature, these items are not included in the income statement.

Accounting for Corporate Income Tax:

Requirement (vi):

Tax expense of an organization could be considered as one of the most important

obligation as it is directly concerned to the government of the country in which the organization

is operating in. AGL Energy had incurred tax expense in 2017 but it had tax benefit in 2016

which adjusted its tax obligation during the period. In 2017, the company had a tax expense of

$225 million while it had a tax benefit of $67 million in 2016 (Graham and Lin 2018).

Requirement (vii):

As per the financial statement of AGL Energy Limited in 2017, the organization

witnessed a profit in 2017 but incurred a loss before the computation of income tax in 2016. It

can be easily identified from the financial statement of the energy supplying firm that it charged

30% corporate tax rate on its profit before tax. Hence, it can be seen that the organization had a

profit of $764 million in 2017 and a corporate tax rate charged on it will get a tax expense of

$225 million. However, in case of the same in 2016, the organization incurred a loss of $474

million but had a tax benefit of $67 million (Marchini and D'Este 2015).

Requirement (v):

The comprehensive income statement could be considered as the expansion to the net

income. AGL Energy Limited provides this statement in order to reflect the detailed information

about the aforementioned items and their appropriate values. The primary reason of listing such

items to the comprehensive statement is that such items provide a holistic overview of the factors

that influences the operations of the business (De Simone 2016). However, being comprehensive

and holistic in nature, these items are not included in the income statement.

Accounting for Corporate Income Tax:

Requirement (vi):

Tax expense of an organization could be considered as one of the most important

obligation as it is directly concerned to the government of the country in which the organization

is operating in. AGL Energy had incurred tax expense in 2017 but it had tax benefit in 2016

which adjusted its tax obligation during the period. In 2017, the company had a tax expense of

$225 million while it had a tax benefit of $67 million in 2016 (Graham and Lin 2018).

Requirement (vii):

As per the financial statement of AGL Energy Limited in 2017, the organization

witnessed a profit in 2017 but incurred a loss before the computation of income tax in 2016. It

can be easily identified from the financial statement of the energy supplying firm that it charged

30% corporate tax rate on its profit before tax. Hence, it can be seen that the organization had a

profit of $764 million in 2017 and a corporate tax rate charged on it will get a tax expense of

$225 million. However, in case of the same in 2016, the organization incurred a loss of $474

million but had a tax benefit of $67 million (Marchini and D'Este 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ACCOUNTING FOR AGL ENERGY LIMITED

Requirement (viii):

The tax is generally calculated on the basis of the income generated by the organization

in a specific time period. The country in which the company is operating charges a certain

amount of corporate tax on the income generated. However, the government of the country

calculates the tax for a certain period and it might happen that it is different from the period

which the company considered for its annual reports (Kim and Zhang 2016). This might create a

difference in the taxable profit and hence the tax amount is influenced. In case the company’s tax

amount is higher than that calculated by the income tax and the company pays the same, the

extra amount is considered as tax assets and is adjusted in next year but if the case is opposite,

then the amount becomes a tax liability and company is obliged to pay the same. In case of AGL

Energy limited, the deferred tax asset in 2017 was $792 million against $953 million in 2016.

However, the deferred tax liability was measured at $13 million in 2017 against $102 million in

2016.

Requirement ix

The payable income tax along with the recent tax asset is a vital asset for the Australian

companies such as AGL Energy Limited. Focused on the yearly statement of this selected

company, it has been gathered that the recent tax assets include certain anticipated payable as

well as receivable tax on the income that is taxable or los for a definite time period. The gain or

loss on the defined benefit plans in other terms known as the actuarial gain or loss. It could be

considered as the actual evaluation of the value of the organization’s defied obligation which

might include pension plan (Nejad and Ahmad 2017). They are also measured with facilitation o

the rates of tax along with laws related with tax enacted at the end of the reporting year. In

contrast, in case of AGL Energy Limited it has been observed that the company has attained

Requirement (viii):

The tax is generally calculated on the basis of the income generated by the organization

in a specific time period. The country in which the company is operating charges a certain

amount of corporate tax on the income generated. However, the government of the country

calculates the tax for a certain period and it might happen that it is different from the period

which the company considered for its annual reports (Kim and Zhang 2016). This might create a

difference in the taxable profit and hence the tax amount is influenced. In case the company’s tax

amount is higher than that calculated by the income tax and the company pays the same, the

extra amount is considered as tax assets and is adjusted in next year but if the case is opposite,

then the amount becomes a tax liability and company is obliged to pay the same. In case of AGL

Energy limited, the deferred tax asset in 2017 was $792 million against $953 million in 2016.

However, the deferred tax liability was measured at $13 million in 2017 against $102 million in

2016.

Requirement ix

The payable income tax along with the recent tax asset is a vital asset for the Australian

companies such as AGL Energy Limited. Focused on the yearly statement of this selected

company, it has been gathered that the recent tax assets include certain anticipated payable as

well as receivable tax on the income that is taxable or los for a definite time period. The gain or

loss on the defined benefit plans in other terms known as the actuarial gain or loss. It could be

considered as the actual evaluation of the value of the organization’s defied obligation which

might include pension plan (Nejad and Ahmad 2017). They are also measured with facilitation o

the rates of tax along with laws related with tax enacted at the end of the reporting year. In

contrast, in case of AGL Energy Limited it has been observed that the company has attained

8CORPORATE ACCOUNTING FOR AGL ENERGY LIMITED

income tax advantage of around $201.9 million in the year 2016 and $103.8 million in the year

2017. Moreover, these amounts are also observed to be reflected within the reconciliation of net

loss segment to the cash flow attained from business operations within the annual report. The

major cause for which such aspects indicate the identical values is that no increased tax expenses

are experienced on the behalf of the company in both the two years.

Requirement x

After evaluating the yearly financial statements report disclosed by AGL Energy Limited

it has been gathered that for the year 2017, this company has not indicated to experience ant

expenses related with income tax for the two years from 2016 to 2017. The cash flow statement

of an organization is the statement which reflects the cash generating capacity of an organization

through three different activities. In addition, it has also earned exemptions on income tax in

both these years for this is the vital reason because of which income tax is paid and is not

encompassed within an item mentioned in the company’s statement of cash flows (Khan,

Serafeim and Yoon 2016).

Requirement xi

After carrying out detailed assessment of the tax treatment of AGL Energy Limited

Company, a surprising aspect that has been noticed is that the company has dealt with extreme

loss before experiencing the expense for income tax in the two years such as 2016 and 2017.

This is because of which the company has attained a huge income tax exemptions. For this

reason, it has turned out to be difficult to associate the real paid tax expense with the existing rate

of tax within the country that is Australia (Henderson et al. 2015). Conversely, as there is no

expenses related to income tax that has been paid by the company, there is no disclosure of

taxable income within the AGL Energy Limited Company statement of cash flows. Additionally,

income tax advantage of around $201.9 million in the year 2016 and $103.8 million in the year

2017. Moreover, these amounts are also observed to be reflected within the reconciliation of net

loss segment to the cash flow attained from business operations within the annual report. The

major cause for which such aspects indicate the identical values is that no increased tax expenses

are experienced on the behalf of the company in both the two years.

Requirement x

After evaluating the yearly financial statements report disclosed by AGL Energy Limited

it has been gathered that for the year 2017, this company has not indicated to experience ant

expenses related with income tax for the two years from 2016 to 2017. The cash flow statement

of an organization is the statement which reflects the cash generating capacity of an organization

through three different activities. In addition, it has also earned exemptions on income tax in

both these years for this is the vital reason because of which income tax is paid and is not

encompassed within an item mentioned in the company’s statement of cash flows (Khan,

Serafeim and Yoon 2016).

Requirement xi

After carrying out detailed assessment of the tax treatment of AGL Energy Limited

Company, a surprising aspect that has been noticed is that the company has dealt with extreme

loss before experiencing the expense for income tax in the two years such as 2016 and 2017.

This is because of which the company has attained a huge income tax exemptions. For this

reason, it has turned out to be difficult to associate the real paid tax expense with the existing rate

of tax within the country that is Australia (Henderson et al. 2015). Conversely, as there is no

expenses related to income tax that has been paid by the company, there is no disclosure of

taxable income within the AGL Energy Limited Company statement of cash flows. Additionally,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE ACCOUNTING FOR AGL ENERGY LIMITED

the company has also made important disclosures concerning the benefits of taxable income

attained along with it has facilitated in attaining knowledge related with tax treatment of this

Australian organization.

the company has also made important disclosures concerning the benefits of taxable income

attained along with it has facilitated in attaining knowledge related with tax treatment of this

Australian organization.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE ACCOUNTING FOR AGL ENERGY LIMITED

References

AGLEnergyLimited.com. 2018. Retrieved from https://www.

AGLEnergyLimited.com/cs/groups/internetcontent/@wc/documents/webcontent/~edisp/2017-

annual-report.pdf

Balakrishnan, K., Watts, R. and Zuo, L., 2016. The effect of accounting conservatism on

corporate investment during the global financial crisis. Journal of Business Finance &

Accounting, 43(5-6), pp.513-542.

Brown, P., Preiato, J. and Tarca, A., 2014. Measuring country differences in enforcement of

accounting standards: An audit and enforcement proxy. Journal of Business Finance &

Accounting, 41(1-2), pp.1-52.

Chen, C.J., Ding, Y. and Xu, B., 2014. Convergence of accounting standards and foreign direct

investment. The International Journal of Accounting, 49(1), pp.53-86.

Christensen, H.B., Lee, E., Walker, M. and Zeng, C., 2015. Incentives or standards: What

determines accounting quality changes around IFRS adoption?. European Accounting

Review, 24(1), pp.31-61.

De Simone, L., 2016. Does a common set of accounting standards affect tax-motivated income

shifting for multinational firms?. Journal of Accounting and Economics, 61(1), pp.145-165.

Graham, R. C., and Lin, K. C., 2018. The influence of other comprehensive income on

discretionary expenditures. Journal of Business Finance & Accounting, 45(1-2), pp. 72-91.

References

AGLEnergyLimited.com. 2018. Retrieved from https://www.

AGLEnergyLimited.com/cs/groups/internetcontent/@wc/documents/webcontent/~edisp/2017-

annual-report.pdf

Balakrishnan, K., Watts, R. and Zuo, L., 2016. The effect of accounting conservatism on

corporate investment during the global financial crisis. Journal of Business Finance &

Accounting, 43(5-6), pp.513-542.

Brown, P., Preiato, J. and Tarca, A., 2014. Measuring country differences in enforcement of

accounting standards: An audit and enforcement proxy. Journal of Business Finance &

Accounting, 41(1-2), pp.1-52.

Chen, C.J., Ding, Y. and Xu, B., 2014. Convergence of accounting standards and foreign direct

investment. The International Journal of Accounting, 49(1), pp.53-86.

Christensen, H.B., Lee, E., Walker, M. and Zeng, C., 2015. Incentives or standards: What

determines accounting quality changes around IFRS adoption?. European Accounting

Review, 24(1), pp.31-61.

De Simone, L., 2016. Does a common set of accounting standards affect tax-motivated income

shifting for multinational firms?. Journal of Accounting and Economics, 61(1), pp.145-165.

Graham, R. C., and Lin, K. C., 2018. The influence of other comprehensive income on

discretionary expenditures. Journal of Business Finance & Accounting, 45(1-2), pp. 72-91.

11CORPORATE ACCOUNTING FOR AGL ENERGY LIMITED

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial accounting.

Pearson Higher Education AU.

Khan, M., Serafeim, G. and Yoon, A., 2016. Corporate sustainability: First evidence on

materiality. The accounting review, 91(6), pp.1697-1724.

Kim, J.B. and Zhang, L., 2016. Accounting conservatism and stock price crash risk: Firm‐level

evidence. Contemporary Accounting Research, 33(1), pp.412-441.

Marchini, P. L., and D'Este, C., 2015. Comprehensive Income: which potential effects on firms’

performance evaluation and users’ decision process?. Financial reporting.

Nejad, M. Y. and Ahmad, A., 2017. Value Relevance of available-for-sale financial instruments

(AFS) and revaluation surplus of PPE (REV) components of other comprehensive income.

In SHS Web of Conferences (Vol. 34). EDP Sciences.

Reid, W., and Myddelton, D. R., 2017. Cash flow statement. In The Meaning of Company

Accounts (pp. 16-16). Routledge.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues, concepts

and practice. Routledge.

Warren, C.S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Watson, L., 2015. Corporate social responsibility research in accounting. Journal of Accounting

Literature, 34, pp.1-16.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial accounting.

Pearson Higher Education AU.

Khan, M., Serafeim, G. and Yoon, A., 2016. Corporate sustainability: First evidence on

materiality. The accounting review, 91(6), pp.1697-1724.

Kim, J.B. and Zhang, L., 2016. Accounting conservatism and stock price crash risk: Firm‐level

evidence. Contemporary Accounting Research, 33(1), pp.412-441.

Marchini, P. L., and D'Este, C., 2015. Comprehensive Income: which potential effects on firms’

performance evaluation and users’ decision process?. Financial reporting.

Nejad, M. Y. and Ahmad, A., 2017. Value Relevance of available-for-sale financial instruments

(AFS) and revaluation surplus of PPE (REV) components of other comprehensive income.

In SHS Web of Conferences (Vol. 34). EDP Sciences.

Reid, W., and Myddelton, D. R., 2017. Cash flow statement. In The Meaning of Company

Accounts (pp. 16-16). Routledge.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues, concepts

and practice. Routledge.

Warren, C.S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Watson, L., 2015. Corporate social responsibility research in accounting. Journal of Accounting

Literature, 34, pp.1-16.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.