AGL Energy Ltd: An Analysis of Accounting Theory and Reporting Issues

VerifiedAdded on 2023/04/20

|11

|2155

|305

Report

AI Summary

This report assesses AGL Energy Ltd's reporting framework, analyzing issues related to business conditions and public perception. It examines the role of the reporting framework in building public confidence and restoring the company's image, particularly in light of criticisms regarding gas pricing. The stakeholder theory is discussed in relation to the challenges faced by AGL Energy Ltd. The report concludes by recommending improvements to the company's reporting framework to enhance transparency and maintain public trust, including cost reduction strategies and clear communication of cost structures.

Running head: ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Accounting Theory and Contemporary Issues

Name of the Student:

Name of the University:

Author’s Note

Accounting Theory and Contemporary Issues

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Executive Summary

The assessment would be considering the business of AGL Energy Ltd for the purpose of

assessing the reporting framework of the business and also analyzing the issues which the

business faces in relation to business condition. The report discusses the role of reporting

framework in a business environment and how the same can be used by the business for building

confidence of the public and restoring the image of the business. The assessment also discusses

the stakeholder’s theory which is associated with the problems which the business of AGL

Energy Ltd faces in current situation. The assessment concludes with recommendations as to

how the business can further improve the reporting framework of the business and also ensure

that transparency is maintained in the preparation of annual reports of the business.

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Executive Summary

The assessment would be considering the business of AGL Energy Ltd for the purpose of

assessing the reporting framework of the business and also analyzing the issues which the

business faces in relation to business condition. The report discusses the role of reporting

framework in a business environment and how the same can be used by the business for building

confidence of the public and restoring the image of the business. The assessment also discusses

the stakeholder’s theory which is associated with the problems which the business of AGL

Energy Ltd faces in current situation. The assessment concludes with recommendations as to

how the business can further improve the reporting framework of the business and also ensure

that transparency is maintained in the preparation of annual reports of the business.

2

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Table of Contents

Introduction......................................................................................................................................3

Discussion........................................................................................................................................4

Issues/ Problems faced by the Business.......................................................................................4

Accounting Requirement.............................................................................................................5

Theories Applicable to the Business............................................................................................7

Theme of the Theory...................................................................................................................8

Conclusion and Recommendations..................................................................................................9

Reference.......................................................................................................................................10

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Table of Contents

Introduction......................................................................................................................................3

Discussion........................................................................................................................................4

Issues/ Problems faced by the Business.......................................................................................4

Accounting Requirement.............................................................................................................5

Theories Applicable to the Business............................................................................................7

Theme of the Theory...................................................................................................................8

Conclusion and Recommendations..................................................................................................9

Reference.......................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Introduction

This assessment is undertaken with an objective of analyzing the impact of conceptual

framework in the reporting process of a business. The assessment would keep the conceptual

framework of reporting as the base and identify whether the business which is chosen is facing

any accounting problems. The company which is selected for this assessment is AGL energy ltd

which is engaged in the field of energy sector. The new article which is selected states that the

business of AGL has been facing a lot of criticism for driving the prices of gas higher by

exporting the supplies to other countries.

AGL Energy ltd is one of the listed companies in the Australian stock exchange and the

business is engaged in providing both retailing of electricity for domestic use and also provides

gas to the customers. The company has further expanded the business in solar power

(Agl.com.au. 2018). The company operates in customer markets, wholesale business and also in

retailing business.

The business falls under the governance of AASB when it comes to financial reporting of

all financial information of the business and the business is expected to follow all relevant

accounting standards and also stick to the conceptual framework of reporting (Too and Weaver

2014). The discussion section would be showing the reporting framework which is followed by

the business.

The main objective of the assessment is to analyze the problems which is faced by the

business of AGL energy and how the same can be solved by the business. In addition to this, the

assessment focuses on conceptual framework which is followed by the business or the purpose of

reporting of financial information of the business,

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Introduction

This assessment is undertaken with an objective of analyzing the impact of conceptual

framework in the reporting process of a business. The assessment would keep the conceptual

framework of reporting as the base and identify whether the business which is chosen is facing

any accounting problems. The company which is selected for this assessment is AGL energy ltd

which is engaged in the field of energy sector. The new article which is selected states that the

business of AGL has been facing a lot of criticism for driving the prices of gas higher by

exporting the supplies to other countries.

AGL Energy ltd is one of the listed companies in the Australian stock exchange and the

business is engaged in providing both retailing of electricity for domestic use and also provides

gas to the customers. The company has further expanded the business in solar power

(Agl.com.au. 2018). The company operates in customer markets, wholesale business and also in

retailing business.

The business falls under the governance of AASB when it comes to financial reporting of

all financial information of the business and the business is expected to follow all relevant

accounting standards and also stick to the conceptual framework of reporting (Too and Weaver

2014). The discussion section would be showing the reporting framework which is followed by

the business.

The main objective of the assessment is to analyze the problems which is faced by the

business of AGL energy and how the same can be solved by the business. In addition to this, the

assessment focuses on conceptual framework which is followed by the business or the purpose of

reporting of financial information of the business,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Discussion

Issues/ Problems faced by the Business

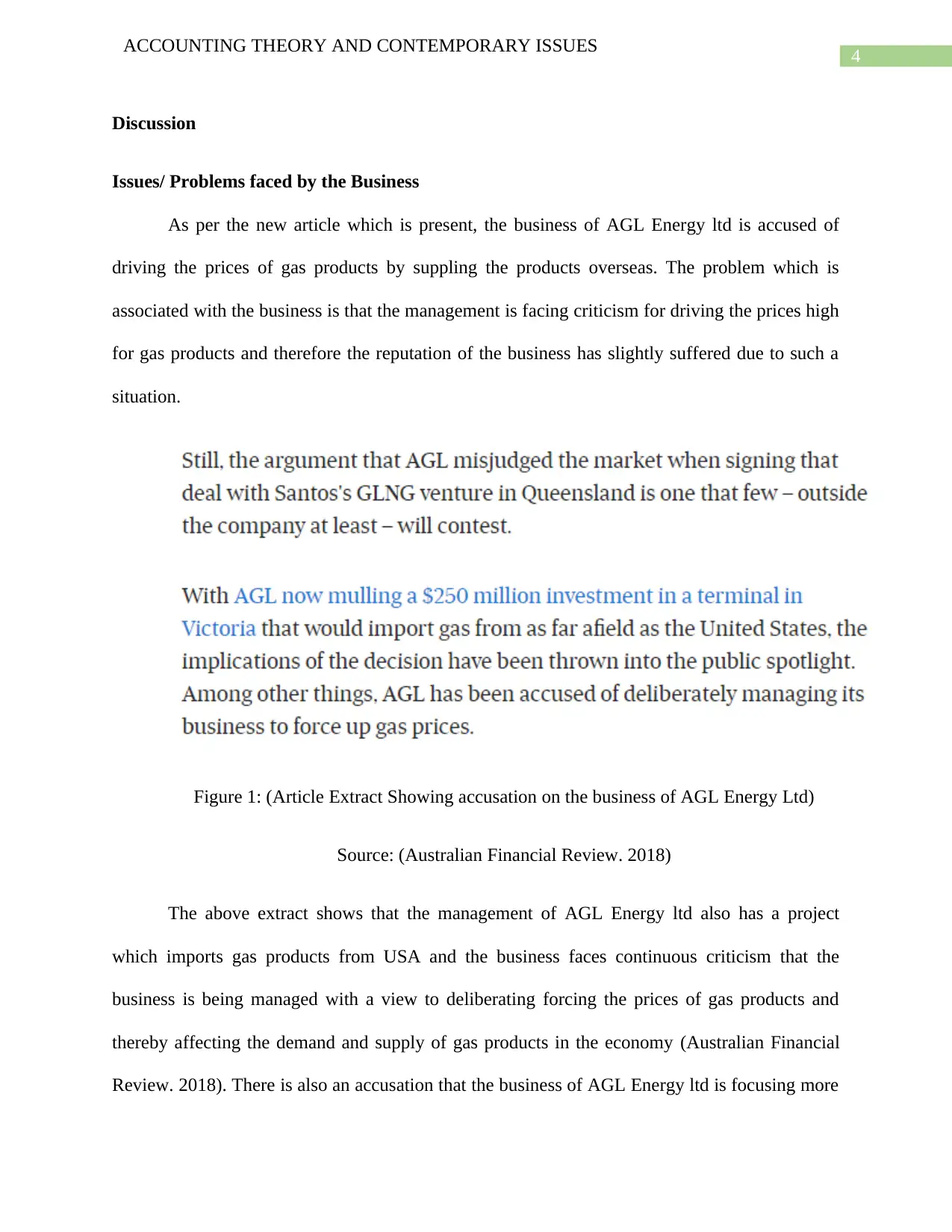

As per the new article which is present, the business of AGL Energy ltd is accused of

driving the prices of gas products by suppling the products overseas. The problem which is

associated with the business is that the management is facing criticism for driving the prices high

for gas products and therefore the reputation of the business has slightly suffered due to such a

situation.

Figure 1: (Article Extract Showing accusation on the business of AGL Energy Ltd)

Source: (Australian Financial Review. 2018)

The above extract shows that the management of AGL Energy ltd also has a project

which imports gas products from USA and the business faces continuous criticism that the

business is being managed with a view to deliberating forcing the prices of gas products and

thereby affecting the demand and supply of gas products in the economy (Australian Financial

Review. 2018). There is also an accusation that the business of AGL Energy ltd is focusing more

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Discussion

Issues/ Problems faced by the Business

As per the new article which is present, the business of AGL Energy ltd is accused of

driving the prices of gas products by suppling the products overseas. The problem which is

associated with the business is that the management is facing criticism for driving the prices high

for gas products and therefore the reputation of the business has slightly suffered due to such a

situation.

Figure 1: (Article Extract Showing accusation on the business of AGL Energy Ltd)

Source: (Australian Financial Review. 2018)

The above extract shows that the management of AGL Energy ltd also has a project

which imports gas products from USA and the business faces continuous criticism that the

business is being managed with a view to deliberating forcing the prices of gas products and

thereby affecting the demand and supply of gas products in the economy (Australian Financial

Review. 2018). There is also an accusation that the business of AGL Energy ltd is focusing more

5

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

on profits by driving the prices of gas products. The management needs to formulate strategies

which can help the business in restoring the confidence of the public and the same can be done

by appropriately demonstrating to the public that the business considers the needs of the public

and also by maintaining transparency in the reporting framework of the business (Bon and

Mustafa 2013).

Accounting Requirement

The management of AGL Energy Ltd is expected to follow conceptual framework of

accounting while preparing the financial statement of the business. In order to assess whether the

business appropriately follows the conceptual framework of reporting, the annual report of the

business is to be analyzed (Edwards 2013). Conceptual framework may be defined as the general

pattern and presentation in which financial statement are prepared following certain principles

and regulations. In order words, the conceptual framework is a guide for accounting professional

for appropriate preparation and presentation of financial information in the annual report of the

business.

The basic requirement of the conceptual framework is to ensure that the annual reports

which is prepared by the management of the company is properly presented and follows all

accounting standards applicable to such a company.

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

on profits by driving the prices of gas products. The management needs to formulate strategies

which can help the business in restoring the confidence of the public and the same can be done

by appropriately demonstrating to the public that the business considers the needs of the public

and also by maintaining transparency in the reporting framework of the business (Bon and

Mustafa 2013).

Accounting Requirement

The management of AGL Energy Ltd is expected to follow conceptual framework of

accounting while preparing the financial statement of the business. In order to assess whether the

business appropriately follows the conceptual framework of reporting, the annual report of the

business is to be analyzed (Edwards 2013). Conceptual framework may be defined as the general

pattern and presentation in which financial statement are prepared following certain principles

and regulations. In order words, the conceptual framework is a guide for accounting professional

for appropriate preparation and presentation of financial information in the annual report of the

business.

The basic requirement of the conceptual framework is to ensure that the annual reports

which is prepared by the management of the company is properly presented and follows all

accounting standards applicable to such a company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Figure 2: (Extract Showing basis of Preparation of the Financial Statement)

Source: (Agl.com.au. 2018)

The annual report of the business is prepared following all relevant accounting standards

which are applicable on the business and also the presentation of the statements which are

included in the annual report is also appropriate (Henderson et al. 2015). Another major

requirement of the conceptual framework is to ensure that the financial statement which is

prepared by the business is showing true and fair view and all relevant information are included

in the annual report (Peecher, Solomon and Trotman 2013). The company has presented all the

aspect of the financial reports such as assets, liabilities, equity, expenses and income in an

appropriate manner and the same ensure that the business has followed all accounting

requirement while preparing the financial statement of the business.

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Figure 2: (Extract Showing basis of Preparation of the Financial Statement)

Source: (Agl.com.au. 2018)

The annual report of the business is prepared following all relevant accounting standards

which are applicable on the business and also the presentation of the statements which are

included in the annual report is also appropriate (Henderson et al. 2015). Another major

requirement of the conceptual framework is to ensure that the financial statement which is

prepared by the business is showing true and fair view and all relevant information are included

in the annual report (Peecher, Solomon and Trotman 2013). The company has presented all the

aspect of the financial reports such as assets, liabilities, equity, expenses and income in an

appropriate manner and the same ensure that the business has followed all accounting

requirement while preparing the financial statement of the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

The annual reports which is prepared by the business also complies with the qualitative

characteristics which should be present in the annual report of the business. The two types of

qualitative characteristics of annual report are shown below:

Fundamental Qualitative Characteristics: The fundamental characteristics states that

the information which are included are relevant in the nature of the business and the same

are also faithfully represented. The annual report of the business for the year 2018 shows

that all relevant information is included in the annual reports and appropriate disclosures

are also provided in the notes to account section of the annual report. In case of faithful

representation of the financial information, the auditor report provides assurance that the

business has followed all regulations of Corporation Act 2001 and also all relevant

accounting standards are followed in the preparation of the financial statement of the

business.

Enhancing Qualitative Characteristics: These characteristics are supporting in nature

to the fundamental characteristics of the business. The management should prepare the

financial statement in such a manner that the same promotes that understandability,

verifiability, timeliness and comparability of the annual report of the business. The

annual reports contain appropriate disclosure for all accounting treatments which are

done by the business and therefore understandability is not a concern.

Theories Applicable to the Business

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

The annual reports which is prepared by the business also complies with the qualitative

characteristics which should be present in the annual report of the business. The two types of

qualitative characteristics of annual report are shown below:

Fundamental Qualitative Characteristics: The fundamental characteristics states that

the information which are included are relevant in the nature of the business and the same

are also faithfully represented. The annual report of the business for the year 2018 shows

that all relevant information is included in the annual reports and appropriate disclosures

are also provided in the notes to account section of the annual report. In case of faithful

representation of the financial information, the auditor report provides assurance that the

business has followed all regulations of Corporation Act 2001 and also all relevant

accounting standards are followed in the preparation of the financial statement of the

business.

Enhancing Qualitative Characteristics: These characteristics are supporting in nature

to the fundamental characteristics of the business. The management should prepare the

financial statement in such a manner that the same promotes that understandability,

verifiability, timeliness and comparability of the annual report of the business. The

annual reports contain appropriate disclosure for all accounting treatments which are

done by the business and therefore understandability is not a concern.

Theories Applicable to the Business

8

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Stakeholder’s Theory

As per this theory, the management is responsible for all activities to the stakeholders of

the business and the company should be accountable to such stakeholders for all activities of the

business. The management should also always act in the best interest of the stakeholders and the

concerns of the stakeholders should be made the primary concern for the business. The

stakeholders are the people who can affect or are affected by the activities of the business

(Hörisch, Freeman and Schaltegger 2014). The problem which is being faced by the management

of AGL Energy Ltd is that the business is facing lot of criticism from the public who also forms

a part of the stakeholders of the business relating to the hike in the prices of the gas products

which is offered in the economy. The management needs to effectively demonstrate to the public

that the activities which are undertaken by the business are for the benefits of the society and

thereby also restore the confidence of the public in the company.

Theme of the Theory

The main theme of the stakeholder theory is quite clear as the emphasis is to be provided

to the stakeholders of the business. The management of AGL Energy Ltd needs to actively

demonstrate that management is dedicated towards the needs of the society and needs to

formulate effective governance policies in order to restore the confidence of the public. The

management of AGL Energy Ltd needs to discuss the implication and long term benefits which

are associated with the policies which are formulated by the business. Another way of

demonstrating effectiveness and efficiency by maintaining a transparency in reporting

framework of the business and also ensuring that the business follows all relevant accounting

standards and principles while reporting its financial position. The theory also states that interest

of the stakeholders should be made the primary concern for the business.

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Stakeholder’s Theory

As per this theory, the management is responsible for all activities to the stakeholders of

the business and the company should be accountable to such stakeholders for all activities of the

business. The management should also always act in the best interest of the stakeholders and the

concerns of the stakeholders should be made the primary concern for the business. The

stakeholders are the people who can affect or are affected by the activities of the business

(Hörisch, Freeman and Schaltegger 2014). The problem which is being faced by the management

of AGL Energy Ltd is that the business is facing lot of criticism from the public who also forms

a part of the stakeholders of the business relating to the hike in the prices of the gas products

which is offered in the economy. The management needs to effectively demonstrate to the public

that the activities which are undertaken by the business are for the benefits of the society and

thereby also restore the confidence of the public in the company.

Theme of the Theory

The main theme of the stakeholder theory is quite clear as the emphasis is to be provided

to the stakeholders of the business. The management of AGL Energy Ltd needs to actively

demonstrate that management is dedicated towards the needs of the society and needs to

formulate effective governance policies in order to restore the confidence of the public. The

management of AGL Energy Ltd needs to discuss the implication and long term benefits which

are associated with the policies which are formulated by the business. Another way of

demonstrating effectiveness and efficiency by maintaining a transparency in reporting

framework of the business and also ensuring that the business follows all relevant accounting

standards and principles while reporting its financial position. The theory also states that interest

of the stakeholders should be made the primary concern for the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Conclusion and Recommendations

The discussion which is show above clearly indicates that the management of AGL

Energy Ltd effectively follows the conceptual framework which is approved by AASB in

reporting financial information of the business. The problem which is faced by the business is

related to the hike in the prices of gas products which has tarnished the reputation of the business

as the factor contributing to such hike in prices of gas products. In order to reverse such a

situation, the following recommendation is suggested to the management of AGL Energy Ltd:

The management needs to reduce all costs of the business with a view point of bringing

down the prices which is charged for gas products.

The management needs to effectively report all the costs which are incurred by the

business in case of gas product in order to make the people understand that no additional

charged are being charged by the business.

The management needs to demonstrate transparency in reporting and ensure that

reporting process is efficiently conducted.

The above principles would allow the management to effectively address the situation and

also restore some level of confidence of the public on the company.

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Conclusion and Recommendations

The discussion which is show above clearly indicates that the management of AGL

Energy Ltd effectively follows the conceptual framework which is approved by AASB in

reporting financial information of the business. The problem which is faced by the business is

related to the hike in the prices of gas products which has tarnished the reputation of the business

as the factor contributing to such hike in prices of gas products. In order to reverse such a

situation, the following recommendation is suggested to the management of AGL Energy Ltd:

The management needs to reduce all costs of the business with a view point of bringing

down the prices which is charged for gas products.

The management needs to effectively report all the costs which are incurred by the

business in case of gas product in order to make the people understand that no additional

charged are being charged by the business.

The management needs to demonstrate transparency in reporting and ensure that

reporting process is efficiently conducted.

The above principles would allow the management to effectively address the situation and

also restore some level of confidence of the public on the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Reference

Agl.com.au. (2018). AGL Energy | An Electricity Provider & Gas Supplier | AGL. [online]

Available at: https://www.agl.com.au/ [Accessed 22 Dec. 2018].

Australian Financial Review. (2018). How AGL Energy got caught out on gas. [online] Available

at: https://www.afr.com/business/energy/gas/how-agl-energy-got-caught-out-on-gas-20180618-

h11iox [Accessed 22 Dec. 2018].

Bon, A.T. and Mustafa, E.M., 2013. Impact of total quality management on innovation in service

organizations: Literature review and new conceptual framework. Procedia Engineering, 53,

pp.516-529.

Edwards, J.R., 2013. A History of Financial Accounting (RLE Accounting). Routledge.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial accounting.

Pearson Higher Education AU.

Hörisch, J., Freeman, R.E. and Schaltegger, S., 2014. Applying stakeholder theory in

sustainability management: Links, similarities, dissimilarities, and a conceptual

framework. Organization & Environment, 27(4), pp.328-346.

Peecher, M.E., Solomon, I. and Trotman, K.T., 2013. An accountability framework for financial

statement auditors and related research questions. Accounting, Organizations and Society, 38(8),

pp.596-620.

Too, E.G. and Weaver, P., 2014. The management of project management: A conceptual

framework for project governance. International Journal of Project Management, 32(8),

pp.1382-1394.

ACCOUNTING THEORY AND CONTEMPORARY ISSUES

Reference

Agl.com.au. (2018). AGL Energy | An Electricity Provider & Gas Supplier | AGL. [online]

Available at: https://www.agl.com.au/ [Accessed 22 Dec. 2018].

Australian Financial Review. (2018). How AGL Energy got caught out on gas. [online] Available

at: https://www.afr.com/business/energy/gas/how-agl-energy-got-caught-out-on-gas-20180618-

h11iox [Accessed 22 Dec. 2018].

Bon, A.T. and Mustafa, E.M., 2013. Impact of total quality management on innovation in service

organizations: Literature review and new conceptual framework. Procedia Engineering, 53,

pp.516-529.

Edwards, J.R., 2013. A History of Financial Accounting (RLE Accounting). Routledge.

Henderson, S., Peirson, G., Herbohn, K. and Howieson, B., 2015. Issues in financial accounting.

Pearson Higher Education AU.

Hörisch, J., Freeman, R.E. and Schaltegger, S., 2014. Applying stakeholder theory in

sustainability management: Links, similarities, dissimilarities, and a conceptual

framework. Organization & Environment, 27(4), pp.328-346.

Peecher, M.E., Solomon, I. and Trotman, K.T., 2013. An accountability framework for financial

statement auditors and related research questions. Accounting, Organizations and Society, 38(8),

pp.596-620.

Too, E.G. and Weaver, P., 2014. The management of project management: A conceptual

framework for project governance. International Journal of Project Management, 32(8),

pp.1382-1394.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.