Evaluating Share Price Behavior of AGL Energy Limited (AGL.AX)

VerifiedAdded on 2023/04/22

|8

|1047

|419

Report

AI Summary

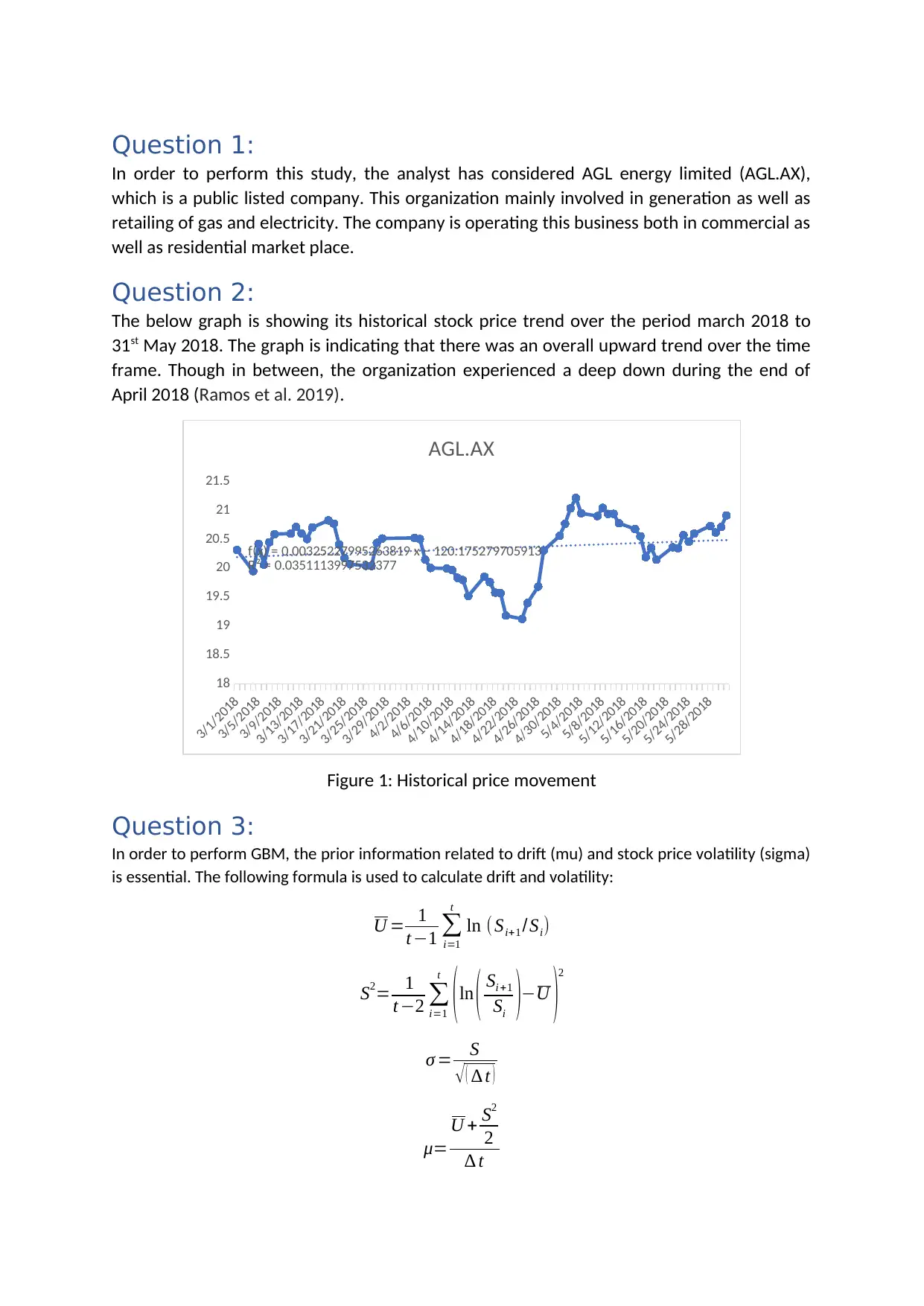

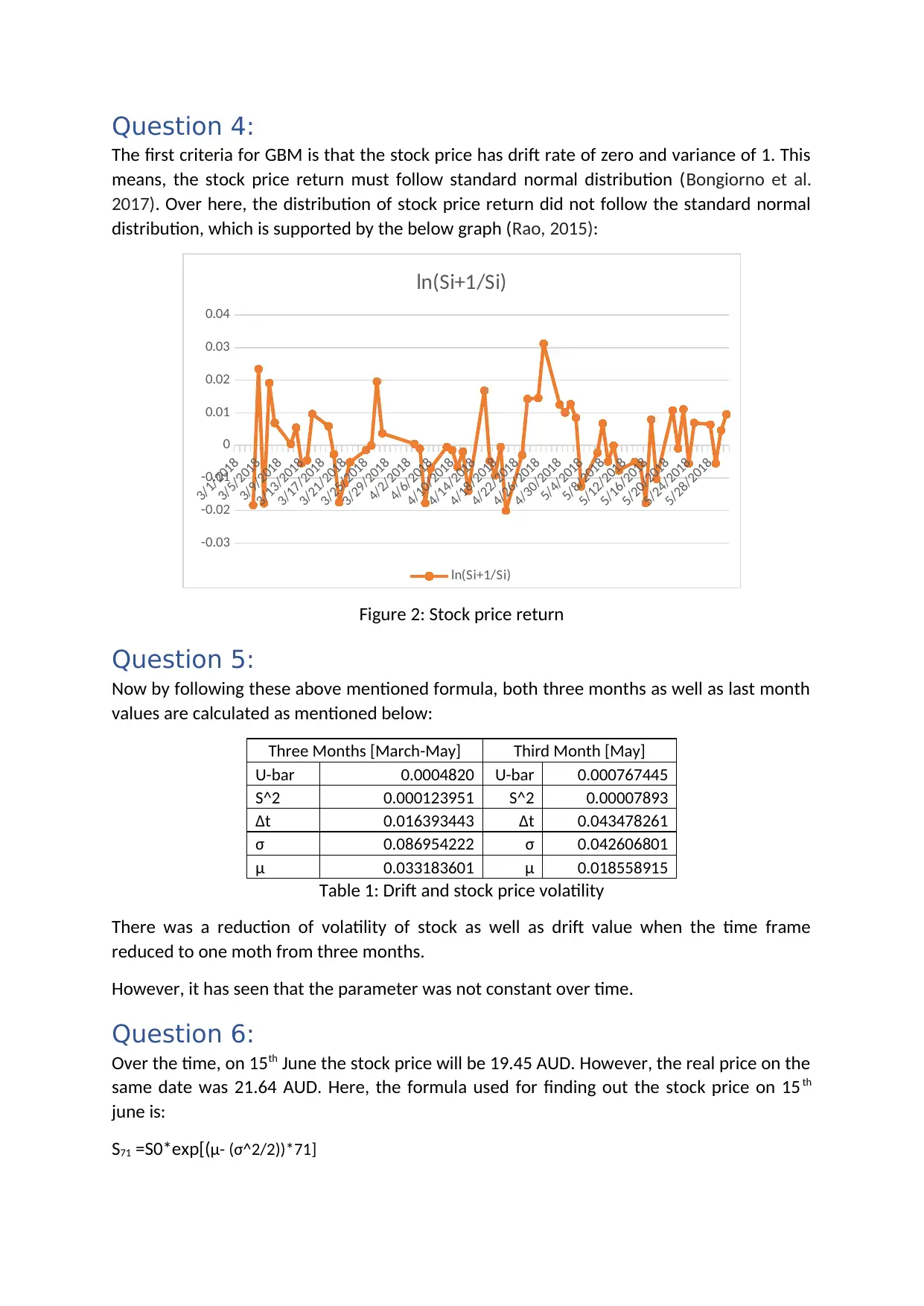

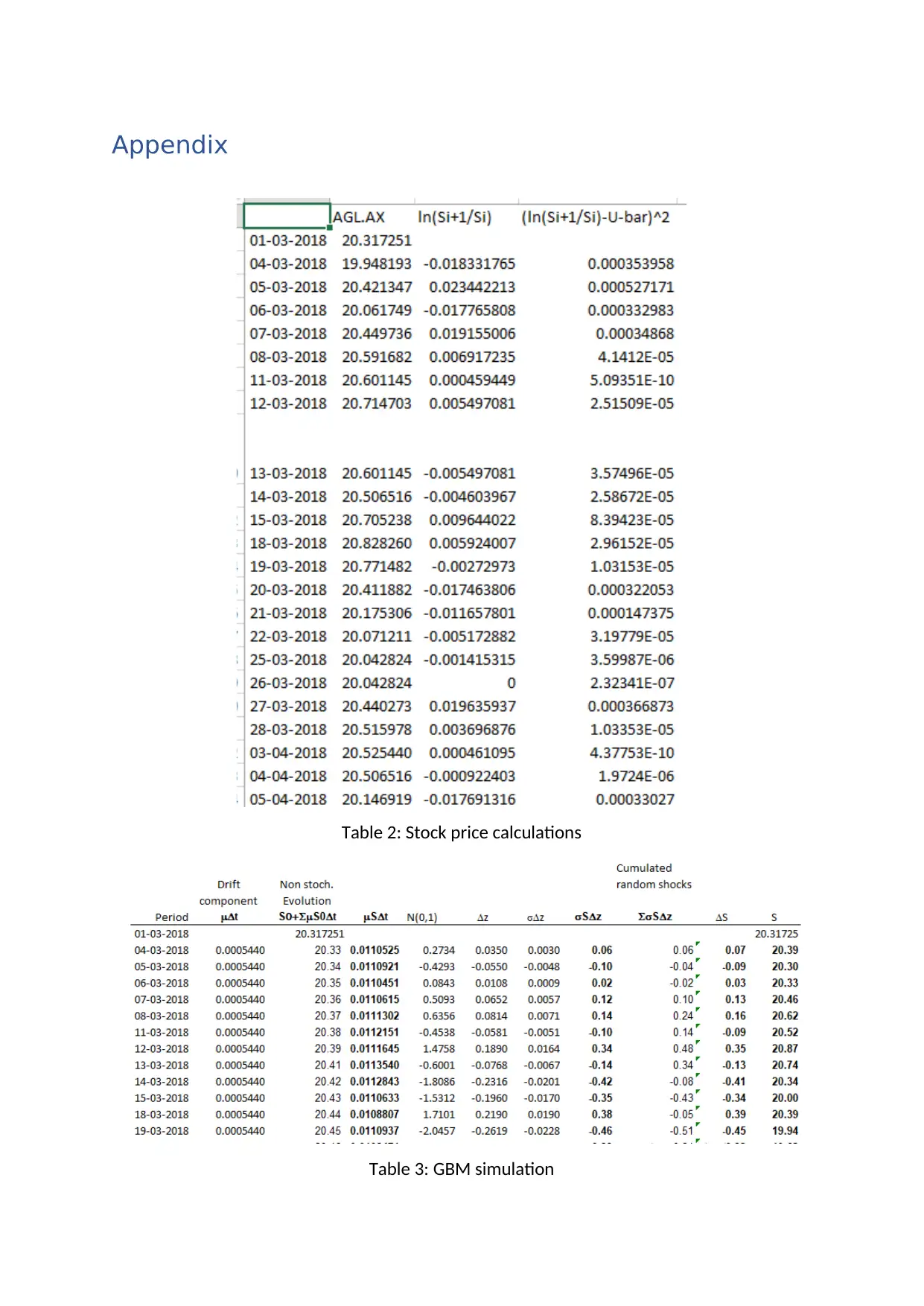

This report examines the behavior and performance of AGL Energy Limited's (AGL.AX) share price, utilizing the geometric Brownian motion (GBM) model. The analysis covers the period from March to May 2018, revealing an overall upward trend with a significant dip in late April. The study calculates drift and volatility using historical stock prices, noting that the stock price return does not strictly follow a standard normal distribution, a key criterion for GBM. Volatility and drift values are computed for both a three-month and a one-month period, showing a reduction in these parameters when the timeframe is shortened. A prediction of the stock price on June 15th is made using the GBM model and compared to the actual price, revealing a discrepancy. The report references academic works discussing the application and limitations of GBM in simulating stock price movements. Desklib offers a variety of study tools, including solved assignments and past papers, to aid students in their academic pursuits.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.