ACCT303, Semester 2: AGL Energy Sustainable Reporting Analysis Report

VerifiedAdded on 2023/06/03

|13

|3376

|234

Report

AI Summary

This report provides a comprehensive analysis of AGL Energy Limited's sustainable reporting practices, focusing on its 2017 sustainability report. It examines the integration of sustainability into AGL's overall business strategy, highlighting the company's commitment to environmental and social responsibility. The report identifies and discusses AGL's key stakeholders, including employees, customers, shareholders, and regulatory bodies, explaining their influence on the company's decision-making processes. It then assesses AGL's performance across various sustainability areas, including energy market evolution, public engagement, corporate governance, and environmental management, identifying both strengths and weaknesses. The analysis includes a commentary on areas of strong and weak sustainability performance, providing a balanced evaluation of the company's achievements and shortcomings. Finally, the report evaluates the quality of AGL's sustainability report, considering its readability, structure, use of graphical data, and adherence to GRI principles or other reporting frameworks. The analysis is based on the ACCT303 assignment brief requirements.

Running Head: Sustainable Reporting and its relevance

Sustainable Reporting Practices

AGL Energy Limited

Sustainable Reporting Practices

AGL Energy Limited

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sustainable Reporting and its relevance 1

Introduction

This report is prepared to highlight the sustainable reporting practices of AGL Energy

Limited which is one of the leading corporations operating in the energy sector of Australia.

AGL Energy is also listed on the Australian Securities Exchange. It is operating its business

as the retailer as well as merchant dealer of energy products and services. The business of

AGL Energy is of such nature that it has to make use of various natural resources to produce

the energy related products and thus it has the responsibility to make the sustainable

deployment of such valuable and useful resources. The company is being committed to its

sustainability objectives since a long time and it is voluntarily disclosing information about

its sustainability practices which are taken up in each year. AGL Energy has been publishing

its sustainability report since 2004 for its stakeholders.

Integration of sustainability strategy in overall business strategy:

AGL Energy Limited is country’s largest privately owned and operated coal fired energy

generator and is also the largest owner of energy generation assets across Australia. Further,

AGL Energy is also one among those corporations which are undertaking their business by

retailing in the Australian market for the energy related products and services. The company

is actively involved its sustainability strategy in its overall business strategy. Through the

adoption of emerging technologies, AGL Energy is aiming at becoming personalised retailers

from mass retailers by providing better business solutions. Further, AGL Energy is also

working towards becoming orchestrator of energy related assets, whether small or large in

nature, in place of being the owner of those assets. This will not only allow the company to

produce efficiently but also to store and distribution of energy among different consumers of

the company. Moreover, AGL Energy is also moving towards the implementation of those

Introduction

This report is prepared to highlight the sustainable reporting practices of AGL Energy

Limited which is one of the leading corporations operating in the energy sector of Australia.

AGL Energy is also listed on the Australian Securities Exchange. It is operating its business

as the retailer as well as merchant dealer of energy products and services. The business of

AGL Energy is of such nature that it has to make use of various natural resources to produce

the energy related products and thus it has the responsibility to make the sustainable

deployment of such valuable and useful resources. The company is being committed to its

sustainability objectives since a long time and it is voluntarily disclosing information about

its sustainability practices which are taken up in each year. AGL Energy has been publishing

its sustainability report since 2004 for its stakeholders.

Integration of sustainability strategy in overall business strategy:

AGL Energy Limited is country’s largest privately owned and operated coal fired energy

generator and is also the largest owner of energy generation assets across Australia. Further,

AGL Energy is also one among those corporations which are undertaking their business by

retailing in the Australian market for the energy related products and services. The company

is actively involved its sustainability strategy in its overall business strategy. Through the

adoption of emerging technologies, AGL Energy is aiming at becoming personalised retailers

from mass retailers by providing better business solutions. Further, AGL Energy is also

working towards becoming orchestrator of energy related assets, whether small or large in

nature, in place of being the owner of those assets. This will not only allow the company to

produce efficiently but also to store and distribution of energy among different consumers of

the company. Moreover, AGL Energy is also moving towards the implementation of those

Sustainable Reporting and its relevance 2

technologies that reduces or prevents the emission of greenhouse gases which are found to be

toxic for the health of various constituents of environment. AGL Energy is undertaking those

sustainable business practices to best serve its responsibilities towards its stakeholders. It is

also believed that the long term success and strong reputation of business could not be

achieved by mere economic performance rather it is also important for the companies to

operate in the environmental friendly manner and to effectively carry out the corporate social

responsibilities (Morhardt, 2010). The company has the aim of achieving high growth and

success of the business by serving its customers in the best ways, acting in the most ethical

manner while operating its business, engaging the stakeholders in its decision making

processes, achieving higher economic profits, promoting the health and safety of its

employees, promptly adopting the changes in the environment and by various other ways

(Manetti, 2011). With the experience of over 180 years in the energy industry of Australia,

AGL Energy has gained huge market standing and reputation which has opened up large

avenues for its growth and development. The management of the company is of the believe

that AGL Energy has the core responsibility of offering sustainable, secured as well as

affordable energy products to its customers. Furthermore, AGL Energy is also aimed at

shaping the sustainable future of the country by making it carbon-constrained world and by

promoting customer advocacy across the country. AGL Energy has the strategy of embracing

its transformation processes, driving effective productivity and unlocking the growth

opportunities at each phase of the business operated by it. As a part of its sustainable

business strategy, AGL Energy had set certain targets for the FY 2017 in terms of its

performance in economic, social, environmental terms. After the completion of 2017, it had

carried a comparative study of actual and expected results and on the basis of actual results

and future expectations, it has again determined the effective targets for 2018. To integrate its

sustainable strategy in the overall business strategy of the business, AGL Energy has

technologies that reduces or prevents the emission of greenhouse gases which are found to be

toxic for the health of various constituents of environment. AGL Energy is undertaking those

sustainable business practices to best serve its responsibilities towards its stakeholders. It is

also believed that the long term success and strong reputation of business could not be

achieved by mere economic performance rather it is also important for the companies to

operate in the environmental friendly manner and to effectively carry out the corporate social

responsibilities (Morhardt, 2010). The company has the aim of achieving high growth and

success of the business by serving its customers in the best ways, acting in the most ethical

manner while operating its business, engaging the stakeholders in its decision making

processes, achieving higher economic profits, promoting the health and safety of its

employees, promptly adopting the changes in the environment and by various other ways

(Manetti, 2011). With the experience of over 180 years in the energy industry of Australia,

AGL Energy has gained huge market standing and reputation which has opened up large

avenues for its growth and development. The management of the company is of the believe

that AGL Energy has the core responsibility of offering sustainable, secured as well as

affordable energy products to its customers. Furthermore, AGL Energy is also aimed at

shaping the sustainable future of the country by making it carbon-constrained world and by

promoting customer advocacy across the country. AGL Energy has the strategy of embracing

its transformation processes, driving effective productivity and unlocking the growth

opportunities at each phase of the business operated by it. As a part of its sustainable

business strategy, AGL Energy had set certain targets for the FY 2017 in terms of its

performance in economic, social, environmental terms. After the completion of 2017, it had

carried a comparative study of actual and expected results and on the basis of actual results

and future expectations, it has again determined the effective targets for 2018. To integrate its

sustainable strategy in the overall business strategy of the business, AGL Energy has

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sustainable Reporting and its relevance 3

formulated strategic goals and targets in various important areas such as corporate

governance practices, ethical conduct, development of sustainable market designs and

frameworks, legislative compliances, customer experiences, community and employee

engagement, environmental management and the economic performance of the business

(Lozano & Huisingh, 2011).

Key stakeholders of AGL Energy Limited:

The stakeholders of any entity are those parties whose decision making processes are

influenced with the actions and performance of such entity in the market. These are the

parties which are directly or indirectly linked to the company in various ways and hence they

require information about the company while making sound and informed decision making in

relation to the business of the company. The stakeholders of AGL Energy are bifurcated into

two main groups i.e. internal stakeholders and the external stakeholders. The internal

stakeholders of the company are those user groups which are directly involved in the internal

business activities and operations of the company. These parties are its employees,

management and its owners. On the other side, external stakeholders are those parties which

are not involved in the internal business operations of the company but still they require the

information about its overall performance to assess its financial and non-financial standing in

the market. The external stakeholders are its investors or shareholders, banks and financial

institutions, regulatory bodies, customers, business community and its suppliers (Gray &

Milne, 2002).

Employees of the company use the information about company’s performance to ascertain its

profitable state so as to as to determine the prospects of wage compensation as well their job

security in the future period. The owners of the company are called its stakeholders because

they base their investment decisions on the basis of overall business performance and

formulated strategic goals and targets in various important areas such as corporate

governance practices, ethical conduct, development of sustainable market designs and

frameworks, legislative compliances, customer experiences, community and employee

engagement, environmental management and the economic performance of the business

(Lozano & Huisingh, 2011).

Key stakeholders of AGL Energy Limited:

The stakeholders of any entity are those parties whose decision making processes are

influenced with the actions and performance of such entity in the market. These are the

parties which are directly or indirectly linked to the company in various ways and hence they

require information about the company while making sound and informed decision making in

relation to the business of the company. The stakeholders of AGL Energy are bifurcated into

two main groups i.e. internal stakeholders and the external stakeholders. The internal

stakeholders of the company are those user groups which are directly involved in the internal

business activities and operations of the company. These parties are its employees,

management and its owners. On the other side, external stakeholders are those parties which

are not involved in the internal business operations of the company but still they require the

information about its overall performance to assess its financial and non-financial standing in

the market. The external stakeholders are its investors or shareholders, banks and financial

institutions, regulatory bodies, customers, business community and its suppliers (Gray &

Milne, 2002).

Employees of the company use the information about company’s performance to ascertain its

profitable state so as to as to determine the prospects of wage compensation as well their job

security in the future period. The owners of the company are called its stakeholders because

they base their investment decisions on the basis of overall business performance and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sustainable Reporting and its relevance 4

capabilities (Kolk, 2008). The management or AGL’s board is referred to the stakeholder of

the company as they require the information about company’s performance to formulate such

policies and targets which are desirable for the growth and success of the business.

AGL Energy presently holds around 3.6 million accounts of its customers which is quite a

wide base of customers. The existing customers of the company and potential customers are

considered as its stakeholders because they are keen to know about the quality of the products

and services offered by the company. Further, the shareholders are the investors who invest

their surplus monies in the company in return of some voting rights or dividend income. The

shareholders of AGL Energy are entitled to the dividend which is the part of company’s

overall profits. Hence, these use the financial information of the company to assess the

financial health of its business before keeping their investments intact and even before

making any further investments (Lozano, 2006). Further, the governmental bodies such as tax

regulators, accounting regulators, environmental bodies which regulate the business of AGL

Energy are its prime stakeholders as they assess the overall performance of its business

towards the compliance with all necessary and relevant laws and regulations. The tax

regulators are keen to know about how AGL Energy is fulfilling its tax obligations. The

environmental regulators are keen to know about how effectively company is adhering to the

environmental protection laws and regulations (Lozano & Huisingh, 2011). Further, the

banks and other financial bodies which are providing AGL Energy a financial assistance are

its key stakeholders as they are also keen to know about the financial standing of the

company before and after sanctioning the loans. If the company is facing high financial risk,

these stakeholders will take their lending decisions accordingly. The business community

constitutes various other firms operating in the same community (often called as competitors)

are also the key stakeholders of the company as their economic decisions are highly

influenced by the AGL Energy actions and performance. The society in which AGL Energy

capabilities (Kolk, 2008). The management or AGL’s board is referred to the stakeholder of

the company as they require the information about company’s performance to formulate such

policies and targets which are desirable for the growth and success of the business.

AGL Energy presently holds around 3.6 million accounts of its customers which is quite a

wide base of customers. The existing customers of the company and potential customers are

considered as its stakeholders because they are keen to know about the quality of the products

and services offered by the company. Further, the shareholders are the investors who invest

their surplus monies in the company in return of some voting rights or dividend income. The

shareholders of AGL Energy are entitled to the dividend which is the part of company’s

overall profits. Hence, these use the financial information of the company to assess the

financial health of its business before keeping their investments intact and even before

making any further investments (Lozano, 2006). Further, the governmental bodies such as tax

regulators, accounting regulators, environmental bodies which regulate the business of AGL

Energy are its prime stakeholders as they assess the overall performance of its business

towards the compliance with all necessary and relevant laws and regulations. The tax

regulators are keen to know about how AGL Energy is fulfilling its tax obligations. The

environmental regulators are keen to know about how effectively company is adhering to the

environmental protection laws and regulations (Lozano & Huisingh, 2011). Further, the

banks and other financial bodies which are providing AGL Energy a financial assistance are

its key stakeholders as they are also keen to know about the financial standing of the

company before and after sanctioning the loans. If the company is facing high financial risk,

these stakeholders will take their lending decisions accordingly. The business community

constitutes various other firms operating in the same community (often called as competitors)

are also the key stakeholders of the company as their economic decisions are highly

influenced by the AGL Energy actions and performance. The society in which AGL Energy

Sustainable Reporting and its relevance 5

is operating its business is the major stakeholder as it is using the resources of the society for

its business operations and hence its success and growth is totally dependent on the support it

obtains from the society. A society only supports those corporations which are actively

participating in the fulfilment of their corporate social responsibilities (Hahn & Kühnen,

2013).

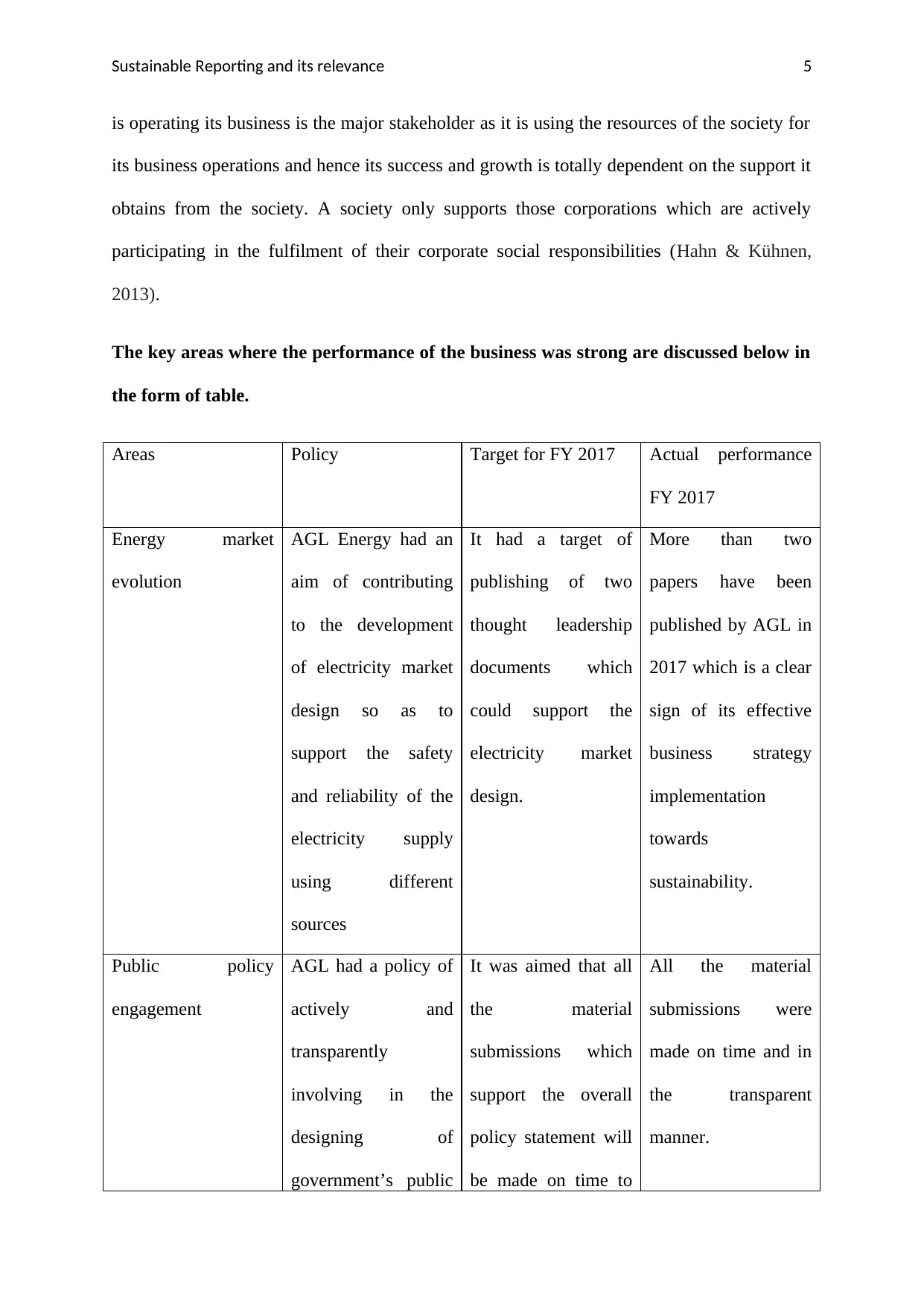

The key areas where the performance of the business was strong are discussed below in

the form of table.

Areas Policy Target for FY 2017 Actual performance

FY 2017

Energy market

evolution

AGL Energy had an

aim of contributing

to the development

of electricity market

design so as to

support the safety

and reliability of the

electricity supply

using different

sources

It had a target of

publishing of two

thought leadership

documents which

could support the

electricity market

design.

More than two

papers have been

published by AGL in

2017 which is a clear

sign of its effective

business strategy

implementation

towards

sustainability.

Public policy

engagement

AGL had a policy of

actively and

transparently

involving in the

designing of

government’s public

It was aimed that all

the material

submissions which

support the overall

policy statement will

be made on time to

All the material

submissions were

made on time and in

the transparent

manner.

is operating its business is the major stakeholder as it is using the resources of the society for

its business operations and hence its success and growth is totally dependent on the support it

obtains from the society. A society only supports those corporations which are actively

participating in the fulfilment of their corporate social responsibilities (Hahn & Kühnen,

2013).

The key areas where the performance of the business was strong are discussed below in

the form of table.

Areas Policy Target for FY 2017 Actual performance

FY 2017

Energy market

evolution

AGL Energy had an

aim of contributing

to the development

of electricity market

design so as to

support the safety

and reliability of the

electricity supply

using different

sources

It had a target of

publishing of two

thought leadership

documents which

could support the

electricity market

design.

More than two

papers have been

published by AGL in

2017 which is a clear

sign of its effective

business strategy

implementation

towards

sustainability.

Public policy

engagement

AGL had a policy of

actively and

transparently

involving in the

designing of

government’s public

It was aimed that all

the material

submissions which

support the overall

policy statement will

be made on time to

All the material

submissions were

made on time and in

the transparent

manner.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

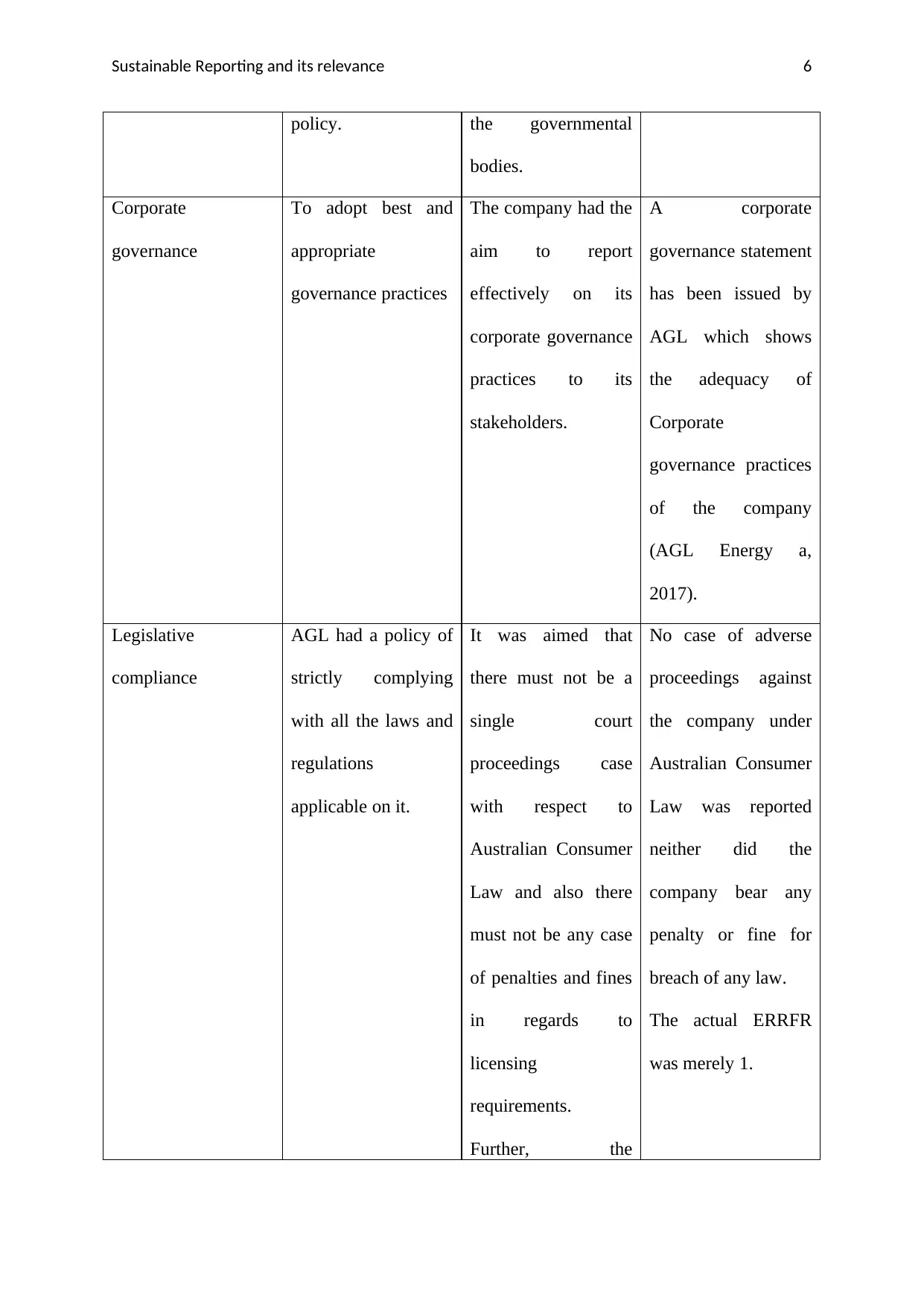

Sustainable Reporting and its relevance 6

policy. the governmental

bodies.

Corporate

governance

To adopt best and

appropriate

governance practices

The company had the

aim to report

effectively on its

corporate governance

practices to its

stakeholders.

A corporate

governance statement

has been issued by

AGL which shows

the adequacy of

Corporate

governance practices

of the company

(AGL Energy a,

2017).

Legislative

compliance

AGL had a policy of

strictly complying

with all the laws and

regulations

applicable on it.

It was aimed that

there must not be a

single court

proceedings case

with respect to

Australian Consumer

Law and also there

must not be any case

of penalties and fines

in regards to

licensing

requirements.

Further, the

No case of adverse

proceedings against

the company under

Australian Consumer

Law was reported

neither did the

company bear any

penalty or fine for

breach of any law.

The actual ERRFR

was merely 1.

policy. the governmental

bodies.

Corporate

governance

To adopt best and

appropriate

governance practices

The company had the

aim to report

effectively on its

corporate governance

practices to its

stakeholders.

A corporate

governance statement

has been issued by

AGL which shows

the adequacy of

Corporate

governance practices

of the company

(AGL Energy a,

2017).

Legislative

compliance

AGL had a policy of

strictly complying

with all the laws and

regulations

applicable on it.

It was aimed that

there must not be a

single court

proceedings case

with respect to

Australian Consumer

Law and also there

must not be any case

of penalties and fines

in regards to

licensing

requirements.

Further, the

No case of adverse

proceedings against

the company under

Australian Consumer

Law was reported

neither did the

company bear any

penalty or fine for

breach of any law.

The actual ERRFR

was merely 1.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sustainable Reporting and its relevance 7

Environmental

Regulatory

Reportable

Frequency Rate

(ERRFR) was

targeted at lower than

1.5 level

Customer satisfaction The policy was to

provide maximum

support to the

customers.

Net Promoter Score

was targeted to be

improved from that

of 2016.

The NPS in FY 2016

was -19.8 and now it

is -18.7 in 2017

Community

engagement

To actively

participate in the

mutual development

of energy projects

those are beneficial

for society.

It was targeted that

at-least 4 events must

be held in respect of

such development

projects.

At least 4 events

were organised at

each particular site.

Employee

engagement

To retain the cream

workforce.

Key talent retention:

≥ 80%

Key talent retention:

93%

Environmental

protection

To protect the

environment from

various pollution

types.

In relation to waste

management

Environmental

Regulatory

Reportable

Frequency Rate

Environmental

Regulatory

Reportable

Frequency Rate

(ERRFR): 1

(AGL Energy b,

Environmental

Regulatory

Reportable

Frequency Rate

(ERRFR) was

targeted at lower than

1.5 level

Customer satisfaction The policy was to

provide maximum

support to the

customers.

Net Promoter Score

was targeted to be

improved from that

of 2016.

The NPS in FY 2016

was -19.8 and now it

is -18.7 in 2017

Community

engagement

To actively

participate in the

mutual development

of energy projects

those are beneficial

for society.

It was targeted that

at-least 4 events must

be held in respect of

such development

projects.

At least 4 events

were organised at

each particular site.

Employee

engagement

To retain the cream

workforce.

Key talent retention:

≥ 80%

Key talent retention:

93%

Environmental

protection

To protect the

environment from

various pollution

types.

In relation to waste

management

Environmental

Regulatory

Reportable

Frequency Rate

Environmental

Regulatory

Reportable

Frequency Rate

(ERRFR): 1

(AGL Energy b,

Sustainable Reporting and its relevance 8

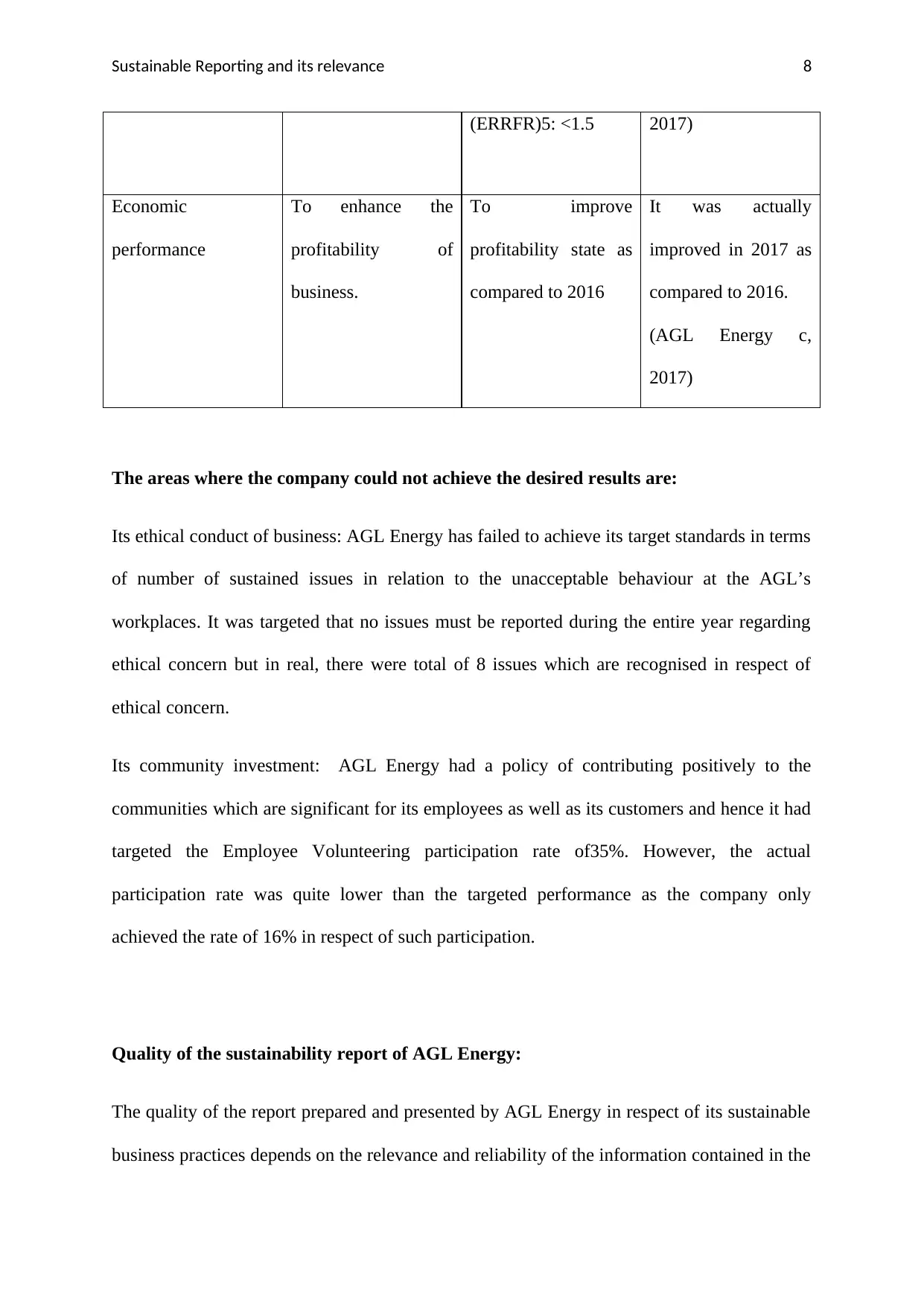

(ERRFR)5: <1.5 2017)

Economic

performance

To enhance the

profitability of

business.

To improve

profitability state as

compared to 2016

It was actually

improved in 2017 as

compared to 2016.

(AGL Energy c,

2017)

The areas where the company could not achieve the desired results are:

Its ethical conduct of business: AGL Energy has failed to achieve its target standards in terms

of number of sustained issues in relation to the unacceptable behaviour at the AGL’s

workplaces. It was targeted that no issues must be reported during the entire year regarding

ethical concern but in real, there were total of 8 issues which are recognised in respect of

ethical concern.

Its community investment: AGL Energy had a policy of contributing positively to the

communities which are significant for its employees as well as its customers and hence it had

targeted the Employee Volunteering participation rate of35%. However, the actual

participation rate was quite lower than the targeted performance as the company only

achieved the rate of 16% in respect of such participation.

Quality of the sustainability report of AGL Energy:

The quality of the report prepared and presented by AGL Energy in respect of its sustainable

business practices depends on the relevance and reliability of the information contained in the

(ERRFR)5: <1.5 2017)

Economic

performance

To enhance the

profitability of

business.

To improve

profitability state as

compared to 2016

It was actually

improved in 2017 as

compared to 2016.

(AGL Energy c,

2017)

The areas where the company could not achieve the desired results are:

Its ethical conduct of business: AGL Energy has failed to achieve its target standards in terms

of number of sustained issues in relation to the unacceptable behaviour at the AGL’s

workplaces. It was targeted that no issues must be reported during the entire year regarding

ethical concern but in real, there were total of 8 issues which are recognised in respect of

ethical concern.

Its community investment: AGL Energy had a policy of contributing positively to the

communities which are significant for its employees as well as its customers and hence it had

targeted the Employee Volunteering participation rate of35%. However, the actual

participation rate was quite lower than the targeted performance as the company only

achieved the rate of 16% in respect of such participation.

Quality of the sustainability report of AGL Energy:

The quality of the report prepared and presented by AGL Energy in respect of its sustainable

business practices depends on the relevance and reliability of the information contained in the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sustainable Reporting and its relevance 9

report (Dilling, 2010). As the information that is contained in the sustainable report of the

company is of high importance for company’s stakeholders for their assessment about

company’s overall performance, it is important to ascertain whether the company has

transparently disclosed all the relevant information which could affect the reader’s decision.

The company has followed a logical pattern while incorporating the information in the

sustainable reports and also the use of diagrams and flow charts has made it easier for the

users of the report to understand the results of overall performance of AGL Energy in all the

areas such as compliance with the code of corporate governance, ethical conduct, corporate

social responsibilities, economic and environmental performance. Moreover, the company

has made use of a scorecard to summarise its policies and aims in different areas and the

results of targeted and actual performance in such particular areas so as to enable the users of

the report to interpret the results more clearly by making a comparative analysis of the

company’s performance (Butler, Henderson & Raiborn, 2011). The company has also

engaged an external independent professional party to authenticate its sustainability report in

order to raise the credibility of the information contained in such report. The report has been

approved by Deloitte Touche Tohmastu (Deloitte) to provide a reasonable assurance to the

readers that all the information contained in the report is true and fair. After incorporating the

detailed section on how AGL is integrating its sustainable strategies in the overall business

strategies, the company has included a concise section on how it operates its business. Apart

from the qualitative information, the sustainability report of AGL Energy is also covering the

quantitative information which makes interesting for the users to understand the performance

results (Jensen & Berg, 2012). The said report also discusses about the risk management

strategies of the company in various areas such as credit risk, exchange risk, IT risk, legal

risk and environmental risk.

report (Dilling, 2010). As the information that is contained in the sustainable report of the

company is of high importance for company’s stakeholders for their assessment about

company’s overall performance, it is important to ascertain whether the company has

transparently disclosed all the relevant information which could affect the reader’s decision.

The company has followed a logical pattern while incorporating the information in the

sustainable reports and also the use of diagrams and flow charts has made it easier for the

users of the report to understand the results of overall performance of AGL Energy in all the

areas such as compliance with the code of corporate governance, ethical conduct, corporate

social responsibilities, economic and environmental performance. Moreover, the company

has made use of a scorecard to summarise its policies and aims in different areas and the

results of targeted and actual performance in such particular areas so as to enable the users of

the report to interpret the results more clearly by making a comparative analysis of the

company’s performance (Butler, Henderson & Raiborn, 2011). The company has also

engaged an external independent professional party to authenticate its sustainability report in

order to raise the credibility of the information contained in such report. The report has been

approved by Deloitte Touche Tohmastu (Deloitte) to provide a reasonable assurance to the

readers that all the information contained in the report is true and fair. After incorporating the

detailed section on how AGL is integrating its sustainable strategies in the overall business

strategies, the company has included a concise section on how it operates its business. Apart

from the qualitative information, the sustainability report of AGL Energy is also covering the

quantitative information which makes interesting for the users to understand the performance

results (Jensen & Berg, 2012). The said report also discusses about the risk management

strategies of the company in various areas such as credit risk, exchange risk, IT risk, legal

risk and environmental risk.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sustainable Reporting and its relevance 10

The use of global reporting initiatives are introduced with the aim of providing guidance to

the companies to report about their impact on the overall economy of the country and its

environment (Guthrie & Farneti, 2008). The GRI principles has also enhanced the quality of

the report as it has encouraged the company to follow the basic principles of global reporting

such as accountability, reliability, accuracy, timeliness, comparability and transparency

(Boiral, 2013). The inclusion of targeted and actual performance for FY 2017 and 2018 has

allowed the readers to compare the information and understand the significant changes in the

actual and targeted performance for 2017 so as to identify the root causes of such variations.

Also, the inclusion of the areas where the company has successfully achieved the targeted

goals and also those areas where it had failed to achieve the desired performance, in the

report is reflecting the transparency of the information about the actual business activities of

AGL Marketing.

Conclusion:

From the above report on the sustainability practices of AGL Energy which are taken up in

the financial year 2017, it can be concluded that company has effectively communicated with

all its stakeholders about its overall performance of the business. The content of the report

published by the company is highly relevant for the readers to understand its social, economic

and environmental performance. Further, the authentication of such report by an independent

professional party i.e. Deloitte has also raised the credibility of the information content of

AGL’s sustainability report.

The use of global reporting initiatives are introduced with the aim of providing guidance to

the companies to report about their impact on the overall economy of the country and its

environment (Guthrie & Farneti, 2008). The GRI principles has also enhanced the quality of

the report as it has encouraged the company to follow the basic principles of global reporting

such as accountability, reliability, accuracy, timeliness, comparability and transparency

(Boiral, 2013). The inclusion of targeted and actual performance for FY 2017 and 2018 has

allowed the readers to compare the information and understand the significant changes in the

actual and targeted performance for 2017 so as to identify the root causes of such variations.

Also, the inclusion of the areas where the company has successfully achieved the targeted

goals and also those areas where it had failed to achieve the desired performance, in the

report is reflecting the transparency of the information about the actual business activities of

AGL Marketing.

Conclusion:

From the above report on the sustainability practices of AGL Energy which are taken up in

the financial year 2017, it can be concluded that company has effectively communicated with

all its stakeholders about its overall performance of the business. The content of the report

published by the company is highly relevant for the readers to understand its social, economic

and environmental performance. Further, the authentication of such report by an independent

professional party i.e. Deloitte has also raised the credibility of the information content of

AGL’s sustainability report.

Sustainable Reporting and its relevance 11

References:

AGL Energy, 2017 a. Corporate Governance Statement: 2017. Available at:

https://www.agl.com.au/about-agl/who-we-are/our-company/corporate-governance Accessed:

07.10.2018

AGL Energy, 2017 b. Sustainability Report. Available at:

http://agl2017.reportonline.com.au/sites/agl2017.reportonline.com.au/files/

sustainability_report_full_report_0.pdf Accessed: 07.10.2018

AGL Energy, 2017c. Annual Report. Available at:

http://agl2017.reportonline.com.au/sites/agl2017.reportonline.com.au/files/

full_financial_annual_report.pdf Accessed: 07.10.2018

Boiral, O., 2013. Sustainability reports as simulacra? A counter-account of A and A+ GRI

reports. Accounting, Auditing & Accountability Journal, 26(7), pp.1036-1071.

Butler, J.B., Henderson, S.C. and Raiborn, C., 2011. Sustainability and the balanced

scorecard: integrating green measures into business reporting. Management Accounting

Quarterly, 12(2), p.1.

Dilling, P.F., 2010. Sustainability reporting in a global context: What are the characteristics

of corporations that provide high quality sustainability reports—An empirical

analysis. International Business & Economics Research Journal, 9(1), pp.19-30.

Gray, R. and Milne, M., 2002. Sustainability reporting: who's kidding whom?. Chartered

Accountants Journal of New Zealand, 81(6), pp.66-70.

Guthrie, J. and Farneti, F., 2008. GRI sustainability reporting by Australian public sector

organizations. Public Money and management, 28(6), pp.361-366.

References:

AGL Energy, 2017 a. Corporate Governance Statement: 2017. Available at:

https://www.agl.com.au/about-agl/who-we-are/our-company/corporate-governance Accessed:

07.10.2018

AGL Energy, 2017 b. Sustainability Report. Available at:

http://agl2017.reportonline.com.au/sites/agl2017.reportonline.com.au/files/

sustainability_report_full_report_0.pdf Accessed: 07.10.2018

AGL Energy, 2017c. Annual Report. Available at:

http://agl2017.reportonline.com.au/sites/agl2017.reportonline.com.au/files/

full_financial_annual_report.pdf Accessed: 07.10.2018

Boiral, O., 2013. Sustainability reports as simulacra? A counter-account of A and A+ GRI

reports. Accounting, Auditing & Accountability Journal, 26(7), pp.1036-1071.

Butler, J.B., Henderson, S.C. and Raiborn, C., 2011. Sustainability and the balanced

scorecard: integrating green measures into business reporting. Management Accounting

Quarterly, 12(2), p.1.

Dilling, P.F., 2010. Sustainability reporting in a global context: What are the characteristics

of corporations that provide high quality sustainability reports—An empirical

analysis. International Business & Economics Research Journal, 9(1), pp.19-30.

Gray, R. and Milne, M., 2002. Sustainability reporting: who's kidding whom?. Chartered

Accountants Journal of New Zealand, 81(6), pp.66-70.

Guthrie, J. and Farneti, F., 2008. GRI sustainability reporting by Australian public sector

organizations. Public Money and management, 28(6), pp.361-366.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.