Management Accounting Report: Financial Analysis of Agmet's Systems

VerifiedAdded on 2020/06/05

|18

|4465

|53

Report

AI Summary

This report delves into the realm of management accounting, focusing on the financial systems of Agmet, a UK-based metal recycling company. It dissects the essential requirements of different management accounting systems, including cost accounting, inventory management, job costing, and price optimizing systems, highlighting their significance in organizational decision-making and financial control. The report then explores various management accounting reporting methods such as budget reports, accounts receivable aging, job cost reports, and inventory and manufacturing reports, demonstrating their utility in monitoring performance and informing strategic decisions. Furthermore, the report provides calculations using marginal and absorption costing, offering a reconciled statement of profit and loss to illustrate the application of these techniques. The report also discusses planning tools, and how management accounting systems adapt to financial problems. Overall, the report provides a comprehensive overview of management accounting principles and their practical application within the context of Agmet's operations, emphasizing the importance of these systems in driving financial performance and strategic planning.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................1

SECTION 1......................................................................................................................................1

P1. Management accounting and essential requirements of different types of management

accounting systems......................................................................................................................1

M1...............................................................................................................................................2

D1................................................................................................................................................3

P2. Explaining different methods used for management accounting reporting..........................3

LO 2.................................................................................................................................................4

P3 Calculate cost using appropriate cost analysis to prepare an income statement using

marginal and absorption costing.................................................................................................4

Reconciled statement of profit and loss shows in the techniques...............................................7

M2...............................................................................................................................................8

D2................................................................................................................................................8

SECTION 2 .....................................................................................................................................9

LO 3.................................................................................................................................................9

PART A...........................................................................................................................................9

P4 Compare and contrast the planning tools used in the management accounting....................9

M3...............................................................................................................................................2

D3 ...............................................................................................................................................2

LO 4.................................................................................................................................................2

PART 2............................................................................................................................................2

P5 How management accounting adopting systems to respond to financial problems. ............2

M4...............................................................................................................................................3

CONCLUSION................................................................................................................................3

REFERENCES................................................................................................................................4

INTRODUCTION ..........................................................................................................................1

SECTION 1......................................................................................................................................1

P1. Management accounting and essential requirements of different types of management

accounting systems......................................................................................................................1

M1...............................................................................................................................................2

D1................................................................................................................................................3

P2. Explaining different methods used for management accounting reporting..........................3

LO 2.................................................................................................................................................4

P3 Calculate cost using appropriate cost analysis to prepare an income statement using

marginal and absorption costing.................................................................................................4

Reconciled statement of profit and loss shows in the techniques...............................................7

M2...............................................................................................................................................8

D2................................................................................................................................................8

SECTION 2 .....................................................................................................................................9

LO 3.................................................................................................................................................9

PART A...........................................................................................................................................9

P4 Compare and contrast the planning tools used in the management accounting....................9

M3...............................................................................................................................................2

D3 ...............................................................................................................................................2

LO 4.................................................................................................................................................2

PART 2............................................................................................................................................2

P5 How management accounting adopting systems to respond to financial problems. ............2

M4...............................................................................................................................................3

CONCLUSION................................................................................................................................3

REFERENCES................................................................................................................................4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is refers to the management oriented accounting. It is the whole

study is based on financial accounting. Management accounting helps to analyse the concept of

accounting system of organisation. Present report is based on the accounting system of Agmet

which is a leading recycler of metal bearing industrial products in UK. Furthermore, this present

report divides into two sections which describes the different aspects of management accounting.

It will focus on different essential requirement of types of management accounting systems. It

explains the methods used for management accounting reporting. It will also explain the some

calculation as well.

SECTION 1

P1. Management accounting and essential requirements of different types of management

accounting systems

In management accounting is the financial and non-financial decision making approach.

In this process organisation management make planning and organising the performance

management system (Chenhall and Moers, 2015). Management accounting system helps Agmet

to produce a management report and accounts which provide the overall structure of the financial

position of the company. Besides, this helps to make short and long term decisions. The main

role of management accounting systems which helps organisation to take best plans and decision

making approach. Main function of management accounting is to forecast the future which helps

company to make further investment plans and expansion ideas.

This may create new opportunities for company. Forecast the future means take decision

making approach which solves the business problems and minimize the future risk (Cooper,

Ezzamel and Qu, 2017). This helps to maintain a strong financial position of company which is

an important function of the organisation. Management accounting another function is to help in

buy or make decision. This helps to minimize the cost and insufficient requirements. This

process helps in operational and strategic levels. There are some types of management

accounting systems and their essential requirement in the organisation.

Cost accounting system: Cost accounting system is the first system of management

accounting. It is also known as product costing systems or costing systems. This helps to

measure the cost of the products. For profitability analysis and inventory valuation. This also

1

Management accounting is refers to the management oriented accounting. It is the whole

study is based on financial accounting. Management accounting helps to analyse the concept of

accounting system of organisation. Present report is based on the accounting system of Agmet

which is a leading recycler of metal bearing industrial products in UK. Furthermore, this present

report divides into two sections which describes the different aspects of management accounting.

It will focus on different essential requirement of types of management accounting systems. It

explains the methods used for management accounting reporting. It will also explain the some

calculation as well.

SECTION 1

P1. Management accounting and essential requirements of different types of management

accounting systems

In management accounting is the financial and non-financial decision making approach.

In this process organisation management make planning and organising the performance

management system (Chenhall and Moers, 2015). Management accounting system helps Agmet

to produce a management report and accounts which provide the overall structure of the financial

position of the company. Besides, this helps to make short and long term decisions. The main

role of management accounting systems which helps organisation to take best plans and decision

making approach. Main function of management accounting is to forecast the future which helps

company to make further investment plans and expansion ideas.

This may create new opportunities for company. Forecast the future means take decision

making approach which solves the business problems and minimize the future risk (Cooper,

Ezzamel and Qu, 2017). This helps to maintain a strong financial position of company which is

an important function of the organisation. Management accounting another function is to help in

buy or make decision. This helps to minimize the cost and insufficient requirements. This

process helps in operational and strategic levels. There are some types of management

accounting systems and their essential requirement in the organisation.

Cost accounting system: Cost accounting system is the first system of management

accounting. It is also known as product costing systems or costing systems. This helps to

measure the cost of the products. For profitability analysis and inventory valuation. This also

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

helps to maintain the cost control activities and in making effective plans. Effective and accurate

cost of products helps to estimate the profitability ratio of company (Eldenburg and et.al., 2016).

Cost accounting or product cost accounting systems help Agmet to identify which product is

productive or which ones are not. It is essential for the company to measure the future estimating

prices. Another essential requirement of product or cost accounting is to estimate the closing

value of material inventory, work in progress and finished goods inventory for preparing

financial statement of company. In cost accounting.

Inventory management systems: It is another management accounting system which

helps to maintain the inventory or stock accounting system (Fullerton, Kennedy and Widener,

2014). Manufacturing companies need to adopt these systems in order to stable the product

overstock to avoid outages. This is the most essential and important tool to make inventory data.

Company applies this system on daily basis according to the situations. Inventory management

system is the vital system in management accounting to show the actual requirement of stock or

raw materials for production. Inventory system helps to solve the challenges by finding right

solutions.

Job costing systems: On the other side, another management accounting system is Job

costing system (Job Costing, 2017). It is the best tool of accounting. This is the manufacturing

cost to an individual product or batches of products which help to identify the product identity.

This system is used generally in those manufacturing firms where products manufactured are

sufficiently different from others. It is the report of direct material and direct labour. Overall, job

costing system accumulate of the costs of material, overhead for a specific job. It is the most

approachable tool which helps to trace the specific cost to individual job examining (Messner,

2016).

Price Optimising systems: This management accounting system determines the

customer’s response against different prices of products and services.

Essentials requirement of management accounting systems

All the accounting management systems is the equally important and essential for the

organisation. These accounting systems help to analyse the actual position of the financial report

will be shown. Moreover, the main aim of the organisation is to maintain the accounting systems

to sustain the effective management performance (Messner, 2016).

2

cost of products helps to estimate the profitability ratio of company (Eldenburg and et.al., 2016).

Cost accounting or product cost accounting systems help Agmet to identify which product is

productive or which ones are not. It is essential for the company to measure the future estimating

prices. Another essential requirement of product or cost accounting is to estimate the closing

value of material inventory, work in progress and finished goods inventory for preparing

financial statement of company. In cost accounting.

Inventory management systems: It is another management accounting system which

helps to maintain the inventory or stock accounting system (Fullerton, Kennedy and Widener,

2014). Manufacturing companies need to adopt these systems in order to stable the product

overstock to avoid outages. This is the most essential and important tool to make inventory data.

Company applies this system on daily basis according to the situations. Inventory management

system is the vital system in management accounting to show the actual requirement of stock or

raw materials for production. Inventory system helps to solve the challenges by finding right

solutions.

Job costing systems: On the other side, another management accounting system is Job

costing system (Job Costing, 2017). It is the best tool of accounting. This is the manufacturing

cost to an individual product or batches of products which help to identify the product identity.

This system is used generally in those manufacturing firms where products manufactured are

sufficiently different from others. It is the report of direct material and direct labour. Overall, job

costing system accumulate of the costs of material, overhead for a specific job. It is the most

approachable tool which helps to trace the specific cost to individual job examining (Messner,

2016).

Price Optimising systems: This management accounting system determines the

customer’s response against different prices of products and services.

Essentials requirement of management accounting systems

All the accounting management systems is the equally important and essential for the

organisation. These accounting systems help to analyse the actual position of the financial report

will be shown. Moreover, the main aim of the organisation is to maintain the accounting systems

to sustain the effective management performance (Messner, 2016).

2

M1

Management accounting system is the most beneficial tool to determine the actual

position of organisation (Otley, 2016). This is the most important and necessary requirement for

the financial accounting system. For example: it helps to reduce the expenses off the company

and show the unnecessary expenses. Therefore, manager of company takes actions to control the

expenses or cost. This is an important function of management accounting systems. Another

advantages of is to improve cash flow, in which budget are the main part of the management

accounting. With the help of cost accounting system, company manages their additional cost and

improves the functioning level of the organisation. Agmet can easily control their expenditure

cost out of necessary cost. For Small scale enterprises these cost accounting systems are very

beneficial to make best decision making approach (Pimentel and Major, 2010).

D1

Management accounting system is the effective tool to enhance the performance

management which gives negative and positive aspects to the company. Moreover, the main

purpose of the organisation is to grab the best opportunities. Company mainly focus on the

financial statement of the annual report to measure the net cost and net income. Besides, it has

the limitation of personal bias personal prejudices and bias of an individual can affect the

objectives of the organisation. Apart from that, due lack of understanding and market knowledge

may give less productivity in making cost effective approaches and management accounting

system (Renz and Herman, eds., 2016).

P2. Explaining different methods used for management accounting reporting

Management accounting reports are very useful for small business owners through which

they get help to monitor company’s activities to prepare the frequent accounting report.

Management accounting reporting is based on the size and time, owner and manager may request

quarterly, monthly weekly. There are different types of managerial accounting reports.

Budget Report: Budget report is very much helpful for small businesses to make their

budget report in order to measure the performance level. This budget report helps to determine

the department performance and control costs. Manager prepares the budget based on the actual

expenses from prior years (Salehi, Rostami and Mogadam, 2010). This makes the opportunity to

control on the unnecessary expenses. Budget report is also very much helpful at the time of

3

Management accounting system is the most beneficial tool to determine the actual

position of organisation (Otley, 2016). This is the most important and necessary requirement for

the financial accounting system. For example: it helps to reduce the expenses off the company

and show the unnecessary expenses. Therefore, manager of company takes actions to control the

expenses or cost. This is an important function of management accounting systems. Another

advantages of is to improve cash flow, in which budget are the main part of the management

accounting. With the help of cost accounting system, company manages their additional cost and

improves the functioning level of the organisation. Agmet can easily control their expenditure

cost out of necessary cost. For Small scale enterprises these cost accounting systems are very

beneficial to make best decision making approach (Pimentel and Major, 2010).

D1

Management accounting system is the effective tool to enhance the performance

management which gives negative and positive aspects to the company. Moreover, the main

purpose of the organisation is to grab the best opportunities. Company mainly focus on the

financial statement of the annual report to measure the net cost and net income. Besides, it has

the limitation of personal bias personal prejudices and bias of an individual can affect the

objectives of the organisation. Apart from that, due lack of understanding and market knowledge

may give less productivity in making cost effective approaches and management accounting

system (Renz and Herman, eds., 2016).

P2. Explaining different methods used for management accounting reporting

Management accounting reports are very useful for small business owners through which

they get help to monitor company’s activities to prepare the frequent accounting report.

Management accounting reporting is based on the size and time, owner and manager may request

quarterly, monthly weekly. There are different types of managerial accounting reports.

Budget Report: Budget report is very much helpful for small businesses to make their

budget report in order to measure the performance level. This budget report helps to determine

the department performance and control costs. Manager prepares the budget based on the actual

expenses from prior years (Salehi, Rostami and Mogadam, 2010). This makes the opportunity to

control on the unnecessary expenses. Budget report is also very much helpful at the time of

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

employee’s incentives. On the basis of budget report owner enhance the incentives of the

employees. In case of funds budgeting company may give the bonus to employees in order to

meet the financial goals (Schaltegger and Burritt, 2017).

Accounts Receivable Aging: this accounts receivable aging report helps to critical the

managing cash flow for companies which extended the credit to their customers. This report

breaks the customer balances by break the credit owned limits. Moreover, the main objective of

this report is to gain the customer preference. In this reporting payments are late by 60 days, 40

days or 30 days. It is the duty of manager to checking and finds the issues with collection

process. Again it is important to make tight credit policy for the customers. So that, company

does not face any issues in future times. This may enhance the possibility of risk and uncertainty.

This report helps to determine the pending debts and unclear checks (Wijaya and et.al., 2015).

Job Cost Reports: job cost report analyse the actual cost of project. Company measure

the estimate revenue to meet the needs of objectives of job profitability. This process helps

company to find the learning Ares. So that, company focus its efforts on the major areas and

reducing the time from wasting areas. This job cost report helps to measure the unwanted

expenses and unwanted activities which arise the expenses for the company. In order to that,

company removes those ineffective activities and make new ineffective changes (Renz and

Herman, eds., 2016).

Inventory and Manufacturing: This report of inventory helps to make the company

manufacturing processes more efficient. Job cost report includes waste, hourly labour costs, per

unit overhead costs items. In this reporting manager of the company compares the different

assembly lines in the company in order to enhance the improvement and bonuses to the best

performing departments. This helps to make environment positive and energetic (Messner,

2016).

On the basis of above reporting methods, these all are for the betterment of the company.

With the help of all these reporting methods company make new financial plans in order to meet

the objectives or goals of the company. This makes the management accounting system more

powerful and expanded (Eldenburg and et.al., 2016).

4

employees. In case of funds budgeting company may give the bonus to employees in order to

meet the financial goals (Schaltegger and Burritt, 2017).

Accounts Receivable Aging: this accounts receivable aging report helps to critical the

managing cash flow for companies which extended the credit to their customers. This report

breaks the customer balances by break the credit owned limits. Moreover, the main objective of

this report is to gain the customer preference. In this reporting payments are late by 60 days, 40

days or 30 days. It is the duty of manager to checking and finds the issues with collection

process. Again it is important to make tight credit policy for the customers. So that, company

does not face any issues in future times. This may enhance the possibility of risk and uncertainty.

This report helps to determine the pending debts and unclear checks (Wijaya and et.al., 2015).

Job Cost Reports: job cost report analyse the actual cost of project. Company measure

the estimate revenue to meet the needs of objectives of job profitability. This process helps

company to find the learning Ares. So that, company focus its efforts on the major areas and

reducing the time from wasting areas. This job cost report helps to measure the unwanted

expenses and unwanted activities which arise the expenses for the company. In order to that,

company removes those ineffective activities and make new ineffective changes (Renz and

Herman, eds., 2016).

Inventory and Manufacturing: This report of inventory helps to make the company

manufacturing processes more efficient. Job cost report includes waste, hourly labour costs, per

unit overhead costs items. In this reporting manager of the company compares the different

assembly lines in the company in order to enhance the improvement and bonuses to the best

performing departments. This helps to make environment positive and energetic (Messner,

2016).

On the basis of above reporting methods, these all are for the betterment of the company.

With the help of all these reporting methods company make new financial plans in order to meet

the objectives or goals of the company. This makes the management accounting system more

powerful and expanded (Eldenburg and et.al., 2016).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

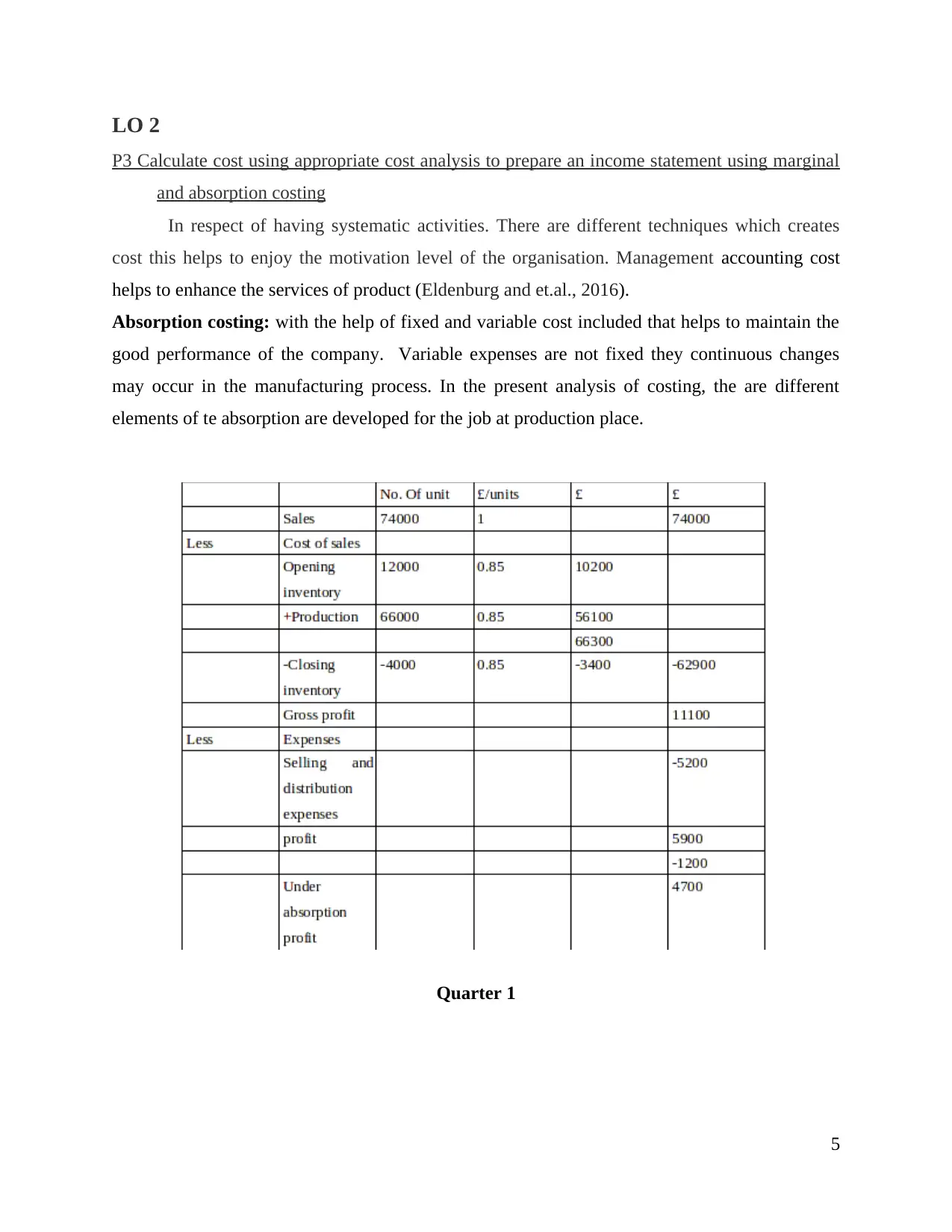

LO 2

P3 Calculate cost using appropriate cost analysis to prepare an income statement using marginal

and absorption costing

In respect of having systematic activities. There are different techniques which creates

cost this helps to enjoy the motivation level of the organisation. Management accounting cost

helps to enhance the services of product (Eldenburg and et.al., 2016).

Absorption costing: with the help of fixed and variable cost included that helps to maintain the

good performance of the company. Variable expenses are not fixed they continuous changes

may occur in the manufacturing process. In the present analysis of costing, the are different

elements of te absorption are developed for the job at production place.

Quarter 1

5

P3 Calculate cost using appropriate cost analysis to prepare an income statement using marginal

and absorption costing

In respect of having systematic activities. There are different techniques which creates

cost this helps to enjoy the motivation level of the organisation. Management accounting cost

helps to enhance the services of product (Eldenburg and et.al., 2016).

Absorption costing: with the help of fixed and variable cost included that helps to maintain the

good performance of the company. Variable expenses are not fixed they continuous changes

may occur in the manufacturing process. In the present analysis of costing, the are different

elements of te absorption are developed for the job at production place.

Quarter 1

5

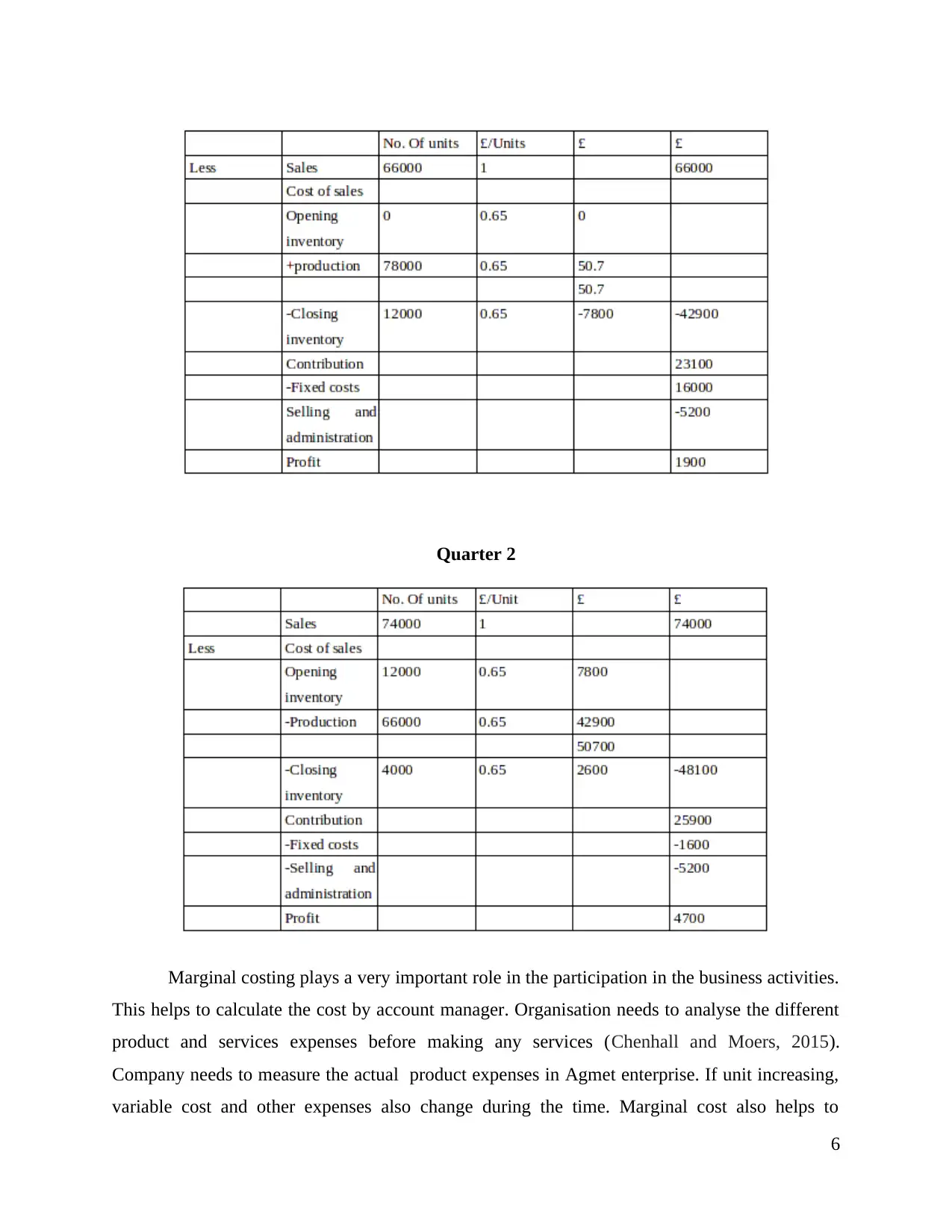

Quarter 2

Marginal costing plays a very important role in the participation in the business activities.

This helps to calculate the cost by account manager. Organisation needs to analyse the different

product and services expenses before making any services (Chenhall and Moers, 2015).

Company needs to measure the actual product expenses in Agmet enterprise. If unit increasing,

variable cost and other expenses also change during the time. Marginal cost also helps to

6

Marginal costing plays a very important role in the participation in the business activities.

This helps to calculate the cost by account manager. Organisation needs to analyse the different

product and services expenses before making any services (Chenhall and Moers, 2015).

Company needs to measure the actual product expenses in Agmet enterprise. If unit increasing,

variable cost and other expenses also change during the time. Marginal cost also helps to

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

determine the techniques that used to create break even analysis. This is the best techniques to

interpret the crucial methods that helps to cover the cost (Eldenburg and et.al., 2016).

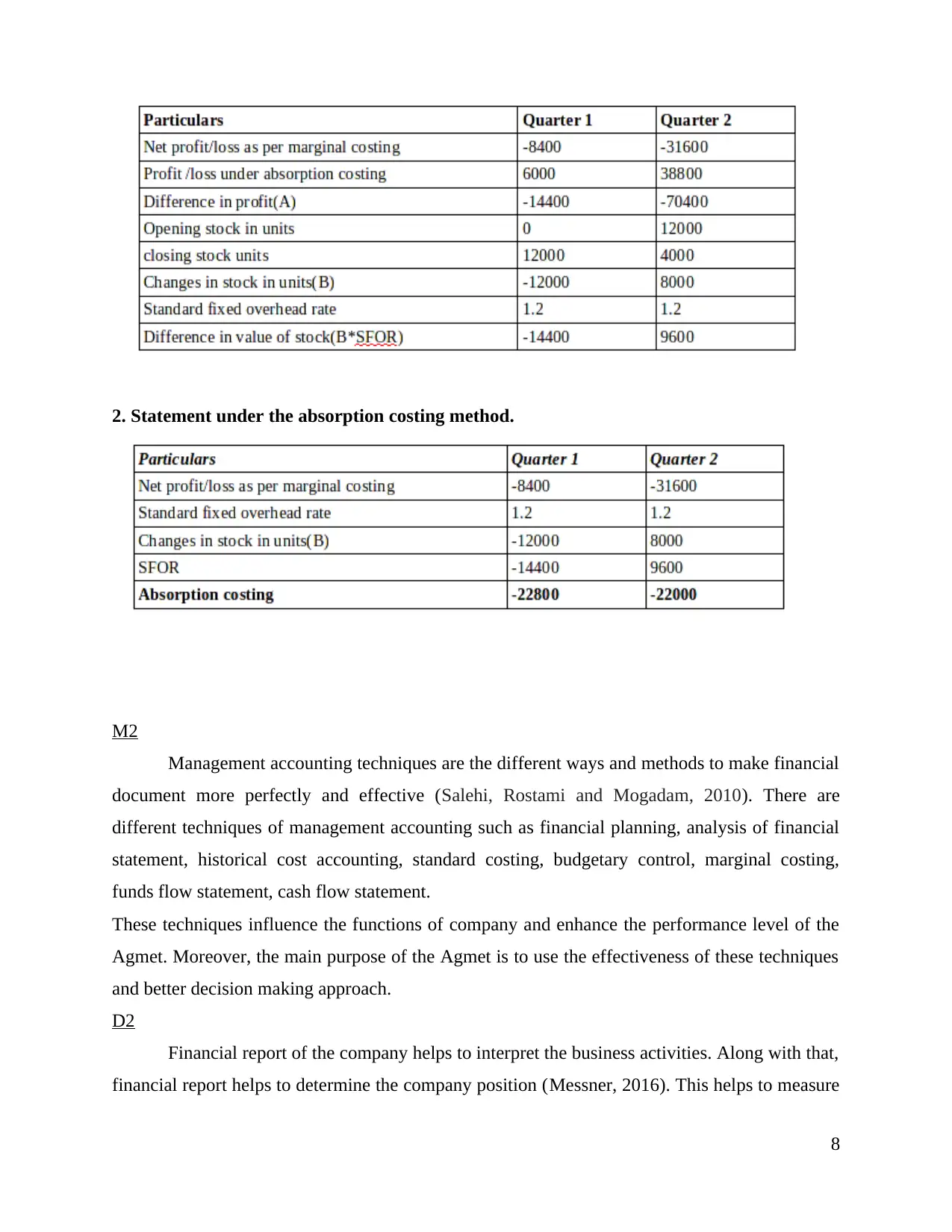

In this present analysis, profit has been calculated with the help of different methods

which includes absorption and marginal cost. These techniques and methods which helps to

enhance the profit of Quarter 1. Agmet determine the two methods or techniques which helps to

create more profit with different approaches. There are huge different between fixed and

variable cost. This is duty of the financial manager to set the benchmark for the company for

future development (Pimentel and Major, 2010).

= 66000*£0.20 = 13200

Total fixed cost = 16000

Under absorption = -2800

Reconciled statement of profit and loss shows in the techniques

Quarter 1= 4700-2800

= 1900

Fixed = 16000

66000*0.20

It is under absorption

Quarter 2

5900-1200

= 4700

74000*0.20

= 14800

Under the absorption = 1200

Types of budget

1. Statement under the marginal costing

7

interpret the crucial methods that helps to cover the cost (Eldenburg and et.al., 2016).

In this present analysis, profit has been calculated with the help of different methods

which includes absorption and marginal cost. These techniques and methods which helps to

enhance the profit of Quarter 1. Agmet determine the two methods or techniques which helps to

create more profit with different approaches. There are huge different between fixed and

variable cost. This is duty of the financial manager to set the benchmark for the company for

future development (Pimentel and Major, 2010).

= 66000*£0.20 = 13200

Total fixed cost = 16000

Under absorption = -2800

Reconciled statement of profit and loss shows in the techniques

Quarter 1= 4700-2800

= 1900

Fixed = 16000

66000*0.20

It is under absorption

Quarter 2

5900-1200

= 4700

74000*0.20

= 14800

Under the absorption = 1200

Types of budget

1. Statement under the marginal costing

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. Statement under the absorption costing method.

M2

Management accounting techniques are the different ways and methods to make financial

document more perfectly and effective (Salehi, Rostami and Mogadam, 2010). There are

different techniques of management accounting such as financial planning, analysis of financial

statement, historical cost accounting, standard costing, budgetary control, marginal costing,

funds flow statement, cash flow statement.

These techniques influence the functions of company and enhance the performance level of the

Agmet. Moreover, the main purpose of the Agmet is to use the effectiveness of these techniques

and better decision making approach.

D2

Financial report of the company helps to interpret the business activities. Along with that,

financial report helps to determine the company position (Messner, 2016). This helps to measure

8

M2

Management accounting techniques are the different ways and methods to make financial

document more perfectly and effective (Salehi, Rostami and Mogadam, 2010). There are

different techniques of management accounting such as financial planning, analysis of financial

statement, historical cost accounting, standard costing, budgetary control, marginal costing,

funds flow statement, cash flow statement.

These techniques influence the functions of company and enhance the performance level of the

Agmet. Moreover, the main purpose of the Agmet is to use the effectiveness of these techniques

and better decision making approach.

D2

Financial report of the company helps to interpret the business activities. Along with that,

financial report helps to determine the company position (Messner, 2016). This helps to measure

8

the competitors position in the market. Besides, another importance of financial report is to make

effectiveness action plan for the company. Moreover, financial report also helps to take the

further plan relating to the business activities (Cooper, Ezzamel and Qu, 2017). Financial report

is very much important for the organisation to measure the performance level of the

management.

SECTION 2

LO 3

PART A

P4 Compare and contrast the planning tools used in the management accounting.

Budgetary control is the process which used to control the company finances. It involves

the comparing of budgeting to actual financial results (Eldenburg and et.al., 2016). This much be

very effective and effective tools to measure the actual expenses of the company. This helps

Agmet to take action for short term and long term. There are some techniques of budgetary

control which helps to enhance the services or functions of the organisation.

Variance analysis: all the budget of the each department made with estimated figures.

Then after at the end it compares with actual accounting figures. With the help of this tool

company finds the variances (Pimentel and Major, 2010). Given variances sometimes favourable

and unfavourable for the company. For example Agmet record the cost and quantity of raw

material we will find the variance labour cost overhead cost. Along with that, this budgetary

technique helps to reduce the cost of the company.

Responsibility accounting: it is the another best budgetary control technique which

creates cost centre, profit centre and investment centre. All employees have responsibility to take

the company policies in serious manner (Pimentel and Major, 2010). On the other sides, it also

takes helps to motivate the employees working. It is responsibility of the sales manager to take

the responsibility. To enhance the sales target of the company. On the basis of this technique or

tools manager can also takes the decision making of employees demotion and promotion.

Zero Base Budgeting (ZBB): Zero base budgeting is the most popular and best

technique of budgeting control. In this technique budget is made on the basis of zero basis. It is

possible at the time when company expenses is equal to company income. Estimated income and

the estimated expenses will be zero (Salehi, Rostami and Mogadam, 2010). It Agmet estimated

9

effectiveness action plan for the company. Moreover, financial report also helps to take the

further plan relating to the business activities (Cooper, Ezzamel and Qu, 2017). Financial report

is very much important for the organisation to measure the performance level of the

management.

SECTION 2

LO 3

PART A

P4 Compare and contrast the planning tools used in the management accounting.

Budgetary control is the process which used to control the company finances. It involves

the comparing of budgeting to actual financial results (Eldenburg and et.al., 2016). This much be

very effective and effective tools to measure the actual expenses of the company. This helps

Agmet to take action for short term and long term. There are some techniques of budgetary

control which helps to enhance the services or functions of the organisation.

Variance analysis: all the budget of the each department made with estimated figures.

Then after at the end it compares with actual accounting figures. With the help of this tool

company finds the variances (Pimentel and Major, 2010). Given variances sometimes favourable

and unfavourable for the company. For example Agmet record the cost and quantity of raw

material we will find the variance labour cost overhead cost. Along with that, this budgetary

technique helps to reduce the cost of the company.

Responsibility accounting: it is the another best budgetary control technique which

creates cost centre, profit centre and investment centre. All employees have responsibility to take

the company policies in serious manner (Pimentel and Major, 2010). On the other sides, it also

takes helps to motivate the employees working. It is responsibility of the sales manager to take

the responsibility. To enhance the sales target of the company. On the basis of this technique or

tools manager can also takes the decision making of employees demotion and promotion.

Zero Base Budgeting (ZBB): Zero base budgeting is the most popular and best

technique of budgeting control. In this technique budget is made on the basis of zero basis. It is

possible at the time when company expenses is equal to company income. Estimated income and

the estimated expenses will be zero (Salehi, Rostami and Mogadam, 2010). It Agmet estimated

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.