Accounting for Share-Based Payments: Agrico plc Case Study Analysis

VerifiedAdded on 2022/08/24

|13

|2322

|23

Homework Assignment

AI Summary

This assignment analyzes the financial reporting of Agrico plc, focusing on share-based payments in accordance with IFRS 2. The solution addresses the accounting treatment of share options, including fair value determination, journal entries, and the impact on financial statements. It includes adjustments to the statement of profit or loss and statement of financial position, along with the calculation of ROCE and interest coverage ratio. Additionally, the assignment delves into the principles of IFRS 2, covering vesting conditions, cancellations, and criticisms of the standard, with discussions on graded vesting and shareholder granting. The assignment provides a comprehensive understanding of share-based payment accounting and its implications for financial reporting.

Running head: ACCOUNTING

Accounting

Name of the Student:

Name of the University:

Author’s Note

Accounting

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

ACCOUNTING

Table of Contents

Answer to Part a.............................................................................................................2

Answer to Part b.............................................................................................................3

Answer to Part d.............................................................................................................6

Share-Based Payments...................................................................................................6

Vesting conditions and cancellation...............................................................................7

IFRS 2............................................................................................................................8

Graded vesting...........................................................................................................8

Shareholder granting..................................................................................................9

Conclusion....................................................................................................................11

Bibliography.................................................................................................................12

Answer to Part a

ACCOUNTING

Table of Contents

Answer to Part a.............................................................................................................2

Answer to Part b.............................................................................................................3

Answer to Part d.............................................................................................................6

Share-Based Payments...................................................................................................6

Vesting conditions and cancellation...............................................................................7

IFRS 2............................................................................................................................8

Graded vesting...........................................................................................................8

Shareholder granting..................................................................................................9

Conclusion....................................................................................................................11

Bibliography.................................................................................................................12

Answer to Part a

2

ACCOUNTING

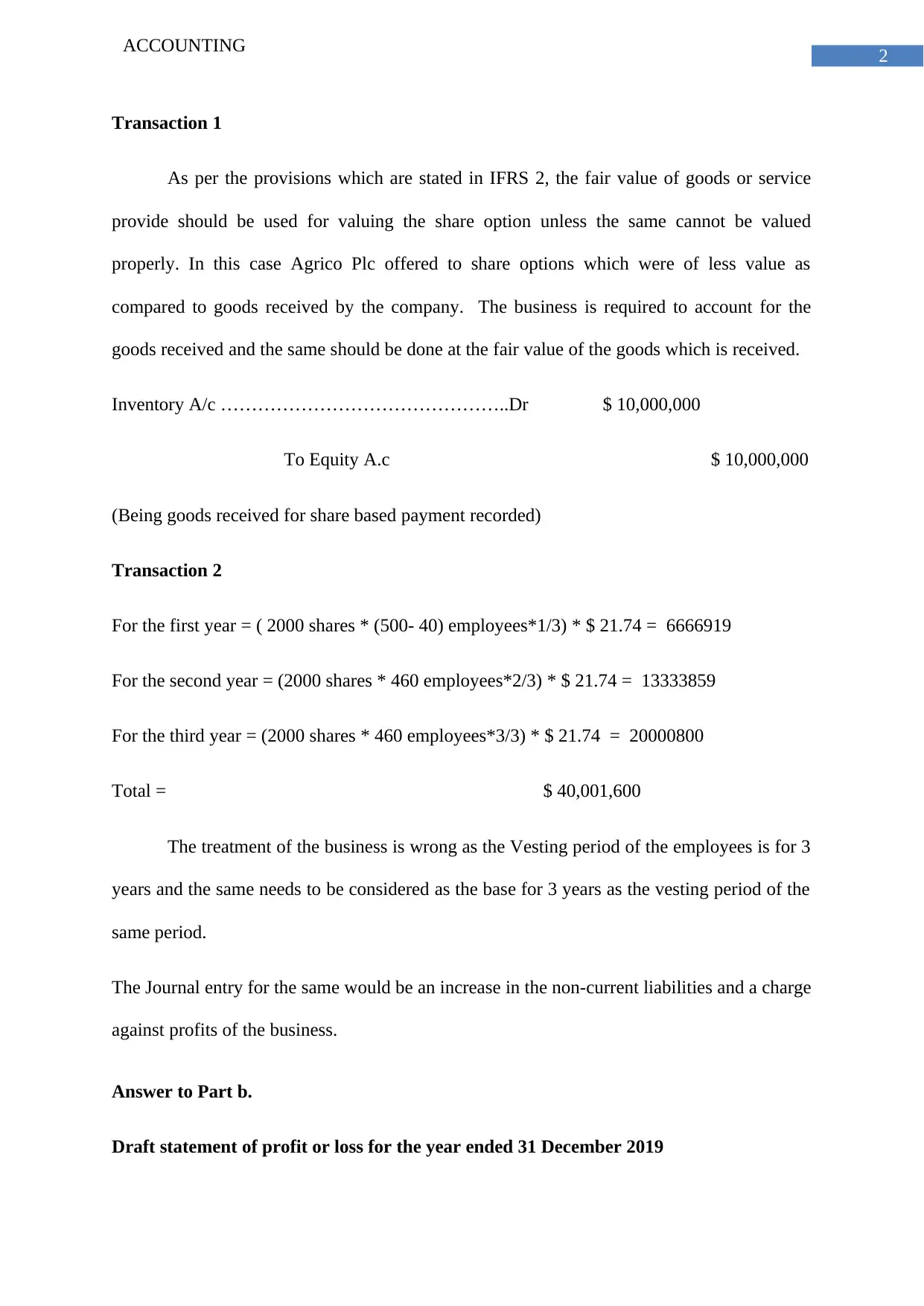

Transaction 1

As per the provisions which are stated in IFRS 2, the fair value of goods or service

provide should be used for valuing the share option unless the same cannot be valued

properly. In this case Agrico Plc offered to share options which were of less value as

compared to goods received by the company. The business is required to account for the

goods received and the same should be done at the fair value of the goods which is received.

Inventory A/c ………………………………………..Dr $ 10,000,000

To Equity A.c $ 10,000,000

(Being goods received for share based payment recorded)

Transaction 2

For the first year = ( 2000 shares * (500- 40) employees*1/3) * $ 21.74 = 6666919

For the second year = (2000 shares * 460 employees*2/3) * $ 21.74 = 13333859

For the third year = (2000 shares * 460 employees*3/3) * $ 21.74 = 20000800

Total = $ 40,001,600

The treatment of the business is wrong as the Vesting period of the employees is for 3

years and the same needs to be considered as the base for 3 years as the vesting period of the

same period.

The Journal entry for the same would be an increase in the non-current liabilities and a charge

against profits of the business.

Answer to Part b.

Draft statement of profit or loss for the year ended 31 December 2019

ACCOUNTING

Transaction 1

As per the provisions which are stated in IFRS 2, the fair value of goods or service

provide should be used for valuing the share option unless the same cannot be valued

properly. In this case Agrico Plc offered to share options which were of less value as

compared to goods received by the company. The business is required to account for the

goods received and the same should be done at the fair value of the goods which is received.

Inventory A/c ………………………………………..Dr $ 10,000,000

To Equity A.c $ 10,000,000

(Being goods received for share based payment recorded)

Transaction 2

For the first year = ( 2000 shares * (500- 40) employees*1/3) * $ 21.74 = 6666919

For the second year = (2000 shares * 460 employees*2/3) * $ 21.74 = 13333859

For the third year = (2000 shares * 460 employees*3/3) * $ 21.74 = 20000800

Total = $ 40,001,600

The treatment of the business is wrong as the Vesting period of the employees is for 3

years and the same needs to be considered as the base for 3 years as the vesting period of the

same period.

The Journal entry for the same would be an increase in the non-current liabilities and a charge

against profits of the business.

Answer to Part b.

Draft statement of profit or loss for the year ended 31 December 2019

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

ACCOUNTING

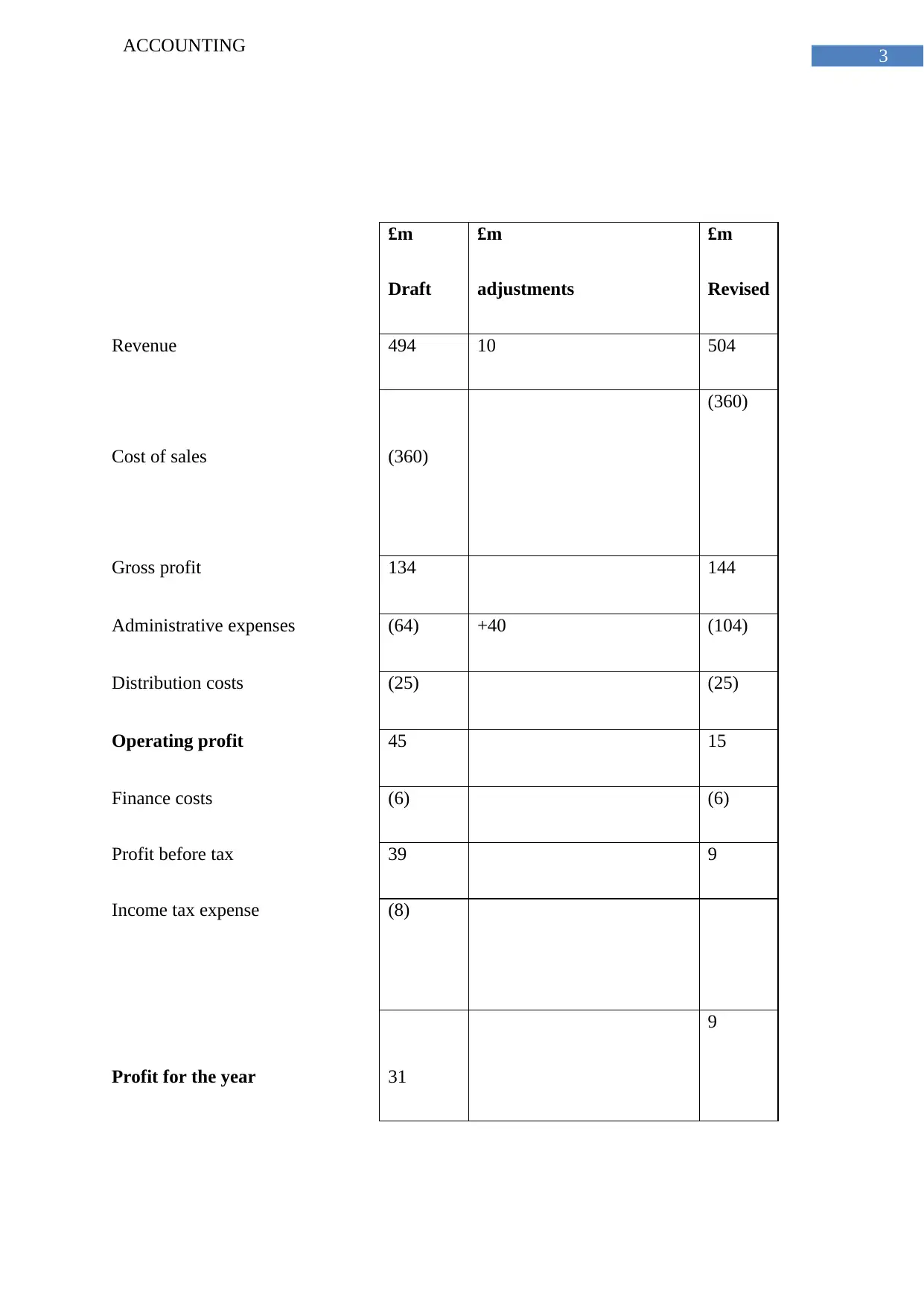

£m

Draft

£m

adjustments

£m

Revised

Revenue 494 10 504

Cost of sales (360)

(360)

Gross profit 134 144

Administrative expenses (64) +40 (104)

Distribution costs (25) (25)

Operating profit 45 15

Finance costs (6) (6)

Profit before tax 39 9

Income tax expense (8)

Profit for the year 31

9

ACCOUNTING

£m

Draft

£m

adjustments

£m

Revised

Revenue 494 10 504

Cost of sales (360)

(360)

Gross profit 134 144

Administrative expenses (64) +40 (104)

Distribution costs (25) (25)

Operating profit 45 15

Finance costs (6) (6)

Profit before tax 39 9

Income tax expense (8)

Profit for the year 31

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

ACCOUNTING

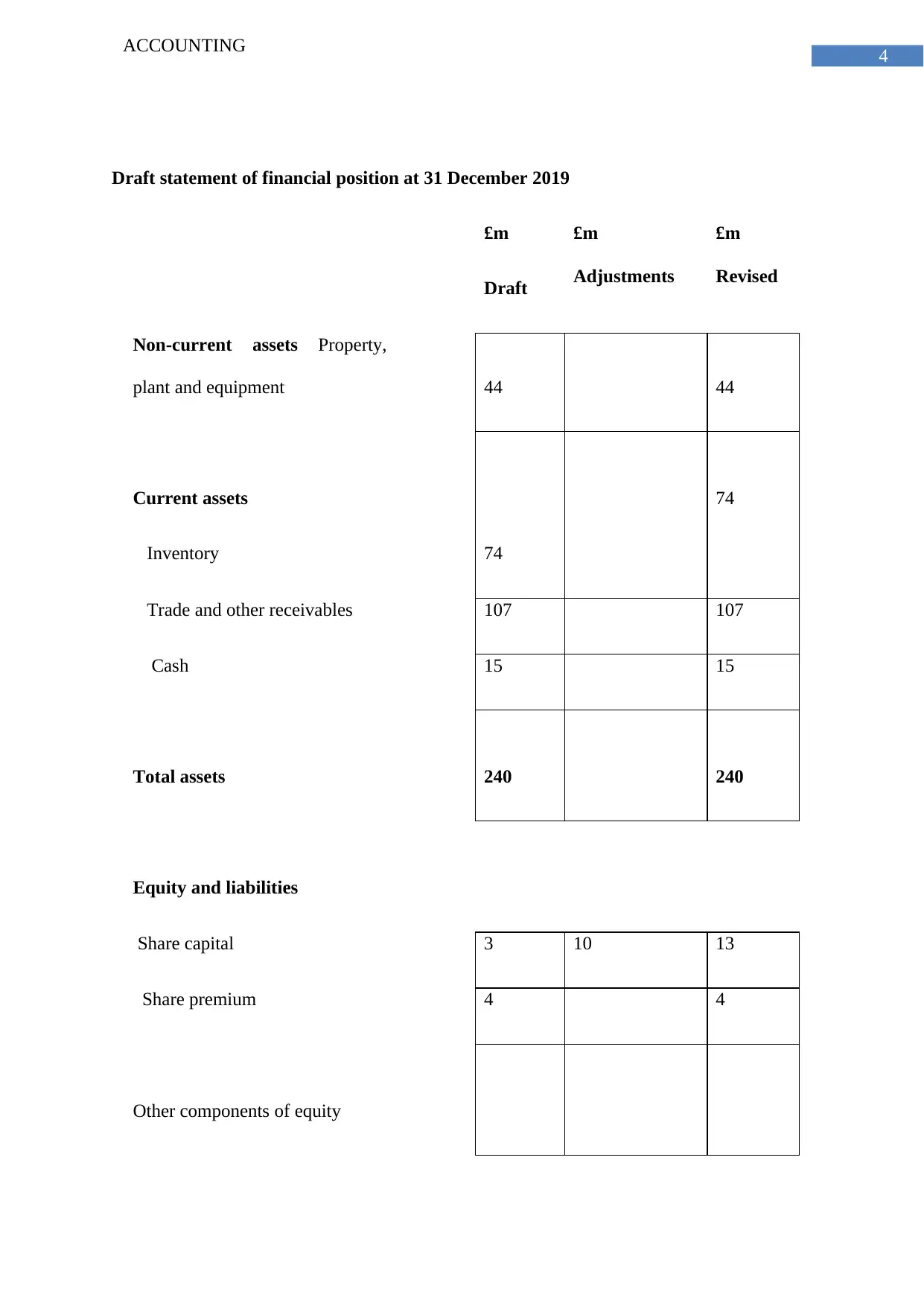

Draft statement of financial position at 31 December 2019

£m

Draft

£m

Adjustments

£m

Revised

Non-current assets Property,

plant and equipment 44 44

Current assets

Inventory 74

74

Trade and other receivables 107 107

Cash 15 15

Total assets 240 240

Equity and liabilities

Share capital 3 10 13

Share premium 4 4

Other components of equity

ACCOUNTING

Draft statement of financial position at 31 December 2019

£m

Draft

£m

Adjustments

£m

Revised

Non-current assets Property,

plant and equipment 44 44

Current assets

Inventory 74

74

Trade and other receivables 107 107

Cash 15 15

Total assets 240 240

Equity and liabilities

Share capital 3 10 13

Share premium 4 4

Other components of equity

5

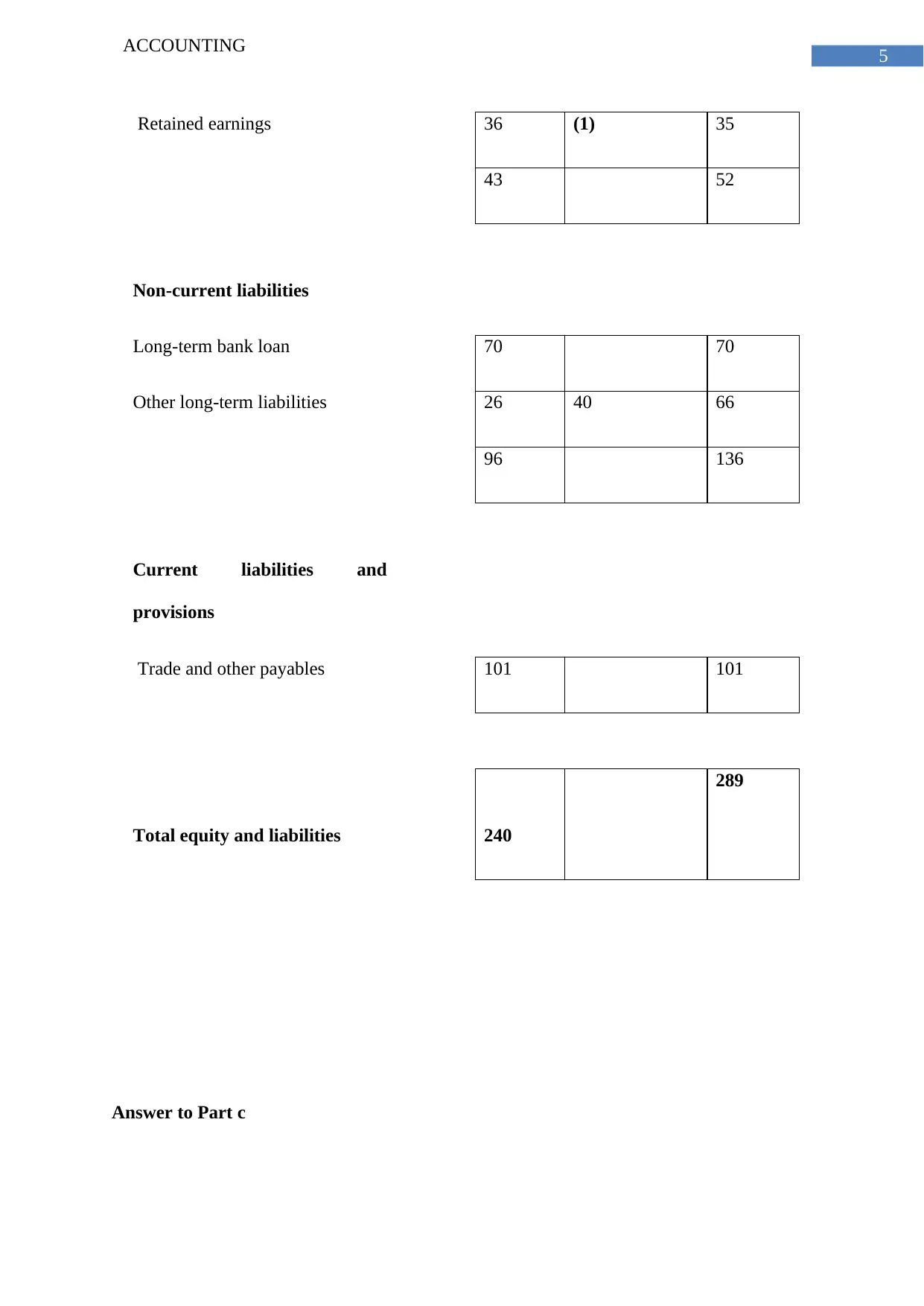

ACCOUNTING

Retained earnings 36 (1) 35

43 52

Non-current liabilities

Long-term bank loan 70 70

Other long-term liabilities 26 40 66

96 136

Current liabilities and

provisions

Trade and other payables 101 101

Total equity and liabilities 240

289

Answer to Part c

ACCOUNTING

Retained earnings 36 (1) 35

43 52

Non-current liabilities

Long-term bank loan 70 70

Other long-term liabilities 26 40 66

96 136

Current liabilities and

provisions

Trade and other payables 101 101

Total equity and liabilities 240

289

Answer to Part c

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

ACCOUNTING

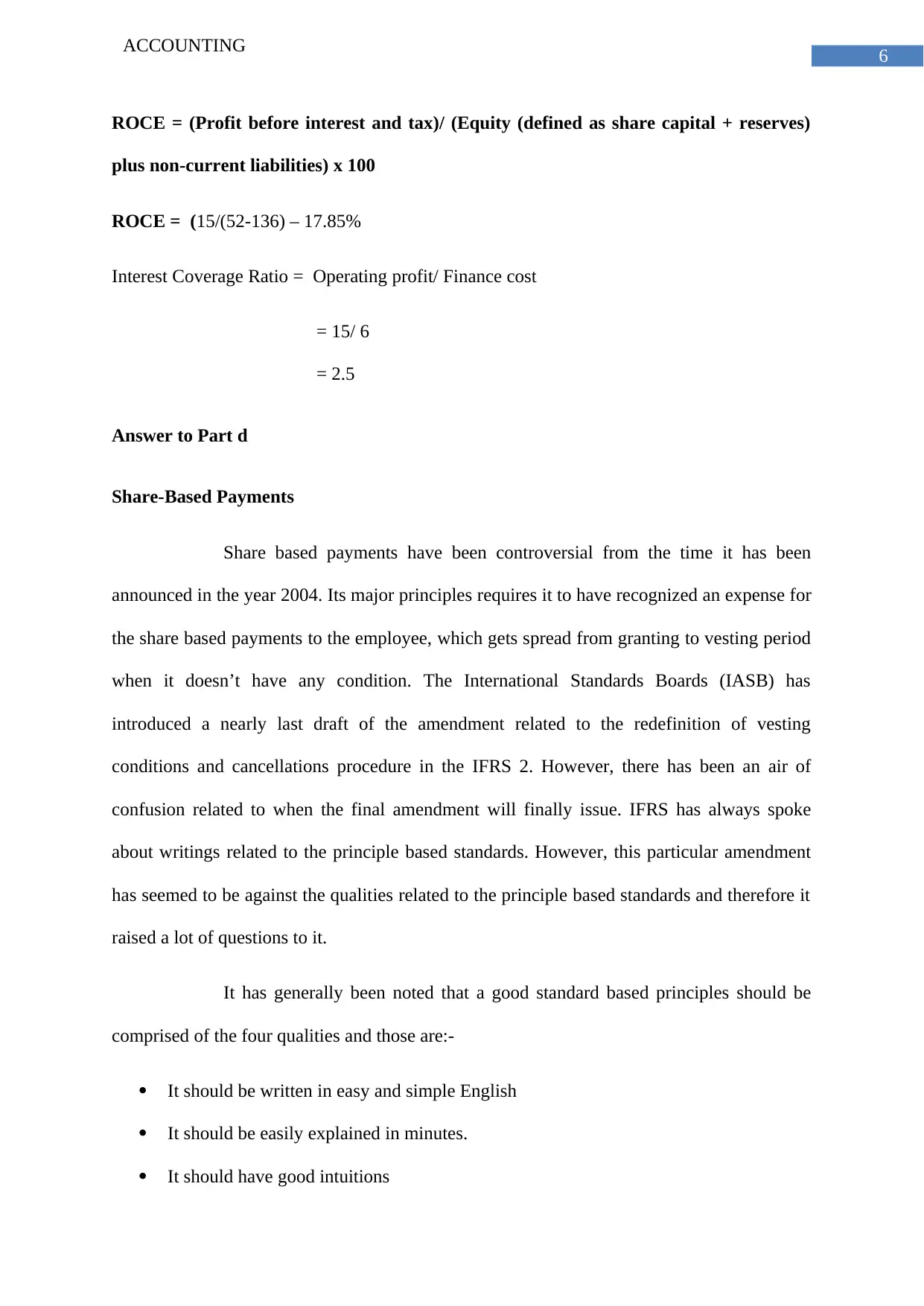

ROCE = (Profit before interest and tax)/ (Equity (defined as share capital + reserves)

plus non-current liabilities) x 100

ROCE = (15/(52-136) – 17.85%

Interest Coverage Ratio = Operating profit/ Finance cost

= 15/ 6

= 2.5

Answer to Part d

Share-Based Payments

Share based payments have been controversial from the time it has been

announced in the year 2004. Its major principles requires it to have recognized an expense for

the share based payments to the employee, which gets spread from granting to vesting period

when it doesn’t have any condition. The International Standards Boards (IASB) has

introduced a nearly last draft of the amendment related to the redefinition of vesting

conditions and cancellations procedure in the IFRS 2. However, there has been an air of

confusion related to when the final amendment will finally issue. IFRS has always spoke

about writings related to the principle based standards. However, this particular amendment

has seemed to be against the qualities related to the principle based standards and therefore it

raised a lot of questions to it.

It has generally been noted that a good standard based principles should be

comprised of the four qualities and those are:-

It should be written in easy and simple English

It should be easily explained in minutes.

It should have good intuitions

ACCOUNTING

ROCE = (Profit before interest and tax)/ (Equity (defined as share capital + reserves)

plus non-current liabilities) x 100

ROCE = (15/(52-136) – 17.85%

Interest Coverage Ratio = Operating profit/ Finance cost

= 15/ 6

= 2.5

Answer to Part d

Share-Based Payments

Share based payments have been controversial from the time it has been

announced in the year 2004. Its major principles requires it to have recognized an expense for

the share based payments to the employee, which gets spread from granting to vesting period

when it doesn’t have any condition. The International Standards Boards (IASB) has

introduced a nearly last draft of the amendment related to the redefinition of vesting

conditions and cancellations procedure in the IFRS 2. However, there has been an air of

confusion related to when the final amendment will finally issue. IFRS has always spoke

about writings related to the principle based standards. However, this particular amendment

has seemed to be against the qualities related to the principle based standards and therefore it

raised a lot of questions to it.

It has generally been noted that a good standard based principles should be

comprised of the four qualities and those are:-

It should be written in easy and simple English

It should be easily explained in minutes.

It should have good intuitions

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

ACCOUNTING

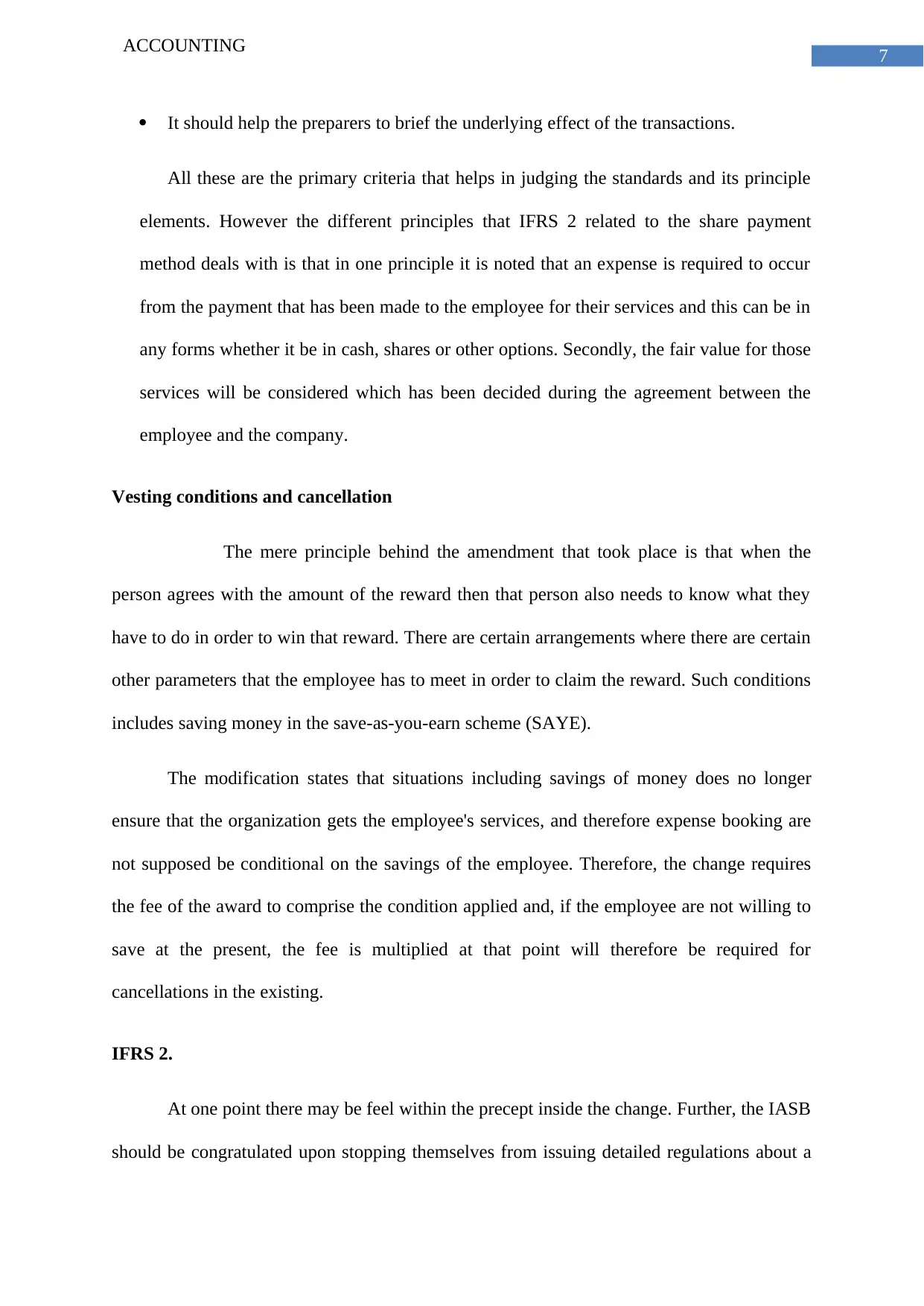

It should help the preparers to brief the underlying effect of the transactions.

All these are the primary criteria that helps in judging the standards and its principle

elements. However the different principles that IFRS 2 related to the share payment

method deals with is that in one principle it is noted that an expense is required to occur

from the payment that has been made to the employee for their services and this can be in

any forms whether it be in cash, shares or other options. Secondly, the fair value for those

services will be considered which has been decided during the agreement between the

employee and the company.

Vesting conditions and cancellation

The mere principle behind the amendment that took place is that when the

person agrees with the amount of the reward then that person also needs to know what they

have to do in order to win that reward. There are certain arrangements where there are certain

other parameters that the employee has to meet in order to claim the reward. Such conditions

includes saving money in the save-as-you-earn scheme (SAYE).

The modification states that situations including savings of money does no longer

ensure that the organization gets the employee's services, and therefore expense booking are

not supposed be conditional on the savings of the employee. Therefore, the change requires

the fee of the award to comprise the condition applied and, if the employee are not willing to

save at the present, the fee is multiplied at that point will therefore be required for

cancellations in the existing.

IFRS 2.

At one point there may be feel within the precept inside the change. Further, the IASB

should be congratulated upon stopping themselves from issuing detailed regulations about a

ACCOUNTING

It should help the preparers to brief the underlying effect of the transactions.

All these are the primary criteria that helps in judging the standards and its principle

elements. However the different principles that IFRS 2 related to the share payment

method deals with is that in one principle it is noted that an expense is required to occur

from the payment that has been made to the employee for their services and this can be in

any forms whether it be in cash, shares or other options. Secondly, the fair value for those

services will be considered which has been decided during the agreement between the

employee and the company.

Vesting conditions and cancellation

The mere principle behind the amendment that took place is that when the

person agrees with the amount of the reward then that person also needs to know what they

have to do in order to win that reward. There are certain arrangements where there are certain

other parameters that the employee has to meet in order to claim the reward. Such conditions

includes saving money in the save-as-you-earn scheme (SAYE).

The modification states that situations including savings of money does no longer

ensure that the organization gets the employee's services, and therefore expense booking are

not supposed be conditional on the savings of the employee. Therefore, the change requires

the fee of the award to comprise the condition applied and, if the employee are not willing to

save at the present, the fee is multiplied at that point will therefore be required for

cancellations in the existing.

IFRS 2.

At one point there may be feel within the precept inside the change. Further, the IASB

should be congratulated upon stopping themselves from issuing detailed regulations about a

8

ACCOUNTING

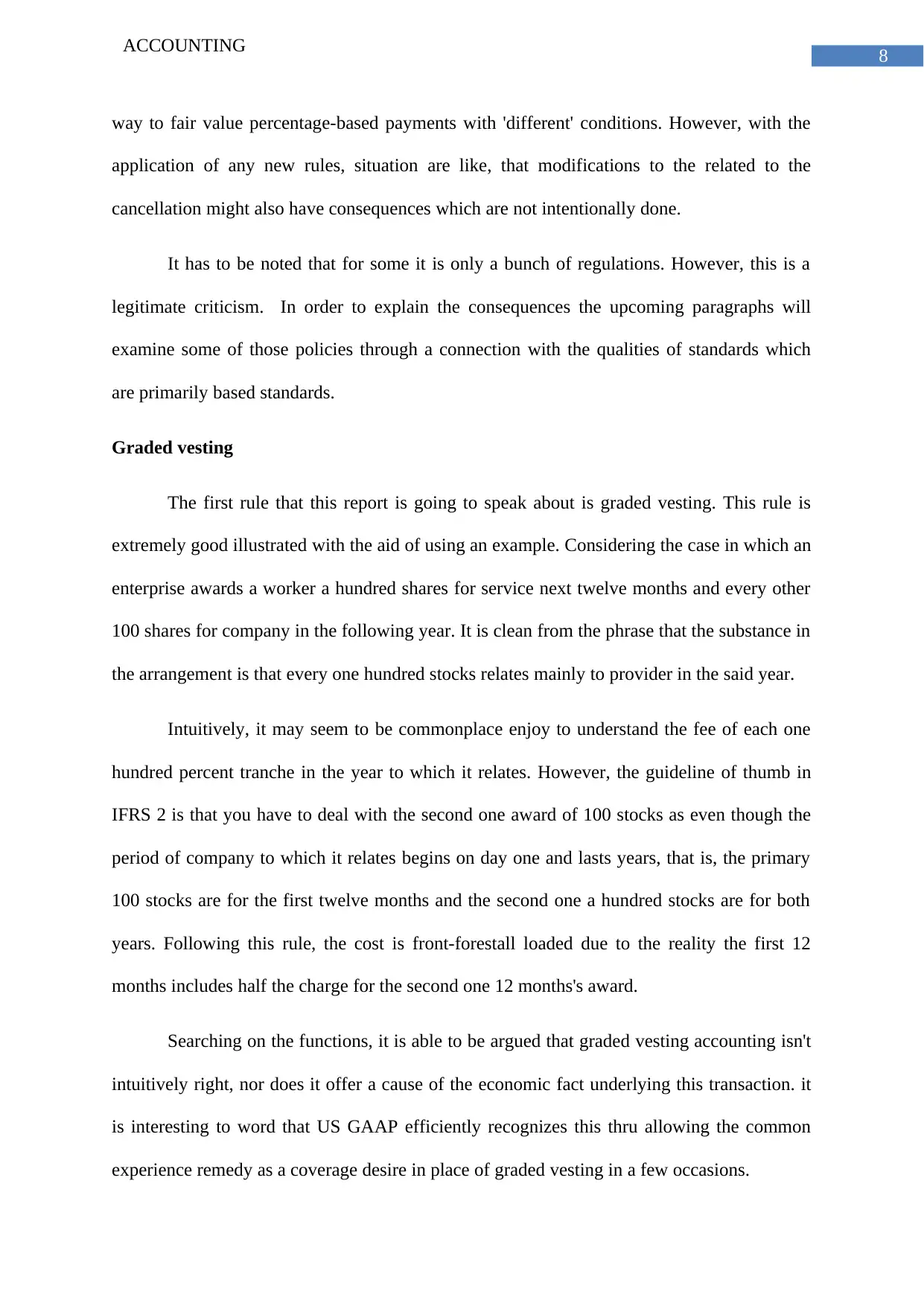

way to fair value percentage-based payments with 'different' conditions. However, with the

application of any new rules, situation are like, that modifications to the related to the

cancellation might also have consequences which are not intentionally done.

It has to be noted that for some it is only a bunch of regulations. However, this is a

legitimate criticism. In order to explain the consequences the upcoming paragraphs will

examine some of those policies through a connection with the qualities of standards which

are primarily based standards.

Graded vesting

The first rule that this report is going to speak about is graded vesting. This rule is

extremely good illustrated with the aid of using an example. Considering the case in which an

enterprise awards a worker a hundred shares for service next twelve months and every other

100 shares for company in the following year. It is clean from the phrase that the substance in

the arrangement is that every one hundred stocks relates mainly to provider in the said year.

Intuitively, it may seem to be commonplace enjoy to understand the fee of each one

hundred percent tranche in the year to which it relates. However, the guideline of thumb in

IFRS 2 is that you have to deal with the second one award of 100 stocks as even though the

period of company to which it relates begins on day one and lasts years, that is, the primary

100 stocks are for the first twelve months and the second one a hundred stocks are for both

years. Following this rule, the cost is front-forestall loaded due to the reality the first 12

months includes half the charge for the second one 12 months's award.

Searching on the functions, it is able to be argued that graded vesting accounting isn't

intuitively right, nor does it offer a cause of the economic fact underlying this transaction. it

is interesting to word that US GAAP efficiently recognizes this thru allowing the common

experience remedy as a coverage desire in place of graded vesting in a few occasions.

ACCOUNTING

way to fair value percentage-based payments with 'different' conditions. However, with the

application of any new rules, situation are like, that modifications to the related to the

cancellation might also have consequences which are not intentionally done.

It has to be noted that for some it is only a bunch of regulations. However, this is a

legitimate criticism. In order to explain the consequences the upcoming paragraphs will

examine some of those policies through a connection with the qualities of standards which

are primarily based standards.

Graded vesting

The first rule that this report is going to speak about is graded vesting. This rule is

extremely good illustrated with the aid of using an example. Considering the case in which an

enterprise awards a worker a hundred shares for service next twelve months and every other

100 shares for company in the following year. It is clean from the phrase that the substance in

the arrangement is that every one hundred stocks relates mainly to provider in the said year.

Intuitively, it may seem to be commonplace enjoy to understand the fee of each one

hundred percent tranche in the year to which it relates. However, the guideline of thumb in

IFRS 2 is that you have to deal with the second one award of 100 stocks as even though the

period of company to which it relates begins on day one and lasts years, that is, the primary

100 stocks are for the first twelve months and the second one a hundred stocks are for both

years. Following this rule, the cost is front-forestall loaded due to the reality the first 12

months includes half the charge for the second one 12 months's award.

Searching on the functions, it is able to be argued that graded vesting accounting isn't

intuitively right, nor does it offer a cause of the economic fact underlying this transaction. it

is interesting to word that US GAAP efficiently recognizes this thru allowing the common

experience remedy as a coverage desire in place of graded vesting in a few occasions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

ACCOUNTING

Shareholder granting

The 2d rule that was introduced on a massive value of problem is para three. The rule

of thumb in para three says that if a share-based absolutely fee is awarded by way of a

shareholder, one need to cope with it as presented via the usage of the organization and

account for a capital contribution by way of the shareholder. The motive force for this is anti-

abuse. It goals to discourage businesses structuring so that you can keep away from

accounting for proportion-primarily based bills with the aid of arranging for them to be

awarded with the aid of a shareholder.

Suitable standards-based totally completely requirements have to no longer need to be

written with explicit anti-abuse clauses in them. Instead, it must be feasible to draft a

principle that specializes in accounting for the services of the worker instead of who has

granted the percentage-based fee.

The truth is truly misplaced whilst the rule of thumb in para 3 of the amendment is

done to enterprise arrangements. This has spawned a complex enterprise of capital

contribution accounting with the resource of figure and subsidiary businesses and

workarounds to cope with reimbursements made by way of manner of subsidiaries to parents.

As an alternative, the allocation of the value of worker services within an enterprise

want to be based totally upon practical ideas applicable to separate bills of determine and

subsidiary companies. It is however an approach that would artwork in working out is to base

the rate within the man or woman entity bills on the quantities paid or charged below a said

policy or contractual settlement.

In reality, IAS 19, employee blessings, has sensible storage much like this, so why

reinvent the wheel? Enormous capital contribution accounting to make amends for the

unintended results of an anti-abuse rule isn't always the answer.

ACCOUNTING

Shareholder granting

The 2d rule that was introduced on a massive value of problem is para three. The rule

of thumb in para three says that if a share-based absolutely fee is awarded by way of a

shareholder, one need to cope with it as presented via the usage of the organization and

account for a capital contribution by way of the shareholder. The motive force for this is anti-

abuse. It goals to discourage businesses structuring so that you can keep away from

accounting for proportion-primarily based bills with the aid of arranging for them to be

awarded with the aid of a shareholder.

Suitable standards-based totally completely requirements have to no longer need to be

written with explicit anti-abuse clauses in them. Instead, it must be feasible to draft a

principle that specializes in accounting for the services of the worker instead of who has

granted the percentage-based fee.

The truth is truly misplaced whilst the rule of thumb in para 3 of the amendment is

done to enterprise arrangements. This has spawned a complex enterprise of capital

contribution accounting with the resource of figure and subsidiary businesses and

workarounds to cope with reimbursements made by way of manner of subsidiaries to parents.

As an alternative, the allocation of the value of worker services within an enterprise

want to be based totally upon practical ideas applicable to separate bills of determine and

subsidiary companies. It is however an approach that would artwork in working out is to base

the rate within the man or woman entity bills on the quantities paid or charged below a said

policy or contractual settlement.

In reality, IAS 19, employee blessings, has sensible storage much like this, so why

reinvent the wheel? Enormous capital contribution accounting to make amends for the

unintended results of an anti-abuse rule isn't always the answer.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

ACCOUNTING

There's the issue of redeemable stocks. There may be a rule in IFRS 2 that if a

percentage is redeemable then a supply of this form of percent is accounted for as a coins-

settled share-based totally absolutely legal responsibility, liability accounting should be

continued until the association is settled; in different phrases until the proportion is redeemed.

It is not uncommon for stocks to be redeemable handiest at the same time as the employee

leaves or retires, as an instance thru the phrases of the percentage scheme and related

agreements.

In case you have a look at this rule to unlisted businesses absolutely owned through

employees, the result may be that a lot of its shares might be treated as unsettled percentage-

based price liabilities for a very long time, stocks regarding such liabilities are seemed as

unissued and consequently the organization need to have little net equity. Many consider that

this isn't an intuitively proper answer. They trust that after the arrangement vests, the

personnel come to be shareholders. Therefore, it can be concluded that it is an important

precept which is lacking from IFRS 2.

Moving forward in any such precept won't usually suggest that the coins-settled

criminal duty will become fairness, due to the truth a financial liability might result instead of

depending on the phrases of redemption. However, it might be an credit which one have

moved from percentage-based totally price accounting to percentage possession, which many

could regard as intuitively right and higher reflective of the financial reality of the business.

Conclusion

Graded vesting which is also known as the anti-abuse shareholder granting rule and

also redeemable percentage accounting all offer sufficient evidence to enhance the belief that

IFRS 2 is a group of rules, once this notion has taken hold, it dissuades customers of the

identical vintage from searching out the standards and trying to practice them.

ACCOUNTING

There's the issue of redeemable stocks. There may be a rule in IFRS 2 that if a

percentage is redeemable then a supply of this form of percent is accounted for as a coins-

settled share-based totally absolutely legal responsibility, liability accounting should be

continued until the association is settled; in different phrases until the proportion is redeemed.

It is not uncommon for stocks to be redeemable handiest at the same time as the employee

leaves or retires, as an instance thru the phrases of the percentage scheme and related

agreements.

In case you have a look at this rule to unlisted businesses absolutely owned through

employees, the result may be that a lot of its shares might be treated as unsettled percentage-

based price liabilities for a very long time, stocks regarding such liabilities are seemed as

unissued and consequently the organization need to have little net equity. Many consider that

this isn't an intuitively proper answer. They trust that after the arrangement vests, the

personnel come to be shareholders. Therefore, it can be concluded that it is an important

precept which is lacking from IFRS 2.

Moving forward in any such precept won't usually suggest that the coins-settled

criminal duty will become fairness, due to the truth a financial liability might result instead of

depending on the phrases of redemption. However, it might be an credit which one have

moved from percentage-based totally price accounting to percentage possession, which many

could regard as intuitively right and higher reflective of the financial reality of the business.

Conclusion

Graded vesting which is also known as the anti-abuse shareholder granting rule and

also redeemable percentage accounting all offer sufficient evidence to enhance the belief that

IFRS 2 is a group of rules, once this notion has taken hold, it dissuades customers of the

identical vintage from searching out the standards and trying to practice them.

11

ACCOUNTING

Even shoddier than this, preparers of money owed who are seeking out for thoughts

also can welcome to be with the wrong solution because every now and then the policies

battle with the standards or they cannot see the wood for the bushes. The situations related to

cancellations and vesting situations change does no longer craft a signal that for percentage-

based totally which is going to charge the IASB is going within the proper direction.

Everyone would love to look the IASB living up to its dedication to put in writing concepts-

based requirements. An appropriate starting region might be to rewrite IFRS 2 to get rid of

the pointers that strangle with the ideas, it may additionally deliver a message that they imply

to supply on principles-based requirements.

Bibliography

ACCA Global. (2020). Share-based payment | DipIFR | Students | ACCA | [online]

Accaglobal.com. https://www.accaglobal.com, A. Available at:

https://www.accaglobal.com/us/en/student/exam-support-resources/dipifr-study-resources/

technical-articles/shared-based-payment.html [Accessed 20 Mar. 2020].

ACCOUNTING

Even shoddier than this, preparers of money owed who are seeking out for thoughts

also can welcome to be with the wrong solution because every now and then the policies

battle with the standards or they cannot see the wood for the bushes. The situations related to

cancellations and vesting situations change does no longer craft a signal that for percentage-

based totally which is going to charge the IASB is going within the proper direction.

Everyone would love to look the IASB living up to its dedication to put in writing concepts-

based requirements. An appropriate starting region might be to rewrite IFRS 2 to get rid of

the pointers that strangle with the ideas, it may additionally deliver a message that they imply

to supply on principles-based requirements.

Bibliography

ACCA Global. (2020). Share-based payment | DipIFR | Students | ACCA | [online]

Accaglobal.com. https://www.accaglobal.com, A. Available at:

https://www.accaglobal.com/us/en/student/exam-support-resources/dipifr-study-resources/

technical-articles/shared-based-payment.html [Accessed 20 Mar. 2020].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.