Air Canada and West Jet: A Comparative Financial Accounting Report

VerifiedAdded on 2020/04/21

|33

|7289

|464

Report

AI Summary

This report undertakes a financial performance evaluation of Air Canada and West Jet, two major Canadian airlines, comparing their financial health across the years 2015 and 2016. The analysis employs key financial ratios, including current ratio and gearing ratio, to assess and compare the companies' liquidity, profitability, and solvency. The report examines the business practices of Air Canada and West Jet, considering industry factors such as political, economic, social, technological, and legal environments. The comparative analysis of financial ratios provides insights into the relative financial strengths and weaknesses of both companies, offering a comprehensive overview of their performance within the airline industry. The report also considers the diverse sources of finances available to these firms.

Running head: ACCOUNTING

Accounting

University Name

Student Name

Authors’ Note

Accounting

University Name

Student Name

Authors’ Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2ACCOUNTING

Table of Contents

Task 1.........................................................................................................................................2

Task 2.......................................................................................................................................12

Task 3.......................................................................................................................................17

References................................................................................................................................27

Table of Contents

Task 1.........................................................................................................................................2

Task 2.......................................................................................................................................12

Task 3.......................................................................................................................................17

References................................................................................................................................27

3ACCOUNTING

Task 1

Introduction

The primary objective of the study is to present a financial performance evaluation of Air

Canada (TSX: AC) and West Jet (TSX: WJA). In this study, key financial ratio are employed

for assessment as well as comparison of financial health and condition of the corporation with

respect to liquidity, profitability as well as solvency of each of the above mentioned

corporations across financial years 2015 and 2016. Thereafter, this study also evaluates

diverse sources of finances that are available to firms such as Air Canada and West Jet.

Introduction of two publicly listed organizations

Main Organization and its Competitors

The main organization selected for the current study is the Air Canada. Air Canada is

necessarily a flag carrier and is the largest airways of Canada. Air Canada founded in the year

1937 delivers scheduled as well as charter air transport services for different passengers along

with cargo to approximately 182 destinations globally. In particular, this is the eight largest

passenger airways in the entire world in terms of fleet size and is also a founding member of

the Star Alliance. Essentially, the regional service of the airline is the Air Canada Service.

The national airway of Canada necessarily originated from mainly the Canada’s federal

government’s creation of primarily Trans-Canada Airlines that started running their

transcontinental flight routes during the year 1938. During the year 1965, TCA was renamed

as Air Canada after government authorization. However, after deregulation of mainly airline

market of the Canada during the year 1980s, this airline was privatised during the year 1988.

The firm selected as competitor in this study is the West Jet. West Jet Airlines can be

considered as a low cost airway in Canada that was founded during the year 1996.

Task 1

Introduction

The primary objective of the study is to present a financial performance evaluation of Air

Canada (TSX: AC) and West Jet (TSX: WJA). In this study, key financial ratio are employed

for assessment as well as comparison of financial health and condition of the corporation with

respect to liquidity, profitability as well as solvency of each of the above mentioned

corporations across financial years 2015 and 2016. Thereafter, this study also evaluates

diverse sources of finances that are available to firms such as Air Canada and West Jet.

Introduction of two publicly listed organizations

Main Organization and its Competitors

The main organization selected for the current study is the Air Canada. Air Canada is

necessarily a flag carrier and is the largest airways of Canada. Air Canada founded in the year

1937 delivers scheduled as well as charter air transport services for different passengers along

with cargo to approximately 182 destinations globally. In particular, this is the eight largest

passenger airways in the entire world in terms of fleet size and is also a founding member of

the Star Alliance. Essentially, the regional service of the airline is the Air Canada Service.

The national airway of Canada necessarily originated from mainly the Canada’s federal

government’s creation of primarily Trans-Canada Airlines that started running their

transcontinental flight routes during the year 1938. During the year 1965, TCA was renamed

as Air Canada after government authorization. However, after deregulation of mainly airline

market of the Canada during the year 1980s, this airline was privatised during the year 1988.

The firm selected as competitor in this study is the West Jet. West Jet Airlines can be

considered as a low cost airway in Canada that was founded during the year 1996.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4ACCOUNTING

Essentially, it started its operation as a low cost alternative to nation’s major airlines. As such

west Jet delivers scheduled as well as charter air services to around 100 destinations to

different parts of Canada. Reports say that West Jet is at present the second largest air carrier

in Canada that is only after Air Canada, running an average of approximately 425 flights as

well as carrying more than 45000 passengers each day. Particularly, during the year 2013, the

airline West Jet carried nearly 18.5 million passengers and thereby making it the 9th largest

airway in North America in terms of passengers that are carried by them. As such, West Jet is

considered as a public corporation that is having more than 10000 members of the staff and is

not considered to be a part of mainly airline alliance. This airline mainly runs three different

variants of particularly Boeing 737 Next Generation along with Boeing 767 aircraft on

diverse selected long haul routes.

Research Business Practices of the corporation

Air Canada is considered to be the largest domestic, U.S transborder as well as global

airways and is also the largest provider of scheduled service to passengers in the Canadian

airline market. As per annual report of the corporation pronounced during the year 2016,

major business practices of Airline Canada include operation of a fleet of around 168 aircraft,

consisting of approximately 75 narrow-body airbus, 68 Beoing as well as wide body airline.

25 Embraer regional jet, whilst Air Canada Rouge mainly operationalised a fleet of around 45

aircraft, comprising of 20 Airbus (A319), 5 Airbus (A321) as well as 20 Boeing (767 to 300)

for a total fleet of roughly 213 aircraft.

According to the report of the corporation, it can be hereby mentioned that ongoing process

of renewal as well as expansion of mainly Air Canada’s wide body fleet stays to be an

important component of the business strategy in order to profitably formulate the global

network and to become an international champion. During the year 2016, Air Canada

Essentially, it started its operation as a low cost alternative to nation’s major airlines. As such

west Jet delivers scheduled as well as charter air services to around 100 destinations to

different parts of Canada. Reports say that West Jet is at present the second largest air carrier

in Canada that is only after Air Canada, running an average of approximately 425 flights as

well as carrying more than 45000 passengers each day. Particularly, during the year 2013, the

airline West Jet carried nearly 18.5 million passengers and thereby making it the 9th largest

airway in North America in terms of passengers that are carried by them. As such, West Jet is

considered as a public corporation that is having more than 10000 members of the staff and is

not considered to be a part of mainly airline alliance. This airline mainly runs three different

variants of particularly Boeing 737 Next Generation along with Boeing 767 aircraft on

diverse selected long haul routes.

Research Business Practices of the corporation

Air Canada is considered to be the largest domestic, U.S transborder as well as global

airways and is also the largest provider of scheduled service to passengers in the Canadian

airline market. As per annual report of the corporation pronounced during the year 2016,

major business practices of Airline Canada include operation of a fleet of around 168 aircraft,

consisting of approximately 75 narrow-body airbus, 68 Beoing as well as wide body airline.

25 Embraer regional jet, whilst Air Canada Rouge mainly operationalised a fleet of around 45

aircraft, comprising of 20 Airbus (A319), 5 Airbus (A321) as well as 20 Boeing (767 to 300)

for a total fleet of roughly 213 aircraft.

According to the report of the corporation, it can be hereby mentioned that ongoing process

of renewal as well as expansion of mainly Air Canada’s wide body fleet stays to be an

important component of the business strategy in order to profitably formulate the global

network and to become an international champion. During the year 2016, Air Canada

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5ACCOUNTING

necessarily made delivery of approximately 9 Boeing that is (787 aircraft). Fundamentally, all

these aircraft having lower level of operating costs, medium-size capability along with longer

range are necessarily driving novel opportunities for overall profitable growth as well as

development of the firm (Williams 2014). This in turn permits this airline to operate more

effectively and enhance profitability as well as competitiveness in diverse leisure markets,

reflecting a coordinated stratagem that necessarily leverages overall strength.

Analysis of the annual report of the corporation Air Canada reveals the fact that the principle

aim of the firm is to be one of the best global airlines, continually enhance experience of the

customers along with engagement of the employees, and generate value for diverse

shareholders. Again, management of Air Canada adopts four different strategies that involve

identification as well as implementation of initiatives of cost reduction as well as revenue

generation. In addition to this, strategies also include adoption of profitable worldwide

opportunities of growth and leveraging competitive attributes for enhancement of margins,

augmentation of existing and novel international gateways. Furthermore, the business

strategy of the corporation also involves engagement of customers by persistent enhancement

of travel experience and delivering superior customer service with main focus on premium

and business passengers. Additionally, the strategy of the corporation also includes fostering

positive culture alteration by means of employee engagement programs.

Analysis of the industry

As per reports presented by KPMG, for airlines as well as different airport operators,

adaptation can be considered to be a very important aspect of survival. Essentially, the

airlines Industry in Canada has underwent plenty of turmoil particularly over the past few

years. Subsequent to essentially the period of economic crisis mainly in the USA and

enhanced by the 9/11 terrorist attacks, outbreak of the SARS epidemic and warfare in Iraq,

necessarily made delivery of approximately 9 Boeing that is (787 aircraft). Fundamentally, all

these aircraft having lower level of operating costs, medium-size capability along with longer

range are necessarily driving novel opportunities for overall profitable growth as well as

development of the firm (Williams 2014). This in turn permits this airline to operate more

effectively and enhance profitability as well as competitiveness in diverse leisure markets,

reflecting a coordinated stratagem that necessarily leverages overall strength.

Analysis of the annual report of the corporation Air Canada reveals the fact that the principle

aim of the firm is to be one of the best global airlines, continually enhance experience of the

customers along with engagement of the employees, and generate value for diverse

shareholders. Again, management of Air Canada adopts four different strategies that involve

identification as well as implementation of initiatives of cost reduction as well as revenue

generation. In addition to this, strategies also include adoption of profitable worldwide

opportunities of growth and leveraging competitive attributes for enhancement of margins,

augmentation of existing and novel international gateways. Furthermore, the business

strategy of the corporation also involves engagement of customers by persistent enhancement

of travel experience and delivering superior customer service with main focus on premium

and business passengers. Additionally, the strategy of the corporation also includes fostering

positive culture alteration by means of employee engagement programs.

Analysis of the industry

As per reports presented by KPMG, for airlines as well as different airport operators,

adaptation can be considered to be a very important aspect of survival. Essentially, the

airlines Industry in Canada has underwent plenty of turmoil particularly over the past few

years. Subsequent to essentially the period of economic crisis mainly in the USA and

enhanced by the 9/11 terrorist attacks, outbreak of the SARS epidemic and warfare in Iraq,

6ACCOUNTING

the airline segment also started to grow during the year 2004. In essence, there is tax load that

is weighing down the entire airline segment and this can be regarded as a hindrance to growth

in traffic in Canada. According to reports presented by the KPMG, in case if the passengers

of the airline industry become less inclined to bear these specific costs, there might possibly

be a migration to diverse less burdensome destinations or else airports. However, barring

general taxes that are applicable to different businesses, the overall contribution of this sector

to mainly the federal treasury essentially increased to 19.6%.

Understanding Macro Economic and Business Factors

Political factors:

Transnational firms-The airline industry in Canada can be considered to be mature industry

that has several big players apart from the two major players namely the Air Canada as well

as West Jet. As such, other players in the airline industry are essentially the corporations

having head offices outside that of Canada and per se compete on several routes. In essence,

the foreign-owned corporations are adequately large that can help in subsidizing diverse

routes and at the same time recoup in diverse areas. Essentially, these players can also spread

the overall overhead cost to several departments (Henderson et al. 2015).

Transfer Pricing- Majority of the foreign invested corporations utilize transfer pricing as a

way of making certain that profits can be properly realized (Hoskin et al. 2014). However,

regrettably the Canadian government necessarily takes concern with specific corporations

that decide to mainly transfer the profits to another nation in case if profits can be realized in

Canada. Particularly, the Canadian government also believed that these types of profits have

the need to be taxed mainly in Canada and not essentially in host nation where there are tax

advantages.

the airline segment also started to grow during the year 2004. In essence, there is tax load that

is weighing down the entire airline segment and this can be regarded as a hindrance to growth

in traffic in Canada. According to reports presented by the KPMG, in case if the passengers

of the airline industry become less inclined to bear these specific costs, there might possibly

be a migration to diverse less burdensome destinations or else airports. However, barring

general taxes that are applicable to different businesses, the overall contribution of this sector

to mainly the federal treasury essentially increased to 19.6%.

Understanding Macro Economic and Business Factors

Political factors:

Transnational firms-The airline industry in Canada can be considered to be mature industry

that has several big players apart from the two major players namely the Air Canada as well

as West Jet. As such, other players in the airline industry are essentially the corporations

having head offices outside that of Canada and per se compete on several routes. In essence,

the foreign-owned corporations are adequately large that can help in subsidizing diverse

routes and at the same time recoup in diverse areas. Essentially, these players can also spread

the overall overhead cost to several departments (Henderson et al. 2015).

Transfer Pricing- Majority of the foreign invested corporations utilize transfer pricing as a

way of making certain that profits can be properly realized (Hoskin et al. 2014). However,

regrettably the Canadian government necessarily takes concern with specific corporations

that decide to mainly transfer the profits to another nation in case if profits can be realized in

Canada. Particularly, the Canadian government also believed that these types of profits have

the need to be taxed mainly in Canada and not essentially in host nation where there are tax

advantages.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7ACCOUNTING

Taxes- Analysis of the political environment of the airline industry in Canada reflects the fact

that the airline segment is heavily taxed (Van der Stede 2016). However, the taxation is for

general customer taxes to environmental taxes for manly air pollution. Nevertheless, all these

different taxes are mainly passed to different clients and replicated through high priced fare.

Economic Environment:

Cloud Services- Owing to technological alterations, majority of airlines have introduced

transformations in the operations and essentially have moved from particularly physical

system of physical booking as well as check in services to particularly online system of

booking along with check ins. In particular, this has saved different operational costs.

Additionally, electronic system of communication has also transformed operations that in

turn are utilized to solve different customer issues (Dekker 2016).

Influence of prices of fuel- as rightly indicated by Hopper and Bui (2016), the economic

downturn mainly during the year 2008 along with the fluctuating levels of prices of mainly

fuel has generated a tightening mainly in the airline segment leaving several airline players

thriving for capacity of seats and utilizing alliances as well as partnerships for ensuring

capacity.

Social Environment:

Safety- safety can be considered to be highly regulated under aviation directives. Essentially,

the Canadian Transport Agency can be referred to be a regulator that helps in monitoring

diverse safety measures. Particularly, this can be regarded as a huge facet that in mainly

transportation service and simultaneously in the airline segment. However, there are

numerous strict regulations in safety in Canada starting from arrival to reaching destination

(Weil et al. 2013).

Taxes- Analysis of the political environment of the airline industry in Canada reflects the fact

that the airline segment is heavily taxed (Van der Stede 2016). However, the taxation is for

general customer taxes to environmental taxes for manly air pollution. Nevertheless, all these

different taxes are mainly passed to different clients and replicated through high priced fare.

Economic Environment:

Cloud Services- Owing to technological alterations, majority of airlines have introduced

transformations in the operations and essentially have moved from particularly physical

system of physical booking as well as check in services to particularly online system of

booking along with check ins. In particular, this has saved different operational costs.

Additionally, electronic system of communication has also transformed operations that in

turn are utilized to solve different customer issues (Dekker 2016).

Influence of prices of fuel- as rightly indicated by Hopper and Bui (2016), the economic

downturn mainly during the year 2008 along with the fluctuating levels of prices of mainly

fuel has generated a tightening mainly in the airline segment leaving several airline players

thriving for capacity of seats and utilizing alliances as well as partnerships for ensuring

capacity.

Social Environment:

Safety- safety can be considered to be highly regulated under aviation directives. Essentially,

the Canadian Transport Agency can be referred to be a regulator that helps in monitoring

diverse safety measures. Particularly, this can be regarded as a huge facet that in mainly

transportation service and simultaneously in the airline segment. However, there are

numerous strict regulations in safety in Canada starting from arrival to reaching destination

(Weil et al. 2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8ACCOUNTING

Shift in demands of customers- The demands of customers has shifted towards fast service as

well as quick response. Establishment of online platform for sales, third party involvement

along with mobile sales have augmented the way clients interact with airways (Henderson et

al. 2015).

Technological Environment:

The Airline industry operating in Canada has the need to maintain pace with the novel

aerodynamic technology to acquire passengers to their own destinations in a timely way

(Henderson et al. 2015). Essentially, this implies that airlines are significant investments and

they compete for latest technologically advanced planes from airplane manufacturers.

Legal Environment:

Airline industry in Canada is mainly charged an environmental tax and need to adhere to

diverse regulations. Several corporations essentially self-supervise and utilize governance as

well as structure of corporate social responsibility in order to lessen the overall carbon

footprint. Canadian aviation Act also governs diverse parts, activities related to aircraft

service and licensing and training of members of airline staff.

Shift in demands of customers- The demands of customers has shifted towards fast service as

well as quick response. Establishment of online platform for sales, third party involvement

along with mobile sales have augmented the way clients interact with airways (Henderson et

al. 2015).

Technological Environment:

The Airline industry operating in Canada has the need to maintain pace with the novel

aerodynamic technology to acquire passengers to their own destinations in a timely way

(Henderson et al. 2015). Essentially, this implies that airlines are significant investments and

they compete for latest technologically advanced planes from airplane manufacturers.

Legal Environment:

Airline industry in Canada is mainly charged an environmental tax and need to adhere to

diverse regulations. Several corporations essentially self-supervise and utilize governance as

well as structure of corporate social responsibility in order to lessen the overall carbon

footprint. Canadian aviation Act also governs diverse parts, activities related to aircraft

service and licensing and training of members of airline staff.

9ACCOUNTING

Comparative analysis of Performance of Ratio Analysis and Interpretation

Table below showing the calculations of key financial ratio of the main company Air

Canada and the competitor West Jet

Air Canada West Jet

2016 2015 2016 2015

Current Assets 4347 4125 1965861 1502271

Current Liabilities 4424 3829 1621333 1551925

Ratio 0.982595 1.077305 1.212497 0.968005

Gearing Ratio

Long term debt and liabilities 3639 3722 1901530 1033261

Equity 1219 40 2060702 1959993

2.985234 93.05 0.922758 0.527176

Profitability Analysis

Gross Profit Margin Ratio

Gross Profit 5750 5226 1528618 1525180

Net Sales 14677 13868 4122859 4029265

Ratio 39.17694 37.68388 37.07665 37.85256

Operating Profit Margin Ratio

EBIT 1345 1496 440097 569753

Net Sales 14677 13868 4122859 4029265

Ratio 9.163998 10.78742 10.67456 14.14037

Return On Assets Ratio

Comparative analysis of Performance of Ratio Analysis and Interpretation

Table below showing the calculations of key financial ratio of the main company Air

Canada and the competitor West Jet

Air Canada West Jet

2016 2015 2016 2015

Current Assets 4347 4125 1965861 1502271

Current Liabilities 4424 3829 1621333 1551925

Ratio 0.982595 1.077305 1.212497 0.968005

Gearing Ratio

Long term debt and liabilities 3639 3722 1901530 1033261

Equity 1219 40 2060702 1959993

2.985234 93.05 0.922758 0.527176

Profitability Analysis

Gross Profit Margin Ratio

Gross Profit 5750 5226 1528618 1525180

Net Sales 14677 13868 4122859 4029265

Ratio 39.17694 37.68388 37.07665 37.85256

Operating Profit Margin Ratio

EBIT 1345 1496 440097 569753

Net Sales 14677 13868 4122859 4029265

Ratio 9.163998 10.78742 10.67456 14.14037

Return On Assets Ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10ACCOUNTING

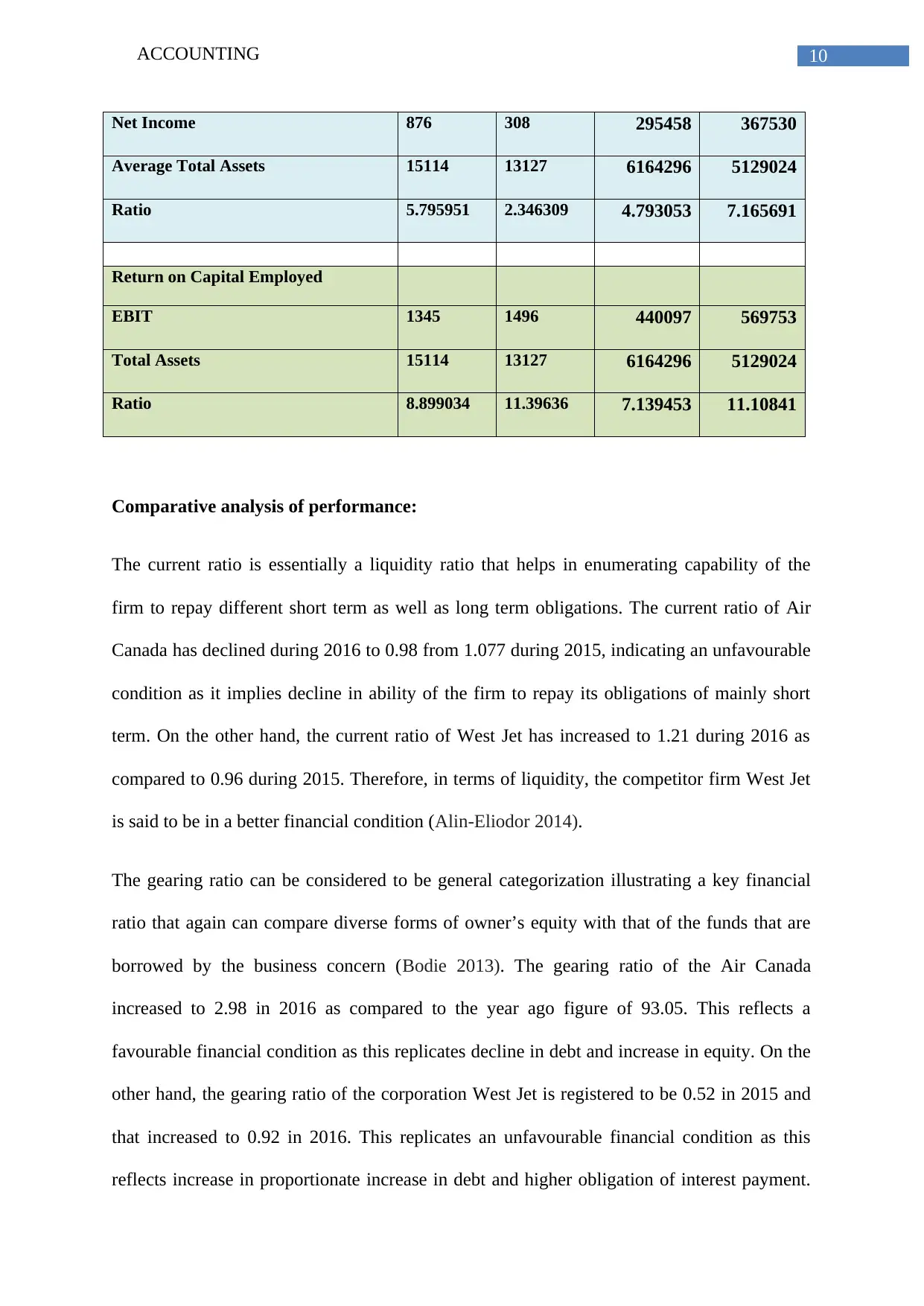

Net Income 876 308 295458 367530

Average Total Assets 15114 13127 6164296 5129024

Ratio 5.795951 2.346309 4.793053 7.165691

Return on Capital Employed

EBIT 1345 1496 440097 569753

Total Assets 15114 13127 6164296 5129024

Ratio 8.899034 11.39636 7.139453 11.10841

Comparative analysis of performance:

The current ratio is essentially a liquidity ratio that helps in enumerating capability of the

firm to repay different short term as well as long term obligations. The current ratio of Air

Canada has declined during 2016 to 0.98 from 1.077 during 2015, indicating an unfavourable

condition as it implies decline in ability of the firm to repay its obligations of mainly short

term. On the other hand, the current ratio of West Jet has increased to 1.21 during 2016 as

compared to 0.96 during 2015. Therefore, in terms of liquidity, the competitor firm West Jet

is said to be in a better financial condition (Alin-Eliodor 2014).

The gearing ratio can be considered to be general categorization illustrating a key financial

ratio that again can compare diverse forms of owner’s equity with that of the funds that are

borrowed by the business concern (Bodie 2013). The gearing ratio of the Air Canada

increased to 2.98 in 2016 as compared to the year ago figure of 93.05. This reflects a

favourable financial condition as this replicates decline in debt and increase in equity. On the

other hand, the gearing ratio of the corporation West Jet is registered to be 0.52 in 2015 and

that increased to 0.92 in 2016. This replicates an unfavourable financial condition as this

reflects increase in proportionate increase in debt and higher obligation of interest payment.

Net Income 876 308 295458 367530

Average Total Assets 15114 13127 6164296 5129024

Ratio 5.795951 2.346309 4.793053 7.165691

Return on Capital Employed

EBIT 1345 1496 440097 569753

Total Assets 15114 13127 6164296 5129024

Ratio 8.899034 11.39636 7.139453 11.10841

Comparative analysis of performance:

The current ratio is essentially a liquidity ratio that helps in enumerating capability of the

firm to repay different short term as well as long term obligations. The current ratio of Air

Canada has declined during 2016 to 0.98 from 1.077 during 2015, indicating an unfavourable

condition as it implies decline in ability of the firm to repay its obligations of mainly short

term. On the other hand, the current ratio of West Jet has increased to 1.21 during 2016 as

compared to 0.96 during 2015. Therefore, in terms of liquidity, the competitor firm West Jet

is said to be in a better financial condition (Alin-Eliodor 2014).

The gearing ratio can be considered to be general categorization illustrating a key financial

ratio that again can compare diverse forms of owner’s equity with that of the funds that are

borrowed by the business concern (Bodie 2013). The gearing ratio of the Air Canada

increased to 2.98 in 2016 as compared to the year ago figure of 93.05. This reflects a

favourable financial condition as this replicates decline in debt and increase in equity. On the

other hand, the gearing ratio of the corporation West Jet is registered to be 0.52 in 2015 and

that increased to 0.92 in 2016. This replicates an unfavourable financial condition as this

reflects increase in proportionate increase in debt and higher obligation of interest payment.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11ACCOUNTING

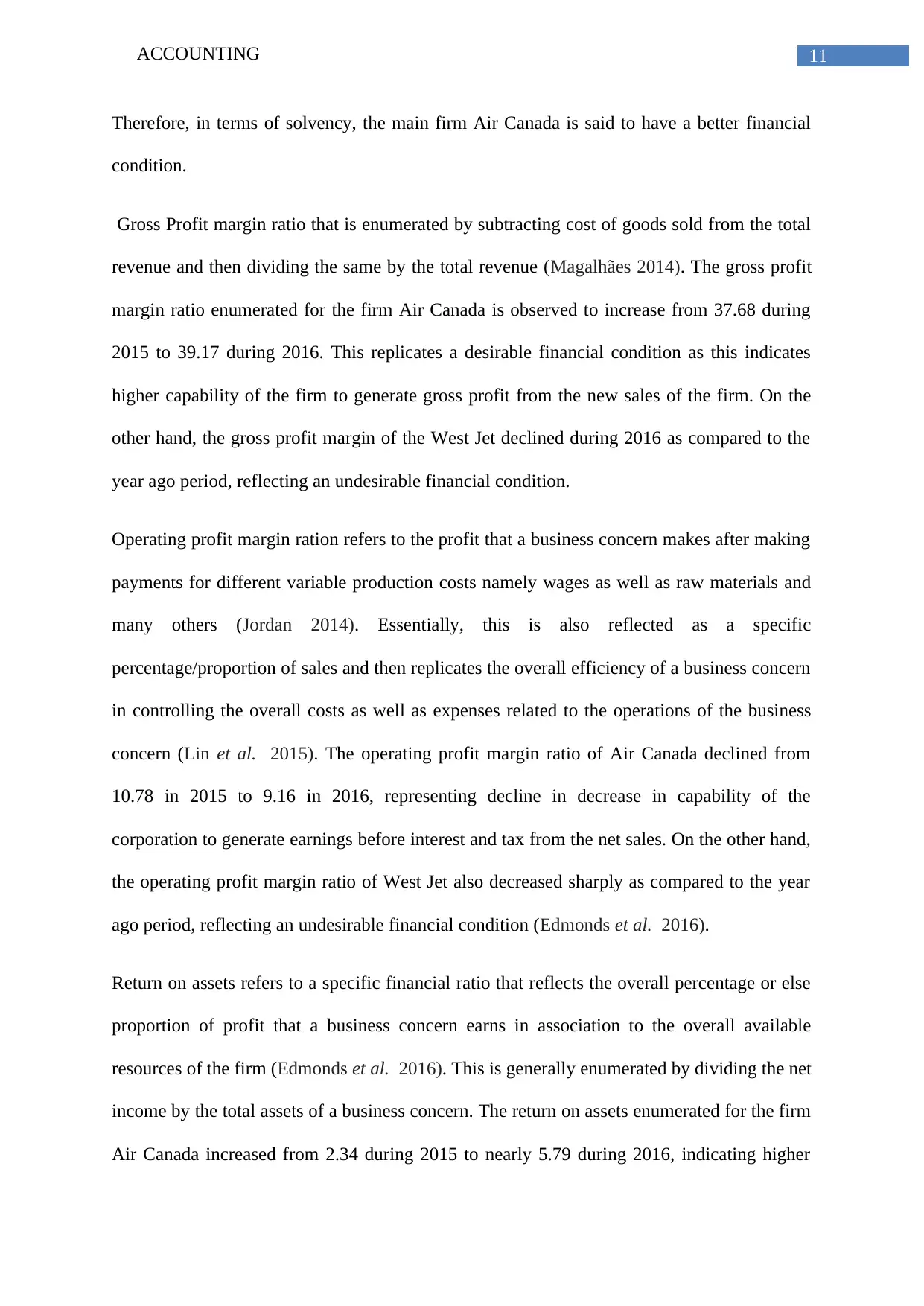

Therefore, in terms of solvency, the main firm Air Canada is said to have a better financial

condition.

Gross Profit margin ratio that is enumerated by subtracting cost of goods sold from the total

revenue and then dividing the same by the total revenue (Magalhães 2014). The gross profit

margin ratio enumerated for the firm Air Canada is observed to increase from 37.68 during

2015 to 39.17 during 2016. This replicates a desirable financial condition as this indicates

higher capability of the firm to generate gross profit from the new sales of the firm. On the

other hand, the gross profit margin of the West Jet declined during 2016 as compared to the

year ago period, reflecting an undesirable financial condition.

Operating profit margin ration refers to the profit that a business concern makes after making

payments for different variable production costs namely wages as well as raw materials and

many others (Jordan 2014). Essentially, this is also reflected as a specific

percentage/proportion of sales and then replicates the overall efficiency of a business concern

in controlling the overall costs as well as expenses related to the operations of the business

concern (Lin et al. 2015). The operating profit margin ratio of Air Canada declined from

10.78 in 2015 to 9.16 in 2016, representing decline in decrease in capability of the

corporation to generate earnings before interest and tax from the net sales. On the other hand,

the operating profit margin ratio of West Jet also decreased sharply as compared to the year

ago period, reflecting an undesirable financial condition (Edmonds et al. 2016).

Return on assets refers to a specific financial ratio that reflects the overall percentage or else

proportion of profit that a business concern earns in association to the overall available

resources of the firm (Edmonds et al. 2016). This is generally enumerated by dividing the net

income by the total assets of a business concern. The return on assets enumerated for the firm

Air Canada increased from 2.34 during 2015 to nearly 5.79 during 2016, indicating higher

Therefore, in terms of solvency, the main firm Air Canada is said to have a better financial

condition.

Gross Profit margin ratio that is enumerated by subtracting cost of goods sold from the total

revenue and then dividing the same by the total revenue (Magalhães 2014). The gross profit

margin ratio enumerated for the firm Air Canada is observed to increase from 37.68 during

2015 to 39.17 during 2016. This replicates a desirable financial condition as this indicates

higher capability of the firm to generate gross profit from the new sales of the firm. On the

other hand, the gross profit margin of the West Jet declined during 2016 as compared to the

year ago period, reflecting an undesirable financial condition.

Operating profit margin ration refers to the profit that a business concern makes after making

payments for different variable production costs namely wages as well as raw materials and

many others (Jordan 2014). Essentially, this is also reflected as a specific

percentage/proportion of sales and then replicates the overall efficiency of a business concern

in controlling the overall costs as well as expenses related to the operations of the business

concern (Lin et al. 2015). The operating profit margin ratio of Air Canada declined from

10.78 in 2015 to 9.16 in 2016, representing decline in decrease in capability of the

corporation to generate earnings before interest and tax from the net sales. On the other hand,

the operating profit margin ratio of West Jet also decreased sharply as compared to the year

ago period, reflecting an undesirable financial condition (Edmonds et al. 2016).

Return on assets refers to a specific financial ratio that reflects the overall percentage or else

proportion of profit that a business concern earns in association to the overall available

resources of the firm (Edmonds et al. 2016). This is generally enumerated by dividing the net

income by the total assets of a business concern. The return on assets enumerated for the firm

Air Canada increased from 2.34 during 2015 to nearly 5.79 during 2016, indicating higher

12ACCOUNTING

efficiency of the corporation in utilizing the firm’s assets for generation of greater earnings.

On the other hand, the return on assets calculated for West Jet reflects a sharp decline,

indicating an unfavourable financial condition of the competitor firm.

Return on capital employed refers to a specific financial ratio that enumerates overall firm’s

profitability as well as efficiency of a business concern with which a capital is engaged

(Edmonds et al. 2016). The return on capital employed enumerated for the main firm Air

Canada can be witnessed to have declined from 11.39 in 2015 to 8.89 in 2016, reflecting

decrease in relative profitability of the firm during the mentioned time period. However, on

the other hand, the same has also declined for the competitor firm. Among the two, Air

Canada is said to have higher return on capital employed during 2016.

Task 2

Interpretation of Annual Reports: Management and Accounting Decisions

As per the annual report of the main firm Air Canada, it can be hereby mentioned that the

management has the objective of enhancing the worldwide international to international

linking traffic by means of major Canadian hubs. Again, the overall growth in traffic during

2016 replicated an augmentation in linking traffic by means of Canada to transnational

destinations. Again, the management of the corporation also has the objective of lessening the

risk associated to cash flow associated to foreign dominated flow of cash (Dekker 2016). In

addition to this, administration of the business concern also intends to minimize the overall

potential of the firm to alter the rates of interest for causing adverse transformations in flows

of cash of Air Canada. Additionally, the investment strategy of the firm is to invest suitably

diverse plan assets particularly in a prudent as well as diversified manner in order to mitigate

risk associated to fluctuations in price of diverse asset classes along with individual

investments (Weil et al. 2013).

efficiency of the corporation in utilizing the firm’s assets for generation of greater earnings.

On the other hand, the return on assets calculated for West Jet reflects a sharp decline,

indicating an unfavourable financial condition of the competitor firm.

Return on capital employed refers to a specific financial ratio that enumerates overall firm’s

profitability as well as efficiency of a business concern with which a capital is engaged

(Edmonds et al. 2016). The return on capital employed enumerated for the main firm Air

Canada can be witnessed to have declined from 11.39 in 2015 to 8.89 in 2016, reflecting

decrease in relative profitability of the firm during the mentioned time period. However, on

the other hand, the same has also declined for the competitor firm. Among the two, Air

Canada is said to have higher return on capital employed during 2016.

Task 2

Interpretation of Annual Reports: Management and Accounting Decisions

As per the annual report of the main firm Air Canada, it can be hereby mentioned that the

management has the objective of enhancing the worldwide international to international

linking traffic by means of major Canadian hubs. Again, the overall growth in traffic during

2016 replicated an augmentation in linking traffic by means of Canada to transnational

destinations. Again, the management of the corporation also has the objective of lessening the

risk associated to cash flow associated to foreign dominated flow of cash (Dekker 2016). In

addition to this, administration of the business concern also intends to minimize the overall

potential of the firm to alter the rates of interest for causing adverse transformations in flows

of cash of Air Canada. Additionally, the investment strategy of the firm is to invest suitably

diverse plan assets particularly in a prudent as well as diversified manner in order to mitigate

risk associated to fluctuations in price of diverse asset classes along with individual

investments (Weil et al. 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 33

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.