Managerial Accounting BAO5522: Air Traffic Navigation Systems Analysis

VerifiedAdded on 2022/10/16

|37

|4921

|410

Report

AI Summary

This report provides a comprehensive analysis of the managerial accounting practices of Air Traffic Navigation Systems Ltd, evaluating its reporting framework against the PwC Value Framework. The assessment examines various aspects of the business, including strategies and objectives, business models, governance, risk management, remuneration, financial and physical assets, customer relations, people and culture, innovation, brands and intellectual assets, processes and supply chain, operational, economic, social, environmental, and segmental performance. Each element is critically analyzed based on report extracts, providing reporting critiques, assessing extensiveness and accessibility, and evaluating comprehensiveness. The analysis offers conclusions and strengths for each element, determining the overall quality of reporting. The report highlights key areas such as strategies for sustainability, corporate governance, risk management policies, remuneration structures, and financial asset management. The study aims to assess the alignment of the company's reporting with the PwC framework, identifying strengths and weaknesses in the presentation of performance information.

Running head: MANAGERIAL ACCOUNTING

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

MANAGERIAL ACCOUNTING

Executive Summary

The main purpose of the assessment is to analyze the business of Air Traffic Navigation Systems

ltd which is engaged in managing air traffic in an appropriate manner. The reporting framework

of the business is considered and analyzed if the same is consistent with the PwC framework of

the business. The discussion would be covering different areas of reporting which is managed by

the business.

MANAGERIAL ACCOUNTING

Executive Summary

The main purpose of the assessment is to analyze the business of Air Traffic Navigation Systems

ltd which is engaged in managing air traffic in an appropriate manner. The reporting framework

of the business is considered and analyzed if the same is consistent with the PwC framework of

the business. The discussion would be covering different areas of reporting which is managed by

the business.

2

MANAGERIAL ACCOUNTING

Table of Contents

PwC Value Framework Elements....................................................................................................8

1. Value Framework Element: Strategies and Objectives............................................................8

Report Extracts:...........................................................................................................................8

Reporting Critique.......................................................................................................................9

Extensiveness and Accessibility..................................................................................................9

Comprehensiveness.....................................................................................................................9

Conclusion and Strength..............................................................................................................9

2. Value Framework Element: Business Model.........................................................................10

Report Extracts:.........................................................................................................................10

Reporting Critique.....................................................................................................................10

Extensiveness and Accessibility................................................................................................10

Comprehensiveness...................................................................................................................11

Conclusion and Strength............................................................................................................11

3. Value Framework Element: Governance...............................................................................11

Report Extracts:.........................................................................................................................11

Reporting Critique.....................................................................................................................12

Extensiveness and Accessibility................................................................................................12

Comprehensiveness...................................................................................................................13

Conclusion and Strength............................................................................................................13

MANAGERIAL ACCOUNTING

Table of Contents

PwC Value Framework Elements....................................................................................................8

1. Value Framework Element: Strategies and Objectives............................................................8

Report Extracts:...........................................................................................................................8

Reporting Critique.......................................................................................................................9

Extensiveness and Accessibility..................................................................................................9

Comprehensiveness.....................................................................................................................9

Conclusion and Strength..............................................................................................................9

2. Value Framework Element: Business Model.........................................................................10

Report Extracts:.........................................................................................................................10

Reporting Critique.....................................................................................................................10

Extensiveness and Accessibility................................................................................................10

Comprehensiveness...................................................................................................................11

Conclusion and Strength............................................................................................................11

3. Value Framework Element: Governance...............................................................................11

Report Extracts:.........................................................................................................................11

Reporting Critique.....................................................................................................................12

Extensiveness and Accessibility................................................................................................12

Comprehensiveness...................................................................................................................13

Conclusion and Strength............................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

MANAGERIAL ACCOUNTING

4. Value Framework Element: Risk Management.....................................................................13

Report Extracts:.........................................................................................................................13

Reporting Critique.....................................................................................................................14

Extensiveness and Accessibility................................................................................................14

Comprehensiveness...................................................................................................................14

Conclusion and Strength............................................................................................................14

5. Value Framework Element: Remuneration............................................................................15

Report Extracts:.........................................................................................................................15

Reporting Critique.....................................................................................................................16

Extensiveness and Accessibility................................................................................................16

Comprehensiveness...................................................................................................................16

Conclusion and Strength............................................................................................................16

6. Value Framework Element: Financial Assets........................................................................17

Report Extracts:.........................................................................................................................17

Reporting Critique.....................................................................................................................17

Extensiveness and Accessibility................................................................................................18

Comprehensiveness...................................................................................................................18

Conclusion and Strength............................................................................................................18

7. Value Framework Element: Physical Assets..........................................................................19

Report Extracts:.........................................................................................................................19

MANAGERIAL ACCOUNTING

4. Value Framework Element: Risk Management.....................................................................13

Report Extracts:.........................................................................................................................13

Reporting Critique.....................................................................................................................14

Extensiveness and Accessibility................................................................................................14

Comprehensiveness...................................................................................................................14

Conclusion and Strength............................................................................................................14

5. Value Framework Element: Remuneration............................................................................15

Report Extracts:.........................................................................................................................15

Reporting Critique.....................................................................................................................16

Extensiveness and Accessibility................................................................................................16

Comprehensiveness...................................................................................................................16

Conclusion and Strength............................................................................................................16

6. Value Framework Element: Financial Assets........................................................................17

Report Extracts:.........................................................................................................................17

Reporting Critique.....................................................................................................................17

Extensiveness and Accessibility................................................................................................18

Comprehensiveness...................................................................................................................18

Conclusion and Strength............................................................................................................18

7. Value Framework Element: Physical Assets..........................................................................19

Report Extracts:.........................................................................................................................19

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

MANAGERIAL ACCOUNTING

Reporting Critique.....................................................................................................................19

Extensiveness and Accessibility................................................................................................20

Comprehensiveness...................................................................................................................20

Conclusion and Strength............................................................................................................20

8. Value Framework Element: Customers.................................................................................21

Report Extracts:.........................................................................................................................21

Reporting Critique.....................................................................................................................21

Extensiveness and Accessibility................................................................................................21

Comprehensiveness...................................................................................................................21

Conclusion and Strength............................................................................................................22

9. Value Framework Element: People & Culture.......................................................................22

Report Extracts:.........................................................................................................................22

Reporting Critique.....................................................................................................................23

Extensiveness and Accessibility................................................................................................23

Comprehensiveness...................................................................................................................23

Conclusion and Strength............................................................................................................23

10. Value Framework Element: Innovation G&S....................................................................24

Report Extracts:.........................................................................................................................24

Reporting Critique.....................................................................................................................25

Extensiveness and Accessibility................................................................................................25

MANAGERIAL ACCOUNTING

Reporting Critique.....................................................................................................................19

Extensiveness and Accessibility................................................................................................20

Comprehensiveness...................................................................................................................20

Conclusion and Strength............................................................................................................20

8. Value Framework Element: Customers.................................................................................21

Report Extracts:.........................................................................................................................21

Reporting Critique.....................................................................................................................21

Extensiveness and Accessibility................................................................................................21

Comprehensiveness...................................................................................................................21

Conclusion and Strength............................................................................................................22

9. Value Framework Element: People & Culture.......................................................................22

Report Extracts:.........................................................................................................................22

Reporting Critique.....................................................................................................................23

Extensiveness and Accessibility................................................................................................23

Comprehensiveness...................................................................................................................23

Conclusion and Strength............................................................................................................23

10. Value Framework Element: Innovation G&S....................................................................24

Report Extracts:.........................................................................................................................24

Reporting Critique.....................................................................................................................25

Extensiveness and Accessibility................................................................................................25

5

MANAGERIAL ACCOUNTING

Comprehensiveness...................................................................................................................25

Conclusion and Strength............................................................................................................25

11. Value Framework Element: Brands and Intellectual Assets..............................................26

Report Extracts:.........................................................................................................................26

Reporting Critique.....................................................................................................................26

Extensiveness and Accessibility................................................................................................27

Comprehensiveness...................................................................................................................27

Conclusion and Strength............................................................................................................27

12. Value Framework Element: Processes and Supply Chain..................................................27

Report Extracts:.........................................................................................................................27

Reporting Critique.....................................................................................................................27

Extensiveness and Accessibility................................................................................................28

Comprehensiveness...................................................................................................................28

Conclusion and Strength............................................................................................................28

13. Value Framework Element: Operational Performance.......................................................29

Report Extracts:.........................................................................................................................29

Reporting Critique.....................................................................................................................29

Extensiveness and Accessibility................................................................................................30

Comprehensiveness...................................................................................................................30

Conclusion and Strength............................................................................................................30

MANAGERIAL ACCOUNTING

Comprehensiveness...................................................................................................................25

Conclusion and Strength............................................................................................................25

11. Value Framework Element: Brands and Intellectual Assets..............................................26

Report Extracts:.........................................................................................................................26

Reporting Critique.....................................................................................................................26

Extensiveness and Accessibility................................................................................................27

Comprehensiveness...................................................................................................................27

Conclusion and Strength............................................................................................................27

12. Value Framework Element: Processes and Supply Chain..................................................27

Report Extracts:.........................................................................................................................27

Reporting Critique.....................................................................................................................27

Extensiveness and Accessibility................................................................................................28

Comprehensiveness...................................................................................................................28

Conclusion and Strength............................................................................................................28

13. Value Framework Element: Operational Performance.......................................................29

Report Extracts:.........................................................................................................................29

Reporting Critique.....................................................................................................................29

Extensiveness and Accessibility................................................................................................30

Comprehensiveness...................................................................................................................30

Conclusion and Strength............................................................................................................30

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

MANAGERIAL ACCOUNTING

14. Value Framework Element: Economic Performance.........................................................31

Report Extracts:.........................................................................................................................31

Reporting Critique.....................................................................................................................31

Extensiveness and Accessibility................................................................................................32

Comprehensiveness...................................................................................................................32

Conclusion and Strength............................................................................................................32

15. Value Framework Element: Social.....................................................................................32

Report Extracts:.........................................................................................................................32

Reporting Critique.....................................................................................................................32

Extensiveness and Accessibility................................................................................................33

Comprehensiveness...................................................................................................................33

Conclusion and Strength............................................................................................................33

16. Value Framework Element: Environmental.......................................................................33

Report Extracts:.........................................................................................................................33

Reporting Critique.....................................................................................................................33

Extensiveness and Accessibility................................................................................................34

Comprehensiveness...................................................................................................................34

Conclusion and Strength............................................................................................................34

17. Value Framework Element: Segmental..............................................................................35

Report Extracts:.........................................................................................................................35

MANAGERIAL ACCOUNTING

14. Value Framework Element: Economic Performance.........................................................31

Report Extracts:.........................................................................................................................31

Reporting Critique.....................................................................................................................31

Extensiveness and Accessibility................................................................................................32

Comprehensiveness...................................................................................................................32

Conclusion and Strength............................................................................................................32

15. Value Framework Element: Social.....................................................................................32

Report Extracts:.........................................................................................................................32

Reporting Critique.....................................................................................................................32

Extensiveness and Accessibility................................................................................................33

Comprehensiveness...................................................................................................................33

Conclusion and Strength............................................................................................................33

16. Value Framework Element: Environmental.......................................................................33

Report Extracts:.........................................................................................................................33

Reporting Critique.....................................................................................................................33

Extensiveness and Accessibility................................................................................................34

Comprehensiveness...................................................................................................................34

Conclusion and Strength............................................................................................................34

17. Value Framework Element: Segmental..............................................................................35

Report Extracts:.........................................................................................................................35

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MANAGERIAL ACCOUNTING

Reporting Critique.....................................................................................................................35

Extensiveness and Accessibility................................................................................................36

Comprehensiveness...................................................................................................................36

Conclusion and Strength............................................................................................................36

Reference.......................................................................................................................................37

MANAGERIAL ACCOUNTING

Reporting Critique.....................................................................................................................35

Extensiveness and Accessibility................................................................................................36

Comprehensiveness...................................................................................................................36

Conclusion and Strength............................................................................................................36

Reference.......................................................................................................................................37

8

MANAGERIAL ACCOUNTING

PwC Value Framework Elements

1. Value Framework Element: Strategies and Objectives

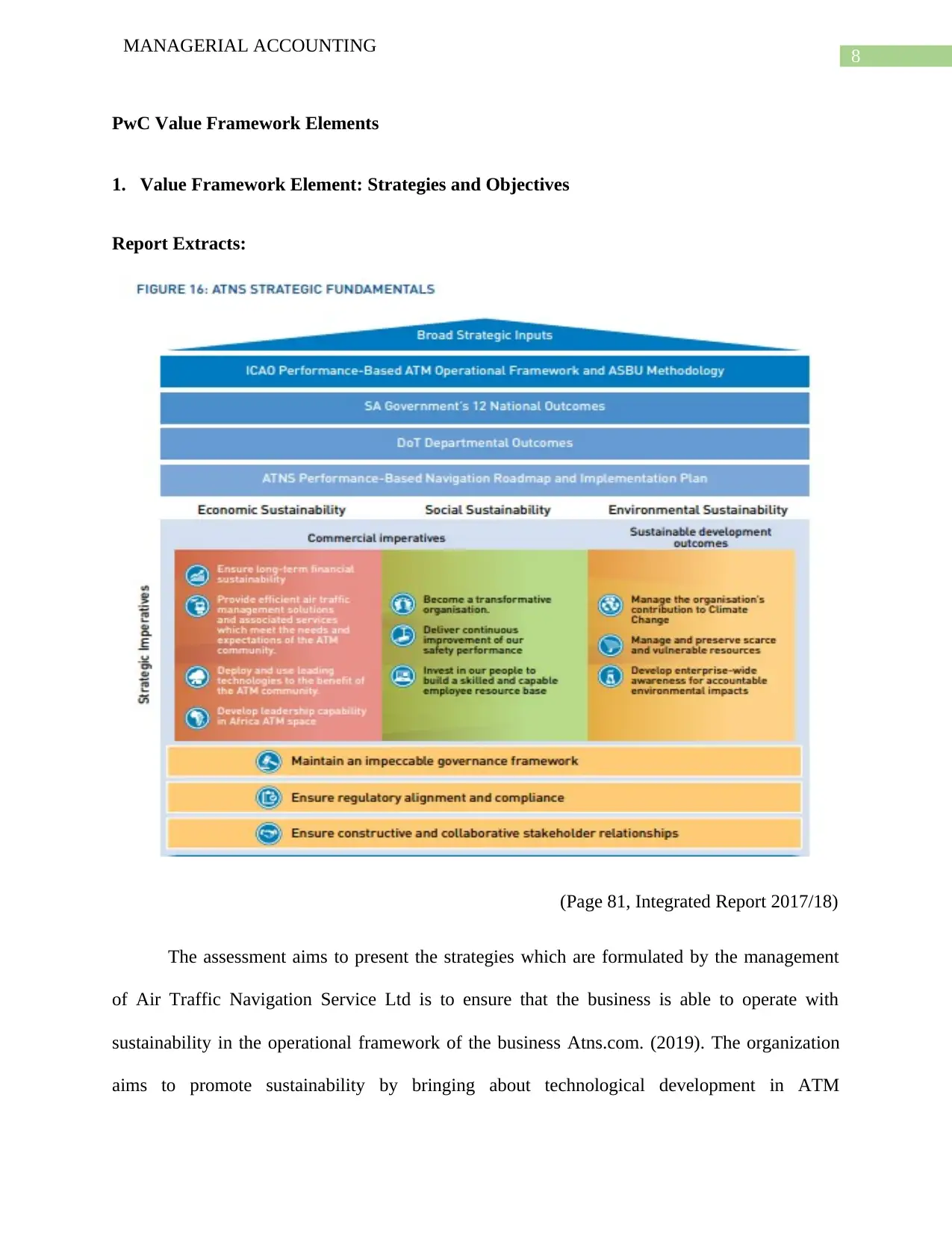

Report Extracts:

(Page 81, Integrated Report 2017/18)

The assessment aims to present the strategies which are formulated by the management

of Air Traffic Navigation Service Ltd is to ensure that the business is able to operate with

sustainability in the operational framework of the business Atns.com. (2019). The organization

aims to promote sustainability by bringing about technological development in ATM

MANAGERIAL ACCOUNTING

PwC Value Framework Elements

1. Value Framework Element: Strategies and Objectives

Report Extracts:

(Page 81, Integrated Report 2017/18)

The assessment aims to present the strategies which are formulated by the management

of Air Traffic Navigation Service Ltd is to ensure that the business is able to operate with

sustainability in the operational framework of the business Atns.com. (2019). The organization

aims to promote sustainability by bringing about technological development in ATM

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

MANAGERIAL ACCOUNTING

Community. Further, the management aims to implement continuous improvements for

managing resources and climatic changes.

Reporting Critique

The reporting critiques which are presented in the annual report of the business are shown

below in point form:

The management of Air Traffic Navigation Service Ltd has shown its strategies in details

focusing on sustainability and innovation.

The business has also set out a proper timeline for achieving the goals of the business.

Extensiveness and Accessibility

The annual report of the business shows a whole section on strategies and

implementation of the same and the same is covered on page 81. The business has presented

appropriate charts and explanation for proper understanding of the strategies.

Comprehensiveness

The strategy section of the annual report of the business shows the future perspective of

the business so that the services of the business are of the best quality. The focus of the business

is sustainability approach in the business.

Conclusion and Strength

The business is focusing on maintaining efficiency in the organization by putting more

emphasis on sustainability practices in the business. The business also focuses on continuous

improvement and innovation for enhancing the operational capabilities of the business.

Therefore, it can be said that the quality of strategies and objectives for the business is ‘good’.

MANAGERIAL ACCOUNTING

Community. Further, the management aims to implement continuous improvements for

managing resources and climatic changes.

Reporting Critique

The reporting critiques which are presented in the annual report of the business are shown

below in point form:

The management of Air Traffic Navigation Service Ltd has shown its strategies in details

focusing on sustainability and innovation.

The business has also set out a proper timeline for achieving the goals of the business.

Extensiveness and Accessibility

The annual report of the business shows a whole section on strategies and

implementation of the same and the same is covered on page 81. The business has presented

appropriate charts and explanation for proper understanding of the strategies.

Comprehensiveness

The strategy section of the annual report of the business shows the future perspective of

the business so that the services of the business are of the best quality. The focus of the business

is sustainability approach in the business.

Conclusion and Strength

The business is focusing on maintaining efficiency in the organization by putting more

emphasis on sustainability practices in the business. The business also focuses on continuous

improvement and innovation for enhancing the operational capabilities of the business.

Therefore, it can be said that the quality of strategies and objectives for the business is ‘good’.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

MANAGERIAL ACCOUNTING

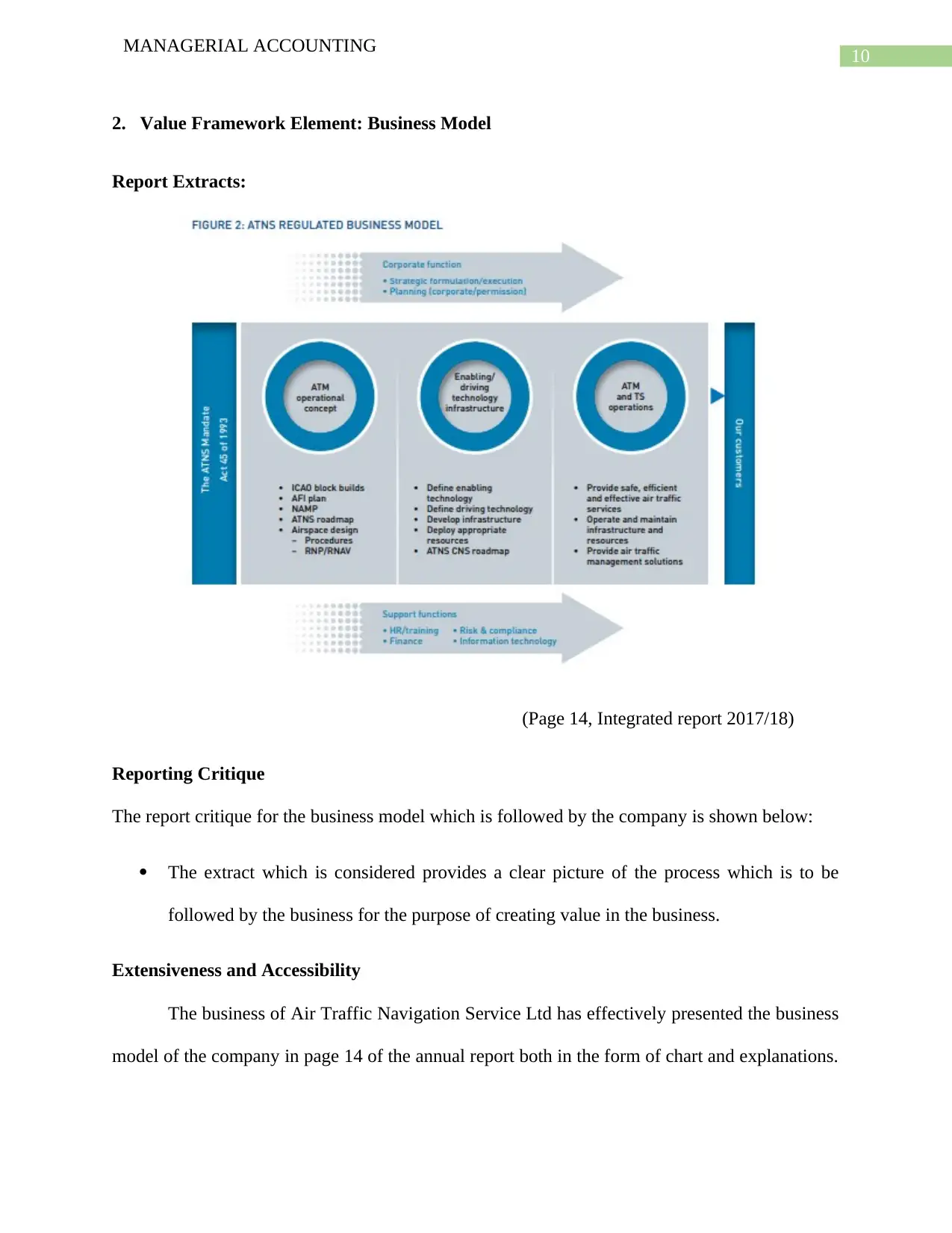

2. Value Framework Element: Business Model

Report Extracts:

(Page 14, Integrated report 2017/18)

Reporting Critique

The report critique for the business model which is followed by the company is shown below:

The extract which is considered provides a clear picture of the process which is to be

followed by the business for the purpose of creating value in the business.

Extensiveness and Accessibility

The business of Air Traffic Navigation Service Ltd has effectively presented the business

model of the company in page 14 of the annual report both in the form of chart and explanations.

MANAGERIAL ACCOUNTING

2. Value Framework Element: Business Model

Report Extracts:

(Page 14, Integrated report 2017/18)

Reporting Critique

The report critique for the business model which is followed by the company is shown below:

The extract which is considered provides a clear picture of the process which is to be

followed by the business for the purpose of creating value in the business.

Extensiveness and Accessibility

The business of Air Traffic Navigation Service Ltd has effectively presented the business

model of the company in page 14 of the annual report both in the form of chart and explanations.

11

MANAGERIAL ACCOUNTING

The business model also sets out the plans of the business for improving quality of services and

also lists out any assumptions which are taken by the management.

Comprehensiveness

The business of Air Traffic Navigation Service Ltd appropriate uses modern technology

and user information for properly maintaining the air traffic. The company considers the

development of aviation industry and is trying to make continuous improvements in the business

structure and performance (Atns.com. 2019).

Conclusion and Strength

The management of the company has implemented proper strategies considering the

business model which is formulated by the business and therefore the reporting quality of the

same is ‘good’.

3. Value Framework Element: Governance

Report Extracts:

The board of directors of the business is responsible for maintaining the governance

standards of the business. The board is trying to make continuous improvement in the corporate

governance structure of the business. An extract which is presented below shows the extracts of

the governance strategies of the business

MANAGERIAL ACCOUNTING

The business model also sets out the plans of the business for improving quality of services and

also lists out any assumptions which are taken by the management.

Comprehensiveness

The business of Air Traffic Navigation Service Ltd appropriate uses modern technology

and user information for properly maintaining the air traffic. The company considers the

development of aviation industry and is trying to make continuous improvements in the business

structure and performance (Atns.com. 2019).

Conclusion and Strength

The management of the company has implemented proper strategies considering the

business model which is formulated by the business and therefore the reporting quality of the

same is ‘good’.

3. Value Framework Element: Governance

Report Extracts:

The board of directors of the business is responsible for maintaining the governance

standards of the business. The board is trying to make continuous improvement in the corporate

governance structure of the business. An extract which is presented below shows the extracts of

the governance strategies of the business

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 37

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.